Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy

Abstract

1. Introduction

“a process, effected by an entity’s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risks to be within its risk appetite, to provide reasonable assurance regarding the achievement of the entity’s objectives”.

Theoretical Background

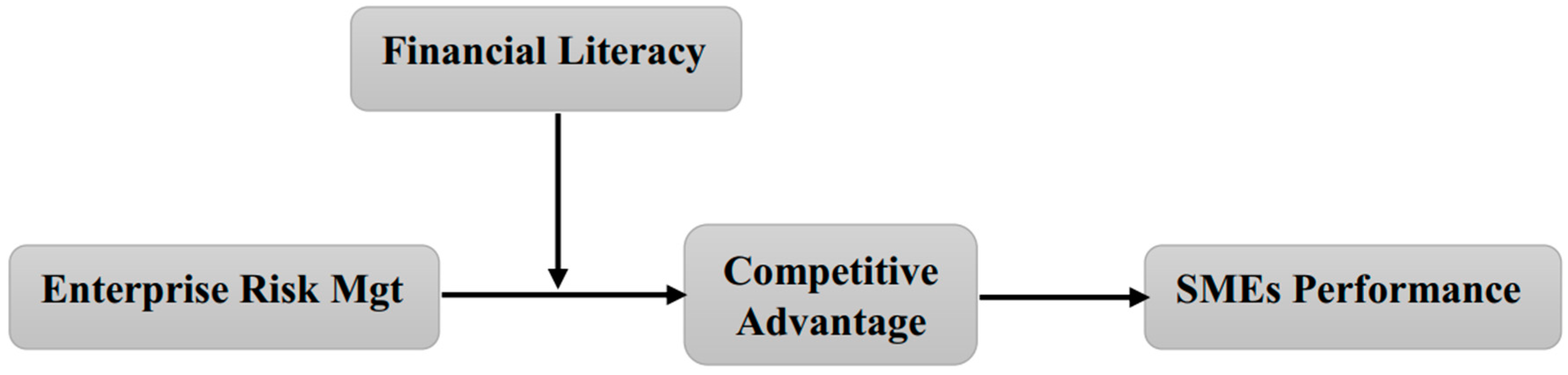

2. Hypothesis Development

2.1. ERM and Firm Performance

2.2. ERM and Competitive Advantage

2.3. Competitive Advantage and SME Performance

2.4. Mediating Role of CA between ERM and SMEs Performance

2.5. Moderating Role of Financial Literacy between ERM and CA

3. Methodology

3.1. Sample and Population

3.2. Measurement of Variables

3.3. Control Variables

4. Data Analyses

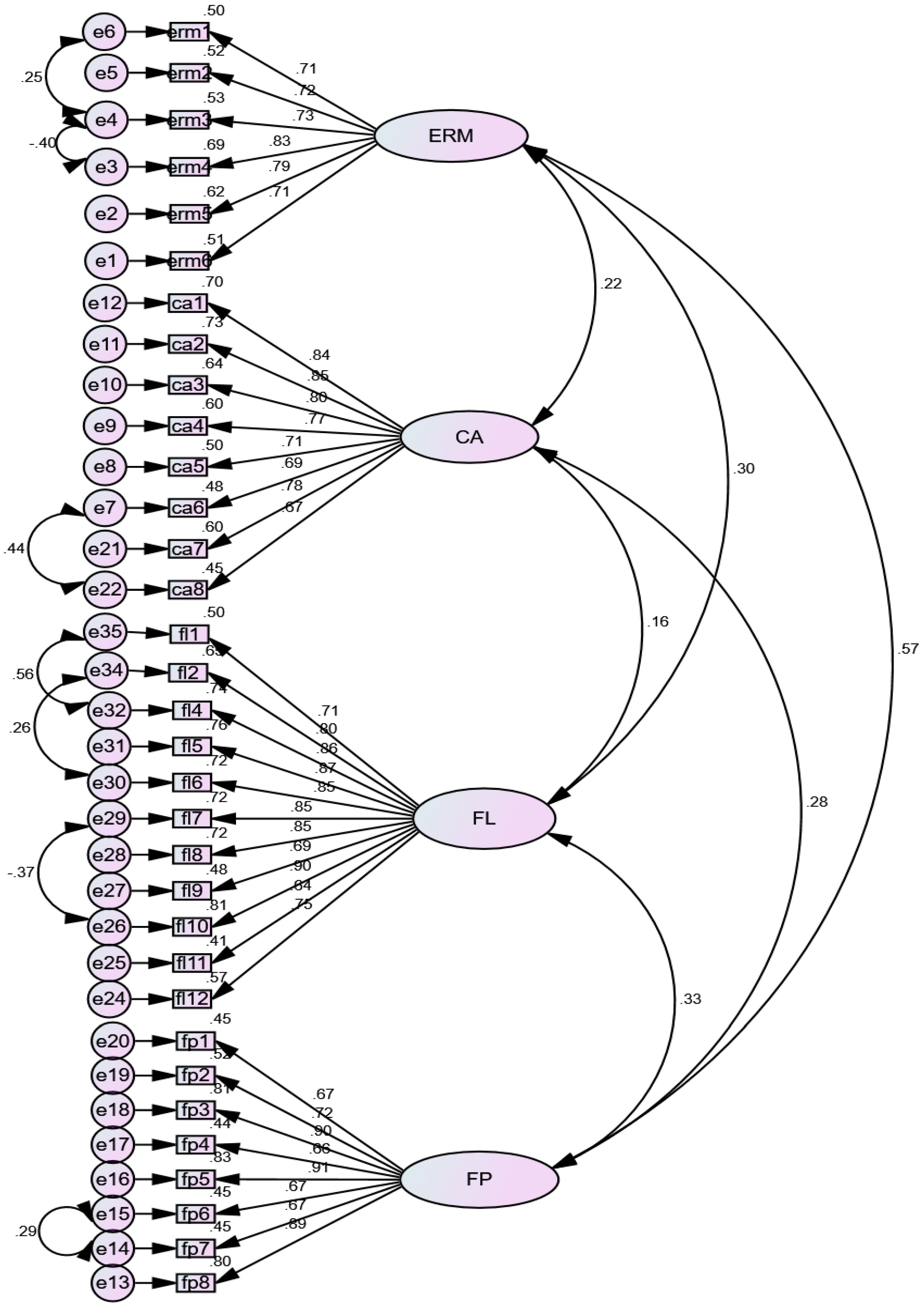

4.1. Confirmatory Factor Analysis

4.2. Correlation

4.3. Common Method Bias

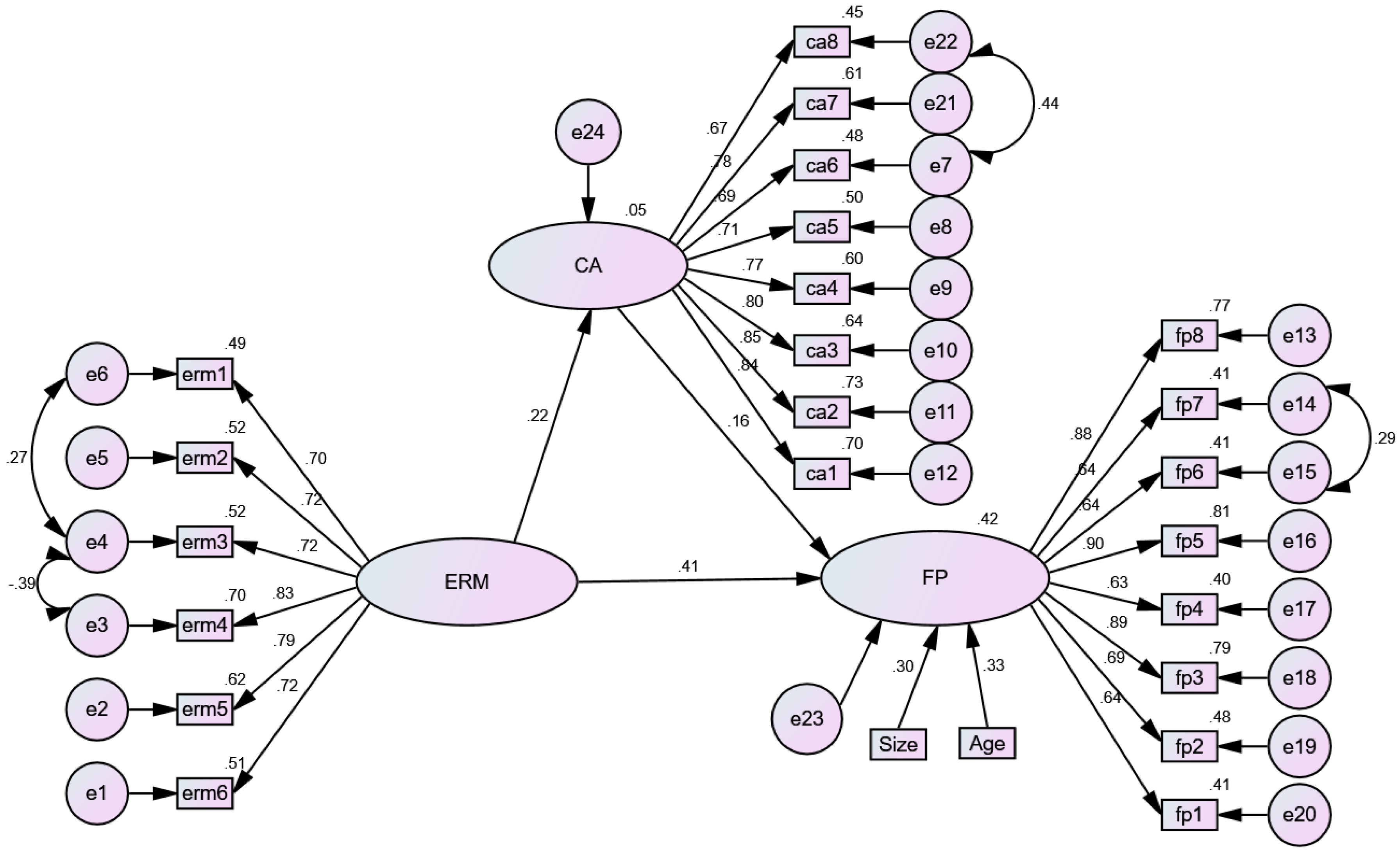

4.4. Structural Model (Mediation Test)

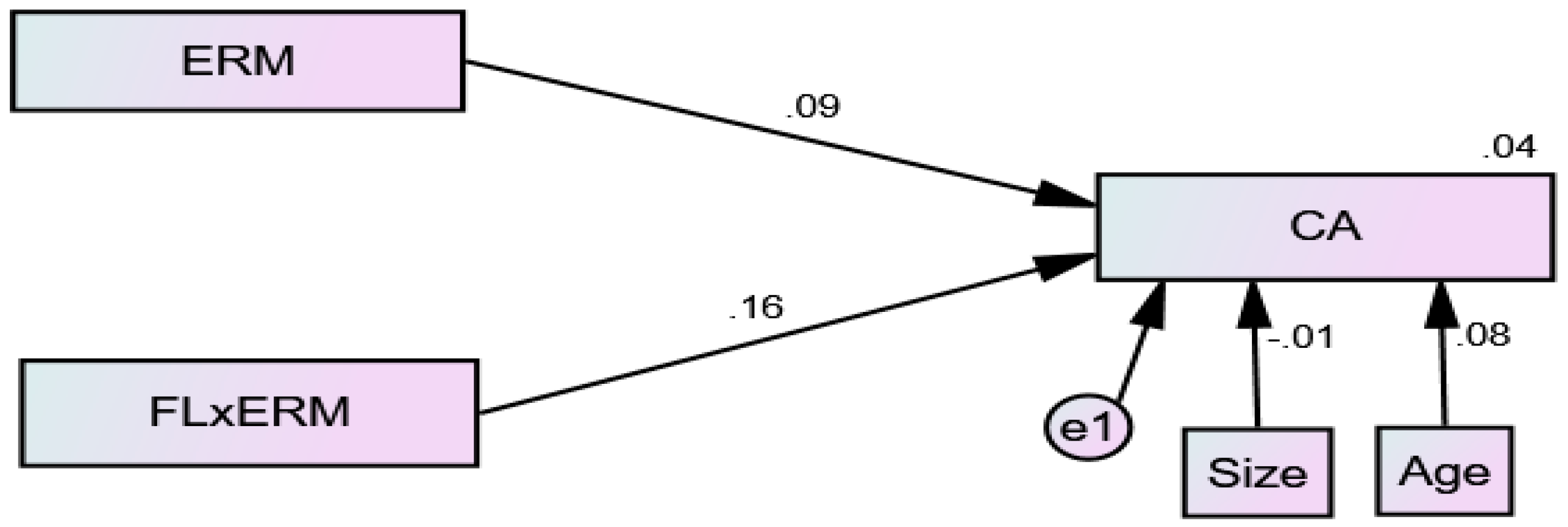

4.5. Structural Model 2 (Moderation Test)

5. Discussion

5.1. Contributions and Implications

5.2. Limitations and Future Research Directions

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Abd Razak, Noraznira, Zuriah Ab Rahman, and Halimahton Borhan. 2016. Modeling firm resources–Enterprise risk management relationships: An empirical finding using PLS-SEM. World Journal of Entrepreneurship, Management and Sustainable Development 12: 35–49. [Google Scholar] [CrossRef]

- Annamalah, Sanmugam, Murali Raman, Govindan Marthandan, and Arvindan Kalisri Logeswaran. 2018. Implementation of Enterprise Risk Management (ERM) Framework in Enhancing Business Performances in Oil and Gas Sector. Economies 6: 4. [Google Scholar] [CrossRef]

- Anwar, Muhammad. 2018. Business model innovation And SMEs Performance—Does competitive advantage mediate? International Journal of Innovation Management. [Google Scholar] [CrossRef]

- Anwar, Muhammad, Sher Khan Zaman, and Najeeb Ullah Khan. 2018. Intellectual Capital, Entrepreneurial Strategy and New Venture Performance: Mediating Role of Competitive Advantage. Business Economic Review 10: 63–94. [Google Scholar] [CrossRef]

- Arena, Marika, Michela Arnaboldi, and Giovanni Azzone. 2010. The organizational dynamics of enterprise risk management. Accounting, Organizations and Society 35: 659–75. [Google Scholar] [CrossRef]

- Armeanu, Danial Ştefan, Georgeta Vintilă, Ştefan Cristian Gherghina, and Dan Cosmin Petrache. 2017. Approaches on Correlation between Board of Directors and Risk Management in Resilient Economies. Sustainability 9: 173. [Google Scholar] [CrossRef]

- Ashraf, Badar Nadeem, Sidra Arshad, and Lliang Yan. 2017. Trade openness and bank risk-taking behavior: Evidence from emerging economies. Journal of Risk and Financial Management 10: 15. [Google Scholar] [CrossRef]

- Barney, Jay. 1991. Firm resources and sustained competitive advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Beasley, Mark, Donald Pagach, and Richard Warr. 2008. Information conveyed in hiring announcements of senior executives overseeing enterprise-wide risk management processes. Journal of Accounting, Auditing Finance 23: 311–32. [Google Scholar] [CrossRef]

- Bogodistov, Yevgen, and Veit Wohlgemuth. 2017. Enterprise risk management: a capability-based perspective. The Journal of Risk Finance 18: 234–51. [Google Scholar] [CrossRef]

- Bongomin, G. Okello Candiya, Joseph Mpeera Ntayi, John C. Munene, and Charles Akol Malinga. 2017. The relationship between access to finance and growth of SMEs in developing economies: Financial literacy as a moderator. Review of International Business and Strategy 27: 520–38. [Google Scholar] [CrossRef]

- Brustbauer, Johannes. 2016. Enterprise risk management in SMEs: Towards a structural model. International Small Business Journal 34: 70–85. [Google Scholar] [CrossRef]

- Callahan, Carolyan, and Jared Soileau. 2017. Does Enterprise risk management enhance operating performance? Advances in Accounting 37: 122–39. [Google Scholar] [CrossRef]

- Chang, Chen Shan, Shang Wu Yu, and Cheng Huang Hung. 2015. Firm risk and performance: the role of corporate governance. Review of Managerial Science 9: 141–73. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organizations of the Treadway Commission (COSO). 2004. Enterprise Risk Management Framework. New York: American Institute of Certified Public Accountants. [Google Scholar]

- Daud, Wan Norhayate Wan, and Ahmad Shukri Yazid. 2009. A conceptual framework for the adoption of enterprise risk management in government-linked companies. International Review of Business Research Papers 5: 229–38. [Google Scholar]

- Dionne, Georages, and Thouraya Triki. 2005. Risk management and corporate governance: The importance of independence and financial knowledge for the board and the audit committee. Cahier de Recherche/Working Paper 5: 15. [Google Scholar] [CrossRef]

- Eckles, Davud L., Robert E. Hoyt, and Steve M. Miller. 2014. Reprint of: The impact of enterprise risk management on the marginal cost of reducing risk: Evidence from the insurance industry. Journal of Banking Finance 49: 409–23. [Google Scholar] [CrossRef]

- Elahi, Ehsan. 2013. Risk management: the next source of competitive advantage. Foresight 15: 117–31. [Google Scholar] [CrossRef]

- Florio, Cristina, and Giulia Leoni. 2017. Enterprise risk management and firm performance: The Italian case. The British Accounting Review 49: 56–74. [Google Scholar] [CrossRef]

- Farrell, Mark, and Ronan Gallagher. 2015. The valuation implications of enterprise risk management maturity. Journal of Risk and Insurance 82: 625–57. [Google Scholar] [CrossRef]

- George, Derren, and Paul Mallery. 2010. SPSS for Windows Step by Step. A Simple Study Guide and Reference (10. Baskı). New York: Pearson. [Google Scholar]

- González-Rodríguez, Maria Rosario, Jose Luis Jiménez-Caballero, Rosario Carmen Martín-Samper, Mehmet Ali Köseoglu, and Fevzi Okumus. 2018. Revisiting the link between business strategy and performance: Evidence from hotels. International Journal of Hospitality Management 72: 21–31. [Google Scholar] [CrossRef]

- Hair, Joseph F., Rolph E. Anderson, Barry J. Babin, and Willium C. Black. 2010. Multivariate Data Analysis: A Global Perspective. Upper Saddle River: Pearson, vol. 7. [Google Scholar]

- Herbane, Brahim. 2010. Small business research: Time for a crisis-based view. International Small Business Journal 28: 43–64. [Google Scholar] [CrossRef]

- Hommel, Ulrich, and Roger King. 2013. The emergence of risk-based regulation in higher education: Relevance for entrepreneurial risk taking by business schools. Journal of Management Development 32: 537–47. [Google Scholar] [CrossRef]

- Hoyt, Robert E., and Andre P. Liebenberg. 2011. The value of enterprise risk management. Journal of Risk and Insurance 78: 795–822. [Google Scholar] [CrossRef]

- Hu, Litze T., and Ppeter M. Bentler. 1999. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling 6: 1–55. [Google Scholar] [CrossRef]

- Kantur, Deniz. 2016. Strategic entrepreneurship: mediating the entrepreneurial orientation-performance link. Management Decision 54: 24–43. [Google Scholar] [CrossRef]

- Khan, Majid Jamal, Dildar Hussain, and Waqar Mehmood. 2016. Why do firms adopt enterprise risk management (ERM)? Empirical evidence from France. Management Decision 54: 1886–907. [Google Scholar] [CrossRef]

- Khan, Sajjad Nawaz, and Engku Ismail Engku Ali. 2017. The Moderating Role of Intellectual Capital between Enterprise Risk Management and Firm Performance: A Conceptual Review. American Journal of Social Sciences and Humanities 2: 9–15. [Google Scholar] [CrossRef]

- Krause, Timothy A, and Yiuman Tse. 2016. Risk management and firm value: recent theory and evidence. International Journal of Accounting and Information Management 24: 56–81. [Google Scholar] [CrossRef]

- Lajili, Kaouthar. 2009. Corporate risk disclosure and corporate governance. Journal of Risk and Financial Management 2: 94–117. [Google Scholar] [CrossRef]

- Lechner, Christian, and Sveinn Vidar Gudmundsson. 2014. Entrepreneurial orientation, firm strategy and small firm performance. International Small Business Journal 32: 36–60. [Google Scholar] [CrossRef]

- Lechner, Philipp, and Nadine Gatzert. 2018. Determinants and value of enterprise risk management: empirical evidence from Germany. The European Journal of Finance 24: 867–87. [Google Scholar] [CrossRef]

- Liu, Chiung Lin, Kuo Chung Shang, Taih Cherng Lirn, Kee Hung Lai, and Y. H. Venus Lun. 2017. Supply chain resilience, firm performance, and management policies in the liner shipping industry. Transportation Research Part A: Policy and Practice 110: 202–19. [Google Scholar] [CrossRef]

- Ludin, Khairul Rizan Mat, Zakiah Muhammaddun Mohamed, and Norman Mohd-Saleh. 2017. The association between CEO characteristics, internal audit quality and risk-management implementation in the public sector. Risk Management 19: 281–300. [Google Scholar] [CrossRef]

- Manab, Norlida Abdul, Isahak Kassim, and Mohd Rashid Hussin. 2010. Enterprise-wide risk management (EWRM) practices: Between corporate governance compliance and value. International Review of Business Research Papers 6: 239–52. [Google Scholar]

- Meidell, Anita, and Katarina Kaarbøe. 2017. How the enterprise risk management function influences decision-making in the organization–A field study of a large, global oil and gas company. The British Accounting Review 49: 39–55. [Google Scholar] [CrossRef]

- Nunnally, Jum, and Ira Bernstein. 1994. Psychometric Theory, 3rd ed. New York: McGraw-Hill. [Google Scholar]

- Oyewobi, Luqman Oyewobi, Abimbola Oluwakemi Windapo, and Rotimi Olabode Bamidele James. 2015. An empirical analysis of construction organisations’ competitive strategies and performance. Built Environment Project and Asset Management 5: 417–31. [Google Scholar] [CrossRef]

- Paape, Leen, and Roland F. Speklè. 2012. The adoption and design of enterprise risk management practices: An empirical study. European Accounting Review 21: 533–64. [Google Scholar] [CrossRef]

- Parnell, John A. 2010. Strategic clarity, business strategy and performance. Journal of Strategy and Management 3: 304–24. [Google Scholar] [CrossRef]

- Parnell, John A., Zhang Long, and Don Lester. 2015. Competitive strategy, capabilities and uncertainty in small and medium sized enterprises (SMEs) in China and the United States. Management Decision 53: 402–31. [Google Scholar] [CrossRef]

- Podsakoff, Philip M., and Dennis W. Organ. 1986. Self-reports in organizational research: problems and prospects’. Journal of Management 12: 531–44. [Google Scholar] [CrossRef]

- Porter, Michael E. 1980. Industry structure and competitive strategy: Keys to profitability. Financial Analysts Journal 36: 30–41. [Google Scholar] [CrossRef]

- Radner, Roy, and Larry Shepp. 1996. Risk vs. profit potential: A model for corporate strategy. Journal of Economic Dynamics Control 20: 1373–93. [Google Scholar] [CrossRef]

- Rasid, Siti Zaleha Abdul, Che Ruhana Isa, and Wan Khairuzzaman Wan Ismail. 2014. Management accounting systems, enterprise risk management and organizational performance in financial institutions. Asian Review of Accounting 22: 128–44. [Google Scholar] [CrossRef]

- Stulz, Rene M. 1996. Rethinking risk management. Journal of Applied Corporate Finance 9: 8–25. [Google Scholar] [CrossRef]

- Sax, Johanna, and Simon S. Torp. 2015. Speak up! Enhancing risk performance with enterprise risk management, leadership style and employee voice. Management Decision 53: 1452–68. [Google Scholar] [CrossRef]

- Semrau, Thorsten, Tina Ambos, and Sascha Kraus. 2016. Entrepreneurial orientation and SME performance across societal cultures: An international study. Journal of Business Research 69: 1928–32. [Google Scholar] [CrossRef]

- Shanahan, Peter, and Jenny McParlane. 2005. Serendipity or strategy? An investigation into entrepreneurial transnational higher education and risk management. On the Horizon 13: 220–28. [Google Scholar] [CrossRef]

- Soin, Kim, and Paul Collier. 2013. Risk and risk management in management accounting and control. Management Accounting Research 24: 82–87. [Google Scholar] [CrossRef]

- Soltanizadeh, Sara, Siti Zaleha Abdul Rasid, Nargess Mottaghi Golshan, and Wan Khairuzzaman Wan Ismail. 2016. Business strategy, enterprise risk management and organizational performance. Management Research Review 39: 1016–33. [Google Scholar] [CrossRef]

- Standard and Poor’s. 2008. Standard & Poor’s Rating Services Us Rating Fees Disclosure. Press Release. Available online: http://www2.standardandpoors.com/spf/pdf/fixedincome/RatingsFees2008.pdfS (accessed on 10 June 2018).

- Su, Zhongfeng, Hai Guo, and Wei Sun. 2017. Exploration and Firm Performance: The Moderating Impact of Competitive Strategy. British Journal of Management 28: 357–71. [Google Scholar] [CrossRef]

- Unnikrishnan, Seema, Rauf Iqbal, Anju Singh, and Indrayani M. Nimkar. 2015. Safety management practices in small and medium enterprises in India. Safety and Health at Work 6: 46–55. [Google Scholar] [CrossRef] [PubMed]

- Wang, Peng Fei, Shi Li, and Jian Zhou. 2010. Financial risk management and enterprise value creation: Evidence from non-ferrous metal listed companies in China. Nankai Business Review International 1: 5–19. [Google Scholar] [CrossRef]

- Wang, Teng Shih, Yi Mian Lin, Edward M. Werner, and Hsihui Chang. 2018. The relationship between external financing activities and earnings management: Evidence from enterprise risk management. International Review of Economics Finance. [Google Scholar] [CrossRef]

- Yilmaz, Ayse Kucuk, and Triant Flouris. 2017. Enterprise risk management in terms of organizational culture and its leadership and strategic management. In Corporate Risk Management for International Business. Singapore: Springer, pp. 65–112. [Google Scholar]

- Zou, Xiang, and Che Hashim Hassan. 2017. Enterprise risk management in China: the impacts on organizational performance. International Journal of Economic Policy in Emerging Economies 10: 226–39. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Frequency | Percentage | |

|---|---|---|

| Industry | ||

| Manufacturing | 110 | 36.2 |

| Trading | 120 | 39.5 |

| Services | 74 | 24.3 |

| Size | ||

| 20–50 employees | 123 | 40.5 |

| 51–100 employees | 112 | 36.8 |

| 101–250 employees | 69 | 22.7 |

| Age | ||

| 10 years and less | 117 | 38.5 |

| 11–20 years | 109 | 35.9 |

| 21 and above years | 78 | 25.7 |

| Total | 304 | 100 |

| Minimum | Maximum | Mean | S.D | Skewness | Kurtosis | |||

|---|---|---|---|---|---|---|---|---|

| Statistic | Statistic | Statistic | Statistic | Statistic | Std. Error | Statistic | Std. Error | |

| erm1 | 2 | 5 | 3.76 | 0.539 | −0.623 | 0.140 | 0.685 | 0.279 |

| erm2 | 2 | 5 | 3.71 | 0.508 | −0.782 | 0.140 | 0.177 | 0.279 |

| erm3 | 2 | 5 | 3.75 | 0.511 | −0.749 | 0.140 | 0.594 | 0.279 |

| erm4 | 2 | 5 | 3.72 | 0.538 | −0.741 | 0.140 | 0.536 | 0.279 |

| erm5 | 2 | 5 | 3.78 | 0.515 | −0.846 | 0.140 | 1.210 | 0.279 |

| erm6 | 2 | 5 | 3.71 | 0.547 | −0.651 | 0.140 | 0.413 | 0.279 |

| ca1 | 2 | 5 | 3.69 | 0.531 | −0.261 | 0.140 | −0.506 | 0.279 |

| ca2 | 2 | 5 | 3.69 | 0.528 | −0.421 | 0.140 | −0.264 | 0.279 |

| ca3 | 2 | 5 | 3.70 | 0.527 | −0.435 | 0.140 | −0.237 | 0.279 |

| ca4 | 2 | 5 | 3.69 | 0.522 | −0.340 | 0.140 | −0.481 | 0.279 |

| ca5 | 2 | 5 | 3.72 | 0.519 | −0.518 | 0.140 | −0.057 | 0.279 |

| ca6 | 2 | 5 | 3.73 | 0.507 | −0.485 | 0.140 | −0.183 | 0.279 |

| ca7 | 2 | 5 | 3.71 | 0.529 | −0.420 | 0.140 | −0.156 | 0.279 |

| ca8 | 2 | 5 | 3.71 | 0.508 | −0.478 | 0.140 | −0.343 | 0.279 |

| fl1 | 2 | 5 | 3.70 | 0.505 | −0.500 | 0.140 | −0.447 | 0.279 |

| fl2 | 2 | 5 | 3.76 | 0.492 | −0.608 | 0.140 | 0.152 | 0.279 |

| fl3 | 2 | 5 | 3.77 | 0.509 | −0.459 | 0.140 | 0.159 | 0.279 |

| fl4 | 2 | 5 | 3.73 | 0.499 | −0.561 | 0.140 | −0.150 | 0.279 |

| fl5 | 2 | 5 | 3.77 | 0.482 | −0.705 | 0.140 | 0.263 | 0.279 |

| fl6 | 2 | 5 | 3.76 | 0.494 | −0.594 | 0.140 | 0.110 | 0.279 |

| fl7 | 2 | 5 | 3.73 | 0.507 | −0.485 | 0.140 | −0.183 | 0.279 |

| fl8 | 2 | 5 | 3.78 | 0.488 | −0.628 | 0.140 | 0.397 | 0.279 |

| fl9 | 2 | 5 | 3.72 | 0.513 | −0.431 | 0.140 | −0.304 | 0.279 |

| fl10 | 2 | 5 | 3.77 | 0.487 | −0.651 | 0.140 | 0.286 | 0.279 |

| fl11 | 2 | 5 | 3.68 | 0.513 | −0.417 | 0.140 | −0.601 | 0.279 |

| fl12 | 2 | 5 | 3.83 | 0.442 | −1.008 | 0.140 | 1.524 | 0.279 |

| f13 | 2 | 5 | 3.73 | 0.515 | −0.414 | 0.140 | −0.214 | 0.279 |

| fp1 | 2 | 5 | 3.83 | 0.424 | −1.228 | 0.140 | 1.836 | 0.279 |

| fp2 | 2 | 5 | 3.79 | 0.476 | −0.738 | 0.140 | 0.594 | 0.279 |

| fp3 | 2 | 5 | 3.75 | 0.482 | −0.896 | 0.140 | 0.469 | 0.279 |

| fp4 | 3 | 5 | 3.81 | 0.441 | −0.858 | 0.140 | 0.513 | 0.279 |

| fp5 | 2 | 5 | 3.77 | 0.482 | −0.883 | 0.140 | 0.661 | 0.279 |

| fp6 | 3 | 5 | 3.83 | 0.424 | −0.967 | 0.140 | 1.004 | 0.279 |

| fp7 | 2 | 5 | 3.82 | 0.470 | −0.728 | 0.140 | 1.026 | 0.279 |

| fp8 | 2 | 5 | 3.78 | 0.460 | −0.928 | 0.140 | 0.529 | 0.279 |

| Estimate | AVE | √AVE | CR | |

|---|---|---|---|---|

| Enterprise Risk Management | 0.56 | 0.75 | 0.88 | |

| erm6 | 0.714 | |||

| erm5 | 0.789 | |||

| erm4 | 0.831 | |||

| erm3 | 0.728 | |||

| erm2 | 0.720 | |||

| erm1 | 0.708 | |||

| Competitive Advantage | 0.59 | 0.77 | 0.92 | |

| ca8 | 0.672 | |||

| ca7 | 0.778 | |||

| ca6 | 0.694 | |||

| ca5 | 0.705 | |||

| ca4 | 0.773 | |||

| ca3 | 0.798 | |||

| ca2 | 0.854 | |||

| ca1 | 0.837 | |||

| Financial Literacy | 0.64 | 0.80 | 0.95 | |

| fl12 | 0.752 | |||

| fl11 | 0.642 | |||

| fl10 | 0.902 | |||

| fl9 | 0.693 | |||

| fl8 | 0.849 | |||

| fl7 | 0.851 | |||

| fl6 | 0.847 | |||

| fl5 | 0.871 | |||

| fl4 | 0.862 | |||

| fl2 | 0.803 | |||

| fl1 | 0.710 | |||

| Firm Performance | 0.59 | 0.77 | 0.92 | |

| fp8 | 0.893 | |||

| fp7 | 0.670 | |||

| fp6 | 0.670 | |||

| fp5 | 0.910 | |||

| fp4 | 0.661 | |||

| fp3 | 0.899 | |||

| fp2 | 0.718 | |||

| fp1 | 0.669 |

| Size | Age | ERM | CA | FL | FP | |

|---|---|---|---|---|---|---|

| Size | 1 | |||||

| Age | 0.113 * | 1 | ||||

| ERM | 0.245 ** | 0.291 ** | 1 | |||

| CA | 0.055 | 0.140 * | 0.234 ** | 1 | ||

| FL | 0.158 ** | 0.126 * | 0.319 ** | 0.168 ** | 1 | |

| FP | 0.389 ** | 0.444 ** | 0.606 ** | 0.302 ** | 0.341 ** | 1 |

| Hypotheses | Direct Effect | p | Indirect Effect | p | Total Effect | p |

|---|---|---|---|---|---|---|

| H4. FP<---ERM (through CA) | 0.401 | 0.001 | 0.033 | 0.006 | 0.434 | 0.001 |

| CA<---ERM | 0.193 | 0.005 | - | - | 0.193 | 0.005 |

| FP<---CA | 0.169 | 0.007 | - | - | 0.007 | |

| FP<---Size (through CA) | 0.147 | 0.001 | - | - | 0.147 | 0.001 |

| FP<---Age (through CA) | 0.156 | 0.001 | - | - | 0.156 | 0.001 |

| Estimate | S.E. | C.R. | P | |||

|---|---|---|---|---|---|---|

| CA | <--- | FLxERM | 0.029 | 0.010 | 2.826 | 0.005 |

| CA | <--- | Age | 0.031 | 0.023 | 1.362 | 0.173 |

| CA | <--- | Size | −0.006 | 0.024 | −0.248 | 0.804 |

| CA | <--- | ERM | 0.081 | 0.050 | 1.617 | 0.106 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, S.; Ishtiaq, M.; Anwar, M. Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy. J. Risk Financial Manag. 2018, 11, 35. https://doi.org/10.3390/jrfm11030035

Yang S, Ishtiaq M, Anwar M. Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy. Journal of Risk and Financial Management. 2018; 11(3):35. https://doi.org/10.3390/jrfm11030035

Chicago/Turabian StyleYang, Songling, Muhammad Ishtiaq, and Muhammad Anwar. 2018. "Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy" Journal of Risk and Financial Management 11, no. 3: 35. https://doi.org/10.3390/jrfm11030035

APA StyleYang, S., Ishtiaq, M., & Anwar, M. (2018). Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy. Journal of Risk and Financial Management, 11(3), 35. https://doi.org/10.3390/jrfm11030035