CO2 Emissions, Energy Consumption, and Economic Growth: New Evidence in the ASEAN Countries

Abstract

1. Introduction

2. Literature Review

2.1. The Environmental Kuznets Curve (EKC) Hypothesis

2.2. The Causal Link between Renewable Energy Use, Economic Growth, and Environmental Degradation

3. Methodology

3.1. Model Specification and Data Source

3.2. Cointegration Tests

3.3. Granger-Causality Test

4. Empirical Results and Discussions

4.1. Results of Unit-Root and Cointegration Tests

4.2. Results of Long-Run Relationship

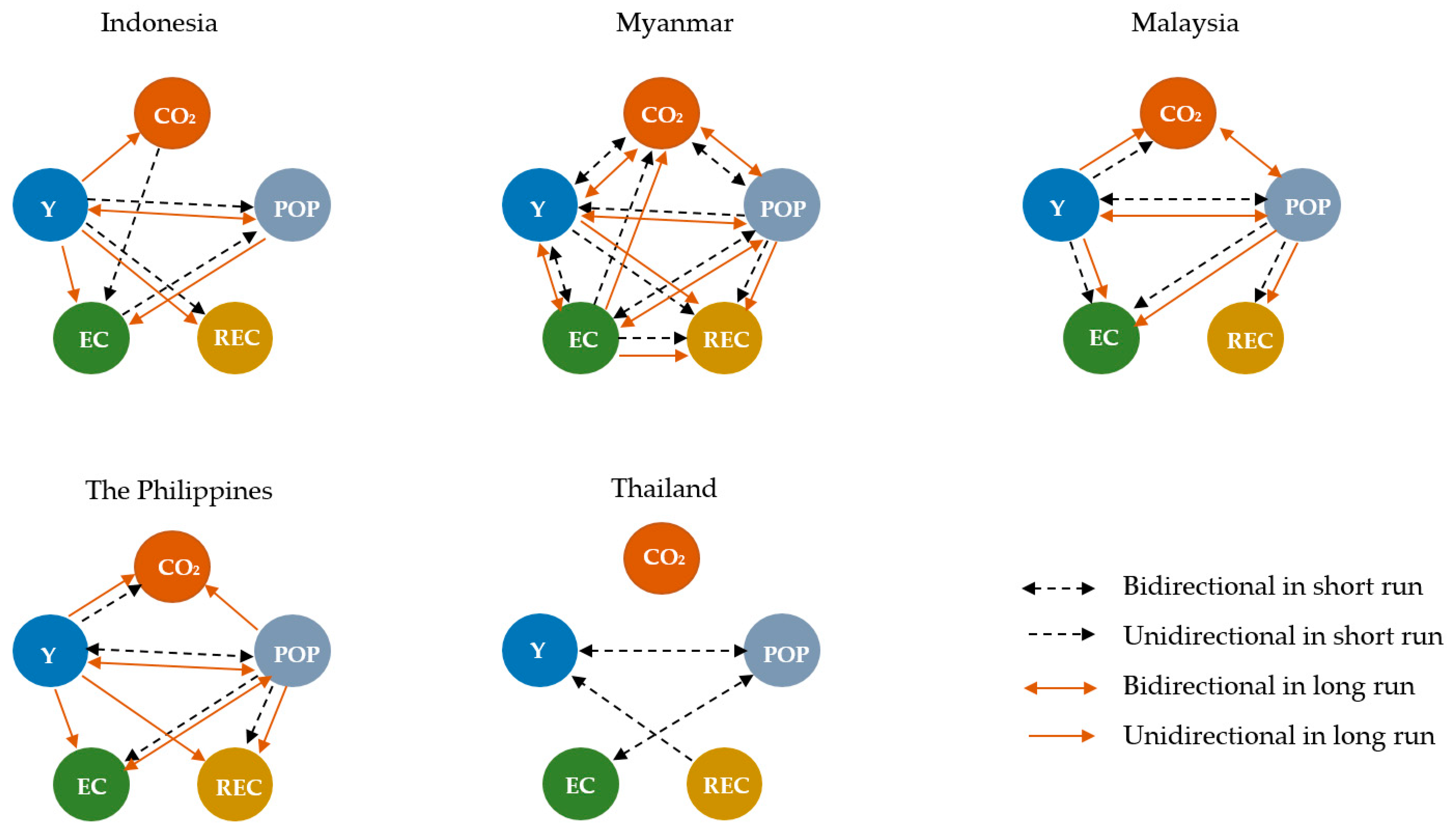

4.3. Results of Granger-Causality Tests

5. Concluding Remarks and Policy Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Ali, Wajahat, Azrai Abdullah, and Muhammad Azam. 2017. Re-visiting the environmental Kuznets curve hypothesis for Malaysia: Fresh evidence from ARDL bounds testing approach. Renewable and Sustainable Energy Reviews 77: 990–1000. [Google Scholar] [CrossRef]

- Al-Mulali, Usama, Behnaz Saboori, and Ilhan Ozturk. 2015. Investigating the environmental Kuznets curve hypothesis in Vietnam. Energy Policy 76: 123–31. [Google Scholar] [CrossRef]

- Ang, James B. 2008. Economic development, pollutant emissions and energy consumption in Malaysia. Journal of Policy Modeling 30: 271–78. [Google Scholar] [CrossRef]

- Apergis, Nicholas, and James E. Payne. 2014. Renewable energy, output, CO2 emissions, and fossil fuel prices in Central America: Evidence from a nonlinear panel smooth transition vector error correction model. Energy Economics 42: 226–32. [Google Scholar] [CrossRef]

- Apergis, Nicholas, James E. Payne, Kojo Menyah, and Yemane Wolde-Rufael. 2010. On the causal dynamics between emissions, nuclear energy, renewable energy, and economic growth. Ecological Economics 69: 2255–60. [Google Scholar] [CrossRef]

- Arouri, Mohamed El Hedi, Adel Ben Youssef, Hatem M’henni, and Christophe Rault. 2012. Energy consumption, economic growth and CO2 emissions in Middle East and North African countries. Energy Policy 45: 342–49. [Google Scholar] [CrossRef]

- Azam, Muhammad, Abdul Qayyum Khan, B. Bakhtyar, and Chandra Emirullah. 2015. The causal relationship between energy consumption and economic growth in the ASEAN-5 countries. Renewable and Sustainable Energy Reviews 47: 732–45. [Google Scholar] [CrossRef]

- Azomahou, Theophile, François Laisney, and Phu Nguyen Van. 2006. Economic development and CO2 emissions: A nonparametric panel approach. Journal of Public Economics 90: 1347–63. [Google Scholar] [CrossRef]

- Begum, Rawshan Ara, Kazi Sohag, Sharifah Mastura Syed Abdullah, and Mokhtar Jaafar. 2015. CO2 emissions, energy consumption, economic and population growth in Malaysia. Renewable and Sustainable Energy Reviews 41: 594–601. [Google Scholar] [CrossRef]

- Bekhet, Hussain Ali, and Nor Salwati Othman. 2018. The role of renewable energy to validate dynamic interaction between CO2 emissions and GDP toward sustainable development in Malaysia. Energy Economics 72: 47–61. [Google Scholar] [CrossRef]

- Belaid, Fateh, and Meriem Youssef. 2017. Environmental degradation, renewable and non-renewable electricity consumption, and economic growth: Assessing the evidence from Algeria. Energy Policy 102: 277–87. [Google Scholar] [CrossRef]

- Bento, João Paulo Cerdeira, and Victor Moutinho. 2016. CO2 emissions, non-renewable and renewable electricity production, economic growth, and international trade in Italy. Renewable and Sustainable Energy Reviews 55: 142–55. [Google Scholar] [CrossRef]

- Bilgili, Faik, Emrah Koçak, and Umit Bulut. 2016. The dynamic impact of renewable energy consumption on CO2 emissions: A revisited Environmental Kuznets Curve approach. Renewable and Sustainable Energy Reviews 54: 838–45. [Google Scholar] [CrossRef]

- De Grauwe, Paul, and Zhaoyong Zhang. 2016. The rise of China and regional integration in East Asia. Scottish Journal of Political Economy 63: 1–6. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Dogan, Eyup, and Ilhan Ozturk. 2017. The influence of renewable and non-renewable energy consumption and real income on CO2 emissions in the USA: Evidence from structural break tests. Environmental Science and Pollution Research 24: 10846–54. [Google Scholar] [CrossRef] [PubMed]

- Dogan, Eyup, and Fahri Seker. 2016. Determinants of CO2 emissions in the European Union: The role of renewable and non-renewable energy. Renewable Energy 94: 429–39. [Google Scholar] [CrossRef]

- Dogan, Eyup, and Berna Turkekul. 2016. CO2 emissions, real output, energy consumption, trade, urbanization and financial development: Testing the EKC hypothesis for the USA. Environmental Science and Pollution Research 23: 1203–13. [Google Scholar] [CrossRef]

- Dong, Kangyin, Renjin Sun, and Gal Hochman. 2017. Do natural gas and renewable energy consumption lead to less CO2 emission? Empirical evidence from a panel of BRICS countries. Energy 141: 1466–78. [Google Scholar] [CrossRef]

- Dong, Kangyin, Gal Hochman, Yaqing Zhang, Renjin Sun, Hui Li, and Hua Liao. 2018. CO2 emissions, economic and population growth, and renewable energy: Empirical evidence across regions. Energy Economics 75: 180–92. [Google Scholar] [CrossRef]

- Elliott, Graham, Thomas J. Rothenberg, and James H. Stock. 1996. Efficient tests for an autoregressive unit root. Econometrica 64: 813–36. [Google Scholar] [CrossRef]

- Fakih, Ali, and Walid Marrouch. 2019. Environmental Kuznets Curve, a Mirage? A Non-parametric Analysis for MENA Countries. International Advances in Economic Research 25: 113–19. [Google Scholar] [CrossRef]

- Gill, Abid Rashid, Kuperan K. Viswanathan, and Sallahuddin Hassan. 2018. A test of environmental Kuznets curve (EKC) for carbon emission and potential of renewable energy to reduce green house gases (GHG) in Malaysia. Environment, Development and Sustainability 20: 1103–14. [Google Scholar] [CrossRef]

- Halicioglu, Ferda, and Natalya Ketenci. 2018. Output, renewable and non-renewable energy production, and international trade: Evidence from EU-15 countries. Energy 159: 995–1002. [Google Scholar] [CrossRef]

- Halicioglu, Ferda. 2009. An econometric study of CO2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy 37: 1156–64. [Google Scholar] [CrossRef]

- Heidari, Hassan, Salih Turan Katircioğlu, and Lesyan Saeidpour. 2015. Economic growth, CO2 emissions, and energy consumption in the five ASEAN countries. International Journal of Electrical Power and Energy Systems 64: 785–91. [Google Scholar] [CrossRef]

- Ibrahim, Mansor H., and Siong Hook Law. 2014. Social capital and CO2 emission–output relations: A panel analysis. Renewable and Sustainable Energy Reviews 29: 528–34. [Google Scholar] [CrossRef]

- Irandoust, Manuchehr. 2016. The renewable energy-growth nexus with carbon emissions and technological innovation: Evidence from the Nordic countries. Ecological Indicators 69: 118–25. [Google Scholar] [CrossRef]

- Iwata, Hiroki, Keisuke Okada, and Sovannroeun Samreth. 2010. Empirical study on the environmental Kuznets curve for CO2 in France: The role of nuclear energy. Energy Policy 38: 4057–63. [Google Scholar] [CrossRef]

- Jaforullah, Mohammad, and Alan King. 2015. Does the use of renewable energy sources mitigate CO2 emissions? A reassessment of the US evidence. Energy Economics 49: 711–17. [Google Scholar] [CrossRef]

- Jalil, Abdul, and Syed F. Mahmud. 2009. Environment Kuznets curve for CO2 emissions: A cointegration analysis for China. Energy Policy 37: 5167–72. [Google Scholar] [CrossRef]

- Jayanthakumaran, Kankesu, and Ying Liu. 2012. Openness and the Environmental Kuznets Curve: Evidence from China. Economic Modelling 29: 566–76. [Google Scholar] [CrossRef]

- Jebli, Mehdi Ben, Slim Ben Youssef, and Ilhan Ozturk. 2016. Testing environmental Kuznets curve hypothesis: The role of renewable and non-renewable energy consumption and trade in OECD countries. Ecological Indicators 60: 824–31. [Google Scholar] [CrossRef]

- Johansen, Søren. 1988. Statistical analysis of cointegration vectors. Journal of Economic Dynamics and Control 12: 231–54. [Google Scholar] [CrossRef]

- Johansen, Søren, and Katarina Juselius. 1990. Maximum likelihood estimation and inference on cointegration—With applications to the demand for money. Oxford Bulletin of Economics and Statistics 2: 170–209. [Google Scholar] [CrossRef]

- Kalaitzidakis, Pantelis, Theofanis Mamuneas, and Thanasis Stengos. 2018. Greenhouse emissions and productivity growth. Journal of Risk and Financial Management 11: 38. [Google Scholar] [CrossRef]

- Le, Thai-Ha, and Euston Quah. 2018. Income level and the emissions, energy, and growth nexus: Evidence from Asia and the Pacific. International Economics 156: 193–205. [Google Scholar] [CrossRef]

- Lean, Hooi Hooi, and Russell Smyth. 2010. CO2 emissions, electricity consumption and output in ASEAN. Applied Energy 87: 1858–64. [Google Scholar] [CrossRef]

- Liu, Xuyi, Shun Zhang, and Junghan Bae. 2017. The impact of renewable energy and agriculture on carbon dioxide emissions: Investigating the environmental Kuznets curve in four selected ASEAN countries. Journal of Cleaner Production 164: 1239–47. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar. 2005. The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics 37: 1979–90. [Google Scholar] [CrossRef]

- Nasreen, Samia, and Sofia Anwar. 2014. Causal relationship between trade openness, economic growth and energy consumption: A panel data analysis of Asian countries. Energy Policy 69: 82–91. [Google Scholar] [CrossRef]

- Nguyen, Kim Hanh, and Makoto Kakinaka. 2019. Renewable energy consumption, carbon emissions, and development stages: Some evidence from panel cointegration analysis. Renewable Energy. 132: 1049–57. [Google Scholar] [CrossRef]

- Ozatac, Nesrin, Korhan K. Gokmenoglu, and Nigar Taspinar. 2017. Testing the EKC hypothesis by considering trade openness, urbanization, and financial development: The case of Turkey. Environmental Science and Pollution Research 24: 16690–701. [Google Scholar] [CrossRef] [PubMed]

- Ozturk, Ilhan, and Ali Acaravci. 2013. The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Economics 36: 262–67. [Google Scholar] [CrossRef]

- Ozturk, Ilhan, and Usama Al-Mulali. 2015. Investigating the validity of the environmental Kuznets curve hypothesis in Cambodia. Ecological Indicators 57: 324–30. [Google Scholar] [CrossRef]

- Pata, Ugur Korkut. 2018. Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: Testing EKC hypothesis with structural breaks. Journal of Cleaner Production 187: 770–79. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Raza, Syed Ali, and Nida Shah. 2018. Testing environmental Kuznets curve hypothesis in G7 countries: The role of renewable energy consumption and trade. Environmental Science and Pollution Research 25: 26965–77. [Google Scholar] [CrossRef]

- Saboori, Behnaz, and Jamalludin Sulaiman. 2013. CO2 emissions, energy consumption and economic growth in association of Southeast Asian Nations (ASEAN) countries: A cointegration approach. Energy 55: 813–22. [Google Scholar] [CrossRef]

- Saboori, Behnaz, Jamalludin Sulaiman, and Saidatulakmal Mohd. 2016. Environmental Kuznets curve and energy consumption in Malaysia: A cointegration approach. Energy Sources, Part B: Economics, Planning, and Policy 11: 861–67. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2009. Renewable energy consumption, CO2 emissions and oil prices in the G7 countries. Energy Economics 31: 456–62. [Google Scholar] [CrossRef]

- Saidi, Kais, and Mounir Ben Mbarek. 2016. Nuclear energy, renewable energy, CO2 emissions, and economic growth for nine developed countries: Evidence from panel Granger causality tests. Progress in Nuclear Energy 88: 364–74. [Google Scholar] [CrossRef]

- Sebri, Maamar, and Ousama Ben-Salha. 2014. On the causal dynamics between economic growth, renewable energy consumption, CO2 emissions and trade openness: Fresh evidence from BRICS countries. Renewable and Sustainable Energy Reviews 39: 14–23. [Google Scholar] [CrossRef]

- Şener, Şerife Elif Can, Julia L. Sharp, and Annick Anctil. 2018. Factors impacting diverging paths of renewable energy: A review. Renewable and Sustainable Energy Reviews 81: 2335–42. [Google Scholar] [CrossRef]

- Shafiei, Sahar, and Ruhul A. Salim. 2014. Non-renewable and renewable energy consumption and CO2 emissions in OECD countries: A comparative analysis. Energy Policy 66: 547–56. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Qazi Muhammad Adnan Hye, Aviral Kumar Tiwari, and Nuno Carlos Leitao. 2013. Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renewable and Sustainable Energy Reviews 25: 109–21. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Nanthakumar Loganathan, Mohammad Zeshan, and Khalid Zaman. 2015. Does renewable energy consumption add in economic growth? An application of autoregressive distributed lag model in Pakistan. Renewable and Sustainable Energy Reviews 44: 576–85. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Muhammad Shafiullah, Vassilios G. Papavassiliou, and Shawkat Hammoudeh. 2017. The CO2–growth nexus revisited: A nonparametric analysis for the G7 economies over nearly two centuries. Energy Economics 65: 183–93. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Ilham Haouas, and Thi Hong Van Hoang. 2019. Economic growth and environmental degradation in Vietnam: Is the environmental Kuznets curve a complete picture? Emerging Markets Review 38: 197–218. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Ronald Ravinesh Kumar, Muhammad Zakaria, and Maryam Hurr. 2017. Carbon emission, energy consumption, trade openness and financial development in Pakistan: A revisit. Renewable and Sustainable Energy Reviews 70: 185–92. [Google Scholar] [CrossRef]

- Soytas, Ugur, Ramazan Sari, and Bradley T. Ewing. 2007. Energy consumption, income, and carbon emissions in the United States. Ecological Economics 62: 482–89. [Google Scholar] [CrossRef]

- Stern, David I. 2004. The rise and fall of the environmental Kuznets curve. World Development 32: 1419–39. [Google Scholar] [CrossRef]

- Sugiawan, Yogi, and Shunsuke Managi. 2016. The environmental Kuznets curve in Indonesia: Exploring the potential of renewable energy. Energy Policy 98: 187–98. [Google Scholar] [CrossRef]

- Tang, Chor Foon, and Bee Wah Tan. 2015. The impact of energy consumption, income and foreign direct investment on carbon dioxide emissions in Vietnam. Energy 79: 447–54. [Google Scholar] [CrossRef]

- To, Anh Hoang, Dao Thi-Thieu Ha, Ha Minh Nguyen, and Duc Hong Vo. 2019. The impact of foreign direct investment on environment degradation: Evidence from emerging markets in Asia. International Journal of Environmental Research and Public Health 16: 1636. [Google Scholar] [CrossRef] [PubMed]

- Vo, Duc Hong, Son Van Huynh, and Dao Thi-Thieu Ha. 2019. The importance of the financial derivatives markets to economic development in the world’s four major economies. Journal of Risk and Financial Management 12: 35. [Google Scholar] [CrossRef]

- Wang, Yi-Chia. 2013. Functional sensitivity of testing the environmental Kuznets curve hypothesis. Resource and Energy Economics 35: 451–66. [Google Scholar] [CrossRef]

- Zoundi, Zakaria. 2017. CO2 emissions, renewable energy and the Environmental Kuznets Curve, a panel cointegration approach. Renewable and Sustainable Energy Reviews 72: 1067–75. [Google Scholar] [CrossRef]

| 1 | We have rescaled all the variables so that a number of values falls between zero and one. As such, these values are negative when taking the logarithm. |

| 2 | For details of the procedures in the bounds test, see earlier studies, such as Pesaran et al. (2001) and Vo et al. (2019). |

| 3 | It should be noted that although the coefficients of the income per capita and its square form are appropriate in terms of signs and significance levels, the estimation results could be spurious if there is a failure of cointegration of the conventional EKC estimation. The spurious regression is caused not by the quadratic function form, but by the fundamental trend relationship between income per capita and pollutants (Wang 2013). Thanks to the confirmation of the two advanced cointegration tests, our regressions do not suffer spurious estimations. |

{kind=link}

| Variable | Observations | Mean | Std. Dev. | Minimum | Maximum |

|---|---|---|---|---|---|

| Indonesia | |||||

| LnCO2 | 44 | −0.04 | 0.53 | −1.11 | 0.94 |

| LnY | 44 | 0.58 | 0.43 | −0.22 | 1.31 |

| LnY2 | 44 | 0.51 | 0.50 | 0.00 | 1.71 |

| LnEC | 44 | −0.61 | 0.37 | −1.21 | −0.12 |

| LnREC | 44 | −0.02 | 1.78 | −3.06 | 1.98 |

| LnPOP | 44 | 5.21 | 0.23 | 4.77 | 5.54 |

| Myanmar | |||||

| LnCO2 | 44 | −1.73 | 0.29 | −2.29 | −0.88 |

| LnY | 44 | −1.14 | 0.64 | −1.79 | 0.24 |

| LnY2 | 44 | 1.70 | 1.11 | 0.00 | 3.21 |

| LnEC | 44 | −1.26 | 0.07 | −1.37 | −0.99 |

| LnREC | 44 | −1.11 | 0.64 | −1.89 | 0.39 |

| LnPOP | 44 | 3.69 | 0.20 | 3.30 | 3.95 |

| Malaysia | |||||

| LnCO2 | 44 | 1.31 | 0.58 | 0.41 | 2.08 |

| LnY | 44 | 1.62 | 0.47 | 0.72 | 2.34 |

| LnY2 | 44 | 2.85 | 1.51 | 0.52 | 5.48 |

| LnEC | 44 | 0.34 | 0.56 | −0.65 | 1.09 |

| LnREC | 44 | 0.49 | 0.54 | −0.66 | 1.35 |

| LnPOP | 44 | 2.94 | 0.31 | 2.40 | 3.41 |

| Philippines | |||||

| LnCO2 | 44 | −0.24 | 0.16 | −0.66 | 0.05 |

| LnY | 44 | 0.50 | 0.16 | 0.25 | 0.92 |

| LnY2 | 44 | 0.27 | 0.19 | 0.06 | 0.84 |

| LnEC | 44 | −0.79 | 0.06 | −0.90 | −0.67 |

| LnREC | 42 | 1.75 | 1.08 | −0.88 | 2.62 |

| LnPOP | 44 | 4.16 | 0.30 | 3.61 | 4.61 |

| Thailand | |||||

| LnCO2 | 44 | 0.54 | 0.75 | −0.68 | 1.53 |

| LnY | 44 | 0.92 | 0.57 | −0.05 | 1.72 |

| LnY2 | 44 | 1.16 | 1.00 | 0.00 | 2.96 |

| LnEC | 44 | −0.20 | 0.57 | −1.02 | 0.69 |

| LnREC | 44 | −0.35 | 0.33 | −1.47 | 0.18 |

| LnPOP | 44 | 4.02 | 0.17 | 3.64 | 4.23 |

| Country | Variable | Level | 1st Difference | Order of Integration | ||||

|---|---|---|---|---|---|---|---|---|

| DF-GLS | DF | PP | DF-GLS | DF | PP | |||

| Indonesia | LnCO2 | −2.13 | −3.08 | −2.96 | −3.97 *** | −6.00 *** | −6.02 *** | I(1) |

| lnY | −2.03 | −1.98 | −2.24 | −3.26 ** | −4.80 *** | −4.74 *** | I(1) | |

| LnY2 | −0.78 | −0.33 | −0.60 | −3.38 ** | −4.83 *** | −4.77 *** | I(1) | |

| LnEC | −1.29 | −1.24 | −1.22 | −3.81 *** | −3.63 ** | −6.68 *** | I(1) | |

| LnREC | −1.18 | −0.65 | −0.86 | −3.09 * | −5.30 *** | −5.26 *** | I(1) | |

| LnPOP | −5.81 *** | −7.57 *** | −4.16 ** | −3.86 *** | 0.55 | −0.35 | I(0) | |

| Myanmar | LnCO2 | −1.01 | −1.57 | −1.50 | −2.99 * | −5.01 *** | −4.71 *** | I(1) |

| lnY | −1.50 | −0.15 | −0.59 | −1.86 | −3.06 | −3.12 | I(2) | |

| LnY2 | −2.33 | −1.22 | −1.71 | −1.84 | −3.32 * | −3.78 ** | I(1) | |

| LnEC | −1.50 | −0.21 | −0.95 | −2.36 | −3.51 * | −3.53 * | I(1) | |

| LnREC | −0.93 | −1.32 | −1.11 | −3.86 *** | −7.13 *** | −7.37 *** | I(1) | |

| LnPOP | −6.07 *** | −2.38 | −1.52 | −5.54 *** | 0.24 | −1.28 | I(1) | |

| Malaysia | LnCO2 | −1.91 | −2.02 | −2.11 | −3.31 ** | −7.86 *** | −7.79 *** | I(1) |

| lnY | −1.68 | −2.20 | −2.35 | −3.01 * | −5.75 *** | −5.72 *** | I(1) | |

| LnY2 | −2.01 | −2.24 | −2.38 | −3.22 ** | −5.98 *** | −5.96 *** | I(1) | |

| LnEC | −1.69 | −1.84 | −1.72 | −3.89 *** | −7.03 *** | −7.39 *** | I(1) | |

| LnREC | −1.92 | −1.81 | −1.97 | −3.96 *** | −5.17 *** | −5.08 *** | I(1) | |

| LnPOP | −3.59 ** | −3.71 ** | 1.53 | −2.96 * | −1.49 | −1.78 | I(0) | |

| Philippines | LnCO2 | −1.89 | −1.44 | −1.74 | −2.81 | −5.70 *** | −5.79 *** | I(1) |

| lnY | −1.22 | 0.04 | −0.69 | −3.07 * | −3.56 ** | −3.52 * | I(1) | |

| LnY2 | −0.81 | 1.78 | 0.84 | −2.63 | −3.53 * | −3.52 * | I(1) | |

| LnEC | −2.04 | −2.49 | −2.53 | −2.51 | −8.62 *** | −8.33 *** | I(1) | |

| LnREC | −1.93 | −1.57 | −1.69 | −2.60 | −3.67 ** | −3.58 ** | I(1) | |

| LnPOP | −6.67 *** | 6.10 *** | 3.42 *** | −3.99 *** | −1.67 | −1.92 | I(1) | |

| Thailand | LnCO2 | −1.54 | −0.74 | −1.17 | −3.14 * | −4.48 *** | −4.44 *** | I(1) |

| lnY | −1.81 | −0.71 | −1.29 | −2.85 | −4.04 ** | −4.04 ** | I(1) | |

| LnY2 | −1.81 | −2.35 | −2.41 | −3.02 * | −4.33 *** | −4.34 *** | I(1) | |

| LnEC | −2.01 | −1.60 | −1.97 | −2.39 | −4.8 *** | −4.91 *** | I(1) | |

| LnREC | −4.79 *** | −5.36 *** | −5.27 *** | −5.17 *** | −8.97 *** | −10.1 *** | I(1) | |

| LnPOP | −2.94 * | −6.60 *** | 4.04 *** | −5.05 *** | −1.36 | −2.02 | I(0) |

| ASEAN Countries | Indonesia | Myanmar | Malaysia | Philippines | Thailand | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: Johansen cointegration test | |||||||||||

| Ho | H1 | λ | trace | λ | trace | λ | trace | λ | trace | λ | trace |

| r = 0 | r ≥ 1 | 84.42 ** | 186.27 ** | 91.29 ** | 201.37 ** | 54.22 ** | 152.94 ** | 67.90 ** | 167.58 ** | 49.73 ** | 117.12 ** |

| r ≤ 1 | r ≥ 2 | 46.51 ** | 101.85 ** | 54.58 ** | 110.08 ** | 43.64 ** | 98.72 ** | 41.53 ** | 99.68 ** | 34.12 ** | 67.40 |

| r ≤ 2 | r ≥ 3 | 31.71 ** | 55.33 ** | 24.37 | 55.50 ** | 25.19 | 55.08 ** | 33.00 ** | 58.15 ** | 15.06 | 33.27 |

| r ≤ 3 | r ≥ 4 | 14.59 | 23.62 | 22.23 ** | 31.14 ** | 17.3 | 29.89 ** | 15.61 | 25.14 | 9.43 | 18.21 |

| r ≤ 4 | r ≥ 5 | 8.22 | 9.03 | 8.36 | 8.90 | 11.76 | 12.59 | 9.38 | 9.53 | 6.05 | 8.77 |

| r ≤ 5 | r ≥ 6 | 0.81 | 0.81 | 0.54 | 0.54 | 0.83 | 0.83 | 0.16 | 0.16 | 2.72 | 2.72 |

| Panel B: Bound cointegration test | |||||||||||

| F-stat | t-stat | F-stat | t-stat | F-stat | t-stat | F-stat | t-stat | F-stat | t-stat | ||

| Ho: No cointegration | 8.24 *** | −6.37 *** | 8.09 *** | −3.81 * | 5.04 ** | −3.98 * | 3.25 | −3.07 | 3.03 | −1.14 | |

| Model | ARDL (1, 1, 2, 1, 1, 1) | ARDL (1, 2, 2, 1, 1, 2) | ARDL (1, 1, 1, 1, 2, 1) | ARDL (1, 1, 2, 1, 1, 2) | ARDL (1, 1, 1, 1, 1, 1) | ||||||

| Variable | Indonesia | Myanmar | Malaysia |

|---|---|---|---|

| FMOLS | |||

| LnY | 0.66 *** | −0.12 | 0.87 *** |

| LnY2 | −0.09 ** | −0.35 *** | 0.08 |

| LnEC | 0.47 *** | 1.72 *** | 0.43 ** |

| LnREC | −0.15 *** | −0.0.003 | −0.0004 |

| LnPOP | 1.58 *** | −0.89 *** | −0.62 * |

| Const | −8.32 *** | 4.15 *** | 1.35 |

| DOLS | |||

| LnY | −0.68 *** | 0.43 *** | −0.78 |

| LnY2 | 0.15 *** | −0.41 *** | 0.64 *** |

| LnEC | 1.76 *** | 2.8 *** | 0.8 *** |

| LnREC | −0.27 *** | −0.49 *** | −0.14 ** |

| LnPOP | 3.6 *** | −1.84 *** | −0.86 ** |

| Const | −18.19 *** | 10.33 *** | 1.87 * |

| Null Hypothesis | Short-Run Granger-Causality Test | Long-Run Granger-Causality Test | ||||||

|---|---|---|---|---|---|---|---|---|

| Indonesia | Myanmar | Malaysia | Philippines | Thailand | Indonesia | Myanmar | Malaysia | |

| ∆LnCO2 ≠ ∆LnEC | 6.20 * | 1.52 | 0.52 | 0.13 | 4.22 | 6.62 * | 2.80 | 0.52 |

| ∆LnCO2 ≠ ∆LnREC | 0.35 | 3.67 | 1.97 | 1.44 | 4.85 * | 0.42 | 4.48 | 2.02 |

| ∆LnCO2 ≠ ∆LnY, ∆LnY2 | 1.77 | 12.88 ** | 4.26 | 6.23 | 6.95 | 1.78 | 14.08 ** | 4.40 |

| ∆LnCO2 ≠ ∆LnPOP | 2.1 | 7.39 ** | 5.91 * | 0.17 | 4.44 | 2.1 | 9.15 ** | 6.95 * |

| ∆LnEC ≠ ∆LnCO2 | 0.34 | 12.24 *** | 3.50 | 0.54 | 5.62 * | 3.45 | 24.60 *** | 3.91 |

| ∆LnEC ≠ ∆LnREC | 2.34 | 5.60 * | 0.35 | 1.00 | 2.86 | 3.86 | 20.99 *** | 1.22 |

| ∆LnEC ≠ ∆LnY, ∆LnY2 | 1.54 | 25.8 *** | 5.17 | 1.71 | 1.44 | 6.52 | 27.57 *** | 5.27 |

| ∆LnEC ≠ ∆LnPOP | 8.06 ** | 22.74 *** | 1.91 | 3.87 | 1.29 | 9.00 ** | 25.66 *** | 3.10 |

| ∆LnREC ≠ ∆LnCO2 | 0.96 | 3.56 | 3.83 | 0.02 | 0.46 | 2.85 | 4.05 | 4.06 |

| ∆LnREC ≠ ∆LnEC | 0.44 | 0.23 | 2.41 | 1.04 | 3.50 | 2.29 | 3.56 | 3.02 |

| ∆LnREC ≠ ∆LnY, ∆LnY2 | 4.09 | 3.87 | 0.79 | 5.87 | 18.48 *** | 4.36 | 9.47 * | 0.98 |

| ∆LnREC ≠ ∆LnPOP | 2.93 | 2.73 | 1.19 | 1.21 | 9.17 ** | 3.84 | 3.38 | 1.33 |

| ∆LnY, ∆LnY2 ≠ ∆LnCO2 | 4.93 | 14.08 *** | 9.58 ** | 17.7 *** | 6.22 | 37.3 *** | 28.67 *** | 12.00 * |

| ∆LnY, ∆LnY2 ≠ ∆LnEC | 6.69 | 13.52 *** | 6.46 | 15.77 *** | 5.01 | 36.65 *** | 24.56 *** | 12.55 * |

| ∆LnY, ∆LnY2 ≠ ∆LnREC | 10.77 *** | 11.08 ** | 3.10 | 2.34 | 4.28 | 34.82 *** | 11.61 * | 9.43 |

| ∆LnY, ∆LnY2 ≠ ∆LnPOP | 22.41 *** | 3.96 | 11.72 ** | 17.35 *** | 19.68 *** | 52.13 *** | 12.17 * | 12.57 * |

| ∆LnPOP ≠ ∆LnCO2 | 0.12 | 13.03 *** | 0.98 | 19.29 *** | 2.70 | 0.93 | 18.93 *** | 94.44 *** |

| ∆LnPOP ≠ ∆LnEC | 0.13 | 15.17 *** | 18.04 *** | 15.07 *** | 9.7 *** | 0.59 | 19.63 *** | 63.13 *** |

| ∆LnPOP ≠ ∆LnREC | 2.09 | 19.48 *** | 6.38 ** | 2.88 | 0.19 | 2.09 | 22.61 *** | 69.21 *** |

| ∆LnPOP ≠ ∆LnY, ∆LnY2 | 6.71 | 21.26 *** | 18.13 *** | 31.45 *** | 9.47 ** | 32.22 *** | 21.41 *** | 87.40 *** |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vo, A.T.; Vo, D.H.; Le, Q.T.-T. CO2 Emissions, Energy Consumption, and Economic Growth: New Evidence in the ASEAN Countries. J. Risk Financial Manag. 2019, 12, 145. https://doi.org/10.3390/jrfm12030145

Vo AT, Vo DH, Le QT-T. CO2 Emissions, Energy Consumption, and Economic Growth: New Evidence in the ASEAN Countries. Journal of Risk and Financial Management. 2019; 12(3):145. https://doi.org/10.3390/jrfm12030145

Chicago/Turabian StyleVo, Anh The, Duc Hong Vo, and Quan Thai-Thuong Le. 2019. "CO2 Emissions, Energy Consumption, and Economic Growth: New Evidence in the ASEAN Countries" Journal of Risk and Financial Management 12, no. 3: 145. https://doi.org/10.3390/jrfm12030145

APA StyleVo, A. T., Vo, D. H., & Le, Q. T.-T. (2019). CO2 Emissions, Energy Consumption, and Economic Growth: New Evidence in the ASEAN Countries. Journal of Risk and Financial Management, 12(3), 145. https://doi.org/10.3390/jrfm12030145