A Comparative Cross-Sectional Study of the Prevalence and Determinants of Health Insurance Coverage in Nigeria and South Africa: A Multi-Country Analysis of Demographic Health Surveys

Abstract

1. Introduction/Background

2. Methodology

2.1. Study Settings

2.2. Justification of the Study Settings

2.3. Study Design

2.4. Data Sources

2.5. Sampling Procedures

2.6. Measures

2.6.1. Outcome Variables

2.6.2. Independent Variables

2.7. Statistical Analysis

2.8. Ethical Considerations

2.9. Patient and Public Involvement

3. Results

3.1. Demographic Characteristics of the Respondents

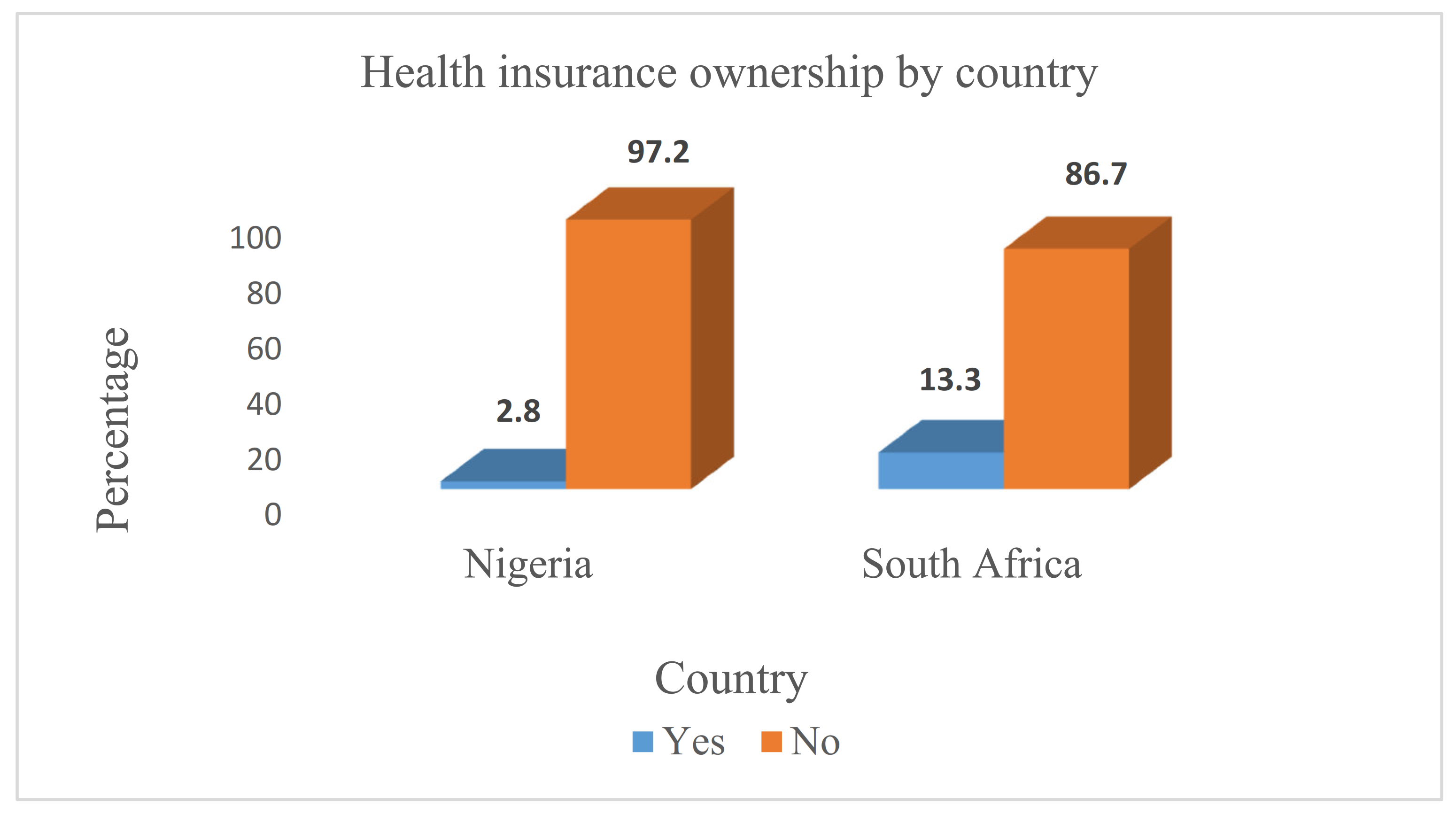

3.2. Distribution of Health Insurance Coverage by Country

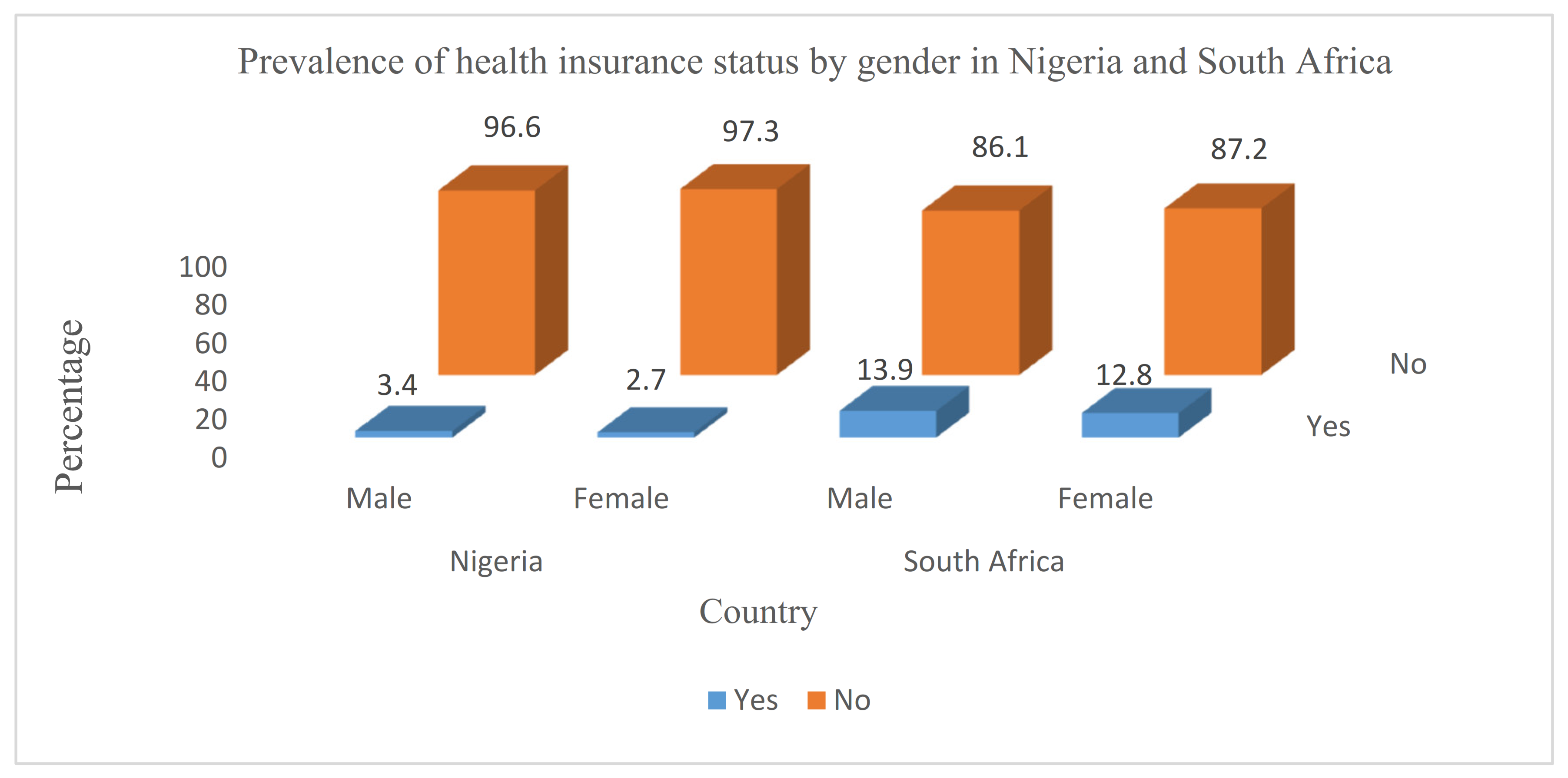

3.3. Distribution of Health Insurance Status by Gender in Nigeria and South Africa

3.4. Distribution of Respondents by Health Insurance Status and Socio-Demographic Factors

3.5. Determinants of Health Insurance Coverage

4. Discussion

5. Further Discussion: Sustaining Health Insurance Coverage via Public Health Financing in Nigeria and South Africa

6. Strengths and Limitations

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

References

- Asakitikpi, A.E. Healthcare Coverage and Affordability in Nigeria: An Alternative Model to Equitable Healthcare Delivery; Universal Health, Coverage; Isabel, A., Ed.; IntechOpen: London, UK, 2019. [Google Scholar]

- Oyekola, I.A.; Ojediran, J.O.; Ajani, O.A.; Oyeyipo, E.J.; Rasak, B. Advancing alternative health care financing through effective community partnership: A necessity for universal health coverage in Nigeria. Cogent Soc. Sci. 2020, 6, 1776946. [Google Scholar]

- Michel, J.; Tediosi, F.; Egger, M.; Barnighausen, T.; McIntyre, D.; Tanner, M.; Evans, D. Universal health coverage financing South Africa: Wishes vs. reality. J. Glob. Health Rep. 2020, 4, e2020061. [Google Scholar] [CrossRef]

- Valiani, S. Structuring sustainable universal health care in South Africa. Int. J. Health Serv. 2020, 5, 234–245. [Google Scholar] [CrossRef] [PubMed]

- Online Website: World Health Organization (WHO). Universal Health Coverage (UHC). World Health Organization Publication. 2021. Available online: www.who.int/news-room/fact-sheets/detail/universal-health-coverage-(uhc) (accessed on 3 May 2021).

- Nemati, E.; Khezri, A.; Nosratnejad, S. The Study of Out-of-pocket Payment and the Exposure of Households with Catastrophic Health Expenditures Following the Health Transformation Plan in Iran. Risk Manag. Healthc. Policy 2020, 13, 1677–1685. [Google Scholar] [CrossRef]

- Koch, S.F.; Setshegetso, N. Catastrophic health expenditures arising from out-of-pocket payments: Evidence from South African income and expenditure surveys. PLoS ONE 2020, 15, e0237217. [Google Scholar] [CrossRef]

- United Nations. Policy Brief: COVID-19 and Universal Health Coverage: Executive Summary; United Nations: San Francisco, CA, USA, 2020; pp. 1–23. [Google Scholar]

- Ilesanmi, O.; Adebiyi, A.; Fatiregun, A. National health insurance scheme: How protected are households in Oyo State, Nigeria from catastrophic health expenditure? Int. J. Health Policy Manag. 2014, 2, 175–180. [Google Scholar] [CrossRef]

- Ssewanyana, S.; Kasirye, I. Estimating catastrophic health expenditures from household surveys: Evidence from living standard measurement surveys (LSMS)–Integrated Surveys on Agriculture (ISA) from sub-Saharan Africa. Appl. Health Econ. Health Policy 2020, 18, 781–788. [Google Scholar] [CrossRef]

- Omwujekwe, O.; Ezumah, N.; Mbachu, C.; Obi, F.; Ichoku, H.; Uzochukwu, B.; Wang, H. Exploring effectiveness of different health financing mechanisms in Nigeria; what needs to change and how can it happen? BMC Health Serv. Res. 2019, 19, 661. [Google Scholar]

- Acharya, A.; Vellakkal, S.; Taylor, F.; Masset, E.; Satija, A.; Burke, M.; Ebrahim, S. Impact of National Health Insurance for the Poor and the Informal Sector in Low-and Middle-Income Countries: A Systematic Review; London: EPPI–Centre, Social Science Research Unit, Institute of Education, University of London:: London, UK, 2012. [Google Scholar]

- Adebayo, E.F.; Uthman, O.A.; Wiysonge, C.S.; Stern, E.A.; Lamont, K.T.; Ataguba, J.E. A systematic review of factors that affect uptake of community-based health insurance in low-income and middle-income countries. BMC Health Serv. Res. 2015, 15, 543. [Google Scholar] [CrossRef]

- Tediosi, F.; Lönnroth, K.; Pablos-Méndez, A.; Raviglione, M. Build back stronger universal health coverage systems after the Covid-19 pandemic: The need for better governance and linkage with universal social protection. BMJ Glob. Health 2020, 5, e004020. [Google Scholar] [CrossRef]

- Hussain, R.; Arif, S. Universal health coverage and Covid-19: Recent developments and implications. J. Pharm. Policy Pract. 2021, 14, 23. [Google Scholar] [CrossRef]

- Adisa, O. Investigating determinants of catastrophic health spending among poorly insured elderly households in urban Nigeria. Int. J. Equity Health 2015, 14, 79. [Google Scholar] [CrossRef]

- Sithole, S.L.; Mathonsi, N.S. Local governance service delivery issues during Apartheid and Post-Apartheid South Africa. Afr. Public Serv. Deliv. Perform. Rev. 2015, 3, 5–30. [Google Scholar] [CrossRef]

- Anand, R.; Kothari, S.; Kumar, N. In International Monetary Fund (IMF). Working papers on labour market dynamics and inequality in South Africa. IMF Work. Pap. Afr. Dev. 2016, WP/16/137, 1–37. [Google Scholar]

- Ifeagwu, S.C.; Yang, J.C.; Parkes-Ratanshi, R.; Brayne, C. Health financing for universal health coverage in sub-Saharan Africa: A systematic review. Glob. Health Res. Policy 2021, 6, 8. [Google Scholar] [CrossRef]

- Akokuwebe, M.E.; Adekanbi, D.M. Corruption in the health sector and implications for service delivery in Oyo State public hospitals. Ilorin J. Sociol. 2017, 9, 200–217. [Google Scholar]

- Rispel, L.C.; de Jager, P.; Fonn, S. Exploring corruption in the South African health sector. Health Policy Plan 2016, 31, 239–249. [Google Scholar] [CrossRef]

- Wagstaff, A.; Eozenou, P.; Smitz, M. Out-of-pocket expenditures on health: A global stocktake. World Bank Res. Obs. 2020, 35, 123–157. [Google Scholar] [CrossRef]

- McLeod, H.; Ramjee, S. Medical Schemes, in South African Health Review; Harrison, S., Bhana, R., Ntuli, A., Eds.; Health Systems Trust: Durban, South Africa, 2007; pp. 47–70. [Google Scholar]

- Mayosi, B.M.; Lawn, J.E.; Van Niekerk, A.; Bradshaw, D.; Abdool Karim, S.S.; Coovadia, H.M. Health in South Africa: Changes and challenges since 2009. Lancet 2012, 380, 2020–2043. [Google Scholar] [CrossRef]

- Naidoo, S. The South African national health insurance: A revolution in health-care delivery! J. Public Health 2012, 34, 149–150. [Google Scholar] [CrossRef]

- Online Website: MacroTrends. South Africa Population Growth Rate 1950–2021. MacroTrends Projection Publications. 2021. Available online: www.macrotrends.net/countries/ZAF/south-africa/population-growth-rate (accessed on 27 April 2021).

- Online Website: MacroTrends. South Africa GDP Per Capita 1960–2021. MacroTrends Projection Publications. 2021. Available online: www.macrotrends.net/countries/ZAF/south-africa/gdp-per-capita (accessed on 26 April 2021).

- Ogundeji, Y.K.; Akomolafe, B.; Ohiri, K.; Butawa, N.N. Factors influencing willingness and ability to pay for social health insurance in Nigeria. PLoS ONE 2019, 14, e0220558. [Google Scholar] [CrossRef] [PubMed]

- Kong, N.Y.; Kim, D.H. Factors influencing healthcare use by health insurance subscribers and medical aid beneficiaries: A study based on data from the Korea welfare panel study database. BMC Public Health 2020, 20, 1133. [Google Scholar] [CrossRef] [PubMed]

- Duku, S.K.O. Differences in the determinants of health enrollment among working-age adults in two regions in Ghana. BMC Health Serv. Res. 2018, 18, 384. [Google Scholar] [CrossRef] [PubMed]

- World Health Organization (WHO). Health Inequities and Their Causes. World Health Organization Newsletters. 2018. Available online: https://www.who.int/news-room/facts-in-pictures/detail/hea lth-inequities-and-their-causes (accessed on 23 August 2021).

- Bambra, C. Levelling up: Global examples of reducing health inequalities. Scand. J. Public Health 2021, 1–6. [Google Scholar] [CrossRef]

- Ebegbulem, J.C. An evaluation of Nigeria−South Africa Bilateral Relations. J. Int. Relat. Foreign Policy 2013, 1, 32–40. [Google Scholar]

- Francisca, I. The theory and practice of electoral processes in a democratic transition: A comparative study of Nigeria and South Africa (1999–2004). Afr. J. Multidiscip. Res. 2019, 4, 44–57. [Google Scholar]

- National Department of Health (NDoH); Statistics South Africa (Stats SA); South African Medical Research Council (SAMRC); ICF. South Africa Demographic and Health Survey 2016; NdoH: Pretoria, South Africa; Stats SA: KwaDukuza, South Africa; SAMRC: Cape Town, South Africa; ICF: Rockville, MD, USA, 2019; pp. 247–248. [Google Scholar]

- National Population Commission (NPC); ICF. Nigeria Demographic and Health Survey 2018; NPC: Abuja, Nigeria; ICF: Rockville, MD, USA, 2019; pp. 48–49. [Google Scholar]

- Online Website: MEASURE DHS and ICF International, Standard recode Manual for DHS 6, in Demographic and Health Surveys Methodology 2013, USAID. Available online: www.dhsprogram.com/pubs/pdf/DHSG4/Recode6_DHS_29th April2021_D HSG4.pdf (accessed on 29 April 2021).

- Online Website: Demographic and Health Survey Program. Wealth Index Construction. Available online: www.dhs program.com/topics/wealth-index/wealth-index-construction.cfm (accessed on 29 April 2021).

- Stats, S.A. Census 2011. Frequently asked questions (FAQ); Stats SA Department, Statistics South Africa: KwaDukuza, South Africa, 2011. [Google Scholar]

- Barasa, E.; Kazungu, J.; Nguhiu, P.; Ravishan, N. Examining the level and inequality in health insurance coverage in 36 sub-Saharan African countries. BMJ Glob. Health 2021, 6, e004712. [Google Scholar] [CrossRef]

- Weldesenbet, A.B.; Kebede, S.A.; Ayele, B.H.; Tusa, B.S. Health insurance coverage and its associated Factors among reproductive-age women in East Africa: A multilevel mixed-effects generalized linear model. Clin. Econ. Outcomes Res. 2021, 13, 693–701. [Google Scholar] [CrossRef]

- United Nations Children’s Fund (UNICEF). Health Budgets Brief of South Africa; UNICEF: New York, NY, USA, 2020; pp. 1–24. [Google Scholar]

- Adebisi, Y.A.; Umah, J.O.; Olaoye, O.C.; Alaran, A.J.; Sina-Odunsi, A.B.; Lucero-Prisno, E. III. Assessment of health budgetary allocation and expenditure toward achieving universal health coverage in Nigeria. Int. J. Health Life Sci. 2020, 6, e102552. [Google Scholar] [CrossRef]

- Smith, E. Foreign Investors are Gearing up to Plug Nigeria’s $82 Billion Health-Care Gap. 2021. Available online: https://ww w.cnbc.com/2021/01/04/nigerias-82-billion-health-care-gap-investors-stan d-by.html (accessed on 14 August 2021).

- Kamara, J.; Jofre-Bonet, M.; Mesnard, A. A discrete choice experiment to elicit the willingness to pay for health insurance by the informal sector workers in Sierra Leone. Int. J. Health Econ. Policy 2018, 3, 1–12. [Google Scholar] [CrossRef]

- Adebola, O.G. Universal health coverage in Nigeria and its determinants: The case of National Health Insurance Scheme. Acad. Rev. Humanit. Soc. Sci. 2020, 3, 97–111. [Google Scholar]

- Tandwa, L.A.; DhI, A. Public engagement in the development of the National Health Insurance: A study involving patients from a central hospital in South Africa. BMC Public Health 2020, 21, 1191. [Google Scholar] [CrossRef] [PubMed]

- Shimamura, Y.; Matsushima, M.; Yamada, H.; Nguyen, M. Willingness-to-pay for family-based health insurance: Findings from household and health facility surveys in Central Vietnam. Glob. J. Health Sci. 2018, 10, 24. [Google Scholar] [CrossRef]

- Abaerei, A.A.; Ncayiyana, J.; Levin, J. Health-care utilization and associated factors in Gauteng Province, South Africa. Glob. Health Action 2017, 10, 1–9. [Google Scholar] [CrossRef]

- Evans, M.; Shisana, O. Gender differences in public perceptions on National Health Insurance. SAMJ 2012, 102, 918–924. [Google Scholar] [CrossRef][Green Version]

- Azad, A.D.; Charles, A.G.; Ding, Q.; Trickey, A.W.; Wren, S.M. The gender gap and healthcare: Associations between gender roles and factors affecting healthcare access in Central Malawi, June–August 2017. Arch. Public Health 2020, 78, 119. [Google Scholar] [CrossRef]

- Oraro, T.; Ngube, N.; Atohmbom, G.Y.; Srivastava, S.; Wyss, K. The influence of gender and household headship on voluntary health insurance: The case of North-West Cameroon. Health Policy Plan 2018, 33, 163–179. [Google Scholar] [CrossRef]

- Abuya, T.; Maina, T.; Chuma, J. Historical account of the national health insurance formulation in Kenya: Experiences from the past decade. BMC Health Serv. Res. 2015, 15, 56. [Google Scholar] [CrossRef]

- Macharia, B.G.; Mwangi, E.M.; Oluoch, M. Factors influencing uptake of social health insurance in Kenya: A case of Nyeri County. Int. J. Curr. Bus. Soc. Sci. (IJCBSS) 2017, 1, 117–194. [Google Scholar]

- Oraro, T.; Wyss, K. How does membership in local savings groups influence the determinants of national health insurance demand? A cross-sectional study in Kisumu, Kenya. Int. J. Equity Health 2018, 17, 170. [Google Scholar] [CrossRef]

- Kirgia, J.M.; Sambogo, L.G.; Nganda, B.; Mwabu, G.M.; Chatora, R.; Mwase, T. Determinants of health insurance ownership among South Africa women. BMC Health Serv. Res. 2005, 5, 17. [Google Scholar]

- Amu, H.; Abdul-Aziz, S.; Agbaglo, E.; Dowou, R.K.; Ameyaw, E.K.; Ahinkorah, B.D.; Kissah-Korsah, K. Mixed effects analysis of factors associated with health insurance coverage among women in sub-Saharan Africa. PLoS ONE 2021, 16, e02484111. [Google Scholar] [CrossRef]

- Amusan, L.; Akokuwebe, M.E.; Odularu, G. Women development in agriculture as agency for fostering innovative agricultural financing in Nigeria. Afr. J. Food Agric. Nutr. Dev. 2021, 21, 18279–18299. [Google Scholar]

- Ayanore, M.A.; Pavlova, M.; Kugbey, N.; Fusheini, A.; Tetteh, J.; Ayanore, A.A.; Akazili, J.; Adongo, P.B.; Groot, W. Health insurance coverage, type of payment for health insurance, and reasons for not being insured under the National Health Insurance Scheme in Ghana. Health Econ. Rev. 2019, 9, 39. [Google Scholar] [CrossRef]

- Kaplan, J.; Ranchod, S. Analysing the Structure and Nature of Medical Scheme Benefit Design in South Africa, in South African Health Review; Padarath, A., King, J., English, R., Eds.; Health Systems Trust: Durban, South Africa, 2015. [Google Scholar]

- Sanogo, N.S.; Fantaye, A.W.; Yaya, S. Universal Health Coverage and Facilitation of Equitable Access to Care in Africa. Front. Public Health 2019, 7, 102. [Google Scholar] [CrossRef]

- Onasanya, A.A. Increasing health insurance enrolment in the informal economic sector. JOGH 2020, 10, 0103129. [Google Scholar] [CrossRef]

- Spaan, E.; Mathijssen, J.; Tromp, N.; McBain, F.; ten Have, A.; Baltussen, R. The impact of health insurance in Africa and Asia: A systematic review. Bull. World Health Organ. 2012, 90, 685–692. [Google Scholar] [CrossRef]

- Dovlo, D. People and their health systems: The right to universal health coverage and the SDGs in Africa. In Sustainable Development Goals and Human Rights. Interdisciplinary Studies in Human Rights; Kaltenborn, M., Krajewski, M., Kuhn, H., Eds.; Springer: Clam, Switzerland, 2019; Volume 5. [Google Scholar]

- Shittu, A.K.; Afolabi, O.S. Community Based health insurance scheme and state-local relations in rural and semi-urban areas of Lagos State, Nigeria. Public Organiz. Rev. 2021, 21, 19–31. [Google Scholar] [CrossRef]

- Chaudhuri, S. Urban poor, economic opportunities and sustainable development through traditional knowledge and practices. Glob. Bioeth. 2015, 26, 2. [Google Scholar] [CrossRef]

- Kuddus, M.A.; Tynan, E.; McBryde, E. Urbanization: A problem for the rich and the poor? Public Health Rev. 2020, 41, 1. [Google Scholar] [CrossRef]

- Fusheini, A.; Eyles, J. Achieving universal health coverage in South Africa through a district health system approach: Conflicting ideologies of healthcare provision. BMC Health Serv. Res. 2016, 16, 558. [Google Scholar] [CrossRef] [PubMed]

- Mhlanga, D.; Garidzirai, R. The influence of racial differences in the demand for healthcare in South Africa: A case of public healthcare. Int. J. Environ. Res. Public Health 2020, 17, 5043. [Google Scholar] [CrossRef] [PubMed]

- Marmot, M.; Friel, S.; Bell, R.; Houweling, T.A.; Taylor, S. Commission on social determinants of health. Closing the gap in a generation: Health equity through action on the social determinants of health. Lancet 2008, 372, 1661–1669. [Google Scholar] [CrossRef]

- Gordon, T.; Booysen, F.; Mbonigaba, J. Socio-economic inequalities in the multiple dimensions of access to health care: The case of South Africa. BMC Public Health 2020, 20, 289. [Google Scholar] [CrossRef]

- Morudu, P.; Kollamparambil, U. Health shocks, medical insurance and household vulnerability: Evidence from South Africa. PLoS ONE 2020, 15, e0228034. [Google Scholar] [CrossRef]

- Akokuwebe, M.E.; Odimegwu, C.; Omololu, F. Prevalence, risk-inducing lifestyle, and perceived susceptibility to kidney diseases by gender among Nigerians residents in South Western Nigeria. Afr. Health Sci. 2020, 20, 860–870. [Google Scholar] [CrossRef]

- Akokuwebe, M.E.; Odimegwu, C. Socioeconomic Determinants of Knowledge of Kidney Disease among Residents in Nigeria Communities in Lagos State, Nigeria. Oman. Med. J. 2019, 34, 444–455. [Google Scholar] [CrossRef]

- Onoka, C.A.; Hanson, K.; Hanefeld, J. Towards universal coverage: A policy analysis of the development of the National Health Insurance Scheme in Nigeria. Health Policy Plan. 2015, 30, 1105–1117. [Google Scholar] [CrossRef]

- World Bank Group. Sub-Saharan Africa South Africa. World Bank Group Poverty & Equity Brief April 2020. Available online: https://povertydata.worldbank.org/poverty/home/ (accessed on 14 June 2021).

- Stats, S.A. Media Release of Quarterly Labour Force Survey (QLFS)–Q1: 2021; Department Statistics South Africa Employment: KwaDukuza, South Africa, 2021. [Google Scholar]

- Trading Economic. South Africa Employment Rate. 2021. Available online: https://tradingeconomics.com/south-africa/employment-rate (accessed on 24 July 2021).

- Trading Economics. Nigeria Employment Rate. 2021. Available online: https://tradingeconomics.com/nigeria/employment-rate (accessed on 12 August 2021).

- BusinessTech. South Africa’s Unemployment Rate Hits New All-Time High. Business Tech Staff Writer. 2021. Available online: https://businesstech.co.za/news/government/495075/south-africas-unemployment-rate-hits-new-all-time-high/June1st2021 (accessed on 1 June 2021).

- Chukwu, E.; Garg, L.; Eze, G. Mobile health insurance system and associated costs: A cross-sectional survey of primary health centers in Abuja, Nigeria. JMIR Mhealth Uhealth 2016, 4, e37. [Google Scholar] [CrossRef]

- Peterson, L.; Comfort, A.; Hatt, L.; van Bastelaer, T. Extending health insurance coverage to the informal sector: Lessons from a private micro health insurance scheme in Lagos, Nigeria. Int. J. Health Plan. Manag. 2018, 33, 5–10. [Google Scholar] [CrossRef]

- Tungu, M.; Amani, P.J.; Hurtig, A.-K.; Kiwara, A.D.; Mwanga, M.; Lindholm, L.; Sebastian, M.S. Does health insurance contribute to improve utilization of health care services for the elderly in rural Tanzania? A cross-sectional study. Glob. Health Action 2020, 13, 1841962. [Google Scholar] [CrossRef]

- Passchier, R.V. Exploring the barriers to implementing national health insurance in South Africa: The People’s perspectives. SAMJ 2017, 107, 836–838. [Google Scholar] [CrossRef]

- Murray, A.; O’Neill, D. Health-care equity-for all generations? Lancet 2009, 373, 299. [Google Scholar] [CrossRef]

- Lee, J.; Schram, A.; Riley, E.; Harris, P.; Baum, F.; Fisher, M.; Freeman, T.; Friel, S. Addressing health equity through action on the social determinants of health: A global review of policy outcome evaluation methods. IJHPM (Int. J. Health Policy Manag.) 2018, 7, 581–592. [Google Scholar] [CrossRef]

- Oduniyi, O.S.; Antwi, M.A.; Tekana, S.S. Farmers’ willingness to pay for index-based livestock insurance in the North West of South Africa. Climate 2020, 8, 47. [Google Scholar] [CrossRef]

- Singu, S.; Acharya, A.; Challagundla, K.; Byrareddy, S.N. Impact of social determinants of health on the emerging COVID-19 pandemic in the United States. Front. Public Health 2020, 8, 406. [Google Scholar]

- Mondal, M.N.; Shitan, M. Relative importance of demographic, socioeconomic and health factors on life expectancy in low-and lower-middle-income countries. J. Epidemiol. 2014, 24, 117–124. [Google Scholar] [CrossRef]

- Goudge, J.; Alaba, O.A.; Govender, V.; Harris, B.; Nxumalo, N.; Chersich, M.F. Social health insurance contributes to universal coverage in South Africa, but generates inequities: Survey among members of a government employee insurance scheme. Int. J. Equity Health 2018, 17, 1–13. [Google Scholar] [CrossRef]

- Shobiye, H.O.; Dada, I.; Ndili, N.; Zamba, E.; Feeley, F.; de Rinke Wit, T. Determinants and perception of health insurance participation among healthcare providers in Nigeria: A mixed-methods study. PLoS ONE 2021, 16, e0255206. [Google Scholar] [CrossRef]

- World Health Organization (WHO). Keeping to the Universal Health Coverage Path in Kenya. World Health Organization Africa|Kenya. 2020. Available online: www.afro-who-int/news/keeping-universal-health-coverage-path-kenya (accessed on 20 January 2022).

- Munge, K.; Mulupi, S.; Barasa, E.; Chuma, J. A critical analysis of purchasing arrangements in Kenya: The case of micro health insurance. BMC Health Serv. Res. 2019, 19, 45. [Google Scholar] [CrossRef]

- Muthaka, D. The role of private health insurance in financing health care in Kenya. In Private Health Insurance: History, Politics and Performance, edited by Sarah Thomson, Anna Sagan & Elias Mossialos, authored by Jonathan North, European Observatory on Health Systems and Policies; Cambridge University Press: Cambridge, UK, 2020; pp. 325–348. [Google Scholar]

- Whyle, E.B.; Olivier, J. Models of public private engagement for health services delivery and financing in Southern Africa: A systematic review. Health Policy Plan. 2016, 31, 1515–1529. [Google Scholar] [CrossRef]

- Deinne, C.E.; Ajayi, D.D. Dynamics of inequality, poverty and sustainable development of Delta State, Nigeria. Geo J. 2021, 86, 431–443. [Google Scholar] [CrossRef]

- Noaratnejad, S.; Rashidian, A.; Dror, D.M. Systematic review of willingness to pay for health insurance in low- and middle-income countries. PLoS ONE 2016, 11, e0157470. [Google Scholar]

- Akokuwebe, M.E.; Idemudia, E.S. Multilevel Analysis of Urban–Rural Variations of Body Weights and Individual-Level Factors among Women of Childbearing Age in Nigeria and South Africa: A Cross-Sectional Survey. Int. J. Environ. Res. Public Health. 2022, 19, 125. [Google Scholar] [CrossRef]

- Aregbeshola, B.S.; Khan, S.M. Out-of-Pocket Payments, Catastrophic Health Expenditure and Poverty among Households in Nigeria 2010. Int. J. Health Policy Manag. (IJHPM) 2018, 7, 798–806. [Google Scholar] [CrossRef]

- Akokuwebe, M.E.; Idemudia, E.S. Prevalence and Socio-demographic Correlates of Body Weight Categories among South African Women of reproductive Age: A Cross-sectional Study. Front. Public Health Sect. Life-Course Epidemiol. Soc. Inequalities Health 2021, 9, 1–17. [Google Scholar] [CrossRef] [PubMed]

- Mutyambiz, C.; Pavlova, M.; Hongoro, C.; Booysten, F.; Groot, W. Incidence, socio-economic inequalities and determinants of catastrophic health expenditure and impoverishment for diabetes care in South Africa: A study at two public hospitals in Tshwane. Int. J. Equity Health 2019, 18, 73. [Google Scholar] [CrossRef] [PubMed]

- Malakoane, B.; Heunis, J.C.; Chikobvu, P.; Kigozi, N.G.; Kruger, W.H. Public health system challenges in the Free State, South Africa: A situation appraisal to inform health system strengthening. BMC Health Serv. Res. 2020, 20, 58. [Google Scholar] [CrossRef] [PubMed]

- Oleribe, O.O.; Momoh, J.; Uzochukwu, B.S.C.; Mbofana, F.; Adebiyi, A.; Barbera, T.; Williams, R.; Taylor-Robinson, S.D. Identifying key challenges facing healthcare systems in Africa and potential solutions. Int. J. Gen. Pract. 2019, 12, 395–403. [Google Scholar] [CrossRef] [PubMed]

- Falchetta, G.; Hammad, A.T.; Shayegh, S. Planning universal accessibility to public health care in sub-Saharan Africa. Proc. Natl. Acad. Sci. USA 2020, 117, 31760–31769. [Google Scholar] [CrossRef] [PubMed]

- World Health Organization (WHO). The World Health Report. Health Systems: Improving Performance. Geneva: WHO. 2000. Available online: www.who.int/whr/2000/en/whr00_en.pdf? (accessed on 18 January 2022).

- World Health Organization (WHO). Everybody’s Business-Strengthening Health Systems to Improve Outcomes: WHO’s Framework for Action. Geneva: WHO. 2007. Available online: www.who.int/healthsystems/strategy/every bodys_business.pdf (accessed on 19 January 2022).

- Liaropoulos, L.; Goranitis, I. Health care financing and the sustainability of health systems. Int. J. Equity Health 2015, 14, 80. [Google Scholar] [CrossRef]

- Siringi, S. Kenya promises care for all with launch of health insurance scheme. Lancet 2001, 358, 1884. [Google Scholar] [CrossRef]

- Abiola, A.O.; Ladi-Akinyemi, T.W.; Oyeleye, O.A.; Oyeleke, G.K.; Olowoselu, O.I.; Abdulkareem, A.T. Knowledge and utilization of National Health Insurance Scheme among adult patients attending a tertiary health facility in Lagos State, South-Western Nigeria. Afr. J. Prm. Health Care Fam. Med. 2019, 11, a2018. [Google Scholar]

{kind=link}

{kind=link}

| Description | Nigeria | South Africa |

|---|---|---|

| Region | Western Africa | Southern Africa |

| Topography | Coastal with varied landscape | Coastal high and low lands |

| Total land area | 923,769 km2 | 1,213,090 km2 |

| Total population | 211,400,708 | 60,093,707 |

| % rural population | 48.04% | 33.3% |

| % urban population | 51.96% | 66.7% |

| Labor force categories | Mainly engaged in professional labor (federal, state and local government, ministries, departments and agencies). Few are engaged in non-professional labor (technical, skilled manual, unskilled manual and agriculture). | Few are engaged in formal sector (non-agricultural). Mainly engaged in informal sector (non-agricultural), agriculture and private households. |

| Country unemployment rate | 32.5% | 32.6% |

| Country employment rate | 66.7% | 38.0% |

| Labor force participation rate | 53.41% | 56.4% |

| % of age dependency ratio | 86.7% | 52.23% |

| NHIS coverage (%) by gender Women Men | 3% 3% | 16% 17% |

| Variables | Nigeria | South Africa | ||||

|---|---|---|---|---|---|---|

| All No. (%) | Men No. (%) | Women No. (%) | All No. (%) | Men No. (%) | Women No. (%) | |

| Age | ||||||

| 15–24 | 19,286 (35.0) | 4019 (30.2) | 15,267 (36.5) | 4220 (34.8) | 1307 (36.1) | 2913 (34.2) |

| 25–34 | 16,569 (30.1) | 3369 (25.3) | 13,200 (31.6) | 3620 (29.8) | 928 (25.7) | 2692 (31.6) |

| 35–44 | 12,751 (23.1) | 3288 (24.7) | 9463 (22.6) | 2670 (22.0) | 674 (18.6) | 1996 (23.4) |

| 45–59 | 6526 (11.8) | 2635 (19.8) | 3891 (9.3) | 1622 (13.4) | 709 (19.6) | 913 (10.7) |

| Education | ||||||

| No education | 17,344 (31.5) | 2946 (22.1) | 14,398 (34.4) | 324 (2.7) | 134 (3.7) | 190 (2.2) |

| Primary | 8297 (15.0) | 1914 (14.4) | 6383 (15.3) | 1467 (12.1) | 605 (16.7) | 862 (10.1) |

| Secondary | 22,898 (41.5) | 6200 (46.6) | 16,698 (39.9) | 9129 (75.2) | 2548 (70.4) | 6581 (77.3) |

| Higher | 6593 (12.0) | 2251 (16.9) | 4342 (10.4) | 1212 (10.0) | 331 (9.2) | 881 (10.4) |

| Place of residence | ||||||

| Urban | 22,690 (40.8) | 5506 (41.4) | 16,984 (40.6) | 6826 (56.3) | 2021 (55.9) | 4805 (56.4) |

| Rural | 32,642 (59.2) | 7805 (58.6) | 24,837 (59.4) | 5306 (43.7) | 1597 (44.1) | 3709 (43.6) |

| Wealth quintile | ||||||

| Poor | 20,967 (38.0) | 4874 (36.6) | 16,093 (38.5) | 5230 (43.1) | 1602 (44.3) | 3628 (42.6) |

| Middle | 11,717 (21.3) | 2858 (21.5) | 8859 (21.2) | 2800 (23.1) | 844 (23.3) | 1956 (23.0) |

| Rich | 22,448 (40.7) | 5579 (41.9) | 16,869 (40.3) | 4102 (33.8) | 1172 (32.4) | 2930 (34.4) |

| Marital status | ||||||

| Never married | 15,774 (28.6) | 5105 (38.4) | 10,669 (25.5) | 7375 (60.8) | 2241 (61.9) | 5134 (60.3) |

| Currently married | 36,906 (66.9) | 8018 (60.2) | 28,888 (69.1) | 4035 (33.3) | 1194 (33.0) | 2841 (33.4) |

| Previously married | 2452 (4.5) | 188 (1.4) | 2264 (5.4) | 722 (5.9) | 183 (5.1) | 539 (6.3) |

| Employment status | ||||||

| Unemployed | 16,508 (29.9) | 1742 (13.1) | 14,766 (35.3) | 7735 (63.8) | 1961 (54.2) | 5774 (67.8) |

| Employed | 38,624 (70.1) | 11,569 (86.9) | 27,055 (64.7) | 4397 (36.2) | 1657 (45.8) | 2740 (32.2) |

| Region | ||||||

| North Central | 10,187 (18.5) | 2415 (18.1) | 7772 (18.6) | - | - | - |

| North East | 10,086 (18.3) | 2447 (18.4) | 7639 (18.3) | - | - | - |

| North West | 13,089 (23.7) | 2960 (22.2) | 10,129 (24.2) | - | - | - |

| South East | 7326 (13.3) | 1755 (13.2) | 5571 (13.3) | - | - | - |

| South South | 6777 (12.3) | 1697 (12.8) | 5080 (12.1) | - | - | - |

| South West | 7667 (13.9) | 2037 (15.3) | 5630 (13.5) | - | - | - |

| Province | ||||||

| Western Cape | - | - | - | 876 (7.2) | 220 (6.1) | 656 (7.7) |

| Eastern Cape | - | - | - | 1516 (12.5) | 475 (13.1) | 1041 (12.2) |

| Northern Cape | - | - | - | 1017 (8.4) | 299 (8.3) | 718 (8.4) |

| Free State | - | - | - | 1190 (9.8) | 336 (9.3) | 854 (10.0) |

| KwaZulu-Natal | - | - | - | 1884 (15.5) | 524 (14.5) | 1360 (16.0) |

| North West | - | - | - | 1291 (10.6) | 428 (11.8) | 863 (10.1) |

| Gauteng | - | - | - | 1279 (10.5) | 416 (11.5) | 863 (10.1) |

| Mpumalanga | - | - | - | 1519 (12.5) | 465 (12.8) | 1054 (12.4) |

| Limpopo | - | - | - | 1560 (12.9) | 455 (12.6) | 1105 (12.0) |

| Population group | ||||||

| Black/African | - | - | - | 10,509 (86.6) | 3150 (87.1) | 7359 (86.4) |

| Other | - | - | - | 1623 (13.4) | 468 (12.9) | 1155 (13.6) |

| Variables | Nigeria | South Africa | ||||

|---|---|---|---|---|---|---|

| No (%) | Yes (%) | p-Value | No. (%) | Yes (%) | p-Value | |

| Gender | 0.132 | 0.145 | ||||

| Male | 12,861 (24.0) | 450 (28.7) | 3114 (46.0) | 504 (48.4) | ||

| Female | 40,704 (76.0) | 1117 (71.3) | 3656 (54.0) | 537 (51.6) | ||

| Age | 0.000 * | 0.000 * | ||||

| 15–24 | 18,984 (35.4) | 302 (19.3) | 2479 (36.6) | 244 (23.4) | ||

| 25–34 | 16,113 (30.1) | 456 (29.1) | 1988 (29.4) | 274 (26.3) | ||

| 35–44 | 12,205 (22.8) | 546 (34.8) | 1372 (20.3) | 291 (28.0) | ||

| 45–59 | 6263 (11.7) | 263 (16.8) | 931 (13.7) | 232 (22.3) | ||

| Education | 0.000 * | 0.000 * | ||||

| No education | 17,230 (32.2) | 114 (7.3) | 221 (3.3) | 9 (0.9) | ||

| Primary | 8237 (15.4) | 60 (3.8) | 979 (14.5) | 48 (4.6) | ||

| Secondary | 22,407 (41.8) | 491 (31.3) | 3140 (75.9) | 667 (64.1) | ||

| Higher | 5691 (10.6) | 902 (57.6) | 430 (6.3) | 317 (30.4) | ||

| Place of residence | 0.000 * | 0.000 * | ||||

| Urban | 21,413 (40.0) | 1077 (68.7) | 3603 (53.2) | 772 (74.2) | ||

| Rural | 32,152 (60.0) | 490 (31.3) | 3167 (46.8) | 269 (25.8) | ||

| Wealth index | 0.000 * | 0.000 * | ||||

| Poor | 20,875 (39.0) | 92 (5.9) | 3238 (47.8) | 133 (12.8) | ||

| Middle | 11,584 (21.6) | 133 (8.5) | 1670 (24.7) | 155 (14.9) | ||

| Rich | 21,106 (39.4) | 1342 (85.6) | 1862 (27.5) | 753 (72.3) | ||

| Marital status | 0.000 * | 0.000 * | ||||

| Never married | 15,403 (28.8) | 371 (23.7) | 4365 (64.5) | 449 (43.1) | ||

| Currently married | 35,758 (66.7) | 1148 (73.2) | 2009 (29.7) | 546 (52.5) | ||

| Previously married | 2404 (4.5) | 48 (3.1) | 396 (5.8) | 46 (4.4) | ||

| Employment status | 0.000 * | 0.000 * | ||||

| Unemployed | 16,142 (30.1) | 366 (23.4) | 4465 (65.9) | 362 (34.8) | ||

| Employed | 37,423 (69.9) | 1201 (76.6) | 2305 (34.1) | 679 (65.2) | ||

| Region | 0.000 * | |||||

| North Central | 9777 (18.3) | 410 (26.2) | - | - | ||

| North East | 9969 (18.6) | 117 (7.5) | - | - | ||

| North West | 12,712 (23.7) | 377 (24.1) | - | - | ||

| South East | 7135 (13.3) | 191 (12.2) | - | - | ||

| South South | 6599 (12.3) | 178 (11.4) | - | - | ||

| South West | 7373 (13.8) | 294 (18.7) | - | - | ||

| Province | 0.000 * | |||||

| Western Cape | - | - | 373 (5.5) | 143 (13.7) | ||

| Eastern Cape | - | - | 875 (12.9) | 108 (10.4) | ||

| Northern Cape | - | - | 563 (8.3) | 99 (9.5) | ||

| Free State | - | - | 670 (9.9) | 87 (8.4) | ||

| KwaZulu-Natal | - | - | 1089 (16.1) | 126 (12.1) | ||

| North West | - | - | 705 (10.4) | 121 (11.6) | ||

| Gauteng | - | - | 701 (10.4) | 139 (13.4) | ||

| Mpumalanga | - | - | 889 (13.1) | 99 (9.5) | ||

| Limpopo | - | - | 905 (13.4) | 119 (11.4) | ||

| Population group | 0.000 * | |||||

| Black African | - | - | 6078 (89.8) | 723 (69.4) | ||

| Other | - | - | 692 (10.2) | 318 (30.6) | ||

| Nigeria | South Africa | |||

|---|---|---|---|---|

| Model 1 (uOR) | Model 2 (aOR) | Model 1 (uOR) | Model 2 (aOR) | |

| OR (95% CI) | OR (95% CI) | OR (95% CI) | OR (95% CI) | |

| Gender | ||||

| Male | RC | RC | RC | RC |

| Female | 1.28 (1.15–1.43) * | 1.85 (0.75–1.97) * | 1.06 (0.93–1.20) * | 1.91 (0.78–2.05) * |

| Age | ||||

| 15–24 | RC | RC | RC | RC |

| 25–34 | 0.53 (0.46–0.62) * | 0.80 (0.67–0.96) * | 0.76 (0.64–0.90) * | 1.82 (1.46–1.98) * |

| 35–44 | 0.36 (0.31–0.42) * | 0.49 (0.40–0.60) * | 0.52 (0.43–0.61) * | 1.29 (1.02–1.63) * |

| 45–59 | 0.36 (0.30–0.42) * | 0.40 (0.32–0.50) * | 0.36 (0.30–0.43) * | 1.01 (0.78–1.32) * |

| Education | ||||

| No education | RC | RC | RC | RC |

| Primary | 1.07 (0.78–1.09) * | 1.05 (0.04–1.20) * | 1.05 (0.03–1.11) * | 1.01 (0.05–1.24) * |

| Secondary | 1.08 (0.06–1.10) * | 1.09 (0.95–1.88) * | 1.06 (0.05–1.28) * | 1.02 (0.15–1.67) * |

| Higher | 1.43 (0.34–1.54) * | 1.34 (0.28–1.42) * | 1.33 (0.16–1.66) * | 1.76 (0.34–1.82) * |

| Place of residence | ||||

| Urban | RC | RC | RC | RC |

| Rural | 3.23 (2.89–3.63) * | 1.07 (0.94–1.23) * | 2.52 (2.15–2.95) * | 0.60 (0.47–0.77) * |

| Region | ||||

| North Central | RC | RC | - | - |

| North East | 2.14 (1.72–2.67) * | 1.21 (0.96–1.52) | - | - |

| North West | 1.10 (0.94–1.30) | 0.59 (0.49–0.70) * | - | - |

| South East | 1.01 (0.83–1.23) | 1.56 (1.28–1.92) * | - | - |

| South South | 1.08 (0.89–1.32) | 1.75 (1.42–2.16) * | - | - |

| South West | 0.74 (0.63–0.87) * | 1.55 (1.30–1.85) * | - | - |

| Province | ||||

| Western Cape | - | - | RC | RC |

| Eastern Cape | - | - | 3.26 (2.52–4.21) * | 0.84 (0.61–1.16) |

| Northern Cape | - | - | 2.53 (1.58–4.05) * | 1.26 (0.74–2.16) |

| Free State | - | - | 3.24 (2.29–4.57) * | 1.07 (0.72–1.61) |

| KwaZulu-Natal | - | - | 3.36 (2.68–4.20) * | 1.06 (0.80–1.40) |

| North West | - | - | 2.12 (1.61–2.78) * | 0.53 (0.37–0.75) * |

| Gauteng | - | - | 2.13 (1.77–2.57) * | 0.93 (0.73–1.22) |

| Mpumalanga | - | - | 3.77 (2.79–5.10) * | 1.08 (0.74–1.57) |

| Limpopo | - | - | 3.02 (2.32–3.94) * | 0.63 (0.44–0.89) * |

| Population group | ||||

| African/Black | - | - | RC | RC |

| Others | - | - | 1.19 (0.16–1.21) * | 1.43 (0.35–1.53) * |

| Wealth quintile | ||||

| Poor | RC | RC | RC | RC |

| Middle | 0.49 (0.38–0.65) * | 0.65 (0.49–0.87) * | 0.34 (0.26–0.44) * | 0.40 (0.31–0.53) * |

| Rich | 1.09 (0.07–1.11) * | 1.20 (0.15–1.25) * | 1.07 (0.06–1.10) * | 1.10 (0.08–1.13) * |

| Marital status | ||||

| Never married | RC | RC | RC | RC |

| Currently married | 1.11 (0.82–1.50) * | 1.20 (0.86–1.68) * | 1.83 (0.61–1.98) * | 1.05 (0.74–1.51) * |

| Previously married | 0.74 (0.65–0.83) | 0.74 (0.63–0.87) | 0.38 (0.33-.043) | 0.53 (0.44–0.63) |

| Employment status | ||||

| Unemployed | RC | RC | RC | RC |

| Employed | 1.69 (0.61–1.78) * | 1.05 (0.91–1.21) | 1.24 (0.21–1.37) * | 1.33 (0.28–1.50) * |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Akokuwebe, M.E.; Idemudia, E.S. A Comparative Cross-Sectional Study of the Prevalence and Determinants of Health Insurance Coverage in Nigeria and South Africa: A Multi-Country Analysis of Demographic Health Surveys. Int. J. Environ. Res. Public Health 2022, 19, 1766. https://doi.org/10.3390/ijerph19031766

Akokuwebe ME, Idemudia ES. A Comparative Cross-Sectional Study of the Prevalence and Determinants of Health Insurance Coverage in Nigeria and South Africa: A Multi-Country Analysis of Demographic Health Surveys. International Journal of Environmental Research and Public Health. 2022; 19(3):1766. https://doi.org/10.3390/ijerph19031766

Chicago/Turabian StyleAkokuwebe, Monica Ewomazino, and Erhabor Sunday Idemudia. 2022. "A Comparative Cross-Sectional Study of the Prevalence and Determinants of Health Insurance Coverage in Nigeria and South Africa: A Multi-Country Analysis of Demographic Health Surveys" International Journal of Environmental Research and Public Health 19, no. 3: 1766. https://doi.org/10.3390/ijerph19031766

APA StyleAkokuwebe, M. E., & Idemudia, E. S. (2022). A Comparative Cross-Sectional Study of the Prevalence and Determinants of Health Insurance Coverage in Nigeria and South Africa: A Multi-Country Analysis of Demographic Health Surveys. International Journal of Environmental Research and Public Health, 19(3), 1766. https://doi.org/10.3390/ijerph19031766