1. Introduction

Along with the swift development of the Chinese economy, the reliance on energy is gradually increasing, as is the demand. However, the widespread use of non-renewable fossil fuels releases large amounts of greenhouse gases (GHG), particularly CO

2, into the atmosphere, which is one of the primary causes of climate change today. China, as the world’s largest carbon emitter [

1], actively engages in international climate governance and diligently executes its emission reduction obligations under the Paris Agreement, which is critical to reaching global carbon neutrality. During the 75th session of the United Nations General Assembly on 22 September 2020, the Chinese government announced that China would scale up its Nationally Determined Contributions (NDCs) by adopting more vigorous policies and measures and strive to peak CO

2 emissions before 2030 and achieve carbon neutrality before 2060 [

2]. This is China’s solemn commitment to a community with a shared future for mankind. As a major strategic decision, the carbon neutrality commitment provides guidelines for China’s high-quality economic development and serves as the foundation for China’s actions to address climate change. After years of theoretical research and application in various industries, new energy has emerged as the most viable method to battle climate change and mitigate global warming [

3]. The development of new energy sources has become a necessity for countries worldwide to achieve carbon neutrality. Under such circumstances, it is necessary for China to intensively develop wind, solar, biomass, ocean and geothermal energy, as well as other new energy sources. In 2020, the global demand for renewable energy increased by 3% [

4], with China being the largest contributor to renewable energy growth [

5]. Nevertheless, renewable energy projects still remain a challenge, especially for developing countries [

6].

We intend to explore the impact of carbon neutrality commitment on new energy companies in this paper. The reason is that the new energy sector, as an emerging industry, needs more support from national policies. It has been shown that incentive-based policies have a positive effect on new energy companies. On the one hand, some scholars have looked into the impact of government policies on new energy companies from the perspective of subsidies. Subsidies from the government can encourage R&D innovation in new energy firms [

7] and improve financial performance [

8,

9]. On the other hand, there are several investigations into the influence of financial support on new energy firms. Green credit may raise the value of new energy enterprises [

10], and stock prices can dramatically rise when companies announce the issuance of green bonds [

11]. However, to the best of our knowledge, there are few studies on the impact of environmental and climate policies on new energy companies at the academic level. Obviously, new energy companies may have a positive impact on the environment, and environmental and climate policies can generate feedback effects on the new energy industry. Carbon neutrality is an important policy in the current global response to climate change [

12]. Therefore, we seek to determine how the carbon neutrality commitment affects the development of new energy enterprises.

This study attempts to address the following three questions. First, how does the carbon neutrality commitment affect the development of companies in the new energy industry? Second, what are the impact mechanisms through which the carbon neutrality commitment promotes the development of new energy companies? Third, does the effect of the carbon neutrality commitment on new energy companies vary with the company’s characteristics and external environment? To answer these questions, this study explores the causal relationship between the carbon neutrality commitment and new energy enterprises’ value, using the panel data of Chinese A-share listed manufacturing companies from January 2019 to March 2022 as a sample. The results obtained in this paper may effectively encourage more capital flows into new energy industries while guiding enterprises to achieve low-carbon transition, promoting green economic development and ecological civilization construction while improving their value.

The remainder of this paper is organized as follows.

Section 2 reviews the literature and devises hypotheses based on the theory.

Section 3 introduces the methodology, variable selection and data sources.

Section 4 presents the empirical findings.

Section 5 presents the robustness tests. Finally,

Section 6 concludes and provides related suggestions.

6. Conclusions and Policy Implications

6.1. Conclusions

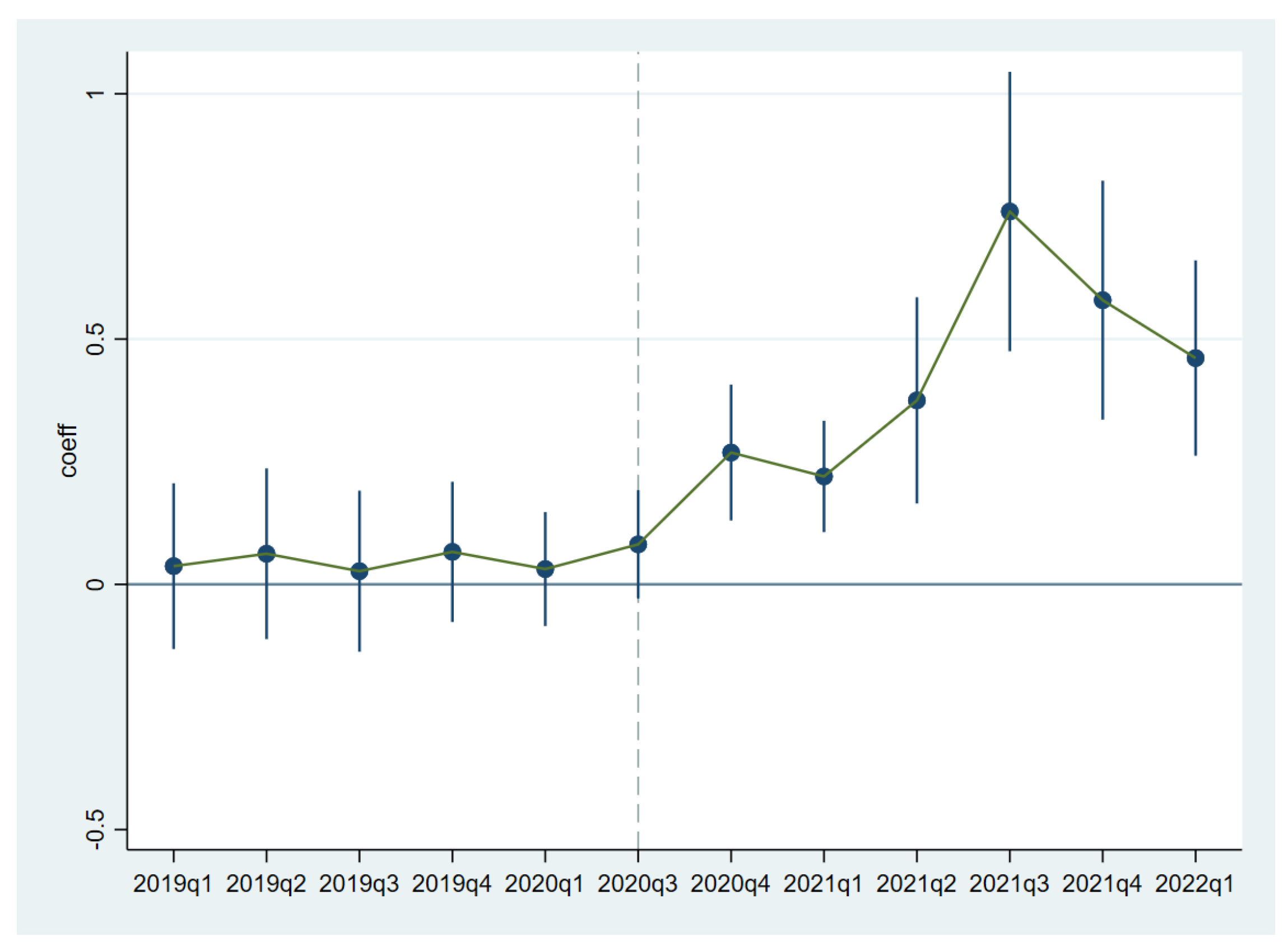

New energy plays an important role in achieving carbon neutrality. Based on quarterly panel data of 2101 Chinese A-share listed manufacturing companies from January 2019 to March 2022, this study applies the DID method to empirically test the impact of the carbon neutrality commitment on the sustainable development of new energy companies. The main conclusions are as follows.

First, China’s carbon neutrality commitment significantly improves the enterprise value of the new energy industry, and consequently contributes to the sustainable development of the companies. Thus far, the impact of carbon neutrality commitment on new energy enterprises has not been investigated. This paper conducts an empirical study with a sample of Chinese companies to confirm the positive impact of the carbon neutrality commitment on the sustainable growth of new energy companies.

Second, the profitability and investor sentiment are important mediating variables of the carbon neutrality commitment, influencing the sustainable growth of new energy enterprises. In China, investors will follow national policies to determine whether an industry or enterprise has investment value. As a strategic emerging industry, new energy needs more financial support for its development. Under the carbon neutrality commitment, investors will favor new energy companies, which will lead to more capital tilting toward the new energy industry. New energy enterprises can use these funds to develop technology and expand their business to achieve sustainable growth. In addition, under the constraint of carbon emission reduction, the demand for new energy products will increase, so that the revenue of new energy enterprises will also rise. For enterprises, profitability is the basis of their sustainable development. Therefore, overall, carbon neutrality commitment contributes to the sustainable development of new energy companies via investor sentiment and profitability.

Third, under the background of carbon neutrality, the value of non-state-owned new energy enterprises has been significantly improved, while the improvement effect of SOEs is less obvious. In addition, the impact of the carbon neutrality commitment on enterprise value improvement in the eastern region is more prominent than that in the central and western regions.

6.2. Policy Implications

Based on the above conclusions, this study puts forward the following policy implications.

First of all, for the government, it is advised to ensure the supply of the new energy industry, as well as providing government subsidies and financial support. Under the carbon neutrality commitment, new energy, which includes hydro, wind, solar, biomass and other types of renewable energy, is the main force of low-carbon energy development, and new energy enterprises will become an indispensable guideline for future high-quality economic development. If new energy enterprises benefit from the government’s policy support, they will be able to improve their own profitability and enterprise value, as well as achieve sustainable development, which in turn will continue to contribute to a reduction in carbon emissions. Furthermore, different preferential policies should be implemented for enterprises with different equity nature and regions. Non-state enterprises still account for a large share of new energy enterprises, and the government should continue to stimulate them through financial subsidies and tax rates to ensure their long-term and steady development. As for SOEs, the government should begin by improving their efficiency and attitude toward fair and equitable participation in market competition, and strengthening R&D and operational efficiency in order to achieve a significant increase in company value. Compared with the eastern region, the industrial development environment in the central and western regions is regressive, and under such conditions, the cultivation and development of new energy enterprises is also more difficult. Therefore, the government must provide more government subsidies and financial support to the central and western regions. In addition, there is also an important point, that is, we need to pay attention to the intensity of policy implementation. According to studies, if the government wrongly over-subsidizes, it will not only hinder the development of firms but may also lead to enterprise “cartilage”, which is not favorable to the healthy development of enterprises [

57]. Therefore, we should make dynamic adjustments to the implementation of the policy.

Secondly, new energy enterprises should fully utilize the positive effect brought about by national policy to improve operational enthusiasm. While focusing on the main business, it is also particularly important for new energy enterprises to improve the level of R&D and innovation. In these ways, they can gain a competitive advantage in the market and maintain a steady increase in enterprise value, so as to better and more quickly adapt to the needs of the new situation of high-quality development, and achieve a “win–win” situation for both enterprises.

Finally, investors should take the policy direction seriously and look for investment possibilities. There is no doubt that carbon neutrality has become a global political consensus. In this context, the value of new energy enterprises is improved, and a high enterprise value generally indicates that the company has more growth potential, profitability and investment opportunities, as well as higher development potential and prospects. As a result, investors may take advantage of the potential to increase their wealth while simultaneously contributing to the growth of the new energy industry and the achievement of carbon neutrality.

{kind=link}

{kind=link}

{kind=link}