Abstract

This study examines the moderating effect of firm size on the relationship between innovation and firm performance of small and medium enterprises in 29 countries in Eastern European and Central Asia. The study also investigates whether the impact of innovation in products and processes on firm performance is affected by financial capital. The method applied is partial least square structural equation modelling. The findings indicate that firm size and the financial capital both moderate and mediate the impact of innovation on firm performance, positively or negatively. The findings have implications for decision makers by highlighting the significance of firm size and financial sources when planning to introduce innovations to enhance firm performance.

1. Introduction

Innovation can play a significant role in enhancing economic growth and has the potential to bring about change and create opportunities for every business. A supportive environment in terms of resources and information in the industry 4.0 provides an opportunity for both large-sized firms and small and medium enterprises (SMEs1) in Eastern Europe and Central Asia to use innovative technology to improve firm performance (Andries and Faems 2013). In the digital era, access to technological innovation is generally found globally, including in European and Asian countries. Technological adoption is mainly found in Eastern European SMEs rather than in Central Asian countries where the average number of employees hired in Central Asian firms is lower. (Damaskopoulos and Evgeniou 2003; Purcarea et al. 2013). The literature recognises innovation as a key factor contributing to firm performance. A number of studies analyse the direct effects of innovation on corporate performance (Mustafa and Yaakub 2018; Prange and Pinho 2017; Rosli and Sidek 2013; Ullah 2020; Wang 2016): however, little is known of the mechanisms that underlie firm-level innovation. There is mixed evidence about whether firm size affects firm performance (Andries and Faems 2013; Benfratello et al. 2008; Dooley et al. 2016). Correspondingly, there is still value in a further investigation of whether the size of a firm affects the performance of innovative SMEs. This study aims to contribute to this debate by further exploring the moderating effect of firm size and its impact on the relationship between innovation and the firm performance of SMEs.

SMEs are typically opaque in terms of their financial health as they are not required to present financial statements to the public. To invest in technology and innovation, external finance from banks and financial institutions are the main sources of funding (Benfratello et al. 2008). However, due to a lack of collateral in a majority of SMEs (Duarte et al. 2017), their credit trustworthiness is lower than that of large-sized firms. As a result, many SMEs experience difficulties in accessing financial capital (Calcagnini et al. 2011). A number of scholars have investigated this direct relationship between SMEs’ finance and firm performance, and the results have indicated either positive or negative relationships. However, there are still insufficient studies that examine whether different types of financing in firms with innovation are associated with an improvement in firm performance. In other words, further consideration needs to be given to the ways in which formal and informal financing impacts on the performance of innovative SMEs. The types of innovative activities in SMEs and large firms are different (Dooley et al. 2016), so financial support could affect their firm performance in various ways. Although many studies examine the effect of technology usage and financial resources on SMEs’ performance (Budiarto and Pramudiati 2018), there is an absence of research that focuses on how these two factors impact on firm performance at the same time. Therefore, the second aim of this study is to examine the mediating effect of financing, specifically how financial capital mediates the relationship between innovation and firm performance. This contributes to prior research regarding the mediating effect of different type of finance on the performance of SMEs (Fernandez 2017). This study extends previous research about capital structure in large-sized firms and SMEs, which mostly discuss funding in relation to liability and equity (Revest and Sapio 2012). It also contributes to the literature by showing that firm size is a relevant factor in the financing behaviour of SMEs and their innovation level.

The study uses the Business Environment and Enterprise Performance Survey (BEEPS), which provides cross-country firm-level data for Eastern Europe and Central Asian countries collected in a 2013 survey. The findings of this study contribute to prior research focusing on a single-country level (Sibanda et al. 2018). The current study analyses 12,890 SMEs across Eastern Europe and Central Asian countries in order to provide precise findings to add to the previous literature regarding the broader picture of the impacts of innovation.

The next section of this article explains the development of the research hypotheses. The third section sets out the research methodology and the data analysis method, which is followed by an account of the empirical findings. The article ends with a discussion and a conclusion.

2. Hypotheses Development

2.1. Impacts of Innovation on Firm Performance

Technology usage promotes sustainability, growth (Fowowe 2017) and can facilitate business success (Budiarto and Pramudiati 2018). Various types of innovative developments are associated with different aspects of performance (Saunila 2014). Previous studies mention a positive relationship between the innovation and performance of SMEs (Centobelli et al. 2019; Chege and Wang 2020; Mashal 2018). The impacts of innovation on the performance of a firm can be demonstrated by both financial and non-financial indicators (Mashal 2018). The positive impacts of innovation include the ability to compete with others (Anwar 2018; Conto et al. 2016), financial accessibility (Abdu and Jibir 2018), connection and communication (Radzi et al. 2017), marketing (Adam et al. 2017), and export performance (Azar and Ciabuschi 2017; Love et al. 2016; Prange and Pinho 2017). However, some critics have a different perspective. For example, Karabulut (2015) found that innovation has negative impacts on firm growth. It has also been suggested that a failure to consider the potential negative effects of innovation could eventually impact on the environment and lead to uncontrollable business growth (Laforet 2011). In spite of reservations like these about potential negative impacts, there is strong support in the literature for the positive effects of innovation on firm performance. Based on previous studies, the first research hypothesis is developed as follows.

H1.

Innovation positively affects the performance in small and medium enterprises.

2.2. Impacts of Financial Capital on Firm Performance of SMEs

Financial capital plays an important role in enhancing firm performance (Contessi and De Nicola 2012; Jaradat et al. 2018; Sibanda et al. 2018). Compared with large firms, SMEs obviously invest less in innovative technology and use less sophisticated technical equipment. Difficulty in accessing external finance is the main barrier to adopting technological innovations. The opacity of SMEs regarding their ability to pay back loans creates difficulties when they wish to access financial capital (Berger and Udell 2006). To access external finance from banks and financial institutions, SME owners are normally required to provide collateral as a guarantee for a loan as this signals the financial health of a firm to lenders (Hanedar et al. 2014). Insufficient finance can later generate a decline in firm performance (Jaradat et al. 2018; Sibanda et al. 2018). SMEs are more likely to access financial support for working capital rather than for enhancing firm growth (Fanta 2012). Short-term credit finance supports day-to-day operation (Leonidou et al. 2018). This credit shows the liquidity of a firm and establishes its credit trustworthiness for suppliers. At the same time, asset liquidity is an important determinant of innovation (Pham et al. 2018). From prior studies, finance seems to be the most significant factor relating to firm performance as compared with other barriers.

Regarding the relationship between accessing finance and firm performance, scholars have different opinions. Sibanda et al. (2018) found that there was a negative impact of access to finance on SME firm performance. In contrast, Jaradat et al. (2018) state that financial accessibility constraints are negatively associated with SMEs’ performance. Financial constraints are seen as the main barrier to innovation by SMEs (Božić and Rajh 2016). The constraints include the accessibility of long-term debt and short-term credit for daily operation. Based on the literature, the second hypothesis is developed.

H2.

Financial capital positively affects the performance of small and medium enterprises.

Innovation activities are driven by the availability of finance. Abdu and Jibir (2018) confirm that SMEs’ innovation activities are limited by internal finance. The decrease in the internal finance of a large-sized firm does not lead to a decline in innovative performance, as they can obtain replacement capital from external formal financial institutions. In contrast, SMEs having problems in generating internal finance have a higher probability of a decline in cash flow. Then, they tend to face difficulties in obtaining formal finance from banks and formal financial institutions. Financial constraints are particularly severe in firms with innovative activities (Božić and Rajh 2016).

Some studies indicate a positive relationship between product and process innovation and support in terms of formal finance, which then impacts firm performance (Ayyagari et al. 2010). Lee et al. (2015) demonstrate that innovative firms are more likely than other firms to be turned down for finance, particularly in SMEs in which performance is related to innovative products or services. This is because of the high cost of innovation which is less likely to be spent by SMEs (Santiago et al. 2017). To enhance firm performance, it is suggested that innovative SMEs should try to obtain financial support from either formal or informal institutions, or both (Benfratello et al. 2008). Based on the literature, the third hypothesis is developed as follows.

H3.

Financial capital mediates the relationship between innovation and the performance of small and medium enterprises.

2.3. Impacts of Firm Size on Firm Performance

Innovative activities within the same physical capital structure in SMEs and in large-sized firms are different (Noori et al. 2017). Innovative projects normally involve large fixed costs. Large firms have a greater ability to access external finance to progress research and development (R&D) projects compared with SMEs (Noori et al. 2017; Schumpeter 1942). This capacity can have a positive impact on firm performance (Sachs and McArthur 2002). Large-sized firms and SMEs typically undertake different types of innovative activities. External innovative activities draw on internal resources and external knowledge as well as technological skills. These activities mainly involve improvements to the productivity of a firm. Internal innovation relates to a company’s resources and capabilities that are associated with innovative R&D activities (Kim et al. 2016). The study states that while both external and internal innovative R&D activities impact the performance of large-sized firms, only internal innovative R&D activities affect the performance of SMEs (Kim et al. 2016). Similarly, Mabenge et al. (2020) state that the impact of innovation seems to be stronger in bigger and younger firms. From these statements, the final hypotheses are created as follows.

H4.

Firm size is associated with the performance of small and medium enterprises.

H5.

Firm size moderates the relationship between innovation and the performance of small and medium enterprises.

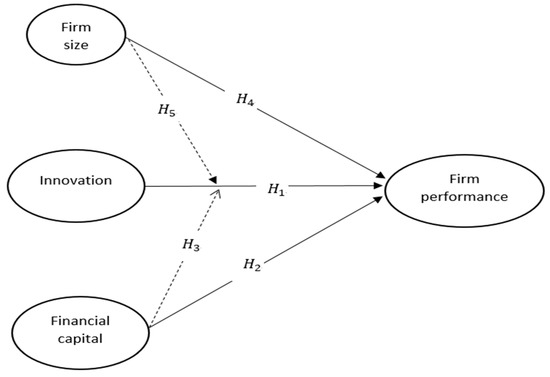

In summary, the five research hypotheses formulated above have been integrated into a research model (Figure 1).

Figure 1.

Research model and hypotheses.

3. Research Methodology

3.1. Samples and Data Collection

The empirical analysis was based on samples of firms across 29 countries in Eastern Europe and Central Asia. This study analyses 12,890 SMEs with 5–99 employees as samples. Data were collected from BEEPS 2013 generated by the World Bank and the European Bank for Reconstruction and Development. The survey comprises various sections including innovation and finance. With the stratified random sampling technique, firms operating in different sectors and geographic region were surveyed. This reduces the selection bias and make samples generalizable.

Descriptive statistics provide an overview of the data. Table 1 illustrates that, overall, medium firms have a higher percentage of both product and process innovation compared with small firms. The main source of finance for small firms is informal finance, (59.27%), which is received from friends and family, whereas for medium firms, the main source is formal finance from banks (45.98%). Additionally, small firms incorporate innovation into their products around two times more than integrating it into the enterprise process. Similar to medium firms, the percentage of product innovation is nearly three times higher than the percentage of process innovation, of 40.8 percent and 14.7 percent, respectively. This could be because technological licences are critical for SMEs to promote their performance. While strategic emphasis on innovative training brings new knowledge and skills to firms, this seems beneficial to human capital rather than corporate performance (Branzei and Vertinsky 2006).

Table 1.

Frequency of innovation and financial capital for all countries.

Descriptive statistics in Table 2 show that approximately half of the sample are small sized firms. The majority of fixed assets in the samples is increased from the previous year. Regarding product innovation, many firms have technological licences in their products. Most firms provide training programmes for staff to improve service quality and the overall management system. On average, about 10 percent of finance is accessed from banks while around 2 percent is by using finance from family and friends. Compared with non-bank finance, SMEs still prefer using bank loans for their operation. Table 3 presents the correlation of latent variables in this study. There is a significant association between the performance of small and medium enterprises and the type of finance accessed. The relationship between firm performance of SMEs and innovation is statistically high. Similarly, the association between financial capital and innovation is found at a significance level of 0.001.

Table 2.

Descriptive statistics for all countries.

Table 3.

Correlation analysis.

3.2. Measures

Firm performance (FP): The endogenous (dependent) variable in this study is firm performance, which captures how well a firm is performing in meeting the multiple financial aspects of business sustainability. Following the measures reported in previous studies of (Wang 2016; Mabenge et al. 2020; Brockman et al. 2012; Jun et al. 2020), firm performance in this study is indicated by total sales and the amount of fixed asset investment. Respondents were asked to indicate the total annual sales in the fiscal year (Sales), and the amount of fixed assets purchased for innovative activities (Fixed_Asset). These two indicators are continuous values.

The exogenous (independent) variable in this study is innovation (Inno). Although some studies use patent (Noori et al. 2017) and R&D expenditure (Lööf and Nabavi 2016; Noori et al. 2017) as proxies of innovation, these two indicators are normally found in large firms rather than SMEs (Gorodnichenko and Schnitzer 2013). This study follows Wellalage and Fernandez (2019), who employed two direct measures of innovation. In this research, the focus is on innovative products and processes. Regarding product innovation, respondents were asked whether their products had a technologically innovative licence. Product_Inno is a dummy variable that takes the value of one if the firms’ products have an innovative licence, and two otherwise. In terms of process innovation, respondents were asked whether their employees are trained in programmes which aim to improve the skills of technology and innovation. Process_Inno is a dummy variable that takes the value of one if the firm has training programmes to improve employees’ technical and innovative skills, and two otherwise.

Financial capital (Fin_Cap): This study captures formal and informal finances for working capital and follows Wellalage and Fernandez (2019) for the proxy used to identify financial capital. Data are taken from survey questions that ask respondents about the proportion of the business’s working capital that was financed from different sources. Formal finance includes loans from banks (state-owned and private) and non-bank institutions. Formal_Fin is a continuous variable presenting as a percentage. Informal finance includes trade credits and loans from friends, families and money lenders. Informal_fin is a continuous variable presenting as a percentage. Table 4 demonstrates measurement of variables.

Table 4.

Measurement of variables.

3.3. Control Variable

The control variables chosen for the analysis are standard in the literature, for instance, as indicated in Adam et al. (2017), Wellalage and Fernandez (2019), Rubera and Kirca (2012), and Guariglia and Liu (2014). Following these examples, the current study controls variables representing firm age and firm type.

3.3.1. Firm Age

Different levels of innovation and financial capital are associated with firm performance differently, particularly when SMEs operate for different time periods. Wellalage and Fernandez (2019) identified SMEs’ finance and innovation, and found a positive relationship between formal financing and innovative products and process. The impact of types of finance is greater for early-stage SMEs than for mature counterparts (Rubera and Kirca 2012). However, informal finance has a more significant impact on mature firms’ product innovation. This contributes to different levels of sales growth and corporate profit (Kerr et al. 2014). Cowling (2006) states that younger firms focus more on the survival of the firm rather than the growth rate. Therefore, the firm age could affect the performance of SMEs if taken into consideration and included into the model.

3.3.2. Firm Type

SMEs which operate in different sectors typically have diverse primary activities, so the ways in which they engage in innovation are not the same. Abdu and Jibir (2018) state that, in terms of the firm sector, manufacturing firms were the most innovative, followed by service firms then retailing firms. For manufacturing SMEs involved in developing products, innovative technology as well as employees’ advanced skills in using tools and machinery may be required. Research and development also play critical roles in promoting new skills and techniques, training, and even the incorporation of raw material in the upstream supply chain. SMEs that operate in the service sector tend to use innovative technology for customer service with the aim of increasing customer satisfaction. Adopting innovation mainly relates to improving staff skills (Gubrium and Holstein 2002). Firms in the retail sector tend to incorporate the benefits of innovative product design from manufacturers and technical skills from the service sector to increase firm performance. Retail firms choose design-driven innovation as a strategy embodied in strategic innovation projects designed to achieve superior performance and gain competitive advantage (Bellini et al. 2017). The various features of SMEs that operate in different sectors in the ways that they engage in technology and innovation may result in a range of possible impacts on their firm performance.

4. Data Analysis

4.1. Reflective Measurement Model Assessment

The study tests the reliability and validity of constructs to ensure the outer (measurement) model is robust (Fornell and Larcker 1981; Hair et al. 2010).

4.1.1. Construct and Indicator Reliability

The indicator’s reliability is evaluated through factor loading between constructs and their items. According to Hair et al. (2016), factor loading estimates should be higher than 0.70. For internal consistency reliability, composite reliability (CR) should be higher than 0.70 (Fornell and Larcker 1981). The results (Table 5) show that all item loadings are higher than the recommended value, suggesting acceptable indicator reliability. The composite reliability varies between 0.709 and 0.854 indicating that the constructs employed have acceptable levels of internal consistency reliability.

Table 5.

Factor loading.

4.1.2. Convergent Validity

To evaluate whether indicators of each latent variable theoretically explain the constructs, the researcher tested convergent validity of the reflective measured constructs (Carmines and Zeller 1979). The convergent validity is evaluated by average variance extracted (AVE), and it should be higher than 0.50 as this indicates that, on average, the construct explains over 50 percent of the variance of its items (Sarstedt et al. 2014). Composite reliabilities for the three reflectively measured constructs ranged from 0.709 to 0.854, exceeding the minimum requirement of 0.70.

4.1.3. Discriminant Validity

Discriminate validity demonstrates the extent to which a construct is categorised from other constructs because of either similarity or difference values (Sarstedt et al. 2014). Fornell and Larcker (1981) and Hair et al. (2010) suggest that the square root of AVE should be higher than inter-construct correlations, and maximum shared variance (MSV) should be lower than AVE. Table 6 demonstrates the Fornell–Larcker test of discriminant validity. This is correspondingly confirmed by cross loadings which are less than all indicator loadings.

Table 6.

Fornell–Larcker test of discriminant validity.

4.2. Structural Model and Hypotheses Testing

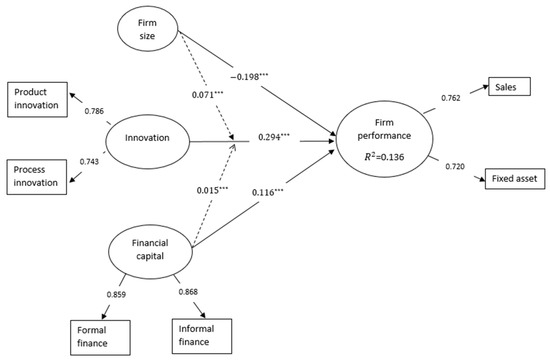

Regarding the inner (structural) model, innovation has the strongest effect on firm performance (path coefficient of 0.304, t-statistics of 24.036), followed by financial capital (path coefficient of 0.122, t-statistics of 10.113). The positive statistical effect shows that the higher the level of innovation, the higher the firm performance. The higher the level of financial capital, the higher the level of firm performance that will result. From the results, hypothesis 1 and 2 are supported.

4.2.1. Structural Model Assessment

The criteria facilitate the structural model assessment including coefficient of determination (R square), cross-validity of redundancy (Q square) and the path coefficients. The empirical finding shows the R-square of 0.117 which mean both innovation and financial capital explain the variance of firm performance of 11.7 percent. We assess the model’s predictive relevance by evaluating the Q square. The smaller the difference between predicted and originated values, the greater the Q square. After running blindfolding, the Q square is above zero for a particular endogenous construct, demonstrating the accuracy in the path model’s prediction (firm performance: 0.063; financial capital: 0.012) (Sarstedt et al. 2014). The strength and significance of the path coefficient are evaluated for the relationships hypothesized between the constructs. After running bootstrapping, we found our path coefficient values to be significant. This is presented by t-statistics which range from −1 to 1. This finding indicates that innovation and financial capital play important roles in driving firm performance with path coefficients of 0.304 and 0.122, respectively. This shows that innovation has a stronger direct effect on firm performance than financial capital.

Additionally, the study focuses on both direct effects and total effects, that is the sum of direct effects and indirect effects between an exogenous and an endogenous construct in the structural model. We further explore whether there is an indirect effect of innovation on firm performance via the mediator financial capital.

4.2.2. Mediating Effect of Financial Capital

To examine the mediating effect of financial capital on the relationship between innovation and firm performance, the direct effect between exogenous latent variables and endogenous latent variables should be significant, as this effect can be seen clearly when correlations between constructs are strong (Zhao et al. 2010). We excluded Fin_Cap from the path model, then ran bootstrap. The result shows standardised path coefficients of indirect effect as 0.015, t-statistic of 6.720, and co-efficiency of total effect as 0.320, t-statistics of 27.591. Table 7 shows that the total effect is statistically significantly stronger than indirect effects, indicating that financial capital is a mediator affecting the relationship between innovation and firm performance. This shows that hypothesis 3 is supported.

Table 7.

Path co-efficient.

4.2.3. Moderating Effect of Firm Size

To investigate the moderating effect of firm size on the relationship between innovation and firm performance, we added the construct indicating firm size (Firm_Size) into the model. The result after running path algorithm shows that firm performance is significantly negatively associated with firm size (beta of −0.198, t-statistics of 13.418). We explore further whether firm size moderates the relationship between innovation and firm performance. The result shows that firm size moderates the relationship between innovation and firm performance (beta = 0.071, t-statistics 6.247). This shows that hypotheses 4 and 5 are supported. This aligns with the studies of Wolff and Pett (2006); Leal-Rodríguez et al. (2015). Compared to medium- and large-sized firms, small firms tend to face resource-constraint problems which makes it critical for them to incorporate the innovation into their products. In terms of flexibility, small firms have the capacity to adapt to their environment and connect with employees, which increases the probability for them to receive innovative ideas (Mintzberg 1979). The higher value of R square (0.123) means that innovation and firm size explain the variance of firm performance of 12.3 percent.

Adding financial capital as the mediator, and firm size as the moderator, produced the R square of 0.136. This means innovation, financial capital and firm size explain the variance of firm performance of 13.6 percent. Table 8 summarizes the hypotheses’ testing results. Figure 2 demonstrates the structural model.

Table 8.

Hypothesis testing results.

Figure 2.

Structural model.

5. Results and Discussion

This study demonstrates the positive effect of innovation on the performance of small and medium enterprises. The findings of this study are consistent with the study Madrid-Guijarro et al. (2013), indicating the capability of SMEs to improve performance and to increase survival rate in the firms using innovation, particularly during high economic development. SMEs embracing innovation in their products and corporate activities tend to survive during recession periods. To generate product innovation, it is important to have both internal and external R&D, as well as to develop employee expertise (Pereira and Leitão 2016).

The findings show financial capital accessed by SMEs also positively impacts their performance. The ability to access financial resources is more critical for firm growth during the economic improvement (Cowling et al. 2018). Formal finance from banks and financial institutes supports SMEs when they invest in technological innovation. The results of this study are aligned with those of Brancati (2015) who further mentions the additional benefits in SMEs accessing bank loans. SMEs can show the soft information indicating their financial health to the banks from their loan relationship and their connections (Berger and Udell 2002). This is then beneficial for firms, particularly for SMEs, to introduce new products and processes to the market. Financial barriers increase the likelihood of failure in SMEs, and push these firms away from innovative projects (García-Quevedo et al. 2018).

Generally, loans or credit finance from banks are one of the choices accessed by SMEs, the cost of using formal finance is relatively low compared to equity finance (Winton and Yerramilli 2008). From an entrepreneurial perspective, SMEs can consider other sources of finance such as crowdfunding, venture capitalists, and business angels. Accessing finance from these channels not only provides lower cost capital, but also gives the opportunity for SMEs to interact with capitalists who can support finance (Van Osnabrugge 2000). Crowdfunding is beneficial to SMEs in presenting innovative products to the public to elicit financial support (Valanciene and Jegeleviciute 2013). Some business angels and venture capitalists are the experts and have specific knowledge, so they can offer mentoring support to SMEs, resulting in increased firm performance (Ramadani 2009). Most of them are interested to invest their money in start-up businesses, particularly those SMEs with a repeatable and scalable business model. Innovation can be used as a strategic tool to enable this model (Richter et al. 2017). The development of an online platform provides SMEs with an opportunity to enlarge their market share and increase their performance. Mature SMEs can use financial bootstrapping to increase their performance, so they face less risk of financial failure (Winborg and Landström 2011).

This study also explores the moderating effects of firm size, and the mediating effect of financial capital on the relationship between innovation and SMEs’ performance. By focusing on product and process innovation, we discover that both moderating and mediating effects are associated with innovative SMEs. This finding contributes to previous studies as it emphasizes the effects of other factors that may increase or decrease the impact of innovative products or services on SMEs’ performance. While the foundation of our conceptual model is innovation, which hypothetically impacts firm performance, a number of studies investigate innovation as a moderator (Donkor et al. 2018) and a mediator (Prange and Pinho 2017) impacting the relationship between many factors and firm performance.

In terms of the role of moderators, it can be seen that the relationship between some factors and firm performance is very weak. This is because those factors impact only slightly on firm performance. The relationship could be stronger when innovation is incorporated into those factors, which could then affect the firm’s performance. (Leal-Rodríguez et al. 2015), recognize the moderating role of firm size in reducing the strong link between organizations promoting awareness of creative perceptions and innovative firm performance. This indicates that the size of a firm is a matter that can influence creative perception in an organization and its performance. Therefore, it will be beneficial to individual firms to consider and take the size of firm into account before investing in innovative projects, products or even adopting innovation to improve their process management.

For a mediating effect, the relationship between independent variables and SME performance will be very strong. If innovation is involved, this could be because innovation acts as the mediator enhancing the impact of those factors on firm performance. According to Omri (2015), a manager’s innovative behaviour can affect innovation output and then impact the enhancement of a firm’s performance. The study found that firm-managing by a manager who has creative ideas can lead to better firm performance.

6. Implications and Conclusions

There are some implications of this study. In terms of samples used, this study provided precise and robust results, especially as this research is the first study which analyses both the direct and indirect impacts of innovation on the performance of SMEs. The study analyses the micro business data collected from BEEPS. Rather than explaining why only enterprises from Eastern Europe and Central Asia are concerned, the study gives an additional explanation of the difference between SMEs from these two continents. The findings of the current research study have several significant policy implications. Policy makers should support SME products gaining the technology licences or even patents which could increase their corporate performance. Some training programmes for staff to embrace innovation to the organization should be provided. Additionally, the findings of this paper suggest that managers take into consideration the differences between the direct and indirect effects of developing a product licence and training programme for improved operation and process management. It is important to pay attention to firm size when incorporating suitable innovative activities. The consideration of suitable activities could relate to types of financial capital and the costs of innovation and technology in relation to business goals. In order to enhance the overall business operation, business owners should also consider the trade-off between cost of financial capital accessed and its benefits, as well as the limitation of firm size.

Although some prior research explores the impacts of innovation on corporate performance (Jorge et al. 2015; Centobelli et al. 2019), few empirical papers have investigated the moderating and mediating effects of firm size and financial capital. Therefore, this paper contributes to the literature by testing the involvement among these factors. The paper extends the literature by further defining the performance of SMEs by including two constructs: fixed asset investment and the number of sales. The appropriate indicators make a precise and robust model.

Further research could explore whether there are other factors that may act as a moderator decreasing the positive impacts of innovation on firm performance, or act as a mediator enhancing performance in innovative SMEs. Additionally, the robustness of this study can be enhanced if other indicators expressing SMEs performance are added, for instance an increase in the number of employees or an increase in firm profit. In terms of innovation, patents could also be considered when investigating innovation in SMEs (Noori et al. 2017).

Author Contributions

Conceptualization, P.K. and P.P.; methodology and analysis, P.K.; writing original draft preparation, P.K.; writing review and editing, P.K.; validation, P.P.; resources, P.P.; visualization, P.P.; supervision, P.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

We are thankful to two anonymous referees for their meaningful comments and constructive suggestions that have improved the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdu, Musa, and Adamu Jibir. 2018. Determinants of firms innovation in Nigeria. Kasetsart Journal of Social Sciences 39: 448–56. [Google Scholar] [CrossRef]

- Adam, Sara, Abeer A. Mahrous, and Wael Kortam. 2017. The relationship between entrepreneurial orientation, marketing innovation and competitive marketing advantage of female entrepreneurs in Egypt. International Journal of Technology Management & Sustainable Development 16: 157–74. [Google Scholar]

- Andries, Petra, and Dries Faems. 2013. Patenting activities and firm performance: Does firm size matter? Journal of Product Innovation Management 30: 1089–98. [Google Scholar] [CrossRef]

- Anwar, Muhammad. 2018. Business model innovation and SMEs performance: Does competitive advantage mediate? International Journal of Innovation Management 22. [Google Scholar] [CrossRef]

- Ayyagari, Meghana, Asli Demirgüç-Kunt, and Vojislav Maksimovic. 2010. Formal versus informal finance: Evidence from China. The Review of Financial Studies 23: 3048–97. [Google Scholar] [CrossRef]

- Azar, Goudarz, and Francesco Ciabuschi. 2017. Organizational innovation, technological innovation, and export performance: The effects of innovation radicalness and extensiveness. International Business Review 26: 324–36. [Google Scholar] [CrossRef]

- Bellini, Emilio, Claudio Dell’Era, Federico Frattini, and Roberto Verganti. 2017. Design-driven innovation in retailing: An empirical examination of new services in car dealership. Creativity and Innovation Management 26: 91–107. [Google Scholar] [CrossRef]

- Benfratello, Luigi, Fabio Schiantarelli, and Alessandro Sembenelli. 2008. Banks and innovation: Microeconometric evidence on Italian firms. Journal of Financial Economics 90: 197–217. [Google Scholar] [CrossRef]

- Berger, A. N., and G. F. Udell. 2002. Small business credit availability and relationship lending: The importance of bank organisational structure. The Economic Journal 112: 32–53. [Google Scholar] [CrossRef]

- Berger, Allen N., and Gregory F. Udell. 2006. A more complete conceptual framework for SME finance. Journal of Banking & Finance 30: 2945–66. [Google Scholar]

- Božić, Ljiljana, and Edo Rajh. 2016. The factors constraining innovation performance of SMEs in Croatia. Economic Research-Ekonomska Istraživanja 29: 314–24. [Google Scholar] [CrossRef]

- Brancati, Emanuele. 2015. Innovation financing and the role of relationship lending for SMEs. Small Business Economics 44: 449–73. [Google Scholar] [CrossRef]

- Branzei, Oana, and Ilan Vertinsky. 2006. Strategic pathways to product innovation capabilities in SMEs. Journal of Business Venturing 21: 75–105. [Google Scholar] [CrossRef]

- Brockman, Beverly K., Michael A. Jones, and Richard C. Becherer. 2012. Customer orientation and performance in small firms: Examining the moderating influence of risk-taking, innovativeness, and opportunity focus. Journal of Small Business Management 50: 429–46. [Google Scholar] [CrossRef]

- Budiarto, Dekeng Setyo, and Ningrum Pramudiati. 2018. Does Technology Improve SMEs Business Success? Empirical Research on Indonesian SMEs. Journal of Economics and Management Sciences 1: 115–21. [Google Scholar] [CrossRef][Green Version]

- Calcagnini, Giorgio, Ilario Favaretto, and Germana Giombini. 2011. Financial Models of Small Innovative Firms: An Empirical Investigation. The Economics of Small Businesses, 151–71. [Google Scholar] [CrossRef]

- Carmines, Edward G., and Richard A. Zeller. 1979. Reliability and Validity Assessment. Ohio: SAGE Publications. [Google Scholar]

- Centobelli, Piera, Roberto Cerchione, and Rajwinder Singh. 2019. The impact of leanness and innovativeness on environmental and financial performance: Insights from Indian SMEs. International Journal of Production Economics 212: 111–24. [Google Scholar]

- Chege, Samwel Macharia, and Daoping Wang. 2020. The influence of technology innovation on SME performance through environmental sustainability practices in Kenya. Technology in Society 60. [Google Scholar] [CrossRef]

- Contessi, Silvio, and Francesca De Nicola. 2012. What Do We Know About the Relationship between Access to Finance and International Trade? Working Paper 2012-054B. St. Louis: FRB. [Google Scholar] [CrossRef]

- Conto, Samuel Martim de, Antunes Júnior José A. Valle, and Guilherme Luís Roehe Vaccaro. 2016. Innovation as a competitive advantage issue: A cooperative study on an organic juice and wine producer. Gestão & Produção 23: 397–407. [Google Scholar]

- Cowling, Marc. 2006. Early stage survival and growth. In Handbook of Entrepreneurship Research: The Life Cycle of Entrepreneurial Ventures. Edited by S. Parker. Berlin: Springer, pp. 477–504. [Google Scholar]

- Cowling, Marc, Weixi Liu, and Ning Zhang. 2018. Did firm age, experience, and access to finance count? SME performance after the global financial crisis. Journal of Evolutionary Economics 28: 77–100. [Google Scholar] [CrossRef]

- Damaskopoulos, Panagiotis, and Theodoros Evgeniou. 2003. Adoption of new economy practices by SMEs in Eastern Europe. European Management Journal 21: 133–45. [Google Scholar] [CrossRef]

- Donkor, Jacob, George Nana Agyekum Donkor, Collins Kankam-Kwarteng, and Eunice Aidoo. 2018. Innovative capability, strategic goals and financial performance of SMEs in Ghana. Asia Pacific Journal of Innovation and Entrepreneurship 12: 238–54. [Google Scholar] [CrossRef]

- Dooley, Lawrence, Breda Kenny, and Michael Cronin. 2016. Interorganizational innovation across geographic and cognitive boundaries: Does firm size matter? RandD Management 46: 227–43. [Google Scholar] [CrossRef]

- Duarte, Fábio Dias, Ana Paula Matias Gama, and José Paulo Esperança. 2017. Collateral-based in SME lending: The role of business collateral and personal collateral in less-developed countries. Research in International Business and Finance 39: 406–22. [Google Scholar] [CrossRef]

- Fanta, Ashenafi Beyene. 2012. Banking reform and SME financing in Ethiopia: Evidence from the manufacturing sector. Journal of Business Management 6: 6057–69. [Google Scholar]

- Fernandez, Viviana. 2017. The finance of innovation in Latin America. International Review of Financial Analysis 53: 37–47. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18: 29–50. [Google Scholar] [CrossRef]

- Fowowe, Babajide. 2017. Access to finance and firm performance: Evidence from African countries. Review of Development Finance 7: 6–17. [Google Scholar] [CrossRef]

- García-Quevedo, José, Agustí Segarra-Blasco, and Mercedes Teruel. 2018. Financial constraints and the failure of innovation projects. Technological Forecasting and Social Change 127: 127–40. [Google Scholar] [CrossRef]

- Gorodnichenko, Yuriy, and Monika Schnitzer. 2013. Financial constraints and innovation: Why poor countries don’t catch up. Journal of the European Economic Association 11: 1115–52. [Google Scholar] [CrossRef]

- Guariglia, Alessandra, and Pei Liu. 2014. To what extent do financing constraints affect Chinese firms’ innovation activities? International Review of Financial Analysis 36: 223–40. [Google Scholar] [CrossRef]

- Gubrium, Jaber F., and James A. Holstein. 2002. Handbook of Interview Research: Context & Method. Thousand Oaks: Sage Publications. [Google Scholar]

- Hair, Joseph F, William C. Black, Barry J Babin, and Rolph E. Anderson. 2010. Multivariate Data Analysis. Upper Saddle River: Prentice Hall. [Google Scholar]

- Hair, Joseph F., Jr., G. Tomas M. Hult, Christian Ringle, and Marko Sarstedt. 2016. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Thousand Oaks: Sage publications. [Google Scholar]

- Hanedar, Elmas Yaldız, Eleonora Broccardo, and Flavio Bazzana. 2014. Collateral requirements of SMEs: The evidence from less-developed countries. Journal of Banking & Finance 38: 106–21. [Google Scholar]

- Jaradat, Zaid AbdulKarim, Roshaiza B. Taha, Rosliza Binti Mat Zin, and Wan Zuriati Wan Zakaria. 2018. The impact of financial accessibility constraints and government regulations on the organisational performance of small-and-medium-sized enterprises. Journal of Business and Retail Management Research 13: 108–20. [Google Scholar] [CrossRef]

- Jorge, Manuel Larrán, Jesús H. Madueno, and Domingo Martinez-Martinez. 2015. Competitiveness and environmental performance in Spanish small and medium enterprises: Is there a direct link? Journal of Cleaner Production 101: 26–37. [Google Scholar] [CrossRef]

- Jun, Jongkun, Thaemin Lee, and Cheol Park. 2020. The mediating role of innovativeness and the moderating effects of strategic choice on SME performance. Journal of Small Business Management, 1–21. [Google Scholar] [CrossRef]

- Karabulut, Ahu Tuğba. 2015. Effects of innovation types on performance of manufacturing firms in Turkey. Procedia-Social and Behavioral Sciences 195: 1355–64. [Google Scholar] [CrossRef]

- Kerr, William R., Ramana Nanda, and Matthew Rhodes-Kropf. 2014. Entrepreneurship as experimentation. The Journal of Economic Perspectives 28: 25–48. [Google Scholar] [CrossRef]

- Kim, Si-jeoung, Eun-mi Kim, Yoonkyo Suh, and ZeKun Zheng. 2016. The effect of service innovation on R&D activities and government support systems: The moderating role of government support systems in Korea. Journal of Open Innovation: Technology, Market, and Complexity 21: 2–5. [Google Scholar]

- Laforet, S. 2011. A framework of organisational innovation and outcomes in SMEs. International Journal of Entrepreneurial Behavior & Research 17: 380–408. [Google Scholar]

- Leal-Rodríguez, Antonio Luis, Stephen Eldridge, José Luis Roldán, Antonio Genaro Leal-Millán, and Jaime Ortega-Gutiérrez. 2015. Organizational unlearning, innovation outcomes, and performance: The moderating effect of firm size. Journal of Business Research 68: 803–9. [Google Scholar] [CrossRef]

- Lee, Neil, Hiba Sameen, and Marc Cowling. 2015. Access to finance for innovative SMEs since the financial crisis. Research Policy 44: 370–80. [Google Scholar] [CrossRef]

- Leonidou, Erasmia, Michael Christofi, Demetris Vrontis, and Alkis Thrassou. 2018. An integrative framework of stakeholder engagement for innovation management and entrepreneurship development. Journal of Business Research. [Google Scholar] [CrossRef]

- Lööf, Hans, and Pardis Nabavi. 2016. Innovation and credit constraints: Evidence from Swedish exporting firms. Economics of Innovation and New Technology 25: 269–82. [Google Scholar] [CrossRef]

- Love, James H., Stephen Roper, and Ying Zhou. 2016. Experience, age and exporting performance in UK SMEs. International Business Review 25: 806–19. [Google Scholar] [CrossRef]

- Mabenge, Blessing Kudzai, Grace Portia Kuda Ngorora-Madzimure, and Charles Makanyeza. 2020. Dimensions of innovation and their effects on the performance of small and medium enterprises: The moderating role of firm’s age and size. Journal of Small Business & Entrepreneurship, 1–25. [Google Scholar] [CrossRef]

- Madrid-Guijarro, A., D. García-Pérez-de-Lema, and H. Van Auken. 2013. An investigation of Spanish SME innovation during different economic conditions. Journal of Small Business Management 51: 578–601. [Google Scholar] [CrossRef]

- Mashal, Antonia. 2018. Do Non-Financial Factors Matter for SME’s Performance? Case from Jordan. International Journal of Business and Social Science 9: 156–67. [Google Scholar]

- Mintzberg, Henry. 1979. The Structuring of Organizations. Englewood Cliffs: Prentice-Hall. [Google Scholar]

- Mustafa, Hamidatun Khusna, and Sabariah Yaakub. 2018. Innovation and technology adoption challenges: Impact on SMEs’ company performance. International Journal of Accounting 3: 57–65. [Google Scholar]

- Noori, Javad, MahdiBagheri Nasrabadi, Najmoddin Yazdi, and Ali Reza Babakhan. 2017. Innovative performance of Iranian knowledge-based firms: Large firms or SMEs? Technological Forecasting and Social Change 122: 179–85. [Google Scholar] [CrossRef]

- OECD. 2017. Enterprise Performance and SME Policies in the Eastern Partner Countries and Peer Regions. Available online: https://www.oecd.org/eurasia/competitiveness-programme/eastern-partners/Enterprise-Performance-and-SME-Policies-in-Eastern-Partner-Countries-and-Peer-Regions.pdf? (accessed on 13 February 2020).

- OEDC. 2018. SME Policy Index: Asean 2018. Retrieved from Paris, France. Available online: https://asean.org/wp-content/uploads/2018/08/Report-ASEAN-SME-Policy-Index-2018.pdf?fbclid=IwAR2ad0sUHbFQo8v-GJTx-eKht_AKd1jonZ8aDTFC8y52uqwsMsjICDtXXUQ (accessed on 18 February 2020).

- Omri, Wale. 2015. Innovative behavior and venture performance of SMEs. European Journal of Innovation Management 18: 195–217. [Google Scholar] [CrossRef]

- Pereira, Dina, and João Leitão. 2016. Absorptive capacity, coopetition and generation of product innovation: Contrasting Italian and Portuguese manufacturing firms. International Journal of Technology Management 71: 10–37. [Google Scholar] [CrossRef]

- Pham, Ly Thi Minh, Lai Van Vo, Huong Thi Thu Le, and Danh Vinh Le. 2018. Asset liquidity and firm innovation. International Review of Financial Analysis 58: 225–34. [Google Scholar] [CrossRef]

- Prange, Christiane, and José Carlos Pinho. 2017. How personal and organizational drivers impact on SME international performance: The mediating role of organizational innovation. International Business Review 26: 1114–23. [Google Scholar] [CrossRef]

- Purcarea, Irina, Maria del Mar Benavides Espinosa, and Andreea Apetrei. 2013. Innovation and knowledge creation: Perspectives on the SMEs sector. Management Decision 51: 1096–107. [Google Scholar] [CrossRef]

- Radzi, Noorhassidah Mohd, Alina Shamsuddin, and Eta Wahab. 2017. Enhancing the competitiveness of Malaysian SMES through technological capability: A perspective. The Social Sciences 12: 719–24. [Google Scholar]

- Ramadani, Veland. 2009. Business angels: Who they really are. Strategic Change: Briefings in Entrepreneurial Finance 18: 249–58. [Google Scholar] [CrossRef]

- Revest, Valérie, and Alessandro Sapio. 2012. Financing technology-based small firms in Europe: What do we know? Small Business Economics 39: 179–205. [Google Scholar] [CrossRef]

- Richter, Chris, Sascha Kraus, Alexander Brem, Susanne Durst, and Clemens Giselbrecht. 2017. Digital entrepreneurship: Innovative business models for the sharing economy. Creativity and Innovation Management 26: 300–10. [Google Scholar] [CrossRef]

- Rosli, M. Mohd, and Syamsuriana Sidek. 2013. The impact of innovation on the performance of small and medium manufacturing enterprises: Evidence from Malaysia. Journal of Innovation Management in Small & Medium Enterprises, 1–16. [Google Scholar] [CrossRef]

- Rubera, Gaia, and Ahmet H. Kirca. 2012. Firm innovativeness and its performance outcomes: A meta-analytic review and theoretical integration. Journal of Marketing 76: 130–47. [Google Scholar] [CrossRef]

- Sachs, Jeffrey D., and John W. McArthur. 2002. Technological advancement and long-term economic growth in Asia. In Technology and the New Economy. Edited by Chong-En Bai and Chi-Wa Yuen. Cambridge: MIT Press, pp. 157–85. [Google Scholar]

- Santiago, Fernando, Claudia De Fuentes, Gabriela Dutrénit, and Natalia Gras. 2017. What hinders innovation performance of services and manufacturing firms in Mexico? Economics of Innovation and New Technology 26: 247–68. [Google Scholar] [CrossRef]

- Sarstedt, Marko, Christian M. Ringle, Donna Smith, Russell Reams, and Joseph F. Hair, Jr. 2014. Partial least squares structural equation modeling (PLS-SEM): A useful tool for family business researchers. Journal of Family Business Strategy 5: 105–15. [Google Scholar] [CrossRef]

- Saunila, Minna. 2014. Innovation capability for SME success: Perspectives of financial and operational performance. Journal of Advances in Management Research 11: 163–75. [Google Scholar] [CrossRef]

- Schumpeter, Joseph A. 1942. Capitalism, Socialism, and Democracy. Rochester: Social Science Research Network. [Google Scholar]

- Sibanda, Kin, Progress Hove-Sibanda, and Herring Shava. 2018. The impact of SME access to finance and performance on exporting behaviour at firm level: A case of furniture manufacturing SMEs in Zimbabwe. Acta Commercii 18: 1–13. [Google Scholar] [CrossRef]

- Ullah, Barkat. 2020. Financial constraints, corruption, and SME growth in transition economies. The Quarterly Review of Economics and Finance 75: 120–32. [Google Scholar] [CrossRef]

- Valanciene, Loreta, and Sima Jegeleviciute. 2013. Valuation of crowdfunding: Benefits and drawbacks. Economics and Management 18: 39–48. [Google Scholar] [CrossRef]

- Van Osnabrugge, Mark. 2000. A comparison of business angel and venture capitalist investment procedures: An agency theory-based analysis. Venture Capital: An International Journal of Entrepreneurial Finance 2: 91–109. [Google Scholar] [CrossRef]

- Wang, Yao. 2016. What are the biggest obstacles to growth of SMEs in developing countries? An empirical evidence from an enterprise survey. Borsa Istanbul Review 16: 167–76. [Google Scholar] [CrossRef]

- Wellalage, Nirosha Hewa, and Viviana Fernandez. 2019. Innovation and SME finance: Evidence from developing countries. International Review of Financial Analysis 66: 101370. [Google Scholar] [CrossRef]

- Winborg, Joakim, and Hans Landström. 2011. Financial bootstrapping in small businesses: Examining small business managers’ resource acquisition behaviors. Journal of Business Venturing 16: 235–54. [Google Scholar] [CrossRef]

- Winton, Andrew, and Vijay Yerramilli. 2008. Entrepreneurial finance: Banks versus venture capital. Journal of Financial Economics 88: 51–79. [Google Scholar] [CrossRef]

- Wolff, James A, and Timothy L. Pett. 2006. Small-firm performance: Modeling the role of product and process improvements. Journal of Small Business Management 44: 268–84. [Google Scholar] [CrossRef]

- Zhao, Xinshu, John G. Lynch, Jr., and Qimei Chen. 2010. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research 37: 197–206. [Google Scholar] [CrossRef]

| 1 | There is no standard for defining SMEs, as the SME definition differs across countries depending on the specific criteria used. According to European Union (EU) criteria, SMEs are the firms having less than 250 employees (OECD 2017) while SMEs in Central Asia are defined differently depending on the size of fixed asset and the number of employees is less than 200 (OEDC 2018). This study follows the definition of SMEs from the Business Environment and Enterprise Performance Survey 2013, cooperatively developed by the World Bank, the European Bank for Reconstruction and Development (EBRD), the European Investment Bank (EIB), and the European Commission (EC) (www.enterprisesurveys.org). SMEs are defined as enterprises which have five to 99 employees. Small firms are firms having five to 19 employees, whereas medium firms are those having 20 to 99 employees. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).