Towards a New Form of Undemocratic Capitalism: Introducing Macro-Equity to Finance Development Post COVID-19 Crisis

{kind=link}

Abstract

1. Introduction: The Problem of Democratic Capitalism

2. Materials and Methods

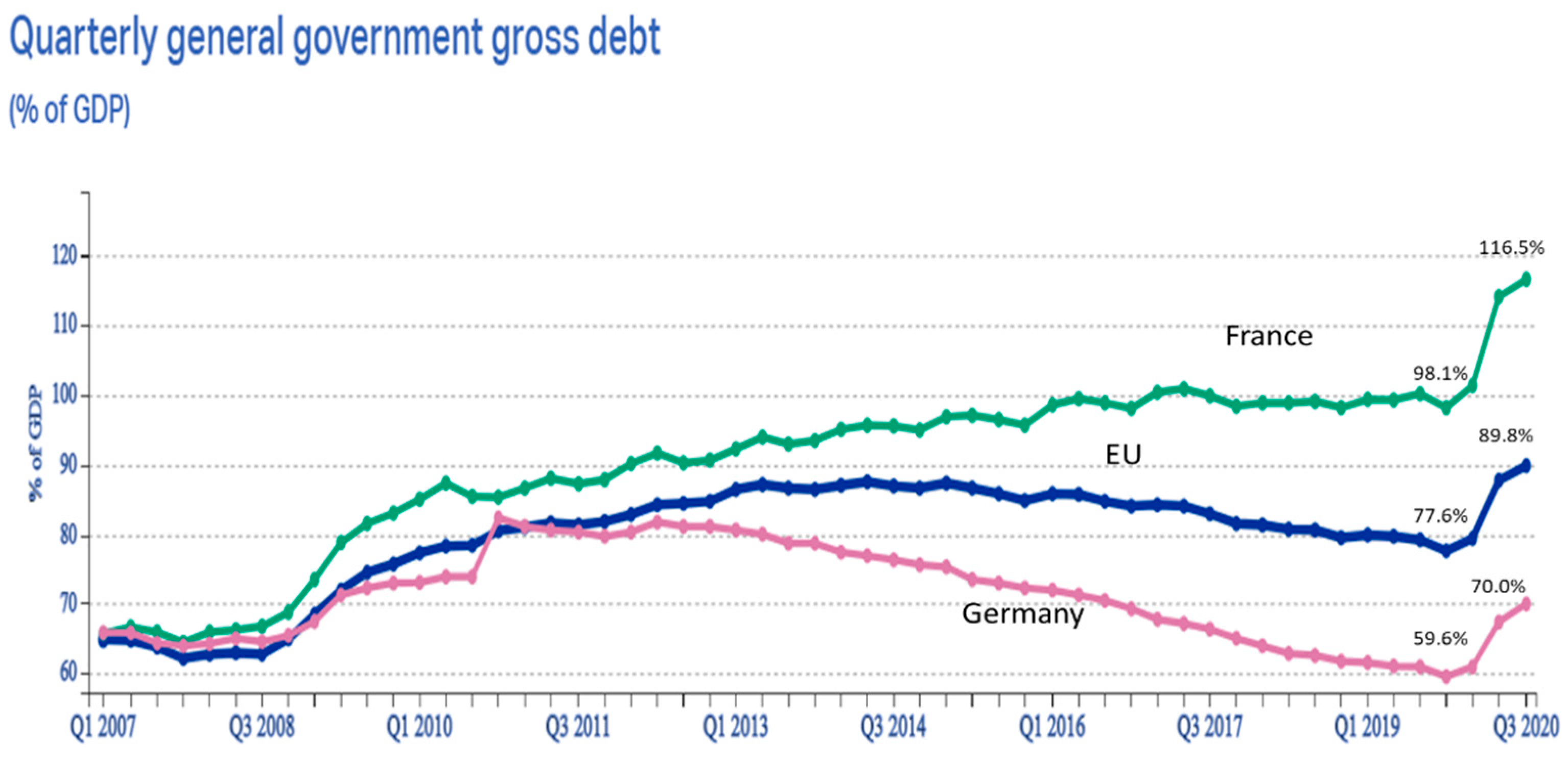

3. The Proposed Solution: Macro-Equity

4. Discussion: Evaluating the Proposition

5. Concluding Remark

Funding

Conflicts of Interest

References

- Ashta, Arvind, and Ndyey Salimata Fall. 2012. Institutional analysis to understand the growth of microfinance institutions in West African Economic and Monetary Union. Corporate Governance 12: 441–59. [Google Scholar] [CrossRef]

- Ashta, Arvind, and Surender Mor. 2017. Fostering Well-Being through Cultural Change: Lessons from Microfinance for Social Entrepreneurs. In Good Governance and Growth in the Global Economy. Edited by Anil Kumar Sinha, Amiya Kumar Mohapatra and Tushar Sankar Banerjee. New Delhi: Bloomsbury, pp. 21–30. [Google Scholar]

- Ashta, Arvind. 2020. Reflections on the financing of Covid-19? Introducing MACRO-Equity and opening Pandora’s Box. Artha 6: 15–21. [Google Scholar]

- Blanc, Sandrine. 2014. Expanding Workers ‘Moral Space’: A Liberal Critique of Corporate Capitalism. Journal of Business Ethics 120: 473–88. [Google Scholar] [CrossRef]

- Blumenthal, David. 2009. Portrait of a Policy and Political Entrepreneur. Health Affairs 28: w1037–39. [Google Scholar] [CrossRef] [PubMed]

- Börgers, Tilman. 1996. On the relevance of learning and evolution to economic theory. Economic Journal 106: 1374–85. [Google Scholar] [CrossRef]

- Bowman, Edward H., and Mason Haire. 1975. A Strategic Posture toward Corporate Social Responsibility. California Management Review 18: 49–58. [Google Scholar] [CrossRef]

- Brooks, Simon. 2005. Corporate social responsibility and strategic management: The prospects for converging discourses. Strategic Change 14: 401–11. [Google Scholar] [CrossRef]

- Brubaker, Earl R. 1983. On the Margolis’ thought experiment,’ and the applicability of demand-revealing mechanisms to large-group decisions. Public Choice 41: 315–19. [Google Scholar] [CrossRef]

- Calderisi, Robert. 2006. The Trouble with Africa: Why Foreign Aid Isn’t Working. New York: Palgrave Macmillan. [Google Scholar]

- Camerer, Colin. 2005. Three Cheers—Psychological, Theoretical, Empirical—For Loss Aversion. Journal of Marketing Research (JMR) 42: 129–33. [Google Scholar] [CrossRef]

- Caste, Nicholas J. 1992. Drug Testing and Productivity. Journal of Business Ethics 11: 301–6. [Google Scholar] [CrossRef]

- Chan, Sewin. 2015. The Next Coming Crisis of Capitalism. Public Administration Review 75: 492–96. [Google Scholar] [CrossRef]

- Clements, Jeffrey D. 2014. Corporations Are Not People: Reclaiming Democracy from Big Money and Global Corporations. San Francisco: Berrett-Koehler Publishers. [Google Scholar]

- Crane, Andrew, Guido Palazzo, Laura J. Spence, and Dirk Matten. 2014. Contesting the Value of “Creating Shared Value”. California Management Review 56: 130–53. [Google Scholar] [CrossRef]

- Cumming, Gordon D. 2018. Towards an enhanced understanding of aid policy reform: Learning from the French case. Public Administration & Development 38: 179–89. [Google Scholar] [CrossRef]

- De Bono, Edward. 1970. Lateral Thinking: A Textbook of Creativity. London: Penguin. [Google Scholar]

- Dzigbede, Komla D., Sarah Beth Gehl, and Katherine Willoughby. 2020. Disaster Resiliency of U.S. Local Governments: Insights to Strengthen Local Response and Recovery from the COVID-19 Pandemic. Public Administration Review 80: 634–43. [Google Scholar] [CrossRef] [PubMed]

- Easterly, William. 2006. The White Man’s Burden: Why the West’s Efforts to Aid the Rest Have Done So Much Ill and So Little Good. London: Penguin Books. [Google Scholar]

- Eccles, Neil. 2010. UN Principles for Responsible Investment Signatories and the Anti-Apartheid SRI Movement: A Thought Experiment. Journal of Business Ethics 95: 415–24. [Google Scholar] [CrossRef]

- Elkington, John, Jed Emerson, and Seb Beloe. 2006. The Value Palette: A Tool For Full Spectrum Strategy. California Management Review 48: 6–28. [Google Scholar] [CrossRef]

- Gao, Yongqiang. 2008. Institutional Change Driven by Corporate Political Entrepreneurship in Transitional China: A Process Model. International Management Review 4: 25–37. [Google Scholar]

- Hayek, Friedrich. 2014. The Road to Serfdom: Text and Documents: The Definitive Edition. London: Routledge. First published by 1945. [Google Scholar]

- IIF. 2020. Global Debt Monitor: Attack of the Debt Tsunami. Washington: IIF. [Google Scholar]

- IMF. 2020. Fiscal Monitor: Policies for the Recovery. Washington: IMF. [Google Scholar]

- Jones, Thomas M. 1995. Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review 20: 404–37. [Google Scholar] [CrossRef]

- Jones, Thomas M., Jeffrey S. Harrison, and Will Felps. 2018. How Applying Instrumental Stakeholder Theory Can Provide Sustainable Competitive Advantage. Academy of Management Review 43: 371–91. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Jack L. Knetsch. 1991. The Endowment Effect, Loss Aversion, and Status Quo Bias. Journal of Economic Perspectives 5: 193–206. [Google Scholar] [CrossRef]

- Karadjov, Boshko. 2019. Economic Freedom, Neoliberalism and Morality: From John Locke to Robert Nozick. Journal of Sustainable Development (1857–8519) 9: 115–24. [Google Scholar]

- Kosack, Stephen. 2014. The Logic of Pro-Poor Policymaking: Political Entrepreneurship and Mass Education. British Journal of Political Science 44: 409–44. [Google Scholar] [CrossRef]

- Liu, Yajie, and Feng Dong. 2020. Corruption, economic development and haze pollution: Evidence from 139 global countries. Sustainability 12: 3523. [Google Scholar] [CrossRef]

- Lucas, Robert E., Jr. 2003. Macroeconomic Priorities. American Economic Review 93: 1–14. [Google Scholar] [CrossRef]

- Maak, Thomas, and Nicolas Stoetter. 2012. Social Entrepreneurs as Responsible Leaders: ‘Fundación Paraguaya’ and the Case of Martin Burt. Journal of Business Ethics 111: 413–30. [Google Scholar] [CrossRef]

- Mankiw, N. Gregory. 2013. Defending the One Percent. Journal of Economic Perspectives 27: 21–34. [Google Scholar] [CrossRef]

- Margolis, Howard. 1982. A thought experiment on demand-revealing mechanisms. Public Choice 38: 87–91. [Google Scholar] [CrossRef]

- Mària, Josep, and Daniel Arenas. 2009. Societal Ethos and Economic Development Organizations in Nicaragua. Journal of Business Ethics 88: 231–44. [Google Scholar] [CrossRef]

- Misangyi, Vilmos F., Gary R. Weaver, and Heather Elms. 2008. Ending Corruption: The Interplay among Institutional Logics, Resources, and Institutional Entrepreneurs. Academy of Management Review 33: 750–70. [Google Scholar] [CrossRef]

- Moyo, Dambisa. 2009. Dead Aid: Why Aid Is Not Working and How There Is a Better Way for Africa. New York: Farrar, Straus and Giroux. [Google Scholar]

- Nkrumah, Kwame. 1965. Neo-Colonialism: The Last Stage of Imperialism. London: Nelson. [Google Scholar]

- Nollert, Michael, and Sebastian Schief. 2011. Preventing the Retrenchment of the Welfare State: Switzerland’s Competitiveness in the World Market for Protection. Competition & Change 15: 315–35. [Google Scholar] [CrossRef]

- Orwell, George. 2009. Nineteen Eighty-Four. London: Secker & Warburg. First published by 1949. [Google Scholar]

- Osborne, David, and Peter Plastrik. 1997. Banishing Bureaucracy: Five Strategies for ReinventingGovernment. Reading: Addison Wesley. [Google Scholar]

- Petras, James, and Henry Veltmeyer. 2000. Globalisation or imperialism? Cambridge Review of International Affairs 14: 32–48. [Google Scholar] [CrossRef]

- Piketty, Thomas. 2014. Capital in the Twenty-First Century. Cambridge: Belknap Press. [Google Scholar]

- Popescu, Cristina Raluca Gh, and Gheorghe N. Popescu. 2019. An Exploratory Study Based on a Questionnaire Concerning Green and Sustainable Finance, Corporate Social Responsibility, and Performance: Evidence from the Romanian Business Environment. Journal of Risk and Financial Management 12: 162. [Google Scholar] [CrossRef]

- Porter, Michael E., and Mark R. Kramer. 2011. Creating shared value. Harvard Business Review 89: 62–77. [Google Scholar]

- Roberts, Alasdair. 2020. The Third and Fatal Shock: How Pandemic Killed the Millennial Paradigm. Public Administration Review 80: 603–9. [Google Scholar] [CrossRef]

- Schneider, Mark, and Paul Teske. 1992. Toward a theory of the political entrepreneur: Evidence from local government. American Political Science Review 86: 737. [Google Scholar] [CrossRef]

- Stiglitz, Joeseph E. 2013. The Price of Inequality: How Today’s Divided Society Endagers Our Future. New York: W.W. Norton & Company. [Google Scholar]

- Taleb, Nassim Nicholas. 2018. Skin in the Game: Hidden Asymmetries in Daily Life. London: Penguin Random House. [Google Scholar]

- Thaler, Richard H., Amos Tversky, Daniel Kahneman, and Alan Schwartz. 1997. The Effect of Myopia and Loss Aversion on Risk Taking: An experimental Test. Quarterly Journal of Economics 112: 647–61. [Google Scholar] [CrossRef]

- Weiser, Philip J. 2008. Alfred Kahn as a Case Study of a Political Entrepreneur: An Essay in Honour of his 90th Birthday. Review of Network Economics 7: 603–15. [Google Scholar] [CrossRef]

- Yoffie, David B., and Sigrid Bergenstein. 1985. Creating Political Advantage: The Rise of the Corporate Political Entrepreneur. California Management Review 28: 124–39. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ashta, A. Towards a New Form of Undemocratic Capitalism: Introducing Macro-Equity to Finance Development Post COVID-19 Crisis. J. Risk Financial Manag. 2021, 14, 116. https://doi.org/10.3390/jrfm14030116

Ashta A. Towards a New Form of Undemocratic Capitalism: Introducing Macro-Equity to Finance Development Post COVID-19 Crisis. Journal of Risk and Financial Management. 2021; 14(3):116. https://doi.org/10.3390/jrfm14030116

Chicago/Turabian StyleAshta, Arvind. 2021. "Towards a New Form of Undemocratic Capitalism: Introducing Macro-Equity to Finance Development Post COVID-19 Crisis" Journal of Risk and Financial Management 14, no. 3: 116. https://doi.org/10.3390/jrfm14030116

APA StyleAshta, A. (2021). Towards a New Form of Undemocratic Capitalism: Introducing Macro-Equity to Finance Development Post COVID-19 Crisis. Journal of Risk and Financial Management, 14(3), 116. https://doi.org/10.3390/jrfm14030116