Intellectual Capital and Knowledge Management Research towards Value Creation. From the Past to the Future

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

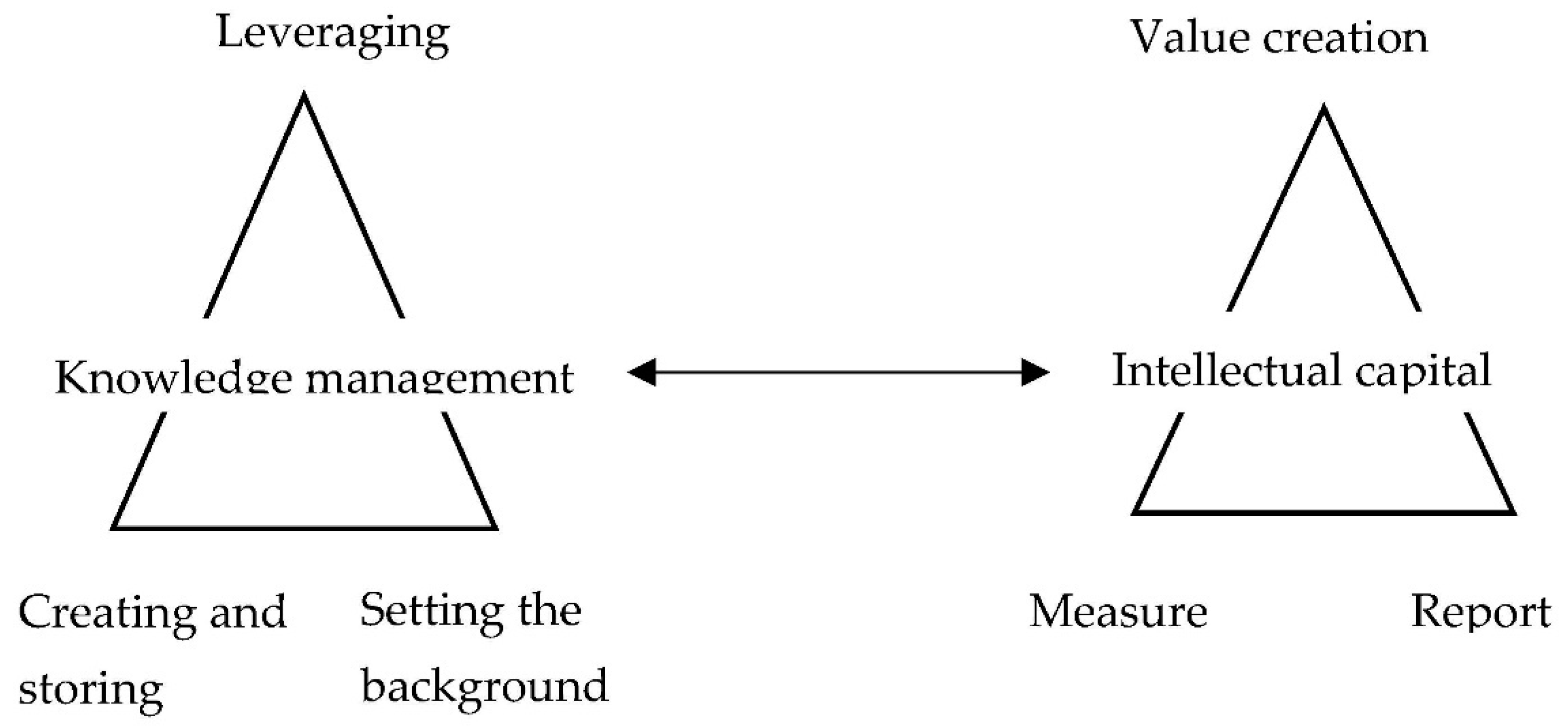

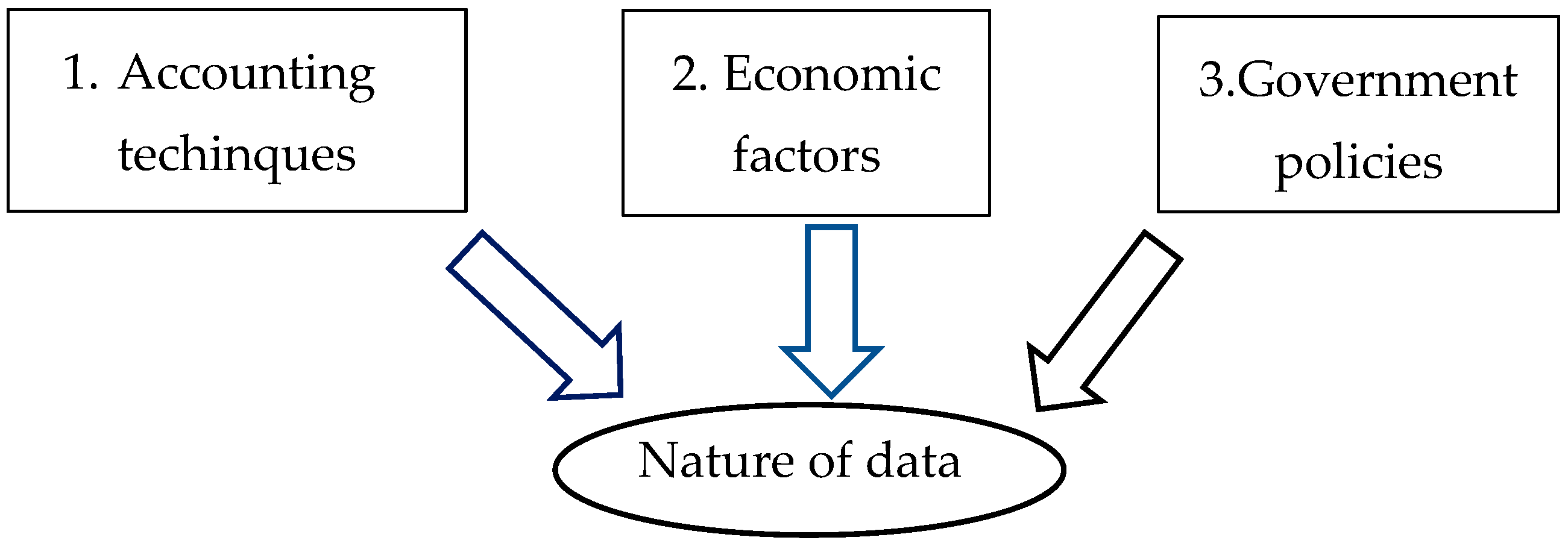

2. Intellectual Capital Measurement and Reporting

2.1. The Impact of Traditional Accounting

2.2. A Few Other Techniques

2.3. Economic Factors

2.4. Government Policies

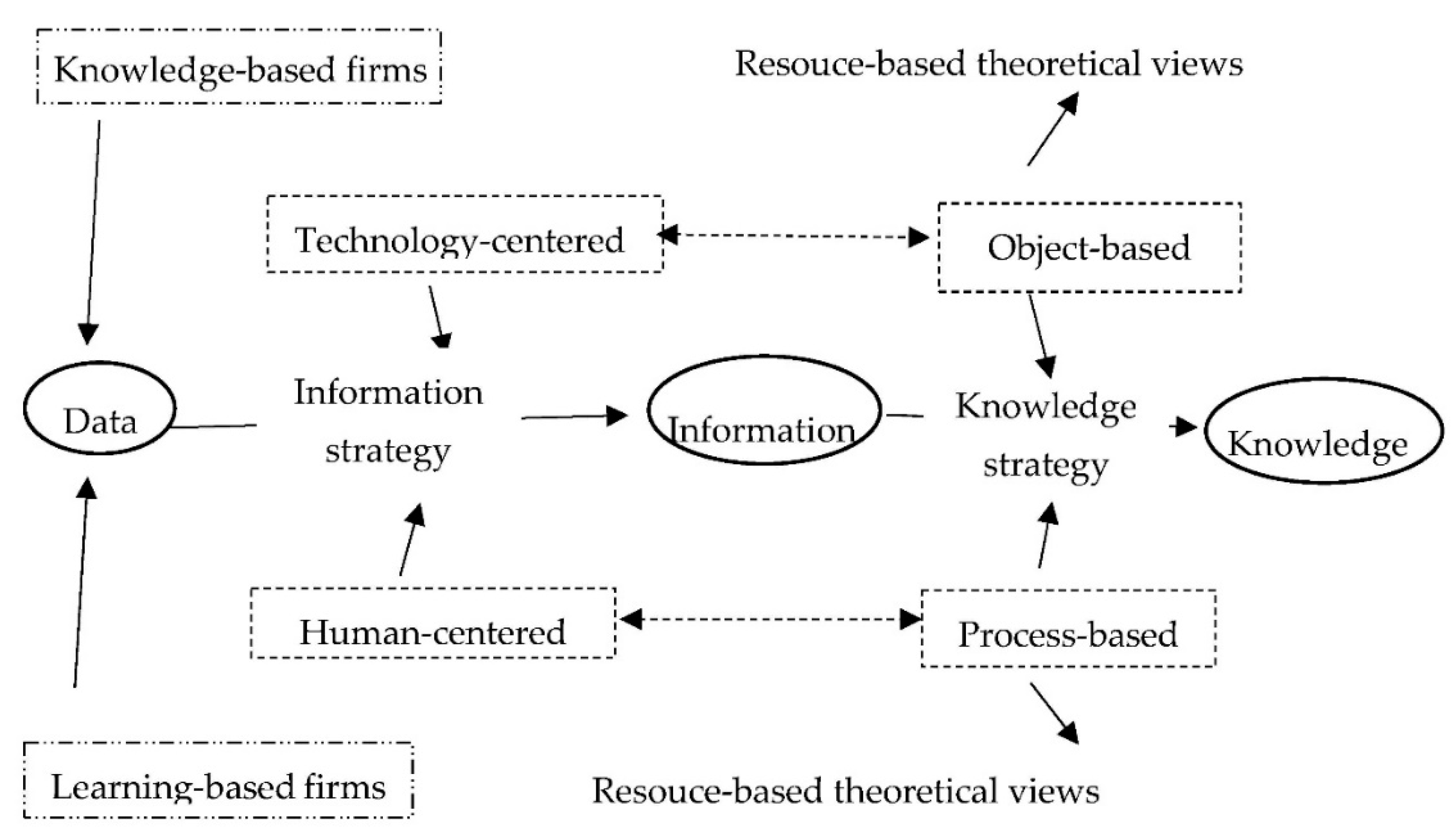

3. Knowledge and Knowledge Management

3.1. Definition of Knowledge

3.2. Knowledge Organization and Learning Organization

3.3. Resource-Based Theory of the Firm

3.4. Frameworks to Manage Knowledge

3.5. Definitions of Knowledge Management

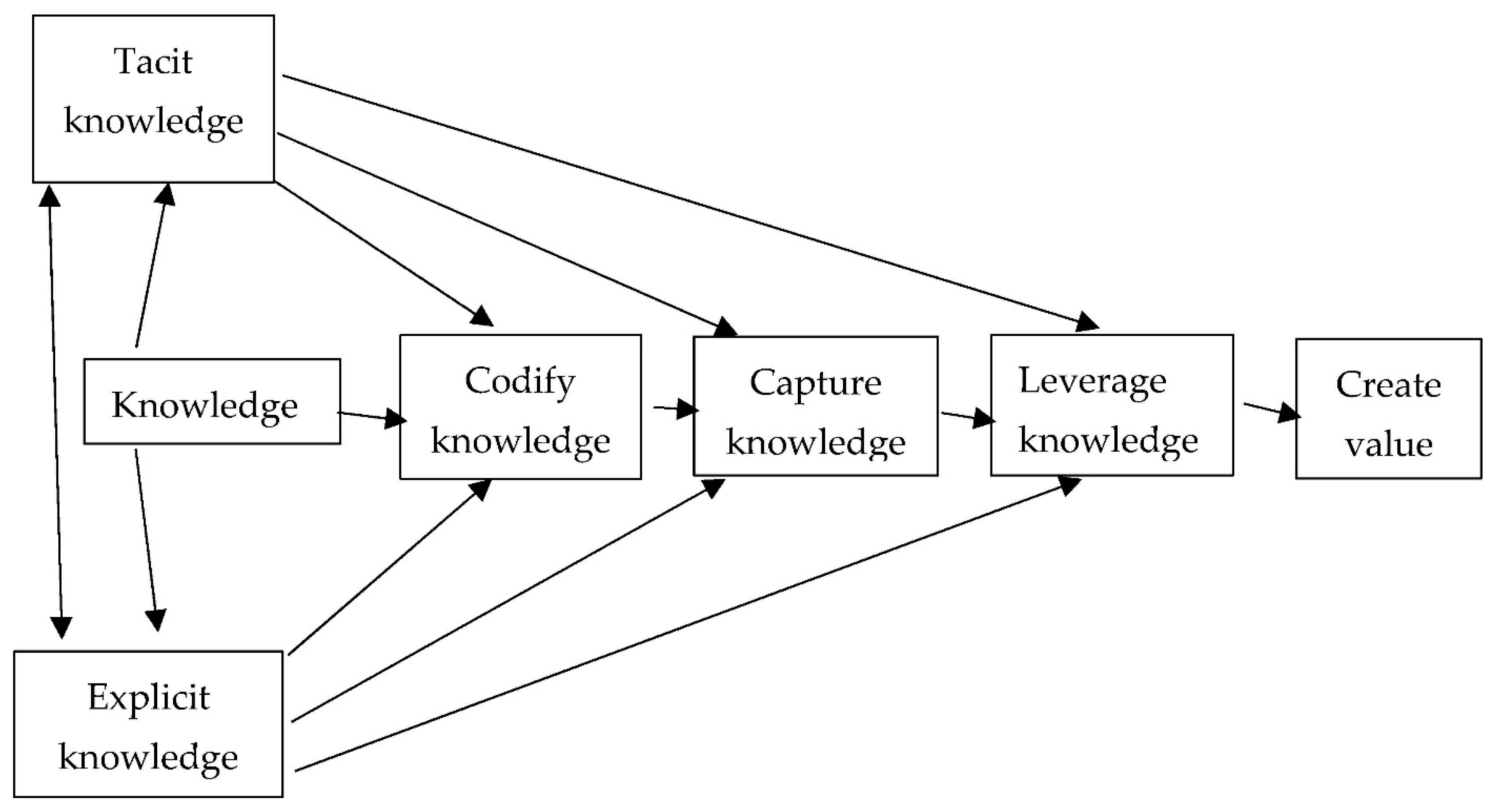

4. Knowledge Capture

4.1. Technology: Expert Systems

4.2. Technology: Databases

4.3. Technology: Web-Based Applications

4.4. Technology: Interactive Online Decisions Support Systems

4.5. Knowledge-Capture Processes

5. Knowledge Transfer

5.1. Role of Information

5.2. Information Strategy

6. Knowledge Leverage

6.1. Knowledge Types

6.2. Knowledge Levels

6.3. Knowledge Leverage Strategies

7. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abeysekera, Indra. 2001a. Intellectual Capital and Knowledge Management: Two Sides of the Same Coin. Economic Review 27: 31–33. [Google Scholar]

- Abeysekera, Indra. 2001b. Leveraging knowledge for short, long term profit. In The Sunday Business Times. Colombo: Wijeya Publications. [Google Scholar]

- Aguirre, Jose Luis, R. Brena, and Francisco J. Cantu-Ortiz. 2001. Multiagent-Based Knowledge Networks. Expert Systems Applications 20: 65–75. [Google Scholar] [CrossRef]

- Ahn, Heinz. 2001. Applying the Balanced Scorecard Concept: An Experience Report. Long Range Planning 34: 441–61. [Google Scholar] [CrossRef]

- Alavi, Mariyam, and DorothyE. Leidner. 2001. Review: Knowledge Management and Knowledge Management Systems: Conceptual Foundations and Research Issues. MIS Quarterly: Management Information Systems 25: 107–36. [Google Scholar] [CrossRef]

- Allen, David. 2001. Hard Currency. Financial Management. Available online: https://www.thefreelibrary.com/Hard+currency.-a078965311 (accessed on 9 April 2021).

- Anthony, Ro N. 1965. Management Accounting Principles. Homewood: Richard D. Irwin Inc. [Google Scholar]

- Armoni, Adi. 1995. Knowledge Acquisition for Medical Diagnosis Systems. Knowledge-Based Systems 8: 223–26. [Google Scholar] [CrossRef]

- Arthur, W. Brian. 1996. Increasing Returns and the New World of Business. Harvard Business Review 74: 100–9. [Google Scholar] [PubMed]

- ASCPA (Australian Society of Certified Practising Accountants). 1999. Members Handbook. Update No. 58. Chatswood: Butterworths Australia, vols. 1, 4. [Google Scholar]

- ASCPA (Australian Society of CPAs), and CMA (The Society of Management Accountants of Canada). 1999. Knowledge Management: Issues, Practice and Innovation. Melbourne: Australian Society of Certified Practising Accountants. [Google Scholar]

- Augier, Mie, and David Teece. 2005. An Economics Perspective on Intellectual Capital. In Perspectives on Intellectual Capital. Edited by Bernard Marr. Alpharetta: Elsevier. [Google Scholar]

- Australian Government. 2021. Participating in the Digital Economy; Department of Industry Sciences, and Industry Resources. Available online: https://www.industry.gov.au/policies-and-initiatives/participating-in-the-digital-economy (accessed on 11 May 2021).

- Backhuijs, J. B., W. G. M. Holterman, S. Holterman, R. P. M. Overgoor, and S. M. Zijlstra. 1999. Reporting on Intangible Assets. Paper presented at the OECD Symposium on Measuring and Reporting of Intellectual Capital, Amsterdam, The Netherlands, June 9–11; Available online: https://www.oecd.org/industry/ind/1947807.pdf (accessed on 9 April 2021).

- Ball, Ray, and Philip Brown. 1968. An Empirical Evaluation of Accounting Numbers. Journal of Accounting Research 6: 159–77. [Google Scholar] [CrossRef]

- Barney, Jay. 1991. Firm Resources and Sustained Competitive Advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Baupin, N., and Khaldoun Zreik. 2000. Remote Decision Support System: A Distributed Information Management System. Knowledge-Based Systems 13: 37–46. [Google Scholar] [CrossRef]

- Benjamin, Alan. 1998. Prototype plc: The 21st Century Annual Report. The 21st Century Annual Report, Corporate Governance. London: Institute of Chartered Accountants of England & Wales. Available online: https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-better-markets/ifbm-reports/new-reporting-models-for-business-2010-version.ashx (accessed on 9 April 2021).

- Bhatt, Ganesh D. 2000. Organizing Knowledge in the Knowledge Development Cycle. Journal of Knowledge Management 4: 15–26. [Google Scholar] [CrossRef]

- Biddle, Gary C., Robert M. Bowen, and James S. Wallace. 1996. Does EVA Beat Earnings? Evidence on Associations with Sock Returns and Firm Values. Journal of Accounting & Economics 24: 301–36. [Google Scholar] [CrossRef]

- Bontis, Nick, Nicola C. Dragonetti, Kristine Jacobsen, and Goran Roos. 1999. A Review of the Tools Available to Measure and Manage Intangible Resources. European Management Journal 17: 391–402. [Google Scholar] [CrossRef]

- Boone, Jeff P., and Krishnamurthy K. Raman. 2001. Off-Balance Sheet R&D Assets and Market Liquidity. Journal of Accounting and Public Policy 20: 97–128. [Google Scholar] [CrossRef]

- Brennan, Naimh. 2001. Reporting Intellectual Capital in Annual Reports: Evidence from Ireland. Accounting, Auditing and Accountability Journal 14: 423–36. [Google Scholar] [CrossRef]

- Bromwich, Michael, and Alnoor Bhimani. 1991. Strategic Investment Appraisal. Management Accounting 72: 45–48. [Google Scholar]

- Brooking, Annie. 1996. Intellectual Capital, Core Assets for the Third Millennium Enterprise. London: International Thomson Business. [Google Scholar]

- Brooking, Annie. 1997. The Management of Intellectual Capital. Long Range Planning 30: 364–65. [Google Scholar] [CrossRef]

- Brown, John Seely, and Paul Duguid. 2000. Balancing Act: How to Capture Knowledge Without Killing It. Harvard Business Review 78: 73–80. [Google Scholar]

- Buhner, Rolf. 1997. Increasing Shareholder Value through Human Asset Management. Long Range Planning 30: 710–17. [Google Scholar] [CrossRef]

- Caddy, Ian, James Guthrie, and Richard Petty. 2001. Managing orphan knowledge: Current Australasian best practice. Journal of Intellectual Capital 2: 384–97. [Google Scholar] [CrossRef]

- Caddy, Ian. 2001. Orphan knowledge: The new challenge for knowledge management. Journal of Intellectual Capital 2: 236–45. [Google Scholar] [CrossRef]

- Centobelli, Piera, Roberto Cerchione, and Emilio Esposito. 2019. Efficiency and Effectiveness of Knowledge Management Systems in SMEs. Production Planning & Control 30: 779–91. [Google Scholar] [CrossRef]

- Chapman, Christopher S. 1997. Reflections on a contingent view of accounting. Accounting, Organizations and Society 22: 189–205. [Google Scholar] [CrossRef]

- Chisholm, Roderick M. 1966. Theory of Knowledge. Hoboken: Prentice Hall Inc. [Google Scholar]

- Collier, Paul M. 2001. Valuing Intellectual Capacity in the Police. Accounting, Auditing & Accountability Journal 14: 437–55. [Google Scholar]

- Conner, Kathleen R., and Coimbatore Krishnarao. Prahalad. 1996. A Resource-Based Theory of the Firm: Knowledge versus Opportunism. Organization Science 7: 477–501. [Google Scholar] [CrossRef]

- Copeland, Tom. 2000. Cutting Costs without Drawing Blood. Harvard Business Review 78: 155–64. [Google Scholar] [PubMed]

- Count, Aw W. 1998. Issues for Integrating Knowledge in New Product Development: Reflections from an Empirical Study. Knowledge Based Systems 11: 391–98. [Google Scholar] [CrossRef]

- Davenport, Thomas H. 1994. Saving IT Soul: Human-Centred Information Management. Harvard Business Review 72: 119–31. [Google Scholar]

- Davenport, Thomas H., and Laurence Prusak. 1998. Working Knowledge, How Organizations Manage What They Know. Boston: Harvard Business School Press. [Google Scholar]

- Davenport, Thomas H., David W. De Long, and Michael C. Beers. 1998. Successful Knowledge Management Projects. Sloan Management Review 39: 43–57. [Google Scholar]

- Davenport, Thomas H., Robert G. Eccles, and Laurence Prusak. 1992. Information Politics. Sloan Management Review 15: 53–65. Available online: https://sloanreview.mit.edu/article/information-politics/ (accessed on 10 April 2021).

- Davies, Jan, and Alan Waddington. 1999. The Management and Measurement of Intellectual Capital. Management Accounting 77: 34. [Google Scholar]

- Dearden, John. 1960. Problem in Decentralized Profit Responsibility. Harvard Business Review 38: 79–86. [Google Scholar]

- Dekker, Rijkje, and Robert de Hoog. 2000. The Monetary Value of Knowledge Assets: A Micro Approach. Expert Systems with Applications 18: 111–24. [Google Scholar] [CrossRef]

- Demarest, Marc. 1997. Understanding Knowledge Management. Long Range Planning 30: 374–84. [Google Scholar] [CrossRef]

- Demirbag, Mehmet, and Hafiz Mirza. 2000. Factors Affecting International Joint Venture Success: An Empirical Analysis of Foreign-Local Partner Relationships and Performance in Joint Venture in Turkey. International Business Review 9: 1–35. [Google Scholar] [CrossRef]

- Devedzic, Vladan. 1999. A Survey of Modern Knowledge Modeling Techniques. Expert Systems with Applications 17: 275–94. [Google Scholar] [CrossRef]

- Dewett, Todd, and Gareth R. Jones. 2001. The Role of Information Technology in the Organisation: A Review, Model, and Assessment. Journal of Management 27: 313–46. [Google Scholar] [CrossRef]

- Dunk, Alan S., and Alan Kilgore. 2001. Short-Term R&D Bias, Competition on Cost Rather Than Innovation, and Time to Market. Scandinavian Journal of Management 17: 409–20. [Google Scholar] [CrossRef]

- Edvinsson, Leif, and Patrick Sullivan. 1996. Developing a Model for Managing Intellectual Capital. European Management Journal 14: 356–64. [Google Scholar] [CrossRef]

- Fernandez-Breis, Jesualdo Tomas, and Rodrigo Martinez-Bejar. 2000. A Cooperative Tool for Facilitating Knowledge Management. Expert Systems with Applications 18: 315–30. [Google Scholar] [CrossRef]

- Galbraith, Jay R. 1977. Organization Design. Philippines: Addison-Wesley Publishing, Inc. [Google Scholar]

- Gavin, David A. 1993. Building a Learning Organization. Harvard Business Review 71: 78–91. [Google Scholar]

- Gelinas, Ulric J., Jr., Richard B. Dull, and Patrick R. Wheeler. 2018. Accounting Information Systems, 11th ed. Victoria: Cengage Learning Australia. [Google Scholar]

- Goleman, Daniel. 1995. Emotional Intelligence. New York: Bantam Books. [Google Scholar]

- Graham, Roger C., and Raymond D. King. 2000. Accounting Practices and the Market Valuation of Accounting Numbers: Evidence from Indonesia, Korea, Malaysia, the Philippines, Taiwan, and Thailand. The International Journal of Accounting 35: 445–70. [Google Scholar] [CrossRef]

- Grant, Robert M. 1996. Towards a Knowledge-Based Theory of the Firm. Strategic Management Journal 17: 109–22. [Google Scholar] [CrossRef]

- Guthrie, James, and Richard Petty. 2000. Intellectual capital: Australian annual reporting practices. Journal of Intellectual Capital 1: 241–51. [Google Scholar] [CrossRef]

- Hansen, Morten T., N. Nitin Nohria, and Thomas J. Tierney. 1999. What’s Your Strategy for Managing Knowledge. Harvard Business Review 77: 106–16. [Google Scholar]

- Hansson, Bo. 1997. Personnel Investments and Abnormal Return: Knowledge-Based Firms and Human Resource Accounting. Journal of Human Resource Costing and Accounting 2: 9–29. [Google Scholar] [CrossRef]

- Heckmian, James S., and Curtis H. Jones. 1967. Put People on Your Balance Sheet. Harvard Business Review 45: 105–13. [Google Scholar]

- Hoegh-Krohn, Nils E. Joachim, and Kjel Henry Knivsfla. 2000. Accounting for Intangible Assets in Scandinavia, the UK, the US, and by the IASC: Challenges and a Solution. The International Journal of Accounting 35: 243–65. [Google Scholar] [CrossRef]

- Holsapple, Clyde W., and Meenu Singh. 2001. The Knowledge Chain Model: Activities for Competitiveness. Expert Systems with Applications 20: 77–98. [Google Scholar] [CrossRef]

- Hori, K. 2000. An Ontology of Strategic Knowledge: Key Concepts and Applications. Knowledge-Based Systems 13: 369–74. [Google Scholar] [CrossRef]

- Huseman, Richard C., and Jon P. Goodman. 1999. Leading with Knowledge. The Nature of Competition in the 21st Century. Thousand Oaks: Sage. [Google Scholar]

- IAS38 (International Financial Reporting Standards 38). 2021. Intangible Assets. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-38-intangible-assets/#about (accessed on 27 May 2021).

- Jordan, Jordan, and Penelope Jones. 1997. Assessing Your Company’s Knowledge Management Style. Long Range Planning 30: 392–98. [Google Scholar] [CrossRef]

- Kaplan, Robert S., and David P. Norton. 1992. The Balanced Scorecard-Measures That Drive Performance. Harvard Business Review 70: 71–79. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 1993. Putting the Balanced Scorecard to Work. Harvard Business Review 71: 134–47. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 1996. Using the Balanced Scorecard as a Strategic Management System. Harvard Business Review 74: 75–85. [Google Scholar]

- Kinsella, Ray, and Vincent McBrierty. 1997. Campus Companies and the Emerging Techno-Academic Paradigm: The Irish Experience. Technovation 17: 245–51. [Google Scholar] [CrossRef]

- Krackhardt, David, and Jeffrey R. Hanson. 1993. Informed Networks: The Company Behind the Chart. Harvard Business Review 71: 104–11. [Google Scholar] [PubMed]

- Lehrer, Keith. 1990. Theory of Knowledge. Boulder: Westview Press Inc. [Google Scholar]

- Lennon, Alexia, and Andrew Wollin. 2001. Learning Organizations: Empirically Investigating Metaphors. Journal of Intellectual Capital 2: 410–22. [Google Scholar] [CrossRef]

- Liebowitz, Jay. 2001a. Knowledge Management and Its Link to Artificial Intelligence. Expert Systems with Applications 20: 1–6. [Google Scholar] [CrossRef]

- Liebowitz, Jay. 2001b. If You Are a Dog Lover, Build Expert Systems; If You Are a Cat Lover, Build Neural Networks. Expert Systems with Applications 21: 63. [Google Scholar] [CrossRef]

- Linowes, Richard G., Tomasz Mroczkowski, Keikio Uchida, and Akira Komatsu. 2000. Using Mental Maps to Highlight Cultural Differences, Visual Portraits of American and Japanese Patterns of Thinking. Journal of International Management 6: 71–100. [Google Scholar] [CrossRef]

- Malhotra, Yogesh. 2000. Knowledge Management for the New World of Business. Available online: http://www.brint.com/km/whatis.htm (accessed on 10 April 2021).

- Malhotra, Yogesh. 2001. Expert Systems for Knowledge Management: Crossing the Chasm Between Information Processing and Sense Making. Expert Systems with Applications 20: 7–16. [Google Scholar] [CrossRef]

- Martensson, Maria. 2000. A Critical Review of Knowledge Management as a Management Tool. Journal of Knowledge Management 4: 204–16. [Google Scholar] [CrossRef]

- Martinez, Michelle Neely. 1998. The Collective Power of Employee Knowledge. HR Magazine 43: 88–94. [Google Scholar]

- Mayo, Andrew, and Elizabeth Lank. 1994. The Power of Learning, A Guide to Gaining Competitive Advantage. London: Institute of Personnel and Development. [Google Scholar]

- Medsker, Larry, Margaret Tan, and Efraim Turban. 1995. Knowledge Acquisition from Multiple Experts: Problems and Issues. Expert Systems with Applications 9: 35–40. [Google Scholar] [CrossRef]

- Morton, Adam. 2002. A Guide through the Theory of Knowledge. Hoboken: John Wiley & Sons. [Google Scholar]

- Mouck, Tom. 1998. Capital Markets Research and Real World Complexity: The Emerging Challenge of Chaos Theory. Accounting, Organizations and Society 23: 189–215. [Google Scholar] [CrossRef]

- Mouritsen, Jan. 1998. Driving Growth: Economic Value Added versus Intellectual Capital. Management Accounting Research 9: 461–82. [Google Scholar] [CrossRef]

- Narula, Rajneesh, and John H. Dunning. 1998. Explaining International R&D Alliances and the Role of Governments. International Business Review 7: 377–97. [Google Scholar] [CrossRef][Green Version]

- Noh, Jermim B., Kunchang C. Lee, Jae-kyeong Kim, Jae-kwang Lee, and Sounghie H. Kim. 2000. A Case-Based Reasoning Approach to Cognitive Map-Driven Tacit Knowledge Management. Expert Systems with Applications 19: 249–59. [Google Scholar] [CrossRef]

- Nonaka, Ikujiro, Ryoko Toyama, and Noboru Konno. 2000. SECI, Ba and Leadership: A Unified Model of Dynamic Knowledge Creation. Long Range Planning 33: 5–34. [Google Scholar] [CrossRef]

- Nonaka, kujiro. 1991. The Knowledge-Creating Company. Harvard Business Review 6: 96–111. [Google Scholar]

- Nonaka, Kujiro. 1994. A Dynamic Theory of Organizational Knowledge Creation. Organization Science 5: 14–37. [Google Scholar] [CrossRef]

- Ntuen, Celestine A., and Jacqueline A. Chestnut. 1995. An Expert System for Selecting Manufacturing Workers for Training. Expert Systems with Applications 9: 309–32. [Google Scholar] [CrossRef]

- Ohsuga, Setsuo. 1995. A Way of Designing Knowledge Based Systems. Knowledge-Based Systems 8: 211–22. [Google Scholar] [CrossRef]

- Parker, Lee D. 2000. Goodbye, Number Cruncher. Australian CPA 70: 50–52. Available online: https://www.scirp.org/(S(i43dyn45teexjx455qlt3d2q))/reference/ReferencesPapers.aspx?ReferenceID=2250484 (accessed on 10 April 2021).

- Petty, Richard, and James Guthrie. 2000. The Case for Reporting on Intellectual Capital: Evidence, Analysis and Future Trends. In The Current State of Business Disciplines, Volume 1, Accounting. Edited by Shri Bhagwan Dahiya. Rohtak: Spellbound Publications. [Google Scholar]

- Power, Michael. 2001. Imagining, Measuring and Managing Intangibles. Accounting, Organizations and Society 26: 691–93. [Google Scholar] [CrossRef]

- Quintas, Paul, Paul Lefrere, and Geoff Jones. 1997. Knowledge Management: A Strategic Agenda. Long Range Planning 30: 385–91. [Google Scholar] [CrossRef]

- Ragothaman, Srinivasan, Jon Carpenter, and Thomas Buttars. 1995. Using Rule Induction for Knowledge Acquisition: An Expert Systems Approach to Evaluating Material Errors and Irregularities. Expert Systems with Applications 9: 483–90. [Google Scholar] [CrossRef]

- Richards, Ian, David Foster, and Ruth Morgan. 1998. Brand Knowledge Management: Growing Brand Equity. Journal of Knowledge Management 2: 47–54. [Google Scholar] [CrossRef]

- Romer, Paul M. 1998a. Bank of America Roundtable on the Soft Revolution: Achieving Growth by Managing Intangibles. Journal of Applied Corporate Finance 11: 8–27. [Google Scholar] [CrossRef]

- Romer, Paul M. 1998b. Two Strategies for Economic Development: Using Ideas and Producing Ideas. In The Strategic Management of Intellectual Capital. Edited by David A. Klein. Woburn: Butterworth-Heinemann. [Google Scholar]

- Ronen, Joshua. 2001. On R&D Capitalization and Value Relevance: A Commentary. Journal of Accounting and Public Policy 20: 241–54. [Google Scholar] [CrossRef]

- Roos, Goran, and Johan Roos. 1997. Measuring Your Company’s Intellectual Performance. Long Range Planning 30: 413–26. [Google Scholar] [CrossRef]

- Roos, Johan, Leif Edvinsson, and Nicola C Dragonetti. 1997. Intellectual Capital, Navigating the New Business Landscape. London: Macmillan Business. [Google Scholar]

- Roos, Johan. 1998. Exploring the Concept of Intellectual Capital (IC). Long Range Planning 31: 150–53. [Google Scholar] [CrossRef]

- Rose, Jacob M., and Christopher J. Wolfe. 2000. The Effects of System Design Alternatives on the Acquisition of Tax Knowledge from a Conceptualized Tax Decision Aid. Accounting, Organizations and Society 25: 285–306. [Google Scholar] [CrossRef]

- Rowley, Jennifer. 1999. What Is Knowledge Management? Library Management 20: 416–19. [Google Scholar] [CrossRef]

- Sadler-Smith, Eugene, David P. Spicer, and Ian Chaston. 2001. Learning Orientations and Growth in Smaller Firms. Long Range Planning 34: 139–58. [Google Scholar] [CrossRef]

- Schaefer, Mary. 1998. Eight Things Communicators Should Know and Do About Knowledge Management. Communication World 15: 26. [Google Scholar]

- Senge, Peter M. 1990. The Fifth Discipline: The Art and Practice of the Learning Organisation. New York: Doubleday. [Google Scholar]

- Stalk, George, Jr., Philip Evans, and Lawrence E. Shulman. 1992. Competing on Capabilities: The New Rules of Corporate Strategy. Harvard Business Review 2: 57–69. [Google Scholar]

- Stolowy, Harve, and Anne Jenny-Cazavan. 2001. International Accounting Disharmony: The Case of Intangibles. Accounting, Auditing & Accountability Journal 14: 477–96. [Google Scholar] [CrossRef]

- Stonehouse, George H., Jonathan D. Pemberton, and Claire E. Barber. 2001. The Role of Knowledge Facilitators and Inhibitors: Lessons from Airline Reservations Systems. Long Range Planning 34: 115–38. [Google Scholar] [CrossRef]

- Studer, Rudi, V. Richard Benjamins, and Deter Fensel. 1998. Knowledge Engineering: Principles and methods. Data & Knowledge Engineering 25: 161–97. [Google Scholar] [CrossRef]

- Sveiby, Karl Erik. 1997. The New Organizational Wealth, Managing & Measuring Knowledge Based Assets, 5th ed. San Francisco: Barrett-Koehler. [Google Scholar]

- Sveiby, Karl Erik. 1998. Measuring Intangibles and Intellectual Capital: An Emerging First Standard. Available online: https://www.sveiby.com/archives/articles/1998 (accessed on 11 April 2021).

- Taylor, W. Andrew, D. H. Weimann, and Peter J. Martin. 1995. Knowledge Acquisition and Synthesis in a Multiple Source Multiple Domain Process Context. Expert Systems with Applications 8: 295–302. [Google Scholar] [CrossRef]

- Teece, David J. 2000. Strategies for Managing Knowledge Assets: The Role of Firm Structure and Industrial Context. Long Range Planning 33: 35–54. [Google Scholar] [CrossRef]

- Teegen, Hildy. 2000. Examining Strategic and Economic Development Implications of Globalising Through Franchising. International Business Review 9: 497–521. [Google Scholar] [CrossRef]

- The Economist Intelligence Unit. 1998. Knowledge Workers Revealed, New Challenges for Asia. Researched and Written with Andersen Consulting. Hong Kong: The Economist Intelligence Unit. [Google Scholar]

- Thompson, Kevin. 1999. Emotional Capital. Oxford: Capstone Publishing. [Google Scholar]

- Tissen, Rene, Daniel Andriessen, and Frank Lopez. 2000. The Knowledge Dividend, Creating High-Performance Companies through Value-Based Knowledge Management. Harlow: Pearson Education. [Google Scholar]

- Tollington, Tony. 2001. UK Brand Asset Recognition Beyond “Transactions or Events”. Long Range Planning 34: 463–87. [Google Scholar] [CrossRef]

- Van der Meer-Kooistra, Jeltje, and Siebre M. Zijlstra. 2001. Reporting on Intellectual Capital. Accounting, Auditing & Accountability Journal 14: 456–76. [Google Scholar]

- Van Wegen, Bert, and Robert de Hoog. 1999. Impacts of Knowledge Based Systems: Beyond Anecdotes and Checklists. Expert Systems with Applications 16: 197–219. [Google Scholar] [CrossRef]

- Vanoirbeek, Christine, Yassine Aziz Rekik, Nikos Karacapilidis, Omar. Abou Khaled, Norbert Ebel, and John-Paul Vader. 2000. A Web-Based Information and Decision Support System for Appropriateness in Medicine. Knowledge-Based Systems 13: 11–19. Available online: https://dl.acm.org/doi/abs/10.1016/S0950-7051(99)00052-0 (accessed on 11 April 2021). [CrossRef]

- Von Krogh, Gorg, Ikujiro Nonaka, and Manfred Aben. 2001. Making the Most of Your Company’s Knowledge: A Strategic Framework. Long Range Planning 34: 421–39. [Google Scholar] [CrossRef]

- Walczak, Steven. 1998. Knowledge Acquisition and Knowledge Representation with Class: The Object-Oriented Paradigm. Expert Systems with Applications 15: 235–44. [Google Scholar] [CrossRef]

- Wallace, James S. 1996. Adopting Residual Income-Based Compensation Plans: Do You Get What You Pay For? Journal of Accounting & Economics 24: 275–300. [Google Scholar] [CrossRef]

- Welbourne, Michael. 2014. Knowledge. New York: Routledge. [Google Scholar]

- Wiig, Karl M. 1993. Knowledge Management Foundations: Thinking About Thinking: How People and Organizations Represent, Create and Use Knowledge. Arlington: Knowledge Research Institute, Schema Press. [Google Scholar]

- Wiig, Karl M. 1997. Knowledge Management: Where Did It Come from and Where Will It Go? Expert Systems with Applications 13: 1–14. [Google Scholar] [CrossRef]

- Wiig, Karl M., Robert De Hoog, and Rob Van der Spek. 1997. Supporting Knowledge Management: A Selection of Methods and Techniques. Expert Systems with Applications 13: 15–27. [Google Scholar] [CrossRef]

- Wong, Kuan Yew, and Elaine Aspinwall. 2005. An Empirical Study of the Important Factors for Knowledge-Management Adoption in the SME Sector. Journal of Knowledge Management 9: 64–82. [Google Scholar] [CrossRef]

- Wooten, Thomas C., and Thomas H. Rowley. 1995. Using Anthropological Interview Strategies to Enhance Knowledge Acquisition. Expert Systems with Applications 9: 469–82. [Google Scholar] [CrossRef]

- Young, David. 1997. Economic Value Added: A Primer for European Managers. European Management Journal 15: 335–43. [Google Scholar] [CrossRef]

- Zambon, Stephano, and Luca Zan. 2000. Accounting Relativism: The Unstable Relationship Between Income Measurement and Theories of the Firm. Accounting, Organizations and Society 25: 799–822. [Google Scholar] [CrossRef]

Short Biography of the Author

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abeysekera, I. Intellectual Capital and Knowledge Management Research towards Value Creation. From the Past to the Future. J. Risk Financial Manag. 2021, 14, 238. https://doi.org/10.3390/jrfm14060238

Abeysekera I. Intellectual Capital and Knowledge Management Research towards Value Creation. From the Past to the Future. Journal of Risk and Financial Management. 2021; 14(6):238. https://doi.org/10.3390/jrfm14060238

Chicago/Turabian StyleAbeysekera, Indra. 2021. "Intellectual Capital and Knowledge Management Research towards Value Creation. From the Past to the Future" Journal of Risk and Financial Management 14, no. 6: 238. https://doi.org/10.3390/jrfm14060238

APA StyleAbeysekera, I. (2021). Intellectual Capital and Knowledge Management Research towards Value Creation. From the Past to the Future. Journal of Risk and Financial Management, 14(6), 238. https://doi.org/10.3390/jrfm14060238