Behavioral Decision Making in Normative and Descriptive Views: A Critical Review of Literature

{kind=link}

Abstract

1. Introduction

2. Methodology and Framework

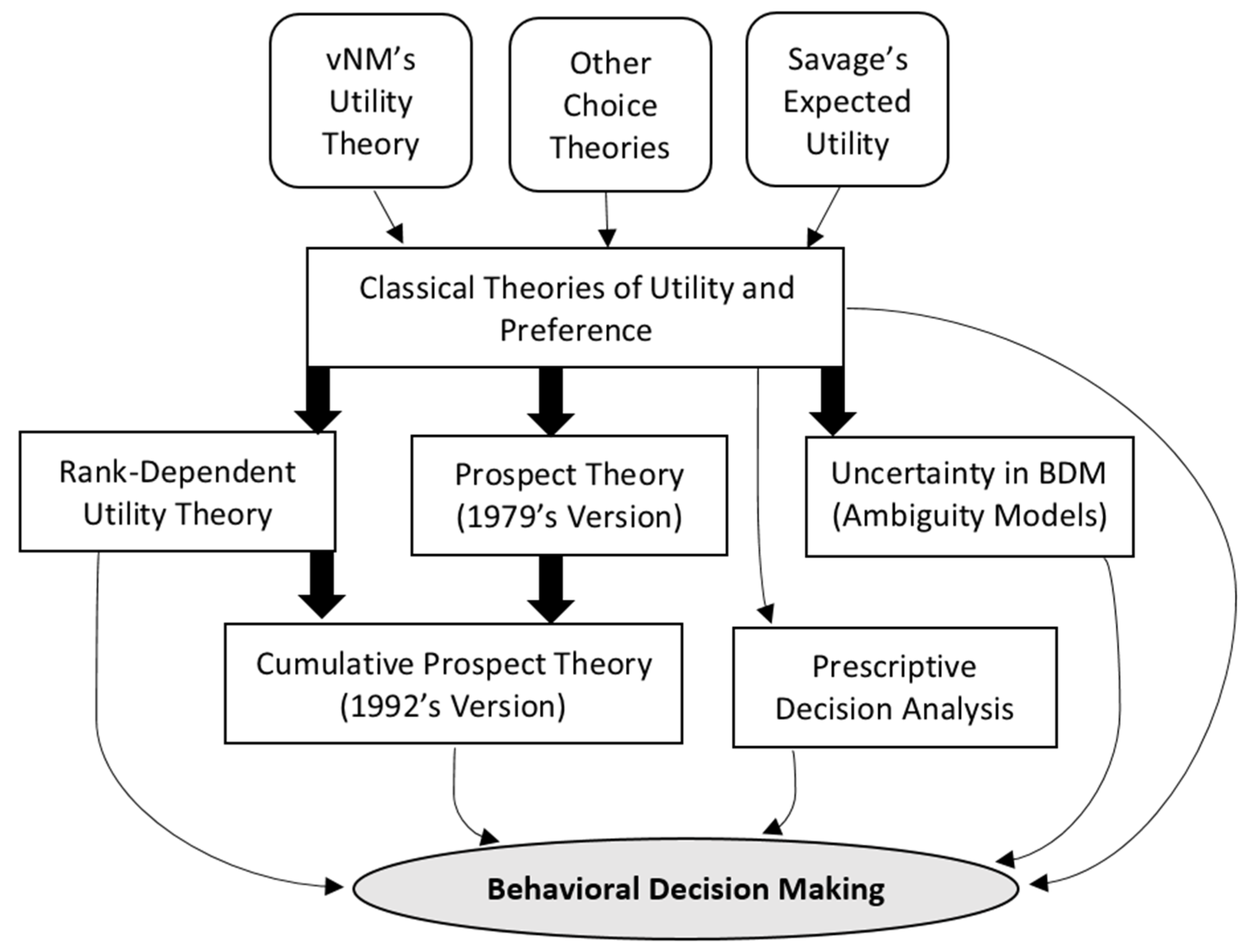

3. Classical Theories of Utility and Preferences

4. Prospect Theory

5. Uncertainty in Economics and Non-Economics

- (1)

- Human preference is represented by (different types of) information. The preference aggregation degenerates as the information aggregation—the intermediate variables.

- (2)

- Prospects (e.g., lotteries or options) are materialized and termed alternatives.

- (3)

- Value function in its simplest form is employed for the evaluation of each alternative. The sum of evaluations over all criteria is the index used for ranking, where the evaluation is in the form of WV, with the value of information V and weights of criteria W.

6. Ambiguity Aversion and Models

7. The Source Method in Decision under Ambiguity

8. Discussion

- (1)

- Loss aversion and reference dependence, e.g., Kahneman and Tversky’s PT;

- (2)

- Fairness and social preference, e.g., Fehr and Schmidt’s (1999) fairness model;

- (3)

- Models of quasi-maximization mistakes, e.g., Rabin, Laibson, and their coauthors.

9. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

| 1 | When the classes are not predefined, such classification is called a clustering or grouping problem, which is an important problem in the field of data mining and machine learning. Interested readers can refer to Han et al. (2012). |

| 2 | For state a and b, acts f and g are called “comonotonic” if f(a) ≻ f(b) implies g(a) ≽ g(b), thus state a and b can be (weakly) ranked. Wakker (2010, p. 279 and Appendix 10.12) commented that the notion of “comonotonicity” proposed by Schmeidler (1989) is not intuitive for applications. |

| 3 | Under nonadditive probabilities, Gilboa and Schmeidler (1989) pointed out that there exist some curious problems, which still adhere to utility maximization. |

| 4 | All states have the sure outcomes, but their probabilities can be subjective rather than objective, therefore, SEU holds. |

| 5 | Wakker (2010 p. 49) pointed out that such a misunderstanding, say Savage’s SEU model is to deviate the objective probability models such as EU theory, is primarily in psychological literature. It, unfortunately, leads to a bigger misunderstanding in modern decision theory as the separation between risk and uncertainty. If so, all modern decision models under risk shall have a generalized version for uncertainty, and all models for uncertainty might also be suitable for risk in one of its degenerated versions. |

References

- Abdellaoui, Mohammed, Aurélien Baillon, Laetitia Placido, and Peter P. Wakker. 2011. The rich domain of uncertainty: Source functions and their experimental implementation. American Economic Review 101: 695–723. [Google Scholar] [CrossRef]

- Allais, Maurice. 1953. Le Comportement de l’Homme Rationnel devant le Risque: Critique des Postulats et Axiomes de l’Ecole Américaine. Econometrica 21: 503–46. [Google Scholar] [CrossRef]

- Anscombe, Frank J., and Robert J. Aumann. 1963. A definition of subjective probability. Annals of Mathematical Statistics 34: 199–205. [Google Scholar] [CrossRef]

- Barberis, Nicholas. 2013. Thirty years of prospect theory in economics: A review and assessment. Journal of Economic Perspectives 27: 173–95. [Google Scholar] [CrossRef]

- Becker, Kai Helge. 2016. An outlook on behavioural OR—Three tasks, three pitfalls, one definition. European Journal of Operational Research 249: 806–15. [Google Scholar] [CrossRef]

- Camerer, Colin F., and Martin Weber. 1992. Recent developments in modeling preferences: Uncertainty and ambiguity. Journal of Risk and Uncertainty 5: 325–70. [Google Scholar] [CrossRef]

- Cerreia-Vioglio, Simone, Fabio Maccheroni, Massimo Marinacci, and Luigi Montrucchio. 2011. Uncertainty averse preferences. Journal of Economic Theory 146: 1275–330. [Google Scholar] [CrossRef]

- Chai, Junyi. 2021a. A model of ambition, aspiration, and happiness. European Journal of Operational Research 288: 692–702. [Google Scholar] [CrossRef]

- Chai, Junyi. 2021b. Dominance-based rough approximation and knowledge reduction: A class-based approach. Soft Computing 25: 11535–49. [Google Scholar] [CrossRef]

- Chai, Junyi, and James N. K. Liu. 2013. Dominance-based decision rules induction for multicriteria ranking. International Journal of Machine Learning and Cybernetics 4: 427–44. [Google Scholar] [CrossRef]

- Chai, Junyi, and James N. K. Liu. 2014. A novel believable rough set approach for supplier selection. Expert Systems with Applications 41: 92–104. [Google Scholar] [CrossRef]

- Chai, Junyi, and Eric W. T. Ngai. 2015. Multi-perspective strategic supplier selection in uncertain environments. International Journal of Production Economics 166: 215–25. [Google Scholar] [CrossRef]

- Chai, Junyi, and Eric W. T. Ngai. 2020. Decision-making techniques in supplier selection: Recent accomplishments and what lies ahead. Expert Systems with Applications 140: 112903. [Google Scholar] [CrossRef]

- Chai, Junyi, James N. K. Liu, and Zeshui Xu. 2012. A new rule-based SIR approach to supplier selection under intuitionistic fuzzy environments. International Journal of Uncertainty, Fuzziness and Knowledge-Based Systems 20: 451–71. [Google Scholar] [CrossRef]

- Chai, Junyi, James N. K. Liu, and Eric W. T. Ngai. 2013a. Application of decision-making techniques in supplier selection: A systematic review of literature. Expert Systems with Applications 40: 3872–85. [Google Scholar] [CrossRef]

- Chai, Junyi, James N. K. Liu, and Zeshui Xu. 2013b. A rule-based group decision model for warehouse evaluation under interval-valued intuitionstic fuzzy environments. Expert Systems with Applications 40: 1959–70. [Google Scholar] [CrossRef]

- Chai, Junyi, Chen Li, Peter P. Wakker, Tong V. Wang, and Jingni Yang. 2015. Reconciling Savage’s and Luce’s modeling of uncertainty: The best of both worlds. Journal of Mathematical Psychology 166: 215–25. [Google Scholar] [CrossRef]

- Chen, Xiaofeng, Yanting Fang, Junyi Chai, and Zeshui Xu. 2021. Does intuitionistic fuzzy analytic hierarchy process work better than analytic hierarchy process? International Journal of Fuzzy Systems 1–16. [Google Scholar] [CrossRef]

- Chew, Soo Hong, and Jacob S. Sagi. 2006. Event exchangeability: Probabilistic sophistication without continuity or monotonicity. Econometrica 74: 771–86. [Google Scholar]

- Chew, Soo Hong, and Jacob S. Sagi. 2008. Small worlds: Modeling attitudes toward sources of uncertainty. Journal of Economic Theory 139: 1–24. [Google Scholar] [CrossRef]

- Choquet, Gustave. 1953. Theory of capacities. Annales de l’lnstitut Fourier 5: 131–295. [Google Scholar] [CrossRef]

- Cinelli, Marco, Milosz Kadzinski, Michael Gonzalez, and Roman Slowinski. 2020. How to support the application of multiple criteria decision analysis? Let us start with a comprehensive taxonomy. Omega 96: 102261. [Google Scholar] [CrossRef]

- Dempster, Arthur P. 1968. Upper and lower probabilities generated by a random closed interval. Annals of Mathematical Statistics 39: 957–66. [Google Scholar] [CrossRef]

- Deng, Julong. 1982. Control problems of grey systems. Systems & Control Letters 1: 288–94. [Google Scholar]

- Edwards, Ward, ed. 1992. Utility: Theories, Measurement, and Applications. Dordrecht: Kluwer Academic Publishers. [Google Scholar]

- Ellsberg, Daniel. 1961. Risk, ambiguity and the Savage axioms. Quarterly Journal of Economics 75: 643–69. [Google Scholar] [CrossRef]

- Ergin, Haluk, and Faruk Gul. 2009. A theory of subjective compound lotteries. Journal of Economic Theory 144: 899–929. [Google Scholar] [CrossRef]

- Fehr, Ernst, and Klaus M. Schmidt. 1999. A theory of fairness, competition, and cooperation. Quarterly Journal of Economics 114: 817–68. [Google Scholar] [CrossRef]

- Fishburn, Peter C. 1988. Nonlinear Preference and Utility Theory. Baltimore: Johns Hopkins University Press. [Google Scholar]

- Fishburn, Peter C. 1989. Generalizations of expected utility theories: A Survey of Recent Proposals. Annals of Operations Research 19: 3–28. [Google Scholar] [CrossRef]

- Fox, Craig R., and Russell A. Poldrack. 2014. Prospect theory on the brain. In Handbook of Neuroeconomics. Edited by Paul W. Glimcher and Ernst Fehr. New York: Elsevier, pp. 533–67. [Google Scholar]

- Fox, Craig R., and Amos Tversky. 1995. Ambiguity aversion and comparative ignorance. Quarterly Journal of Economics 110: 585–603. [Google Scholar] [CrossRef]

- Fox, Craig R., and Amos Tversky. 1998. A Belief-Based Account of Decision under Uncertainty. Management Science 44: 879–895. [Google Scholar] [CrossRef]

- Franco, L. Alberto, Raimo P. Hamalainen, Etienne A. J. A. Rouwette, and Ilkka Leppanen. 2021. Taking stock of behavioural OR: A review of behavioural studies with an intervention focus. European Journal of Operational Research 293: 401–18. [Google Scholar] [CrossRef]

- French, Kenneth R., and James M. Poterba. 1991. Investor diversification and international equity markets. American Economic Review 81: 222–26. [Google Scholar]

- Gajdos, Thibault, Takashi Hayashi, Jean-Marc Tallon, and Jean-Christophe Vergnaud. 2008. Attitude towards Imprecise Information. Journal of Economic Theory 140: 27–65. [Google Scholar] [CrossRef]

- Ghirardato, Paolo, Fabio Maccheroni, and Massimo Marinacci. 2004. Differentiating ambiguity and ambiguity attitude. Journal of Economic Theory 118: 133–73. [Google Scholar] [CrossRef]

- Gilboa, Itzhak. 1987. Expected utility with purely subjective nonadditive probabilities. Journal of Mathematical Economics 16: 65–88. [Google Scholar] [CrossRef]

- Gilboa, Itzhak. 2009. Theory of Decision under Uncertainty. Econometric Society Monograph Series; Cambridge: Cambridge University Press. [Google Scholar]

- Gilboa, Itzhak, and David Schmeidler. 1989. Maxmin expected utility with a non-unique prior. Journal of Mathematical Economics 18: 141–53. [Google Scholar] [CrossRef]

- Gilboa, Itzhak, and David Schmeidler. 1993. Updating ambiguous beliefs. Journal of Economic Theory 59: 33–49. [Google Scholar] [CrossRef]

- Golman, Russell, David Hagmann, and George Loewenstein. 2016. Information avoidance. Journal of Economic Literature 55: 96–135. [Google Scholar] [CrossRef]

- Hadar, Josef, and William R. Russell. 1971. Stochastic dominance and diversification. Journal of Economic Theory 3: 288–305. [Google Scholar] [CrossRef]

- Halevy, Yoram. 2007. Ellsberg revisited: An experimental study. Econometrica 75: 503–36. [Google Scholar] [CrossRef]

- Hämäläinen, Raimo P., Jukka Luoma, and Esa Saarinen. 2013. On the importance of behavioral operational research: The case of understanding and communicating about dynamic systems. European Journal of Operational Research 228: 623–24. [Google Scholar] [CrossRef]

- Han, Jiawei, Micheline Kamber, and Jian Pei. 2012. Data Mining: Concepts and Techniques, 3rd ed. Burlington: Morgan Kaufmann. [Google Scholar]

- Hansen, Lars Peter. 2014. Nobel Lecture: Uncertainty outside and inside Economic Models. Journal of Political Economy 122: 945–87. [Google Scholar] [CrossRef]

- Hansen, Lars Peter, and Thomas J. Sargent. 2001. Robust control and model uncertainty. American Economic Review 91: 60–66. [Google Scholar] [CrossRef]

- Hansen, Lars Peter, Thomas J. Sargent, and Thomas D. Tallarini, Jr. 1999. Robust permanent income and pricing. Review of Economic Studies 66: 873–907. [Google Scholar] [CrossRef]

- Ho, Teck H., Noah Lim, and Colin F. Camerer. 2006. How “psychological” should economic and marketing models be? Journal of Marketing Research 43: 341–44. [Google Scholar] [CrossRef]

- Houthakker, Hendrik S. 1950. Revealed preference and the utility function. Economica 17: 159–74. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky, eds. 2000. Choices, Values and Frame. New York: Russell Sage Foundation. Cambridge University Press. [Google Scholar]

- Karni, Edi. 1985. Decision Making under Uncertainty. The Case of State-Dependent Preferences. Cambridge: Harvard University Press. [Google Scholar]

- Karni, Edi, and David Schmeidler. 1990. Utility theory with uncertainty. Handbook of Mathematical Economics 4: 1763–831. [Google Scholar]

- Keynes, John Maynard. 1948. A Treatise on Probability, 2nd ed. London: McMillan. First published 1921. [Google Scholar]

- Kilka, Michael, and Martin Weber. 2001. What determines the shape of the probability weighting function under uncertainty. Management Science 47: 1712–26. [Google Scholar] [CrossRef]

- Klibanoff, Peter, Massimo Marinacci, and Sujoy Mukerji. 2005. A smooth model of decision making under ambiguity. Econometrica 73: 1849–92. [Google Scholar] [CrossRef]

- Knight, Frank H. 1921. Risk, Uncertainty, and Profit. New York: Houghton Mifflin. [Google Scholar]

- Koszegi, Botond. 2014. Behavioral contract theory. Journal of Economic Literature 52: 1075–118. [Google Scholar] [CrossRef]

- Luce, R. Duncan. 1991. Rank- and sign-dependent linear utility models for binary gambles. Journal of Economic Theory 53: 75–100. [Google Scholar] [CrossRef]

- Luce, R. Duncan, and Peter C. Fishburn. 1991. Rank- and sign-dependent linear utility models for finite first-order gambles. Journal of Risk and Uncertainty 4: 29–59. [Google Scholar] [CrossRef]

- Maccheroni, Fabio, Massimo Marinacci, and Aldo Rustichini. 2006. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica 74: 1447–98. [Google Scholar] [CrossRef]

- Machina, Mark J. 2009. Risk, ambiguity, and the rank-dependence axioms. American Economic Review 99: 385–92. [Google Scholar] [CrossRef]

- Machina, Mark J., and David Schmeidler. 1992. A more robust definition of subjective probability. Econometrica 60: 745–80. [Google Scholar] [CrossRef]

- Machina, Mark J., and David Schmeidler. 1995. Bayes without Bernoulli: Simple conditions for probabilistically sophisticated choice. Journal of Economic Theory 67: 106–28. [Google Scholar] [CrossRef]

- Marttunen, Mika, Judit Lienert, and Valerie Belton. 2017. Structuring problems for multi-criteria decision analysis in practice: A literature review of method combinations. European Journal of Operational Research 263: 1–17. [Google Scholar] [CrossRef]

- Morton, Alec, and Barbara Fasolo. 2009. Behavioural decision theory for multi-criteria decision analysis: A guided tour. Journal of the Operational Research Society 60: 262–75. [Google Scholar] [CrossRef]

- Quiggin, John. 1982. A theory of anticipated utility. Journal of Economic Behavior and Organization 3: 323–43. [Google Scholar] [CrossRef]

- Rabin, Matthew. 1998. Psychology and economics. Journal of Economic Literature 36: 11–46. [Google Scholar]

- Rabin, Matthew. 2013. Incorporating limited rationality into economics. Journal Economic Literature 51: 528–43. [Google Scholar] [CrossRef]

- Ramsey, Frank P. 1931. Truth and probability. In The Foundations of Mathematics and Other Logical Essays. Edited by Richard B. Braithwaite. London: Routledge and Kegan Paul, pp. 156–98. [Google Scholar]

- Rottenstreich, Yuval, and Amos Tversky. 1997. Unpacking, repacking, and anchoring: Advances in support theory. Psychological Review 104: 406–15. [Google Scholar] [CrossRef] [PubMed]

- Samuelson, Paul A. 1938. A note on the pure theory of consumer’s behaviour. Economica 5: 61–71. [Google Scholar] [CrossRef]

- Sarin, Rakesh K., and Peter P. Wakker. 1992. A simple axiomatization of nonadditive expected utility. Econometrica 60: 1255–72. [Google Scholar] [CrossRef]

- Savage, Leonard J. 1972. The Foundations of Statistics, 2nd ed. New York: Wiley and Dover Publications. First published 1954. [Google Scholar]

- Schmeidler, David. 1989. Subjective probability and expected utility without additivity. Econometrica 57: 571–87. [Google Scholar] [CrossRef]

- Shafer, Glenn. 1976. A Mathematical Theory of Evidence. Princeton: The Princeton University Press. [Google Scholar]

- Siniscalchi, Marciano. 2009. Vector expected utility and attitudes toward variation. Econometrica 77: 801–55. [Google Scholar] [CrossRef][Green Version]

- Smith, Vernon L. 1969. Measuring nonmonetary utilities in uncertain choices: The ellsberg urn. Quarterly Journal of Economics 83: 324–29. [Google Scholar] [CrossRef]

- Thaler, Richard H. 2016. Behavioral economics: Past, present, and future. American Economic Review 106: 1577–600. [Google Scholar] [CrossRef]

- Tversky, Amos, and Daniel Kahneman. 1992. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5: 297–323. [Google Scholar] [CrossRef]

- Tversky, Amos, and Derek J. Koehler. 1994. Support theory: A nonextensional representation of subjective probability. Psychological Review 101: 547–67. [Google Scholar] [CrossRef]

- Tversky, Amos, and Peter Wakker. 1995. Risk attitudes and decision weights. Econometrica 63: 1255–80. [Google Scholar] [CrossRef]

- von Neumann, John, and Oskar Morgenstern. 1944. Theory of Games and Economic Behavior. Princeton: Princeton University Press. [Google Scholar]

- von Winterfeldt, Detlof, and Ward Edwards. 1986. Decision Analysis and Behavioural Research: 1. Cambridge: Cambridge University Press. [Google Scholar]

- Wakker, Peter P. 1984. Cardinal coordinate independence for expected utility. Journal of Mathematical Psychology 28: 110–17. [Google Scholar] [CrossRef]

- Wakker, Peter P. 1989. Continuous subjective expected utility with nonadditive probabilities. Journal of Mathematical Economics 18: 1–27. [Google Scholar] [CrossRef]

- Wakker, Peter P. 2000. Luce’s paradigm for decision under uncertainty. Journal of Mathematical Psychology 44: 488–93. [Google Scholar] [CrossRef]

- Wakker, Peter P. 2008. Uncertainty. In The New Palgrave: A Dictionary of Economics. Edited by Lawrence Blume and Steven N. Durlauf. London: The MacMillan Press, vol. 8, pp. 428–39. [Google Scholar]

- Wakker, Peter P. 2010. Prospect Theory: For Risk and Ambiguity. Cambridge: Cambridge University Press. [Google Scholar]

- Wallenius, Jyrki, James S. Dyer, Peter C. Fishburn, Ralph E. Steuer, Stanley Zionts, and Kalyanmoy Deb. 2008. Multiple Criteria Decision Making, Multiattribute Utiliƒty Theory: Recent Accomplishments and What Lies Ahead. Management Science 54: 1336–49. [Google Scholar] [CrossRef]

- Weber, Martin, and Colin F. Camerer. 1987. Recent developments in modelling preferences under risk. OR Spektrum 9: 129–51. [Google Scholar] [CrossRef]

- Winkler, Robert L. 1991. Ambiguity, probability, preference, and decision analysis. Journal of Risk and Uncertainty 4: 285–97. [Google Scholar] [CrossRef]

- Wong, Wing-Keung. 2007. Stochastic dominance and mean–variance measures of profit and loss for business planning and investment. European Journal of Operational Research 182: 829–43. [Google Scholar] [CrossRef]

- Wong, Wing-Keung. 2020. Review on behavioral economics and behavioral finance. Studies in Economics and Finance 37: 625–72. [Google Scholar] [CrossRef]

- Wong, Wing-Keung. 2021. Editorial statement and research ideas for behavioral financial economics in the emerging market. International Journal of Emerging Markets 16: 946–51. [Google Scholar] [CrossRef]

- Wong, Wing-Keung, and Raymond H. Chan. 2008. Prospect and Markowitz stochastic dominance. Annals of Finance 4: 105–29. [Google Scholar] [CrossRef]

- Zadeh, Lotfi A. 1978. Fuzzy sets as a basis for a theory of possibility. Fuzzy Sets and Systems 1: 3–28. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chai, J.; Weng, Z.; Liu, W. Behavioral Decision Making in Normative and Descriptive Views: A Critical Review of Literature. J. Risk Financial Manag. 2021, 14, 490. https://doi.org/10.3390/jrfm14100490

Chai J, Weng Z, Liu W. Behavioral Decision Making in Normative and Descriptive Views: A Critical Review of Literature. Journal of Risk and Financial Management. 2021; 14(10):490. https://doi.org/10.3390/jrfm14100490

Chicago/Turabian StyleChai, Junyi, Zhiquan Weng, and Wenbin Liu. 2021. "Behavioral Decision Making in Normative and Descriptive Views: A Critical Review of Literature" Journal of Risk and Financial Management 14, no. 10: 490. https://doi.org/10.3390/jrfm14100490

APA StyleChai, J., Weng, Z., & Liu, W. (2021). Behavioral Decision Making in Normative and Descriptive Views: A Critical Review of Literature. Journal of Risk and Financial Management, 14(10), 490. https://doi.org/10.3390/jrfm14100490