Which Sustainability Dimensions Affect Credit Risk? Evidence from Corporate and Country-Level Measures

Abstract

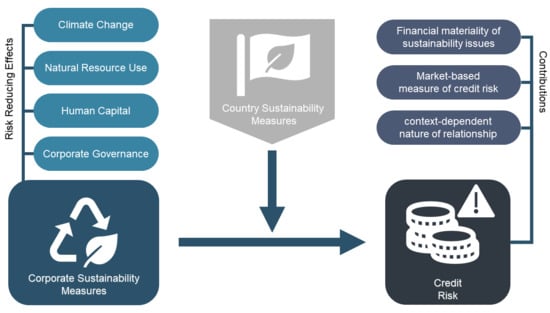

1. Introduction

2. Related Literature and Hypothesis Development

3. Data and Methodology

3.1. Sample Selection

3.2. Variables

3.2.1. Corporate Default Swap (CDS) Spreads

3.2.2. Corporate Social Performance (CSP) Dimensions

3.2.3. Country Sustainability

3.2.4. Control Variables

3.3. Empirical Approach

4. Results

4.1. Preliminary Analysis

4.2. The Effects of Corporate Social Performance (CSP) Dimensions on Credit Risk

4.3. The Effects of Corporate Social Performance (CSP) Dimensions and Country Sustainability on Credit Risk

4.4. Robustness Checks

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Alali, Fatima, Asokan Anandarajan, and Wei Jiang. 2012. The Effect of Corporate Governance on Firm’s Credit Ratings: Further Evidence Using Governance Score in the United States. Accounting & Finance 52: 291–312. [Google Scholar]

- Ali, Saerat, Benjamin Liu, and Jen Je Su. 2018. Does Corporate Governance Quality affect Default Risk? The Role of Growth Opportunities and Stock Liquidity. International Review of Economics and Finance 58: 422–48. [Google Scholar] [CrossRef]

- Amel-Zadeh, Amir, and George Serafeim. 2018. Why and How Investors Use ESG Information: Evidence from a Global Survey. Financial Analysts Journal 74: 87–103. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Olympia Bover. 1995. Another Look at the Instrumental Variable Estimation of Error-Eomponents Models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Ashbaugh-Skaife, Hollis, Daniel W. Collins, and Ryan LaFond. 2006. The Effects of Corporate Governance on Firms’ Credit Ratings. Journal of Accounting and Economics 42: 203–43. [Google Scholar] [CrossRef]

- Attig, Najah, Sadok El Ghoul, Omrane Guedhami, and Jungwon Suh. 2013. Corporate Social Responsibility and Credit Ratings. Journal of Business Ethics 117: 679–94. [Google Scholar] [CrossRef]

- Barnett, Michael L. 2007. Stakeholder Influence Capacity and the Variability of Financial Returns to Corporate Social Responsibility. Academy of Management Review 32: 794–816. [Google Scholar] [CrossRef]

- Bedendo, Mascia, and Paolo Colla. 2015. Sovereign and Corporate Credit Risk: Evidence from the Eurozone. Journal of Corporate Finance 33: 34–52. [Google Scholar] [CrossRef]

- Bhojraj, Sanjeev, and Partha Sengupta. 2003. Effect of Corporate Governance on Bond Ratings and Yields: The Role of Institutional Investors and Outside Directors. Journal of Business 76: 455–75. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Bouslah, Kais, Lawrence Kryzanowski, and Bouchra M’Zali. 2013. The Impact of the Dimensions of Social Performance on Firm Risk. Journal of Banking and Finance 37: 1258–73. [Google Scholar] [CrossRef]

- Brambor, Thomas, William Roberts Clark, and Matt Golder. 2006. Understanding Interaction Models: Improving Empirical Analyses. Political Analysis 14: 63–82. [Google Scholar] [CrossRef]

- Brogaard, Jonathan, Dan Li, and Ying Xia. 2017. Stock liquidity and default risk. Journal of Financial Economics 124: 486–502. [Google Scholar] [CrossRef]

- Campbell, John Y., and Glen B. Taksler. 2003. Equity Volatility and Corporate Bond Yields. Journal of Finance 18: 2321–50. [Google Scholar] [CrossRef]

- Capasso, Giusy, Gianfranco Gianfrate, and Marco Spinelli. 2020. Climate change and credit risk. Journal of Cleaner Production 266: 121634. [Google Scholar] [CrossRef]

- Capelle-Blancard, Gunther, and Petit. 2015. The Weighting of CSR Dimensions: One Size Does Not Fit All. Business & Society 56: 919–43. [Google Scholar]

- Chatterji, Aaron K., David I. Levine, and Michael W. Toffel. 2009. How well do social ratings actually measure corporate social responsibility? Journal of Economics and Management Strategy 18: 125–69. [Google Scholar] [CrossRef]

- Chava, Sudheer. 2014. Environmental Externalities and Cost of Capital. Management Science 60: 2111–380. [Google Scholar] [CrossRef]

- Chen, Huafeng Jason, Marcin Kacperczyk, and Hernan Ortiz-Molina. 2012. Do Nonfinancial Stakeholders Affect the Pricing of Risky Debt? Evidence from Unionized Workers. Review of Finance 16: 347–83. [Google Scholar] [CrossRef]

- Coase, Ronald H. 1934. The Nature of the Firm. Economica 4: 386–405. [Google Scholar] [CrossRef]

- Collin-Dufresne, Pierre, Robert S. Goldstein, and J. Spencer Martin. 2001. The Determinants of Credit Spread Changes. The Journal of Finance 56: 2177–207. [Google Scholar] [CrossRef]

- Corò, Filippo, Alfonso Dufour, and Simeone Varotto. 2013. Credit and Liquidity Components of Corporate CDS Spreads. Journal of Banking and Finance 37: 5511–25. [Google Scholar] [CrossRef]

- Das, Sanjiv R., and Paul Hanouna. 2009. Hedging Credit: Equity Lquidity Matters. Journal of Financial Intermediation 18: 112–23. [Google Scholar] [CrossRef]

- Das, Sanjiv R., Paul Hanouna, and Atulya Sarin. 2009. Accounting-Based versus Market-Based Cross-Sectional Models of CDS Spreads. Journal of Banking and Finance 33: 719–30. [Google Scholar] [CrossRef]

- Drago, Danilo, Concetta Carnevale, and Raffaele Gallo. 2019. Do Corporate Social Responsibility Ratings affect Credit Default Swap Spreads? Corporate Social Responsibility and Environmental Management 26: 644–52. [Google Scholar] [CrossRef]

- Duan, Jin Chuan. 1994. Maximum Likelihood Estimation using Price Data of the Derivative Contract. Mathematical Finance 4: 155–67. [Google Scholar] [CrossRef]

- Duan, Jin Chuan, and Elisabeth Van Laere. 2012. A Public Good Approach to Credit Ratings—From Concept to Reality. Journal of Banking and Finance 36: 3239–47. [Google Scholar] [CrossRef]

- Eccles, Robert G., and Judith C. Stroehle. 2018. Exploring Social Origins in the Construction of ESG Measures. Available online: https://ssrn.com/abstract=3212685 (accessed on 1 June 2020).

- El Ghoul, Sadok, Omrane Guedhami, and Yongtae Kim. 2017. Country-Level Institutions, Firm Value, and the Role of Corporate Social Responsibility Initiatives. Journal of International Business Studies 48: 360–85. [Google Scholar] [CrossRef]

- Fabozzi, Frank J., Steven V. Mann, and Moorad Choudhry. 2003. Measuring and Controlling Interest Rate and Credit Risk. Hoboken: John Wiley & Sons, Ltd. [Google Scholar]

- Ge, Wenxia, and Mingzhi Liu. 2015. Corporate Social Responsibility and the Cost of Corporate Bonds. Journal of Accounting and Public Policy 34: 597–624. [Google Scholar] [CrossRef]

- Girerd-Potin, Isabelle, Sonia Jimenez-Garcès, and Pascal Louvet. 2014. Which Dimensions of Social Responsibility Concern Financial Investors? Journal of Business Ethics 121: 559–76. [Google Scholar] [CrossRef]

- Goss, Allen, and Gordon S. Roberts. 2011. The Impact of Corporate Social Responsibility on the Cost of Bank Loans. Journal of Banking and Finance 35: 1794–810. [Google Scholar] [CrossRef]

- Gutierrez-Nieto, Begona, Carlos Serrano-Cinca, and Juan Camon-Cala. 2016. A Credit Score System for Socially Responsible Lending. Journal of Business Ethics 133: 691–701. [Google Scholar] [CrossRef]

- Hoepner, Andreas, Ioannis Oikonomou, Bert Scholtens, and Michael Schröder. 2016. The Effects of Corporate and Country Sustainability Characteristics on The Cost of Debt: An International Investigation. Journal of Business Finance and Accounting 43: 158–90. [Google Scholar] [CrossRef]

- Huang, Jun, Wei Hu, and Guowei Zhu. 2018. The Effect of Corporate Social Responsibility on Cost of Corporate Bond: Evidence from China. Emerging Markets Finance and Trade 54: 255–68. [Google Scholar] [CrossRef]

- Jiraporn, Pornsit, Napatsorn Jiraporn, Adisak Boeprasert, and Kiyoung Chang. 2014. Does Corporate Social Responsibility (CSR) Improve Credit Ratings? Evidence from Geographic Identification. Financial Management 43: 505–31. [Google Scholar] [CrossRef]

- Jung, Juhyun, Kathleen Herbohn, and Peter Clarkson. 2018. Carbon Risk, Carbon Risk Awareness and the Cost of Debt Financing. Journal of Business Ethics 150: 1151–71. [Google Scholar] [CrossRef]

- Kane, Gregory D., Uma Velury, and Bernadette M. Ruf. 2005. Employee Relations and the Likelihood of Occurrence of Corporate Financial Distress. Journal of Business Finance and Accounting 32: 1083–106. [Google Scholar] [CrossRef]

- Khan, Mozaffar, George Serafeim, and Aaron Yoon. 2016. Corporate Sustainability: First Evidence on Materiality. The Accounting Review 91: 1697–724. [Google Scholar] [CrossRef]

- Kiesel, Florian, and Felix Lücke. 2019. ESG in credit ratings and the impact on financial markets. Financial Markets, Institutions and Instruments 28: 263–90. [Google Scholar] [CrossRef]

- Kim, Moshe, Jordi Surroca, and Josep A. Tribó. 2014. Impact of Ethical Behavior on Syndicated Loan Rates. Journal of Banking and Finance 38: 122–44. [Google Scholar] [CrossRef]

- Klein, Christian, and Cristoph Stellner. 2014. Does sovereign risk matter? New evidence from Eurozone corporate bond ratings and zero-volatility spreads. Review of Financial Economics 23: 64–74. [Google Scholar] [CrossRef]

- Klock, Mark. S., Sattar. A. Mansi, and William F. Maxwell. 2005. Does Corporate Governance Matter to Bondholders? Journal of Financial and Quantitative Analysis 40: 693–719. [Google Scholar] [CrossRef]

- Kölbel, Julian F., Timo Busch, and Leonhardt M. Jansco. 2017. How Media Coverage of Corporate Social Irresponsibility Increases Financial Risk. Strategic Management Journal 38: 2266–84. [Google Scholar] [CrossRef]

- La Rosa, Fabio, Giovanni Liberatore, Francesco Mazzi, and Simeone Terzani. 2018. The impact of corporate social performance on the cost of debt and access to debt financing for listed European non-financial firms. European Management Journal 36: 519–29. [Google Scholar] [CrossRef]

- Lee, Hwang Hee, and Jung-Soon Hyun. 2019. The asymmetric effect of equity volatility on credit default swap spreads. Journal of Banking and Finance 98: 125–36. [Google Scholar] [CrossRef]

- Lee, Jongsub, Andy Naranjo, and Stace Sirmans. 2016. Exodus from Sovereign Risk: Global Asset and Information Networks in the Pricing of Corporate Credit Risk. Journal of Finance 71: 1813–56. [Google Scholar] [CrossRef]

- Longstaff, Francis, Sanjay Mithal, and Eric Neis. 2005. Corporate Yield Spreads: Default Risk or Liquidty? New evidence from the credit default swap market. Journal of Finance 60: 2213–53. [Google Scholar] [CrossRef]

- Magnanelli, Barbara Sveva, and Maria Federica Izzo. 2017. Corporate Social Performance and Cost of debt: The Relationship. Social Responsibility Journal 13: 250–65. [Google Scholar] [CrossRef]

- Mattingly, James E. 2015. Corporate Social Performance: A Review of Empirical Research Examining the Corporation–Society Relationship Using Kinder, Lydenberg, Domini Social Ratings Data. Business and Society 56: 796–839. [Google Scholar] [CrossRef]

- Menz, Klaus Michael. 2010. Corporate Social Responsibility: Is it Rewarded by the Corporate Bond Market? A Critical Note. Journal of Business Ethics 96: 117–34. [Google Scholar] [CrossRef]

- Nandy, Monomita, and Suman Lodh. 2012. Do Banks Value the Eco-Friendliness of Firms in their Corporate Lending Decision? Some Empirical Evidence. International Review of Financial Analysis 25: 83–93. [Google Scholar] [CrossRef]

- Nizam, Esma, Adam Ng, Ginanjar Dewandaru, Ruslan Nagayev, and Malik Abdulrahman Nkoba. 2019. The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector. Journal of Multinational Financial Management 49: 35–53. [Google Scholar] [CrossRef]

- Oikonomou, Ioannis, Chris Brooks, and Stephen Pavelin. 2014. The Effects of Corporate Social Performance on the Cost of Corporate Debt. The Financial Review 49: 49–75. [Google Scholar] [CrossRef]

- Orlitzky, Marc, Frank L. Schmidt, and Sara L. Rynes. 2003. Corporate Social and Financial Performance: A Meta-analysis. Organization Studies 24: 403–41. [Google Scholar] [CrossRef]

- Perrault, Elise, and Michael A. Quinn. 2018. What Have Firms Been Doing? Exploring What KLD Data Report About Firms’ Corporate Social Performance in the Period 2000–10. Business and Society 57: 890–928. [Google Scholar] [CrossRef]

- PRI. 2017. Shifting Perceptions: ESG, Credit Risk and Ratings—Part 1: State of Play. Available online: https://www.unpri.org/download_report/36678 (accessed on 1 June 2020).

- PRI. 2019. Shifting Perceptions: ESG, Credit Risk and Ratings—Part 3: From Disconnects to Action Areas. Available online: https://www.unpri.org/download?ac=5819 (accessed on 1 June 2020).

- Roodman, David. 2009. How to do xtabond2: An Introduction to difference and system GMM in Stata. The Stata Journal 9: 86–136. [Google Scholar] [CrossRef]

- Schaefer, Stephen M., and Ilya A. Strebulaev. 2008. Structural Models of Credit Risk are Useful: Evidence from Hedge Ratios on Corporate Bonds. Journal of Financial Economics 90: 1–19. [Google Scholar] [CrossRef]

- Sharfman, Mark P. 1996. The Construct Validity of the Kinder, Lydenberg & Domini Social Performance Ratings Data. Journal of Business Ethics 15: 287–96. [Google Scholar]

- Sharfman, Mark P., and Chitru S. Fernando. 2008. Environmental Risk Management and the Cost of Capital. Strategic Management Journal 29: 569–92. [Google Scholar] [CrossRef]

- Stellner, Christoph, Christian Klein, and Bernhard Zwergel. 2015. Corporate Social Responsibility and Eurozone Corporate Bonds: The Moderating Role of Country Sustainability. Journal of Banking & Finance 59: 538–49. [Google Scholar]

- Su, Weichieh, Mike W. Peng, Weiqiang Tan, and Yan-Leung Cheung. 2016. The Signaling Effect of Corporate Social Responsibility in Emerging Economies. Journal of Business Ethics 134: 479–91. [Google Scholar] [CrossRef]

- Sun, Wenbin, and Kexiu Cui. 2014. Linking Corporate Social Responsibility to Firm Default Risk. European Management Journal 32: 275–87. [Google Scholar] [CrossRef]

- Surroca, Jordi, Josep A. Tribó, and Sandra A. Waddock. 2010. Corporate Responsibility and Financial Performance: The Role of Intangible Resources. Strategic Management Journal 31: 463–90. [Google Scholar] [CrossRef]

- Tang, Dragon Yongjun, and Hong Yan. 2010. Market Conditions, Default Risk and Credit Spreads. Journal of Banking and Finance 34: 724–34. [Google Scholar] [CrossRef]

- Tolikas, Konstantinos, and Nikolas Topaloglou. 2017. Is default risk priced equally fast in the credit default swap and the stock markets? An empirical investigation. Journal of International Financial Markets, Institutions and Money 51: 39–57. [Google Scholar] [CrossRef]

- UN Environment and World Bank. 2017. Roadmap for a Sustainable Financial System. Available online: http://unepinquiry.org/publication/roadmap-for-asustainable-%0Afinancial-system/ (accessed on 1 June 2020).

- UN. 2019. United Nations Secretary-General’s Roadmap for Financing the 2030 Agenda for Sustainable Development 2019–21. Available online: https://www.un.org/sustainabledevelopment/wp-content/uploads/2019/07/UN-SG-Roadmap-Financing-the-SDGs-July-2019.pdf (accessed on 1 June 2020).

- UNCTAD. 2014. World Investment Report 2014: Investing in the SDGs: An Action Plan. Available online: https://unctad.org/en/PublicationsLibrary/wir2014_en.pdf (accessed on 1 June 2020).

- Utz, Sebastian. 2018. Over-investment or risk mitigation? Corporate social responsibility in Asia-Pacific, Europe, Japan, and the United States. Review of Financial Economics 36: 167–93. [Google Scholar] [CrossRef]

- Verwijmeren, Patrick, and Jeroen Derwall. 2010. Employee Well-being, Firm Leverage, and Bankruptcy Risk. Journal of Banking and Finance 34: 956–64. [Google Scholar] [CrossRef]

- Waddock, Sandra A. 2003. Myths and Realities of Social Investing. Organization and Environment 16: 369–80. [Google Scholar] [CrossRef]

- Williamson, Oliver E. 1985. The Economic Institutions of Capitalism. New York: Free Press. [Google Scholar]

- Windmeijer, Frank. 2005. A Finite Sample Correction for the Variance of Linear Efficient Two-Step GMM Estimators. Journal of Econometrics 126: 25–51. [Google Scholar] [CrossRef]

- Xiao, Chengyong, Qian Wang, Taco van der Vaart, and Dirk Pieter van Donk. 2018. When Does Corporate Sustainability Performance Pay off? The Impact of Country-Level Sustainability Performance. Ecological Economics 146: 325–33. [Google Scholar] [CrossRef]

- Zeidan, Rodrigo, Claudio Boechat, and Angela Fleury. 2015. Developing a Sustainability Credit Score System. Journal of Business Ethics 127: 283–96. [Google Scholar] [CrossRef]

- Zerbib, Olivier David. 2019. The Effect of Pro-Environmental Preferences on Bond Prices: Evidence from Green Bonds. Journal of Banking and Finance 98: 39–60. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Panel A: By Year | n | ||||

| 2013 | 523 | ||||

| 2014 | 518 | ||||

| 2015 | 523 | ||||

| 2016 | 530 | ||||

| Total | 2094 | ||||

| Panel B: By Industry | n | ||||

| Energy | 147 | ||||

| Materials | 257 | ||||

| Industrials | 421 | ||||

| Consumer Discretionary | 443 | ||||

| Consumer Staples | 226 | ||||

| Health Care | 122 | ||||

| Information Technology | 157 | ||||

| Telecommunication Services | 82 | ||||

| Utilities | 156 | ||||

| Real Estate | 83 | ||||

| Total | 2094 | ||||

| Panel C: By Country | n | Country | n | Country | n |

| United States | 956 | Spain | 25 | Austria | 5 |

| Japan | 411 | Finland | 23 | Belgium | 4 |

| France | 130 | Malaysia | 20 | Israel | 4 |

| United Kingdom | 124 | Italy | 18 | New Zealand | 4 |

| Germany | 85 | Brazil | 16 | Norway | 4 |

| Australia | 54 | China | 14 | Portugal | 4 |

| South Korea | 43 | Denmark | 9 | Russia | 4 |

| Hong Kong | 42 | Mexico | 9 | Thailand | 4 |

| Sweden | 35 | Greece | 8 | Philippines | 1 |

| Netherlands | 30 | Singapore | 8 | ||

| Total | 2094 | ||||

| Firm-Level Variables | N | Mean | SD | Minimum | Median | Maximum |

|---|---|---|---|---|---|---|

| CDS | 2094 | 4.43 | 0.79 | 3.02 | 4.32 | 6.80 |

| DTD | 2094 | 6.16 | 2.96 | 0.40 | 5.82 | 14.50 |

| Size | 2094 | 9.57 | 1.22 | 6.74 | 9.54 | 12.31 |

| TD/TA | 2094 | 0.30 | 0.14 | 0.03 | 0.28 | 0.70 |

| ST/LT | 2094 | 0.07 | 0.12 | 0.00 | 0.00 | 0.61 |

| MV/BV | 2094 | 3.40 | 6.26 | −12.18 | 2.06 | 48.46 |

| Margin | 2094 | 12.44 | 9.96 | −10.89 | 10.53 | 54.14 |

| CA/CL | 2094 | 1.45 | 0.74 | 0.35 | 1.29 | 4.71 |

| CASH/TA | 2094 | 0.09 | 0.05 | −0.04 | 0.08 | 0.25 |

| STKVOL | 2094 | 0.28 | 0.10 | 0.13 | 0.26 | 0.65 |

| Climate | 2050 | 7.15 | 2.54 | 0.00 | 7.65 | 10.00 |

| Resource | 1954 | 5.46 | 2.51 | 0.00 | 5.20 | 10.00 |

| WasteMgt | 1937 | 5.93 | 2.45 | 0.00 | 5.98 | 10.00 |

| EnvOpps | 926 | 5.40 | 1.66 | 0.08 | 5.49 | 9.77 |

| HumanCap | 2075 | 4.69 | 1.98 | 0.00 | 4.73 | 10.00 |

| ProdSafe | 1127 | 4.00 | 2.18 | 0.00 | 3.85 | 10.00 |

| SocialOpps | 316 | 5.35 | 1.66 | 0.70 | 5.40 | 9.50 |

| Stakehldr | 33 | 5.67 | 2.16 | 0.80 | 5.80 | 9.60 |

| CorpGov | 2091 | 6.24 | 2.41 | 0.00 | 6.25 | 10.00 |

| BusEthics | 753 | 4.43 | 1.79 | 0.00 | 4.38 | 9.90 |

| Country-Level Variables | ||||||

| YPC | 2094 | 10.71 | 0.31 | 9.15 | 10.82 | 10.94 |

| 2094 | 1.90 | 0.97 | -1.13 | 1.74 | 5.11 | |

| MKTVOL | 2094 | 0.02 | 0.01 | 0.01 | 0.02 | 0.05 |

| Sovereign | 2094 | 3.22 | 0.58 | 2.16 | 3.09 | 5.37 |

| C_ESG | 2094 | 55.41 | 2.78 | 40.94 | 55.84 | 63.63 |

| C_ENV | 2094 | 43.78 | 8.63 | 15.84 | 41.00 | 58.14 |

| C_SOC | 2094 | 52.37 | 3.77 | 38.09 | 50.82 | 65.05 |

| C_GOV | 2094 | 73.94 | 5.94 | 35.25 | 74.34 | 86.79 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | (15) | (16) | (17) | (18) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | CDS | 1 | |||||||||||||||||

| (2) | DTD | −0.429 | 1 | ||||||||||||||||

| (3) | SIZE | −0.491 | 0.479 | 1 | |||||||||||||||

| (4) | TD/TA | 0.237 | −0.125 | −0.144 | 1 | ||||||||||||||

| (5) | ST/LT | −0.155 | −0.038 | −0.018 | −0.129 | 1 | |||||||||||||

| (6) | MV/BV | −0.093 | 0.217 | 0.162 | 0.104 | −0.061 | 1 | ||||||||||||

| (7) | Margin | −0.116 | 0.382 | 0.301 | 0.079 | −0.146 | 0.118 | 1 | |||||||||||

| (8) | CA/CL | 0.008 | 0.110 | −0.081 | −0.247 | 0.006 | −0.038 | 0.051 | 1 | ||||||||||

| (9) | CASH/TA | −0.203 | 0.416 | 0.296 | −0.021 | −0.103 | 0.289 | 0.288 | 0.060 | 1 | |||||||||

| (10) | STKVOL | 0.433 | −0.681 | −0.459 | 0.107 | 0.103 | −0.140 | −0.355 | 0.083 | −0.285 | 1 | ||||||||

| (11) | YPC | −0.215 | 0.110 | 0.046 | −0.007 | −0.019 | 0.088 | −0.089 | −0.040 | 0.059 | −0.078 | 1 | |||||||

| (12) | ΔY | 0.155 | 0.195 | 0.046 | 0.020 | −0.147 | 0.119 | 0.147 | 0.042 | 0.148 | −0.131 | −0.166 | 1 | ||||||

| (13) | STKVOL | −0.126 | −0.184 | −0.110 | 0.001 | 0.144 | −0.100 | −0.135 | 0.027 | −0.150 | 0.215 | −0.024 | −0.440 | 1 | |||||

| (14) | Sovereign | 0.158 | −0.152 | −0.074 | −0.005 | 0.052 | −0.105 | 0.090 | 0.035 | −0.069 | 0.056 | −0.700 | −0.102 | 0.353 | 1 | ||||

| (15) | C_ESG | −0.262 | 0.012 | −0.032 | 0.019 | 0.094 | 0.025 | −0.190 | 0.024 | 0.053 | 0.015 | 0.566 | −0.014 | 0.147 | −0.503 | 1 | |||

| (16) | C_ENV | 0.057 | 0.272 | 0.110 | 0.179 | −0.217 | 0.169 | 0.038 | 0.061 | 0.270 | −0.096 | 0.333 | 0.178 | −0.132 | −0.346 | 0.368 | 1 | ||

| (17) | C_SOC | −0.194 | −0.240 | −0.018 | −0.039 | 0.138 | −0.067 | −0.200 | −0.091 | −0.047 | 0.103 | −0.014 | −0.136 | 0.030 | −0.152 | 0.525 | −0.205 | 1 | |

| (18) | C_GOV | −0.221 | 0.052 | −0.022 | −0.085 | 0.053 | 0.053 | −0.054 | −0.036 | 0.014 | −0.111 | 0.671 | −0.013 | −0.098 | −0.527 | 0.534 | −0.130 | 0.234 | 1 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| CDSit−1 | 0.7343 *** | 0.7378 *** | 0.7545 *** | 0.6137 *** | 0.7503 *** | 0.6858 *** | 0.8746 *** | 0.7414 *** | 0.7038 *** |

| (0.054) | (0.058) | (0.054) | (0.066) | (0.053) | (0.063) | (0.071) | (0.053) | (0.066) | |

| Dimension | −0.0099 *** | −0.0095 *** | −0.0007 | −0.0080 | −0.0140 *** | −0.0020 | −0.0142 | −0.0102 *** | −0.0111 |

| (0.003) | (0.004) | (0.003) | (0.009) | (0.004) | (0.005) | (0.012) | (0.004) | (0.007) | |

| DTD | −0.0063 | −0.0074 | −0.0058 | −0.0067 | −0.0064 | −0.0007 | 0.0054 | −0.0070 | −0.0065 |

| (0.004) | (0.004) | (0.004) | (0.009) | (0.004) | (0.006) | (0.007) | (0.004) | (0.007) | |

| SIZE | −0.0560 *** | −0.0549 *** | −0.0590 *** | −0.0932 *** | −0.0595 *** | −0.0802 *** | −0.0238 | −0.0601 *** | −0.0587 *** |

| (0.012) | (0.013) | (0.012) | (0.018) | (0.012) | (0.018) | (0.022) | (0.012) | (0.016) | |

| TD/TA | 0.2062 *** | 0.1759 ** | 0.2023 *** | 0.2775 ** | 0.1975 *** | 0.3009 *** | 0.2090 | 0.1940 ** | 0.1945 * |

| (0.079) | (0.080) | (0.077) | (0.130) | (0.075) | (0.113) | (0.148) | (0.077) | (0.113) | |

| ST/LT | −0.1336 | −0.1399 | −0.1242 | −0.0449 | −0.0956 | −0.2166 * | −0.1564 | −0.1297 | −0.1741 |

| (0.085) | (0.085) | (0.083) | (0.124) | (0.079) | (0.125) | (0.187) | (0.084) | (0.128) | |

| MV/BV | −0.0014 | −0.0016 | −0.0016 | 0.0028 | −0.0016 | −0.0012 | −0.0007 | −0.0016 * | −0.0039 ** |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.002) | (0.001) | (0.002) | |

| Margin | 0.0019 ** | 0.0018 ** | 0.0016 ** | 0.0035 ** | 0.0016 ** | −0.0007 | 0.0005 | 0.0018 ** | 0.0048 *** |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.003) | (0.001) | (0.001) | |

| CA/CL | 0.0199 ** | 0.0113 | 0.0200 ** | 0.0310 ** | 0.0197 ** | −0.0001 | −0.0101 | 0.0157 | 0.0004 |

| (0.010) | (0.010) | (0.010) | (0.015) | (0.009) | (0.015) | (0.028) | (0.010) | (0.018) | |

| CASH/TA | 0.2647 | 0.4228 ** | 0.4476 ** | −0.1913 | 0.3956 ** | −0.1390 | −0.4536 | 0.3429 * | 0.2986 |

| (0.188) | (0.187) | (0.181) | (0.303) | (0.180) | (0.273) | (0.381) | (0.182) | (0.297) | |

| STKVOL | 0.5275 *** | 0.5324 *** | 0.4804 *** | 0.5752 ** | 0.4853 *** | 0.7309 *** | 0.4527 | 0.5156 *** | 0.8847 *** |

| (0.179) | (0.192) | (0.173) | (0.284) | (0.175) | (0.218) | (0.404) | (0.178) | (0.249) | |

| YPC | −0.0562 * | −0.0504 | −0.0659 * | −0.1937 *** | −0.0351 | −0.0108 | 0.0364 | −0.0512 * | −0.0374 |

| (0.032) | (0.037) | (0.039) | (0.070) | (0.029) | (0.060) | (0.078) | (0.030) | (0.046) | |

| ΔY | 0.0226 *** | 0.0180 ** | 0.0234 *** | 0.0449 *** | 0.0232 *** | 0.0269 ** | −0.0198 | 0.0277 *** | 0.0351 *** |

| (0.008) | (0.008) | (0.008) | (0.014) | (0.008) | (0.013) | (0.022) | (0.008) | (0.012) | |

| MKTVOL | −10.8673 *** | −11.1249 *** | −11.0446 *** | −12.3092 *** | −10.4142 *** | −13.4127 *** | −7.8630 ** | −10.4184 *** | −8.5336 *** |

| (1.821) | (2.093) | (1.953) | (2.331) | (1.796) | (2.045) | (3.380) | (1.803) | (1.919) | |

| Sovereign | 0.0231 | 0.0205 | 0.0190 | 0.0308 | 0.0232 | 0.0771 *** | 0.0797 ** | 0.0219 | 0.0102 |

| (0.020) | (0.021) | (0.020) | (0.035) | (0.019) | (0.028) | (0.040) | (0.019) | (0.025) | |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 2.2429 *** | 2.1687 *** | 2.2376 *** | 4.4784 *** | 1.9650 *** | 2.0377 ** | 0.2137 | 2.1963 *** | 2.0080 *** |

| (0.546) | (0.601) | (0.625) | (0.987) | (0.506) | (0.920) | (1.042) | (0.535) | (0.759) | |

| # of Observations | 2050 | 1954 | 1937 | 926 | 2075 | 1127 | 316 | 2091 | 753 |

| # of Firms | 582 | 557 | 548 | 266 | 589 | 349 | 98 | 591 | 223 |

| # of Instruments | 27 | 27 | 27 | 27 | 27 | 27 | 27 | 27 | 27 |

| Hansen Test | 0.1158 | 0.3209 | 0.3192 | 0.0835 | 0.2971 | 0.4585 | 0.4712 | 0.3043 | 0.0878 |

| AR (1) | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| AR (2) | 0.4981 | 0.4067 | 0.8176 | 0.2521 | 0.2926 | 0.5421 | 0.6142 | 0.3460 | 0.4690 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| CDSit−1 | 0.7330 *** | 0.7359 *** | 0.7515 *** | 0.6105 *** | 0.7458 *** | 0.6676 *** | 0.8762 *** | 0.7330 *** | 0.7411 *** |

| (0.056) | (0.060) | (0.058) | (0.063) | (0.055) | (0.061) | (0.069) | (0.055) | (0.058) | |

| C_ESG | −0.0365 *** | −0.0166 ** | −0.0214 ** | −0.0435 ** | −0.0214 *** | −0.0238 ** | 0.0253 | −0.0310 *** | −0.0304 *** |

| (0.010) | (0.008) | (0.010) | (0.018) | (0.008) | (0.011) | (0.018) | (0.010) | (0.010) | |

| Dimension | −0.1685 *** | −0.0253 | −0.0713 | −0.1692 | −0.0994 * | −0.0545 | 0.1381 | −0.1483 ** | −0.2010 * |

| (0.058) | (0.058) | (0.064) | (0.135) | (0.055) | (0.094) | (0.146) | (0.060) | (0.103) | |

| Interaction | 0.0029 *** | 0.0003 | 0.0013 | 0.0030 | 0.0016 | 0.0009 | −0.0027 | 0.0025 ** | 0.0035 * |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.002) | (0.003) | (0.001) | (0.002) | |

| DTD | −0.0086 * | −0.0095 * | −0.0077 | −0.0058 | −0.0081 * | −0.0038 | 0.0067 | −0.0090 * | −0.0045 |

| (0.005) | (0.005) | (0.005) | (0.008) | (0.005) | (0.006) | (0.007) | (0.005) | (0.006) | |

| Size | −0.0568 *** | −0.0560 *** | −0.0600 *** | −0.0966 *** | −0.0602 *** | −0.0855 *** | −0.0219 | −0.0625 *** | −0.0553 *** |

| (0.012) | (0.013) | (0.013) | (0.018) | (0.013) | (0.018) | (0.022) | (0.013) | (0.015) | |

| TD/TA | 0.2197 *** | 0.1936 ** | 0.2132 ** | 0.3322 ** | 0.2169 *** | 0.3385 *** | 0.2272 | 0.2113 *** | 0.2328 ** |

| (0.083) | (0.085) | (0.083) | (0.135) | (0.079) | (0.117) | (0.149) | (0.081) | (0.117) | |

| ST/LT | −0.0934 | −0.1096 | −0.0973 | 0.0317 | −0.0665 | −0.1913 | −0.1689 | −0.0832 | −0.0835 |

| (0.079) | (0.079) | (0.079) | (0.112) | (0.074) | (0.121) | (0.190) | (0.077) | (0.111) | |

| MV/BV | −0.0015 | −0.0018 | −0.0017 | 0.0030 | −0.0017 * | −0.0012 | −0.0006 | −0.0017 * | −0.0033 * |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.002) | (0.001) | (0.002) | |

| Margin | 0.0016 * | 0.0014 * | 0.0013 | 0.0015 | 0.0011 | −0.0012 | −0.0001 | 0.0014 * | 0.0036 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.003) | (0.001) | (0.001) | |

| CA/CL | 0.0216 ** | 0.0156 | 0.0218 ** | 0.0291 ** | 0.0225 ** | 0.0035 | −0.0093 | 0.0186 ** | 0.0024 |

| (0.009) | (0.009) | (0.009) | (0.014) | (0.009) | (0.014) | (0.027) | (0.009) | (0.016) | |

| CASH/TA | 0.3234 * | 0.5065 *** | 0.5167 *** | 0.0556 | 0.4883 *** | −0.0357 | −0.4643 | 0.3966 ** | 0.5265 * |

| (0.185) | (0.182) | (0.177) | (0.287) | (0.176) | (0.267) | (0.397) | (0.180) | (0.286) | |

| STKVOL | 0.4774 *** | 0.5073 *** | 0.4674 *** | 0.5951 ** | 0.4680 *** | 0.7451 *** | 0.4564 | 0.5101 *** | 0.7515 *** |

| (0.175) | (0.189) | (0.174) | (0.268) | (0.174) | (0.221) | (0.393) | (0.177) | (0.239) | |

| YPC | 0.0119 | 0.0002 | −0.0069 | −0.0813 | 0.0111 | 0.0501 | 0.0250 | 0.0056 | 0.0321 |

| (0.035) | (0.040) | (0.043) | (0.076) | (0.031) | (0.060) | (0.078) | (0.032) | (0.042) | |

| ΔY | 0.0286 *** | 0.0258 *** | 0.0297 *** | 0.0495 *** | 0.0293 *** | 0.0358 ** | −0.0277 | 0.0343 *** | 0.0368 *** |

| (0.009) | (0.009) | (0.009) | (0.014) | (0.009) | (0.015) | (0.021) | (0.009) | (0.013) | |

| MKTVOL | −9.5820 *** | −9.3960 *** | −9.4418 *** | −10.0426 *** | −9.1626 *** | −11.5012 *** | −9.4207 *** | −9.4259 *** | −7.1737 *** |

| (1.572) | (1.747) | (1.695) | (2.184) | (1.540) | (1.928) | (3.297) | (1.621) | (1.880) | |

| Sovereign | 0.0009 | −0.0066 | −0.0053 | −0.0279 | −0.0034 | 0.0322 | 0.0969 ** | −0.0042 | −0.0218 |

| (0.019) | (0.019) | (0.019) | (0.032) | (0.018) | (0.032) | (0.045) | (0.018) | (0.025) | |

| Year Effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 3.6038 *** | 2.6026 *** | 2.8554 *** | 5.8183 *** | 2.7273 *** | 2.9257 *** | −1.1193 | 3.4241 *** | 2.7919 *** |

| (0.795) | (0.720) | (0.801) | (1.307) | (0.695) | (1.123) | (1.668) | (0.818) | (0.955) | |

| # of Observations | 2050 | 1954 | 1937 | 926 | 2075 | 1127 | 316 | 2091 | 753 |

| # of Firms | 582 | 557 | 548 | 266 | 589 | 349 | 98 | 591 | 223 |

| # of Instruments | 29 | 29 | 29 | 29 | 29 | 29 | 29 | 29 | 29 |

| Hansen Test | 0.0806 | 0.2625 | 0.2175 | 0.0705 | 0.2593 | 0.6357 | 0.4667 | 0.2800 | 0.0360 |

| AR (1) | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| AR (2) | 0.4258 | 0.3591 | 0.8952 | 0.3436 | 0.2498 | 0.4381 | 0.6120 | 0.3013 | 0.4381 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| CDSit−1 | 0.7224 *** | 0.7250 *** | 0.7318 *** | 0.6124 *** | 0.7359 *** | 0.6635 *** | 0.8594 *** | 0.7389 *** | 0.7151 *** |

| (0.056) | (0.059) | (0.056) | (0.071) | (0.055) | (0.062) | (0.077) | (0.052) | (0.062) | |

| C_ENV | 0.0094 *** | 0.0097 *** | 0.0097 *** | 0.0026 | |||||

| (0.003) | (0.003) | (0.003) | (0.005) | ||||||

| C_SOC | −0.0154 *** | −0.0139 * | −0.0216 | ||||||

| (0.005) | (0.007) | (0.021) | |||||||

| C_GOV | −0.0114 *** | −0.0127 ** | |||||||

| (0.004) | (0.005) | ||||||||

| Dimension | 0.0164 | 0.0343 * | 0.0327 ** | −0.0150 | −0.0186 | 0.0464 | −0.1941 | −0.0768 ** | −0.1316 * |

| (0.018) | (0.019) | (0.016) | (0.041) | (0.041) | (0.064) | (0.169) | (0.033) | (0.074) | |

| Interaction | −0.0005 | −0.0009 ** | −0.0007 * | 0.0002 | 0.0002 | −0.0009 | 0.0033 | 0.0009 ** | 0.0016 |

| (0.000) | (0.000) | (0.000) | (0.001) | (0.001) | (0.001) | (0.003) | (0.000) | (0.001) | |

| DTD | −0.0117 ** | −0.0120 ** | −0.0109 ** | −0.0116 | −0.0146 *** | −0.0094 | 0.0034 | −0.0087 * | −0.0054 |

| (0.005) | (0.005) | (0.005) | (0.011) | (0.005) | (0.006) | (0.007) | (0.005) | (0.006) | |

| Size | −0.0611 *** | −0.0575 *** | −0.0632 *** | −0.0907 *** | −0.0577 *** | −0.0805 *** | −0.0308 | −0.0636 *** | −0.0643 *** |

| (0.012) | (0.013) | (0.012) | (0.018) | (0.012) | (0.017) | (0.025) | (0.012) | (0.016) | |

| TD/TA | 0.1538 ** | 0.1345 * | 0.1602 ** | 0.2049 | 0.1914 *** | 0.3166 *** | 0.1720 | 0.1720 ** | 0.1849 |

| (0.074) | (0.075) | (0.073) | (0.125) | (0.074) | (0.111) | (0.151) | (0.073) | (0.112) | |

| ST/LT | −0.0827 | −0.0967 | −0.0857 | −0.0147 | −0.0596 | −0.1695 | −0.1666 | −0.0885 | −0.1311 |

| (0.082) | (0.080) | (0.080) | (0.127) | (0.076) | (0.118) | (0.200) | (0.079) | (0.122) | |

| MV/BV | −0.0014 | −0.0017 | −0.0017 | 0.0021 | −0.0017 * | −0.0013 | −0.0006 | −0.0016 * | −0.0034 * |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.002) | (0.001) | (0.002) | |

| Margin | 0.0023 *** | 0.0022 *** | 0.0019 ** | 0.0043 *** | 0.0012 | −0.0014 | 0.0019 | 0.0019 ** | 0.0051 *** |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.003) | (0.001) | (0.001) | |

| CA/CL | 0.0157 | 0.0086 | 0.0159 | 0.0335 ** | 0.0163 * | −0.0061 | −0.0193 | 0.0156 | −0.0016 |

| (0.010) | (0.011) | (0.010) | (0.016) | (0.009) | (0.015) | (0.032) | (0.010) | (0.017) | |

| CASH/TA | 0.1160 | 0.3081 | 0.2587 | −0.3635 | 0.4930 *** | 0.0347 | −0.5638 | 0.3027 | 0.2541 |

| (0.201) | (0.196) | (0.197) | (0.335) | (0.176) | (0.256) | (0.458) | (0.184) | (0.290) | |

| STKVOL | 0.4689 *** | 0.4991 *** | 0.4812 *** | 0.5644 * | 0.4323 ** | 0.6959 *** | 0.4554 | 0.4729 *** | 0.8470 *** |

| (0.174) | (0.187) | (0.173) | (0.289) | (0.171) | (0.216) | (0.409) | (0.169) | (0.239) | |

| YPC | −0.0971 *** | −0.0957 *** | −0.1168 *** | −0.2267 *** | −0.1030 *** | −0.1043 | 0.0209 | 0.0297 | 0.0826 |

| (0.031) | (0.035) | (0.037) | (0.075) | (0.033) | (0.064) | (0.080) | (0.036) | (0.051) | |

| ΔY | 0.0177 ** | 0.0162 ** | 0.0194 ** | 0.0413 *** | 0.0169 ** | 0.0160 | −0.0199 | 0.0314 *** | 0.0357 *** |

| (0.008) | (0.008) | (0.008) | (0.015) | (0.008) | (0.014) | (0.022) | (0.008) | (0.012) | |

| MKTVOL | −10.8221 *** | −11.4893 *** | −11.6094 *** | −12.5057 *** | −9.9901 *** | −12.8498 *** | −8.0197 ** | −10.8015 *** | −9.8122 *** |

| (1.799) | (2.117) | (1.976) | (2.355) | (1.745) | (1.982) | (3.450) | (1.880) | (2.074) | |

| Sovereign | 0.0328 | 0.0287 | 0.0315 | 0.0443 | −0.0192 | 0.0142 | 0.0857 * | 0.0142 | 0.0096 |

| (0.021) | (0.022) | (0.022) | (0.037) | (0.019) | (0.031) | (0.047) | (0.018) | (0.025) | |

| Year Effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 2.3949 *** | 2.3395 *** | 2.5175 *** | 4.7127 *** | 3.7316 *** | 4.1352 *** | 1.6888 | 2.2646 *** | 1.7090 ** |

| (0.553) | (0.607) | (0.623) | (1.051) | (0.811) | (1.283) | (1.960) | (0.522) | (0.731) | |

| # of Observations | 2050 | 1954 | 1937 | 926 | 2075 | 1127 | 316 | 2091 | 753 |

| # of Firms | 582 | 557 | 548 | 266 | 589 | 349 | 98 | 591 | 223 |

| # of Instruments | 29 | 29 | 29 | 29 | 29 | 29 | 29 | 29 | 29 |

| Hansen Test | 0.1092 | 0.3834 | 0.4409 | 0.0492 | 0.2482 | 0.6428 | 0.4554 | 0.3411 | 0.0949 |

| AR (1) | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| AR (2) | 0.5133 | 0.4213 | 0.8282 | 0.2419 | 0.2048 | 0.4070 | 0.7006 | 0.3301 | 0.5004 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abdul Razak, L.; Ibrahim, M.H.; Ng, A. Which Sustainability Dimensions Affect Credit Risk? Evidence from Corporate and Country-Level Measures. J. Risk Financial Manag. 2020, 13, 316. https://doi.org/10.3390/jrfm13120316

Abdul Razak L, Ibrahim MH, Ng A. Which Sustainability Dimensions Affect Credit Risk? Evidence from Corporate and Country-Level Measures. Journal of Risk and Financial Management. 2020; 13(12):316. https://doi.org/10.3390/jrfm13120316

Chicago/Turabian StyleAbdul Razak, Lutfi, Mansor H. Ibrahim, and Adam Ng. 2020. "Which Sustainability Dimensions Affect Credit Risk? Evidence from Corporate and Country-Level Measures" Journal of Risk and Financial Management 13, no. 12: 316. https://doi.org/10.3390/jrfm13120316

APA StyleAbdul Razak, L., Ibrahim, M. H., & Ng, A. (2020). Which Sustainability Dimensions Affect Credit Risk? Evidence from Corporate and Country-Level Measures. Journal of Risk and Financial Management, 13(12), 316. https://doi.org/10.3390/jrfm13120316