Assessing Digital Transformation of Cost Accounting Tools in Healthcare

Abstract

1. Introduction

2. Literature Review

2.1. Cost Accounting Tools

2.2. Digital Technologies Used in Costing

3. Methodology

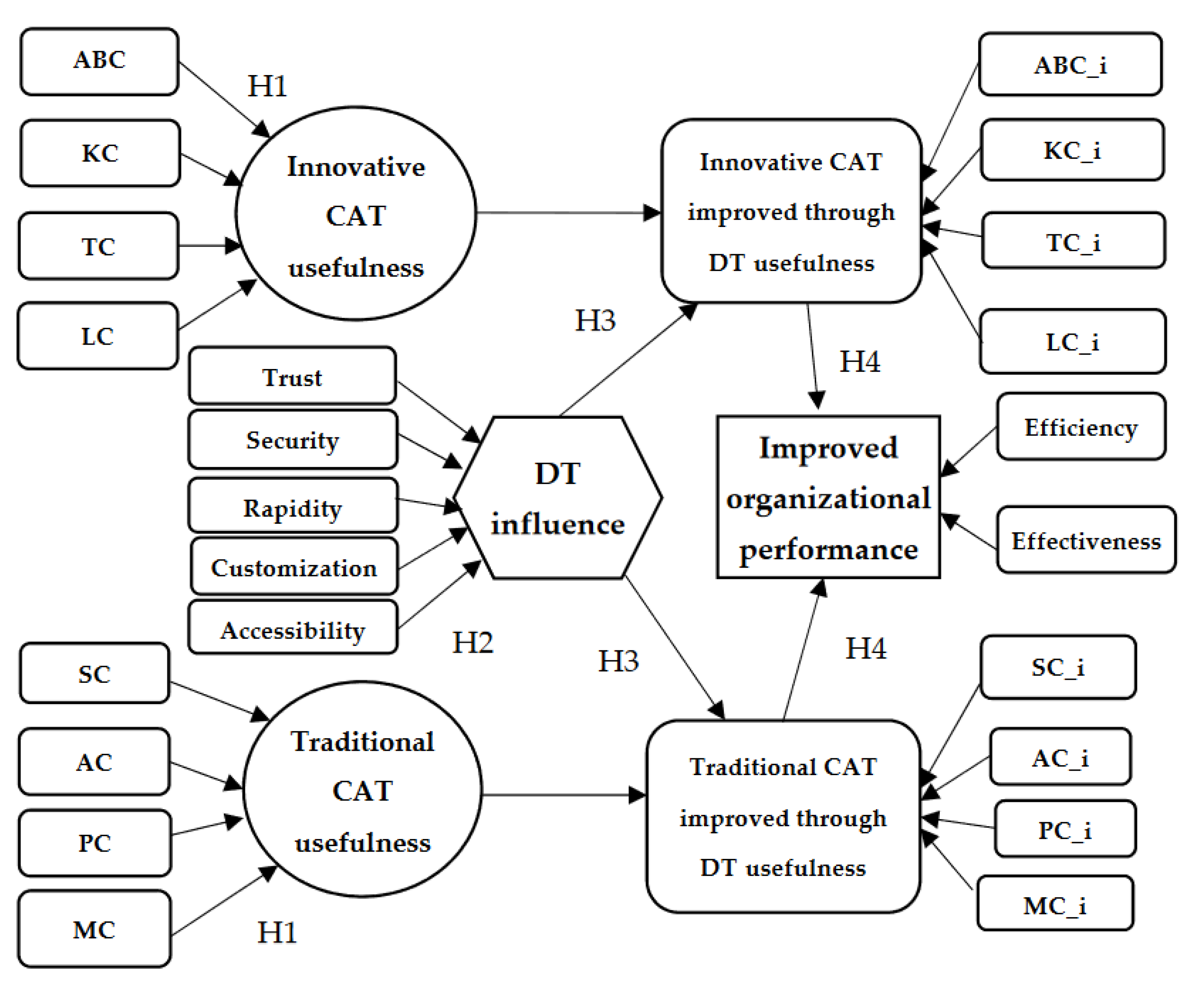

3.1. Research Design

3.2. Selected Variables

3.3. Selected Sample and Methods

4. Results

5. Discussion

5.1. Theoretical Implications

5.2. Empirical Implications

5.3. Limitations and Further Research

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| AI | Artificial intelligence |

| BD | Big data |

| BC | Blockchain |

| CC | Cloud computing |

| IoT | Internet of Things |

| AM | Accounting Management |

| CAT | Cost Accounting Tools |

| DT | Digital transformation |

| SC | Standard Costing |

| AC | Absorption Costing |

| PC | Process Costing |

| MC | Marginal Costing |

| ABC | Activity-Based Costing |

| TC | Target Costing |

| LC | Life Cycle Costing |

| KC | Kaizen Costing |

Appendix A

{kind=link}

{kind=link}

| Variables | Items |

|---|---|

| Demographic variables | What is your gender? |

| What is your age range? | |

| Innovative CAT usefulness | On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of ABC for accounting management? |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of TC for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of LC for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of KC for accounting management? | |

| Traditional CAT usefulness | On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of SC for accounting management? |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of AC for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of PC for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of MC for accounting management? | |

| DT influence | On a scale from 1 to 5 (1—not at all important, 5—very important), what do you think is the importance of trust in CAT improved through DT? |

| On a scale from 1 to 5 (1—not at all important, 5—very important), what do you think is the importance of security in CAT improved through DT? | |

| On a scale from 1 to 5 (1—not at all important, 5—very important), what do you think is the importance of rapidity in CAT improved through DT? | |

| On a scale from 1 to 5 (1—not at all important, 5—very important), what do you think is the importance of customization in CAT improved through DT? | |

| On a scale from 1 to 5 (1—not at all important, 5—very important), what do you think is the importance of accessibility in CAT improved through DT? | |

| Innovative CAT improved through DT usefulness | On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of ABC improved through DT for accounting management? |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of TC improved through DT for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of LC improved through DT for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of KC improved through DT for accounting management? | |

| Traditional CAT improved through DT usefulness | On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of SC improved through DT for accounting management? |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of AC improved through DT for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of PC improved through DT for accounting management? | |

| On a scale from 1 to 5 (1—not at all useful, 5—very useful), what is the usefulness of MC improved through DT for accounting management? | |

| Improved organizational performance | On a scale from 1 to 5 (1—very small, 5—very high), what do you think is the influence of CAT improved through DT on increasing organizational efficiency? |

| On a scale from 1 to 5 (1—very small, 5—very high), what do you think is the influence of CAT improved through DT on increasing organizational effectiveness? |

References

- PwC. Global Industry 4.0 Survey. 2016. Available online: http://www.pwc.com/gx/en/industries/industry-4.0.html (accessed on 2 April 2022).

- Piccarozzi, M.; Aquilani, B.; Gatti, C. Industry 4.0 in management studies: A systematic literature review. Sustainability 2018, 10, 3821. [Google Scholar] [CrossRef]

- Betto, F.; Sardi, A.; Garengo, P.; Sorano, E. The Evolution of Balanced Scorecard in Healthcare: A Systematic Review of Its Design, Implementation, Use, and Review. Int. J. Environ. Res. Public Health 2022, 19, 10291. [Google Scholar] [CrossRef] [PubMed]

- Arundel, A.; Bloch, C.; Ferguson, B. Advancing innovation in the public sector: Aligning innovation measurement with policy goals. Res. Policy 2019, 48, 789–798. [Google Scholar] [CrossRef]

- Rikhardsson, P.; Yigitbasioglu, O. Business intelligence & analytics in management accounting research: Status and future focus. Int. J. Account. Inf. Syst. 2018, 29, 37–58. [Google Scholar]

- Yoon, S. A Study on the Transformation of Accounting Based on New Technologies: Evidence from Korea. Sustainability 2020, 12, 8669. [Google Scholar] [CrossRef]

- IFAC. Technology and the Profession—A Guide to ICAEW’s Work. 2019. Available online: https://www.ifac.org/knowledge-gateway/preparing-future-ready-professionals/discussion/technology-and-profession-guide (accessed on 28 March 2022).

- ACCA/IMA. Digital Darwinism: Thriving in the Face of Technology Change. Available online: https://www.accaglobal.com/in/en/technical-activities/technical-resources-search/2013/october/digital-darwinism.html (accessed on 8 April 2022).

- Dash, S.; Shakyawar, S.K.; Sharma, M.; Kaushik, S. Big data in healthcare: Management, analysis, and future prospects. J. Big Data 2019, 6, 54. [Google Scholar] [CrossRef]

- Smys, S.; Raj, J.S. Internet of things and big data analytics for health care with cloud computing. J. Inf. Technol. Digit. World 2019, 1, 9–18. [Google Scholar] [CrossRef]

- Kelly, J.T.; Campbell, K.L.; Gong, E.; Scuffham, P. The Internet of Things: Impact and Implications for Health Care Delivery. J. Med. Internet Res. 2020, 22, e20135. [Google Scholar] [CrossRef]

- Rathee, G.; Sharma, A.; Saini, H.; Saini, H.; Kumar, R.; Iqbal, R. A hybrid framework for multimedia data processing in IoT-healthcare using blockchain technology. Multimed. Tools Appl. 2020, 79, 9711–9733. [Google Scholar] [CrossRef]

- Selvaraj, S.; Sundaravaradhan, S. Challenges and opportunities in IoT healthcare systems: A systematic review. SN Appl. Sci. 2020, 2, 139. [Google Scholar] [CrossRef]

- Bhuiyan, M.N.; Rahman, M.M.; Billah, M.M.; Saha, D. Internet of Things (IoT): A Review of Its Enabling Technologies in Healthcare Applications, Standards Protocols.Security and Market Opportunities. IEEE Internet Things J. 2021, 8, 10474–10498. [Google Scholar] [CrossRef]

- Li, W.; Chai, Y.; Khan, F.; Jan, S.R.U.; Verma, S.; Menon, V.G.; Li, X. A Comprehensive Survey on Machine Learning-Based Big Data Analytics for IoT-Enabled Smart Healthcare System. Mob. Netw. Appl. 2021, 26, 234–252. [Google Scholar] [CrossRef]

- Zhang, Y.; Sun, Y.; Jin, R.; Lin, K.; Liu, W. High-Performance Isolation Computing Technology for Smart IoT Healthcare in Cloud Environments. IEEE Internet Things J. 2021, 8, 16872–16879. [Google Scholar] [CrossRef]

- Cozzoli, N.; Salvatore, F.P.; Faccilongo, N.; Milone, M. How can big data analytics be used for healthcare organization management? Literary framework and future research from a systematic review. BMC Health Serv. Res. 2022, 22, 809. [Google Scholar] [CrossRef]

- Javaid, M.; Haleem, A.; Singh, R.P.; Rab, S.; Ul Haq, M.I.; Raina, A. Internet of Things in the global healthcare sector: Significance, applications, and barriers. Int. J. Intell. Netw. 2022, 3, 165–175. [Google Scholar] [CrossRef]

- Tabitha, N.; Ogungbade, I.I. Cost Accounting Techniques Adopted by Manufacturing and Service Industry within the Last Decade. Int. J. Adv. Manag. Econ. 2016, 5, 48–61. [Google Scholar]

- Kaplan, R.S. The Evolution of Management Accounting. Account. Rev. 1984, 59, 390–418. [Google Scholar]

- Ohno, T. Toyota Production System-Beyond Management of Large-Scale Production; Diamond Publishing: Shibuya-ku, Tokyo, 1978. (In Japanese) [Google Scholar]

- Johnson, H.T.; Kaplan, R.S. Relevance Lost: The Rise and Fall of Management Accounting; Harvard University Press: Cambridge, MA, USA, 1987. [Google Scholar]

- Sulaiman, M.; Ahmad, N.N.; Alwi, N.M. Is standard costing obsolete? Empirical evidence from Malaysia. Manag. Audit. J. 2005, 20, 109–124. [Google Scholar] [CrossRef]

- Marie, A.; Cheffi, W.; Louis, R.J.; Rao, A. Is standard costing still relevant? Evidence from Dubai. Manag. Account. Q. 2010, 11, 1–10. [Google Scholar]

- Badem, A.C.; Ergin, E.; Dury, C. Is Standard Costing Still Used? Evidence from Turkish Automotive Industry; International Business Research, Canadian Center of Science and Education: Toronto, ON, Canada, 2013. [Google Scholar]

- Pavlatos, O.; Kostakis, H. Management accounting innovations in a time of economic crisis. J. Econ. Asymm. 2018, 18, e00106. [Google Scholar] [CrossRef]

- Williamson, D. Cost and Management Accounting; Prentice Hall: Hemel Hempstead, UK, 1996. [Google Scholar]

- Waweru, N.M. The origin and evolution of management accounting: A review of the theoretical framework. Probl. Perspect. Manag. 2010, 8, 165–181. [Google Scholar]

- Angelakis, G.; Theriou, N.; Floropoulos, I.; Mandilas, A. Traditional and Currently Developed Management Accounting Practices-A Greek Study. Int. J. Econ. Bus. Adm. 2015, 3, 52–87. [Google Scholar] [CrossRef]

- Ashfaq, K.; Younas, S.; Usman, M.; Hanif, Z. Traditional Vs. Contemporary Management Accounting Practices and its Role and Usage across Business Life Cycle Stages: Evidence from Pakistani Financial Sector. Int. J. Acad. Res. Account. Financ. Manag. Sci. 2014, 4, 104–125. [Google Scholar] [CrossRef] [PubMed]

- Garrison, R.H.; Noreen, E.; Brewer, P.C. ISE Managerial Accounting; McGraw-Hill Education: New York, NY, USA, 2020. [Google Scholar]

- Kaplan Publishing Content Team. ACCA-Management Accounting (MA); Kaplan Publishing Content Team: Wokingham, UK, 2022. [Google Scholar]

- Bhimani, A.; Gosselin, M.; Ncube, M. Strategy and activity-based costing: A cross-national study of process and outcome contingencies. Int. J. Account. Audit. Perform. Eval. 2005, 2, 187–205. [Google Scholar] [CrossRef]

- Wegmann, G. Activity-based Management in France: A focus on the information systems department of a bank. In Proceedings of the International Conference on Economics, Business and Marketing Management, Shanghai, China, 11–13 March 2011; Institute of Electrical and Electronics Engineers, Inc. (IEEE): Piscataway, NJ, USA, 2011; pp. 144–148. [Google Scholar]

- Bhimani, A. Digital data and management accounting: Why we need to rethink research methods. J. Manag. Cont. 2020, 31, 9–23. [Google Scholar] [CrossRef]

- Charaf, K.; Rahmouni, A.F. Using importance-performance analysis to evaluate the satisfaction of Activity-Based Costing adopters. Account. Manag. Inf. Syst. 2014, 13, 665–685. [Google Scholar]

- Faria, A.; Ferreira, L.; Trigueiros, D. Analyzing customer profitability in hotels using activity-based costing. Tour. Manag. Stud. 2018, 14, 65–74. [Google Scholar] [CrossRef]

- Leksono, E.B.; Suparno, S.; Vanany, I. Integration of a Balanced Scorecard, DEMATEL, and ANP for Measuring the Performance of a Sustainable Healthcare Supply Chain. Sustainability 2019, 11, 3626. [Google Scholar] [CrossRef]

- Al-hosban, A.; Alsharairi, M.; Al-Tarawneh, I. The effect of using the target cost on reducing costs in the tourism companies in Aqaba special economic zone authority. J. Sustain. Financ. Invest. 2021, 1–16. [Google Scholar] [CrossRef]

- High, W. Short cycle manufacturing (SCM) implementation: An approach taken at Motorola. Target 1987, 3, 19–24. [Google Scholar]

- Omotayo, T.; Awuzie, B.; Egbelakin, T.; Obi, L.; Ogunnusi, M. AHP-systems thinking analyses for Kaizen costing implementation in the construction industry. Buildings 2020, 10, 230. [Google Scholar] [CrossRef]

- Yiğit, A.M. Kaizen Approach to Reducing Production Costs and a Case Study. J. Bus. Res.-Turk 2022, 14, 1267–1277. [Google Scholar] [CrossRef]

- Dugdale, D.; Jones, C.; Green, S. Contemporary Management Accounting Practices in UK Manufacturing; CIMA Publishing: London, UK, 2005. [Google Scholar]

- Bhimani, A.; Willcocks, L. Digitisation, Big Data and the transformation of accounting information. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- FSB (Financial Stability Board) Artificial Intelligence and Machine Learning in Financial Services: Market Developments and Financial Stability Implications. 2017. Available online: http://www.fsb.org/wp-content/uploads/P011117.pdf (accessed on 25 April 2022).

- Bauguess, S. The role of big data, machine learning, and AI in assessing risks: A regulatory perspective. In Champagne Keynote Speech; Securities and Exchange Commission: New York, NY, USA, 2017. Available online: https://www.sec.gov/news/speech/bauguess-big-data-ai (accessed on 21 April 2022).

- Yook, K.H. Challenges and prospect for management accounting in Industry 4.0. Korean J. Manag. Accoun. Res. 2019, 19, 33–57. [Google Scholar] [CrossRef]

- Breiman, L. Random forests. Mach. Learn. 2001, 45, 5–32. [Google Scholar] [CrossRef]

- Cutler, A.; Cutler, D.R.; Stevens, J. Random forests. In Ensemble Machine Learnings; Springer: Manhattan, NY, USA, 2012; pp. 157–175. [Google Scholar]

- Schmitz, J.; Leoni, G. Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda. Aust. Account. Rev. 2019, 29, 331–342. [Google Scholar] [CrossRef]

- George, K.; Patatoukas, P.N. The Blockchain Evolution and Revolution of Accounting. 2020. Available online: https://ssrn.com/abstract=3681654 (accessed on 7 April 2022).

- Secinaro, S.; Calandra, D.; Biancone, P. Blockchain, trust, and trust accounting: Can blockchain technology substitute trust created by intermediaries in trust accounting? A theoretical examination. Int. J. Manag. Pract. 2021, 14, 129–145. [Google Scholar] [CrossRef]

- Andersen, N. Blockchain Technology: A Game-Changer in Accounting. Available online: https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/Blockchain_A%20game-changer%20in%20accounting.pdf (accessed on 2 April 2022).

- Tang, Y.; Xiong, J.; Becerril-Arreola, R.; Iyer, L. Ethics of Blockchain. J. Inf. Technol. People 2019, 33, 602–632. [Google Scholar] [CrossRef]

- Sherif, S.; Mohsin, H. The effect of emergent technologies on accountant’s ethical blindness. Int. J. Dig. Account. Res. 2021, 21, 61–94. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Krahel, J.P.; Titera, W.R. Consequences of Big Data and formalization on accounting and auditing standards. Account. Horiz. 2015, 29, 409–422. [Google Scholar] [CrossRef]

- Mistry, I.; Tanwar, S.; Tyagi, S.; Kumar, N. Blockchain for 5G-enabled IoT for industrial automation: A systematic review, solutions, and challenges. Mech. Syst. Signal Process. 2020, 135, 106382. [Google Scholar] [CrossRef]

- Schuh, G.; Potente, T.; Wesch-Potente, C.; Weber, A.R.; Prote, J.-P. Collaboration Mechanisms to increase productivity in the Context of Industry 4.0. Procedia Cirp. 2014, 19, 51–56. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A. Imagineering Audit 4.0. J. Emerg. Technol. Account. 2016, 13, 1–15. [Google Scholar] [CrossRef]

- Mitra, A.; Kundu, A.; Chattopadhyay, M.; Chattopadhyay, S. A cost-efficient one-time password-based authentication in cloud environment using equal length cellular automata. J. Ind. Inf. Integr. 2017, 5, 17–25. [Google Scholar] [CrossRef]

- Da Xu, L.; Xu, E.L.; Li, L. Industry 4.0: State of the art and future trends. Int. J. Prod. Res. 2018, 56, 2941–2962. [Google Scholar] [CrossRef]

- Stoica, O.C.; Ionescu-Feleagă, L. Digitalization in Accounting: A Structured Literature Review. In Proceedings of the 4th International Conference on Economics and Social Sciences: Resilience and Economic Intelligence through Digitalization and Big Data Analytics, Sciendo, Bucharest, Romania, 10–11 June 2021; pp. 453–464. [Google Scholar] [CrossRef]

- Yürekli, E.; Haşiloglu, S.B. Evaluation of the Factors Affecting the Purchasing Decisions of Accounting Package Programs. J. Internet Appl. Manag. 2017, 8, 47–64. [Google Scholar] [CrossRef][Green Version]

- Khayer, A.; Bao, Y.; Nguyen, B. Understanding cloud computing success and its impact on firm performance: An integrated approach. Ind. Manag. Data. Syst. 2020, 120, 963–985. [Google Scholar] [CrossRef]

- Christauskas, C.; Misevicience, R. Cloud computing-based accounting for small to medium-sized business. Inz. Ekon. Eng. Econ. 2012, 23, 14–21. [Google Scholar] [CrossRef]

- Phillips, B.A. How Cloud Computing Will Change Accounting Forever. 2012. Available online: https://docplay-er.net/2537016-How-the-cloud-will-change-accounting-forever.html (accessed on 16 April 2022).

- Ionescu, B.; Ionescu, I.; Bendovschi, A.; Tudoran, L. Traditional accounting vs. cloud accounting. In Proceedings of the 8th International Conference Accounting and Management Informational Systems, Bucharest, Romania, 12–13 June 2013; pp. 106–125. [Google Scholar]

- Grigoroudis, E.; Orfanoudaki, E.; Zopounidis, C. Strategic Performance Measurement in a Healthcare Organisation: A Multiple Criteria Approach Based on Balanced Scorecard. Omega 2012, 40, 104–119. [Google Scholar] [CrossRef]

- Park, E.S.; Park, M.S. Factors of the Technology Acceptance Model for Construction IT. Appl. Sci. 2020, 10, 8299. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef]

- Chau, P.Y.K. An empirical assessment of a modified technology acceptance model. J. Manag. Inf. Syst. 1996, 13, 185–204. [Google Scholar] [CrossRef]

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef]

- Gefen, D. TAM or just plain habit: A look at experienced online shoppers. J. Organ. End User Comput. 2003, 15, 1–13. [Google Scholar] [CrossRef]

- King, W.R.; He, J. A meta-analysis of the technology acceptance model. Inf. Manag. 2006, 43, 740–755. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef]

- Ngubelanga, A.; Duffett, R. Modeling Mobile Commerce Applications’ Antecedents of Customer Satisfaction among Millennials: An Extended TAM Perspective. Sustainability 2021, 13, 5973. [Google Scholar] [CrossRef]

- Na, S.; Heo, S.; Han, S.; Shin, Y.; Roh, Y. Acceptance Model of Artificial Intelligence (AI)-Based Technologies in Construction Firms: Applying the Technology Acceptance Model (TAM) in Combination with the Technology-Organisation-Environment (TOE) Framework. Buildings 2022, 12, 90. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psych. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M.A. Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Bohm, V.; Lacaille, D.; Spencer, N.; Barber, C.E.H. Scoping Review of Balanced Scorecards for Use in Healthcare Settings: Development and Implementation. BMJ Open Qual. 2021, 10, e001293. [Google Scholar] [CrossRef] [PubMed]

- Wu, X. Application and Thinking of Cloud Accounting in Accounting Informatization. J. Phys. Conf. Ser. 2021, 1992, 032109. [Google Scholar] [CrossRef]

- Coman, D.M.; Ionescu, C.A.; Duica, A.; Coman, M.D.; Uzlau, M.C.; Stanescu, S.G.; State, V. Digitization of Accounting: The Premise of the Paradigm Shift of Role of the Professional Accountant. Appl. Sci. 2022, 12, 3359. [Google Scholar] [CrossRef]

- Gonçalves, M.J.A.; da Silva, A.C.F.; Ferreira, C.G. The Future of Accounting: How Will Digital Transformation Impact the Sector? Informatics 2022, 9, 19. [Google Scholar] [CrossRef]

- Sandberg, J.; Holmström, J.; Lyytinen, K. Digitization and phase transitions in platform organizing logics: Evidence from the process automation industry. MIS Q. 2020, 44, 129–153. [Google Scholar] [CrossRef]

- Aslam, J.; Saleem, A.; Khan, N.T.; Kim, Y.B. Factors influencing blockchain adoption in supply chain management practices: A study based on the oil industry. J. Innov. Knowl. 2021, 6, 124–134. [Google Scholar] [CrossRef]

- Zuo, Z.; Lin, Z. Government R&D subsidies and firm innovation performance: The moderating role of accounting information quality. J. Innov. Knowl. 2022, 7, 100176. [Google Scholar] [CrossRef]

- Da Costa, R.L.; Pereira, L.; Dias, Á.; Gongalves, R.; Jerónimo, C.H. Balanced Scorecard Adoption in Healthcare. Int. J. Electron. Healthc. 2022, 12, 22–40. [Google Scholar] [CrossRef]

- Kroon, N.; Alves, M.d.C.; Martins, I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. J. Open Innov. Technol. Mark. Complex. 2021, 7, 163. [Google Scholar] [CrossRef]

- Bălăcescu, A.; Pătrașcu, A.; Păunescu, M. Adaptability to Teleworking in European Countries. Amfiteatru Econ. 2021, 23, 683–699. [Google Scholar] [CrossRef]

- Marr, B. Data Strategy: How to Profit from a World of Big Data, Analytics and the Internet of Things; Kogan Page: London, UK, 2017. [Google Scholar]

- Agrawal, A.; Gans, J.; Goldfarb, A. Prediction Machines: The Simple Economics of Artificial Intelligence; Harvard Business Review Press: Brighton, MA, USA, 2018. [Google Scholar]

- Huerta, E.; Jensen, S. An Accounting Information Systems Perspective on Data Analytics and Big Data. J. Inf. Syst. 2017, 31, 101–114. [Google Scholar] [CrossRef]

- Coyne, E.M.; Coyne, J.G.; Walker, K.B. Big Data information governance by accountants. Int. J. Account. Inf. Manag. 2018, 26, 153–170. [Google Scholar] [CrossRef]

- Trinchero, E.; Farr-Wharton, B.; Brunetto, Y. A Social Exchange Perspective for Achieving Safety Culture in Healthcare Organizations. Int. J. Public Sect. Manag. 2019, 32, 142–156. [Google Scholar] [CrossRef]

| CAT | Description | References |

|---|---|---|

| Standard costing | SC is a managerial accounting tool that analyzes real-cost variations compared to the standard costs pre-established in the planning phase. This costing method is used in the exception management method. Each cost element has a standard cost established scientifically (technical characteristics of the products, historical costs, etc.). The analysis of the differences between standard and actual costs makes it possible to detect deviations and take corrective measures to remove the cause of inefficiency [21,22,23,24]. Although it is a tool that allows correcting errors, it does not allow combating deviations in real time but only after the end of the production process. SC offers convenience and rapidity in calculating production costs, preparing budgets, setting product prices, and evaluating the performance of organizational divisions. However, contemporary price dynamics, rapid change in cost structure, and delayed feedback make this method ineffective, especially in high-dynamism economic sectors (such as IT). | [23,24,25,26] |

| Absorption costing | AC, known as the total cost method, considers all the production costs of the product or service. Whether they are variable or fixed costs, they are gradually absorbed until the total cost is reached. Financial statements use the principles of absorption costs, as this method no longer requires subsequent accounting treatments. However, AC is not very compatible with highly automated work environments without considering significant investments in IT solutions. Nevertheless, AC was relevant, considering direct labor costs were the most significant component of the total cost. | [19,20,27,28,29] |

| Process costing | PC is used when the organization produces homogeneous standardized goods. PC is also used in industries involving an assembly process. The calculation of costs implies accumulating all costs for each stage of production or process. Then, the unit cost is determined in each stage by dividing the cost of each process by the units produced. The process costing system is useful in industries with high innovation. | [28,30,31,32] |

| Marginal costing | MC has two variants: variable costing and direct costing. This costing tool assesses separately variable and fixed costs, respectively direct and indirect costs, to support the decision-making process. MC enables managers to focus on changes in cost structure and make decisions based on this information. MC is useful for supporting short-term decisions concerning purchases, sales, outsourcing a part of the production process, etc. | [26,27,28,29] |

| CAT | Description | References |

|---|---|---|

| Activity-based costing | ABC, designed in the mid-1980s, achieved a more appropriate and realistic allocation of the organization’s overhead. The implementation of this tool is related to combating the disadvantages of SC. ABC identifies cost factors according to the distribution of indirect expenses and the organization’s general expenses on the cost of activities. The costs of the activities are then used to form the costs of the products or services. Monitoring the activities and resource consumption allocated to each activity allows a more judicious distribution of costs by products and services. Resources are allocated to activities, and activities are allocated to cost objects based on consumption estimates. The concept of ABC formed the basis of the activity-based management (ABM) system used successfully in the services sector. ABM allows the removal of activities that do not add value and a better distribution of costs. However, ABC is expensive, time-consuming, and challenging to adjust. The DT proposed by Industry 4.0 can streamline this method. | [33,34,35,36,37] |

| Target costing | TC emerged in response to the challenges posed by consumer demand for diversity and the shortening of product life cycles. TC considers the costs of products in the design phase, which have become increasingly significant in a product’s total costs over its life cycle. Being a multidisciplinary approach to costing, TC involves process reengineering and total quality management techniques. The basic principle is to set a competitive price for a product, starting from the market price. Then, by subtracting a desirable profit margin, the target cost is obtained. The costing tool is suitable for the services sector and the industry, allowing a highly competitive approach. Based on the target cost, cost elements can be estimated so that the final cost fits into the target cost. | [19,27,28,38,39] |

| Life cycle costing | LC aims to identify the total cost associated with the entire life cycle of a product or service, considering the design costs and all the company costs related to the product. LC allows the assessment of an asset’s costs over its life cycle, making it possible to quantify the consequences of the decision and improve forecasts by understanding the trade-off between performance and cost. Disadvantages include a lack of data and high time consumption. LC is useful when launching a product requiring large initial capital outflows. | [27,28,29,35,40] |

| Kaizen costing | KC is based on the continuous improvement cycle involving all organization members, from top managers to simple workers. Therefore, the costing tool can increase productivity, gain a competitive advantage, and increase overall performance. In addition, KC has the advantage of minimal application costs. In addition, KC has the advantage of minimal application costs. Like ABC, this method has been associated with a management system (Kaizen Management) dedicated to improving effectiveness, efficiency, quality, and overall organizational performance. Improving the quality of processes and products increases the company’s profits and customer loyalty. | [19,41,42] |

| Variables | Items | Scales |

|---|---|---|

| Demographic variables | Gender | Male(1), Female (2) |

| Age | 18–30 years (1), 31–45 years (2), 46–65 years (3) | |

| Innovative CAT usefulness | ABC | On a scale of 1 to 5 (1—not at all useful, 5—very useful) |

| TC | ||

| LC | ||

| KC | ||

| Traditional CAT usefulness | SC | |

| AC | ||

| PC | ||

| MC | ||

| DT influence | Trust | On a scale of 1 to 5 (1—not at all important, 5—very important) |

| Security | ||

| Rapidity | ||

| Customization | ||

| Accessibility | ||

| Innovative CAT improved through DT usefulness | ABC | On a scale of 1 to 5 (1—not at all useful, 5—very useful) |

| TC | ||

| LC | ||

| KC | ||

| Traditional CAT improved through DT usefulness | SC | |

| AC | ||

| PC | ||

| MC | ||

| Improved organizational performance | Efficiency | On a scale of 1 to 5 (1—very small, 5—very high) |

| Effectiveness |

| Cronbach’s Alpha | Composite Reliability | AVE | |

|---|---|---|---|

| DT influence | 0.927 | 0.945 | 0.777 |

| Improved organizational performance | 0.849 | 0.930 | 0.868 |

| Innovative CAT improved through DT | 0.866 | 0.909 | 0.713 |

| Innovative CAT usefulness | 0.864 | 0.908 | 0.711 |

| Traditional CAT improved through DT | 0.824 | 0.883 | 0.655 |

| Traditional CAT usefulness | 0.806 | 0.873 | 0.632 |

| Hypothesis | DT Influence | Innovative CAT Usefulness | Traditional CAT Usefulness | ||||

|---|---|---|---|---|---|---|---|

| Outer Loading | Outer Weights | Outer Loading | Outer Weights | Outer Loading | Outer Weights | ||

| H1 | SC | 0.794 | 0.325 | ||||

| AC | 0.823 | 0.330 | |||||

| PC | 0.821 | 0.326 | |||||

| MC | 0.738 | 0.274 | |||||

| ABC | 0.856 | 0.301 | |||||

| TC | 0.861 | 0.307 | |||||

| LC | 0.840 | 0.280 | |||||

| KC | 0.815 | 0.298 | |||||

| H2 | Accessibility | 0.787 | 0.203 | ||||

| Customization | 0.902 | 0.226 | |||||

| Rapidity | 0.953 | 0.248 | |||||

| Security | 0.931 | 0.242 | |||||

| Trust | 0.823 | 0.214 | |||||

| Hypothesis | Original Sample | Standard Deviation | T Statistics | p Values | Validation | |

|---|---|---|---|---|---|---|

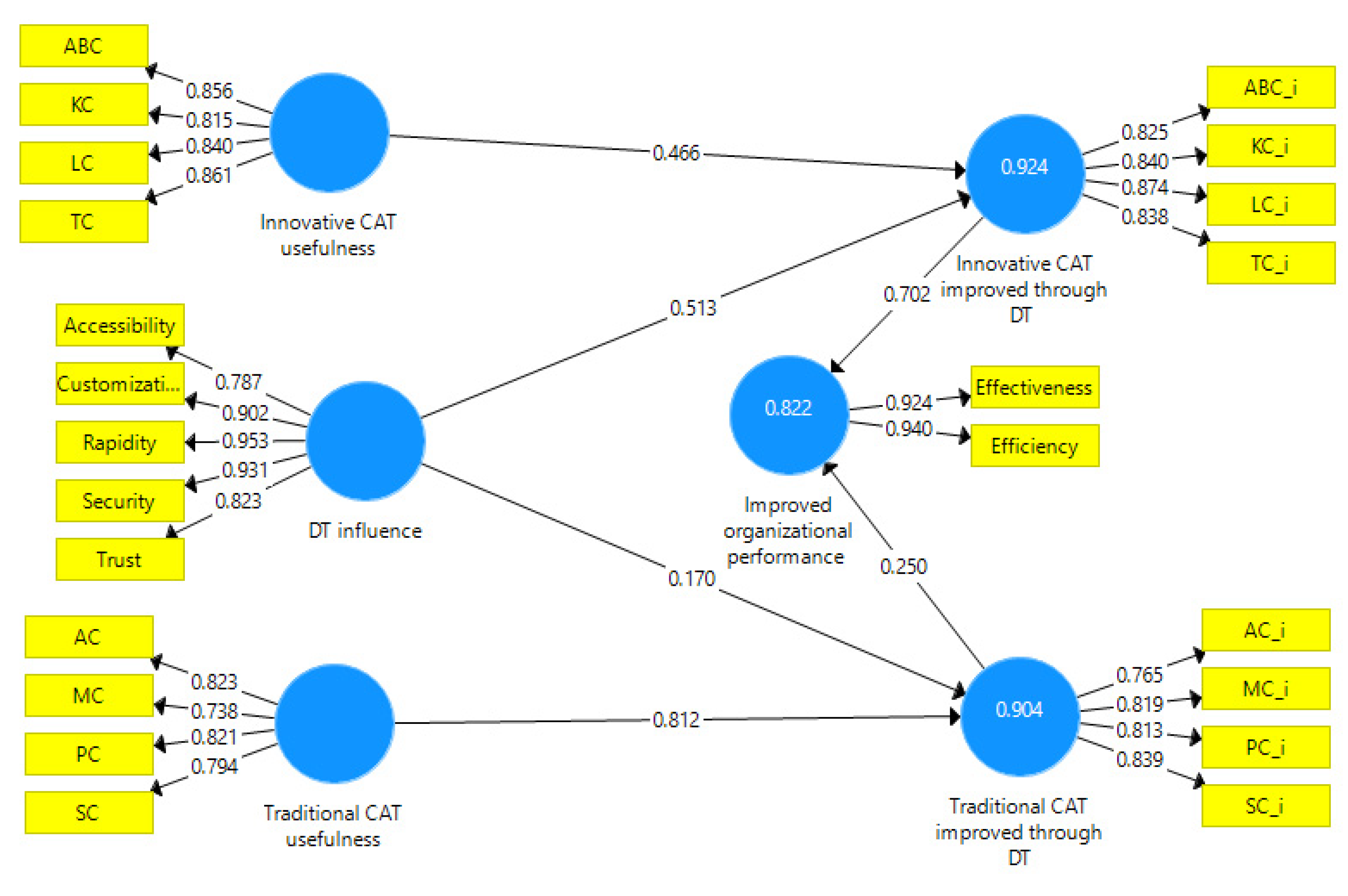

| H3 | DT influence → Innovative CAT improved through DT | 0.513 | 0.040 | 12.802 | 0.000 | Validated |

| DT influence → Traditional CAT improved through DT | 0.170 | 0.033 | 5.195 | 0.000 | ||

| H4 | Innovative CAT improved through DT performance → Improved organizational performance | 0.702 | 0.031 | 22.641 | 0.000 | Validated |

| Traditional CAT improved through DT → Improved organizational performance | 0.250 | 0.031 | 4.893 | 0.000 | ||

| Innovative CAT usefulness → Innovative CAT improved through DT | 0.466 | 0.041 | 11.348 | 0.000 | ||

| Traditional CAT usefulness → Traditional CAT improved through DT | 0.812 | 0.035 | 6.703 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vărzaru, A.A. Assessing Digital Transformation of Cost Accounting Tools in Healthcare. Int. J. Environ. Res. Public Health 2022, 19, 15572. https://doi.org/10.3390/ijerph192315572

Vărzaru AA. Assessing Digital Transformation of Cost Accounting Tools in Healthcare. International Journal of Environmental Research and Public Health. 2022; 19(23):15572. https://doi.org/10.3390/ijerph192315572

Chicago/Turabian StyleVărzaru, Anca Antoaneta. 2022. "Assessing Digital Transformation of Cost Accounting Tools in Healthcare" International Journal of Environmental Research and Public Health 19, no. 23: 15572. https://doi.org/10.3390/ijerph192315572

APA StyleVărzaru, A. A. (2022). Assessing Digital Transformation of Cost Accounting Tools in Healthcare. International Journal of Environmental Research and Public Health, 19(23), 15572. https://doi.org/10.3390/ijerph192315572