1. Introduction

The Middle East and North Africa region is currently witnessing changes toward the deal of the century. It is promoted by Israel’s normalization with many Arab countries such as the United Arab Emirates, Bahrain, Sudan, Qatar, and Morocco (and probably Saudi Arabia and Oman). Despite the historical maritime border talks between Lebanon and Israel that have started in October 2020 (and still ongoing), its success is not guaranteed. In fact, it is extremely challenging to predict geopolitical changes in Lebanon under Hezbollah’s domination.

1.1. Hezbollah, Israel, and Saudi Arabia: Geopolitical Background

Founded in 1982 by Iran, Hezbollah’s—the Islamic resistance army—mission was exclusively to liberate the Israeli occupation of southern Lebanon. Paradoxically, in May 2000, when the Israeli military army withdrew from Lebanon, Hezbollah “theoretically” lost the legitimacy to keep its weapons (

UNSCOL [2004] 2006). For that, Hezbollah had to wear many hats, all under the resistance umbrella: it positioned itself as a resistant militia (1) to defend the Palestinian cause against Israel, (2) to protect southern Lebanon from future Israeli attacks, and (3) to weaken Saudi Arabia’s regional influence for ideological rivalry. Regardless of its declared resistance agenda, Hezbollah is nothing but Iran’s proxy that behaves at its behest (

DeVore 2012;

Seliktar and Rezaei 2020) to gain geopolitical-strategic depth in the region.

Since ideology, civilization, religion, and geopolitics appear complementary (

Kuçi 2020;

Sheikh 2003). Hezbollah had to accumulate an array of sophisticated armaments, rockets, and weapons. It has also expanded tens of thousands of trained fighters in order to spread ideological—

Welayat Al-Faqih—ethnic grounds far and wide (

Salamey and Othman 2011;

Al-Aloosy 2020) no matter the devastation caused, as long as it increases the Persian footprint (

Haddad 2006;

Jones 2019). Yemen, Iraq, and Syria are testimonies of the poverty, starvation, corruption, and terrorism caused by Hezbollah’s invasion under different military group names to control territory, natural resources, or other important geographical positions or places (

Friedman 2018).

Being heavily armed, Hezbollah could successfully become deeply embedded within the sociopolitical structures of Lebanon may (

May 2020;

Wiegand 2009) or more precisely, it becomes the de facto policy decision-maker (

Worrall et al. 2015;

Norton 2007). For instance, in May 2008, because the Lebanese government decided to dismantle Hezbollah’s military communications network, Hezbollah turned its weapons inward toward Beirut (the capital of Lebanon), against pro-government civil people and gunmen. They killed 18 people and injured 38 in three days of battles before the government gave up.

1.2. Lebanon and Hezbollah: From the Best of Friends to the Best of Enemies

Hezbollah’s domination is not limited to affecting the Lebanese sovereignty, but it also has a deleterious effect socially, economically, and globally. In fact, Hezbollah abuses its military and political “superpowers” to violate Lebanese laws, human rights, and even international laws such as United Nations Security Council Resolutions 1559 and 1701 (

UNSCOL [2004] 2006). Moreover, it announces explicitly through official speeches that it has proud recourse to illegal and criminal activities: corruption, bribery, financial transaction, money laundering, and tax evasion that has exceeded 10 percent of GDP in 2017 (

Blom-Bank 2017), with a Tax Evasion Index of 0.69, as estimated by

Vo et al. (

2020). Additionally, Hezbollah is the leader in smuggling, human trafficking, and production and trafficking of drugs (

Badran and Ottolenghi 2020). With that being said, Hezbollah has earned, with merit, its listing as a terrorist organization/military wing by more than 65 countries government (

United.States.Government 2019,

2021). Expectedly, Lebanese politicians and institutions are continually undergoing US sanctions from The Global Magnitsky Human Rights Accountability and the Office of Foreign Assets Control accused of having contributed, directly or indirectly, to Hezbollah’s illegal activities.

1.3. Research Question and Hypothesis

The consequences of Hezbollah’s underground activities and geopolitical tensions are bore by Lebanon (the country). It would be valuable to assess empirically the impact of Saudi Arabian and Israeli geopolitical threats with Hezbollah on the Lebanese financial market. It goes back to 1997 when

Schrodt (

1997) tried to create an early warning indicator of geopolitical risks between Israel and Hezbollah (in the south of Lebanon) to forecast future conflict and to help policymakers avoid financial crises. However, his study lacks precision due to data limitations.

Although the literature is abundant in political science regarding Lebanese geopolitics, it remains rare, if not inexistant, in economics and econometrics. Instead, studies are rather press releases, newspaper articles, or economic reports elaborated by the United Nations, Reuters, the World Bank, or other international organizations. These publications are somehow descriptive and merely limited to estimating the cost of reconstruction (after a war) or to exposing in value the costs and losses of geopolitical conflicts on education, welfare, agriculture, and employment.

This paper aims to investigate empirically—on a monthly basis, from June 2000 (after Lebanon deliberation) to November 2018—the dynamic causality-independence between geopolitical risks of Israel and Saudi Arabia (towards Hezbollah) and the Lebanese financial market.

This study employs Granger causality tests under vector autoregression (VAR) models, followed by first—orthogonalize—Cholesky decomposition–impulse response functions and variance decomposition of variables to detect the dynamic relations between Israeli and Saudi Arabian geopolitical risks with the Lebanese financial market and economic activity.

This study aims to achieve one of two possible conclusions:

If the Lebanese financial market shows independency or low dependency–causality to the regional geopolitical risks, then Hezbollah’s geopolitical tensions with Israel and Saudi Arabia do not seem to negatively affect the Lebanese financial stability. Consequently, economic reforms, monetary and fiscal policies, as well as internal legal reforms can be improved independently from the geopolitical, international, and diplomatic arrangements.

If the Lebanese financial market shows significant dependency–causality to the regional geopolitical risks, then Hezbollah’s tensions with Israel and Saudi Arabia trigger the Lebanese financial stability and economic activity. Therefore, instead of solving the Lebanese economic crisis from a purely economic perspective, measures towards negotiation and conflict resolution with the neighborhood are needed, which require de-Hezbollizing Lebanon.

One would find it evident that geopolitical risks negatively affect the financial stability and economic activity; however, the literature shows different conclusions depending on the country’s category, income level, and even polity.

The remainder of the paper is structured as follows:

Section 2 includes a literature review.

Section 3 describes the data and statistical tests.

Section 4 illustrates the graphical analysis with preliminary deductions.

Section 5 exposes the methodology.

Section 6 interprets and discusses results and findings.

Section 7 closes with a conclusion and recommendations.

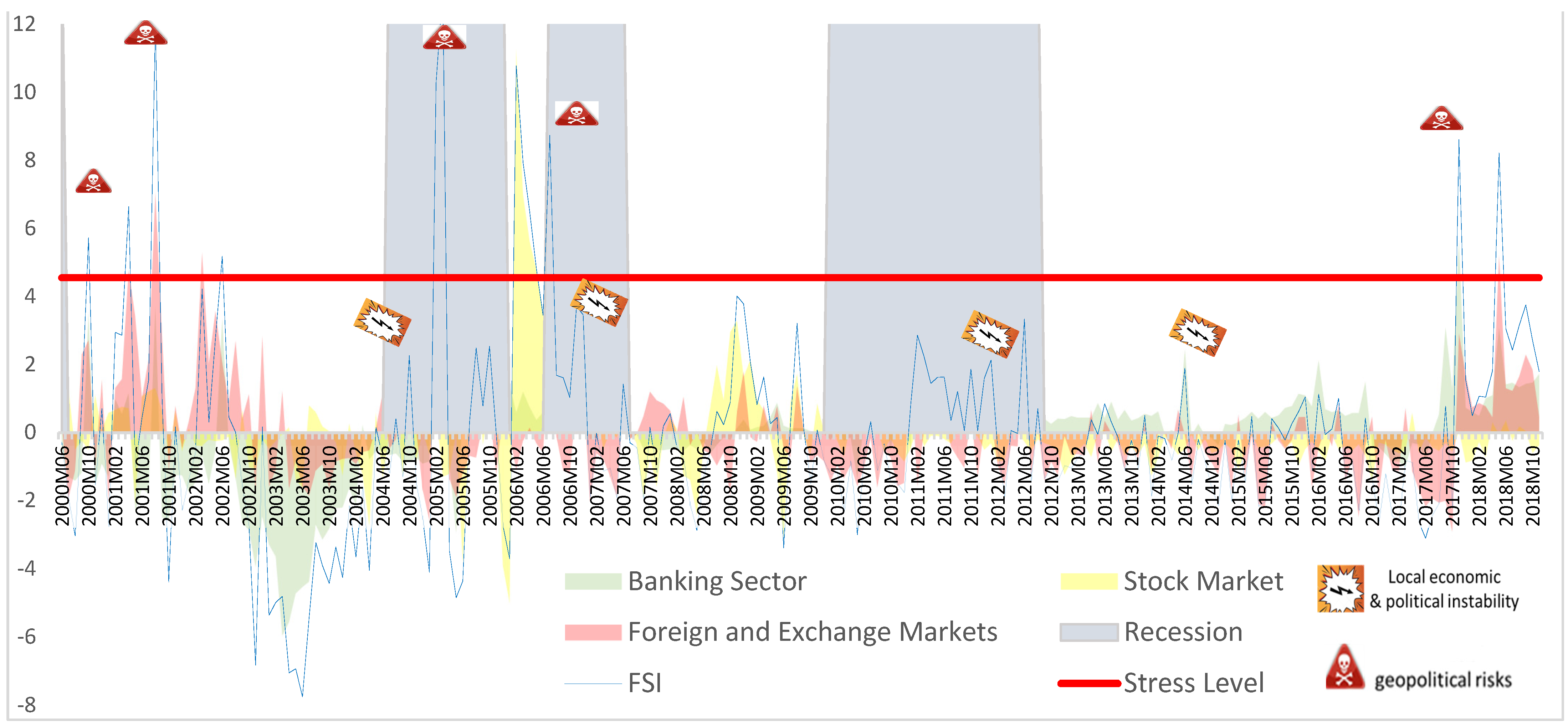

4. Graphical Analysis and Preliminary Deductions

It appears common that the aforementioned authors interpret graphically the FSI spikes with the business cycle before proceeding with empirical models. FSI fluctuations are represented in

Figure 2. Recession periods are reported in the shaded areas.

High fluctuations that are reported in positive values indicate stressful periods/financial crises, while low fluctuations reported in negative values indicate low stress periods. The stress level is represented by 1.5 times the standard deviation of the FSI.

Graphical analysis shows that most of the economic and political trouble trigger FSI at a low level (below the stress level). They are mainly triggered by credit rating downgrading (in May 2008, February 2011, May 2012, November 2013, December 2014, and September 2015); by the central bank’s interventions through financial engineering (in May and August 2016 and in September 2017); or by internal political trouble such as conflict between political parties, government members’ resignation (January 2011, February 2015), or election delays (2014–2016).

On the other hand, most FSI high spikes that surpass the stress level seem to be associated with regional geopolitical threats. For instance, the dates April and October 2000, April 2001, and July 2006 detect tensions with Israel. In July 2006, few years after the Israel-Lebanon ceasefire, Lebanon faced a one-month-destructive war with Israel. Nevertheless, Israel responded to Hezbollah attacks (

Sharp et al. 2006) rather than attacking Lebanon. It is stated in

Schmitt (

2007) that “

Israel did not attack the government of Lebanon, but rather Hizbullah military assets within Lebanon”.

The two most severe financial crises with the highest spike levels were hit in February 2005 when the Lebanese prime minister named Hariri was assassinated and in November 2017 when the Lebanese prime minister, Hariri Junior, was detained in Saudi Arabia and was forced to resign. In appearance, these dates seem to be caused by internal political trouble. In reality, the Hezbollah is in the details: In October 2020, the Special Tribunal for Lebanon-United Nations Security council resolution 1757 declared that the prime minister was assassinated in February 2005 by a terrorist attack from a member of Hezbollah. Similarly, in November 2017, Saudi Arabia detained the prime minister as an expression of its disagreement toward Hariri Junior’s cooperation with the Hezbollah political party.

The graphical analysis presumes that high FSI spikes are related to the regional geopolitical tensions with Hezbollah whereas local political or economic pressures are not. Similarly, it appears that most of the recession periods overlap positive high FSI spikes. Nevertheless, empirical tests are crucial to verify the preliminary deductions.

5. Methodology

VAR is a natural framework for examining Granger causality, commonly employed by macroeconomists to characterize the joint dynamic behavior of variables such as geopolitical risks with other macroeconomic variables. Similarly, Impulse–Response Functions measure the dynamic marginal effects of each shock on all of the variables over time. Finally, the variance decompositions examine how important each of the shocks is a component of the overall (unpredictable) variance of each of the variable over time.

5.1. Preliminary VAR Steps

VAR times-series analysis first requires verifying that all variables are stationary then choosing the appropriate lag length criteria.

5.1.1. Stationarity

Variable stationarity is tested with Augmented Dickey Fuller (ADF) and Phillips–Perron (PP). The results are reported in

Table 4.

5.1.2. Lag Length Criteria

The literature analyzing the choice of the appropriate VAR lag length criteria is vast. However, the aforementioned authors (Cf. section literature review) have chosen the traditional Akaike Information Criterion suggested by Akaike.

The lag order selection criteria of the sequential modified (LR) test statistic, the Final Prediction Error (FPE), Schwarz information Criterion (SC), Hannan–Quinn information criterion (HQ), and the Akaike Information Criterion (AIC) are reported in

Table 5,

Table 6,

Table 7 and

Table 8.

5.2. Vector Autoregressive Model-VAR, Residual Serial Correlation, and Granger Causality Test

The VAR model is conceived to capture dynamic interactions among the variables undertaken. The cause-and-effect relationship among variables can be verified under the Block Exogeneity Wald framework. For instance, if past values of one variable such as FSI helps predict future values of another variable such as ECO, then it is said that FSI Granger causes ECO or that ECO is affected by FSI. The simple Granger causality test considers only two variables, and it is expressed in the following way:

where ECO

t and FSI

t are the growth rate of ECO and FSI in time

t, ECO

t−i and FSI

t−i are the growth rate of ECO and FSI in time

t −

i, and

ε and ҙ denote error terms. Based on both Ordinary Least Squares (OLS) coefficient and significance, possible cases obtained are:

Unidirectional Granger causality from FSI to ECO or from ECO to FSI means that one variable increases the prediction on the second variable but not vice versa.

Bidirectional causality is where ECO predicts FSI and FSI predicts ECO too.

Independence between ECO and FSI indicates absence of Granger causality.

Granger causality is often tested in a context of model. Since omitted variable bias might cause problems, this paper considers VAR models or n− equation VAR with n-variable linear system in which each variable is a linear function of its own lagged values and past values of the remaining n-1 variables (

Stock and Watson 2001). A VAR model has at least three variables. Given Y

t, the vector of variables, the classical VAR model becomes:

where Y

t is an m × 1 vector of the endogenous variables and u

t is an m × 1 vector of the error terms in Equation (3).

p is the number of lags that adequately models the dynamic structure. The coefficients of further lags of variables are not statistically significant, and the error terms are white noise. The error terms may, however, be correlated across equations. If the p parameters are jointly significant, then the null hypothesis that states that one variable (x) does not Granger cause the other variable (y) can be rejected. Similarly, if the p parameters are jointly significant, then the null hypothesis that states that one variable (y) does not Granger cause the other variable(x) can be rejected.

In this study, the dynamic relation between FSI, FXFXD, and ECO is first verified. Then, the possible dynamic relation between regional geopolitical risks and the Lebanese financial market is tested so the VAR model considers four variables: Israel GPR, Saudi Arabia GPR, FSI, and FXFXD. Finally, the VAR is run twice, as a robustness check, by including each time one GPR (GPR of Israel or Saudi Arabia) and excluding the other one.

5.2.1. Residual Serial Correlation

The VAR residual serial correlation-Lagrange Multiplier (LM) tests are performed in

Table 9,

Table 10 and

Table 11 to assess the validity of VAR regressions and to make sure the null hypothesis of the absence of autocorrelation in lag given by AIC at 5% is accepted.

5.2.2. Granger Causality Test

Granger causality tests are run to examine the causal relation between regional GPRs and FSI along with FXFXD and ECO. The results are reported in

Table 12,

Table 13 and

Table 14.

5.3. Impulse–Response Functions and Variance Decompositions of Variables

The Impulse–Response Functions (IRFs) aim to analyze the dynamic effects of the system when the model receives an impulse or an exogenous shock on the dynamic path of the variables of each estimated VAR. The departure point of every IRF for a linear VAR model is its moving average (MA) representation, which is also the Forecast Error Impulse Response (FEIR) function

for the

period after the shock is obtained by

with

=

,

K is the number of endogenous variables and

p is the lag order of the VAR.

The off-diagonal elements of the estimated variance–covariance matrix is not zero; therefore, a contemporaneous correlation between the variables in the VAR model would exist. In this study, the IRFs consider some restrictions on the VAR errors to address possible contemporaneous correlations that residual impulses ignore: the Cholesky decomposition method. The Cholesky decomposition method isolates the structural errors by recursive orthogonalization. Further information on contemporaneous relationships can be introduced to the FEIR by simply multiplying it by a matrix F:

The orthogonal impulse response functions consist of decomposing the variance–covariance matrix so that ∑ = PP’, where P is a lower triangular matrix with positive diagonal elements, which is often obtained by a Cholesky decomposition. The latter requires placing variables of interest on the basis of the speed at which the variables act in response to shocks. Accordingly, the variables placed higher in the ordering have contemporaneous impact on the variables lower in the ordering. However, the variables placed lower in the ordering do not have a contemporaneous impact on the variables higher in the ordering.

The corresponding orthogonal impulse response function is then:

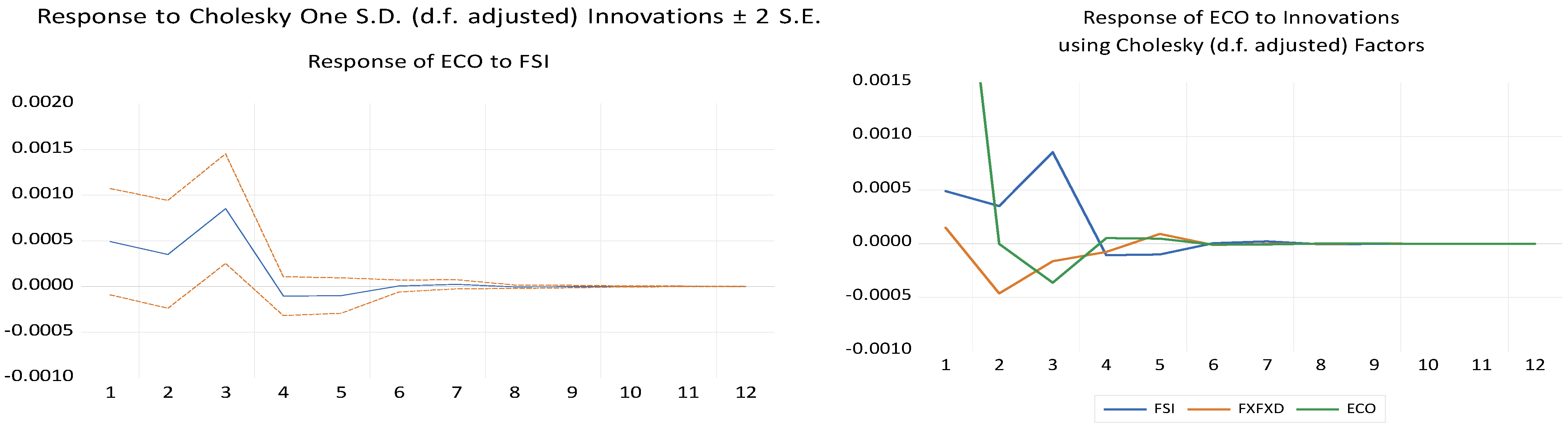

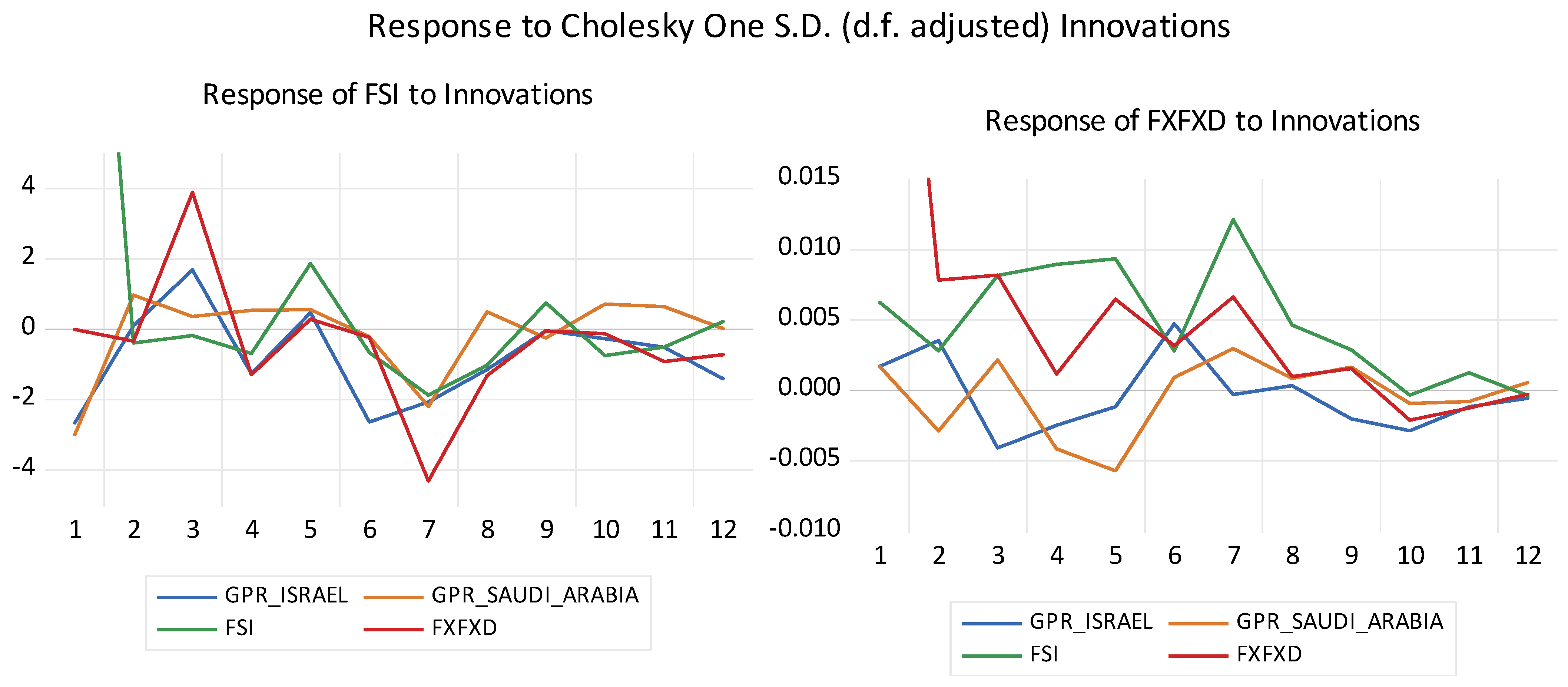

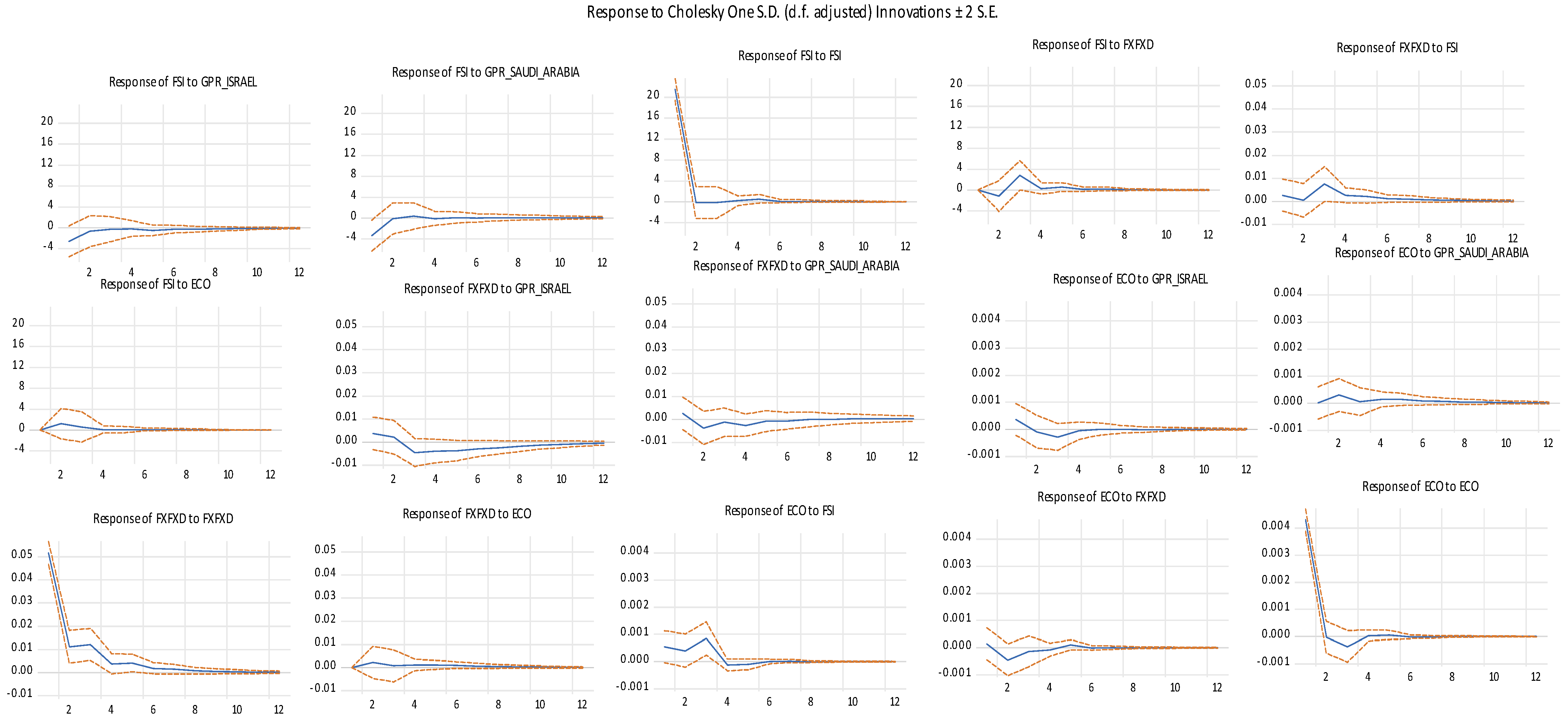

This study considers the GPR of Israel to have a greater impact; hence, it is first ordered-orthogonalized in IRFs. The response of ECO to FSI and to other variables (combined) are reported in

Figure 3. The combined response of FSI and FXFXD to GPR shocks are reported in

Figure 4. The global multiple VAR model IRFs are reported in

Figure A1.

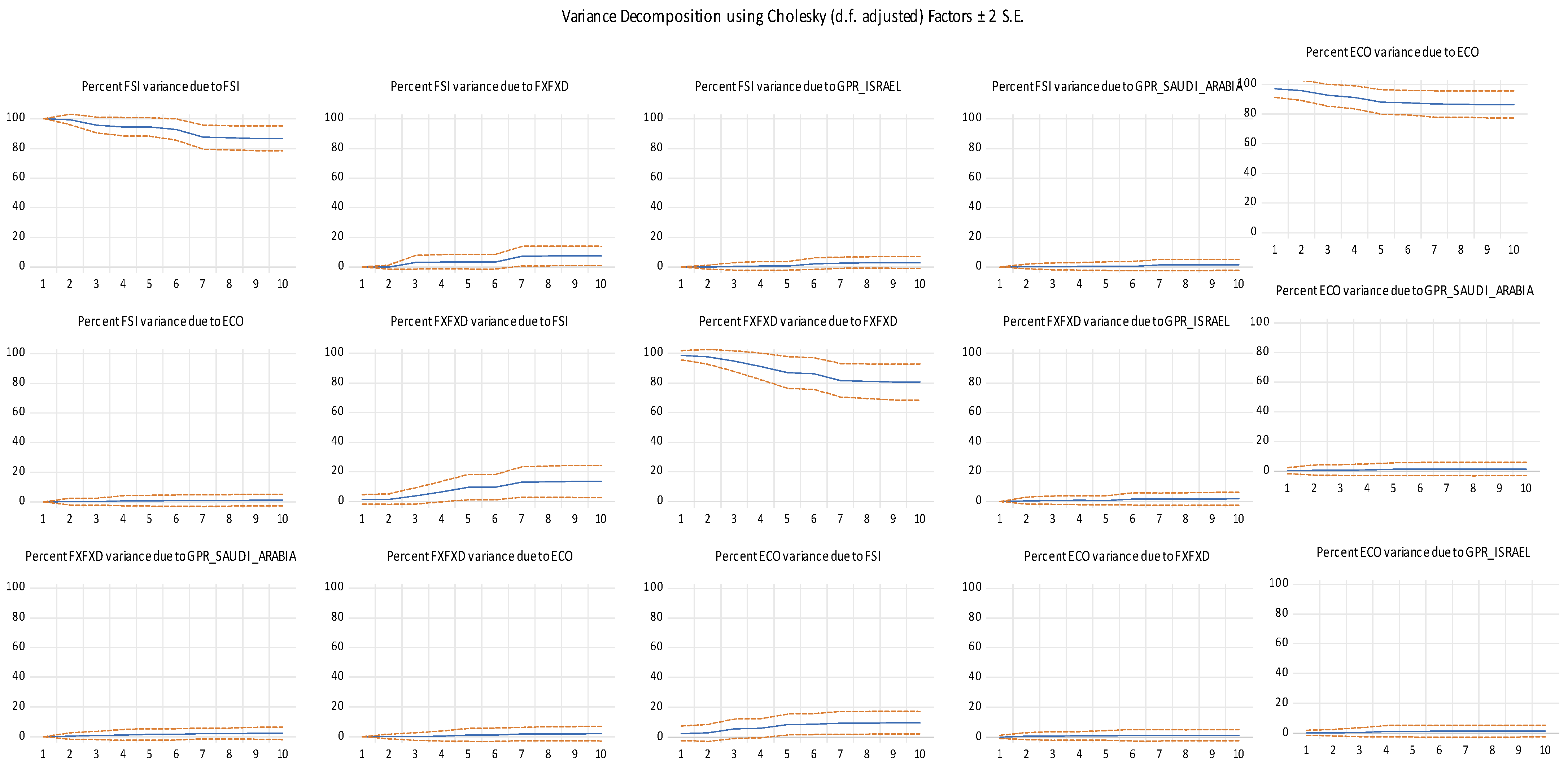

Variance Decompositions of Variables

The variance decomposition of variables shows the portion of variance in the forecast error for each variable due to innovations to all variables in the system (or when a shock is given to one variable). Variance decompositions are represented graphically in

Figure 5 and numerically in

Table A1 in

Appendix A.

7. Conclusions

Over the years, Hezbollah’s role evolved from being hosted by Lebanon to taking Lebanon hostage (

Schmitt 2007) at the behest of the Iran’s ideology (

DeVore 2012;

Seliktar and Rezaei 2020). Hezbollah’s activities that are mostly illegal have harmful consequences on the Lebanese economy. Moreover, it takes sovereign decisions as well as risky actions in the region, mainly against Israel (for resistance ideology raison d’être) and Saudi Arabia (for ideological and geopolitical rivalry), and then forces Lebanon to pay the consequences (

Grumet 2015). Geopolitical consequences of Hezbollah’s domination have been extensively studied and analyzed in politics, sociology, and geopolitics. However, empirical economic studies remain rare, if not inexistent. They are rather descriptive and informative economic news, published in newspapers and press releases. Economic reports elaborated by the United Nations, Reuters, the World Bank, or other international organizations are limited to estimating the cost of reconstruction (after a war) or to exposing in value the costs or the losses on welfare, agriculture, and employment.

The present paper aims to analyze empirically the impact of regional geopolitical tensions with Hezbollah on the Lebanese financial market and economic activity (ECO).

It first proceeds with graphical analysis of the Lebanese financial market that is measured with the Financial Stress Index (FSI), on a monthly basis from 1998 to January 2018 (

Ishrakieh et al. 2020a,

2020b). In this study, the FSI was updated to November 2018 and its analysis started from June 2006 after complete Israeli deliberation from Lebanese territories. Graphical analysis presumes that local economic and political trouble, although numerous, do not seem to generate high FSI spikes whereas high FSI spikes seem to be associated with regional geopolitical tensions where

Hezbollah is in the details. Similarly, it appears that most of the recession periods overlap positive, high FSI spikes. Nevertheless, empirical tests are crucial to verify the preliminary deductions.

The GPR index of Saudi Arabia and Israel were taken from

Caldara and Iacoviello (

2018), calculated on a monthly basis from January 1985 to September 2018 (GPR data were lately updated to October 2020).

The innovative character of this paper is also in the choice of the adequate level of foreign reserves (FX) that best fits a dollarized country (

Gonçalves 2008): The central bank’s foreign reserves to total deposit in foreign currencies (denoted FXFXD).

This study aimed to achieve to one of two possible conclusions:

If the Lebanese financial market shows independency or low dependency–causality to the regional geopolitical risks, then Hezbollah geopolitical tensions with Israel and Saudi Arabia do not seem to negatively affect the Lebanese financial stability. In consequence, economic reforms, monetary and fiscal policies can be improved independently from the geopolitical, international, and diplomatic arrangements.

If the Lebanese financial market shows significant dependency–causality to the regional geopolitical risks, then Hezbollah’s tensions with Israel and Saudi Arabia trigger Lebanese financial stability and economic activity. Therefore, instead of solving the economic crisis from a purely economic perspective, measures towards negotiation and conflict resolution with the neighborhood are needed, which require de-Hezbollizing Lebanon.

The results reveal a significant unidirectional relation from FSI to ECO (p-value 0.004), which means that, in Lebanon, a financial stress seems to be followed by an economic recession within two months while the economic activity does not seem to be strong enough to “Granger cause” a financial market instability.

Empirical outcomes also expose a bidirectional relation between FXFXD and FSI that is highly significant when the VAR model includes GPRs (with

p-value = 0.00) and barely significant internally (

p-value = 0.08). The FXFXD–FSI bidirectional relationship indicates that, when uncertainty (especially resulting from geopolitical tensions) is expressed in the financial market (FSI), economic agents look after converting local currency to foreign ones (FXFXD). Consequently, the depletion of FX arises and then “Granger causes” a more severe financial crisis (FSI) that may ends in an economic contraction (as verified by the unidirectional relation from FSI and ECO). The deduction seems aligned with the IMF–2017 country report analysis for Lebanon where

Ahuja et al. (

2017) stated: “

A common shock to bank liquidity, that leads to a demand for foreign currency, could result in a drop in international reserves (1 percent of deposits are equivalent to 3.7 percent of reserves)”.

The findings indicate that Israel and Saudi Arabia geopolitical risks affect the Lebanese financial market differently. While Israel geopolitical risks appear to be a good predictor for the Lebanese financial crisis within six months, Saudi Arabia GPR does not. This means that the Lebanese financial market remains intact although its heavy involvement in the Lebanese economy that is mainly conducted through the labor market and the touristic sector. In fact, based on the FSI and ECO unidirectional causality, the Lebanese financial market must first be affected in order to hit the economic activity. In other words, even if the GRP of Saudi Arabia triggers the Lebanese economy, the financial market will not be affected. Undoubtedly, a more pointed dynamic relation between Saudi Arabia GPR and the Lebanese economic sectors or, more precisely, the touristic sector will be more informative. Likewise,

Hamadeh and Bassil (

2017) verified the impact of geopolitics, or more precisely terrorism, on the Lebanese touristic sector. Moreover, they found that Arab tourists are significantly more affected than the European ones.

Although Saudi Arabia’s geopolitical risks toward Hezbollah (in Lebanon) are not powerful enough to destabilize the Lebanese financial market, it is found to be a threat for Turkey.

Mansour-Ichrakieh and Zeaiter (

2019) proceeded with a similar empirical analysis between Saudi Arabia GPR and the Turkish financial market and found that Saudi Arabia GPR does not only trigger a severe financial crisis in Turkey, but it also changes its state (threshold VAR) from a low stress level to a high stress level. The findings raise the question of whether Saudi Arabia considers Turkey more dangerous than Hezbollah.

Finally, this study exhibits the existence of a unidirectional causality between Israel GPR and the Lebanese financial market and sheds light on its deleterious effect. In fact, based on the previous bidirectional causality between FSI and FXFXD and the dynamic relation between FSI and ECO, this paper concludes that, when Israel and Hezbollah play geopolitics, the Lebanese financial market seems to respond obviously, by gradually depleting the central bank’s foreign reserves. The latter in return predicts further destabilization of the Lebanese financial market before hitting the economic activity.

The findings do not specify whether the threats are generated from Israel or from Hezbollah unless a Hezbollah GPR index is constructed and then VAR models and Granger causality tests are run.

Regardless of who acts and who reacts (Hezbollah or Israel), the perpetual tit-for-tat between them drives Lebanon and its economy the main victims. For instance, in July 2006, after Hezbollah captured Israeli soldiers, Israel responded severely and attacked Hezbollah inside of Lebanon (

Sharp et al. 2006). Although “

Israel did not attack the government of Lebanon, but rather Hizbullah military assets within Lebanon” (

Schmitt 2007), Lebanon’s cities and infrastructures underwent destruction as well as more than 900,000 Lebanese civilians or about ¼ of the total population became displaced (

Internal Displacement Monitoring Center 2010).

Geopolitical tension is not necessarily expressed by military or terrorist attacks, but it is also through several media channels. Media campaigns raise geopolitical risks especially when the speakers are engaged in military or terrorist acts and want visibility in the media following their actions (

Tsesis 2017). Hezbollah’s leader is so talented in public speaking that his speeches are extensively studied in the literature. Many researchers have been breaking down, analyzing, interpreting, and even revealing hidden messages.

Israel geopolitical risks overshoot the Lebanese financial instability through depleting central bank’s foreign reserves and then end up weakening the economic activity.

Since Israeli geopolitical risks cause deleterious effect on the Lebanese financial stability, the author concludes that, in order to enhance a future financial stability and to promote economic growth, political–geopolitical measures toward negotiation and conflict resolution with the neighborhood (against Hezbollah ideology) are needed, which require first de-Hezbollizing Lebanon. Future studies in law, political science, and geopolitics are expected in order to verify how “realistic” is it to “de-Hezbollize” Lebanon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}