1. Introduction

This paper offers four main contributions for long-term retirement planning, with a goal to maximize the likelihood of solvency during the lifetime of the investor: (i) The model in the paper combines dynamic portfolio optimization (

Merton 1969,

1971;

Browne 1995;

Dammon et al. 2004;

Horan 2006a,

2006b;

Das et al. 2019;

Jaconetti and Bruno 2008;

Spitzer and Singh 2006;

Wang et al. 2011) and tax optimization over multiple retirement (and possibly non-retirement) accounts (

Brown et al. 2017;

Cook et al. 2015;

Sumutka et al. 2012;

DiLellio and Ostrov 2017,

2018) into one algorithm, whereas these have been handled as separate problems in the literature. (ii) Unlike most tax optimization papers, we include the effect of annual stochastic stock returns, as opposed to using fixed returns. (iii) We also consider optimization that takes into account mortality risk and its concomitant uncertain portfolio horizon, which is more realistic and useful than assuming a known terminal date or looking to optimize portfolio longevity. (iv) The analyses in the paper determine that portfolio optimization has first-order consequences on lifetime portfolio solvency, whereas the impact of tax optimization has second-order consequences. This insight means algorithms may ignore all but the most important features of the tax code when they are considering how to optimize lifetime solvency, making the optimization algorithm computationally feasible. The less important features of the tax code can then be considered independently for each individual and their specific circumstances. Some of the additional results in the paper show that this paper’s approach clearly outperforms a target date fund strategy, that it can determine the optimal time to initiate the collection of social security, and that it can determine whether or not any given annuity should be purchased by an investor. The algorithm also accommodates required minimum distributions (RMDs), infusions to the various accounts, and how to exploit conversions between retirement accounts. The approach shown here extends the academic literature and offers a comprehensive algorithm for practical retirement planning.

The innovations in this approach are timely. Over the coming decades, the United States will see a considerable increase in the percent of its population that is retired. For this coming generation of retirees, there has been a strong shift away from defined benefit plans like pensions in favor of tax deferred accounts (TDAs), such as traditional 401(k)s and IRAs, and Roth accounts (see, for example,

Department of Labor (

2019), Table E7). In general, the move away from pensions has led to fewer saved resources for these retirees, but more flexibility in how these resources may be used.

This means that many individuals in the coming wave of retirees will need to be more careful and clever than their predecessors if they hope to remain solvent throughout their retirement, but these individuals will also have more tools at their command than previous generations. In particular, to help attain the goal of staying solvent, investors will have the ability to change the investments in their portfolio and to determine how to allocate withdrawals between three types of accounts (TDAs, Roth accounts, and taxable accounts) in order to meet annual consumption needs while adhering to the different tax regulations governing these accounts.

There are key differences in the main features of how a TDA, a Roth account, and a taxable account are taxed in the current American tax system. For TDAs, contributions, in the year they are made, are deductible from taxable income, but withdrawals, in the year they are made, are taxed as income. For Roth accounts, the opposite holds in the sense that contributions are not deductible from taxable income, so they are taxed as income in the year they are made, but then the Roth account is not subject to tax after that. For both TDAs and Roth accounts, we assume that withdrawals are not made before an investor is 59.5 years old, since those withdrawals may be subject to penalties. Starting at age 72, TDAs (though not Roth accounts) are subject to required minimum distributions (RMDs) to avoid penalties. In taxable accounts, bonds and cash are subject to different rules than stock. The interest from cash and bonds is taxed as income. There is no tax on stock, except when it is sold, at which point the stock’s gains are subject to capital gains taxes.

Sources that are taxed as income, such as TDA withdrawals, bond and cash interest, as well as earned income from work, are subject to a progressive tax system with rates ranging from 10% to 37%. Long term capital gains (for stock sold more than a year after being purchased, as we will always assume) are subject to a progressive tax system with rates that are 0%, 15%, or 20%, depending on both income and gains. Wealthier investors may also be subject to a 3.8% Net Investment Income Tax. There are complicated rules to determine what portion of Social Security payments are taxed as income. This paper incorporates those Social Security rules, and the current rules for all the features described above for TDAs, Roth accounts, taxable accounts, and earned income. Since it is unclear how legislation might change the tax structure in the future, we assume the current tax structure holds throughout our calculations in this paper, although we can also incorporate stochastic models for evolving tax structures, as discussed at the end of this paper in the conclusions section.

Determining the optimal investment strategy and determining the optimal tax strategy for allocating withdrawals involve different, complex issues. In part because of this, these two strategic questions are generally separated from each other in the literature, which will be discussed in the next two sections. In one branch of the literature, the optimal investment strategy is explored, but usually the portfolio is considered to be tax free, or, on occasion, the entire portfolio is a taxable account. In the other branch, tax optimization via withdrawal allocations between accounts is considered, but significant assumptions about the investments are made, such as a projected, generally constant, rate of return. The tax code, by necessity, is also simplified, but how much impact do these simplifying assumptions create?

In this paper, we consider both investment optimization and tax optimization

1 together, using ideas from both branches of the literature. Instead of the two creating a more complicated optimization when they are combined, we find that they lead to important simplifications instead.

The approach to optimally attaining the investor’s goal of staying solvent will start with determining investment optimization on a post-tax basis using dynamic programming. This computes the optimal dynamic investment portfolio strategy by working chronologically backwards in time. We note that in addition to using the stochastic nature of the investments, we also account for the stochastic nature of mortality, which is uncommon in the literature. However, working with the mortality distribution is crucial for optimizing the probability that the investor will remain solvent until their death. We will compare this to the far more common, but far less realistic, assumption of a projected date of death for the investor. In addition, note that the model is superior to the typical approach of looking to optimize portfolio longevity, since, for example, a 100-year-old investor with significant money should be in a conservative portfolio for their remaining years, not an aggressive one in the hopes of having it last another 100 or more years.

Having obtained the optimal investment strategy, the algorithm optimizes the tax strategy using Monte Carlo simulation, which works chronologically forwards in time. We determine annual taxes by carefully following the progressive taxation rules in America for the two main sources of tax revenue from individuals: Income taxes, which includes tax generated by Social Security income, and capital gains taxes. Within this framework, we look to optimize two variables numerically. The first variable is the level of TDA consumption, which is the key scalar quantity for tax optimization when withdrawal allocations are structured correctly. The theory for this structure is a generalization, and improvement, on what is known as the “informed strategy” in the literature. The second variable is a correction factor that accounts for the fact that we must approximate the portfolio’s overall post-tax worth by using the current pre-tax worth of the three accounts (TDA, Roth, and taxable), and we cannot be certain how much tax will be levied on future withdrawals in the TDA and future realized capital gains in the taxable account.

We find the following key result: The probability that the investor remains solvent is strongly affected by their investment strategy, but the effect of the taxation optimization, while present, is much weaker. For example, for the three investors analyzed in this paper, we will see that investment optimization increases their solvency probability by 16.5, 16.6, and 4.7 percentage points over a standard target date fund strategy, whereas tax optimization increases their solvency probability by, at most, 1.7, 1.2, and 2.8 percentage points respectively. This suggests that adding further complicated details of the tax code or the withdrawal allocation structure between accounts is not worthwhile, as it will not have a meaningful effect on the solvency probability.

This is not to say that tax optimization is not important, of course. Investment optimization may have a far larger effect on the probability of solvency, but tax optimization generates far more stable sources of additional money. So, for example, an investor may have consumption needs of $80,000 every year, while tax optimization may generate an extra $50,000 over the course of retirement. The ability to fund an extra 5/8 of a year will not have much of an effect on their probability of remaining solvent until their death, but no wealth manager should leave an extra $50,000 in tax savings on the table.

In this paper we assume we know the following information about investors: Their current age, the current amount of money in their TDA and Roth accounts, and, for their taxable account, the current amount in bonds (and cash), as well as the current amount in stock and its cost basis. We also assume we are given projections which can vary over time for: (1) the time they will retire and, prior to that, the amount of money they would like to contribute to their TDA and the amount to their Roth in each year they are working, (2) the amount of earned income they will receive each year, (3) standard or itemized deductions for income tax each year, (4) the amount of Social Security income for each year, (5) additional after-tax income each year that is neither earned nor derived from the investor’s three accounts, such as projected inheritance money, for example, (6) the investor’s mortality table, and (7) perhaps most importantly, projected after-tax consumption needs each year, which, if desired, can also be made to depend on the investor’s wealth since investors with less wealth may wish to reduce their consumption and investors with more wealth may wish to increase their consumption. We also assume an annual rate of inflation, the interest rate for the bonds/cash, and the expected return and the covariance matrix for the stochastic stock investments. Since these projections and circumstances will change over time for investors, the algorithm we describe in this paper should be periodically rerun to incorporate any updated information.

A summary of the main contributions of this paper is as follows: (1) The paper develops an approach where dynamic programming for investment optimization can be combined with numerical methods for tax optimization. (2) The optimization approach for the combined investment and tax strategy is extended to the context where both investment returns and mortality are stochastic. (3) The implementation here expands and improves previous tax efficiency approaches, obtaining a simple, but effective, approach to tax optimization. (4) Our results show that investment optimization is far more important than tax optimization for maximizing the probability that an investor can remain solvent. This means that more complicated taxation models with more variables are unlikely to generate meaningful and improved results for a retiree’s solvency probability. (5) The new investment optimization approach in this paper leads to a much higher solvency probability than using a target date fund or a static portfolio if the likelihood of an investor’s death is determined by a mortality table. Furthermore, these advantages become even stronger if the mortality table is replaced with the more common, though unrealistic, assumption of a projected date of death for the investor. (6) The combined optimization algorithm in this paper can be used to determine (a) when an investor should optimally start collecting Social Security, (b) the price at which an annuity transitions from increasing to decreasing the investor’s solvency probability, and (c) how changes in the investors’ saving or spending behavior over time will affect their optimal probability of solvency.

The rest of the paper proceeds as follows.

Section 2 briefly relates the new approach shown here to the investment optimization literature, while

Section 3 compares this paper’s approach with extant methods in the tax optimization literature. Our model and its assumptions are presented in

Section 4.

Section 5 contains extensive numerical analyses showcasing the main results in the paper. Discussion and conclusions are in

Section 6.

3. Tax Optimization: Past Approaches and Our Approach

It is quite common for retirement planning books (e.g.,

Lange (

2009),

Rodgers (

2009),

Solin (

2010), and

Larimore et al. (

2011)) and major investment firms (e.g.,

Fidelity (

2015),

Jaconetti and Bruno (

2008), and

Vanguard (

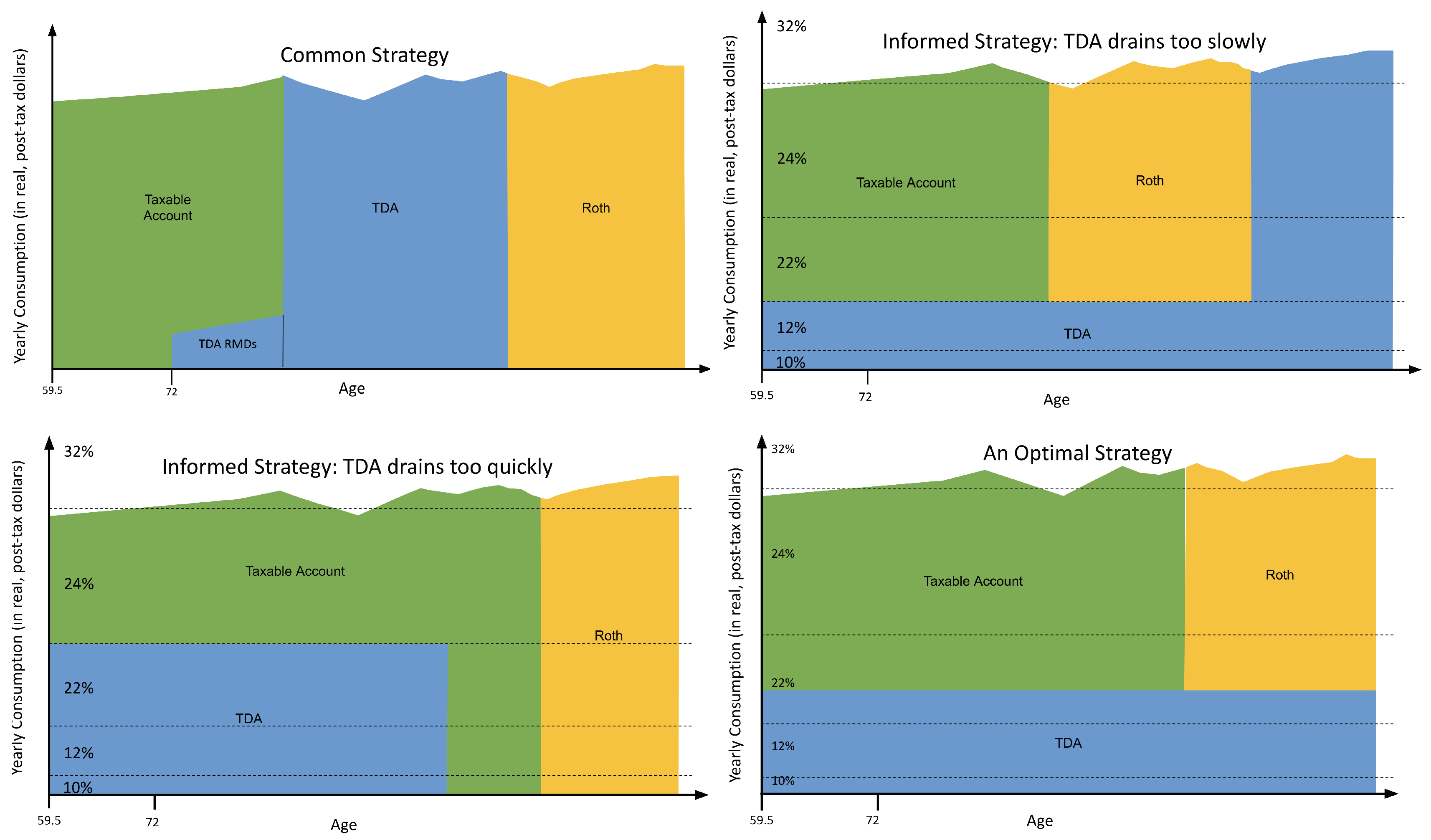

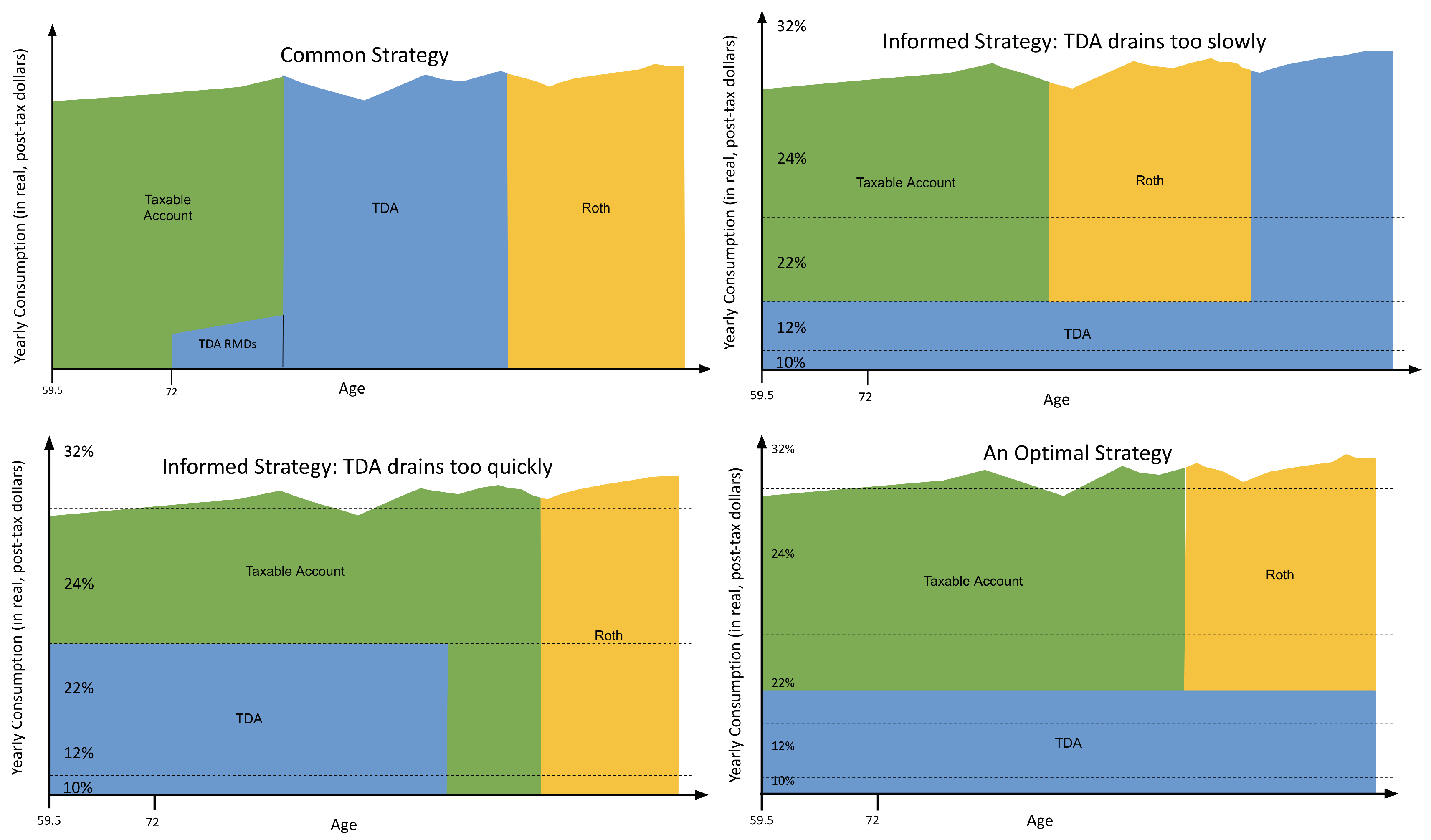

2016)) to recommend a “common strategy” for withdrawal sequencing during retirement; that is, after taking out the required minimum distributions (RMDs) from the TDA account, the retiree should satisfy their remaining consumption needs by first draining their taxable account, then their TDA, and finally their Roth (see the upper left panel in

Figure 1).

On occasion, a variation of the common strategy is recommended where the Roth is drained before the TDA instead of the other way around. There is a reason for the uncertainty in the sequencing of the TDA and Roth: In a constant (flat) tax rate environment for the TDA, the order in which the TDA and the Roth are removed actually makes no difference. Compelling examples of this were shown in

Horan (

2006a) and

Spitzer and Singh (

2006). A short, but very general proof of this fact is given in

DiLellio and Ostrov (

2018). This means that for TDA and Roth decumulation, the optimal strategy for investors is solely to reduce the tax rate for their TDA distributions, meaning they should take advantage of the lowest income tax brackets as much as possible.

Given this, Horan, in

Horan (

2006a) and

Horan (

2006b), proposed an “informed strategy” for TDA and Roth decumulation. In the informed strategy, distributions are taken from the TDA up to the top of a specific tax bracket and the Roth account is used for any additional consumption that needs to be satisfied. Should the Roth or TDA become exhausted, the other account must be used to cover all consumption needs in future years. This was expanded in

Sumutka et al. (

2012) to include taxable accounts. This expanded informed strategy is, as before, to take distributions from the TDA up to the top of a specific tax bracket, but to satisfy any additional consumption, the investor drains the taxable account first, then the Roth, then the TDA. We note that since our goal is to optimize the probability of investor solvency, draining the taxable account first is desirable because that minimizes capital gains taxes. If our goal was to optimize a bequest, we would need to consider the fact that capital gains are forgiven at death, which can make the optimal tax strategy far more complicated (e.g., see

DiLellio and Ostrov (

2018)).

A question that naturally arises with the informed strategy is which tax bracket to choose. If the tax bracket is too low, TDA distributions in later years will be at high tax rates (see the upper right panel in

Figure 1). If the tax bracket is too high, the TDA will be exhausted early and therefore unable to take advantage of lower tax brackets in later years (see the lower left panel in

Figure 1). We note that tax bracket limits are adjusted by inflation in the tax code, therefore we use real dollars in

Figure 1, which means the TDA consumption is constant over time in the graph when the consumption level stays at the top of the chosen tax bracket.

The optimal strategy that we propose and use here is to move beyond the tax bracket limitations in the informed strategy and simply choose the optimal constant TDA consumption level,

L, leading to the lower right panel in

Figure 1. This is akin to the approach taken in

DiLellio and Ostrov (

2017), where

L is found analytically for deterministic returns, a known time of death, and no taxable account. In this paper, we have stochastic returns, a distribution for the time of death, and a taxable account, so the optimal constant TDA level,

L, must be determined numerically. Since this is just a single number, as opposed to a function over time, we can use standard optimization techniques to find the optimal value of

L. Even better, the assumption of a constant

L, even in our current stochastic context, is quite reasonable: Once

L is optimized, we maintain results that look like the lower right panel in

Figure 1 over a rather wide range of typical investor outcomes, as we will see later.

We are also able to accommodate other sources of income. Sources subject to no tax can simply be subtracted from the (post-tax) consumption needs of the investor. Sources subject to income tax can be added to the bottom of the graph in

Figure 1 before the TDA is considered. One can think of these sources subject to income tax as looking like a sandy shore with the blue water of the TDA then being poured on top of the shore until the water level reaches

L. We note that while we think of

L as a post-tax level in the context of

Figure 1, in this paper we report

L in terms of its corresponding pre-tax value since we normally think about income tax brackets and sources subject to income tax in pre-tax terms.

We further tweak our withdrawal sequencing in two other ways. The first is that we always make certain that RMDs are distributed from the TDA each year, which can force the TDA distributions to rise above level

L in some years. The second is that we take advantage of Roth conversions as was done in

Cook et al. (

2015). That is, as soon as possible, we convert all of the TDA distribution except for RMDs to the Roth account (since RMDs cannot legally be converted) and address the resulting additional consumption need this leaves by using withdrawals from the taxable account. This drains the taxable account more quickly, further reducing capital gains.

4. The Model and Assumptions

In this section, we detail our model. As discussed in

Section 2, we determine the optimal investment strategy first, using dynamic programming. The details of this approach, including how to accommodate the mortality table, are contained in

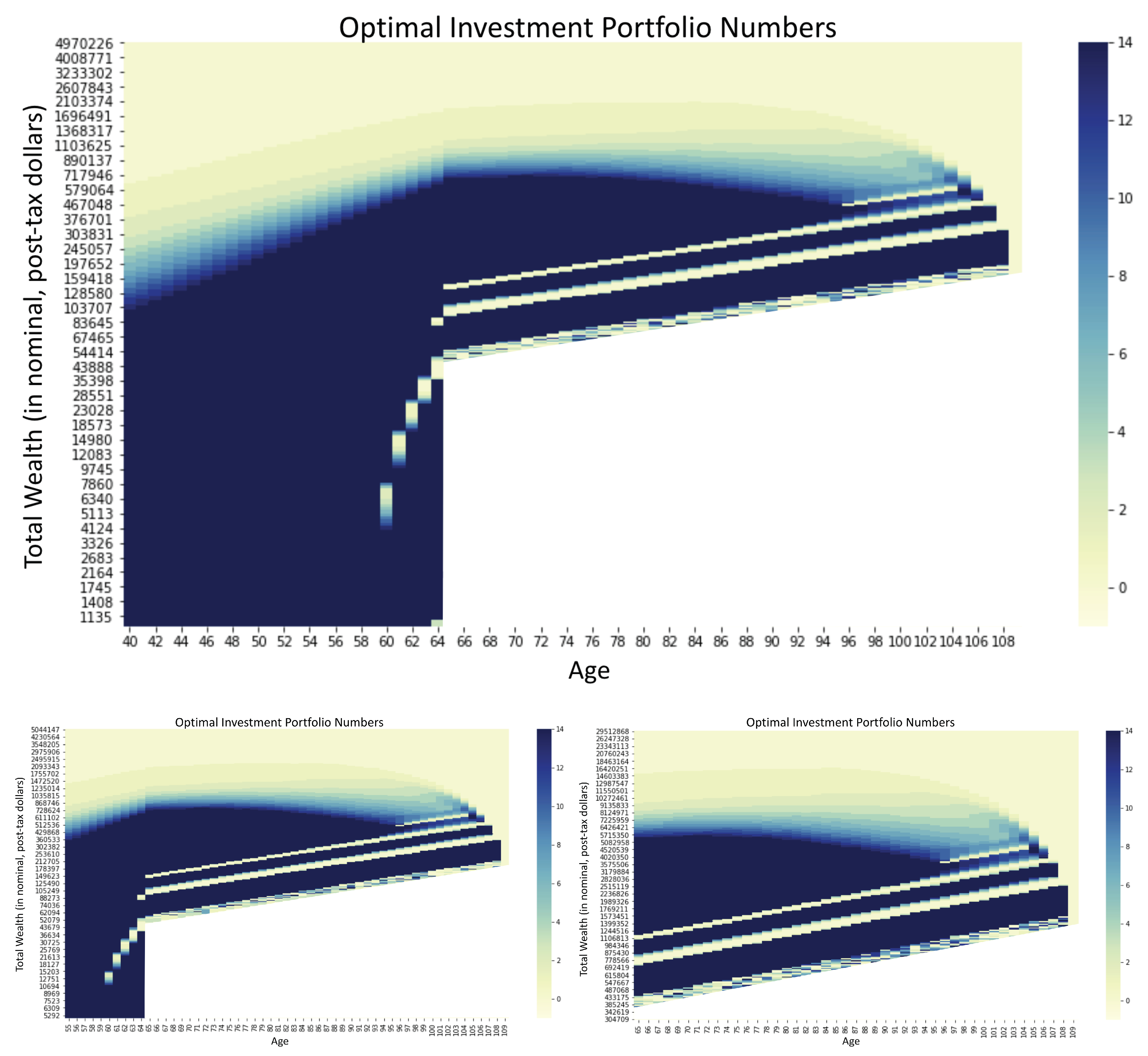

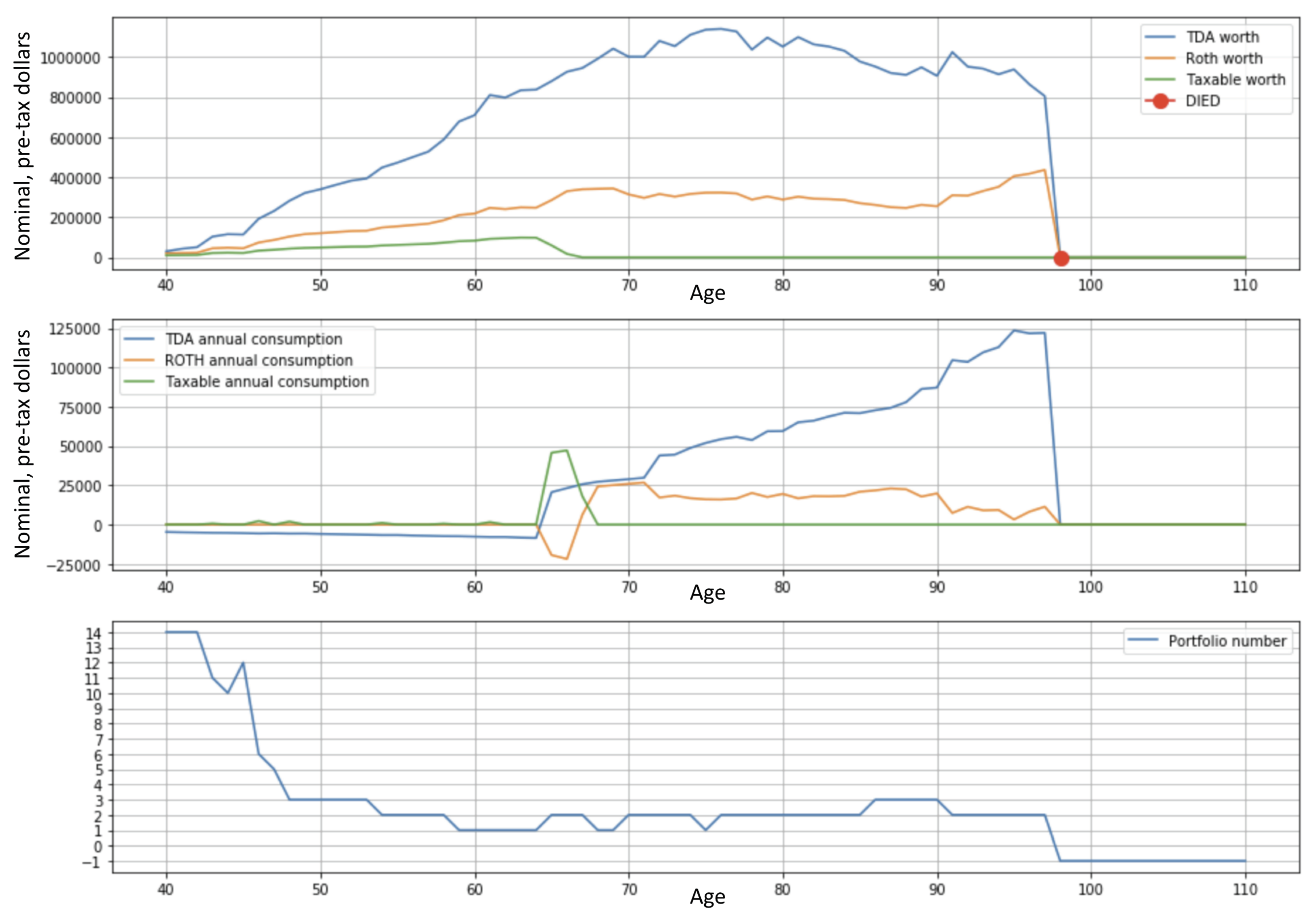

Appendix A. We note again that dynamic programming computes the optimal investment strategy by evolving it chronologically backwards in time. This is important because the optimal strategy depends on future choices, which only a backwards-in-time method has access to.

This is followed by determining the optimal tax strategy. Since we must consider the different taxation rules that apply to each of the three different accounts, and these can become complicated and depend on knowledge of past choices, we employ Monte Carlo methods, which evolve forwards in time so that we can account for path dependence. That is, our overall scheme for investment optimization followed by tax optimization is a “backwards-forwards” algorithm.

After the investment optimization is performed in the backwards part of the algorithm, we know the optimal investment allocation at any time t, given the post-tax worth of the overall portfolio at that time. Unfortunately, since we employ Monte Carlo methods for tax optimization, which evolve forwards in time, we can only know the pre-tax worth of the three accounts, not their post-tax worth, since the tax rates that will be applied in the future are not known in the present. Therefore, we must estimate the post-tax worth from our knowledge of the present. This estimate is accomplished in two phases.

Phase 1 of the post-tax estimate: In the first phase we determine an initial estimate for the post-tax worth of the overall portfolio by adding the pre-tax worth of each account, after removing an estimate of the taxes that will be levied on each account. Specifically, we sum: (1) The worth of the Roth, which has no taxes, (2) the worth of taxable bonds, after income taxes have been removed from any interest generated that year, (3) the worth of taxable stock, after applying a capital gains rate (usually 15%) to all capital gains currently in the taxable stock account, and (4) the worth of the TDA, after taking out taxes from the entire TDA at the overall rate calculated for that year’s TDA distribution.

Phase 2 of the post-tax estimate: Since our initial approximation for the post-tax worth of the portfolio is imperfect, we add a second phase to form our final approximation. In this second phase, we simply multiply the initial approximation generated in the first phase by a constant conversion correction factor, , that we will look to optimize. The product of with our initial approximation forms our final approximation for the overall post-tax worth of the portfolio, which is then used to generate the optimal investment selection for the investor from our dynamic programming results.

This means we have two numbers, L and , to optimize. Were the initial post-tax approximation perfect, we would find that . In practice, we see optimum numbers like more often.

Within our optimization algorithm for L and , we need a model for computing taxes. Our taxation model is an extensive mathematization of the federal tax code for computing income taxes and capital gains taxes. This includes laws for taxation on the following sources:

Earned income, TDA withdrawal income, and interest income from the taxable bond account, all of which are taxed as regular income using federal income tax brackets and rates;

TDA contributions, which are deducted from regular income, and annual standard deductions or projected itemized deductions;

Income from realized capital gains from the taxable stock account, which is taxed using capital gains tax brackets and rates that are affected by the investor’s regular income;

Net investment income tax (NIIT) for wealthier investors;

Social Security income, which has particularly complicated taxation rules in that the amount that is subject to being taxed as regular income depends on the other sources of regular income and sources of capital gains income listed above, which then affects the overall taxation rates for these other sources of income.

As they vary, we do not include state or local taxes in this paper, although these generally can be easily accommodated for any specific locality.

We make a number of simplifying assumptions that, for most investors, involve taxation effects that are much smaller than those determined by the taxation model for income and realized capital gains above:

We assume all capital gains are long term. We ignore capital losses. We ignore the effect of dividends;

For simplicity, we calculate gains using the average cost basis method. Although LIFO (Last In, First Out) is more tax efficient, the difference is small (see

Das et al. (

2017), for example);

We allow no withdrawals from the TDA nor Roth before age 59.5, even though withdrawals of contributions to Roth accounts can often be made without a penalty.

As stated earlier, investors can and should take advantage of these smaller features of the tax code (e.g., they should harvest capital losses, they should make withdrawals from the taxable stock account using LIFO, etc.). However, we will show that even the larger tax effects we do consider only have a second-order impact on the optimized strategy when compared to the first-order tax effects of the investment strategy. Therefore, it makes little sense to worry about the effect of these smaller aspects of the tax code, since they are third-order effects in the context of this paper.

We assume, as in

Figure 1, that current tax bracket rates will continue to hold and that the bracket limits will continue to be adjusted by inflation, as current tax law requires. Of course tax bracket rates and limits may be changed by subsequent legislation, as we discuss in the conclusions section.

We consider the effect of our taxation model on 10,000 Monte Carlo trials, subject to optimized investments as they evolve chronologically forwards in time. The values of L and maximizing the probability of remaining solvent for these trials are determined using the Nelder–Mead algorithm, with the constraint that . While this constraint is rarely needed, there are cases where the constraint keeps the algorithm from straying and wasting computational time.

6. Conclusions

Both investment optimization and tax optimization are important for retirees, but they have very different mechanisms and implications. Investment optimization is probabilistic in nature, balancing risk and return. Tax optimization is path-dependent and far more deterministic, making choices that have known tax consequences. Investment optimization and tax optimization have generally been performed independently of each other, despite the fact that they affect each other. In this paper we have shown that the effect of investment optimization on the probability that an investor will remain solvent throughout their lifetime is significantly higher than the effect of tax optimization. This means that investment optimization can reasonably be done with little or even no thought to tax optimization, but tax optimization should then be done in the context of this optimized investment strategy. Tax optimization is still important, because the money generated by tax optimization is generally stable and would be foolish to ignore.

This paper presents an investment and tax optimization scheme based on this premise. In the first stage, the algorithm optimizes the investment strategy using dynamic programming in post-tax dollars, which is computed backwards in time. This optimal investment strategy is then incorporated into a second stage that optimizes the tax strategy using Monte Carlo simulation, which evolves forwards in time. The model carefully computes taxes from all typically significant sources of income and capital gains for American investors. It accommodates infusions into TDAs, Roth accounts, and taxable stock and bond accounts, and then it optimizes withdrawal allocations from these accounts to meet consumption needs. The model incorporates Social Security, standard or itemized deductions, and required minimum distributions (RMDs) from the TDA. It also minimizes capital gains taxes by using early non-RMD TDA money for Roth conversions instead of for consumption, so the taxable stock account must be drained earlier to address the investor’s consumption needs.

The sensitivity of the investor’s optimal solvency to variations in a number of parameters is explored, including pre- and post-retirement income, pre- and post-retirement consumption needs, and the initial worth of the TDA. The model may be used to compute the appropriate price for purchasing annuities using either pre-tax or post-tax money. It shows that even under the optimized investment and tax strategy, it is still generally best for unmarried investors to put off collecting Social Security as long as possible.

Of course, this assumes that Social Security payout rules are not changed by legislation in the future, and it assumes that the Social Security Trust Funds do not become depleted, resulting in lowered payouts. As stated in the introduction, for the sake of simplicity we have assumed that the tax structure does not change over time. Of course, the tax structure can and often does change over time. For example,

Croce et al. (

2012) and

Pastor and Veronesi (

2012) studied how tax changes can be triggered by changes to macroeconomic factors. It is difficult to use dynamic programming to study how to optimally invest with potential tax structure changes. This is due to the need both for an accurate stochastic model for how tax parameters, such as tax bracket limits and rates, change in the future and for the additional state space variables needed to accommodate these parameters, which quickly slows the dynamic programming calculation via the so-called “curse of dimensionality” (see

Brown et al. (

2017), however, for a dynamic programming approach over two periods that explores how to best allocate funds between a TDA and a Roth account). Fortunately, our method only uses dynamic programming on a post-tax basis, so it is not subject to these computational problems. Indeed, the Monte Carlo nature of our forwards-in-time tax calculations can easily be extended to accommodate just about any stochastic model for changing tax parameters over time without a change in computational speed. Furthermore, our model is particularly well suited to accommodating models such as

Hassett and Metcalf (

1999), where the distribution for tax parameter changes is correlated to stock returns.

This paper’s model can also be extended in a variety of other different directions. For example, the investor’s consumption needs can be made to depend on both the investor’s wealth and age, instead of just the age as we have in this paper. The dependence on wealth makes intuitive sense since an investor will generally reduce their consumption as their wealth decreases. As another example, the investor’s consumption needs can be made to be stochastic instead of deterministic to reflect any uncertainty that investors have about their future consumption needs. Another optional extension is to consider different investment portfolios in each of the investor’s three accounts to allow further tax optimization. We can also consider how to optimize the probability of being able to make a desired bequest, taking advantage of the fact that capital gains are forgiven at death. As a final example, it is possible to expand the model to married couples in addition to single investors. This requires considering the mortality distribution for the death of either spouse at first, and then the mortality distribution for the surviving spouse, as well as switching from the tax brackets for married couples to those for single individuals after the first spouse dies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}