The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method

Abstract

:1. Introduction

2. Literature Review

3. Hypothesis Proposed

4. Model Specification

4.1. Variable Selection

- Explained variables. This article selects short-term loans and long-term loans as the variables to be interpreted, wherein short-term financing is the explanatory variable for Hypotheses 1 and 3, and long-term financing is the explanatory variable for Hypotheses 2 and 4.

- Explanatory variables. In 2012, the former CBRC issued the Green Credit Guidelines, which marked the beginning of the Green Credit Policy, meaning that the time virtual variable will be 1 in 2012 and later, and 0 before 2012.

- 3.

- Control variables. A set of control variables that have been shown to affect corporate debt financing has been selected to measure the impact of the Green Credit Policy and to test the hypothesis proposed in this paper. It includes the basic indicators of corporate age [55] and corporate size [56], profitability [53] using the yield valve and liquidity ratio [57], the debt service capacity using the asset liability ratio and the cash flow interest protection multiple [58], and so on.

4.2. Model Specification

5. Results and Discussion

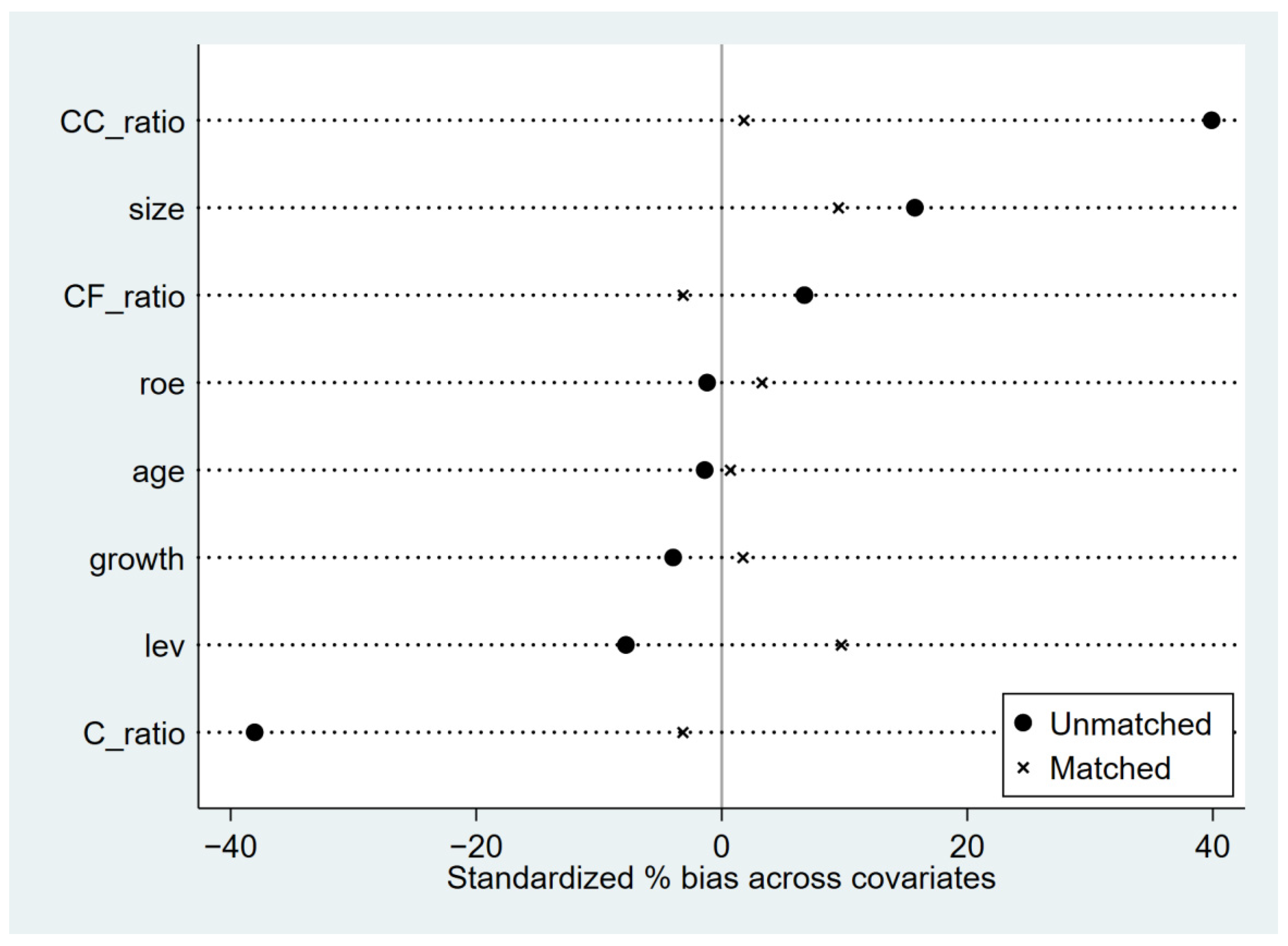

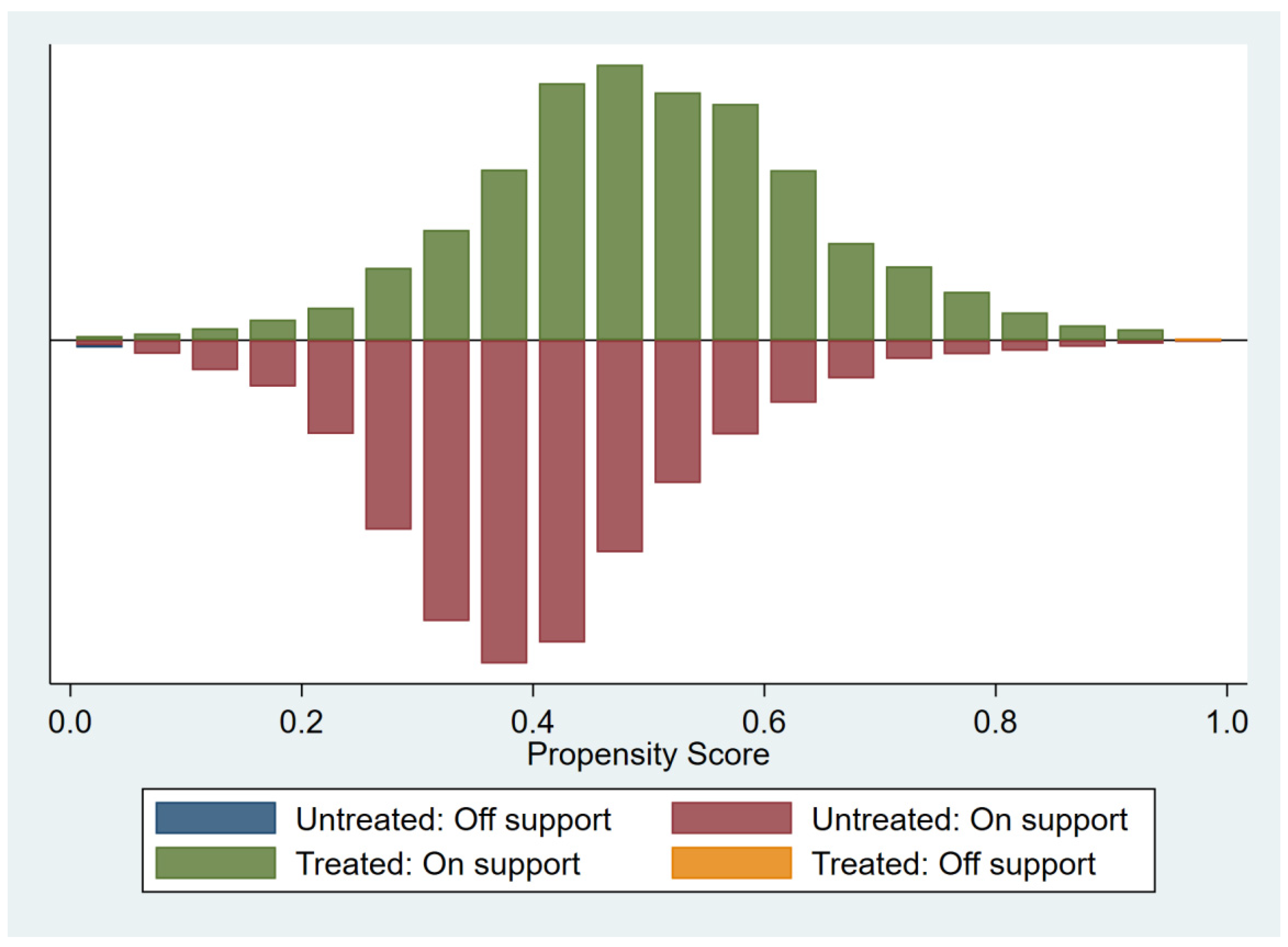

5.1. Propensity Score Matching Results

5.2. Analysis of DID Model

5.2.1. Regression Results and Analysis of the Effects of the Green Credit Policy on the Short-Term and Long-Term Financing of Heavily Polluting Enterprises

5.2.2. The Effect of Ownership on the Relationship between the Green Credit Policy and the Short-Term and Long-Term Financing of Heavily Polluting Enterprises

5.3. Robustness Test

5.3.1. Propensity Score Matches

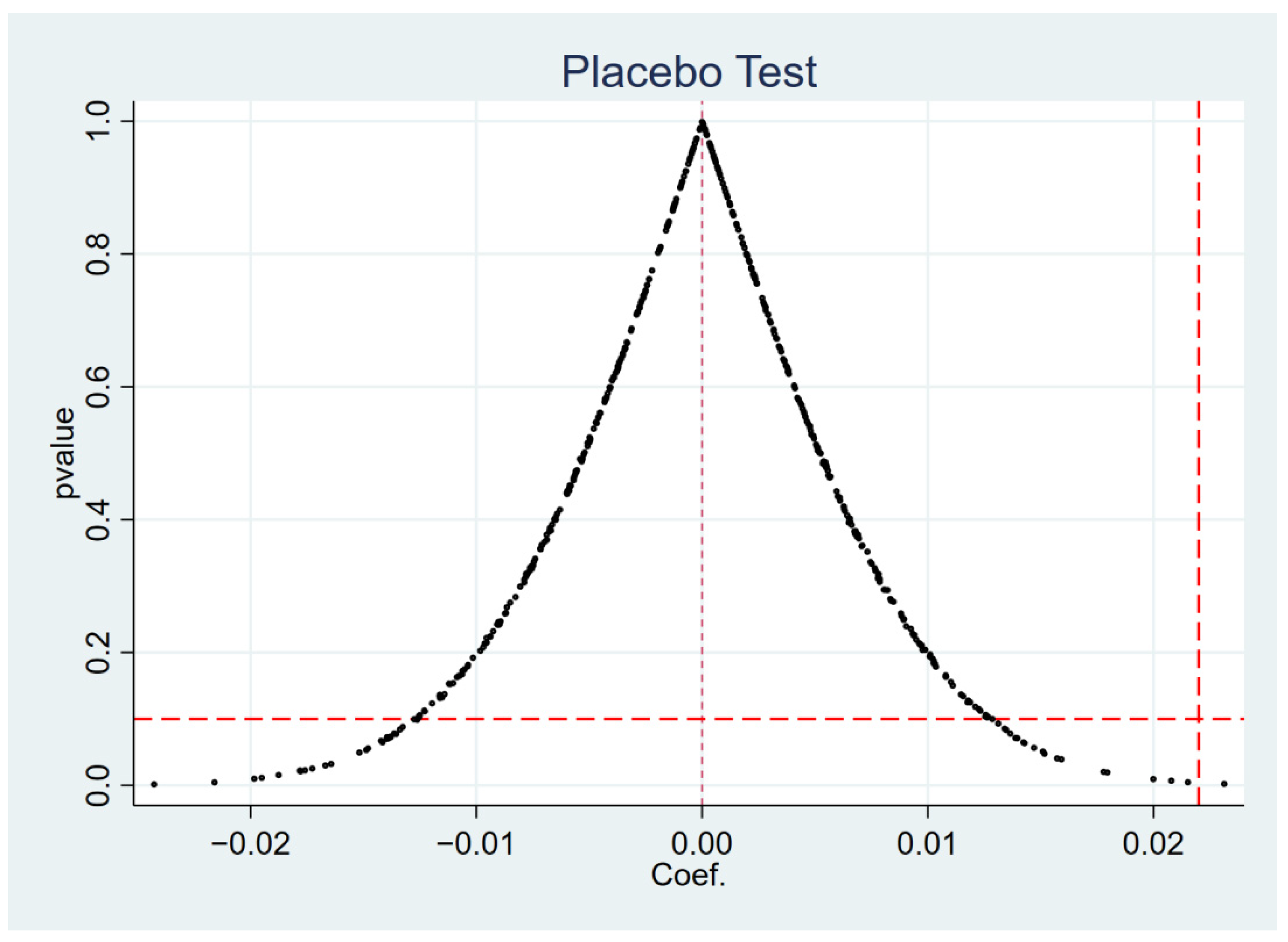

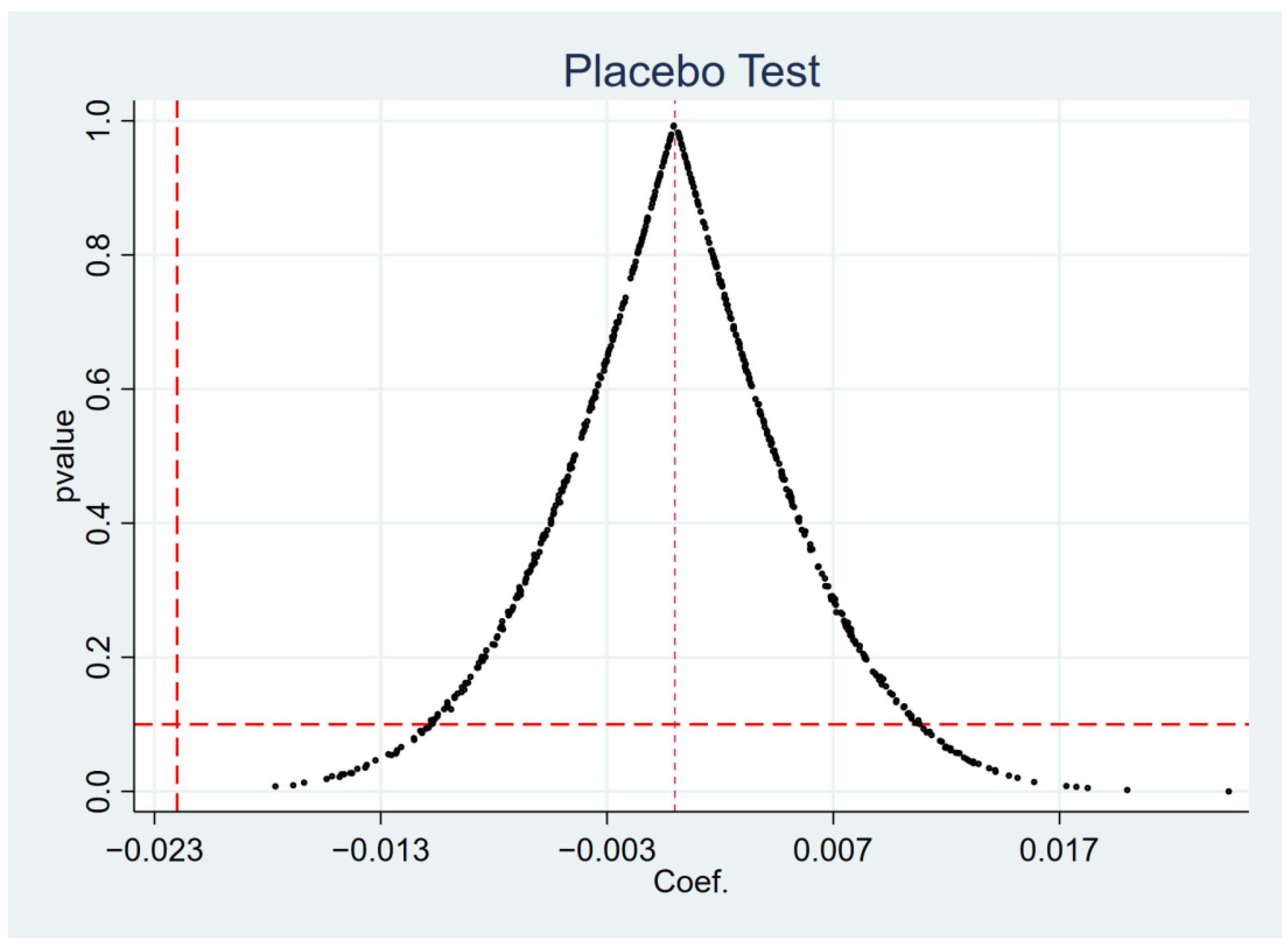

5.3.2. Placebo Test

6. Discussion

6.1. Discussion of Analysis Results

6.2. Suggestions for Policy

- Although the Green Credit Policy has a restraining effect on the long-term financing of heavily polluting enterprises, it also increases the short-term financing of heavily polluting enterprises, which weakens the implementation efficiency of the Green Credit Policy. To address this problem, the relevant state departments should clearly unify the implementation standards of the Green Credit Policy, establish clear requirements for both the long-term and the short-term financing of heavily polluting enterprises, regulate the lending behavior of financial institutions, and prevent financial institutions from enabling access to short-term credit for heavily polluting enterprises in pursuit of profits.

- At present, the implementation effect of the Green Credit Policy is asymmetrical, and there is a problem in that the implementation effect for state-owned enterprises is not as good as that for non-state-owned enterprises. In order to solve this problem, it is necessary to clarify the supervisory responsibilities of financial departments, and strengthen supervision. The relevant state departments should construct an evaluation index system for the Green Credit Policy, and unify the evaluation standards of the policy’s implementation effect, which will help to restrain the credit behavior of banks and avoid the weakening of the policy’s effect via the ownership preferences of banks.

- The Green Credit Policy has shown a restrictive effect on debt financing for heavily polluting enterprises, but the ultimate goal of the Green Credit Policy is to reduce environmental pollution caused by heavily polluting enterprises through green innovation, or transformation and upgrading. It often takes a long time for the transformation of heavily polluting enterprises to achieve results, and without incentives, enterprises may be trapped in a vicious cycle of continuous inadequate financing, which in turn makes it difficult for them to transform, and exacerbates pollution. In order for enterprises to respond to the Green Credit Policy and actively carry out green transformation, this paper suggests that regulators and financial institutions should give enterprises corresponding incentives according to their actual situation, such as tax relief and subsidy support for enterprises in the transformation period.

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Zhang, J.; Wei, S. Status and characteristics of urban air pollution in China. Sichuan Environ. 2006, 3, 104–108,112. [Google Scholar] [CrossRef]

- Cui, H.; Liu, M. Research on resource dynamics in the ninth forest inventory in China. J. West China For. Sci. 2020, 49, 90–95. [Google Scholar] [CrossRef]

- Hu, A.; Zhou, S. Green development: Functional definition, mechanism analysis and development strategy. China Popul. -Resour. Environ. 2014, 24, 14–20. [Google Scholar]

- Lu, C.; Wang, B.; Chen, T.; Yang, J.A. Document Analysis of Peak Carbon Emissions and Carbon Neutrality Policies Based on a PMC Index Model in China. Int. J. Environ. Res. Public Health 2022, 19, 9312. [Google Scholar] [CrossRef]

- Hong, M.; Li, Z.; Drakeford, B. Do the green credit guidelines affect corporate green technology innovation? Empirical research from China. Int. J. Environ. Res. Public Health 2021, 18, 1682. [Google Scholar] [CrossRef]

- Sun, Y.; Sun, Y.; Li, X. Constructing a green financial innovation system with the PPP environmental protection industry fund. Int. J. Technol. Manag. 2021, 85, 319–332. [Google Scholar] [CrossRef]

- Qin, J.; Cao, J. Carbon Emission Reduction Effects of Green Credit Policies: Empirical Evidence From China. Front. Environ. Sci. 2022, 10, 798072. [Google Scholar] [CrossRef]

- Liu, L.; He, L. Output and welfare effect of green credit in China: Evidence from an estimated DSGE model. J. Clean. Prod. 2021, 294, 126326. [Google Scholar] [CrossRef]

- Zhang, X.; Xu, K.; He, M. Development status and some considerations on Energy Internet construction in Beijing-Tianjin-Hebei region. Heliyon 2022, 8, e08722. [Google Scholar] [CrossRef]

- Hu, Y.; Zheng, J. Is Green Credit a Good Tool to Achieve “Double Carbon” Goal? Based on Coupling Coordination Model and PVAR Model. Sustainability 2021, 13, 14074. [Google Scholar] [CrossRef]

- Ding, L.; Zhuang, Y.; Jiang, S. Green credit and high-quality sustainable development of banks. Environ. Sci. Pollut. Res. 2022. [Google Scholar] [CrossRef] [PubMed]

- Hu, G.; Wang, X.; Wang, Y. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Guo, Q.; Zhou, M.; Liu, N.; Wang, Y. Spatial Effects of Environmental Regulation and Green Credits on Green Technology Innovation under Low-Carbon Economy Background Conditions. Int. J. Environ. Res. Public Health 2019, 16, 3027. [Google Scholar] [CrossRef] [PubMed]

- Li, S.; Zhang, W.; Zhao, J. Does Green Credit Policy promote the green innovation efficiency of heavy polluting industries?-empirical evidence from China’s industries. Environ. Sci. Pollut. Res. 2022, 29, 46721–46736. [Google Scholar] [CrossRef]

- Gao, D.; Mo, X.; Duan, K.; Li, Y. Can Green Credit Policy Promote Firms’ Green Innovation? Evidence from China. Sustainability 2022, 14, 3911. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, C.; Luo, S. Resource Allocation Effect of Green Credit Policy: Based on DID Model. Mathematics 2021, 9, 159. [Google Scholar] [CrossRef]

- Wang, E.; Liu, X.; Wu, J.; Cai, D. Green Credit, Debt Maturity, and Corporate Investment—Evidence from China. Sustainability 2019, 11, 583. [Google Scholar] [CrossRef]

- Guo, L.; Tan, W.; Xu, Y. Impact of green credit on green economy efficiency in China. Environ. Sci. Pollut. Res. 2022, 29, 35124–35137. [Google Scholar] [CrossRef]

- Li, Y.; Ding, T.; Zhu, W. Can Green Credit Contribute to Sustainable Economic Growth? An Empirical Study from China. Sustainability 2022, 14, 6661. [Google Scholar] [CrossRef]

- Chen, C.; Zhang, Y.; Bai, Y.; Li, W. The impact of green credit on economic growth-The mediating effect of environment on labor supply. PLoS ONE 2021, 16, 9. [Google Scholar] [CrossRef]

- Lei, X.; Wang, Y.; Zhao, D.; Chen, Q. The local-neighborhood effect of green credit on green economy: A spatial econometric investigation. Environ. Sci. Pollut. Res. 2021, 28, 46. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Lei, X.; Zhao, D.; Long, R.; Wu, M. The Dual Impacts of Green Credit on Economy and Environment: Evidence from China. Sustainability 2021, 13, 4574. [Google Scholar] [CrossRef]

- Lyu, B.; Da, J.Y.; Ostic, D.; Yu, H.C. How Does Green Credit Promote Carbon Reduction? A Mediated Model. Front. Environ. Sci. 2022, 10, 878060. [Google Scholar] [CrossRef]

- Zhang, A.; Deng, R.; Wu, Y. Does the Green Credit Policy Reduce the Carbon Emission Intensity of Heavily Polluting Industries? -Evidence from China’s Industrial Sectors. J. Environ. Manag. 2022, 311, 114815. [Google Scholar] [CrossRef] [PubMed]

- Xiao, Z.; Yu, L.; Liu, Y.; Bu, X.; Yin, Z. Does Green Credit Policy Move the Industrial Firms toward a Greener Future? Evidence from a Quasi-Natural Experiment in China. Front. Environ. Sci. 2022, 9, 810305. [Google Scholar] [CrossRef]

- Yang, F.; Xu, Q.; Li, K.; Yuen, K.F.; Shi, W. The inhibition effect of bank credits on PM2.5 concentrations: Spatial evidence from high-polluting firms in China. Environ. Pollut. 2022, 308, 119639. [Google Scholar] [CrossRef]

- Lian, Y.; Gao, J.; Ye, T. How does green credit affect the financial performance of commercial banks?-Evidence from China. J. Clean. Prod. 2022, 344, 131069. [Google Scholar] [CrossRef]

- Xi, B.; Wang, Y.; Yang, M. Green credit, green reputation, and corporate financial performance: Evidence from China. Environ. Sci. Pollut. Res. 2021, 29, 2401–2419. [Google Scholar] [CrossRef]

- Deng, X.; Hao, H.; Chang, M.; Ren, X.; Wang, L. Influencing Factors of Green Credit Efficiency in Chinese Commercial Banks. Front. Environ. Sci. 2022, 10, 941053. [Google Scholar] [CrossRef]

- Yin, W.; Zhu, Z.; Kirkulak-Uludag, B.; Zhu, Y. The determinants of green credit and its impact on the performance of Chinese banks. J. Clean. Prod. 2021, 286, 124991. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, Y.; Wang, H.; Ouyang, X.; Xie, Y. Can green credit policy promote low-carbon technology innovation? J. Clean. Prod. 2022, 359, 132061. [Google Scholar] [CrossRef]

- Sun, Y.; Shi, B. The impact of Green Credit Policy on corporate innovation-an empirical study based on PSM-DID model. Ecol. Econ. 2019, 35, 87–91+160. [Google Scholar]

- Zhang, S.; Wu, Z.; He, Y.; Hao, Y. How does the green credit policy affect the technological innovation of enterprises? Evidence from China. Energy Econ. 2022, 106236. [Google Scholar] [CrossRef]

- Wang, H.; Qi, S.; Zhou, C.; Zhou, J.; Huang, X. Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 2022, 331, 129834. [Google Scholar] [CrossRef]

- Wang, X.; Wang, Y. A study on green credit policies to enhance green innovation. Manag. World 2021, 37, 173–188+11. [Google Scholar] [CrossRef]

- Zhang, Z.; Duan, H.; Shan, S.; Liu, Q.; Geng, W. The Impact of Green Credit on the Green Innovation Level of Heavy-Polluting Enterprises-Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 650. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, X.; Xing, C. How Does China’s Green Credit Policy Affect the Green Innovation of High Polluting Enterprises? the Perspective of Radical and Incremental Innovations. J. Clean. Prod. 2022, 336, 130387. [Google Scholar] [CrossRef]

- Yang, L.; Zhang, Z. The impact of Green Credit Policy on green innovation in enterprises. Sci. Res. 2022, 40, 345–356. [Google Scholar] [CrossRef]

- Chen, X.; Shi, Y.; Song, X. Green credit constraints, business credit and corporate environmental governance. Stud. Int. Financ. 2019, 12, 13–22. [Google Scholar] [CrossRef]

- Lai, T.; Li, S.; Liu, Q. Green Policy and Corporate Social Responsibility: Empirical Analysis of the Green Credit Guidelines in China. J. Asian Econ. 2022, 82, 101531. [Google Scholar] [CrossRef]

- Zhang, Y.; Wu, T. The impact of green credit on the cost of credit financing for listed companies-estimation based on a difference-in-difference model. Financ. Econ. 2018, 12, 8–12. [Google Scholar] [CrossRef]

- Xu, X.; Li, J. Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. J. Clean. Prod. 2020, 264, 121574. [Google Scholar] [CrossRef]

- Zhu, B.; Zhao, Y. Carbon risk and the cost of bank loans: Evidence from China. Technol. Forecast. Soc. Chang. 2022, 180, 121741. [Google Scholar] [CrossRef]

- Wang, L.; Zhu, Y. Green Credit Policy, Accounting Information Quality and Debt Cost. In Proceedings of the International Conference on Strategic Management, Antalya, Turkey, 28–30 October 2016; pp. 815–819. [Google Scholar]

- Liu, J.; Xia, Y.; Fan, Y.; Lin, S.; Wu, J. Assessment of a Green Credit Policy aimed at energy-intensive industries in China based on a financial CGE model. J. Clean. Prod. 2017, 163, 293–302. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. The Cost of Capital, Corporation Finance and the Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Rajan, R.G. Insiders and Outsiders: The Choice between Informed and Arm’s Length Debt. J. Financ. 1992, 47, 1367–4000. [Google Scholar] [CrossRef]

- Jensen, M. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Jalilvand, A.; Harris, R.S. Corporate Behavior in Adjusting to Capital Structure and Dividend Targets: An Econometric Study. J. Financ. 1984, 39, 127–145. [Google Scholar] [CrossRef]

- Diamond, D.W. Debt Maturity Structure and Liquidity Risk. Q. J. Econ. 1991, 106, 709–737. [Google Scholar] [CrossRef]

- Wei, Z.; Wang, Z.; Wu, Y.; Li, C. Financial ecosystem, audit opinion and debt financing cost. Audit. Res. 2012, 3, 98–105. [Google Scholar]

- Wang, C. An analysis of countermeasures to optimize the debt financing structure of state-owned enterprises. China J. Commer. 2020, 5, 62–63. [Google Scholar] [CrossRef]

- Li, G.; Liu, L. The cost of debt financing and private credit discrimination. J. Financ. Res. 2009, 12, 137–150. [Google Scholar]

- Ma, C.; Xu, J. Research on the bottlenecks and paths of debt financing for private SMEs. Mod. Bus. 2020, 23, 146–147. [Google Scholar] [CrossRef]

- Yu, K.; Li, Z.; Zhang, X.; Xu, J. The Puzzle of Corporate Investment Efficiency:The Financing Constraint Hypothesis and Monetary Policy Shocks. Econ. Res. J. 2014, 49, 106–120. [Google Scholar]

- Luo, H.; Chen, L. Research on the impact of VAT transformation on corporate financing constraints. Account. Res. 2012, 12, 43–49,94. [Google Scholar]

- Wang, Y.; Song, M. Macroeconomic uncertainty, capital demand and corporate investment. Econ. Res. J. 2014, 49, 4–17. [Google Scholar]

- Cheng, L.; Wang, Z. Credit discrimination and bank shareholding reform-empirical evidence based on borrowing overdue firms. J. Financ. Econ. 2015, 41, 82–93. [Google Scholar] [CrossRef]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching as an Econometric Evaluation Estimator. Rev. Econ. Stud. 1998, 65, 261–294. [Google Scholar] [CrossRef]

- Chai, S.; Zhang, K.; Wei, W.; Ma, W.; Abedin, M.Z. The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. J. Clean. Prod. 2022, 363, 132458. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef]

- Li, W.; Cui, G.; Zheng, M. Does green credit policy affect corporate debt financing? Evidence from China. Environ. Sci. Pollut. Res. 2021, 29, 5162–5171. [Google Scholar] [CrossRef] [PubMed]

- Feng, Y.; Shen, Q. How Does Green Credit Policy Affect Total Factor Productivity at the Corporate Level in China: The Mediating Role of Debt Financing and the Moderating Role of Financial Mismatch. Environ. Sci. Pollut. Res. 2022, 29, 23237–23248. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Symbol | Variable Interpretation |

|---|---|---|---|

| Explained variable | Short-term financing | Short-term loan | Short-term loan = short-term liabilities/total assets |

| Long-term financing | Long-term loan | Long-term loan = long-term liabilities/total assets | |

| Explanatory variable | Group virtual variable | The value of heavily polluting enterprises is 1, and that of non-heavily polluting enterprises is 0 | |

| Time virtual variable | Defined as 1 in 2012 and onwards, 0 before 2012 | ||

| Difference-in-difference variable | The interaction term represents the net effect of the policy | ||

| Nature of ownership | [(state shares + state-owned corporate shares)/total share capital] × 100% of the value of more than 50% that state-owned enterprise valuation is 1, otherwise 0 | ||

| Control variable | Age of enterprise | Age of enterprise establishment | |

| Scale of enterprise | Total assets of enterprises at year-end (logarithm taken) | ||

| Corporate profitability | Net Profit/average stockholders’ equity | ||

| Enterprise Development Capability (growth) | (current year main business income-last year main business income)/last year main business income | ||

| Current ratio | Average current assets/average current liabilities | ||

| Cash flow ratio | NET cash flow from operating activities/current liabilities | ||

| Cash flow interest earned ratio | NET cash flow from operating activities/interest expense | ||

| Ratio of liabilities to assets (financial risk) | Average total liabilities/average total assets of the business for the year |

| Before the Policy Was Implemented | After the Policy Was Implemented | Difference | |

|---|---|---|---|

| Non-heavily polluting enterprise () | |||

| Heavily polluting enterprise () | |||

| DID |

| Unmatched | Mean | %Reduct | t-Test | V(T)/ | ||||

|---|---|---|---|---|---|---|---|---|

| Variable | Matched | Treated | Control | %bias | |bias| | t | p > t | V(C) |

| age | U | 26.54 | 26.59 | −1.400 | −0.650 | 0.517 | 0.88 * | |

| M | 26.543 | 26.518 | 0.7 | 50.200 | 0.310 | 0.758 | 0.89 * | |

| C_ratio | U | 1.0282 | 1.2526 | −38.000 | −17.780 | 0.000 | 1.060 | |

| M | 1.0285 | 1.0473 | −3.200 | 91.600 | −1.480 | 0.139 | 1.30 * | |

| CC_ratio | U | 0.173 | 0.092 | 39.900 | 18.750 | 0.000 | 1.32 * | |

| M | 0.172 | 0.169 | 1.8 | 95.500 | 0.750 | 0.454 | 1.000 | |

| CF_ratio | U | 4.621 | 3.968 | 6.7 | 3.110 | 0.002 | 0.66 * | |

| M | 4.620 | 4.927 | −3.200 | 53.000 | −1.540 | 0.123 | 0.92 * | |

| lev | U | 0.571 | 0.584 | −7.800 | −3.640 | 0.000 | 0.990 | |

| M | 0.571 | 0.555 | 9.699 | −24.700 | 4.400 | 0.000 | 1.07 * | |

| roe | U | 0.044 | 0.046 | −1.200 | −0.560 | 0.575 | 1.17 * | |

| M | 0.044 | 0.039 | 3.3 | −173.200 | 1.430 | 0.153 | 1.10 * | |

| growth | U | 0.172 | 0.191 | −4.000 | −1.840 | 0.066 | 0.78 * | |

| M | 0.172 | 0.163 | 1.7 | 56.800 | 0.800 | 0.425 | 0.93 * | |

| size | U | 22.531 | 22.322 | 15.700 | 7.340 | 0.000 | 1.020 | |

| M | 22.529 | 22.403 | 9.5 | 39.600 | 4.160 | 0.000 | 0.960 | |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | N | Mean | SD | Min | Max |

| ownership | 8797 | 0.615 | 0.487 | 0 | 1 |

| Short-term loan | 8797 | 0.174 | 0.111 | 0 | 0.534 |

| Long-term loan | 8797 | 0.0844 | 0.102 | 0 | 0.465 |

| age | 8797 | 26.57 | 3.631 | 20 | 36 |

| C_ratio | 8797 | 1.150 | 0.594 | 0.184 | 4.498 |

| CC_ratio | 8797 | 0.128 | 0.205 | −0.402 | 1.024 |

| CF_ratio | 8797 | 4.266 | 9.794 | −24.67 | 53.49 |

| lev | 8797 | 0.578 | 0.163 | 0.160 | 1.100 |

| roe | 8797 | 0.0454 | 0.159 | −0.859 | 0.388 |

| growth | 8797 | 0.183 | 0.488 | −0.579 | 3.478 |

| size | 8797 | 22.41 | 1.335 | 19.43 | 25.98 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | Short-Term Loan | Short-Term Loan | Long-Term Loan | Long-Term Loan |

| did | 0.023 *** | 0.022 *** | −0.029 *** | −0.023 *** |

| (4.95) | (5.41) | (−6.66) | (−6.09) | |

| treat | 0.002 | 0.006 * | 0.050 *** | 0.032 *** |

| (0.45) | (1.94) | (15.23) | (11.56) | |

| period | −0.050 *** | −0.029 *** | 0.009 *** | −0.019 *** |

| (−16.05) | (−10.03) | (3.59) | (−7.58) | |

| age | 0.000 | 0.000 | ||

| (0.85) | (1.09) | |||

| C_ratio | −0.037 *** | 0.017 *** | ||

| (−18.61) | (8.42) | |||

| CC_ratio | −0.071 *** | 0.218 *** | ||

| (−10.31) | (26.97) | |||

| CF_ratio | −0.001 *** | −0.003 *** | ||

| (−5.89) | (−19.91) | |||

| lev | 0.156 *** | 0.207 *** | ||

| (17.67) | (25.46) | |||

| roe | −0.042 *** | 0.002 | ||

| (−4.41) | (0.33) | |||

| growth | −0.010 *** | 0.003 | ||

| (−4.16) | (1.56) | |||

| size | −0.019 *** | 0.022 *** | ||

| (−19.40) | (26.82) | |||

| Constant | 0.194 *** | 0.561 *** | 0.064 *** | −0.566 *** |

| (82.52) | (25.70) | (35.18) | (−30.46) | |

| Observations | 8797 | 8797 | 8797 | 8797 |

| R-squared | 0.038 | 0.271 | 0.034 | 0.310 |

| F test | 0 | 0 | 0 | 0 |

| r2_a | 0.0379 | 0.270 | 0.0339 | 0.309 |

| F | 121.3 | 257.9 | 93.23 | 245.6 |

| State-Owned | Non-State-Owned | State-Owned | Non-State-Owned | |

|---|---|---|---|---|

| Variables | Short-Term Loan | Short-Term Loan | Long-Term Loan | Long-Term Loan |

| did | 0.022 *** | 0.026 *** | −0.021 *** | −0.026 *** |

| (4.04) | (4.05) | (−4.40) | (−4.50) | |

| treat | 0.010 ** | −0.002 | 0.028 *** | 0.040 *** |

| (2.47) | (−0.40) | (7.64) | (9.41) | |

| period | −0.020 *** | −0.047 *** | −0.024 *** | −0.010 *** |

| (−5.22) | (−10.09) | (−7.23) | (−2.66) | |

| age | 0.001 ** | −0.001 | 0.000 | 0.000 |

| (2.10) | (−1.14) | (0.40) | (1.30) | |

| C_ratio | −0.034 *** | −0.043 *** | 0.017 *** | 0.018 *** |

| (−12.49) | (−14.46) | (6.34) | (5.82) | |

| CC_ratio | −0.060 *** | −0.081 *** | 0.214 *** | 0.220 *** |

| (−6.81) | (−7.37) | (21.40) | (16.65) | |

| CF_ratio | −0.001 *** | −0.000 | −0.003 *** | −0.003 *** |

| (−6.62) | (−1.48) | (−14.97) | (−13.10) | |

| lev | 0.176 *** | 0.125 *** | 0.200 *** | 0.218 *** |

| (15.39) | (8.93) | (19.02) | (17.06) | |

| roe | −0.038 *** | −0.051 *** | −0.012 | 0.026 ** |

| (−2.97) | (−3.52) | (−1.24) | (2.29) | |

| growth | −0.010 *** | −0.008 ** | 0.005 * | 0.001 |

| (−3.29) | (−2.49) | (1.74) | (0.44) | |

| size | −0.021 *** | −0.014 *** | 0.024 *** | 0.019 *** |

| (−17.82) | (−8.79) | (22.63) | (14.66) | |

| Constant | 0.584 *** | 0.522 *** | −0.600 *** | −0.515 *** |

| (20.54) | (15.09) | (−24.58) | (−17.91) | |

| Observations | 5408 | 3389 | 5408 | 3389 |

| R-squared | 0.264 | 0.293 | 0.301 | 0.330 |

| F test | 0 | 0 | 0 | 0 |

| r2_a | 0.263 | 0.291 | 0.300 | 0.327 |

| F | 145.1 | 133.6 | 154.4 | 92.22 |

| 1:4 Neighborhood Match | Caliper Match | |||

|---|---|---|---|---|

| Variables | Short-Term Loan | Long-Term Loan | Short-Term Loan | Long-Term Loan |

| did | 0.026 *** | −0.021 *** | 0.023 *** | −0.023 *** |

| (5.98) | (−5.48) | (5.49) | (−6.25) | |

| treat | 0.005 | 0.029 *** | 0.006 * | 0.033 *** |

| (1.52) | (9.97) | (1.88) | (11.69) | |

| period | −0.033 *** | −0.017 *** | −0.029 *** | −0.019 *** |

| (−10.40) | (−6.28) | (−10.03) | (−7.57) | |

| age | 0.000 | 0.000 | 0.000 | 0.000 |

| (1.12) | (0.77) | (0.88) | (1.07) | |

| C_ratio | −0.036 *** | 0.017 *** | −0.038 *** | 0.018 *** |

| (−17.22) | (7.51) | (−18.91) | (8.63) | |

| CC_ratio | −0.063 *** | 0.210 *** | −0.068 *** | 0.213 *** |

| (−8.48) | (24.33) | (−9.85) | (26.29) | |

| CF_ratio | −0.001 *** | −0.003 *** | −0.001 *** | −0.003 *** |

| (−5.87) | (−17.90) | (−6.13) | (−19.61) | |

| lev | 0.159 *** | 0.198 *** | 0.157 *** | 0.207 *** |

| (16.65) | (22.70) | (17.75) | (25.32) | |

| roe | −0.046 *** | 0.004 | −0.042 *** | 0.002 |

| (−4.61) | (0.55) | (−4.37) | (0.22) | |

| growth | −0.009 *** | 0.003 | −0.010 *** | 0.003 |

| (−3.43) | (1.38) | (−4.16) | (1.49) | |

| size | −0.018 *** | 0.022 *** | −0.019 *** | 0.022 *** |

| (−17.71) | (24.97) | (−19.45) | (26.87) | |

| Constant | 0.553 *** | −0.556 *** | 0.562 *** | −0.567 *** |

| (23.16) | (−27.98) | (25.74) | (−30.44) | |

| Observations | 7629 | 7629 | 8796 | 8796 |

| R-squared | 0.274 | 0.287 | 0.271 | 0.303 |

| F test | 0 | 0 | 0 | 0 |

| r2_a | 0.273 | 0.286 | 0.270 | 0.303 |

| F | 228.2 | 196.7 | 258.9 | 240.5 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, Y.; Zhang, Y. The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method. Int. J. Environ. Res. Public Health 2022, 19, 11287. https://doi.org/10.3390/ijerph191811287

Yang Y, Zhang Y. The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method. International Journal of Environmental Research and Public Health. 2022; 19(18):11287. https://doi.org/10.3390/ijerph191811287

Chicago/Turabian StyleYang, Yan, and Yingli Zhang. 2022. "The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method" International Journal of Environmental Research and Public Health 19, no. 18: 11287. https://doi.org/10.3390/ijerph191811287

APA StyleYang, Y., & Zhang, Y. (2022). The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method. International Journal of Environmental Research and Public Health, 19(18), 11287. https://doi.org/10.3390/ijerph191811287