Influence of ESGC Indicators on Financial Performance of Listed Pharmaceutical Companies

, , and

, , and

Abstract

1. Introduction

1.1. Stakeholder Theory

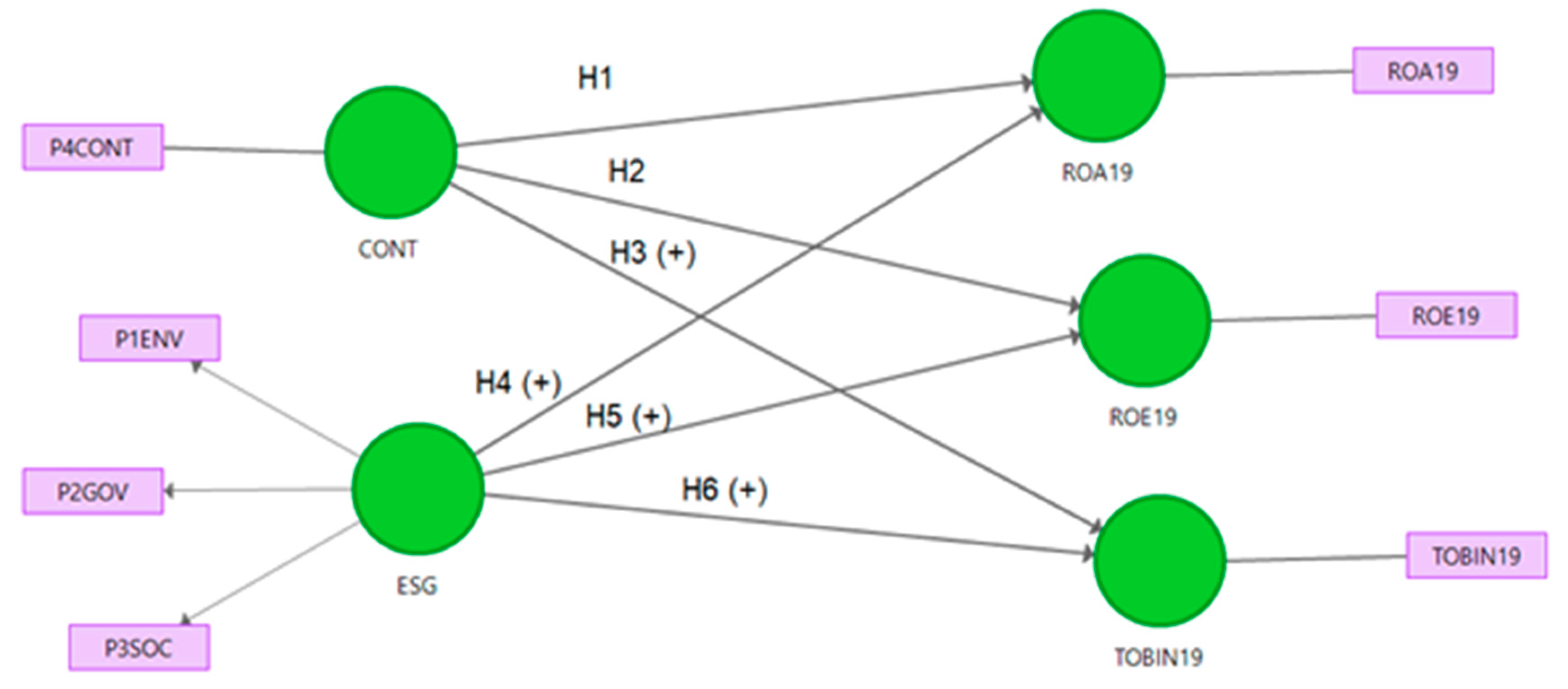

1.2. Hypotheses

2. Materials and Methods

2.1. Data

2.2. Confirmatory Model

2.3. PLS-SEM

3. Results

3.1. Descriptive Analysis

3.2. Measurement Model

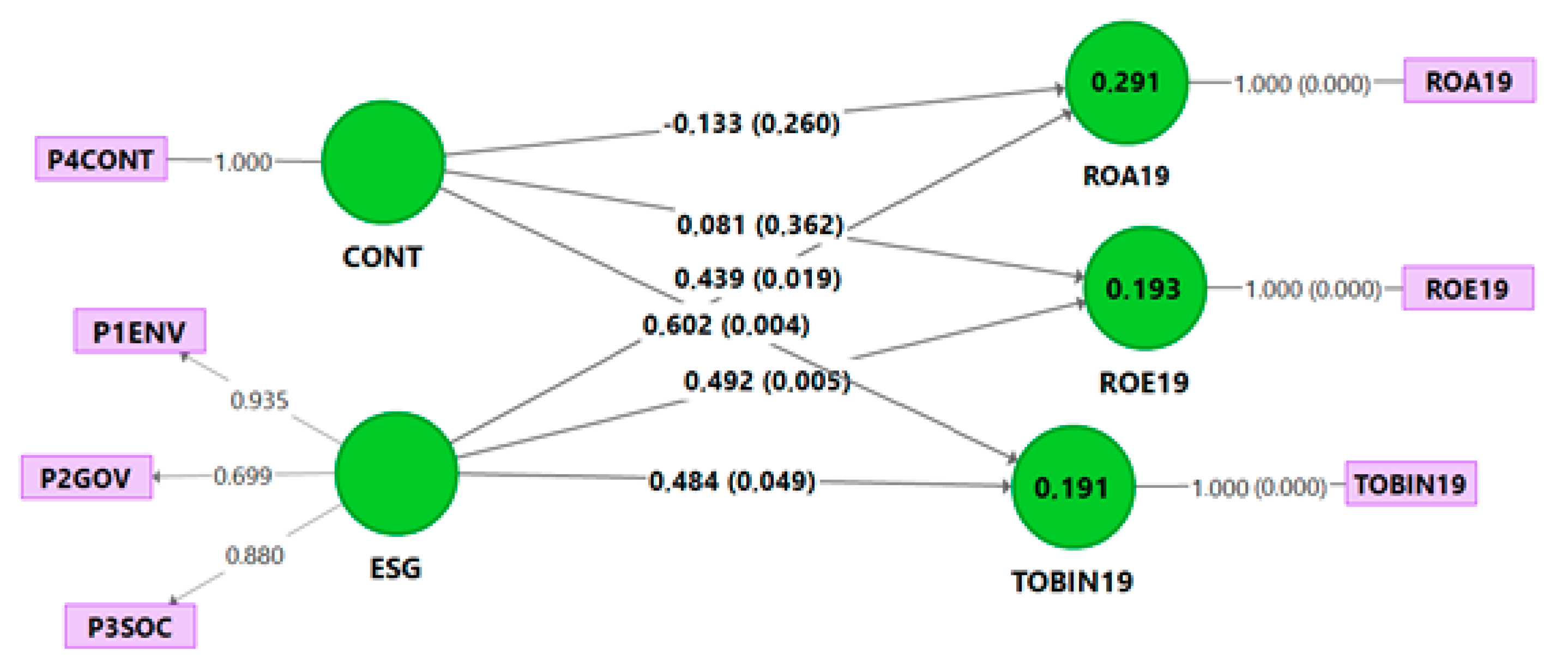

3.3. Structural Model

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Name | TICKER | Environment Pillar Score | Social Pillar Score | Governance Pillar Score | Controversies Score |

|---|---|---|---|---|---|

| ABBVIE INC. | ABBV | A- | A | B+ | C |

| ABBOTT LABORATORIES | ABT | B+ | A− | A− | C |

| ALKERMES PLC | ALKS | B− | A+ | D+ | A+ |

| BRISTOL-MYERS SQUIBB | BMY | B+ | A− | A− | B+ |

| BLUEPRINT MEDI CM ST | BPMC | D− | C | C+ | A+ |

| CARDINAL HEALTH INC | CAH | C | C− | B | D− |

| CATALENT, INC. | CTLT | C− | B− | C− | A+ |

| ELANCO ANIMAL HEALTH | ELAN | D | D+ | C | A+ |

| ENDO INT’L PLC | ENDP | D | C+ | D+ | D+ |

| ESPERION THERAPTC CM | ESPR | D− | C | C | A+ |

| FLEXION THERAPEUTICS | FLXN | D− | A− | C | A+ |

| AMICUS THERAPEUTICS | FOLD | D− | A− | C− | A+ |

| HERON THERAPEUTICS | HRTX | D− | B− | C− | A+ |

| HORIZON THRPT PB OS | HZNP | D− | C− | D+ | A- |

| IRONWOOD PHARMA CM A | IRWD | D− | A− | C | A+ |

| JAZZ PHARMA PLC | JAZZ | D− | C− | C | B− |

| JOHNSON AND JOHNS DC | JNJ | A+ | A+ | A− | D− |

| LILLY ELI CO | LLY | A− | A | C+ | B− |

| MADRIGAL PHARMA | MDGL | D− | C− | D+ | A+ |

| MALLINCKRODT PLC | MNK | C− | C | C− | D− |

| MERCK CO INC | MRK | A | A+ | B | C |

| MYLAN NV ORD SHS | MYL | B− | B− | A− | D+ |

| PRESTIGE CONSUMER HE | PBH | D− | D+ | C | A+ |

| PACIRA BIOSCIENCES | PCRX | D− | C− | C+ | A+ |

| PFIZER INC | PFE | B+ | A− | C+ | B+ |

| PERRIGO COMPANY PLC | PRGO | B+ | A− | B− | C+ |

| SAGE THERAPEUTIC COM | SAGE | C− | A+ | C | D+ |

| SUPERNUS PHARM | SUPN | D− | D | C− | A+ |

| ZOGENIX, INC. | ZGNX | D− | B− | A+ | D− |

| ZOETIS INC. | ZTS | C− | B− | B+ | A+ |

References

- Freeman, R.E. Stakeholder theory of the modern corporation. In Ethical Issues in Business: A Philosophical Approach, 8th ed.; Donaldson, T., Werhane, P., Eds.; Pearson/Prentice Hall: Upper Saddle River, NJ, USA, 2008. [Google Scholar]

- United Nations (UN). Transforming Our World: The 2030 Agenda for Sustainable Development. 2015. Available online: http://www.un.org/ga/search/view_doc.asp?symbol=A/RES/70/1&Lang=E (accessed on 6 March 2021).

- Commission of the European Communities. Communication from the Commission Concerning Corporate Social Responsibility: A Business Contribution to Sustainable Development (COM (2002) 347 Final of 2.7.2002). 2002. Available online: https://www.eea.europa.eu/policy-documents/com-2002-347-final (accessed on 6 March 2021).

- Porter, M.; Kramer, M.R. Strategy and Society: The link between competitive advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2007, 85, 139. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Hurst, G.A.; Clark, J.H. Editorial overview: Education in green and sustainable chemistry and green and sustainable pharmacy: An integrated approach. Sustain. Chem. Pharm. 2020, 16, 100272. [Google Scholar] [CrossRef]

- Min, M.; Desmoulins-Lebeault, F.; Esposito, M. Should pharmaceutical companies engage in corporate social responsibility? J. Manag. Dev. 2017, 36, 58–70. [Google Scholar] [CrossRef]

- Droppert, H.; Bennett, S. Corporate social responsibility in global health: An exploratory study of multinational pharmaceutical firms. Glob. Health 2015, 11, 15. [Google Scholar] [CrossRef]

- O’Riordan, L.; Fairbrass, J. Corporate social responsibility (CSR): Models and theories in stakeholder dialogue. J. Bus. Ethics 2008, 83, 745–758. [Google Scholar] [CrossRef]

- O’Riordan, L.; Fairbrass, J. Managing CSR stakeholder engagement: A new conceptual framework. J. Bus. Ethics 2014, 125, 121–145. [Google Scholar] [CrossRef]

- Smith, A.D. Corporate social responsibility practices in the pharmaceutical industry. Bus. Strategy Ser. 2008, 9, 306–315. [Google Scholar] [CrossRef]

- Demir, M.; Min, M. Consistencies and discrepancies in corporate social responsibility reporting in the pharmaceutical industry. Sustain. Account. Manag. Policy J. 2019, 10, 333–364. [Google Scholar] [CrossRef]

- Klatte, S.; Schaefer, H.C.; Hempel, M. Pharmaceuticals in the environment—A short review on options to minimize the exposure of humans, animals and ecosystems. Sustain. Chem. Pharm. 2017, 5, 61–66. [Google Scholar] [CrossRef]

- Hemple, M. Towards a sustainable pharmacy. Sustain. Chem. Pharm. 2017, 5, 60. [Google Scholar] [CrossRef]

- Kumar, A.; Chang, B.I.X. Human health risk assessment of pharmaceuticals in water: Issues and challenges ahead. Int. J. Environ. Res. Public Health 2010, 7, 3929–3953. [Google Scholar] [CrossRef] [PubMed]

- Triebskorn, R.; Casper, H.; Scheil, V.; Schwaiger, J. Ultrastructural effects of pharmaceuticals (carbamazepine, clofibric acid, metoprolol, diclofenac) in rainbow trout (Oncorhynchus mykiss) and common carp (Cyprinus carpio). Anal. Bioanal. Chem. 2007, 387, 1405–1416. [Google Scholar] [CrossRef]

- Chaturvedi, U.; Sharma, M.; Dangayach, G.S.; Sarkar, P. Evolution and adoption of sustainable practices in the pharmaceutical industry: An overview with an Indian perspective. J. Clean. Prod. 2017, 168, 1358–1369. [Google Scholar] [CrossRef]

- Milanesi, M.; Runfola, A.; Guercini, S. Pharmaceutical industry riding the wave of sustainability: Review and opportunities for future research. J. Clean. Prod. 2020, 261, 121204. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Cek, K.; Eyupoglu, S. Does environmental, social and governance performance influence economic performance? J. Bus. Econ. Manag. 2020, 21, 1165–1184. [Google Scholar] [CrossRef]

- Ferrero-Ferrero, I.; Fernández-Izquierdo, M.Á.; Muñoz-Torres, M.J. The effect of environmental, social and governance consistency on economic results. Sustainability 2016, 8, 1005. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Yoon, B.; Lee, J.H.; Byun, R. Does ESG performance enhance firm value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar] [CrossRef]

- Zhao, C.; Guo, Y.; Yuan, J.; Wu, M.; Li, D.; Zhou, Y. ESG and corporate financial performance: Empirical evidence from China’s listed power generation companies. Sustainability 2018, 10, 2607. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kim, Y. Country-level institutions, firm value, and the role of corporate social responsibility initiatives. J. Int. Bus. Stud. 2017, 48, 360–385. [Google Scholar] [CrossRef]

- Rodríguez-Fernández, M.; Sánchez-Teba, E.M.; López-Toro, A.A.; Borrego-Domínguez, S. Influence of ESGC indicators on financial performance of listed travel and leisure companies. Sustainability 2019, 11, 5529. [Google Scholar] [CrossRef]

- Rodríguez-Fernández, M.; Gaspar-González, A.I.; Sánchez-Teba, E.M. Sustainable social responsibility through stakeholders engagement. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2425–2436. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Sternberg, E. The defects of stakeholder theory. Corp. Gov. 1997, 5, 3–10. [Google Scholar] [CrossRef]

- Preston, L.E. Agents, stewards and stakeholder. Acad. Manag. Rev. 1998, 23, 9–13. [Google Scholar] [CrossRef]

- Jones, T.M.; Wicks, A.C. Convergent stakeholder theory. Acad. Manag. 1999, 24, 206–221. [Google Scholar] [CrossRef]

- Preston, L.E.; Donaldson, T. Stakeholder management and organizational wealth. Acad. Manag. Rev. 1999, 24, 619–625. [Google Scholar] [CrossRef]

- Pesqueux, Y.; Damak-Ayadi, S. Stakeholder theory in perspective. Int. J. Bus. Soc. 2005, 5, 5–21. [Google Scholar] [CrossRef]

- Kaufman, A.; Englander, E. Behavioral Economics, Federalism and the Triumph of Stakeholder Theory Governance ICSRaC; Palgrave Macmillan: London, UK, 2011. [Google Scholar]

- Al-Hajj, S.; Fisher, B.; Smith, J.; Pike, I. Collaborative visual analytics: A health analytics approach to injury prevention. Int. J. Environ. Res. Public Health 2017, 14, 1056. [Google Scholar] [CrossRef]

- Wang, B.; Tang, H.; Zhang, Q.; Cui, F. Exploring connections among ecosystem services supply, demand and human well-being in a mountain-basin system, China. Int. J. Environ. Res. Public Health 2020, 17, 5309. [Google Scholar] [CrossRef]

- Chen, J.; Liu, L. Eco-efficiency and private firms’ relationships with heterogeneous public stakeholders in China. Int. J. Environ. Res. Public Health 2020, 17, 6983. [Google Scholar] [CrossRef]

- Moro-Visconti, R.; Morea, D. Healthcare digitalization and pay-for-performance incentives in smart hospital project financing. Int. J. Environ. Res. Public Health 2020, 17, 2318. [Google Scholar] [CrossRef] [PubMed]

- Xie, L.; Han, H. Capacity sharing and capacity investment of environment-friendly manufacturing: Strategy selection and Performance Analysis. Int. J. Environ. Res. Public Health 2020, 17, 5790. [Google Scholar] [CrossRef] [PubMed]

- Yin, S.; Zhang, N.; Li, B. Improving the effectiveness of multi-agent cooperation for green manufacturing in China: A theoretical framework to measure the performance of green Technology innovation. Int. J. Environ. Res. Public Health 2020, 17, 3211. [Google Scholar] [CrossRef] [PubMed]

- Yang, L.; Qin, H.; Gan, Q.S. Internal control quality, enterprise environmental protection investment and finance performance: An Empirical Study of China’s A-Share heavy pollution industry. Int. J. Environ. Res. Public Health 2020, 17, 6082. [Google Scholar] [CrossRef] [PubMed]

- Carroll, A.B.; Shabana, K.M. The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Waddock, S.; Graves, S. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Callan, S.J.; Thomas, J.M. Corporate financial performance and corporate social performance: An update and reinvestigation. Corp. Soc. Responsib. Environ. Mgmt. 2009, 16, 61–78. [Google Scholar] [CrossRef]

- Berete, M. Relationship between Corporate Social Responsibility and Financial Performance in the Pharmaceutical Industry. Ph.D. Thesis, Walden University, Minneapolis, MN, USA, 2011. [Google Scholar]

- Chelawat, H.; Trivedi, I.V. The business value of ESG performance: The Indian context. Asian J. Bus. Ethics 2016, 5, 195–210. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good? A Meta-Analysis and Redirection of Research on the Relationship between Corporate Social and Financial Performance; Harvard Business School, Harvard University: Boston, MA, USA, 2007. [Google Scholar]

- Van Beurden, P. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Wood, D.J. Measuring corporate social performance: A review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Wagner, M.; Schaltegger, S. The effect of corporate environmental strategy choice and environmental performance on competitiveness and economic performance: An empirical study of EU manufacturing. Eur. Manag. J. 2004, 22, 557–572. [Google Scholar] [CrossRef]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Ambec, S.; Lanoie, P. Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. In Corporate Ethics and Corporate Governance; Zimmerli, W.C., Holzinger, M., Richter, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2007. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Pol. 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Salop, S.; Scheffman, D. Cost-Raising Strategies. J. Ind. Econ. 1987, 36, 19–34. [Google Scholar] [CrossRef]

- Hart, S. A natural-resource based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Aragon-Correa, J.A.; Sharma, S. A contingent resource-based view of proactive corporate environmental strategy. Acad. Manag. Rev. 2003, 28, 71–88. [Google Scholar] [CrossRef]

- Walley, N.; Whitehead, B. It is not easy being green. Harv. Bus. Rev. 1994, 72, 46–52. [Google Scholar]

- Graci, S.; Dodds, R. Why go green? The business case for environmental commitment in the Canadian hotel industry. Anatolia 2008, 19, 251–270. [Google Scholar] [CrossRef]

- King, A.; Lenox, M. Exploring the locus of profitable pollution reduction. Manag. Sci. 2002, 48, 289–299. [Google Scholar] [CrossRef]

- Nehrt, C. Timing and intensity effects of environmental investments. Strateg. Manag. J. 1996, 17, 535–547. [Google Scholar] [CrossRef]

- Dalal, K.K.; Thaker, N. ESG and corporate financial performance: A panel study of Indian companies. IUP J. Corp. Gov. 2019, 18, 44–59. [Google Scholar]

- Paolone, F.; Cucari, N.; Wu, J.; Tiscini, R. How do ESG pillars impact firms’ marketing performance? A configurational analysis in the pharmaceutical sector. J. Bus. Ind. Mark. 2021. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Orlitzky, M. Does firm size confound the relationship between corporate social performance and financial performance? Bus. Ethics 2001, 33, 167–180. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Admin. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good and Does It Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance; Working Paper; Harvard University: Cambridge, MA, USA, 2009. [Google Scholar]

- Servaes, H.; Tamayo, A. The Impact of corporate social responsibility on firm value: The role of customer awareness. Manag. Sci. 2013, 59, 1045–1061. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Aouadi, A.; Marsat, S. Do ESG controversies matter for firm value? Evidence from international data. J. Bus. Ethics 2018, 151, 1027–1047. [Google Scholar] [CrossRef]

- Churet, C.; Eccles, R.G. Integrated reporting, quality of management, and financial performance. J. Appl. Corp. Financ. 2014, 26, 56–64. [Google Scholar]

- Sharabati, A. Effect of corporate social responsibility on Jordan pharmaceutical industry’s business performance. Soc. Responsib. J. 2018, 14, 566–583. [Google Scholar] [CrossRef]

- Halbritter, G.; Dorfleitner, G. The wages of social responsibility—Where are they? A critical review of ESG investing. Rev. Financ. Econ. 2015, 26, 25–35. [Google Scholar] [CrossRef]

- Refinitiv. Environmental, Social and Governance (ESG) Scores from Refinitv. April 2020. Available online: https://www.esade.edu/itemsweb/biblioteca/bbdd/inbbdd/archivos/Thomson_Reuters_ESG_Scores.pdf (accessed on 20 April 2021).

- Ringle, C.M.; Wende, S.; Becker, J.M. “SmartPLS 3”. Available online: http://www.smartpls.com (accessed on 20 April 2021).

- Cepeda-Carrión, G.; Cegarra-Navarro, J.; Cillo, V. Tips to use partial least squares structural equation modelling (PLS-SEM) in knowledge management. J. Knowl. Manag. 2019, 23, 67–89. [Google Scholar] [CrossRef]

- Reinartz, W.; Haenlein, M.; Henseler, J. An empirical comparison of the efficacy of covariance-based and variance-based SEM. Int. J. Res. Mark. 2009, 26, 332–344. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. In Modern Methods for Business Research; Marcoulides, G.A.E., Ed.; Lawrence Erlbaum Associates Publisher: London, UK, 1998; pp. 295–336. [Google Scholar]

- Hair, J.F.J.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–151. [Google Scholar] [CrossRef]

- Werts, C.E.; Linn, R.L.; Jöreskog, K.G. Intraclass reability estimate: Testing structural assumption. Educ. Psychol. Meas. 1974, 34, 25–33. [Google Scholar] [CrossRef]

- Cronbach, L.J. Coefficient alpha and internal structure of test. Psychometrika 1951, 16, 297–334. [Google Scholar] [CrossRef]

- Nunnally, J.C.; Bernstein, I.H. Psychometric Theory, 3rd ed.; McGraw-Hill, Inc.: New York, NY, USA, 1994. [Google Scholar]

- Geisser, S. The predictive sample reuse method with applications. J. Am. Stat. Assoc. 1975, 70, 320–328. [Google Scholar] [CrossRef]

- Stone, M. Cross-validatory choice and assessment of statistical predictions. J. R. Stat. Soc. Ser. B (Method) 1974, 36, 111–147. [Google Scholar] [CrossRef]

- Chin, W.W. How to write and report PLS analyses. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang., H., Eds.; Springer Handbooks of Computational Statistics Series; Springer: Heidelberg, Germany; Dordrecht, The Netherlands; London, UK; New York, NY, USA, 2010; Volume 2, pp. 655–690. [Google Scholar]

- Roldán, J.L.; Sánchez-Franco, M.J. Variance-Based structural equation modeling: Guidelines for using partial least squares in information systems research. In Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems; Mora, M., Steebkamp, A.L., Gelman, O., Raisinghani, M.S., Eds.; IGI Global: Hershey, PA, USA, 2012; pp. 193–221. [Google Scholar]

- Hair, J.F.; Hult, G.T.; Ringle, C.M.; Sarstedt, M.; Castillo-Apraiz, J.; Cepeda Carrion, G.; Roldán, J.L. Manual de Partial Least Squares Structural Equation Modeling (PLS-SEM); Omnia Publisher S.L.: Barcelona, Spain, 2019. [Google Scholar]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A New Criterion for assessing discriminant validity in variance-based structural Equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences Mahwah; Lawrence Erlbaum: Mahwah, NJ, USA, 1988. [Google Scholar]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M. Common beliefs and reality about PLS: Comments on Rönkkö & Evermann. Organ. Res. Methods 2014, 17, 182–209. [Google Scholar]

- Henseler, J. Bridging design and behavioral research with variance-based structural equation modeling. J. Advert. 2017, 46, 178–192. [Google Scholar] [CrossRef]

- Omar, B.F.; Zallom, N.O. Corporate social responsibility and market value: Evidence from Jordan. J. Financ. Repor. Accoun. 2016, 14, 2–29. [Google Scholar] [CrossRef]

- Mahapatra, B.; Walia, M.; Patel, S.K.; Battala, M.; Mukherjee, S.; Patel, P. Sustaining consistent condom use among female sex workers by addressing their vulnerabilities and strengthening community-led organizations in India. PLoS ONE 2020, 15, e0235094. [Google Scholar] [CrossRef] [PubMed]

- Turcsanyi, J.; Sisaye, S. Corporate social responsibility and its link to financial performance: Application to Johnson & Johnson, a pharmaceutical company. World Rev. Sci. Technol. Sustain. Dev. 2013, 10, 4–18. [Google Scholar] [CrossRef]

- Sanches-Garcia, A.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Sassen, R.; Hinze, A.K.; Hardeck, I. Impact of ESG factors on firm risk in Europe. J. Bus. Econ. 2016, 86, 867–904. [Google Scholar] [CrossRef]

- Hong, H.; Kacperczyk, M. The price of sin: The effects of social norms on markets. J. Financ. Econ. 2009, 93, 15–36. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A study of environmental disclosure practices of Australian corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Richardson, A.J.; Welker, M. Social disclosure, financial disclosure and the cost of equity capital. Account. Organ. Soc. 2001, 26, 597–616. [Google Scholar] [CrossRef]

- Mendes-Da-Silva, W.; Onusic, L.M.; Bergmann, D.R. The influence of e-disclosure on the ex-ante cost of capital of listed companies in Brazil. J. Emerg. Mark. Financ. 2014, 13, 1–31. [Google Scholar] [CrossRef]

- Andersen, M.L.; Dejoy, J.S. Corporate Social and Financial Performance: The role of size, industry, risk, R&D and advertising expenses as control variables. Bus. Soc. Rev. 2011, 116, 237–256. [Google Scholar] [CrossRef]

- Baron, D.P. Private politics, corporate social responsibility, and integrated strategy. J. Econ. Manag. Strateg. 2001, 10, 7–45. [Google Scholar] [CrossRef]

- Hillman, A.M.; Keim, G.D. Shareholder value, stockholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Siew, R.Y.; Balatbat, M.C.; Carmichael, D.G. The relationship between sustainability practices and financial performance of construction companies. Smart Sustain. Built Environ. 2013, 2, 6–27. [Google Scholar] [CrossRef]

| Indicators | No. | Missing | Mean | Median | Min. | Max. | Standard Deviation | Excess Kurtosis | Skewness |

|---|---|---|---|---|---|---|---|---|---|

| P1ENV | 1 | 0 | 0.343 | 0.29 | 0.04 | 0.96 | 0.317 | −1.322 | 0.499 |

| P2GOV | 2 | 0 | 0.54 | 0.54 | 0.04 | 0.96 | 0.276 | −1.283 | 0.024 |

| P3SOC | 3 | 0 | 0.481 | 0.46 | 0.21 | 0.87 | 0.208 | −1.099 | 0.26 |

| P4CONT | 4 | 0 | 0.344 | 0.21 | 0.04 | 0.96 | 0.333 | −1.332 | 0.526 |

| ROA19 | 5 | 0 | −7.754 | 1.31 | −58.36 | 13.68 | 23.095 | 0.182 | −1.254 |

| ROE19 | 6 | 0 | −23.043 | 2.55 | −332.94 | 74.59 | 84.323 | 6.693 | −2.359 |

| TOBIN19 | 7 | 0 | 5.223 | 3.94 | 0.46 | 18.77 | 4.294 | 3.782 | 1.934 |

| Indicators/ | Loadings > 0.7 | |||

|---|---|---|---|---|

| Construct | ESG | CA > 0.7 | CR > 0.7 | AVE > 0.5 |

| ESG | 0.818 | 0.911 | 0.880 | |

| P1ENV | 0.935 | |||

| P2GOV | 0.699 | |||

| P3SOC | 0.880 | |||

| P4CONT | 1 | 1 | 1 | |

| ROA19 | 1 | 1 | 1 | |

| ROE19 | 1 | 1 | 1 | |

| TOBIN19 | 1 | 1 | 1 |

| Indicator/Construct | 1. CONT | 2. ESG | 3. ROA19 | 4. ROE19 | 5. TOBIN19 |

|---|---|---|---|---|---|

| 1 | 0.710 | 0.438 | 0.262 | 0.265 |

| −0.696 | 0.844 | 0.483 | 0.410 | 0.129 |

| −0.438 | 0.531 | 1 | 0.851 | 0.094 |

| −0.262 | 0.436 | 0.851 | 1 | 0.006 |

| 0.265 | 0.065 | −0.094 | 0.006 | 1 |

| Indicator or Construct | R2 | R2 Adjusted | Q2 | f2 | VIF(<3.3) | |||

|---|---|---|---|---|---|---|---|---|

| CONT | ESG | 3 | 4 | 5 | ||||

| 1.942 | 1.942 | 1.942 | |||||

| 1.942 | 1.942 | 1.942 | |||||

| 0.291 | 0.227 | 0.238 | 0.013 | 0.140 | |||

| 0.193 | 0.120 | 0.117 | 0.004 | 0.155 | |||

| 0.191 | 0.117 | 0.112 | 0.231 | 0.149 | |||

| Hyp | Paths | Beta Path β | f2 | Signif | t-Statistics | p‑Value | Supported/Rejected |

|---|---|---|---|---|---|---|---|

| H1 | CONT -> ROA19 | −0.133 | 0.013 | NS | 0.644 | 0.260 | H1 rejected |

| H2 | CONT -> ROE19 | 0.081 | 0.004 | NS | 0.353 | 0.362 | H2 rejected |

| H3 | CONT -> TOBIN19 | 0.602 | 0.231 | ** | 2.634 | 0.004 | H3 supported |

| H4 | ESG -> ROA19 | 0.439 | 0.140 | ** | 2.070 | 0.019 | H4 supported |

| H5 | ESG -> ROE19 | 0.492 | 0.155 | ** | 2.582 | 0.005 | H5 supported |

| H6 | ESG -> TOBIN19 | 0.484 | 0.149 | ** | 1.651 | 0.049 | H6 supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

López-Toro, A.A.; Sánchez-Teba, E.M.; Benítez-Márquez, M.D.; Rodríguez-Fernández, M. Influence of ESGC Indicators on Financial Performance of Listed Pharmaceutical Companies. Int. J. Environ. Res. Public Health 2021, 18, 4556. https://doi.org/10.3390/ijerph18094556

López-Toro AA, Sánchez-Teba EM, Benítez-Márquez MD, Rodríguez-Fernández M. Influence of ESGC Indicators on Financial Performance of Listed Pharmaceutical Companies. International Journal of Environmental Research and Public Health. 2021; 18(9):4556. https://doi.org/10.3390/ijerph18094556

Chicago/Turabian StyleLópez-Toro, Alberto A., Eva María Sánchez-Teba, María Dolores Benítez-Márquez, and Mercedes Rodríguez-Fernández. 2021. "Influence of ESGC Indicators on Financial Performance of Listed Pharmaceutical Companies" International Journal of Environmental Research and Public Health 18, no. 9: 4556. https://doi.org/10.3390/ijerph18094556

APA StyleLópez-Toro, A. A., Sánchez-Teba, E. M., Benítez-Márquez, M. D., & Rodríguez-Fernández, M. (2021). Influence of ESGC Indicators on Financial Performance of Listed Pharmaceutical Companies. International Journal of Environmental Research and Public Health, 18(9), 4556. https://doi.org/10.3390/ijerph18094556