The Perceived Effectiveness of Blockchain for Digital Operational Risk Resilience in the European Union Insurance Market Sector

Abstract

1. Introduction

2. Literature Review

3. Aim and Objective

4. Research Questions

5. Methodology

5.1. Designing the Tool

5.2. Sample

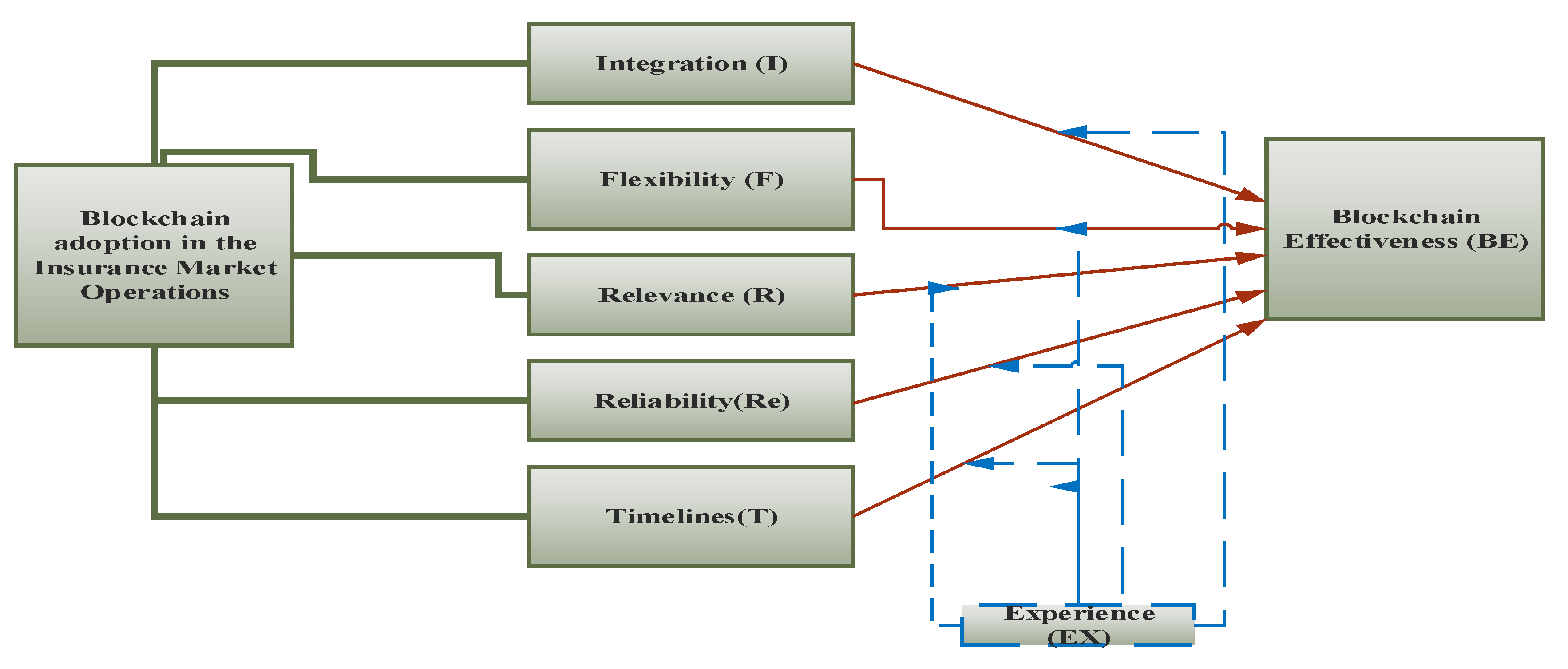

5.3. Hypotheses

5.4. Data Analysis

6. Findings and Analysis

6.1. Participants’ Demographics

6.2. Exploratory Factor Analysis

6.3. Confirmatory Factor Analysis

6.4. Structural Model

- H1:

- There is a significant effect of integration on BE.

- H2:

- There is a significant impact of reliability on BE.

- H3:

- There is a significant impact of flexibility on BE.

- H4:

- There is a significant impact of relevance on BE.

- H5:

- There is a significant impact of timeliness on BE.

- A statistically significant relationship was found between reliability and BE (B = −0.134, p < 0.05).

- A statistically significant relationship was found between flexibility and BE (B = 0.179, p < 0.05).

- A statistically significant relationship was found between relevance and BE (B = 0.568, p < 0.01).

- A statistically insignificant relationship was found between integration and BE (B = 0.024, p > 0.05).

- A statistically insignificant relationship was found between timeliness and BE (B = 0.115, p > 0.05).

6.5. Moderation Effect of Experience

7. Discussions and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abdallah, Ahmad Adel Jamil. 2014. The impact of using accounting information systems on the quality of financial statements submitted to the income and sales tax department in Jordan. European Scientific Journal 9. [Google Scholar] [CrossRef]

- Al-Dalabeeh, Abed El. Rahman, and Hussein Ali Al-Zeaud. 2012. Accounting information systems and their role in the measurement and cost thrifting in public shareholding industrial companies in Jordan. International Journal of Business and Management 7: 97. [Google Scholar] [CrossRef][Green Version]

- Altawalbeh, Mohammad Abdullah Fayad, Firas Na’elRawhi Hashem, and Khalid Ali Ahmad Alduneibat. 2017. The Role of Accounting Information Systems in Activating the Role of the Responsibility in the Jordanian Industrial Companies. Journal of Modern Accounting and Auditing 13: 1–7. [Google Scholar]

- Alzeban, Abdulaziz, and David Gwilliam. 2014. Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation 23: 74–86. [Google Scholar] [CrossRef]

- Attewell, Paul, and James B. Rule. 1991. Survey and other methodologies applied to IT impact research: Experiences from a comparative study of business computing. In The Information Systems Research Challenge: Survey Research Methods. Edited by Kenneth L. Kraemer. Cambridge: Harvard Business School Press, vol. 3, pp. 299–316. [Google Scholar]

- Aytaç, Mustafa, and Burcu Öngen. 2012. Examining the construct validity of the new environmental paradigm scale with confirmatory factor analysis. Journal of Statisticians. (Doğrulayıcıfaktöranaliziileyeniçevreselparadigmaölçeğininyapıgeçerliliğininincelenmesi, İstatistikçilerDergisi) 5: 14–22. [Google Scholar]

- Bayram, Nuran. 2010. Introduction to Structural Equation Modeling. Bursa: Ekin Publishing House; YapısalEşitlikModellemesineGiriş. [Google Scholar]

- Braun, Virginia, and Victoria Clarke. 2006. Using thematic analysis in psychology. Qualitative Research in Psychology 3: 77–101. [Google Scholar] [CrossRef]

- Chenhall, Robert H., and Deigan Morris. 1986. The impact of structure, environment, and interdependence on the perceived usefulness of management accounting systems. Accounting Review 61: 16–35. [Google Scholar]

- Cochran, William G. 2007. Sampling Techniques. Hoboken: John Wiley and Sons. [Google Scholar]

- Collomb, Alexis, and France Klara Sok. 2016. Blockchain/Digital Ledger Technology (DLT): What impact on the financial sector? Digiworld Economic Journal 103: 93. [Google Scholar]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef]

- Crawford, Bridget J. 2020. Blockchain Wills. Indiana Law Journal 95: 735. [Google Scholar]

- Creative Research Systems. n.d. Sample Size Calculator. Available online: https://www.surveysystem.com/sscalc.htm (accessed on 6 July 2021).

- European Commission. 2020a. A Digital Finance Strategy for Europe. Digital Finance EU. September. Available online: https://ec.europa.eu/info/sites/default/files/business_economy_euro/banking_and_finance/200924-digital-finance-factsheet_en.pdf (accessed on 6 July 2021).

- European Commission. 2020b. Digital Finance Package. September. Available online: https://ec.europa.eu/info/publications/200924-digital-finance-proposals_en#_blank (accessed on 6 July 2021).

- European Commission. 2020c. The European Commission: Proposal for a Regulation of the European Parliament and of the Council on Digital Operational Resilience for the Financial Sector and Amending Regulations (EC) No 1060/2009, (EU) No 648/2012, (EU) No 600/2014 and (EU) No 909/2014. com/2020/595 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020PC0595 (accessed on 6 July 2021).

- European Commission. 2020d. Proposal for a Directive of the European Parliament and of the Council Amending Directives 2006/43/EC, 2009/65/EC, 2009/138/EU, 2011/61/EU, EU/2013/36, 2014/65/EU, (EU) 2015/2366 and EU/2016/2341. com/2020/596 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020PC0596 (accessed on 6 July 2021).

- Fallucchi, Francesca, Marco Gerardi, Michele Petito, and Ernesto William De Luca. 2021. Blockchain Framework in Digital Government for the Certification of Authenticity. Timestamping and Data Property. Paper presented at 54th Hawaii International Conference on System Sciences, Kauai Island, HI, USA, January 5–8; pp. 1–10. [Google Scholar]

- Grima, Simon. 2020. The Perceived Effectiveness by Insurers of the EIOPA Guidelines on ICT Governance Systems. Paper presented at 21st AIDA Serbia Conference, Sabac, Serbia, April 3–5. [Google Scholar]

- Grima, Simon. 2020. A Steep framework analysis of the key factors impacting the use of blockchain technology in the insurance industry. The Geneva Papers on Risk and Insurance Issues and Practices 45: 398–425. [Google Scholar] [CrossRef]

- Hair, Joseph F. 1998. Multivariate Data Analysis. Upper Saddle River: Prentice-Hall. [Google Scholar]

- Herda, David N., and Kasey A. Martin. 2016. The effects of auditor experience and professional commitment on acceptance of underreporting time: A moderated mediation analysis. Current Issues in Auditing 10: A14–A27. [Google Scholar] [CrossRef]

- Hinton, Perry R., Brownlow Charlotte, Isabella Mcmurray, and Cozens Bob. 2004. SPSS Explained, 2nd ed. London and New York: Routledge. [Google Scholar]

- Hulin, Charles, Robert Cudeck, Richard G. Netemeyer, Dillon R. William, and Mc Donald Roderick. 2001. Measurements. Journal of Consumer Psychology 10: 55–69. [Google Scholar] [CrossRef]

- Iansiti, Marco, and Karim R. Lakhani. 2017. The Truth About Blockchain. Harvard Business Review. Technology. Available online: https://hbr.org/2017/01/the-truth-about-blockchain (accessed on 30 July 2021).

- Levy, Paul S., and Stanley Lemeshow. 1999. Sampling of Populations: Methods and Applications, 3rd ed. New York: John Wiley and Sons. [Google Scholar]

- Markgraf, Bert. 2019. Characteristics of a Good Management Information System. CHRON Newsletters. March 5. Available online: https://smallbusiness.chron.com/characteristics-good-management-information-system-59060.html (accessed on 30 July 2021).

- Mousmouti, Maria. 2014a. The “effectiveness test” as a tool for law reform. IALS Student Law Review 2: 4–8. [Google Scholar] [CrossRef]

- Mousmouti, Maria. 2014b. ‘Effectiveness as an Aid to Legislative Drafting’. The Loophole 17: 1–61. [Google Scholar]

- Naderifar, Mahin, Hamideh Goli, and Fereshteh Ghaljaie. 2017. Snowball Sampling: A Purposeful Method of Sampling in Qualitative Research. Strides in Development of Medical Education 14: 1–6. [Google Scholar] [CrossRef]

- Napitupulu, Ilham Hidayah, Sri Mahyuni, and Jojor Lisbet Sibarani. 2016. The impact of internal control effectiveness to the quality of management accounting information system: The survey on State-Owned Enterprises (SOEs). Journal of Theoretical and Applied Information Technology 88: 358–66. [Google Scholar]

- Netemeyer, Richard, and Robert Cudeck. 2001. Can a Reliability Coefficient Be Too High? Journal of Consumer Psychology 10: 55–58. [Google Scholar]

- Patel, F. 2015. Effects of accounting information system on Organizational Profitability. IJRAR–International Journal of Research and Analytical Reviews 2: 72–76. [Google Scholar]

- Pinsonneault, Alain, and Kenneth L. Kraemer. 1993. Survey Research Methodology in Management Information Systems: An Assessment. Journal of Management Information Systems 10: 75–105. [Google Scholar] [CrossRef]

- Pratap, Mayank. 2018. Everything You Need to Know about Smart Contracts: A Beginner’s Guide. August 27. Available online: https://hackernoon.com/everything-you-need-to-know-about-smart-contracts-a-beginners-guide-c13cc138378a (accessed on 30 July 2021).

- Qatanani, Khaled M., and Abdulqawi A. Hezabr. 2015. The effect of using accounting information systems to improve the value chain in the business organizations-empirical study. European Journal of Accounting Auditing and Finance Research 3: 1–11. [Google Scholar]

- Shagari, Shamsudeen Ladan, Akilah Abdullah, and Rafeah Mat Saat. 2017. Contributory Factors of Accounting Information Systems Effectiveness in Nigerian Banking Sector. Asian Journal of Multidisciplinary Studies 151. Available online: https://www.academia.edu/35004033/Asian_Journal_of_Multidisciplinary_Studies_Contributory_Factors_of_Accounting_Information_Systems_Effectiveness_in_Nigerian_Banking_Sector (accessed on 6 July 2021).

- Stake, Robert E. 2005. Qualitative Case Studies. In The Sage Handbook of Qualitative Research. Edited by Norman K. Denzin and Yvonna S. Lincoln. Washington, DC: Sage Publications Ltd., pp. 443–66. [Google Scholar]

- Suen, Lee-Jen Wu, Hui-Man Huang, and Hao-Hsien Lee. 2014. A Comparison of Convenience Sampling and Purposive Sampling. Bethesda: PubMed. [Google Scholar]

- Taber, Keith S. 2016. The Use of Cronbach’s Alpha When Developing and Reporting Research Instruments in Science Education. Research in Science Education 48: 1–24. [Google Scholar] [CrossRef]

- Tan, Ömer Faruk. 2016. Impact of Accounting Information Systems on Internal Auditors in Turkey. ÖneriDergisi 12: 245–60. [Google Scholar] [CrossRef]

- Teru, Susan Peter, Innocent Idoku, and Jane Tinyang Ndeyati. 2017. A Review of the Impact of Accounting Information System for Effective Internal Control on Firm Performance. Indian Journal of Finance and Banking 1: 52–59. [Google Scholar] [CrossRef]

- Toth, Zsuzsanna. 2012. The current role of accounting information systems. Theory, Methodology, Practice 8: 91. [Google Scholar]

- Vidal-Tomás, David, and Ana Ibañez. 2018. Semi-strong efficiency of Bitcoin. Finance Research Letters 27: 259–65. [Google Scholar] [CrossRef]

- Xanthaki, Helen. 2008. On Transferability of Legislative Solutions: The Functionality Test. In Drafting Legislation. A Modern Approach. Edited by Constantin Stefanou and Helen Xanthaki. Aldershot: Ashgate. [Google Scholar]

- Yazan, Bedrettin. 2015. Three approaches to case study methods in education. In The Qualitative Report. Edited by Yin Merriam and Stake. Fort Lauderdale: Nova Southeastern University (NSU), vol. 20, pp. 134–52. Available online: https://nsuworks.nova.edu/cgi/viewcontent.cgi?article=2102&context=tqr (accessed on 6 August 2021).

- Yin, Rober K. 2014. Case Study Research: Design and Methods. Thousand Oaks: Sage. [Google Scholar]

{kind=link}

{kind=link}

| Preposition | Construct | Number of Items | Sources |

|---|---|---|---|

| 1 | Integration (I) | 4 (Statements 2 to 5) | Chenhall and Morris (1986); Napitupulu et al. (2016); Tan (2016); Qatanani and Hezabr (2015) |

| 2 | Flexible (F) | 4 (Statements 10 to 13) | Napitupulu et al. (2016); Shagari et al. (2017); Tan (2016) |

| 3 | Reliability (Re) | 5 (Statements 6 to 9 and statement 1) | Napitupulu et al. (2016); Shagari et al. (2017) |

| 4 | Relevance (R) | 4 (Statements 14 to 17) | Teru et al. (2017); Al-Dalabeeh and Al-Zeaud (2012); Abdallah (2014); Shagari et al. (2017); Markgraf (2019) |

| 5 | Timeliness (T) | 3 (Statements 18 to 20) | Chenhall and Morris (1986); Patel (2015); Shagari et al. (2017) |

| 6 | Experience (EX) | 3 | Toth (2012); Altawalbeh et al. (2017); Herda and Martin (2016) |

| 7 | Effectiveness | 6 | Alzeban and Gwilliam (2014) |

| STATEMENT | |

|---|---|

| 1 | Blockchain can improve the accuracy of data and information management |

| 2 | Blockchain includes internal controls which can help to reduce the cases of fraud in the accounting data |

| 3 | The integration of Blockchain can improve the internal control effectiveness |

| 4 | Blockchain encourages the spirit of creativity and innovation among all employees |

| 5 | The information contained in the reports issued by Blockchain are credible and transparent |

| 6 | Blockchain can provide information that reduces errors during work |

| 7 | There is trust in the quality of Blockchain |

| 8 | The reliability of Blockchain outputs is important for decision-makers |

| 9 | Blockchain in my organization can help in complementing the formal procedures |

| 10 | Blockchain can adapt to modern legislation and laws |

| 11 | The flexibility of can increase the internal control effectiveness |

| 12 | Blockchain can provide information capable of correcting previous events |

| 13 | Blockchain provides various options for selection |

| 14 | Blockchain can provide efficient and relevant information to serve any purpose |

| 15 | Blockchain can provide operational reports related to the current operations of the organization |

| 16 | Blockchain can provide relevant information supporting organization strategy |

| 17 | Blockchain can provide relevant information for decision making |

| 18 | Blockchain can ensure that requested information is created immediately upon request |

| 19 | Blockchain can ensure that correct and consistent information is provided on time when required |

| 20 | Blockchain can ensure that data is available regularly enough to influence management decisions |

| No. | Statement |

|---|---|

| 1 | BE1. With Blockchain the internal controls and governance and performance are improved |

| 2 | BE2. With Blockchain the internal controls, governance and operations to ascertain that results are consistent with organization goals are improved |

| 3 | BE3. With Blockchain the accuracy and reliability improved |

| 4 | BE4. With Blockchain the compliance with policies, plans, laws and regulations are improved |

| 5 | BE5. With Blockchain the effectiveness of risk management is improved |

| 6 | BE6. With Blockchain the internal controls, governance, and operations to ascertain that results are consistent with organization goals are improved |

| No. | Statement |

|---|---|

| 1 | E1. Employee training to increase their skill and knowledge in Blockchain helps in the use of the application |

| 2 | E2. Experience and Knowledge of Blockchain and Insurance helps to achieve consistent, and quality results |

| 3 | E3. The experience and knowledge of Blockchain and Insurance helps controllers to use Blockchain in an efficient manner |

| F1 | F2 | F3 | F4 | F5 | |

|---|---|---|---|---|---|

| BV5. Blockchain can improve the accuracy of data and information management | 0.859 | ||||

| BV2. Blockchain includes internal controls which can help to reduce the cases of fraud in the accounting data | 0.842 | ||||

| BV3. The integration of Blockchain can improve the internal control effectiveness | 0.769 | ||||

| BV4. Blockchain encourages the spirit of creativity and innovation among all employees | 0.555 | ||||

| BV12. The information contained in the reports issued by Blockchain are credible and transparent | 0.793 | ||||

| BV13. Blockchain can provide information that reduces errors during work | 0.771 | ||||

| BV11. There is trust in the quality of Blockchain | 0.661 | ||||

| BV10. The reliability of Blockchain outputs is important for decision makers | 0.621 | ||||

| BV1. Blockchain in my organization can help in complementing the formal procedures | 0.754 | ||||

| BV7. Blockchain can adapt to modern legislation and laws | 0.709 | ||||

| BV9. The flexibility of Blockchain can increase the internal control effectiveness | 0.610 | ||||

| BV8. Blockchain can provide information capable of correcting previous events | 0.600 | ||||

| BV6. Blockchain provides various options for the selection | 0.595 | ||||

| BV14. Blockchain can provide efficient and relevant information to serve any purpose | 0.738 | ||||

| BV15. Blockchain can provide operational reports related to the current operations of the organization | 0.738 | ||||

| BV16. Blockchain can provide relevant information supporting the organization strategy | 0.720 | ||||

| BV17. Blockchain can provide relevant information for decision making | 0.682 | ||||

| BV20. Blockchain can ensure that requested information is created immediately upon request | 0.815 | ||||

| BV19. Blockchain can ensure that correct and consistent information is provided on time when required | 0.787 | ||||

| BV18. Blockchain can ensure that data is available regularly enough to influence management decisions | 0.679 |

| Factor | Name of Factor | Item | Mean | Min-Max | Cronbach Alpha |

|---|---|---|---|---|---|

| Factor 1 (F1) | Integration | 4 | 3.539 | 3.413–3.729 | 0.79 |

| Factor 2 (F2) | Reliability | 4 | 4.103 | 3.916–4.181 | 0.71 |

| Factor 3 (F3) | Flexibility | 5 | 3.502 | 3.361–3.657 | 0.70 |

| Factor 4 (F4) | Relevance | 4 | 4.002 | 3.986–4.310 | 0.70 |

| Factor 5 (F5) | Timeliness | 3 | 3.417 | 3.409–3.423 | 0.65 |

| β0 | β1 | S.E. | C.R. | R2 | p | |||

|---|---|---|---|---|---|---|---|---|

| Measurement Model | ||||||||

| BV1 | <--- | F | 0.581 | 1 | 0.337 | |||

| BV6 | <--- | F | 0.549 | 0.938 | 0.105 | 8.915 | 0.296 | *** |

| BV7 | <--- | F | 0.617 | 1.123 | 0.117 | 9.567 | 0.383 | *** |

| BV9 | <--- | F | 0.629 | 1.179 | 0.122 | 9.672 | 0.400 | *** |

| BV5 | <--- | I | 0.650 | 1 | 0.437 | |||

| BV3 | <--- | I | 0.754 | 1.016 | 0.077 | 13.269 | 0.518 | *** |

| BV2 | <--- | I | 0.833 | 1.184 | 0.087 | 13.564 | 0.697 | *** |

| BV11 | <--- | Re | 0.584 | 0.821 | 0.079 | 10.374 | 0.336 | *** |

| BV12 | <--- | Re | 0.736 | 1.006 | 0.089 | 11.334 | 0.540 | *** |

| BV13 | <--- | Re | 0.718 | 1 | 0.522 | |||

| BV20 | <--- | T | 0.730 | 1 | 0.534 | |||

| BV19 | <--- | T | 0.617 | 0.831 | 0.098 | 8.483 | 0.381 | *** |

| BV18 | <--- | T | 0.520 | 0.712 | 0.088 | 8.057 | 0.268 | *** |

| BV17 | <--- | R | 0.582 | 1 | 0.490 | |||

| BV16 | <--- | R | 0.521 | 0.93 | 0.101 | 9.228 | 0.396 | *** |

| BV15 | <--- | R | 0.687 | Oca.16 | 0.122 | 9.495 | 0.284 | *** |

| BV14 | <--- | R | 0.628 | 1.094 | 0.118 | 9.242 | 0.224 | *** |

| BE2 | <--- | BE | 0.644 | 1 | 0.416 | |||

| BE3 | <--- | BE | 0.701 | 1.198 | 0.099 | 12.149 | 0.492 | *** |

| BE5 | <--- | BE | 0.692 | 1.108 | 0.092 | 12.053 | 0.473 | *** |

| BE6 | <--- | BE | 0.720 | 1.173 | 0.095 | 12.341 | 0.523 | *** |

| Structural Model | ||||||||

| BE | <--- | I | 0.024 | 0.022 | 0.066 | 0.329 | 0.428 | 0.742 |

| BE | <--- | Re | −0.134 | −0.123 | 0.062 | −1.987 | ** | |

| BE | <--- | F | 0.179 | 0.207 | 0.103 | 2.003 | ** | |

| BE | <--- | R | 0.568 | 0.526 | 0.085 | 6.164 | *** | |

| BE | <--- | T | 0.115 | 0.113 | 0.062 | 1.835 | 0.067 | |

| Moderation Effects | Standardized Indirect Effect (β) | Bootstrap Lower–Upper Bounds TZ %95 | Hypothesis Decision |

|---|---|---|---|

| BE<---EX<---F | 0.042 | −0.061–0.143 | Reject |

| BE<---EX<---I | 0.050 | −0.034–0.142 | Reject |

| BE<---EX<---Re | 0.063 | −0.017–0.155 | Reject |

| BE<---EX<---T | 0.090 | 0.019–0.179 | Accept |

| BE<---EX<---R | 0.274 | 0.122–0.512 | Accept |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Grima, S.; Kizilkaya, M.; Sood, K.; ErdemDelice, M. The Perceived Effectiveness of Blockchain for Digital Operational Risk Resilience in the European Union Insurance Market Sector. J. Risk Financial Manag. 2021, 14, 363. https://doi.org/10.3390/jrfm14080363

Grima S, Kizilkaya M, Sood K, ErdemDelice M. The Perceived Effectiveness of Blockchain for Digital Operational Risk Resilience in the European Union Insurance Market Sector. Journal of Risk and Financial Management. 2021; 14(8):363. https://doi.org/10.3390/jrfm14080363

Chicago/Turabian StyleGrima, Simon, Murat Kizilkaya, Kiran Sood, and Mehmet ErdemDelice. 2021. "The Perceived Effectiveness of Blockchain for Digital Operational Risk Resilience in the European Union Insurance Market Sector" Journal of Risk and Financial Management 14, no. 8: 363. https://doi.org/10.3390/jrfm14080363

APA StyleGrima, S., Kizilkaya, M., Sood, K., & ErdemDelice, M. (2021). The Perceived Effectiveness of Blockchain for Digital Operational Risk Resilience in the European Union Insurance Market Sector. Journal of Risk and Financial Management, 14(8), 363. https://doi.org/10.3390/jrfm14080363