Greek Banking Sector Stock Reaction to ECB’s Monetary Policy Interventions

Abstract

1. Introduction

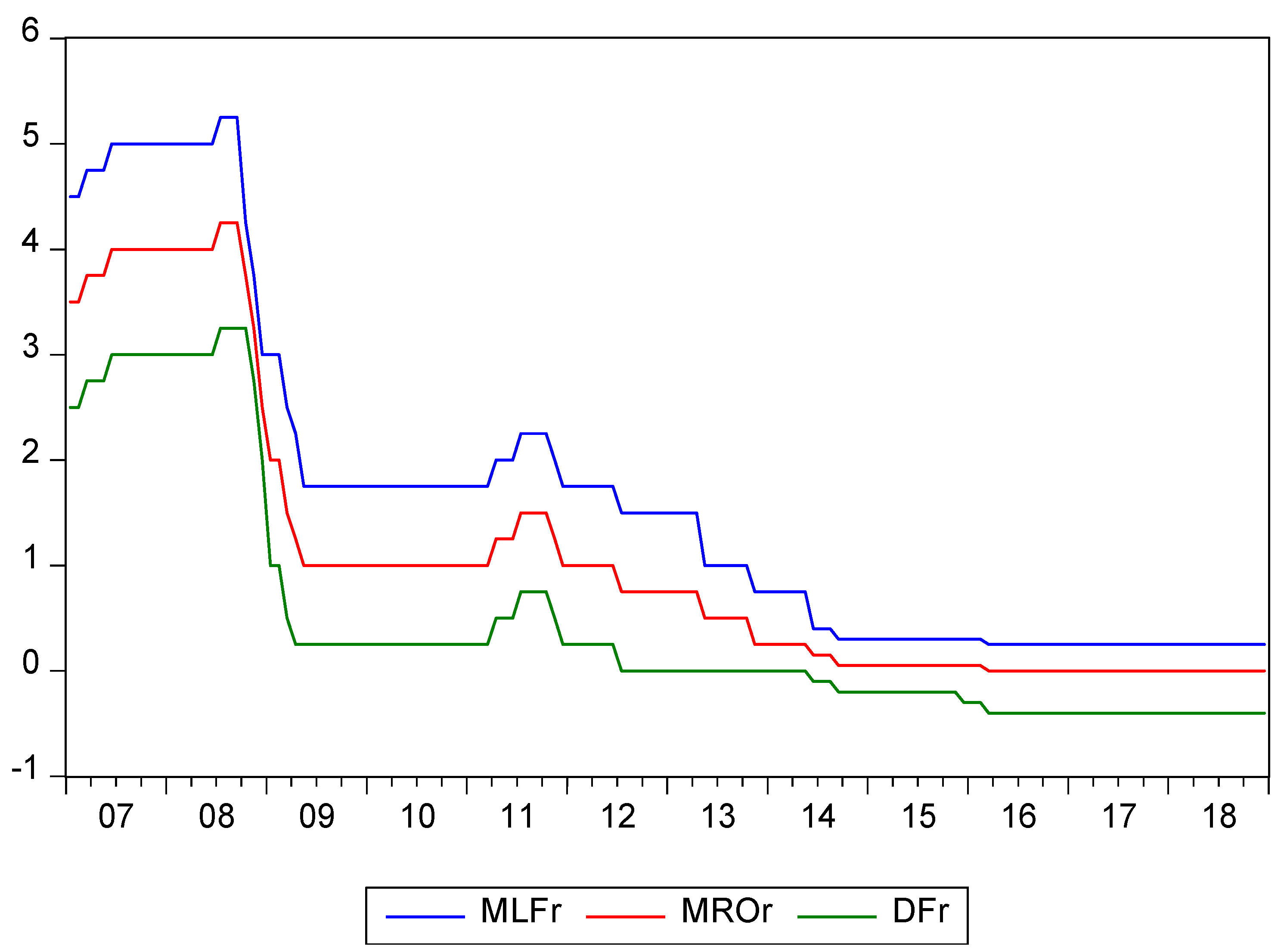

2. Monetary Policy Interventions in the Euro Area

3. Literature Review

4. Channels of Transmission of Monetary Policy

5. Empirical Approach

5.1. Data

5.2. Methodology

6. Discussion of Results

Robustness Tests

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Date | Description | MRO Rate Change | Category of Policy |

|---|---|---|---|

| 8 March 2007 | G.C. meeting | +0.25 | IRIN |

| 6 June 2007 | G.C. meeting | +0.25 | IRIN |

| 22 August 2007 | Supplementary LTROs announcement | LIQ | |

| 6 September 2007 | Supplementary LTROs | LIQ | |

| 8 November 2007 | Renewal of supplementary LTROs | LIQ | |

| 10 January 2008 | US dollar liquidity providing operations | LIQ | |

| 7 February 2008 | Renewal of two supplementary LTROs | LIQ | |

| 11 March 2008 | US dollar liquidity operations | LIQ | |

| 28 March 2008 | Introduction of supplementary 6-month LTROs | LIQ | |

| 2 May 2008 | US dollar liquidity providing operations | LIQ | |

| 3 July 2008 | G.C. meeting | +0.25 | IRIN |

| 30 July 2008 | US dollar liquidity providing operations | LIQ | |

| 31 July 2008 | Renewal of two LTROs | LIQ | |

| 4 September 2008 | Renewal of LTROs | LIQ | |

| 18 September 2008 | US dollar liquidity providing operations | LIQ | |

| 26 September 2008 | US dollar liquidity providing operations | LIQ | |

| 29 September 2008 | Temporary swap lines with the Fed | LIQ | |

| 7 October 2008 | Enhance of LTROs and expansion of US dollar liquidity operations | LIQ | |

| 8 October 2008 | Fixed rate tender procedure with full allotment (FRTPFA) for MROs | −0.5 | IRC |

| 13 October 2008 | US dollar liquidity providing operations | LIQ | |

| 15 October 2008 | Expansion of assets eligible as collateral, enhancement of LTROs | LIQ | |

| 6 November 2008 | G.C. meeting | -0.5 | IRC |

| 4 December 2008 | G.C. meeting | −0.75 | IRC |

| 18 December 2008 | Fixed rate tender procedure with full allotment for MROs | LIQ | |

| 19 December 2008 | US dollar liquidity providing operations | LIQ | |

| 15 January 2009 | G.C. meeting | −0.5 | IRC |

| 3 February 2009 | Extension of temporary swap lines with the Fed | LIQ | |

| 5 March 2009 | Continuation of FRTPFA for MROs and LTROs | −0.5 | IRC |

| 19 March 2009 | US dollar liquidity providing operations | LIQ | |

| 2 April 2009 | G.C. meeting | −0.25 | IRC |

| 6 April 2009 | Establishment of a reciprocal currency arrangement with the Fed | LIQ | |

| 7 May 2009 | Covered bond purchases (CBPP1) and one-year LTROs | −0.25 | IRC |

| 4 June 2009 | Technical modalities of CBPP1 | ME | |

| 25 June 2009 | Extension of liquidity swap arrangements with the Fed | LIQ | |

| 24 September 2009 | GovC decided to continue US dollar liquidity operations | LIQ | |

| 3 December 2009 | Continuation of FRTFA for MROs, and enhancement of LTROs | LIQ | |

| 4 March 2010 | Continuation of FRTFA for MROs, and enhancement of LTROs | LIQ | |

| 3 May 2010 | Change in eligibility of Greek debt instruments | LIQ | |

| 10 May 2010 | Securities market programme (SMP) | ME | |

| 10 June 2010 | FRTPFA in the regular 3-month LTROs | LIQ | |

| 2 September 2010 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 2 December 2010 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 17 December 2010 | Temporary swap facility with the Bank of England | LIQ | |

| 21 December 2010 | Extension of liquidity swap arrangements with the Fed | LIQ | |

| 3 March 2011 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 7 April 2011 | G.C. meeting | +0.25 | IRIN |

| 9 June 2011 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 29 June 2011 | Extension of liquidity swap arrangements with the Fed | LIQ | |

| 7 July 2011 | GovC meeting | +0.25 | IRIN |

| 4 August 2011 | MROs, 3-month and 6-month LTROs at FRTPFA | LIQ | |

| 8 August 2011 | Reactivation of SMP for Italy and Spain | ME | |

| 25 August 2011 | Extension of liquidity swap arrangements with the Fed | LIQ | |

| 15 September 2011 | US dollar liquidity operations in coordination with other CB | LIQ | |

| 6 October 2011 | Launch of new covered bond purchase program (CBPP2) | ME | |

| 3 November 2011 | Technical modalities of CBPP2 | −0.25 | IRC |

| 30 November 2011 | Establishment of a temporary network of reciprocal swap lines | LIQ | |

| 8 December 2011 | Two 3-year LTROs, increase of collateral availability | −0.25 | IRC |

| 21 December 2011 | Results of first 3-year LTRO | LIQ | |

| 9 February 2012 | Approval of National credit claims criteria | LIQ | |

| 28 February 2012 | Results of second 3-year LTRO | LIQ | |

| 8 March 2012 | Eligibility of Greek bonds in Eurosystem credit operations | LIQ | |

| 6 June 2012 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 22 June 2012 | Increase of collateral availability for counterparties | LIQ | |

| 5 July 2012 | G.C. meeting | −0.25 | IRC |

| 26 July 2012 | Draghi’s speech in London “whatever it takes …OMT” | ME | |

| 2 August 2012 | Outright monetary transactions-OMT | ME | |

| 6 September 2012 | Technical details of OMTs | ME | |

| 12 September 2012 | Extension of liquidity swap arrangements with the BoE | LIQ | |

| 6 December 2012 | MROs and 3-month LTROs at FRTPFA | LIQ | |

| 13 December 2012 | Extension of liquidity swap arrangements with the Fed | LIQ | |

| 19 December 2012 | Eligibility of Greek debt instruments | LIQ | |

| 21 February 2013 | Publishing of the Eurosystem’s holdings acquired under SMP | ME | |

| 22 March 2013 | Collateral rules | LIQ | |

| 2 May 2013 | Extension of MROs and 3-month LTROs at FRTPFA | −0.25 | IRC |

| 16 September 2013 | Extension of liquidity swap arrangements with the BoE | LIQ | |

| 31 October 2013 | Standing swap arrangements with other central banks | LIQ | |

| 7 November 2013 | Extension of MROs and 3-month LTROs at FRTPFA | −0.25 | IRC |

| 5 June 2014 | Targeted LTROs launched and other measures | −0.1 | IRC |

| 17 June 2014 | US dollar liquidity providing operations | LIQ | |

| 3 July 2014 | Details for first series of TLTROs | LIQ | |

| 29 July 2014 | Legal acts for TLTROs | LIQ | |

| 04 September 2014 | CBPP3 and ABSPP announcement | −0.1 | IRC |

| 18 September 2014 | The ECB allots €82.6 billion in TLTRO1 | LIQ | |

| 2 October 2014 | Details for ABSPP and CBBP3 | ME | |

| 17 November 2014 | M. Draghi, speech at the E.P. | ME | |

| 4 December 2014 | Q.E. programme with sovereign bonds (Draghi’s press conference) | ME | |

| 22 January 2015 | Expanded Asset Purchase Programme (APP) and other measures | ME | |

| 5 March 2015 | PSPP details and implementation | ME | |

| 3 September 2015 | Decision to increase the PSPP issue share limit | ME | |

| 23 September 2015 | ECB adjusts purchase process in ABSPP | ME | |

| 3 December 2015 | Extension of APP until the end of March 2017. | ME | |

| 10 March 2016 | Increase of monthly purchases under APP, launch of TLTRO2 and CSPP | −0.05 | IRC |

| 21 April 2016 | Details for CSPP | ME | |

| 3 May 2016 | Legal acts on the second series of TLTROs | LIQ | |

| 2 June 2016 | The Eurosystem will start making purchases under CSPP | ME | |

| 22 June 2016 | ECB reinstates waiver affecting the eligibility of Greek bonds | LIQ | |

| 5 October 2016 | Changes to collateral eligibility criteria | LIQ | |

| 3 November 2016 | ECB reviews its risk control framework for collateral assets | LIQ | |

| 8 December 2016 | APP calibration, EUR 60 billion monthly purchases until December 2017 | ME | |

| 19 January 2017 | Details for PSPP | ME | |

| 26 October 2017 | APP calibration, EUR 30 billion monthly purchases until September 2018 | ME | |

| 14 December 2017 | Changes to collateral eligibility criteria | LIQ | |

| 14 June 2018 | APP transition, EUR 15 billion monthly purchases until December 2018 | ME |

| 1 | See Floros and Chatziantoniou (2017) for more details about the Greek debt crisis. |

| 2 | For details about European Stability Mechanism and European Financial Stability Facility loans to euro area peripheral member states, see https://www.esm.europa.eu/, accessed on 30 August 2022. |

| 3 | After the share capital increases, the Hellenic Financial Stability Fund on behalf of Greek government became the main shareholder of the four core banks. |

| 4 | For details about expanded asset purchasing programme, see European Central Bank (2019), Economic Bulletin, issue 2. |

| 5 | Expanded APP consists of four programs for purchases of covered bonds, asset backed securities, public sector bonds, and corporate sector bonds (CBPP, ABSPP, PSPP, and CSPP). |

| 6 | Source: statistical data warehouse of the ECB. |

| 7 | See relevant press releases on 3 May 2010, 8 March 2012, 19 December 2012, and 22 June 2016, European Central Bank (2010, 2012a, 2012b, 2016). |

| 8 | For more details see European Central Bank (2021), Assessing the efficacy, efficiency, and potential side effects of the ECB’s monetary policy instruments since 2014, occasional paper series, no. 278. |

| 9 | For an overview of the unconventional transmission channels, see European Central Bank (2015), Economic Bulletin, issue 7. |

| 10 | See Table A1 in Appendix A for a detailed presentation of interventions along with their categorization. |

| 11 | For the return generating process of market model, we follow the procedure of Hendricks and Singhal (2003), Vortelinos and Gkillas (2019). |

| 12 | A multivariable panel regression model was estimated for a five-day event period; results are available upon request. |

| 13 | We did not estimate our model using jointly IRC, LIQ, ME as independent variables as we noticed multicollinearity issues. |

| 14 | |

| 15 | Ricci (2015), Fiordelisi and Galloppo (2018) as well as Vortelinos and Gkillas (2019) used the same procedure to investigate monetary impacts over time. |

References

- Altavilla, Carlo, Domenico Giannone, and Michele Lenza. 2016. The financial and macroeconomic effects of OMT announcements. International Journal of Central Banking 12: 29–57. [Google Scholar] [CrossRef]

- Avramidis, Panagiotis, Ioannis Asimakopoulos, Dimitris Malliaropoulos, and Nickolaos Travlos. 2020. Do banks appraise internal capital markets during credit shocks? Evidence from the Greek Crisis. Journal of Financial Intermediation 45: 100855. [Google Scholar] [CrossRef]

- Bernanke, Ben S., and Kenneth N. Kuttner. 2005. What explains the stock market’s reaction to Federal Reserve policy? Journal of Finance 60: 1221–57. [Google Scholar] [CrossRef]

- Boeckx, Jef, Maarten Dossche, and Gert Peersman. 2017. Effectiveness and transmission of the ECB’s balance sheet policies. International Journal of Central Banking 13: 297–333. [Google Scholar] [CrossRef]

- Bredin, Don, Stuart Hyde, Dirk Nitzsche, and Gerard O’Reilly. 2009. European monetary policy surprises: The aggregate and sectoral stock market response. International Journal of Finance & Economics 14: 156–71. [Google Scholar]

- Charalambakis, Evangelos, Yiannis Dendramis, and Elias Tzavalis. 2017. On the Determinants of npls: Lessons from Greece. Bank of Greece Working Papers 220. Athens: Bank of Greece. [Google Scholar]

- Chebbi, Tarek. 2019. What does unconventional monetary policy do to stock markets in the euro area? International Journal of Financial Economics 24: 391–411. [Google Scholar] [CrossRef]

- Cour-Thiman, Philippe, and Bernhard Winkler. 2013. The ECB’s Non-Standard Monetary Policy Measures. The Roll of Institutional Factors and Finance Structure. ECB Working Paper Series 1528; Frankfurt am Main: European Central Bank. [Google Scholar]

- Dell’Ariccia, Giovani, Pau Rabanal, and Damiano Sandri. 2018. Unconventional monetary policies in the Euro Area, Japan, and the United Kingdom. Journal of Economic Perspectives 32: 147–72. [Google Scholar] [CrossRef]

- Ehrmann, Michael, and Marcel Fratzscher. 2004. Taking stock: Monetary policy transmission to equity markets. Journal of Money, Credit, and Banking 36: 719–37. [Google Scholar] [CrossRef]

- European Central Bank. 2010. Press Release. ECB Announces Change in Eligibility of debt Instruments Issued or Guaranteed by the Greek Government. Frankfurt am Main: European Central Bank. [Google Scholar]

- European Central Bank. 2012a. Press Release. Eligibility of Bonds Issued or Guaranteed by the Greek Government in Eurosystem Credit Operations. Frankfurt am Main: European Central Bank. [Google Scholar]

- European Central Bank. 2012b. Press Release. ECB Announces Change in Eligibility of Debt Instruments Issued or Guaranteed by the Greek Government. Frankfurt am Main: European Central Bank. [Google Scholar]

- European Central Bank. 2015. The Transmission of the ECB’s Recent Non-Standard Monetary Policy Measures. ECB Article, Economic Bulletin, Issue 7, November 2015. Frankfurt am Main: European Central Bank, pp. 32–51. [Google Scholar]

- European Central Bank. 2016. Press Release. ECB Reinstates Waiver Affecting the Eligibility of Greek Bonds Used as Collateral in Eurosystem Monetary Policy Operations. Frankfurt am Main: European Central Bank. [Google Scholar]

- European Central Bank. 2019. Taking Stock of the Eurosystem’s Asset Purchase Programme after the End of Net Asset Purchases. ECB Article, Economic Bulletin, Issue 2, March 2019. Frankfurt am Main: European Central Bank, pp. 69–92. [Google Scholar]

- European Central Bank. 2021. Assessing the Efficacy, Efficiency and Potential Side Effects of the ECB’s Monetary Policy Instruments Since 2014. ECB Occasional Paper Series, 278; September, Frankfurt am Main: European Central Bank. [Google Scholar]

- Falagiarda, Matteo, Peter McQuade, and Marcel Tirpak. 2015. Spillovers from the ECB’s Non-Standard Monetary Policies on Non-Euro Area E.U. Countries: Evidence from an Event Study Analysis. ECB Working Paper Series 1869; Frankfurt am Main: European Central Bank. [Google Scholar]

- Falagiarda, Matteo, and Stefan Reitz. 2015. Announcements of ECB unconventional programs: Implications for the sovereign spreads of stressed euro area countries. Journal of International Money and Finance 53: 276–95. [Google Scholar] [CrossRef]

- Fausch, Jurg, and Markus Sigonius. 2018. The impact of ECB monetary policy surprises on the german stock market. Journal of Macroeconomics 55: 46–63. [Google Scholar] [CrossRef]

- Fiordelisi, Franco, and Giussepe Galloppo. 2018. Stock market reaction to policy interventions. The European Journal of Finance 24: 1817–34. [Google Scholar] [CrossRef]

- Fiordelisi, Franco, and Ornella Ricci. 2016. “Whatever it takes” An empirical assessment of the value of policy actions in banking. Review of Finance 20: 2321–47. [Google Scholar] [CrossRef]

- Fiordelisi, Franco, Giuseppe Galloppo, and Ornella Ricci. 2014. The effect of monetary policy interventions on interbank markets, equity indices and G-SIFIs during financial crisis. Journal of Financial Stability 11: 49–61. [Google Scholar] [CrossRef]

- Fiorelli, Cristiana, and Valentina Meliciani. 2019. Economic growth in the era of unconventional monetary instruments: A FAVAR approach. Journal of Macroeconomics 62: 1–20. [Google Scholar] [CrossRef]

- Floros, Christos, and Ioannis Chatziantoniou. 2017. The Greek Debt Crisis: In Quest of Growth in Times of Austerity. London: Palgrave MacMillan. [Google Scholar]

- Fratzscher, Marcel, Marco Lo Duca, and Roland Straub. 2014. ECB unconventional monetary policy actions: Market impact, international spillovers and transmission channels. Paper presented at the 15th Jacques Polak Annual Research Conference, Washington, DC, USA, November 13–14. [Google Scholar]

- Gambacorta, Leonardo, Borris Hofmann, and Gert Peersman. 2014. The effectiveness of unconventional monetary policy at the zero lower bound: A cross-country analysis. Journal of Money, Credit and Banking 46: 615–642. [Google Scholar] [CrossRef]

- Georgiadis, Georgios, and Johannes Gräb. 2016. Global financial market impact of the announcement of the ECB’s asset purchase programme. Journal of Financial Stability 26: 257–65. [Google Scholar] [CrossRef]

- Haitsma, Reinder, Deren Unlamis, and Jacob de Haan. 2016. The impact of the ECB’s conventional and unconventional monetary policies on stock markets. Journal of Macroeconomics 48: 101–16. [Google Scholar] [CrossRef]

- Hau, Harald, and Sandy Lai. 2016. Asset allocation and monetary policy: Evidence from the Eurozone. Journal of Financial Economics 120: 309–29. [Google Scholar] [CrossRef]

- Hendricks, Kevin, and Vinod Singhal. 2003. The effect of supply chain glitches on shareholder wealth. Journal of Operations Management 21: 501–22. [Google Scholar] [CrossRef]

- Jäger, Jannik, and Theocharis Grigoriadis. 2017. The effectiveness of the ecb’s unconventional monetary policy: Comparative evidence from crisis and non-crisis euro-area countries. Journal of International Money and Finance 78: 21–43. [Google Scholar] [CrossRef]

- Kholodilin, Konstantin, Alberto Montagnoli, Oreste Napolitano, and Boriss Siliverstovs. 2009. Assessing the impact of the ECB’s monetary policy on the stock markets: A sectoral view. Economics Letters 105: 211–13. [Google Scholar] [CrossRef]

- Kucharcukova, Oxana Babeka, Peter Claeys, and Borek Vasicek. 2016. Spillover of the ECB’s monetary policy outside the euro area: How different is conventional from unconventional policy? Journal of Policy Modeling 38: 199–225. [Google Scholar] [CrossRef]

- Louri, Helen, and Petros Migiakis. 2019. Financing Economic Growth in Greece: Lessons from the Crisis. Bank of Greece working papers 262. Athens: Bank of Greece. [Google Scholar]

- MacKinlay, Craig. 1997. The event studies in economics and finance. Journal of Economic Literature 33: 13–39. [Google Scholar]

- Martins, Luis Felipe, Joana Batista, and Alexandra Ferreira-Lopes. 2019. Unconventional monetary policies and bank credit in the Eurozone: An events study approach. International Journal of Finance and Economics 24: 1210–24. [Google Scholar] [CrossRef]

- Moder, Isabella. 2019. Spillovers from the ECB’s non standard monetary policy measures on southeastern Europe. International Journal of Central Banking 15: 127163. [Google Scholar]

- Pacicco, Fausto, Luigi Vena, and Andrea Venegoni. 2019. Market reactions to ECB policy innovations: A cross-country analysis. Journal of International Money and Finance 91: 126–37. [Google Scholar] [CrossRef]

- Patelis, Alex D. 1997. Stock return predictability and the role of monetary policy. Journal of Finance 52: 1951–72. [Google Scholar] [CrossRef]

- Petrakis, Nikolaos, Christos Lemonakis, Christos Floros, and Constantin Zopounidis. 2022. Eurozone stock market reaction to monetary policy interventions and other covariates. Journal of Risk and Financial Management 15: 56. [Google Scholar] [CrossRef]

- Ricci, Ornella. 2015. The impact of monetary policy announcements on the stock price of large European banks during the financial crisis. Journal of Banking and Finance 52: 245–55. [Google Scholar] [CrossRef]

- Ridogon, Roberto, and Brian Sack. 2004. The impact of monetary policy on asset prices. Journal of Monetary Economics 51: 1553–75. [Google Scholar]

- Rogers, John H., Chiara Scotti, and Jonathan H. Wright. 2014. Evaluating asset-market effects of unconventional monetary policy: A multi-country review. Economic Policy 29: 749–99. [Google Scholar] [CrossRef]

- Rosa, Carlo. 2011. The Validity of the Event-study Approach: Evidence from the Impact of the Fed’s Monetary Policy on US and Foreign Asset Prices. Economica 78: 429–39. [Google Scholar] [CrossRef]

- Rudebusch, Glen. 1998. Do measures of monetary policy in a VAR make sense? International Economic Review 39: 255–98. [Google Scholar] [CrossRef]

- Thorbecke, Willem. 1997. On stock market returns and monetary policy. Journal of Finance 52: 635–654. [Google Scholar] [CrossRef]

- Tobin, James. 1978. Monetary policy and the economy: The transmission mechanism. Southern Economic Journal 44: 421–31. [Google Scholar] [CrossRef]

- Trebesch, Christoph, and Jeromin Zettelmeyer. 2014. ECB Interventions in Distressed Sovereign Debt Markets: The Case of Greek Bonds. Working paper 4731. Munich: CESifo. [Google Scholar]

- Vortelinos, Dimitrios, and Konstantinos Gkillas. 2019. Reaction of EU stock markets to ECB policy interventions. International Journal of Banking, Accounting and Finance 10: 39–66. [Google Scholar] [CrossRef]

- Zettelmeyer, Jeromin, Trebesch Christoph, Gulati Mitu, Monacelli Tommaso, and Whelan Karl. 2013. The Greek Debt Restructuring: An Autopsy. Economic Policy 25: 515–63. [Google Scholar]

| Monetary Policy Category | Number of Interventions |

|---|---|

| Interest rate cuts (IRC) | 15 |

| Interest rate increases (IRIN) | 5 |

| Monetary easing (ME) | 22 |

| Liquidity provision (LIQ) | 61 |

| Total | 103 |

| Variable | Mean | Median | Std. Dev. |

|---|---|---|---|

| CAR(0,0) | 0.001533 | 0.000253 | 0.042928 |

| CAR(0,+1) | 0.001160 | 0.001112 | 0.072824 |

| CAR(−1,+1) | 0.000305 | −0.001588 | 0.077599 |

| Dependent Variable CAR(0,0) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.000868 | 0.002274 | −0.002450 | 0.002619 | −0.003233 | 0.005615 |

| IRC | 0.016485 * | 0.005959 | 0.018067 * | 0.006087 | 0.017370 ** | 0.006984 |

| ME | 0.006327 | 0.005239 | ||||

| LIQ | 0.002776 | 0.004559 | ||||

| R squared | 1.84% | 2.19% | 1.84% | |||

| Dependent Variable CAR(0,1) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.003789 | 0.003833 | −0.005852 | 0.004427 | −0.007166 | 0.006801 |

| IRC | 0.033984 * | 0.010045 | 0.036047 * | 0.010287 | 0.037361 * | 0.011514 |

| ME | 0.008253 | 0.008854 | ||||

| LIQ | 0.004953 | 0.008236 | ||||

| R squared | 2.72% | 2.9% | 2.8% | |||

| Dependent Variable CAR(−1,1) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.003466 | 0.004112 | −0.006010 | 0.004748 | −0.007282 | 0.007296 |

| IRC | 0.025897 ** | 0.010776 | 0.028441 ** | 0.011032 | 0.029713 ** | 0.012352 |

| ME | 0.010174 | 0.009495 | ||||

| LIQ | 0.005597 | 0.008835 | ||||

| R squared | 1.39% | 1.67% | 1.48% | |||

| Dependent Variable CAR(0,0) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.002575 | 0.003681 | −0.002979 | 0.003700 | −0.003233 | 0.005615 |

| IRC | 0.016811 * | 0.005978 | 0.018093 * | 0.006095 | 0.017370 ** | 0.006984 |

| ME | 0.005956 | 0.005556 | ||||

| LIQ | 0.000785 | 0.005059 | ||||

| TD | 0.002590 | 0.004395 | 0.000943 | 0.004655 | 0.002776 | 0.004559 |

| R squared | 1.93% | 2.20% | 1.93% | |||

| Dependent Variable CAR(0,1) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.002154 | 0.006219 | −0.002856 | 0.006249 | -0.005958 | 0.009482 |

| IRC | 0.033672 * | 0.010099 | 0.035901 * | 0.010296 | 0.036905 * | 0.011795 |

| ME | 0.010359 | 0.009385 | ||||

| LIQ | 0.004544 | 0.008544 | ||||

| TD | −0.002481 | 0.007425 | −0.005346 | 0.007863 | −0.001409 | 0.007700 |

| R squared | 2.74% | 3.03% | 2.81% | |||

| Dependent Variable CAR(-1,1) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | coeff. | std.error | coeff. | std.error | coeff. | std.error |

| γ | −0.000482 | 0.006670 | −0.001391 | 0.006698 | −0.004330 | 0.010171 |

| IRC | 0.025328 ** | 0.010831 | 0.028216 ** | 0.011035 | 0.028598 ** | 0.012651 |

| ME | 0.013420 | 0.010059 | ||||

| LIQ | 0.004596 | 0.009164 | ||||

| TD | −0.004529 | 0.007963 | −0.008240 | 0.008428 | −0.003444 | 0.008259 |

| R squared | 1.46% | 1.90% | 1.53% | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Petrakis, N.; Lemonakis, C.; Floros, C.; Zopounidis, C. Greek Banking Sector Stock Reaction to ECB’s Monetary Policy Interventions. J. Risk Financial Manag. 2022, 15, 448. https://doi.org/10.3390/jrfm15100448

Petrakis N, Lemonakis C, Floros C, Zopounidis C. Greek Banking Sector Stock Reaction to ECB’s Monetary Policy Interventions. Journal of Risk and Financial Management. 2022; 15(10):448. https://doi.org/10.3390/jrfm15100448

Chicago/Turabian StylePetrakis, Nikolaos, Christos Lemonakis, Christos Floros, and Constantin Zopounidis. 2022. "Greek Banking Sector Stock Reaction to ECB’s Monetary Policy Interventions" Journal of Risk and Financial Management 15, no. 10: 448. https://doi.org/10.3390/jrfm15100448

APA StylePetrakis, N., Lemonakis, C., Floros, C., & Zopounidis, C. (2022). Greek Banking Sector Stock Reaction to ECB’s Monetary Policy Interventions. Journal of Risk and Financial Management, 15(10), 448. https://doi.org/10.3390/jrfm15100448