Pricing Perpetual American Put Options with Asset-Dependent Discounting

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Preliminaries

2.1. Assumptions

2.2. Optimal Stopping Time

2.3. Scale Functions

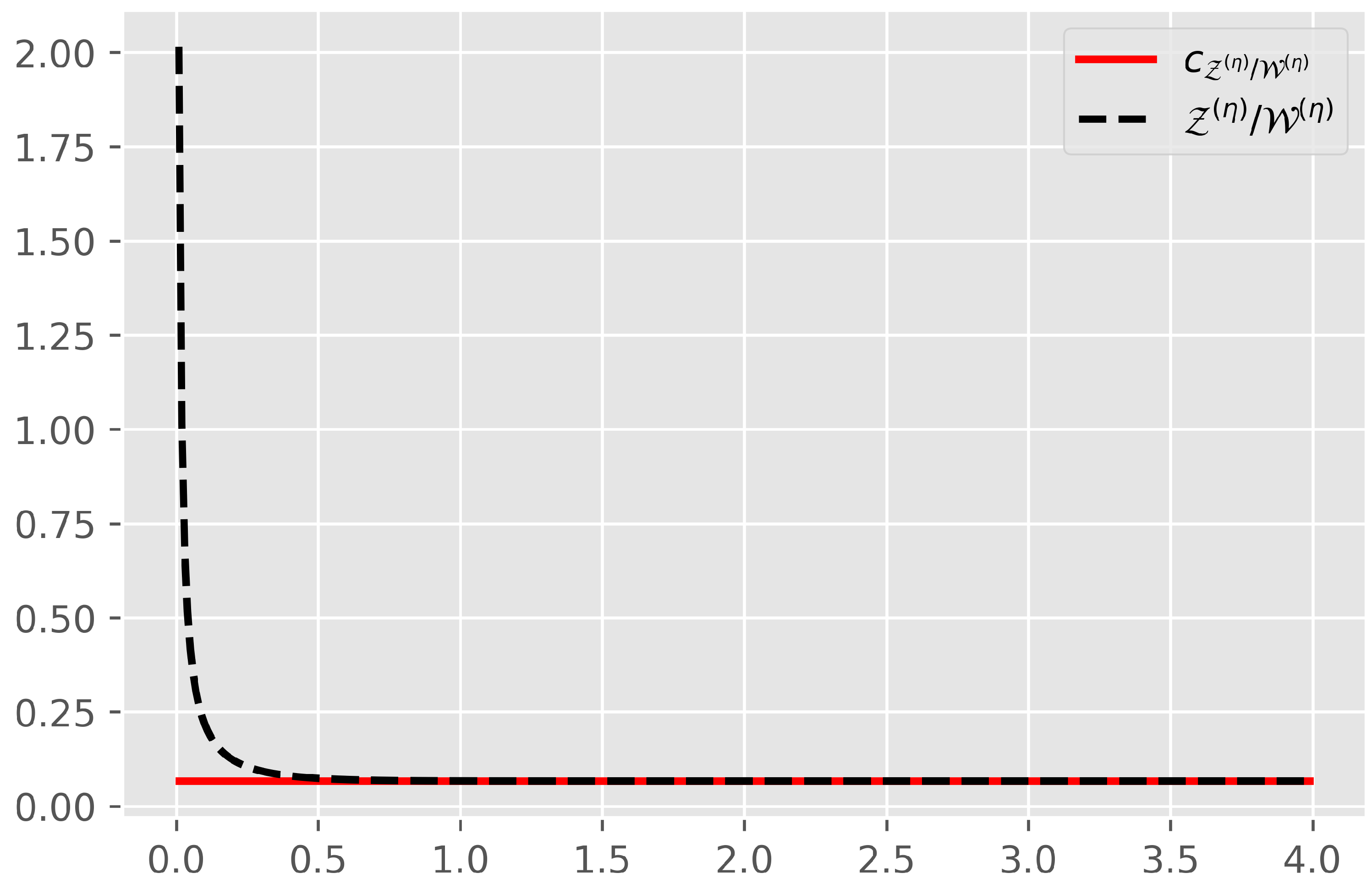

2.4. Theoretical Representation of the Price

- 1.

- For and

- 2.

- For and

- 3.

- For andwhere

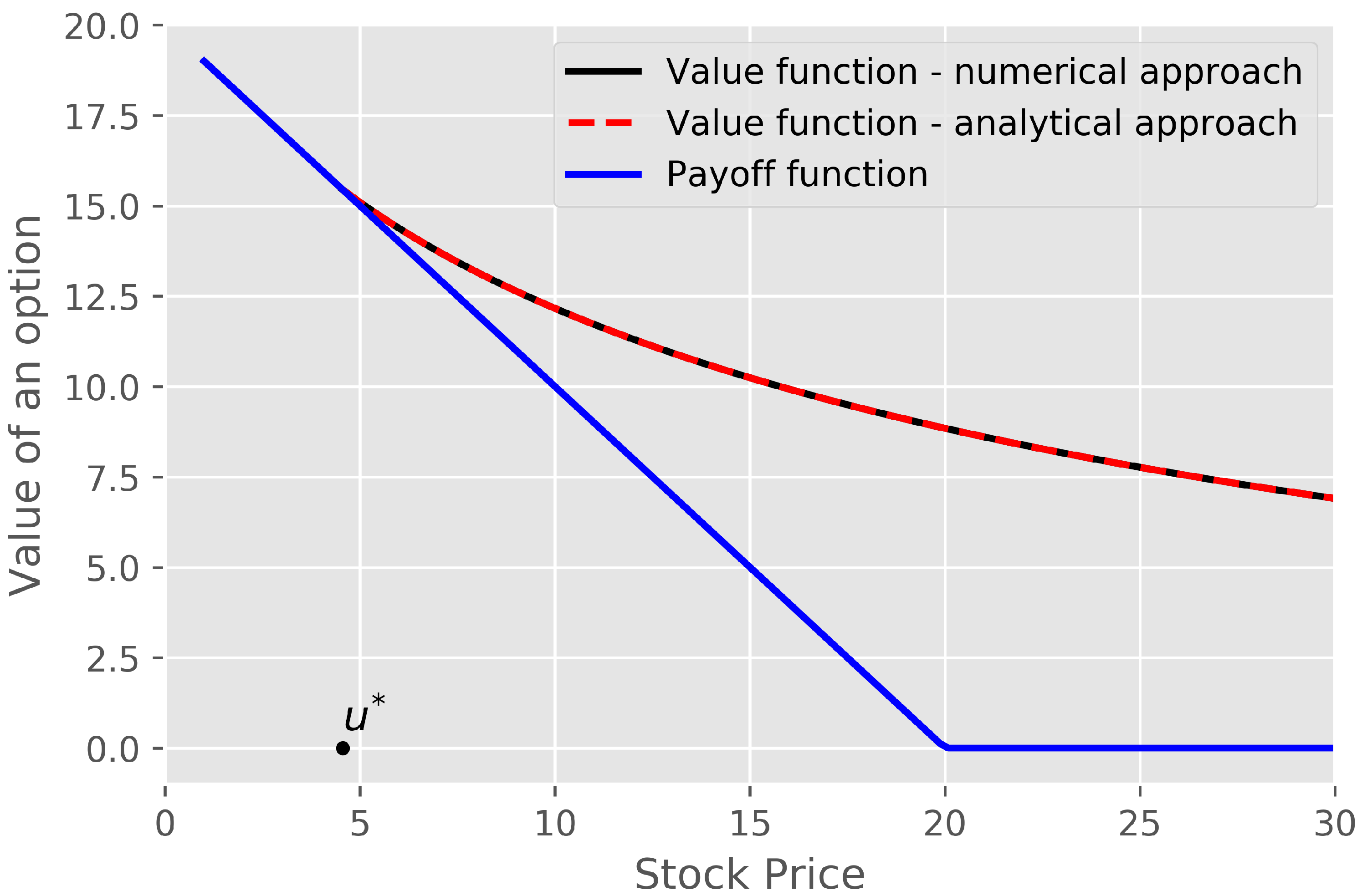

3. Option Pricing—Analytical Approach

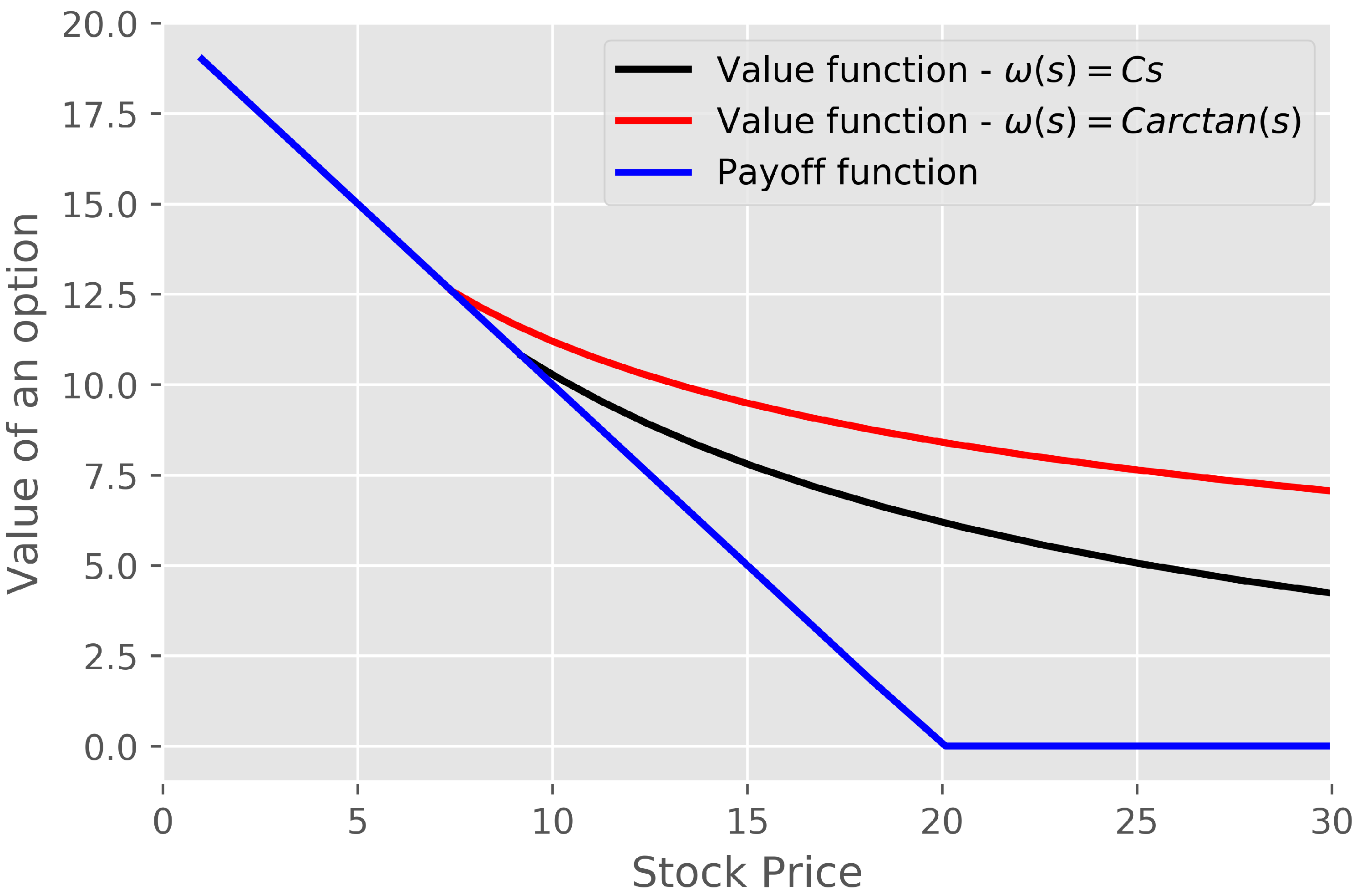

3.1. Constant Discount Function

3.2. Linear Discount Function

3.2.1.

3.2.2.

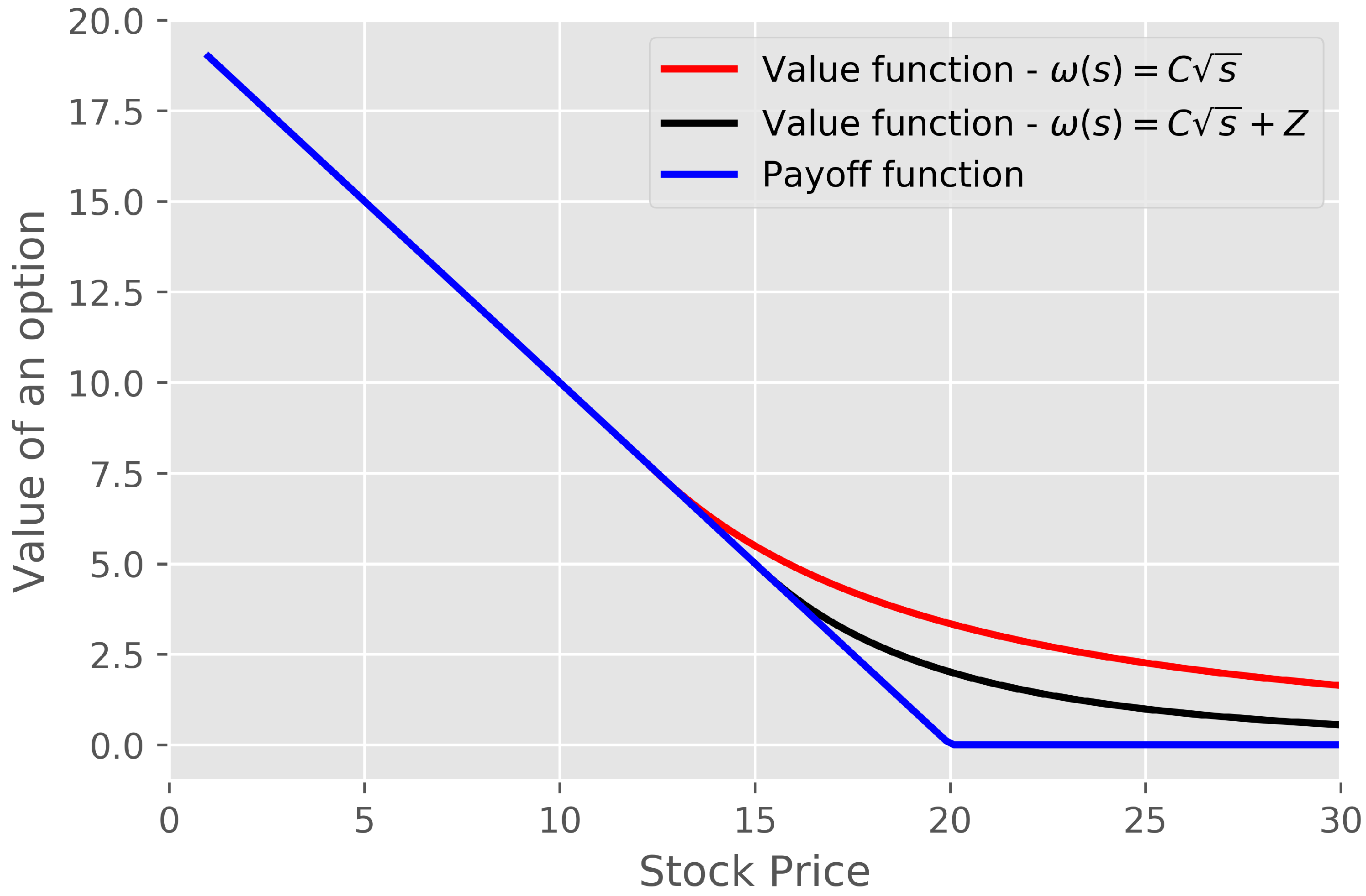

3.3. Power Discount Function

3.3.1.

3.3.2.

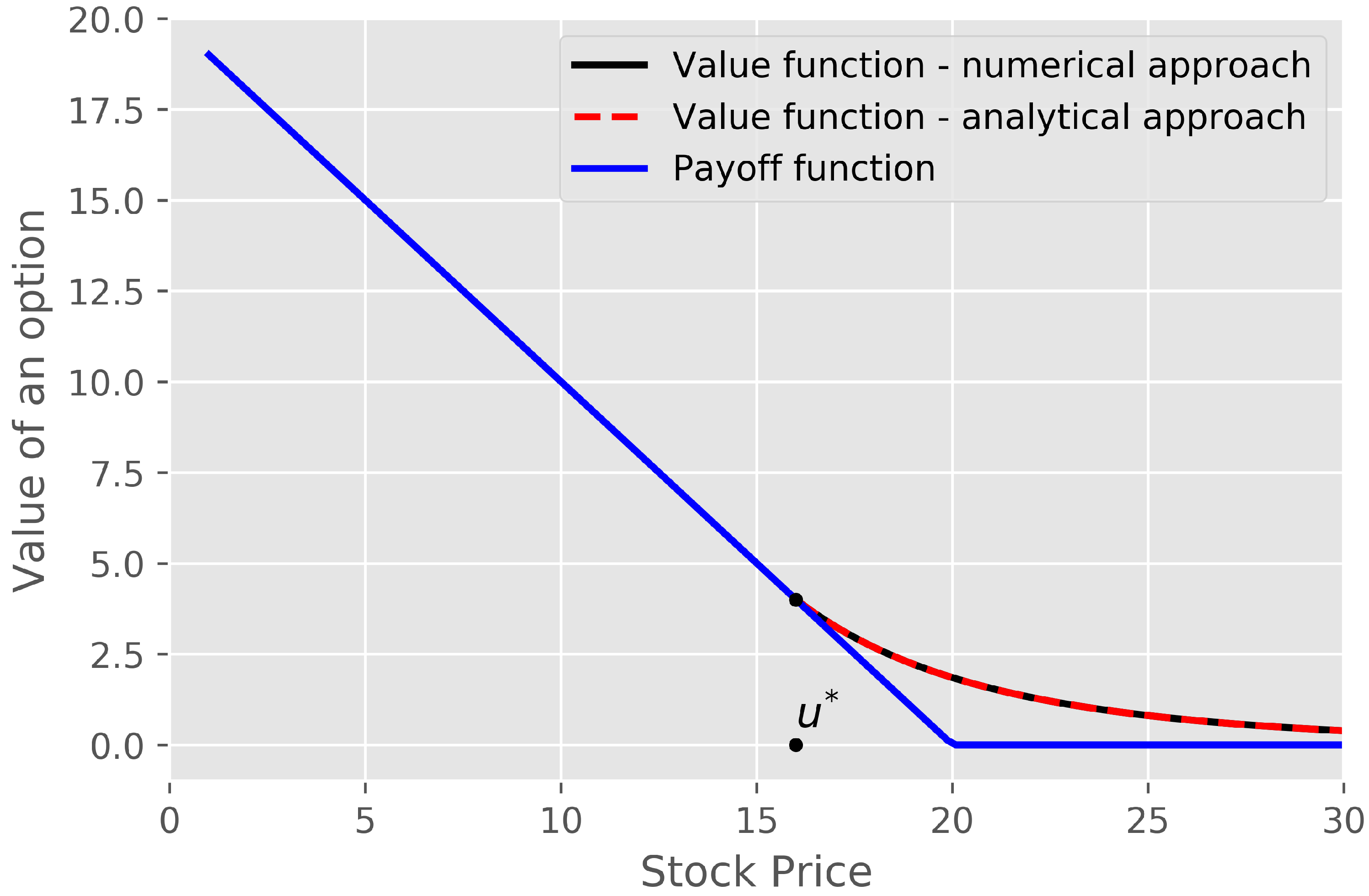

4. Option Pricing—Numerical Approach

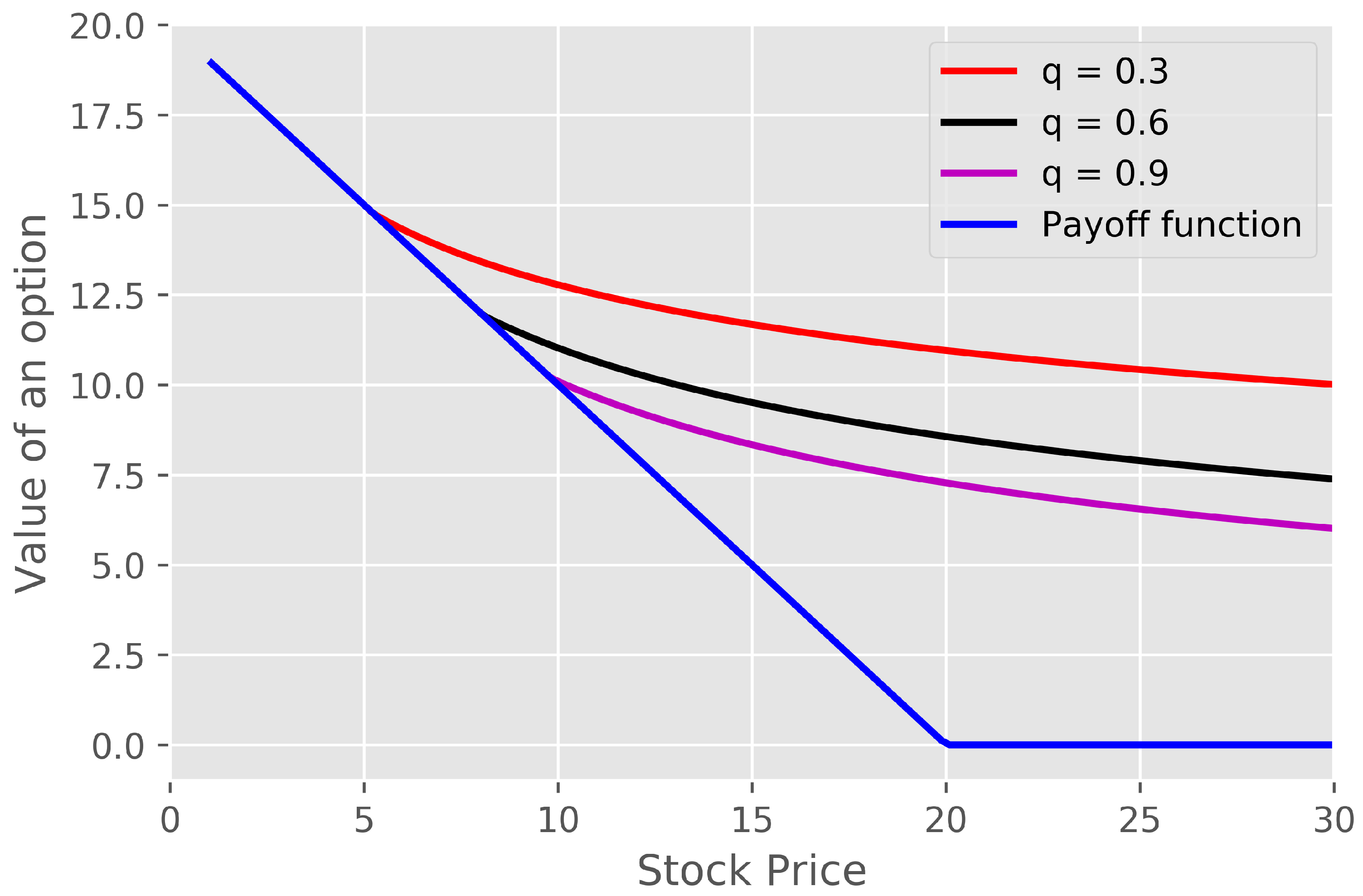

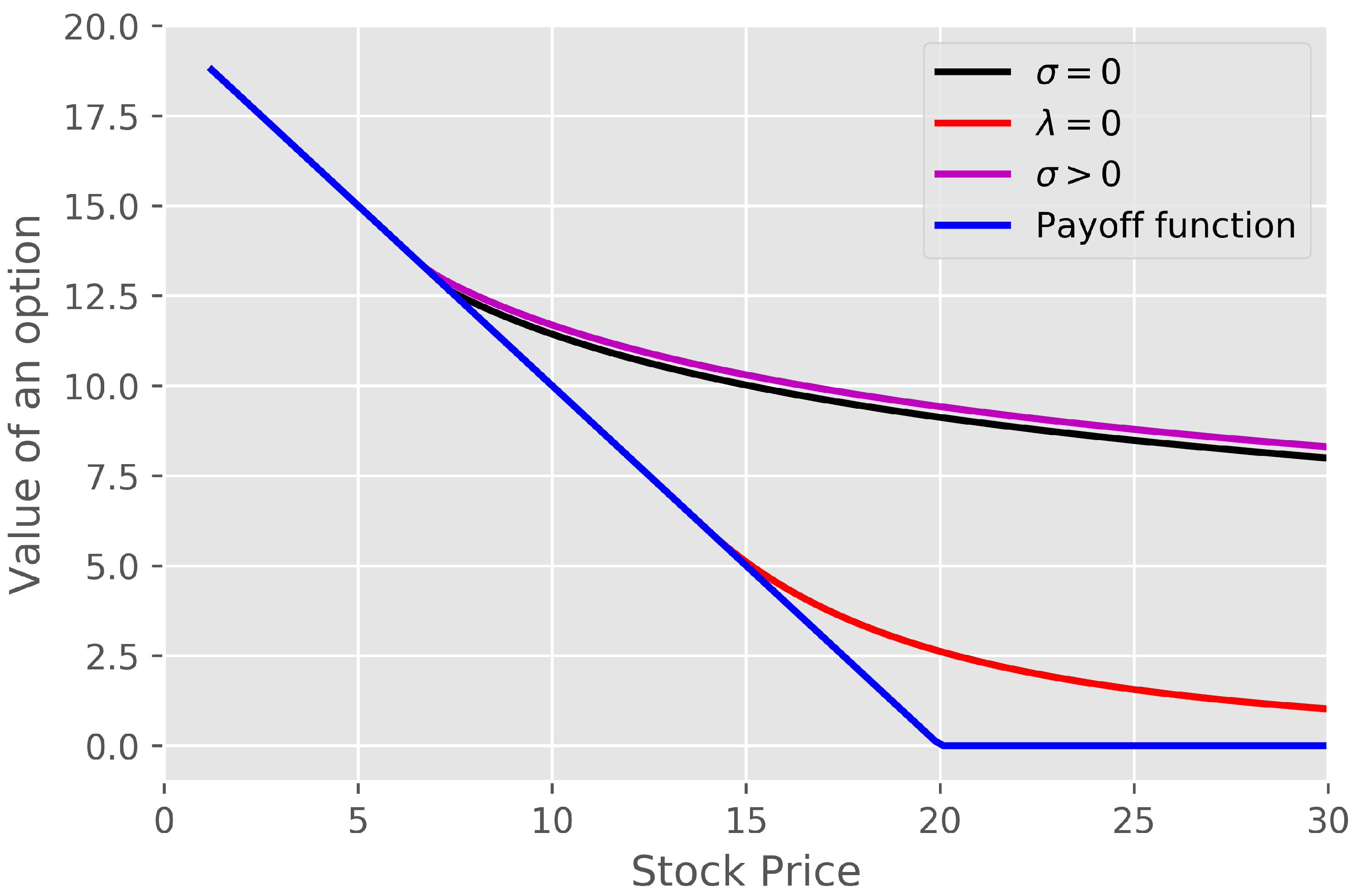

4.1. Different Discount Functions

4.1.1.

4.1.2.

4.1.3. and

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Al-Hadad, Jonas, and Zbigniew Palmowski. 2021. Perpetual American Options with Asset-Dependent Discounting. Submitted for Publication. Available online: https://arxiv.org/abs/2007.09419 (accessed on 18 July 2020).

- Cohen, Serge, Alexey Kuznetsov, Andreas Kyprianou, and Victor Rivero. 2013. Lévy Matters II. Berlin/Heidelberg: Springer. [Google Scholar]

- Cont, Rama, and Peter Tankov. 2004. Financial Modelling with Jump Processes. Boca Raton: Chapman & Hall. [Google Scholar]

- De Donno, Marzia, Zbigniew Palmowski, and Joanna Tumilewicz. 2020. Double continuation regions for American and Swing options with negative discount rate in Lévy models. Mathematical Finance 30: 196–227. [Google Scholar] [CrossRef]

- Kou, Steven G. 2002. A Jump-Diffusion Model for Option Pricing. Management Science 48: 1086–1101. [Google Scholar] [CrossRef]

- Kyprianou, Andreas E. 2006. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Berlin/Heidelberg: Springer. [Google Scholar]

- Li, Bo, and Zbigniew Palmowski. 2018. Fluctuations of omega–killed spectrally negative Lévy processes. Stochastic Processes and their Applications 128: 3273–99. [Google Scholar] [CrossRef]

- Linetsky, Vadim. 1999. Step options. Mathematical Finance 9: 55–96. [Google Scholar] [CrossRef]

- Loeffen, Ronnie L., Jean-François Renaud, and Xiaowen Zhou. 2014. Occupation times of intervals until first passage times for spectrally negative Lévy processes. Stochastic Processes and their Applications 124: 1408–143. [Google Scholar] [CrossRef]

- Palmowski, Zbigniew, and Tomasz Rolski. 2002. A technique for exponential change of measure for Markov processes. Bernoulli 8: 767–85. [Google Scholar]

- Peskir, Goran, and Albert Shiryaev. 2006. Optimal Stopping and Free–Boundary Problems. Basel: Birkhäuser. [Google Scholar]

- Prause, Karsten. 1999. The Generalized Hyperbolic Model: Estimation, Financial Derivatives, and Risk Measures. Ph.D. thesis, University of Freiburg, Breisgau, Germany. Available online: https://d-nb.info/961152192/34 (accessed on October 1999).

- Rodosthenous, Neofytos, and Hongzhong Zhang. 2018. Beating the omega clock: An optimal stopping problem with random time-horizon under spectrally negative Lévy models. Annals of Applied Probability 28: 2105–40. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al-Hadad, J.; Palmowski, Z. Pricing Perpetual American Put Options with Asset-Dependent Discounting. J. Risk Financial Manag. 2021, 14, 130. https://doi.org/10.3390/jrfm14030130

Al-Hadad J, Palmowski Z. Pricing Perpetual American Put Options with Asset-Dependent Discounting. Journal of Risk and Financial Management. 2021; 14(3):130. https://doi.org/10.3390/jrfm14030130

Chicago/Turabian StyleAl-Hadad, Jonas, and Zbigniew Palmowski. 2021. "Pricing Perpetual American Put Options with Asset-Dependent Discounting" Journal of Risk and Financial Management 14, no. 3: 130. https://doi.org/10.3390/jrfm14030130

APA StyleAl-Hadad, J., & Palmowski, Z. (2021). Pricing Perpetual American Put Options with Asset-Dependent Discounting. Journal of Risk and Financial Management, 14(3), 130. https://doi.org/10.3390/jrfm14030130