3. The First Explorative Case Study: Microsoft’s Acquisition of LinkedIn in 2016

On 11 June 2016, Microsoft Corporation announced a merger with LinkedIn under which the transaction valued at approximately USD 26.2 bn. What triggers the acquisition-based dynamic capabilities of such a technologically advanced corporation such as Microsoft? What similarities and complementarity of dynamic capabilities of Microsoft and LinkedIn existed and what building blocks of the business model of LinkedIn could be transferred to Microsoft’s business model?

Regarding the similarities of the dynamic capabilities, both companies were successful when they were developing new market niches, Microsoft with Office products and LinkedIn with its professional social network. Both companies were successful in sensing possible needs in non-developed markets, seizing popular products and services and keeping them on track over the years, maintaining leading positions and achieving satisfactory results. Companies used both in-house resources and acquisitions for transformation, developing new tools, and adopting products to various operational systems.

When it comes to its complementarities and triggers of acquisition-based dynamic capabilities, the first trigger is the fact that Microsoft was behind iOS and Google mobile ecosystems. Moreover, the Skype example shows that Microsoft was rather weak in sensing in already developed, rapidly growing markets, such as consumer internet. The dynamic capabilities of Microsoft showed poor results when the company tried to gain leadership positions in an already developed market. In contrast, LinkedIn successfully runs a social network on mobile devices with a high mobile presence (60% of users).

The second trigger is the deal as a means for Microsoft to foray into the professional social networking space. LinkedIn had immense potential to grow as a professional social network with revenue generation similar to that of a software business. However, despite having a strong user base of 433 million in 2016, LinkedIn continued its struggle to grow the user base and had little scope for profit.

Thereby, LinkedIn’s users offered opportunities for Microsoft to develop its cloud and customer relationship management initiatives (

Sapersen and Gonzales 2017). As far as Microsoft was concerned, the main objective for the tech giant was to occupy a position at the center of peoples’ business lives. That leads to the conclusion that the building blocks of the corporation’s business model are compatible and transferable if Microsoft keeps LinkedIn autonomous in its development and provides it resources for the development.

In turn, it evidences the high probability to generate dynamic capabilities-based synergies in the acquisition of LinkedIn. The acquisition-based dynamic capabilities helped Microsoft to innovate a business model by obtaining managerial synergies as shown in

Table 1.

To measure dynamic capabilities-based synergies of the Microsoft acquisition, and to justify the proposition, the author used real options application employing BSOPM and BOPM. The first valuation model used to measure dynamic capabilities-based synergies in M&A deal was based on the Black–Scholes option pricing model (

Black and Scholes 1973), namely: C (S, t) = S0 × N(d

1) − K × e

−rT × N(d

2), where N(d

1), N(d

2) are the cumulative distribution functions of the standard normal distribution; C (S, t) is call option price at time t; S0 is the price of the underlying asset at time 0; K is the exercise price at time t; T is time in years; r is a risk-free rate; e is a mathematical constant approximately equal to 2.71828, the base of the natural logarithm; σ is expected volatility of an underlying asset’s value.

On 13 June 2016, the capitalization of Microsoft was USD 394.1 bn; the capitalization of LinkedIn was USD 25.7 bn (

Pillars of Wall Street 2017). The first valuation model used to measure dynamic capabilities-based synergies in M&A deals was based on the Black–Scholes option pricing model (

Black and Scholes 1973) as shown in

Table 2 and

Table 3.

Dynamic capabilities-based synergies of Microsoft’s acquisition of LinkedIn are USD 92.8 bn by BSOPM valuation. The valuation of the acquisition’s synergies by the Binominal Option Pricing Model (BOPM) is USD 91.3 bn and given in

Table 4,

Table 5 and

Table 6.

Once the binominal tree of assets value is completed, the next step is to calculate the possible payoff synergies) and roll back the values using risk-neutral probabilities as given in

Table 6.

Thus, the forecasted market capitalization of Microsoft Inc. in one year after the acquisition of LinkedIn is the cumulative capitalization of a target and an acquirer before the announcement—(So) USD 419.8 bn plus estimated synergies of USD 92 bn, which equals USD 511.8 bn. Microsoft capitalization on 19 June 2017 was USD 551.59 bn. Therefore, expected synergies were fully realized and the added market value even bigger than predicted. However, the connection of the theoretical value with actual value largely depends on the timing of the prices taken and is entirely difficult to justify precisely in this study. Meanwhile, having compared the calculated option value with the takeover premium paid, one should be concluded that this acquisition added market value to Microsoft corporation thanks to dynamic capabilities-based synergy.

4. Second Explorative Case Study: Amazon’s Acquisition of Whole Foods

On 16 June 2017 Amazon.com announced that it would purchase Whole Foods Market for a total of USD 13.7 billion. So, what do Amazon hope to gain with this acquisition? There are several similarities between the dynamic capabilities of Amazon and Whole Foods. Both companies are sensing market demands and seizing external opportunities in online and offline grocery businesses. However, their transforming capabilities need to be mutually complemented. There are several complementarities between the dynamic capabilities of Amazon and Whole Foods.

One of Amazon’s weaknesses is the huge cost of losses due to food items becoming bad, a problem which the company had never faced with toys and books and had no great experience in the offline retail environment. In contrast, Whole Foods became an organic supermarket that distinguishes itself by offering “highest quality natural and organic products”. The first trigger of acquisition-based dynamic capabilities is as follows. To grab more grocery market share, Amazon should learn to sell food offline (

Kowitt 2018).

On the other hand, having a variety of niche products with a high price charge, the growth of Whole Foods had slowed because competitors began to offer organic foods at a lower price. From 2013 to 2016, Whole Foods lost nearly half its market value (

Helmore 2017). That is why just a few days after the merger, Amazon dropped prices by as much as 43% on a range of Whole Foods products (

Garfield 2017). It makes the probability to exercise the real option of the acquisition of Whole Foods very high. The acquisition-based dynamic capabilities helped Amazon to innovate a business model by getting managerial synergies as shown in

Table 7.

To measure dynamic capabilities-based synergies of Amazon acquisition, and to justify the proposition, the author used real options application employing BSOPM and BOPM. On 16 June 2017, the capitalization of Amazon was USD 478.6 bn; the capitalization of Whole Foods was USD 13.8 bn (

Pillars of Wall Street 2017). The first valuation model used to measure dynamic capabilities-based synergies in M&A deal was based on the Black–Scholes option pricing model (

Black and Scholes 1973) as shown in

Table 8 and

Table 9.

Dynamic capabilities-based synergies of Amazon’s acquisition of Whole Foods are USD 58.0 bn by BSOPM valuation. The valuation of the acquisition’s synergies by the Binominal Option Pricing Model (BOPM) is USD 60.36 bn and is given in

Table 10,

Table 11 and

Table 12.

Thus, the forecasted market capitalization of Amazon Inc. in one year after the acquisition is the cumulative capitalization of target and acquirer before the announcement—(So) USD 492.40 bn plus estimated synergies USD 59 bn, which equals USD 551.40 bn. Thereby, from an option-pricing point of view, this acquisition provides significant dynamic capabilities-based synergies. In short, Amazon’s acquisition of Whole Foods was able to generate significant value-added for the acquirer’s shareholders.

5. Discussion and Contributions of Research

Teece argues “that studies that provide a better understanding of business model innovation, implementation, and change will also shed light on important aspects of dynamic capabilities” (

Teece 2018, p. 40). The paper contributes to this scientific discussion on the role of dynamic capabilities in business model innovation and justifies the proposition of Teece that “the crafting, refinement, implementation, and transformation of business models are outputs of high-order (dynamic) capabilities” (

Teece 2018, p. 40).

Technological changes and new demand make previously acquired competencies obsolete and call for new competencies to be built (

Danneels 2008,

2016). In this vein, empirical research is essential to the progress of research on dynamic capabilities (

Danneels 2016) and on real options applications in strategic management (

Trigeorgis and Reuer 2017).

Jahanshahi and Nawaser (

2018) argue that future research can test the relationship of a real options theory and dynamic capabilities framework in the project and firm-level (

Jahanshahi and Nawaser 2018, p. 400). This paper contributes to this scientific discussion. The current paper justifies the role of dynamic capabilities as antecedents of success of M&A deals and demonstrates real options application to measure managerial synergies in M&A deals.

Moreover, the paper contributes and demonstrates how acquisition-based dynamic capabilities provide managerial synergies. Having tested empirically this relationship, the current paper enriches our knowledge about how organizations can benefit from real options and redefine dynamic capabilities framework to the heart of strategic management. This is the major theoretical contribution of the current paper.

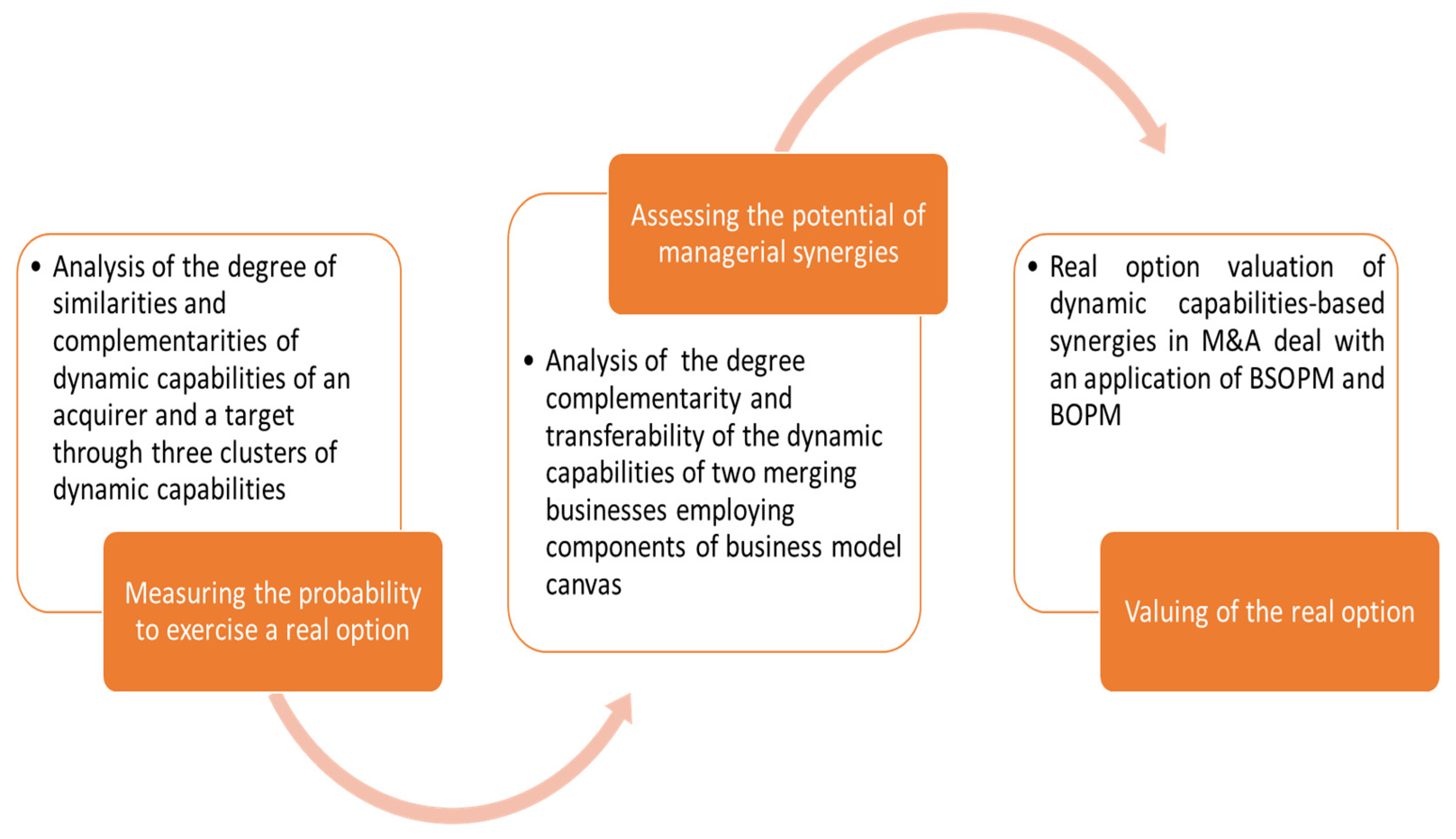

Having explored two case studies, the proposition has been justified empirically. This paper contributes to the understanding of the micro-foundations of similarities and complementarity among dynamic capabilities of an acquirer and a target in M&A deals in the ICT industry and the transferability of building blocks of their business models. Moreover, advancing future research designs for real options valuation,

Trigeorgis and Reuer (

2017, p. 57) argue “we would encourage the use of real option with a greater focus … on individual real option cases”. The current paper also contributes to the real options theory by two illustrative real option cases.

Thereby, the proposition has been justified quantitatively with an application of the Black-Sholes Option Pricing Model and Binominal Option Pricing Lattice techniques. To sum up theoretical and managerial contribution, the relationship among research variables is given in

Figure 1.

Figure 1 also presents the main proposed construct for future research as well as for practical due diligence purposes in the merging process. Acquirers need to absorb the dynamic capabilities of targets and to transfer building blocks of the target’s business model on their own. Thereby, an acquirer converts an M&A deal into a value creation process (synergies) that can be valued by real options.

6. Conclusions, Limitations, and Future Research Direction

Trigeorgis (

1995) argued that it is crucially important that appropriate valuation techniques be employed to capture the various strategic considerations that could support many acquisitions. The paper contributes to this request as well. The relationship among research variables provides a dynamic view on M&A deals to help executives in the sustaining of long-run competitive advantage and strategic adaptability.

Acquisition and alliance are some of the dynamic mechanisms by which the firm’s competencies portfolio is altered (

Danneels 2016). The acquisitions of Microsoft and Amazon of LinkedIn and Whole Foods were able to generate significant value-added for the acquirers’ shareholders. “In most acquisitions, even those where synergy is real and creates value, the acquiring firm’s stockholders get little or none of the benefits from synergy” (

Damodaran 2005, p. 41), due to biased evaluation process and managerial hubris (pride). However, this statement is not about Microsoft and Amazon corporations.

The current paper also demonstrates the limitation of real options application to measure a dynamic capabilities-based synergy. It is difficult to validate the synergetic effect of one isolated acquisition deal when several acquisitions happen within the anticipation of the duration of achieving synergy. In this vein, more research is needed to justify the developed proposition.

Ongoing areas of an empirical investigation into dynamic capabilities, on topics such as acquisitions and alliances, among others, would also benefit from additional research (

Schilke et al. 2018). What is more, exploration of dynamic capabilities to create new market-related and technological resources and their effects on managerial synergies (market value added) is an intriguing area for future research (

Danneels 2016).

{kind=link}