On Prices of Privacy Coins and Bitcoin

Abstract

:1. Introduction

2. Literature Review

3. Related Literature and Analysis

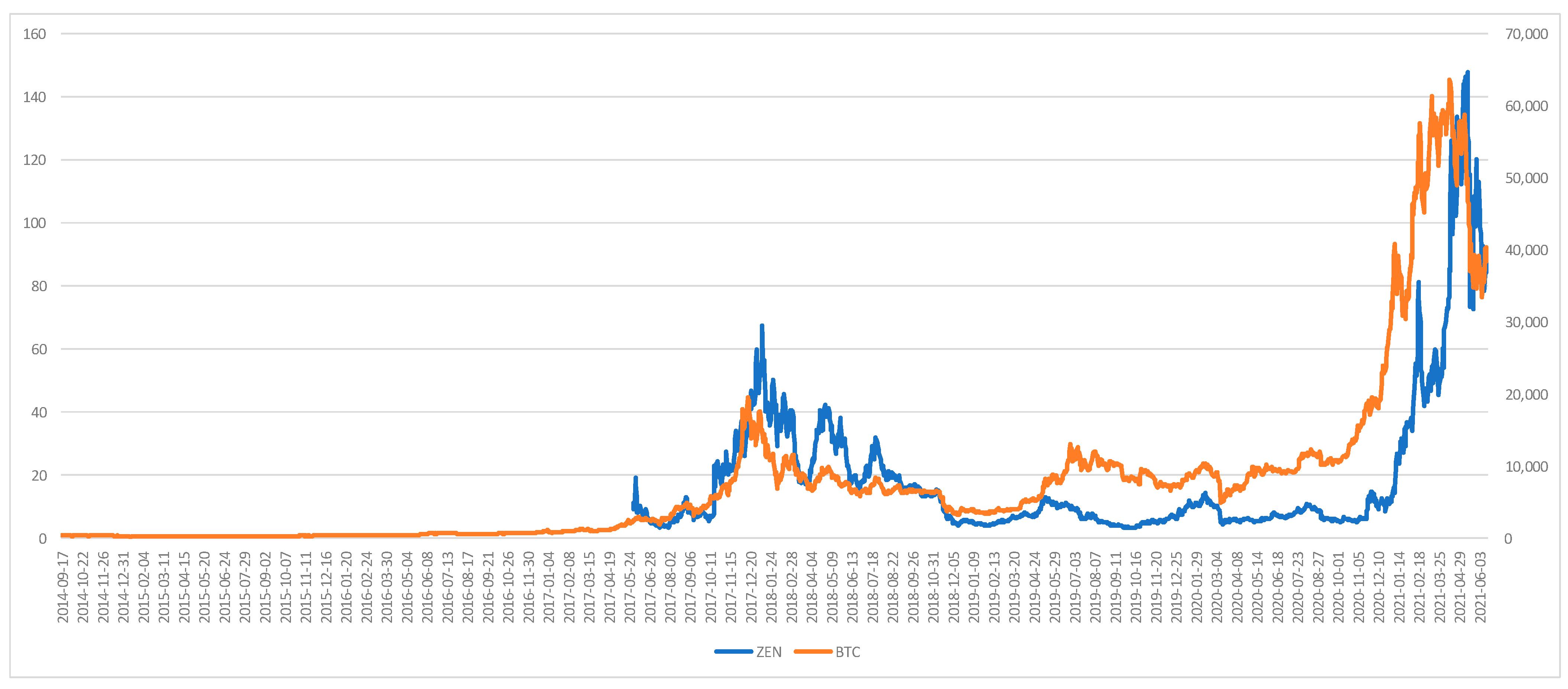

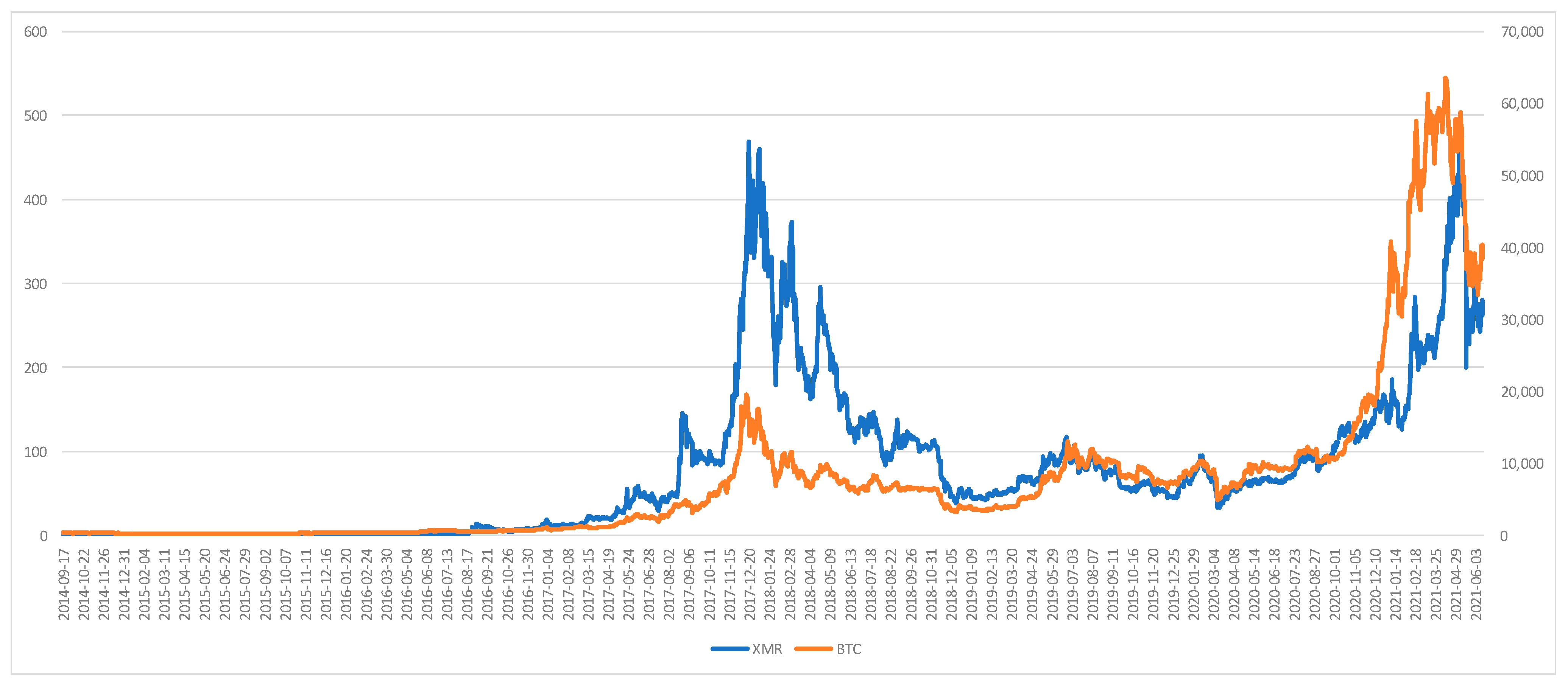

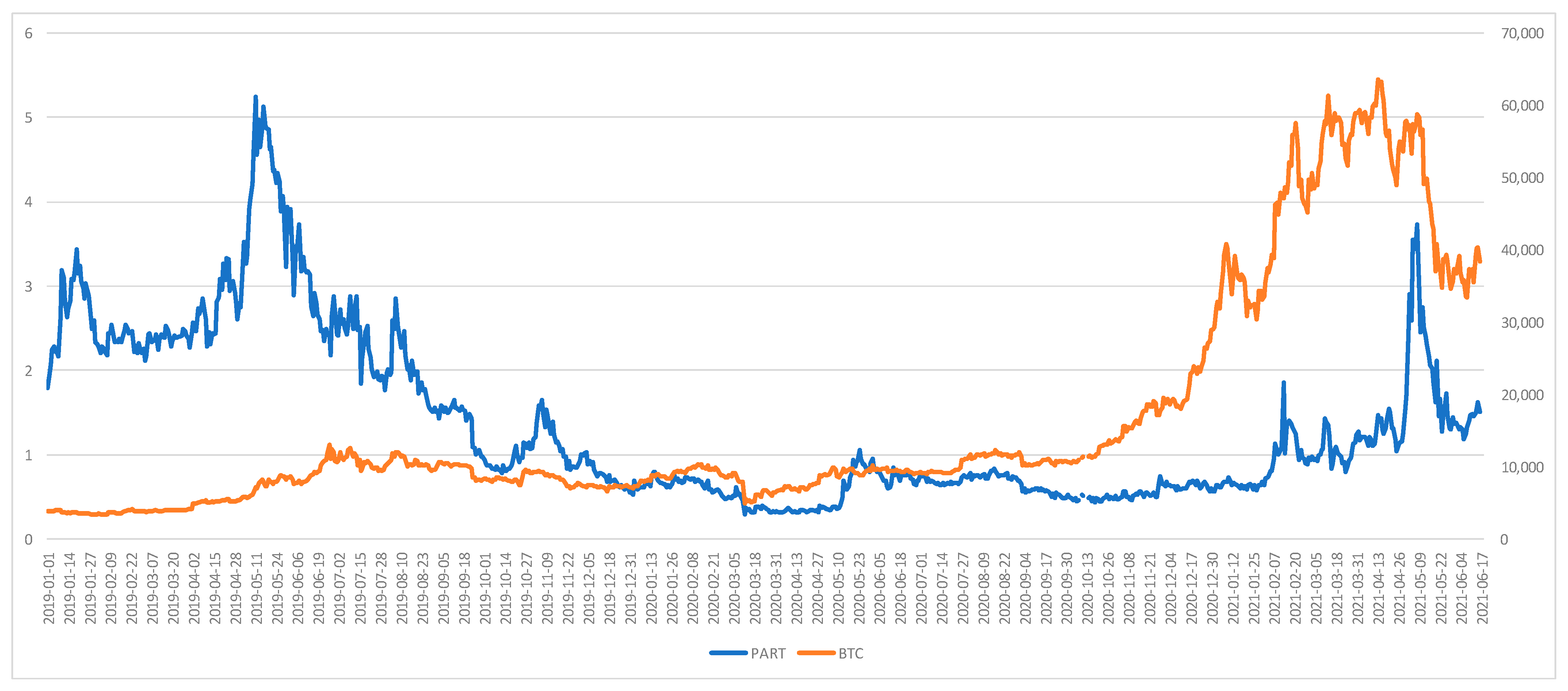

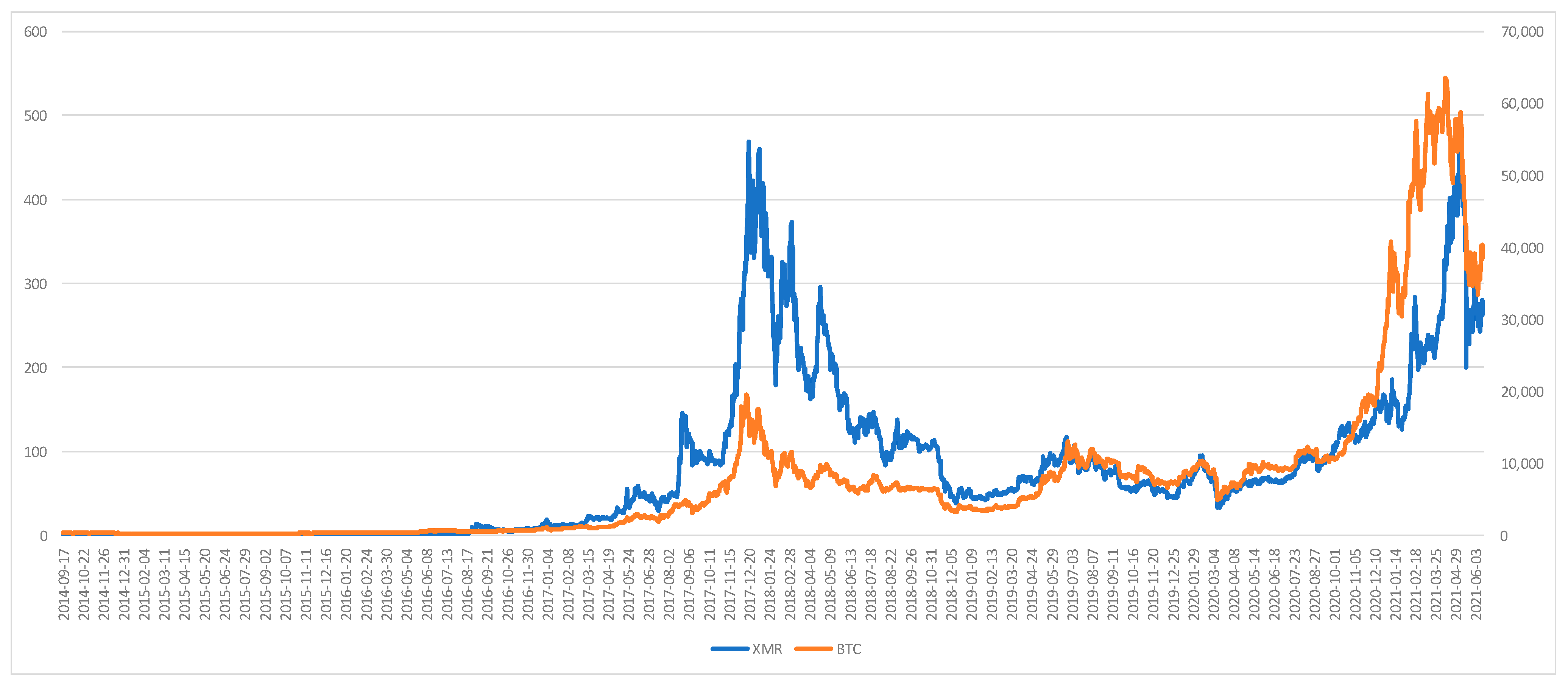

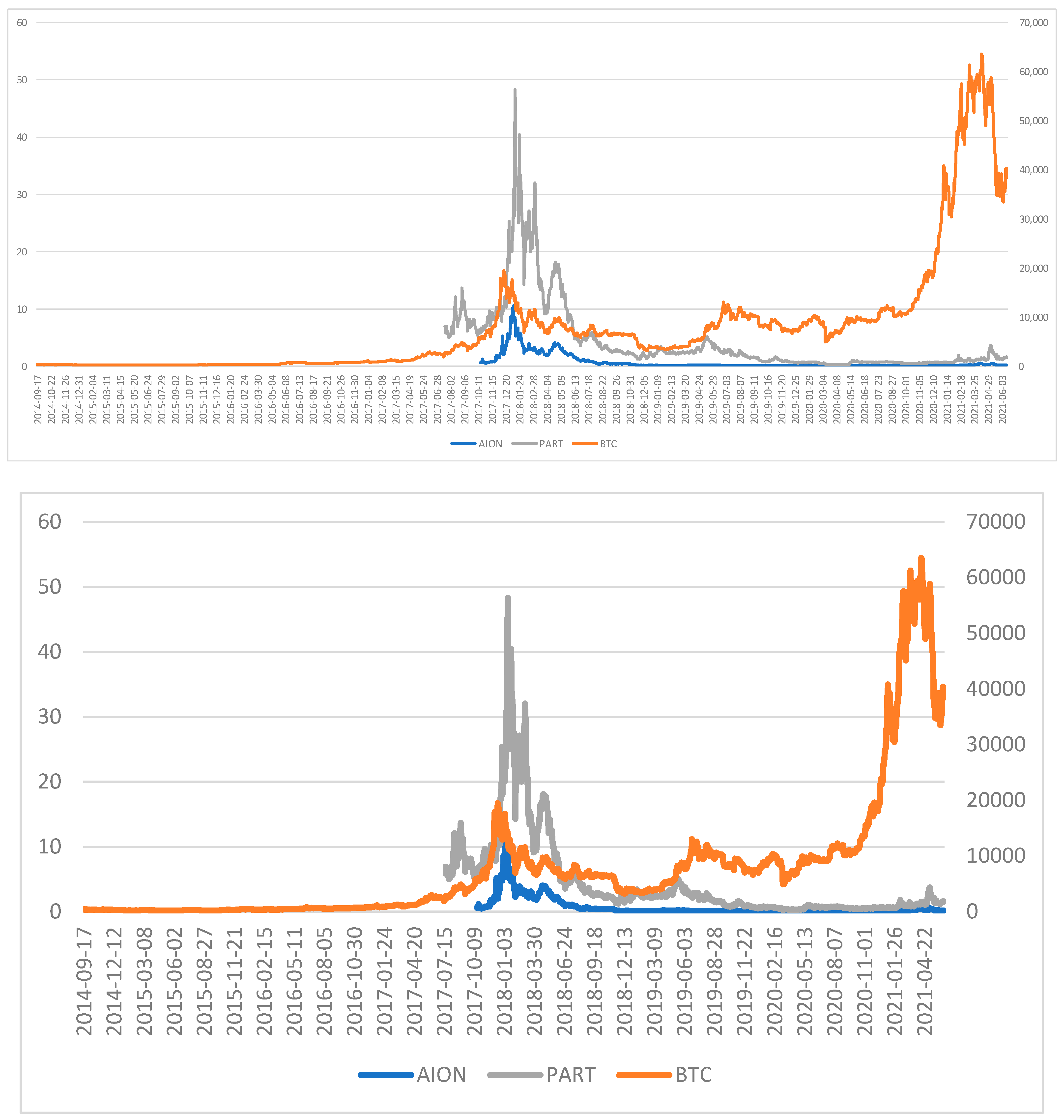

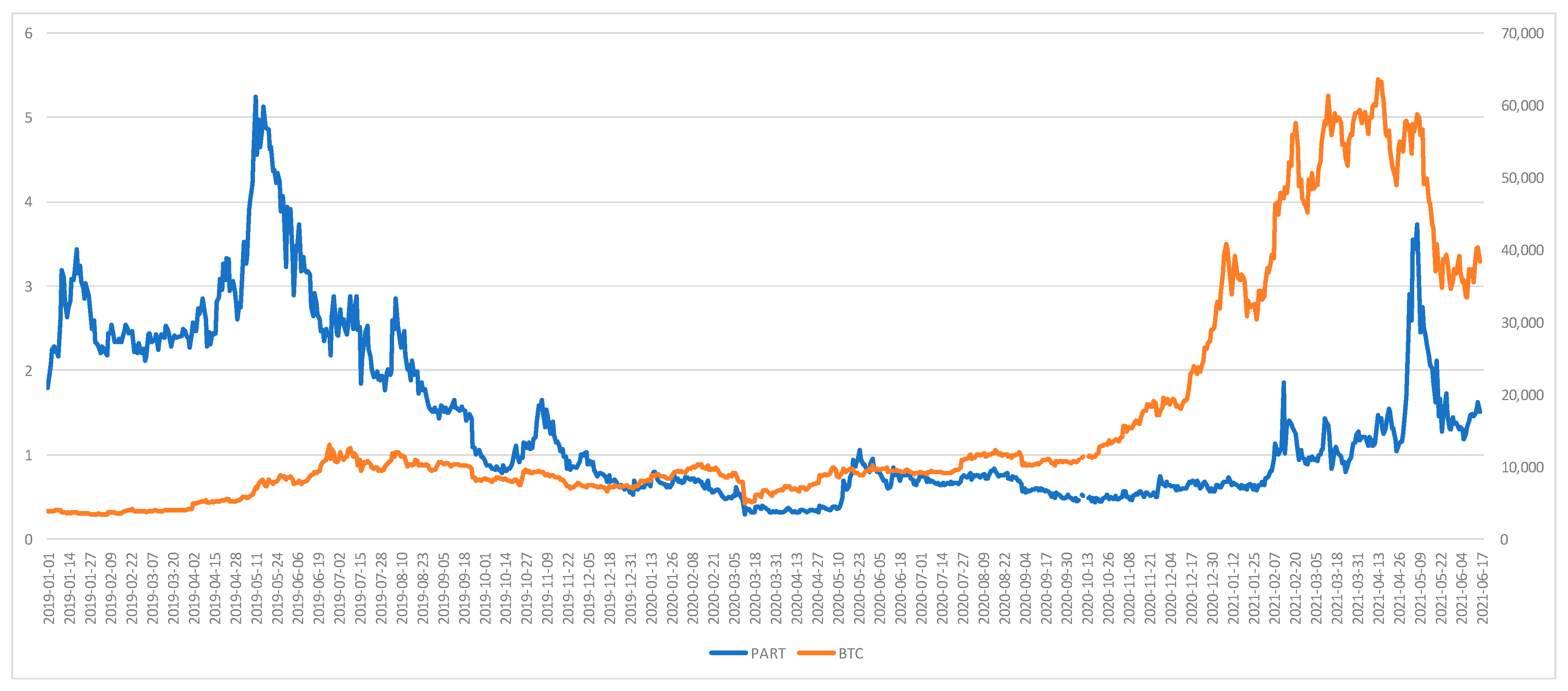

4. Results

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

Cryptocurrencies and Their Respective Data Starting Point

References

- Baydakova, Anna. 2021. Russian public officials banned from holding cryptocurrency. Coindesk. January 25. Available online: https://www.coindesk.com/russian-public-officials-banned-crypto-holdings (accessed on 22 June 2021).

- Blockchain.com. 2021. Cost Per Transaction. Available online: https://www.blockchain.com/charts/cost-per-transaction (accessed on 23 June 2021).

- Burnham, Terence C. 2020. Stephanie Kelton, The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy: PublicAffairs, New York. Journal of Bioeconomics, 1–7. [Google Scholar] [CrossRef]

- Böhme, R., N. Christin, B. Edelman, and T. Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef] [Green Version]

- Casino, Fran, Thomas K. Dasaklis, and Constantinos Patsakis. 2019. A systematic literature review of blockchain-based applications: Current status, classification and open issues. Telematics and Informatics 36: 55–81. [Google Scholar] [CrossRef]

- Chaum, David. 1993. Numbers can be a better form of cash than paper. In Computer Security and Industrial Cryptography. Edited by Bart Preneel, René Govaerts and Joos Vandewalle. Lecture Notes in Computer Science. Berlin/Heidelberg: Springer, vol. 741. [Google Scholar]

- Coindesk. 2021. Media Platform for the Cryptocurrencies and Digital Assets. June 18. Available online: https://www.coindesk.com/ (accessed on 18 June 2021).

- CoinMarketCap. 2021. Today’s Cryptocurrency Prices by Market Cap. June 21. Available online: https://coinmarketcap.com/ (accessed on 21 June 2021).

- Eldefrawy, Karim, Ashish Gehani, and Alexandre Matton. 2019. Longitudinal Analysis of Misuse of Bitcoin. In Applied Cryptography and Network Security. Edited by Robert Deng, Valérie Gauthier-Umaña, Martin Ochoa and Moti Yung. ACNS 2019. Lecture Notes in Computer Science. Cham: Springer, vol. 11464. [Google Scholar] [CrossRef]

- Giudici, Paolo, and Paolo Pagnottoni. 2019. High frequency price change spillovers in Bitcoin markets. Risks 7: 111. [Google Scholar] [CrossRef] [Green Version]

- Giudici, Paolo, and Paolo Pagnottoni. 2020. Vector error correction models to measure connectedness of Bitcoin exchange markets. Appl Stochastic Models Bus Indian 36: 95–109. [Google Scholar] [CrossRef] [Green Version]

- Giudici, Paolo, Paolo Pagnottoni, and Gloria Polinesi. 2020. Network models to enhance automated cryptocurrency portfolio management. Frontiers in Artificial Intelligence 3: 22. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Giudici, Paolo, T. Leach, and Paolo Pagnottoni. 2021. Libra or Librae? Basket based stablecoins to mitigate foreign exchange volatility spillovers. Finance Research Letters. in press, corrected proof. [Google Scholar] [CrossRef]

- Handagama, Sandali. 2021. Egyptians are buying Bitcoin despite prohibitive new banking laws. Coindesk. March 5. Available online: https://www.coindesk.com/egyptians-are-buying-bitcoin-despite-prohibitive-new-banking-laws (accessed on 22 June 2021).

- Harvey, John, and Ines Branco-Illodo. 2020. Why Cryptocurrencies want privacy: A review of political motivations and branding expressed in “Privacy Coin” whitepapers. Journal of Political Marketing 19: 107–36. [Google Scholar] [CrossRef]

- Heavens, Andrew. 2021. China bans financial, payment institutions from cryptocurrency business. Reuters. May 18. Available online: https://www.reuters.com/technology/chinese-financial-payment-bodies-barred-cryptocurrency-business-2021-05-18/ (accessed on 22 June 2021).

- Herskind, Lasse, Panagiota Katsikouli, and Nicola Dragoni. 2020. Privacy and Cryptocurrencies—A Systematic Literature Review. IEEE Access 8: 54044–59. [Google Scholar] [CrossRef]

- Hilmola, Olli-Pekka. 2014. Labile Fiat Currencies: Sketch of Future Alternatives. In Innovation in Financial Services: A Dual Ambiguity. Edited by Anne-Laure Mention and Marko Torkkeli. Newcastle upon Tyne: Cambridge Scholars Publishing, pp. 12–31. [Google Scholar]

- Hwang, Min-Shiang, Iuon-Chang Lin, and Li-Hua Li. 2001. A simple micro-payment scheme. The Journal of Systems and Software 55: 221–29. [Google Scholar] [CrossRef]

- Iansiti, Marco, and Karim R. Lakhani. 2017. The truth about blockchain. Harvard Business Review 95: 118–27. [Google Scholar]

- Kharif, Olga. 2020. Bitcoin whales’ ownership concentration is rising during rally. Bloomberg News. November 18. Available online: https://www.bloomberg.com/news/articles/2020-11-18/bitcoin-whales-ownership-concentration-is-rising-during-rally (accessed on 24 June 2021).

- Kim, Cynthia. 2018. South Korea to ban cryptocurrency traders from using anonymous bank accounts. Reuters. January 23. Available online: https://www.reuters.com/article/us-southkorea-bitcoin-idUKKBN1FC069 (accessed on 22 June 2021).

- Orcutt, Mike. 2017. Criminals thought Bitcoin was the perfect hiding place, but they thought wrong. MIT Technology Review. September 11. Available online: https://www.technologyreview.com/2017/09/11/149211/criminals-thought-bitcoin-was-the-perfect-hiding-place-they-thought-wrong/ (accessed on 24 June 2021).

- Pagnottoni, Paulo. 2019. Neural network models for Bitcoin option pricing. Frontiers in Artificial Intelligence 2: 5. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Pagnottoni, Paulo, and Thomas Dimpfl. 2019. Price discovery on Bitcoin markets. Digital Finance 1: 139–61. [Google Scholar] [CrossRef] [Green Version]

- Rearick. 2021. Pirate Chain (ARRR) Price Predictions: Where Will the ARRR Crypto Go After Sky-High Gains? InvestorsPlace. April 23. Available online: https://investorplace.com/2021/04/pirate-chain-arrr-price-predictions-where-will-the-arrr-crypto-go-after-sky-high-gains/ (accessed on 24 June 2021).

- Resta, Marina, Paulo Pagnottoni, and Maria Elena De Giuli. 2020. Technical analysis on the Bitcoin market: Trading opportunities or investors’ pitfall? Risks 8: 44. [Google Scholar] [CrossRef]

- Shoffman, Marc. 2021. Cryptocurrency novice got £185,000 Bitcoin in his account by MISTAKE. The Sun. May 21. Available online: https://www.thesun.co.uk/money/15027543/cryptocurrency-novice-got-185000-bitcoin-by-mistake/ (accessed on 24 June 2021).

- Schilling, Linda, and Harald Uhlig. 2019. Some simple bitcoin economics. Journal of Monetary Economics 106: 16–26. [Google Scholar] [CrossRef]

- Szalay, Eva. 2021. Goldman Sachs executes its first bitcoin derivatives trades. Financial Times. May 7. Available online: https://www.ft.com/content/5ec1d0aa-7992-4fb8-8011-9d7f7b44faac (accessed on 16 July 2021).

- Tsiulin, Sergey, Kristian Hegner Reinau, Olli-Pekka Hilmola, and Nikolay Goryaev. 2020. Blockchain in maritime port management: Defining key conceptual framework. Review of International Business and Strategy 30: 201–24. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2016. The inefficiency of Bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Watorek, Marcin, Stanislaw Drożdż, Jaroslaw Kwapień, Ludvico Minati, Pawel Oświęcimka, and Marek Stanuszek. 2021. Multiscale characteristics of the emerging global cryptocurrency market. Physics Reports 901: 1–82. [Google Scholar] [CrossRef]

- Wayback Machine. 2021. Internet Archive. Available online: https://archive.org/web/ (accessed on 21 June 2021).

- Wright, Marie. 1997. Authenticating electronic cash transactions. Computer Fraud & Security 4: 10–13. [Google Scholar] [CrossRef]

- Yahoo Finance. 2021. All screeners/Matching cryptocurrencies. June 18. Available online: https://finance.yahoo.com/cryptocurrencies/ (accessed on 18 June 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Crypto | Market Cap |

|---|---|

| BTC | 640.2 |

| ETH | 246.2 |

| USDT | 62.7 |

| BNB | 50.1 |

| ADA | 43.9 |

| DOGE | 34.5 |

| XRP | 33.6 |

| USDC | 24.4 |

| DOT | 18.5 |

| UNI | 11.1 |

| BCH | 10.0 |

| LTC | 9.8 |

| BUSD | 9.7 |

| SOL | 9.0 |

| LINK | 8.8 |

| MATIC | 8.5 |

| THETA | 8.3 |

| XLM | 6.6 |

| WBTC | 6.5 |

| VET | 6.0 |

| 2 largest | 886.4 |

| Share | 62% |

| 10 largest | 1165.4 |

| Share | 82% |

| 20 largest | 1248.5 |

| Share | 88% |

| Total market cap: | 1420.0 |

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

|---|---|---|---|---|---|---|---|

| BTC | 11,823.4% | 8526.8% | 3653.2% | 174.4% | 874.9% | 420.4% | 27.6% |

| ZEN | 47.1% | 1464.6% | 886.4% | 602.0% | |||

| XMR | 59,730.5% | 55,872.1% | 1894.4% | −22.4% | 476.1% | 509.1% | 104.8% |

| CVC | −73.5% | 340.6% | 1235.7% | 179.6% | |||

| ZEC | 185.9% | −76.0% | 131.9% | 394.0% | 144.0% | ||

| XVG | 670,350.0% | 178,686.7% | 121,800.0% | −82.8% | 280.2% | 649.9% | 265.9% |

| Dash | 8226.9% | 4691.7% | 1341.0% | −84.6% | 99.6% | 286.5% | 83.4% |

| ARK | −86.3% | 166.5% | 642.2% | 167.1% | |||

| NAV | 51,060.2% | 21,492.5% | 974.0% | −89.1% | 152.7% | 356.3% | 211.5% |

| XDN | 3207.4% | 3414.1% | 2642.7% | −89.2% | 82.4% | 290.5% | 155.3% |

| QRL | −89.8% | 46.4% | 308.8% | 52.8% | |||

| KMD | −90.7% | 12.0% | 80.6% | 84.8% | |||

| PART | −91.0% | 8.1% | 254.7% | 239.0% | |||

| BCN | 5462.5% | 1335.5% | 667.2% | −92.5% | −37.8% | 57.8% | 171.3% |

| PIVX | 10,279.0% | −93.2% | −14.2% | 230.6% | 130.6% | ||

| SKY | −96.8% | 25.4% | 199.0% | 131.0% | |||

| AION | −96.9% | 13.9% | 217.0% | 145.1% | |||

| ARRR | 13935.8% | 2688.5% | |||||

| BAT | 225.4% | ||||||

| IOTX | 174.4% | 537.8% | 228.3% | ||||

| NIX | 12.1% | 304.1% | 212.4% | ||||

| STORJ | 204.0% | ||||||

| WAN | 102.4% | 303.9% | 124.1% | ||||

| XSN | 115.2% | 296.0% | 0.2% |

| AION | ARK | ARRR | BAT | BCN | BTC | CVC | Dash | IOTX | KMD | NAV | NIX | PART | PIVX | QRL | SKY | STORJ | WAN | XDN | XMR | XSN | XVG | ZEC | ZEN | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AION | 1.000 | |||||||||||||||||||||||

| ARK | 0.917 | 1.000 | ||||||||||||||||||||||

| ARRR | 0.661 | 0.604 | 1.000 | |||||||||||||||||||||

| BAT | 0.957 | 0.954 | 0.680 | 1.000 | ||||||||||||||||||||

| BCN | 0.847 | 0.745 | 0.603 | 0.776 | 1.000 | |||||||||||||||||||

| BTC | −0.062 | 0.139 | 0.551 | 0.851 | 0.103 | 1.000 | ||||||||||||||||||

| CVC | 0.776 | 0.878 | 0.619 | 0.936 | 0.627 | 0.419 | 1.000 | |||||||||||||||||

| Dash | 0.883 | 0.956 | 0.703 | 0.921 | 0.769 | 0.332 | 0.835 | 1.000 | ||||||||||||||||

| IOTX | 0.586 | 0.949 | 0.681 | 0.963 | 0.496 | 0.682 | 0.924 | 0.889 | 1.000 | |||||||||||||||

| KMD | 0.905 | 0.944 | 0.646 | 0.960 | 0.752 | 0.176 | 0.852 | 0.943 | 0.893 | 1.000 | ||||||||||||||

| NAV | 0.944 | 0.967 | 0.575 | 0.952 | 0.795 | 0.260 | 0.835 | 0.951 | 0.928 | 0.946 | 1.000 | |||||||||||||

| NIX | 0.761 | 0.756 | 0.613 | 0.919 | 0.658 | 0.392 | 0.665 | 0.762 | 0.731 | 0.791 | 0.813 | 1.000 | ||||||||||||

| PART | 0.906 | 0.872 | 0.688 | 0.771 | 0.774 | −0.143 | 0.690 | 0.826 | 0.409 | 0.830 | 0.885 | 0.494 | 1.000 | |||||||||||

| PIVX | 0.956 | 0.960 | 0.644 | 0.960 | 0.826 | 0.101 | 0.818 | 0.943 | 0.796 | 0.938 | 0.968 | 0.861 | 0.914 | 1.000 | ||||||||||

| QRL | 0.959 | 0.927 | 0.610 | 0.845 | 0.809 | −0.001 | 0.817 | 0.912 | 0.769 | 0.913 | 0.946 | 0.770 | 0.923 | 0.956 | 1.000 | |||||||||

| SKY | 0.950 | 0.873 | 0.573 | 0.926 | 0.869 | −0.023 | 0.734 | 0.856 | 0.586 | 0.882 | 0.905 | 0.836 | 0.859 | 0.924 | 0.908 | 1.000 | ||||||||

| STORJ | 0.913 | 0.940 | 0.508 | 0.907 | 0.678 | 0.730 | 0.867 | 0.770 | 0.869 | 0.928 | 0.872 | 0.860 | 0.598 | 0.886 | 0.724 | 0.870 | 1.000 | |||||||

| WAN | 0.973 | 0.905 | 0.665 | 0.973 | 0.830 | 0.060 | 0.612 | 0.881 | 0.796 | 0.856 | 0.938 | 0.837 | 0.920 | 0.975 | 0.954 | 0.938 | 0.927 | 1.000 | ||||||

| XDN | 0.921 | 0.815 | 0.769 | 0.919 | 0.835 | 0.184 | 0.717 | 0.789 | 0.827 | 0.836 | 0.870 | 0.791 | 0.828 | 0.855 | 0.867 | 0.864 | 0.851 | 0.970 | 1.000 | |||||

| XMR | 0.658 | 0.757 | 0.798 | 0.893 | 0.612 | 0.737 | 0.819 | 0.829 | 0.836 | 0.776 | 0.771 | 0.555 | 0.582 | 0.704 | 0.669 | 0.644 | 0.773 | 0.517 | 0.664 | 1.000 | ||||

| XSN | 0.548 | 0.745 | 0.371 | 0.636 | 0.461 | 0.515 | 0.732 | 0.708 | 0.764 | 0.659 | 0.723 | 0.479 | 0.426 | 0.636 | 0.662 | 0.572 | 0.519 | 0.620 | 0.669 | 0.673 | 1.000 | |||

| XVG | 0.868 | 0.830 | 0.764 | 0.959 | 0.766 | 0.387 | 0.790 | 0.843 | 0.948 | 0.915 | 0.868 | 0.723 | 0.725 | 0.856 | 0.812 | 0.858 | 0.878 | 0.870 | 0.860 | 0.803 | 0.712 | 1.000 | ||

| ZEC | 0.886 | 0.906 | 0.773 | 0.932 | 0.638 | 0.094 | 0.878 | 0.757 | 0.883 | 0.889 | 0.746 | 0.765 | 0.856 | 0.753 | 0.931 | 0.820 | 0.803 | 0.836 | 0.657 | 0.574 | 0.766 | 0.631 | 1.000 | |

| ZEN | 0.293 | 0.444 | 0.866 | 0.883 | 0.251 | 0.772 | 0.656 | 0.437 | 0.801 | 0.464 | 0.391 | 0.540 | 0.234 | 0.331 | 0.345 | 0.317 | 0.704 | 0.335 | 0.352 | 0.844 | 0.554 | 0.549 | 0.460 | 1.000 |

| AION | ARK | ARRR | BAT | BCN | BTC | CVC | Dash | IOTX | KMD | NAV | NIX | PART | PIVX | QRL | SKY | STORJ | WAN | XDN | XMR | XSN | XVG | ZEC | ZEN | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AION | 1.000 | |||||||||||||||||||||||

| ARK | 0.908 | 1.000 | ||||||||||||||||||||||

| ARRR | 0.661 | 0.604 | 1.000 | |||||||||||||||||||||

| BAT | 0.957 | 0.954 | 0.680 | 1.000 | ||||||||||||||||||||

| BCN | 0.633 | 0.474 | 0.603 | 0.776 | 1.000 | |||||||||||||||||||

| BTC | 0.650 | 0.830 | 0.551 | 0.851 | 0.168 | 1.000 | ||||||||||||||||||

| CVC | 0.823 | 0.945 | 0.619 | 0.936 | 0.389 | 0.937 | 1.000 | |||||||||||||||||

| Dash | 0.867 | 0.871 | 0.703 | 0.921 | 0.549 | 0.824 | 0.908 | 1.000 | ||||||||||||||||

| IOTX | 0.887 | 0.956 | 0.681 | 0.963 | 0.446 | 0.867 | 0.956 | 0.901 | 1.000 | |||||||||||||||

| KMD | 0.923 | 0.917 | 0.646 | 0.960 | 0.641 | 0.695 | 0.855 | 0.885 | 0.886 | 1.000 | ||||||||||||||

| NAV | 0.887 | 0.963 | 0.575 | 0.952 | 0.475 | 0.861 | 0.952 | 0.887 | 0.956 | 0.902 | 1.000 | |||||||||||||

| NIX | 0.858 | 0.854 | 0.613 | 0.919 | 0.644 | 0.628 | 0.790 | 0.805 | 0.826 | 0.897 | 0.868 | 1.000 | ||||||||||||

| PART | 0.423 | 0.212 | 0.688 | 0.771 | 0.755 | −0.106 | 0.107 | 0.304 | 0.179 | 0.383 | 0.209 | 0.430 | 1.000 | |||||||||||

| PIVX | 0.929 | 0.934 | 0.644 | 0.960 | 0.606 | 0.699 | 0.865 | 0.858 | 0.905 | 0.905 | 0.921 | 0.876 | 0.398 | 1.000 | ||||||||||

| QRL | 0.765 | 0.788 | 0.610 | 0.845 | 0.600 | 0.745 | 0.816 | 0.859 | 0.792 | 0.818 | 0.830 | 0.805 | 0.449 | 0.797 | 1.000 | |||||||||

| SKY | 0.891 | 0.912 | 0.573 | 0.926 | 0.641 | 0.729 | 0.886 | 0.903 | 0.888 | 0.933 | 0.921 | 0.895 | 0.416 | 0.916 | 0.871 | 1.000 | ||||||||

| STORJ | 0.913 | 0.940 | 0.508 | 0.907 | 0.678 | 0.730 | 0.867 | 0.770 | 0.869 | 0.928 | 0.872 | 0.860 | 0.598 | 0.886 | 0.724 | 0.870 | 1.000 | |||||||

| WAN | 0.909 | 0.967 | 0.665 | 0.973 | 0.465 | 0.857 | 0.956 | 0.907 | 0.966 | 0.918 | 0.956 | 0.855 | 0.171 | 0.908 | 0.801 | 0.897 | 0.927 | 1.000 | ||||||

| XDN | 0.872 | 0.904 | 0.769 | 0.919 | 0.532 | 0.786 | 0.889 | 0.906 | 0.929 | 0.877 | 0.890 | 0.806 | 0.294 | 0.877 | 0.809 | 0.864 | 0.851 | 0.929 | 1.000 | |||||

| XMR | 0.741 | 0.842 | 0.798 | 0.893 | 0.291 | 0.916 | 0.913 | 0.894 | 0.897 | 0.766 | 0.842 | 0.689 | 0.023 | 0.749 | 0.763 | 0.753 | 0.773 | 0.895 | 0.896 | 1.000 | ||||

| XSN | 0.570 | 0.712 | 0.371 | 0.636 | 0.101 | 0.811 | 0.746 | 0.638 | 0.724 | 0.568 | 0.738 | 0.562 | −0.079 | 0.626 | 0.655 | 0.589 | 0.519 | 0.719 | 0.663 | 0.730 | 1.000 | |||

| XVG | 0.869 | 0.926 | 0.764 | 0.959 | 0.440 | 0.870 | 0.947 | 0.918 | 0.953 | 0.878 | 0.930 | 0.823 | 0.168 | 0.869 | 0.803 | 0.863 | 0.878 | 0.961 | 0.944 | 0.934 | 0.709 | 1.000 | ||

| ZEC | 0.850 | 0.881 | 0.773 | 0.932 | 0.456 | 0.848 | 0.909 | 0.956 | 0.917 | 0.864 | 0.883 | 0.797 | 0.193 | 0.849 | 0.828 | 0.848 | 0.803 | 0.929 | 0.938 | 0.948 | 0.730 | 0.953 | 1.000 | |

| ZEN | 0.761 | 0.823 | 0.866 | 0.883 | 0.361 | 0.846 | 0.891 | 0.875 | 0.883 | 0.769 | 0.819 | 0.687 | 0.078 | 0.754 | 0.714 | 0.738 | 0.704 | 0.875 | 0.881 | 0.947 | 0.648 | 0.937 | 0.926 | 1.000 |

| Classes | AION | ARK | ARRR | BAT | BCN | CVC | Dash | IOTX | KMD | NAV | NIX | PART |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| −1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| −0.9 | 0 | 0 | 0 | 0 | 0 | 0 | 27 | 0 | 0 | 0 | 0 | 0 |

| −0.7 | 24 | 0 | 0 | 0 | 33 | 0 | 49 | 0 | 0 | 26 | 0 | 5 |

| −0.5 | 44 | 25 | 0 | 0 | 34 | 24 | 42 | 48 | 0 | 45 | 48 | 24 |

| −0.3 | 52 | 56 | 11 | 27 | 139 | 44 | 24 | 37 | 48 | 161 | 41 | 42 |

| −0.1 | 32 | 44 | 19 | 20 | 259 | 38 | 58 | 67 | 36 | 199 | 29 | 108 |

| 0 | 7 | 24 | 3 | 5 | 132 | 15 | 51 | 20 | 8 | 107 | 32 | 65 |

| 0.1 | 14 | 17 | 2 | 20 | 138 | 12 | 48 | 46 | 14 | 103 | 26 | 82 |

| 0.3 | 58 | 62 | 80 | 15 | 342 | 40 | 145 | 111 | 110 | 269 | 72 | 127 |

| 0.5 | 161 | 100 | 62 | 49 | 270 | 156 | 308 | 79 | 203 | 286 | 65 | 108 |

| 0.7 | 243 | 297 | 141 | 86 | 375 | 304 | 296 | 187 | 389 | 338 | 213 | 214 |

| 0.9 | 447 | 647 | 162 | 103 | 482 | 509 | 783 | 260 | 471 | 549 | 406 | 461 |

| 1 | 157 | 178 | 60 | 0 | 163 | 191 | 536 | 166 | 216 | 284 | 25 | 93 |

| Total: | 1239 | 1450 | 540 | 325 | 2367 | 1333 | 2367 | 1021 | 1495 | 2367 | 957 | 1329 |

| −0.3–1: | 120 | 81 | 11 | 27 | 206 | 68 | 142 | 85 | 48 | 232 | 89 | 71 |

| Share: | 10% | 6% | 2% | 8% | 9% | 5% | 6% | 8% | 3% | 10% | 9% | 5% |

| 0.1–1: | 173 | 166 | 35 | 72 | 735 | 133 | 299 | 218 | 106 | 641 | 176 | 326 |

| Share: | 14% | 11% | 6% | 22% | 31% | 10% | 13% | 21% | 7% | 27% | 18% | 25% |

| Classes | PIVX | QRL | SKY | STORJ | WAN | XDN | XMR | XSN | XVG | ZEC | ZEN |

|---|---|---|---|---|---|---|---|---|---|---|---|

| −1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| −0.9 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| −0.7 | 0 | 0 | 0 | 0 | 0 | 100 | 0 | 0 | 0 | 0 | 0 |

| −0.5 | 55 | 2 | 9 | 0 | 25 | 83 | 15 | 32 | 117 | 22 | 23 |

| −0.3 | 115 | 25 | 40 | 0 | 32 | 84 | 58 | 99 | 60 | 18 | 41 |

| −0.1 | 86 | 11 | 37 | 0 | 51 | 170 | 72 | 41 | 130 | 29 | 56 |

| 0 | 29 | 14 | 70 | 0 | 12 | 89 | 32 | 54 | 102 | 43 | 31 |

| 0.1 | 36 | 11 | 37 | 0 | 14 | 112 | 54 | 25 | 102 | 22 | 24 |

| 0.3 | 104 | 65 | 82 | 0 | 79 | 231 | 130 | 78 | 320 | 98 | 57 |

| 0.5 | 285 | 212 | 163 | 17 | 84 | 300 | 259 | 95 | 387 | 98 | 137 |

| 0.7 | 461 | 367 | 318 | 62 | 206 | 371 | 384 | 220 | 351 | 254 | 216 |

| 0.9 | 590 | 563 | 455 | 40 | 406 | 703 | 566 | 317 | 480 | 651 | 562 |

| 1 | 92 | 100 | 213 | 1 | 175 | 124 | 797 | 102 | 280 | 359 | 232 |

| Total: | 1853 | 1370 | 1424 | 120 | 1084 | 2367 | 2367 | 1063 | 2329 | 1594 | 1379 |

| −0.3–1: | 170 | 27 | 49 | 0 | 57 | 267 | 73 | 131 | 177 | 40 | 64 |

| Share: | 9% | 2% | 3% | 0% | 5% | 11% | 3% | 12% | 8% | 3% | 5% |

| 0.1–1: | 321 | 63 | 193 | 0 | 134 | 638 | 231 | 251 | 511 | 134 | 175 |

| Share: | 17% | 5% | 14% | 0% | 12% | 27% | 10% | 24% | 22% | 8% | 13% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hilmola, O.-P. On Prices of Privacy Coins and Bitcoin. J. Risk Financial Manag. 2021, 14, 361. https://doi.org/10.3390/jrfm14080361

Hilmola O-P. On Prices of Privacy Coins and Bitcoin. Journal of Risk and Financial Management. 2021; 14(8):361. https://doi.org/10.3390/jrfm14080361

Chicago/Turabian StyleHilmola, Olli-Pekka. 2021. "On Prices of Privacy Coins and Bitcoin" Journal of Risk and Financial Management 14, no. 8: 361. https://doi.org/10.3390/jrfm14080361

APA StyleHilmola, O.-P. (2021). On Prices of Privacy Coins and Bitcoin. Journal of Risk and Financial Management, 14(8), 361. https://doi.org/10.3390/jrfm14080361