Sustainable Economic Development, Digital Payment, and Consumer Demand: Evidence from China

Abstract

:1. Introduction

2. Literature Review

2.1. COVID-19 Pandemic and Sustainable Economic Development

2.2. Willingness and Behavior to Use Digital Payments

2.3. Consumption Behavior and Consumption Demand

2.4. The Impact of Digital Payments on Consumer Demand

3. Research Design

3.1. Data Source

3.2. Variable Selection

3.2.1. Explained Variable

3.2.2. Core Explanatory Variable

3.2.3. Control Variables

3.2.4. Instrumental Variables

3.3. Econometric Model

4. Test Results and Analysis

4.1. Descriptive Statistics

4.2. Correlation Test

4.3. Benchmark Regression

4.4. Endogeneity Test

4.4.1. Variable Lag

4.4.2. Instrumental Variable Method

4.4.3. PSM-DID Methods

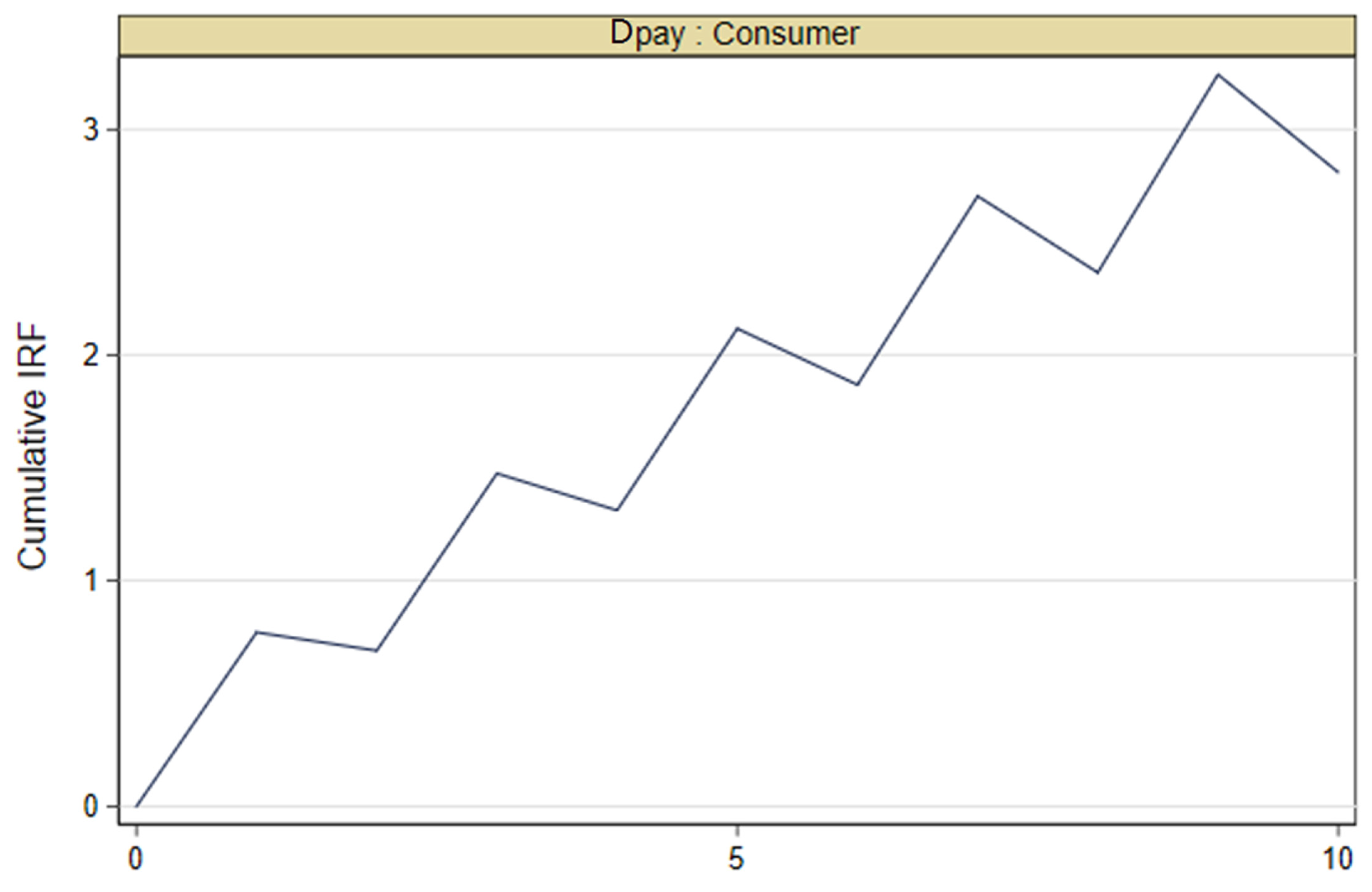

4.4.4. PVAR Model

4.5. Robustness Test

4.5.1. Variable Substitution Method

4.5.2. Changing the Sample Size

4.5.3. Robust Test

4.6. Heterogeneity Test

4.6.1. Regional Heterogeneity

4.6.2. Temporal Heterogeneity

4.6.3. Urban-Rural Heterogeneity

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Luarn, P.; Lin, H.-H. Toward an understanding of the behavioral intention to use mobile banking. Comput. Hum. Behav. 2005, 21, 873–891. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Antecedents of the adoption of the new mobile payment systems: The moderating effect of age. Comput. Hum. Behav. 2014, 35, 464–478. [Google Scholar] [CrossRef]

- Yang, Q.; Pang, C.; Liu, L.; Yen, D.C.; Tarn, J.M. Exploring consumer perceived risk and trust for online payments: An empirical study in China’s younger generation. Comput. Hum. Behav. 2015, 50, 9–24. [Google Scholar] [CrossRef]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Beck, T.; Pamuk, H.; Ramrattan, R.; Uras, B.R. Payment instruments, finance and development. J. Dev. Econ. 2018, 133, 162–186. [Google Scholar] [CrossRef]

- Yao, M.; Di, H.; Zheng, X.; Xu, X. Impact of payment technology innovations on the traditional financial industry: A focus on China. Technol. Forecast. Soc. Chang. 2018, 135, 199–207. [Google Scholar] [CrossRef]

- Lashitew, A.A.; van Tulder, R.; Liasse, Y. Mobile phones for financial inclusion: What explain the diffusion of mobile money innovations? Res. Policy 2019, 48, 1201–1215. [Google Scholar] [CrossRef]

- Karimi, S.; Liu, Y.L. The differential impact of “mood” on consumers’ decisions, a case of mobile payment adoption. Comput. Hum. Behav. 2020, 102, 132–143. [Google Scholar] [CrossRef]

- Gross, D.B. An empirical analysis of personal bankruptcy and delinquency. Rev. Financ. Stud. 2002, 15, 319–347. [Google Scholar] [CrossRef] [Green Version]

- Durkin, T.A.; Price, N. Credit cards: Use and Consumer Attitudes, 1970–2000. Fed. Reserve Bull. 2000, 86, 623–634. [Google Scholar] [CrossRef]

- Moody’s Analytics. The Impact of Electronic Payments on Economic Growth; Moody’s Analytics Inc.: West Chester, PA, USA, 2016. [Google Scholar]

- Xu, X.; Li, Q.; Peng, L.; Hsia, T.-L.; Huang, C.-J.; Wu, J.-H. The impact of informational incentives and social influence on consumer behavior during Alibaba’s online shopping carnival. Comput. Hum. Behav. 2017, 76, 245–254. [Google Scholar] [CrossRef]

- Mao, L.; Chen, S. The Growth of Mobile Payment and Effect on Consumption via Cash and Bankcard. In Proceedings of the International Conference on Biomedical Engineering and Informatics, Shenyang, China, 14–16 October 2015; Volume 10, pp. 872–877. [Google Scholar]

- Anderson, D.M.; Strand, A.; Collins, J.M. The Impact of Electronic Payments for Vulnerable Consumers: Evidence from Social Security. J. Consum. Aff. 2018, 52, 35–60. [Google Scholar] [CrossRef]

- Lombart, C.; Millan, E.; Normand, J.M.; Verhulst, A.; Labbé-Pinlon, B.; Moreau, G. Effects of physical, non-immersive virtual, and immersive virtual store environments on consumers’ perceptions and purchase behavior. Comput. Hum. Behav. 2020, 110, 106374. [Google Scholar] [CrossRef]

- Deliu, D. The Impact of a Socio-Economic Crisis on Corporate Governance Effectiveness and Sustainable Development. Acumen: The Current New Coronavirus (COVID-19) Pandemic. In Education Excellence and Innovation Management: A 2025 Vision to Sustain Economic Development during Global Challenges; International Business Information Management Association: Sewilla, Spain, 2020; pp. 17447–17457. [Google Scholar]

- Chen, S. What Implications Does COVID-19 Have on Sustainable Economic Development in the Medium and Long Terms? Front. Econ. China 2020, 15, 380–395. [Google Scholar]

- Li, J.; Wu, Y.; Xiao, J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef] [Green Version]

- Nundy, S.; Ghosh, A.; Mesloub, A.; Albaqawy, G.A.; Alnaim, M.M. Impact of COVID-19 pandemic on socio-economic, energy-environment and transport sector globally and sustainable development goal (SDG). J. Clean. Prod. 2021, 312, 127705. [Google Scholar] [CrossRef]

- Ahmed, M.Y.; Sarkodie, S.A. How COVID-19 pandemic may hamper sustainable economic development. J. Public Aff. 2021, 21, e2675. [Google Scholar] [CrossRef]

- Yin, C.; Zhao, W.; Cherubini, F.; Pereira, P. Integrate ecosystem services into socio-economic development to enhance achievement of sustainable development goals in the post-pandemic era. Geogr. Sustain. 2021, 2, 68–73. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strategy Environ. 2022, 5, 1–17. [Google Scholar] [CrossRef]

- Vavoura, C.; Vavouras, I. Sustainable economic development in the European Union and COVID-19. Evol. Inst. Econ. Rev. 2022, 19, 449–467. [Google Scholar] [CrossRef]

- Zhou, G.; Zhu, J.; Luo, S. The impact of fintech innovation on green growth in China: Mediating effect of green finance. Ecol. Econ. 2022, 193, 107308. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Arango, C.; Huynh, K.P.; Sabetti, L. Consumer payment choice: Merchant card acceptance versus pricing incentives. J. Bank. Financ. 2015, 55, 130–141. [Google Scholar] [CrossRef]

- David, B.; Abel, F.; Patrick, W. Debit card and demand for cash. J. Bank. Financ. 2016, 73, 55–66. [Google Scholar] [CrossRef]

- Cocosila, M.; Trabelsi, H. An integrated value-risk investigation of contactless mobile payments adoption. Electron. Commer. Res. Appl. 2016, 20, 159–170. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Muñoz-Leiva, F.; Sánchez-Fernández, J. A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Serv. Bus. 2018, 12, 25–64. [Google Scholar] [CrossRef]

- Park, J.; Ahn, J.; Thavisay, T.; Ren, T. Examining the role of anxiety and social influence in multi-benefits of mobile payment service. J. Retail. Consum. Serv. 2019, 47, 140–149. [Google Scholar] [CrossRef]

- Verkijika, S.F. An effective response model for understanding the acceptance of mobile payment systems. Electron. Commer. Res. Appl. 2020, 39, 100905. [Google Scholar] [CrossRef]

- Li, B.G.; McAndrews, J.; Wang, Z. Two-sided market, R&D, and payments system evolution. J. Monet. Econ. 2019, 115, 180–199. [Google Scholar]

- Vondolia, G.K.; Navrud, S. Are non-monetary payment modes more uncertain for stated preference elicitation in developing countries? J. Choice Model. 2019, 30, 73–87. [Google Scholar] [CrossRef] [Green Version]

- Morse, E.A. From Rai stones to Blockchains: The transformation of payments. Comput. Law Secur. Rev. 2018, 34, 946–953. [Google Scholar] [CrossRef]

- Kim, M.; Kim, S.; Kim, J. Can mobile and biometric payments replace cards in the Korean offline payments market? Consumer preference analysis for payment systems using a discrete choice model. Telemat. Inform. 2019, 38, 46–58. [Google Scholar] [CrossRef]

- Shefrin, H.M.; Thaler, R.H. The Behavioral Life-Cycle Hypothesis. Econ. Inq. 1988, 26, 10–14. [Google Scholar] [CrossRef]

- Phelps, E.S.; Pollak, R.A. On Second-best National Saving and Game-equilibrium Growth. Rev. Econ. Stud. 1968, 35, 185–199. [Google Scholar] [CrossRef]

- Chung, S.H.; Herrnstein, R.J. Choice and Delay of Reinforcement. J. Exp. Anal. Behav. 2013, 10, 67–74. [Google Scholar] [CrossRef] [Green Version]

- Ludvigson, S. Consumption and Credit: A Model of Time-Varying Liquidity Constraints. Rev. Econ. Stat. 1999, 81, 434–447. [Google Scholar] [CrossRef] [Green Version]

- Soman, D.; Cheema, A. The effect of credit on spending decisions: The role of the credit limit and credibility. Mark. Sci. 2002, 21, 32–53. [Google Scholar] [CrossRef] [Green Version]

- Zhao, M.; Hsu, M. China’ s economic fluctuations and consumption smoothing: Is consumption more volatile than output in China? China Econ. Rev. 2012, 23, 918–927. [Google Scholar] [CrossRef]

- Zhao, D.; Wu, T.; He, Q. Consumption inequality and its evolution in urban China. China Econ. Rev. 2017, 46, 208–228. [Google Scholar] [CrossRef]

- Bechlioulis, A.P.; Brissimis, S.N. Consumer Debt Non-Payment and the Borrowing Constraint: Implications for Consumer Behavior. J. Bank. Financ. 2019, 101, 161–172. [Google Scholar] [CrossRef]

- Cao, J.; Ho, M.S.; Hu, W.; Jorgenson, D. Estimating flexible consumption functions for urban and rural households in China. China Econ. Rev. 2020, 61, 101453. [Google Scholar] [CrossRef]

- Cachon, G.P.; Swinney, R. The Value of Fast Fashion: Quick Response, Enhanced Design, and Strategic Consumer Behavior. Manag. Sci. 2011, 57, 778–795. [Google Scholar] [CrossRef] [Green Version]

- Kraft, H.; Munk, C. Optimal housing, consumption, and investment decisions over the life cycle. Manag. Sci. 2011, 57, 1025–1041. [Google Scholar] [CrossRef] [Green Version]

- Hwang, M.; Park, S. The impact of Walmart supercenter conversion on consumer shopping behavior. Manag. Sci. 2016, 62, 817–828. [Google Scholar] [CrossRef]

- Jinkins, D. Conspicuous consumption in the United States and China. J. Econ. Behav. Organ. 2016, 127, 115–132. [Google Scholar] [CrossRef] [Green Version]

- Yamamori, T.; Iwata, K.; Ogawa, A. Does money illusion matter in intertemporal decision making? J. Econ. Behav. Organ. 2018, 145, 465–473. [Google Scholar] [CrossRef]

- Aviv, Y.; Wei, M.M.; Zhang, F. Responsive pricing of fashion products: The effects of demand learning and strategic consumer behavior. Manag. Sci. 2019, 65, 2982–3000. [Google Scholar] [CrossRef]

- Iviane, R.L.; Francisco, L.-C.; Juanm, S.-F.; Francisco, M.-L. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar]

- Sugden, R.; Wang, M.; John, D. Take it or leave it: Experimental evidence on the effect of time-limited offers on consumer behavior. J. Econ. Behav. Organ. 2019, 168, 1–23. [Google Scholar] [CrossRef]

- Petach, L.A.; Tavani, D. Consumption externalities and growth: Theory and evidence for the United States. J. Econ. Behav. Organ. 2021, 183, 976–997. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.; Wang, K.; Zhang, X.; Cheng, Z. Measuring the Development of Digital Inclusive Finance in China: Index Compilation and Spatial Characteristics. China Econ. Q. 2020, 19, 1401–1418. (In Chinese) [Google Scholar]

{kind=link}

| Variable Types | Variable Name | Variable Code | Variable Definition and Measurement Method |

|---|---|---|---|

| Explained variable | Consumer demand | Consumer | Per capita consumption expenditure |

| Urban consumption demand | Con-urban | Urban per capita consumption expenditure | |

| Rural consumption demand | Con-rural | Rural per capita consumption expenditure | |

| Explanatory variables | Digital pay | D-pay | Digital payment index in Peking University Digital Financial Inclusion Index |

| Control variables | Level of economic development | GDP | GDP per capita |

| Degree of financial development | Finance | Financial sector as a share of GDP | |

| Urbanization rate | Urbanization | Ratio of urban population to total population at year-end | |

| Education level | Education | Number of higher education students per 10,000 people | |

| Instrumental variable | Degree of digitization | Digital | Financial digitization degree index in Peking University Digital Financial Inclusion Index |

| Variables | N | Mean | p50 | sd | Min | Max |

|---|---|---|---|---|---|---|

| Consumer | 310 | 13.34 | 13.31 | 0.45 | 12.17 | 14.67 |

| Con-urban | 310 | 9.93 | 9.93 | 0.29 | 9.34 | 10.78 |

| Con-rural | 310 | 9.15 | 9.16 | 0.38 | 8.05 | 10.02 |

| Dpay | 310 | 1.85 | 1.97 | 0.92 | 0.00 | 3.80 |

| GDP | 310 | 10.78 | 10.73 | 0.44 | 9.68 | 12.01 |

| Finance | 310 | 9.27 | 6.48 | 14.77 | 0.46 | 97.53 |

| Urbanization | 310 | 0.58 | 0.57 | 0.13 | 0.22 | 0.90 |

| Education | 310 | 1.97 | 1.91 | 0.56 | 0.74 | 4.13 |

| Digital | 310 | 2.90 | 3.23 | 1.17 | 0.08 | 4.62 |

| Variable | Consumer | Con-Urban | Con-Rural | Dpay | DigitalL | GDP | Finance | Urbanization | Education |

|---|---|---|---|---|---|---|---|---|---|

| Consumer | 1.000 | ||||||||

| Con-urban | 0.931 | 1.000 | |||||||

| 0.000 | |||||||||

| Con-rural | 0.808 | 0.923 | 1.000 | ||||||

| 0.000 | 0.000 | ||||||||

| Dpay | 0.623 | 0.818 | 0.851 | 1.000 | |||||

| 0.000 | 0.000 | 0.000 | |||||||

| Digital | 0.414 | 0.614 | 0.657 | 0.840 | 1.000 | ||||

| 0.000 | 0.000 | 0.000 | 0.000 | ||||||

| GDP | 0.866 | 0.896 | 0.899 | 0.697 | 0.451 | 1.000 | |||

| 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| Finance | −0.036 | 0.086 | −0.110 | 0.046 | 0.070 | 0.014 | 1.000 | ||

| 0.533 | 0.129 | 0.054 | 0.425 | 0.221 | 0.803 | ||||

| Urbanization | 0.904 | 0.789 | 0.784 | 0.476 | 0.259 | 0.864 | −0.224 | 1.000 | |

| 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||

| Education | 0.477 | 0.408 | 0.489 | 0.347 | 0.249 | 0.514 | −0.214 | 0.638 | 1.000 |

| 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variable | (1) | (2) |

|---|---|---|

| m1 | m2 | |

| Consumer | Consumer | |

| Dpay | 0.066 *** | |

| (3.698) | ||

| GDP | 0.408 *** | 0.226 *** |

| (6.666) | (2.924) | |

| Finance | 0.009 *** | 0.005 ** |

| (3.519) | (1.992) | |

| Urbanization | 3.539 *** | 3.150 *** |

| (9.488) | (8.300) | |

| Education | −0.200 *** | −0.162 *** |

| (−4.899) | (−3.925) | |

| Constant | 7.202 *** | 9.221 *** |

| (15.015) | (12.811) | |

| Observations | 310 | 310 |

| R-squared | 0.884 | 0.890 |

| Number of id | 31 | 31 |

| F | 525.9 | 442.8 |

| Variable | (1) | (2) |

|---|---|---|

| m1 | m2 | |

| Consumer | Consumer | |

| L.Dpay | 0.085 *** | |

| (4.558) | ||

| L.GDP | 0.218 *** | −0.013 |

| (3.141) | (−0.151) | |

| L.Finance | 0.017 *** | 0.013 *** |

| (5.612) | (4.114) | |

| L.Urbanization | 3.602 *** | 3.080 *** |

| (8.486) | (7.265) | |

| L.Education | −0.158 *** | −0.118 ** |

| (−2.891) | (−2.209) | |

| Constant | 9.116 *** | 11.712 *** |

| (16.773) | (15.150) | |

| Observations | 279 | 279 |

| R-squared | 0.841 | 0.854 |

| Number of id | 31 | 31 |

| F | 322.8 | 283.3 |

| Variable | (1) | (2) | (3) |

|---|---|---|---|

| m1 | m2 | m3 | |

| Consumer | Consumer | Consumer | |

| Dpay | 0.102 *** | 0.074 *** | 0.075 *** |

| (2.676) | (2.730) | (2.834) | |

| GDP | 0.130 | 0.195 * | 0.193 * |

| (1.079) | (1.948) | (1.951) | |

| Finance | 0.003 | 0.002 | 0.002 |

| (1.044) | (0.594) | (0.581) | |

| Urbanization | 2.943 *** | 3.047 *** | 3.041 *** |

| (6.852) | (6.946) | (6.962) | |

| Education | −0.142 *** | −0.159 *** | −0.159 *** |

| (−3.093) | (−3.383) | (−3.383) | |

| Constant | 10.295 *** | 9.632 *** | 9.659 *** |

| (8.244) | (9.737) | (9.943) | |

| Observations | 310 | 279 | 279 |

| Number of id | 31 | 31 | 31 |

| chi2 | 8.759 × 106 | 8.213 × 106 | 8.215 × 106 |

| Sample | Treated | Controls | Difference | S.E. | Tstat |

|---|---|---|---|---|---|

| Unmatched | 13.628 | 13.200 | 0.428 | 0.049 | 8.7 |

| Matched | 13.628 | 13.501 | 0.127 | 0.105 | 1.2 |

| Variable | Coef. | Std. Err. | z | P > z | 95% Conf. | Interval |

|---|---|---|---|---|---|---|

| Consumer | ||||||

| L1.Consumer | −2.143 | 0.920 | −2.330 | 0.020 | −3.946 | −0.339 |

| L1.Dpay | 0.771 | 0.247 | 3.130 | 0.002 | 0.288 | 1.254 |

| Dpay | ||||||

| L1.Consumer | −4.358 | 1.589 | −2.740 | 0.006 | −7.472 | −1.243 |

| L1.Dpay | 2.038 | 0.421 | 4.830 | 0.000 | 1.212 | 2.864 |

| Variable | (1) | (2) |

|---|---|---|

| m1 | m2 | |

| Consumer2 | Consumer2 | |

| Dpay | 0.095 *** | |

| (3.065) | ||

| GDP | 1.049 *** | 0.788 *** |

| (9.965) | (5.876) | |

| Finance | −0.006 | −0.011 ** |

| (−1.261) | (−2.315) | |

| Urbanization | 2.087 *** | 1.528 ** |

| (3.251) | (2.322) | |

| Education | −0.300 *** | −0.245 *** |

| (−4.266) | (−3.426) | |

| Constant | 6.099 *** | 8.999 *** |

| (7.390) | (7.213) | |

| Observations | 310 | 310 |

| R-squared | 0.807 | 0.814 |

| Number of id | 31 | 31 |

| F | 287.9 | 239.2 |

| Variable | (1) | (2) |

|---|---|---|

| m1 | m2 | |

| Consumer | Consumer | |

| Dpay | 0.068 *** | |

| (3.789) | ||

| GDP | 0.388 *** | 0.208 *** |

| (6.422) | (2.751) | |

| Finance | 0.007 *** | 0.003 |

| (2.759) | (1.193) | |

| Urbanization | 3.724 *** | 3.237 *** |

| (9.766) | (8.216) | |

| Education | −0.215 *** | −0.167 *** |

| (−4.991) | (−3.802) | |

| Constant | 7.357 *** | 9.392 *** |

| (15.548) | (13.254) | |

| Observations | 310 | 310 |

| R-squared | 0.885 | 0.891 |

| Number of id | 31 | 31 |

| F | 529.1 | 446.7 |

| Variable | (1) | (2) |

|---|---|---|

| m1 | m2 | |

| Consumer | Consumer | |

| Dpay | 0.068 ** | |

| (2.392) | ||

| GDP | 0.388 *** | 0.208 |

| (3.250) | (1.414) | |

| Finance | 0.007 | 0.003 |

| (0.902) | (0.513) | |

| Urbanization | 3.724 *** | 3.237 *** |

| (5.089) | (4.585) | |

| Education | −0.215 *** | −0.167 ** |

| (−2.904) | (−2.215) | |

| Constant | 7.357 *** | 9.392 *** |

| (7.802) | (7.031) | |

| Observations | 310 | 310 |

| R-squared | 0.885 | 0.891 |

| Number of id | 31 | 31 |

| F | 163.9 | 126.4 |

| Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Northeast | East | Central | West | |

| Consumer | Consumer | Consumer | Consumer | |

| Dpay | 0.056 | 0.046 * | 0.080 | 0.142 *** |

| (0.981) | (1.745) | (0.900) | (2.640) | |

| GDP | 0.425 | 0.142 | 0.014 | 0.272 * |

| (1.373) | (1.278) | (0.058) | (1.712) | |

| Finance | 0.023 | 0.025 *** | 0.006 | 0.001 |

| (1.133) | (3.410) | (0.193) | (0.231) | |

| Urbanization | 2.423 | 2.792 *** | 4.234 | 2.244 * |

| (0.760) | (6.167) | (1.370) | (1.982) | |

| Education | −0.379 * | 0.001 | −0.238 | −0.257 *** |

| (−2.072) | (0.014) | (−1.110) | (−3.091) | |

| Constant | 8.019 ** | 9.896 *** | 10.949 *** | 9.359 *** |

| (2.759) | (8.781) | (6.395) | (6.574) | |

| Observations | 30 | 100 | 60 | 120 |

| R-squared | 0.864 | 0.928 | 0.907 | 0.892 |

| Number of id | 3 | 10 | 6 | 12 |

| F | 27.93 | 220.2 | 95.50 | 170.4 |

| Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Northeast | East | Central | West | |

| Consumer | Consumer | Consumer | Consumer | |

| Dpay | 0.152 | −0.012 | −0.101 | 0.066 |

| (1.660) | (−0.383) | (−1.234) | (1.270) | |

| GDP | 1.096 ** | 0.178 | 0.114 | 0.145 |

| (3.120) | (0.704) | (0.449) | (0.996) | |

| Finance | −0.023 | 0.033 *** | 0.079 *** | 0.007 ** |

| (−0.570) | (2.773) | (2.919) | (2.042) | |

| Urbanization | 8.088 | 4.398 *** | 6.597 * | 3.536 ** |

| (1.875) | (5.337) | (1.940) | (2.553) | |

| Education | −1.849 ** | 0.010 | −0.314 | 0.042 |

| (−2.586) | (0.091) | (−1.110) | (0.234) | |

| Constant | 0.825 | 8.444 *** | 8.762 *** | 9.605 *** |

| (0.205) | (3.667) | (4.634) | (7.718) | |

| Observations | 15 | 50 | 30 | 60 |

| R-squared | 0.926 | 0.928 | 0.949 | 0.942 |

| Number of id | 3 | 10 | 6 | 12 |

| F | 17.43 | 89.76 | 70.84 | 139.1 |

| Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Northeast | East | Central | West | |

| Consumer | Consumer | Consumer | Consumer | |

| Dpay | −0.022 | −0.123 | 0.078 | 0.128 |

| (−0.036) | (−0.798) | (0.375) | (0.773) | |

| GDP | 0.488 | 0.702 ** | 0.110 | 0.958 ** |

| (0.353) | (2.108) | (0.180) | (2.406) | |

| Finance | 0.131 ** | 0.013 | −0.059 | 0.000 |

| (2.398) | (1.109) | (−0.968) | (0.047) | |

| Urbanization | −2.996 | 2.462 * | 4.566 | −3.352 |

| (−0.303) | (1.890) | (0.976) | (−1.176) | |

| Education | −0.423 | −0.146 | −0.389 | −0.066 |

| (−1.233) | (−1.303) | (−1.304) | (−0.478) | |

| Constant | 10.402 | 4.750 | 10.423 ** | 4.708 |

| (1.034) | (1.537) | (2.133) | (1.460) | |

| Observations | 15 | 50 | 30 | 60 |

| R-squared | 0.675 | 0.693 | 0.519 | 0.463 |

| Number of id | 3 | 10 | 6 | 12 |

| F | 2.907 | 15.81 | 4.101 | 7.421 |

| Variable | (1) | (2) | (3) |

|---|---|---|---|

| m1 | m2 | m3 | |

| Consumer | Con-urban | Con-rural | |

| Dpay | 0.066 *** | 0.111 *** | 0.139 *** |

| (3.698) | (12.003) | (11.998) | |

| GDP | 0.226 *** | 0.313 *** | 0.518 *** |

| (2.924) | (7.830) | (10.391) | |

| Finance | 0.005 ** | 0.002 | 0.001 |

| (1.992) | (1.520) | (0.618) | |

| Urbanization | 3.150 *** | 0.827 *** | 0.551 ** |

| (8.300) | (4.213) | (2.252) | |

| Education | −0.162 *** | −0.008 | 0.096 *** |

| (−3.925) | (−0.383) | (3.622) | |

| Constant | 9.221 *** | 5.860 *** | 2.791 *** |

| (12.811) | (15.745) | (6.019) | |

| Observations | 310 | 310 | 310 |

| R-squared | 0.890 | 0.963 | 0.970 |

| Number of id | 31 | 31 | 31 |

| F | 442.8 | 1444 | 1757 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, R. Sustainable Economic Development, Digital Payment, and Consumer Demand: Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 8819. https://doi.org/10.3390/ijerph19148819

Zhou R. Sustainable Economic Development, Digital Payment, and Consumer Demand: Evidence from China. International Journal of Environmental Research and Public Health. 2022; 19(14):8819. https://doi.org/10.3390/ijerph19148819

Chicago/Turabian StyleZhou, Rui. 2022. "Sustainable Economic Development, Digital Payment, and Consumer Demand: Evidence from China" International Journal of Environmental Research and Public Health 19, no. 14: 8819. https://doi.org/10.3390/ijerph19148819

APA StyleZhou, R. (2022). Sustainable Economic Development, Digital Payment, and Consumer Demand: Evidence from China. International Journal of Environmental Research and Public Health, 19(14), 8819. https://doi.org/10.3390/ijerph19148819