The Evolution Characteristics and Influence Mechanism of Chinese Venture Capital Spatial Agglomeration

Abstract

1. Introduction

2. Materials and Methods

2.1. Data Source and Processing

2.2. Research Method

2.2.1. Gini Coefficient

2.2.2. Concentration Coefficient

2.2.3. Location Quotient

2.2.4. Spatial Econometric Model

Spatial Autocorrelation Test

Spatial Durbin Model

2.2.5. Research Hypothesis

2.2.6. Index Selection

Dependent Variable

Explaining Variable

3. Spatial and Temporal Pattern and Agglomeration Characteristics of Venture Capital

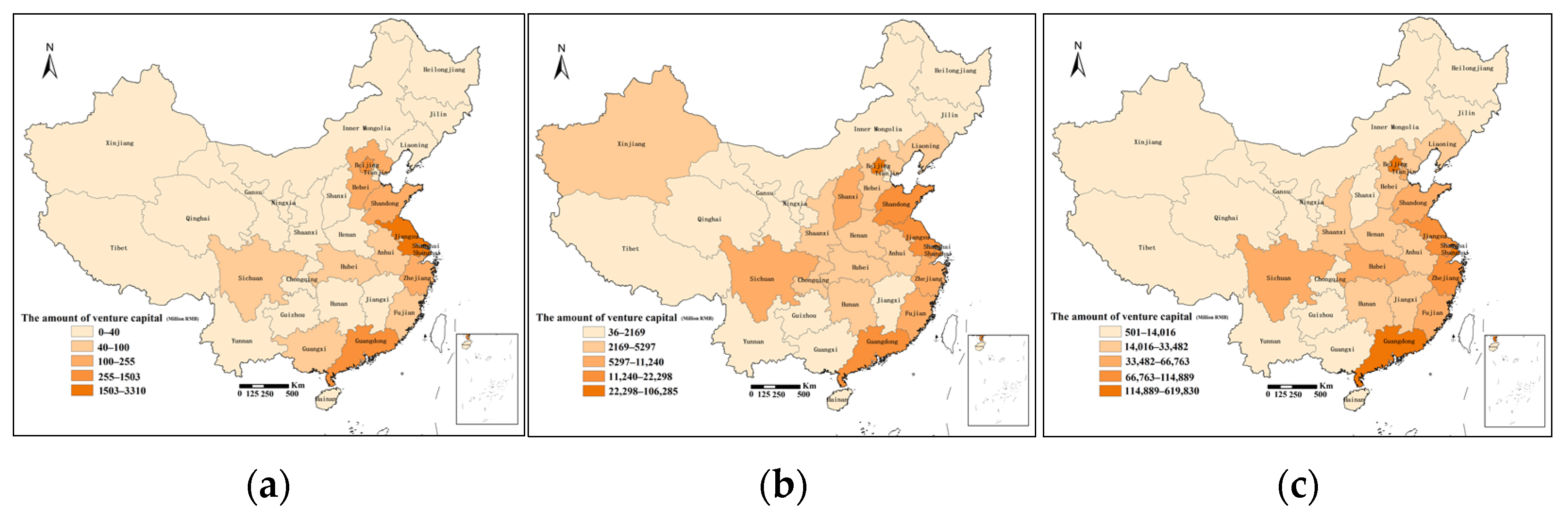

3.1. Changes in Spatial Agglomeration Pattern

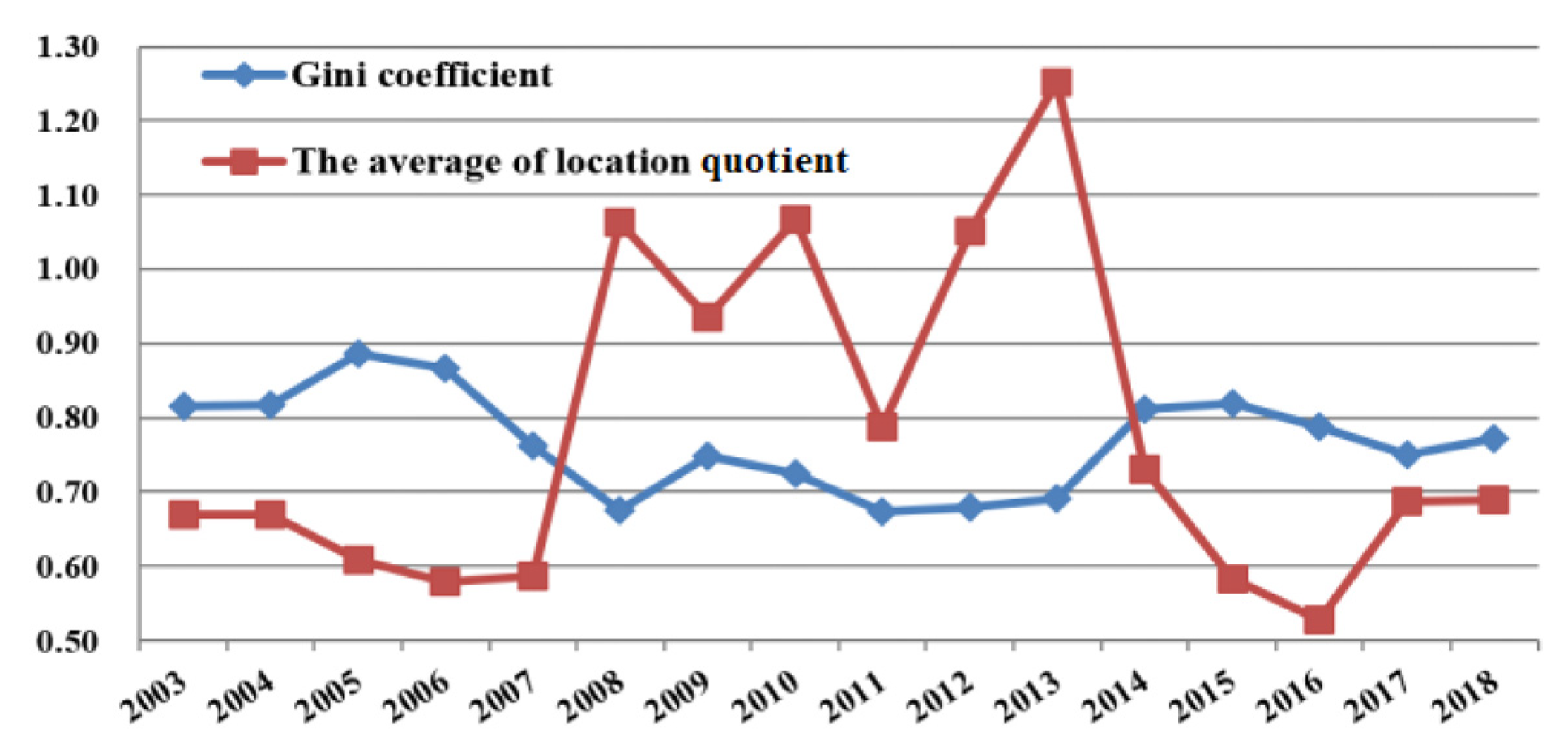

3.2. Changes in the Degree of Spatial Agglomeration

- By analyzing the changes of venture capital investment scale gini coefficient, the study has shown that the agglomeration level of venture capital investment scale reached the maximum in 2005 (the gini coefficient value of 2005 was 0.886). It indicates that the spatial distribution of venture capital investment in China was unbalanced, the regional distribution gap was large, and the agglomeration trend was obvious. Subsequently, the agglomeration level decreased gradually until 2012 (the gini coefficient value of 2012 was 0.674). However, after 2013, the gini coefficient level gradually increased, which proved that the agglomeration imbalance of venture capital investment began to increase after 2013. (as shown in Figure 2).

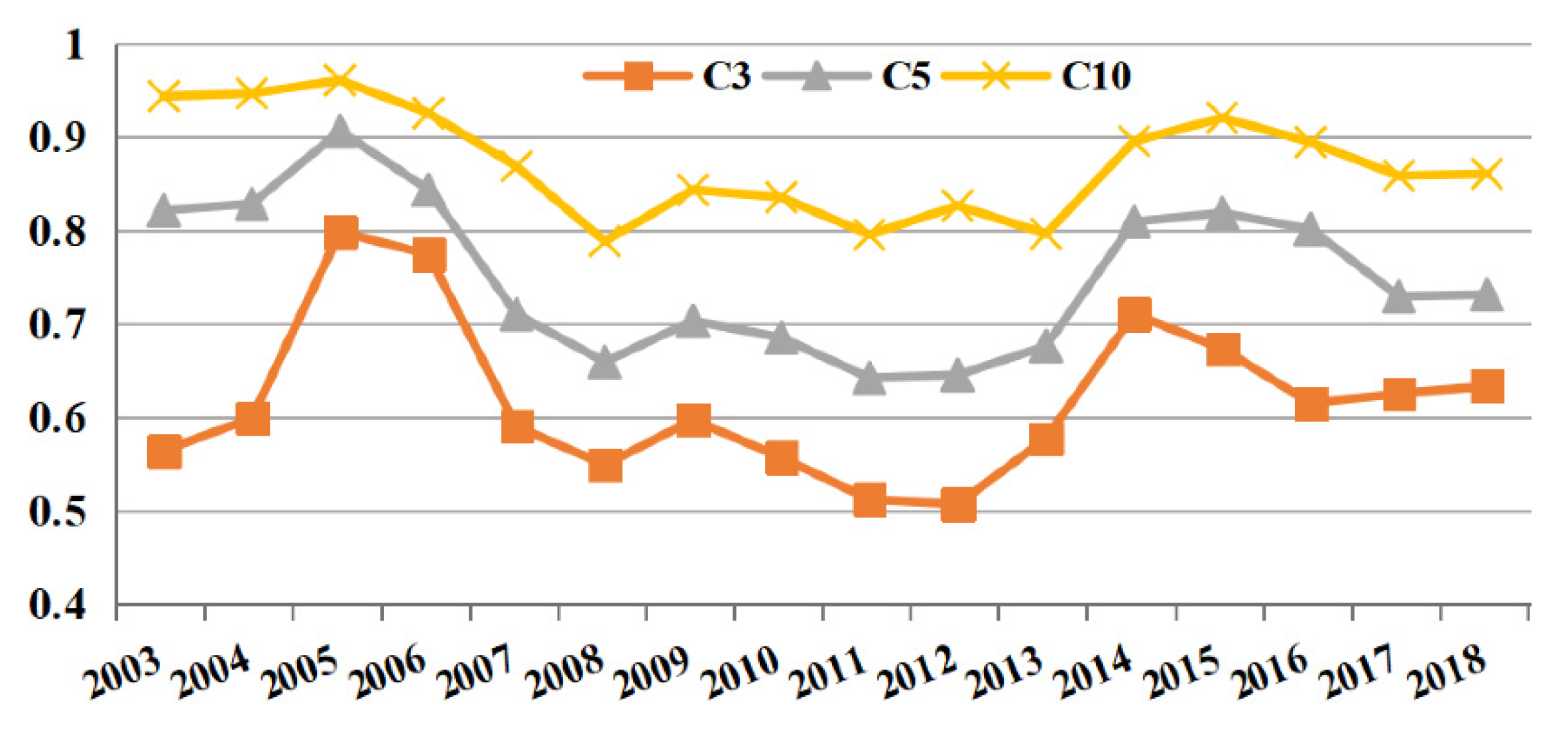

- The calculation results showed that the concentration coefficient of China’s venture capital was relatively high. As shown in the Formula (2) of concentration coefficient, Cn measures the proportion of the top n provinces with the largest venture capital amount. Referring to previous research experience, n is generally taken as 3, 5, and 10. The concentration coefficient of the top three regions with the largest venture capital amount increased from 0.564 to 0.633 during the period from 2003 to 2018, while the concentration coefficient of the top five and top 10 regions with the largest venture capital amount decreased from 0.821 and 0.943 to 0.731 and 0.860 during the period from 2003 to 2018. From the perspective of time dimension, the concentration coefficients of the top 3, 5 and 10 regions with the largest proportion of venture capital amount all showed an upward trend first, then a downward trend. It indicates that the concentration degree of venture capital gradually weakened at first and gradually increased after 2013. (as shown in Figure 3).

- Through the calculation of location quotient coefficient of the provinces, we found that the areas of high location quotient index were mainly concentrated in Beijing, Shanghai, Guangdong, and other regions. From 2008 to 2013, there were more areas with quotient coefficient greater than 1. It was proved that the level of some regions with high degree of venture capital agglomeration (Beijing, Shanghai, Guangzhou, etc.) decreased, while the location quotient coefficient of some other provinces increased correspondingly. This led to the sudden changes of this coefficient from 2008 to 2013. It is also proved that at this stage, the degree of concentration of venture capital in China decreased. However, the number of regions where the location quotient coefficient of venture capital was greater than 1 decreased after 2013, which proved that the uneven distribution of venture capital in China was further enhanced. Similarly, the average location quotient of the whole country also presented the same changing trend. (as shown in Figure 2).

4. Empirical Analysis

4.1. Model Setup

4.2. Results Analysis

4.2.1. Spatial Econometric Model Regression Results for National Samples

4.2.2. Regression Results of Different Time Periods

4.2.3. Regression Results of Eastern, Central and Western Region Samples

5. Conclusions and Implications

5.1. Conclusions

- From the perspective of provincial scale, both venture capital institutions and venture capital projects showed significant agglomeration characteristics, which were very similar in spatial form, mainly concentrated in the first-tier cities and the eastern coastal areas. It shows that venture capital had local investment preference. At the same time, the phenomenon of spatial agglomeration of venture capital in China had spatial autocorrelation in section units, which forms strong spatial dependence and positive spatial spillover effect among provinces. This positive spatial spillover effect indicates that the development of venture capital in neighboring provinces can promote the improvement of venture capital in the region.

- By constructing a spatial econometric model based on three different spatial weight matrices, it was found that there was a strong spatial dependence and positive spillover effects of space in venture capital agglomeration between the provinces in China. Considering the goodness of fit and logarithmic likelihood, the estimation effect of SDM based on economic distance was better than that of other models. The spatial distribution pattern of venture capital was mainly influenced by factors of economic environment, science and technology environment, financial environment, social environment, and entrepreneurial environment. First, economic environment is the most important factor affecting the spatial agglomeration of venture capital. Secondly, scientific and technological environmental factor had a positive effect on the spatial clustering of venture capital, and most of them passed the significance test. Thirdly, financial environment factor had a weak correlation and positive effect on the spatial agglomeration of venture capital. At the same time, the development of regional venture capital requires a high level of facilities and services to match, so as to ensure the level of industry standardization and maturity of the whole market. In the end, the two indexes selected for entrepreneurial environment were positive and negative, with a high level of significance.

- Due to the degree of spatial agglomeration, venture capital can be divided into three stages in terms of time. Combined with the three indicators of Gini coefficient, location quotient index, and concentration coefficient, we can divide the period of research time into three stages: (1) from 2003 to 2007, (2) from 2008 to 2012, (3) from 2013 to 2018, the degree of spatial agglomeration of venture capital experienced a short rise, then a significant decline, and then a gradual increase. It can be found that the factors affecting spatial agglomeration of venture capital changed significantly with the passage of time.

- According to the economic development level and geographical position of each province, the study area was divided into three regions: eastern region, central region, and western region. From the regression results of eastern, central, and western region samples, we can see that the degree of spillover effect was the lowest in the central region, the highest in the western region, and the middle in the eastern region.

5.2. Implications

- (1)

- Firstly, this paper proposes to strengthen regional venture capital cooperation between neighboring provinces and regions, promote the free flow of venture capital between regions, so as to promote the optimal allocation of venture capital in a larger scope and promote the integration of the financial market.

- (2)

- Secondly, the development of venture capital requires relevant economic environment and supporting industries, such as law firms, accounting firms, evaluation institutions, research institutions, etc. These institutions serve many venture capital funds and can better play to their professional advantages. At the same time, under the condition of insufficient overall scale, some regions are encouraged to guide the development of venture capital in policy. The support of venture capital should be focused on a region, and the development of a high-quality venture capital cluster should be cultivated. The government should support the development of the venture capital industry and cultivate high-quality venture capital clusters in different regions.

- (3)

- Scientific and technological innovation ability, financial development, communication and network development, social services, and entrepreneurial activity level are the external environment of venture capital in the cluster area of venture capital. Therefore, the government should play a greater role in creating an institutional environment for the development of venture capital. The government can promote the development strategy and create a cultural and social atmosphere that encourages enterprises to innovate in science and technology. Only by advocating technological innovation as the core of competition, encouraging enterprise innovation and industrial cooperation, and ensuring the activity of competitive market, can the positive spillover effect of venture capital be brought into full play. By guiding the spillover mechanism of venture capital agglomeration, it can promote the driving effect of regional economic development and industrial transformation and upgrading.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Li, Z.; Xu, M.; He, C.; Pan, F. Review and prospects on financial geography. Econ. Geogr. 2018, 38, 7–15. [Google Scholar]

- Liu, G.; Liu, Y.P. Study on the effect of venture capital on the industrial transformation and upgrading. Ind. Econ. Rev. 2019, 10, 45–55. [Google Scholar]

- Xue, C.; Dang, X.; Shi, B.; Gu, J. Information Sharing and Investment Performance in the Venture Capital Network Community: An Empirical Study of Environmental-Social-Governance Start-Ups. Int. J. Environ. Res. Public Health 2019, 16, 1023. [Google Scholar] [CrossRef]

- Florida, R.; Smith, M. Venture capital, high technology and regional development. Reg. Stud. 1988, 22, 33–48. [Google Scholar] [CrossRef]

- Florida, R.; Smith, D. Venture capital formation, investment and regional industrialization. Ann. Assoc. Am. 1993, 83, 434–451. [Google Scholar] [CrossRef]

- Thompson, C. The geography of venture capital. Prog. Hum. Geogr. 1989, 13, 62–98. [Google Scholar] [CrossRef]

- Cai, L.; Zhu, X.; Sun, K. Cluster analysis of area distribution of venture capitals in China. Chin. J. Manag. 2004, 1, 195–198. [Google Scholar]

- He, C.; Guo, Q.; Ma, Y.; Fan, S.; Zhao, Y. Progress of economic geography in the West: A literature review. Acta Geogr. Sin. 2014, 69, 1207–1223. [Google Scholar]

- Wang, M.; Wei, Y.; Qiu, J. Spatial agglomeration and urban network of venture capital investment in China. J. Financ. Econ. 2014, 40, 117–131. [Google Scholar]

- Xu, Y.; Pan, F.; Jiang, X.; Qu, Y.; Liang, J. The geography and syndication investment networks of venture capital in Beijing. Prog. Geogr. 2016, 35, 358–367. [Google Scholar]

- Zook, M.A. Grounded Capital: Venture Financing and the Geography of the Internet Industry, 1994–2000. J. Econ. Geogr. 2002, 2, 151–177. [Google Scholar] [CrossRef]

- Samila, S.; Sorenson, O. Venture capital, entrepreneurship and economic growth. Rev. Econ. Stat. 2011, 93, 338–349. [Google Scholar] [CrossRef]

- Long, Y.; Zhao, H.; Zhang, X.; Li, Y. High-speed railway and venture capital investment. Econ. Res. J. 2017, 52, 195–208. [Google Scholar]

- Gompers, P.; Lerner, J. What drives venture capital fundraising? Natl. Bur. Econ. Res. Work. Pap. 1999. [Google Scholar] [CrossRef]

- Bernard, G.; Sandra, M. The dynamics of venture capital industry. Int. J. Technol. Manag. 1999, 34, 146–160. [Google Scholar]

- Chahine, S.; Arthursj, D.; Filatotchevi, I. The effects of venture capital syndicate diversity on earnings management and performance of IPOs in the US and UK: An institutional perspective. J. Corp. Financ. 2012, 18, 179–192. [Google Scholar] [CrossRef]

- Chen, D.; Chen, X. The evolution of venture capital spatial layout and its driving factors. Rev. Invest. Stud. 2015, 34, 4–15. [Google Scholar]

- French, K.; Poterba, J. Investor diversification and international equity markets. Am. Econ. Rev. 1991, 81, 222–226. [Google Scholar]

- Coval, J.; Moskowitz, T.T. Home bias at home: Local equity preference in domestic portfolios. J. Financ. 1999, 54, 2045–2073. [Google Scholar] [CrossRef]

- Martin, R.; Christian, B.; Britta, K. Spatial proximity effects and regional equity gaps in the venture capital market evidence from Germany and the United Kingdom. Environ. Plan. A 2005, 37, 1207–1231. [Google Scholar] [CrossRef]

- She, J.; Tang, B. Study on formation mechanism of regional imbalance in venture capital development. Sci. Sci. Manag. S. T. 2007, 28, 112–115. [Google Scholar]

- Zhao, X.B.; Wang, T.; Zhang, J.X. Information flow and asymmetric information as key determinants for service and financial centre development: A case on socialist china. Econ. Geo. 2002, 22, 408–414. [Google Scholar]

- Kolympiris, C.; Kalaitzandonakes, N.; Miller, D. Spatial collocation and venture capital in the US biotechnology industry. Res. Policy 2011, 40, 1188–1199. [Google Scholar] [CrossRef]

- Fritsch, M.; Schilder, D. The regional supply of venture capital: Can syndication overcome bottlenecks? Econ. Geogr. 2012, 88, 59–76. [Google Scholar] [CrossRef]

- Stuart, T.; Sorenson, O. The geography of opportunity: Spatial heterogeneity in founding rates and the performance of biotechnology firms. Res. Policy 2003, 32, 229–253. [Google Scholar] [CrossRef]

- Fang, J.; Liu, H. How and why venture capital flows in the Beijing-Tianjin-Hebei Urban Agglomeration. Prog. Geogr. 2017, 36, 68–77. [Google Scholar]

- Zhao, J.; Sun, T.; Li, G. Agglomeration and firm location choice of China’s automobile manufacturing industry. Acta Geogr. Sin. 2014, 69, 850–862. [Google Scholar] [CrossRef]

- Haggett, P. Locational Analysis in Human Geography; Edward Arnold: London, UK, 1977. [Google Scholar]

- Tan, S.; Rao, Y.; Zhu, X. 2012. Study on the Influence of Land Investment on Regional Economic Growth. China Popul. Resour. Environ. 1965, 22, 61–67. [Google Scholar]

- Anselin, L. Spatial Econometrics: Methods and Models; Kluwer Academic Publishers: Dordrecht, The Netherlands, 1988. [Google Scholar]

- Mourao, P.R. ‘Keeping up with the (Portuguese) Joneses’—A study on the spatial dependence of municipal expenditure. Appl. Econ. 2019, 51, 3689–3709. [Google Scholar] [CrossRef]

- Levratto, N. Does Firm Creation Depend on Local Context? A Focus on the Neighbouring Effect. Working Papers 40, Réseau de Recherche sur l’Innovation./Research Network on Innovation. 2014. Available online: https://ideas.repec.org/p/rii/rridoc/40.html (accessed on 27 December 2020).

- Wang, S.; Yuan, Y.; Wang, H. Corruption, Hidden Economy and Environmental Pollution: A Spatial Econometric Analysis Based on China’s Provincial Panel Data. Int. J. Environ. Res. Public Health 2019, 16, 2871. [Google Scholar] [CrossRef]

- Ren, Y.; Xu, L.; You, W. A spatial econometric model and its application on the factors of financial industry agglomeration. J. Quant. Tech. Econ. 2010, 27, 104–115. [Google Scholar]

- Long, X.; Zhu, Y.; Cai, W.; Li, S. An empirical analysis of spatial tax competition among Chinese counties based on spatial econometric models. Econ. Res. J. 2014, 49, 41–53. [Google Scholar]

- Wang, J.; Gu, G.; Yao, L. Urbanization, spatial spillover effects and urban-rural income gap in China: Based on provincial panel data from 2002 to 2012. J. Financ. Econ. 2015, 41, 55–66. [Google Scholar]

- Yao, L. Venture capital, regional technological innovation and spatial spill over effects: An empirical research based on the spatial panel data from 31 provinces in China. Contemp. Econ. Manag. 2018, 40, 7–12. [Google Scholar]

- Anselin, L. The Econometrics of Panel Data; Springer: Berlin, Germany, 2008. [Google Scholar]

- LaSage, J.; Pace, R. Introduction to Spatial Econometrics, Statistics: Textbooks and Monographs; CRC Press: Boca Raton, FL, USA, 2009. [Google Scholar]

- Audretsch, D.; Acs, Z. New-firm Startups, Technology, and Macroeconomic Fluctuations. Small Bus. Econ. 1994, 6, 439–449. [Google Scholar] [CrossRef]

- Shachmurove, Y. A historical overview of financial crises in the United States. Glob. Financ. J. 2001, 22, 217–231. [Google Scholar] [CrossRef]

- Kortum, S.; Lerner, J. Assessing the Contribution of Venture Capital to Innovation. Rand J. Econ. 2000, 31, 674–692. [Google Scholar] [CrossRef]

- Hirukawa, M.; Ueda, M. Venture Capital and Innovation: Which is First? Pac. Econ. Rev. 2011, 16, 421–465. [Google Scholar] [CrossRef]

- Gompers, P.; Kovner, A.; Lerner, J.; Scharfstein, D. Venture capital investment cycles: The impact of public markets. J. Financ. Econ. 2008, 87, 1–23. [Google Scholar] [CrossRef]

- Sorenson, O.; Stuart, T. Syndication Networks and the Spatial Distribution of Venture Capital Investments. Am. J. Sociol. 2001, 6, 1546–1588. [Google Scholar] [CrossRef]

- Yang, R.; Chen, K.; Zhu, S. The Credit Behavior of Rural Households from the Perspective of Social Network. Econ. Res. J. 2011, 11, 116–129. [Google Scholar]

- Groh, A.; Lieser, K. The European Venture Capital and Private Equity Country Attractiveness Indices. J. Corp. Financ. 2010, 16, 205–224. [Google Scholar] [CrossRef]

- Galbraith, J.K. The affluent society. Read edition. In The Affluent Society, 40th ed.; Galbraith, J.K., Ed.; Houghton Mifflin Company: New York, NY, USA, 1998. [Google Scholar]

- Mourao, P.R. What is China seeking from Africa? An analysis of the economic and political determinants of Chinese Outward Foreign Direct Investment based on Stochastic Frontier Models. China Econ. Rev. 2017, 48, 258–268. [Google Scholar] [CrossRef]

- Wong, Y.; Gao, Y. The Index System Study on Scientific and Technological Innovation Environment. Forum Sci. Technol. China 2009, 2, 31–35. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Name of the Variable | Description of Variable | Specific Indicators | |

|---|---|---|---|

| Dependent Variable | Degree of concentration of venture capital | Location quotient index of venture capital (LQVC) | |

| Explaining Variable | Factor of economic environment | Economic development level | Regional per capita GDP (Eco) |

| Factor of science and technology environment | Scientific and technological innovation ability level | Number of patents (including invention patents, designs and utility models) (Tec) | |

| Factor of financial environment | Financial development level | Total deposits and loans of financial institutions at the end of the year (ten thousand RMB) (Fin) | |

| Factor of social environment | Communication and network development level | Regional per capita transportation and communication expenses (RMB/person) (Com) | |

| Social services level | Proportion of tertiary industry (%) (Ser) | ||

| Factor of entrepreneurial environment | Entrepreneurial activity level | The number of private companies owned by people aged 15–60 in the region (Ent) | |

| Labor market rigidity level | The proportion of state-owned employment in the region (%) (Lab) |

| Year | Gini Coefficient | C3 | C5 | C10 | Location Quotient | |

|---|---|---|---|---|---|---|

| The Number of Provinces (E > 1) | The Average of Location Quotient | |||||

| 2003 | 0.816 | 0.564 | 0.821 | 0.943 | 5 | 0.675 |

| 2004 | 0.816 | 0.599 | 0.828 | 0.946 | 5 | 0.669 |

| 2005 | 0.886 | 0.798 | 0.906 | 0.960 | 4 | 0.609 |

| 2006 | 0.867 | 0.774 | 0.843 | 0.925 | 3 | 0.579 |

| 2007 | 0.763 | 0.590 | 0.710 | 0.868 | 6 | 0.587 |

| 2008 | 0.676 | 0.549 | 0.659 | 0.788 | 11 | 1.063 |

| 2009 | 0.748 | 0.597 | 0.703 | 0.843 | 7 | 0.935 |

| 2010 | 0.724 | 0.557 | 0.685 | 0.835 | 8 | 1.068 |

| 2011 | 0.674 | 0.512 | 0.642 | 0.795 | 8 | 0.787 |

| 2012 | 0.679 | 0.507 | 0.645 | 0.826 | 8 | 1.051 |

| 2013 | 0.691 | 0.577 | 0.676 | 0.796 | 10 | 1.252 |

| 2014 | 0.811 | 0.710 | 0.809 | 0.895 | 3 | 0.730 |

| 2015 | 0.819 | 0.673 | 0.818 | 0.920 | 5 | 0.583 |

| 2016 | 0.788 | 0.615 | 0.801 | 0.894 | 5 | 0.527 |

| 2017 | 0.751 | 0.625 | 0.729 | 0.858 | 5 | 0.687 |

| 2018 | 0.772 | 0.633 | 0.731 | 0.860 | 6 | 0.690 |

| Year | Moran’s I | Z Statistic | Year | Moran’s I | Z Statistic |

|---|---|---|---|---|---|

| 2003 | 0.311 | 3.502 | 2011 | 0.298 | 3.652 |

| 2004 | 0.348 | 3.437 | 2012 | 0.453 | 4.355 |

| 2005 | 0.293 | 3.843 | 2013 | 0.248 | 2.973 |

| 2006 | 0.069 | 1.919 | 2014 | 0.190 | 2.854 |

| 2007 | 0.284 | 3.664 | 2015 | 0.337 | 3.738 |

| 2008 | 0.255 | 3.377 | 2016 | 0.383 | 4.364 |

| 2009 | 0.234 | 3.656 | 2017 | 0.250 | 3.005 |

| 2010 | 0.220 | 3.325 | 2018 | 0.310 | 3.871 |

| Variables | OLS | SDM | ||

|---|---|---|---|---|

| Adjacent Matrix | Geographical Distance Matrix | Economic Distance Matrix | ||

| Eco | 1.152 *** | 1.257 *** | 1.319 *** | 1.341 *** |

| (5.822) | (5.693) | (6.133) | (5.413) | |

| Tec | 0.302 ** | 0.304 ** | 0. 305 ** | 0.310 ** |

| (2.034) | (2.126) | (2.143) | (2.596) | |

| Fin | 0.080 *** | 0.046 * | 0.046 ** | 0.043 *** |

| (4.531) | (2.405) | (2.501) | (2.714) | |

| Com | 0.301 ** | 0.304 ** | 0.324 ** | 0.352 ** |

| (2.362) | (2.021) | (2.837) | (2.722) | |

| Ent | 0.213 ** | 0.387 ** | 0.337 ** | 0.690 *** |

| (2.260) | (2.299) | (2.324) | (4.135) | |

| Ser | 1.009 ** | 1.771 *** | 1.484 *** | 1.980 *** |

| (2.801) | (4.374) | (3.205) | (5.099) | |

| Lab | −0.050 * | −0.063 * | −0.068 * | −0.088 * |

| (−1.460) | (−1.575) | (−1.054) | (−1.247) | |

| W × Eco | 0.337 | 0.428 * | 0.481 ** | |

| (0.861) | (1.253) | (2.057) | ||

| W × Tec | 0.554 ** | 0.595 * | 0.590 * | |

| (2.473) | (1.741) | (1.587) | ||

| W × Fin | −0.504 * | −1.083 | −1.373 * | |

| (−1.396) | (−0.816) | (−1.725) | ||

| W × Com | −0.228 | −1.150 | 1.114 * | |

| (−0.481) | (−1.088) | (1.278) | ||

| W × Ent | −0.336 | −0.632 | −0.011 | |

| (−1.079) | (−0.537) | (−0.021) | ||

| W × Ser | 0.511 | −3.806 * | −3.361 ** | |

| (0.525) | (−1.086) | (−2.727) | ||

| W × Lab | −0.116 | −0.401 | −0.351 * | |

| (−0.824) | (−0.644) | (−1.153) | ||

| ρ | 0.199 ** | 0.201 ** | 0.210 ** | |

| (2.085) | (2.101) | (2.292) | ||

| Adj-squared | 0.645 | 0.678 | 0.680 | 0.681 |

| Log-L | 225.81 | −583.369 | −581.796 | −581.408 |

| Variables | Adjacent Matrix | Geographical Distance Matrix | Economic Distance Matrix | |||

|---|---|---|---|---|---|---|

| Direct Effect Coefficient | Indirect Effect Coefficient | Direct Effect Coefficient | Indirect Effect Coefficient | Direct Effect Coefficient | Indirect Effect Coefficient | |

| Eco | 1.271 *** | 0.125 * | 1.350 *** | 0.225 ** | 1.329 *** | 0.320 ** |

| (5.874) | (1.339) | (5.517) | (2.155) | (5.173) | (2.906) | |

| Tec | 0.131 ** | 0.015 | 0.308 ** | 0.019 | 0.351 * | 0.022 |

| (2.354) | (0.122) | (2.011) | (0.147) | (1.301) | (0.671) | |

| Fin | 0.046 ** | 0.105 ** | 0.046 ** | 0.114 * | 0.045 *** | 0.106 ** |

| (2.409) | (2.541) | (2.449) | (1.674) | (4.275) | (2.192) | |

| Com | 0.108 * | −0.001 | 0.105 ** | 0.014 | 0.116 ** | 0.011 |

| (2.418) | (−0.039) | (2.206) | (0.026) | (2.504) | (0.322) | |

| Ent | 0.386 ** | 0.004 | 0.266 * | 0.078 | 0.692 *** | 0.066 * |

| (2.262) | (0.142) | (1.472) | (0.307) | (4.170) | (1.901) | |

| Ser | 1.769 *** | 0.717 ** | 1.529 *** | 0.788 ** | 2.017 *** | 0.995 ** |

| (4.225) | (2.137) | (3.301) | (2.208) | (5.334) | (2.904) | |

| Lab | −0.061 * | −0.001 | −0.073 | −0.019 | −0.086 * | −0.008 |

| (−1.639) | (−0.053) | (−1.008) | (−0.135) | (−1.206) | (−0.610) | |

| Variables | 2003–2007 | 2008–2012 | 2013–2018 | |||

|---|---|---|---|---|---|---|

| Coefficient | Coefficient (W × Variable) | Coefficient | Coefficient (W × Variable) | Coefficient | Coefficient (W × Variable) | |

| Eco | 1.294 *** | 0.648 ** | 0.625 | 0.989 ** | 1.952 *** | −0.680 |

| (4.189) | (1.809) | (1.355) | (2.686) | (4.184) | (−0.638) | |

| Tec | 0.225 * | −1.701 ** | 0.124 * | 2.040 *** | 0.311 *** | 1.008** |

| (1.877) | (−1.713) | (1.767) | (3.515) | (2.578) | (2.201) | |

| Fin | 0.027 ** | −2.434 * | 0.009 ** | −2.005 | 0.096 ** | −0.440 |

| (2.669) | (−1.410) | (2.253) | (−1.448) | (2.424) | (−0.516) | |

| Com | 0.007 ** | 1.322 * | 0.033 ** | 2.017 * | 0.033 ** | 1.059 * |

| (−2.013) | (1.602) | (2.092) | (1.499) | (2.102) | (1.856) | |

| Ent | 1.409 *** | 3.911 ** | 0.416 * | −1.549 * | 0.539 *** | −0.969 * |

| (3.541) | (2.503) | (1.436) | (−1.714) | (3.339) | (−1.725) | |

| Ser | 2.068 ** | 0.319 | 1.318 ** | −7.187 *** | 2.599 *** | −4.933 *** |

| (2.141) | (0.106) | (2.308) | (−3.331) | (5.586) | (−2.785) | |

| Lab | −0.845 * | 3.115 | −0.602 * | −2.162 * | −0.030 * | −0.112 |

| (−1.963) | (0.863) | (−1.388) | (−1.316) | (−1.586) | (−0.475) | |

| ρ | 0.247 ** | 0.134 * | 0.287 *** | |||

| (2.326) | (1.918) | (3.604) | ||||

| observation | 155 | 155 | 186 | |||

| Log-likelihood | −234.070 | −180.523 | −149.888 | |||

| Adj-Squared | 0.662 | 0.687 | 0.827 | |||

| Variables | East Region | Central Region | West Region | |||

|---|---|---|---|---|---|---|

| Coefficient | Coefficient (W × Variable) | Coefficient | Coefficient (W × Variable) | Coefficient | Coefficient (W × Variable) | |

| Eco | 0.700 *** | 0.473 | 0.738 * | −1.610 | 1.578 *** | 7.576 *** |

| (2.870) | (0.405) | (1.352) | (−0.897) | (3.204) | (3.804) | |

| Tec | 0.345 ** | −0.390 | 0.347 * | 0.110 | 0.036 * | −1.188 |

| (1.955) | (−0.846) | (1.781) | (0.232) | (1.466) | (−1.357) | |

| Fin | 0.395 * | −0.909 | 0.541 | −1.990 * | 0.259 | 2.710 * |

| (1.352) | (−0.949) | (0.760) | (−1.444) | (0.626) | (1.653) | |

| Com | 1.023 *** | 2.580 ** | 0.265 | 0.489 | 0.469 * | 4.644 *** |

| (2.661) | (2.135) | (0.287) | (0.213) | (1.837) | (2.844) | |

| Ent | 0.772 *** | 1.084 * | 1.209 ** | 1.007 | 0.736 ** | 0.516 |

| (3.391) | (1.625) | (2.391) | (1.256) | (2.371) | (0.523) | |

| Ser | 2.306 ** | −2.066 | −0.474 * | −7.621 * | 0.423 * | 9.594 ** |

| (2.227) | (−1.095) | (−2.009) | (−2.057) | (2.024) | (2.348) | |

| Lab | −0.548 * | −1.083 | 0.092* | −1.802 | −0.018 * | 0.268 |

| (−1.896) | (−0.741) | (1.830) | (−0.550) | (−1.212) | (0.862) | |

| ρ | 0.210 ** | 0.168 * | 0.251 *** | |||

| (2.605) | (1.750) | (3.512) | ||||

| observation | 168 | 126 | 140 | |||

| Log-likelihood | −173.974 | −144.577 | −184.960 | |||

| Adj-Squared | 0.809 | 0.330 | 0.518 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yao, L.; Singleton, A.; Sun, P.; Dong, G. The Evolution Characteristics and Influence Mechanism of Chinese Venture Capital Spatial Agglomeration. Int. J. Environ. Res. Public Health 2021, 18, 2974. https://doi.org/10.3390/ijerph18062974

Yao L, Singleton A, Sun P, Dong G. The Evolution Characteristics and Influence Mechanism of Chinese Venture Capital Spatial Agglomeration. International Journal of Environmental Research and Public Health. 2021; 18(6):2974. https://doi.org/10.3390/ijerph18062974

Chicago/Turabian StyleYao, Li, Alex Singleton, Pingjun Sun, and Guanpeng Dong. 2021. "The Evolution Characteristics and Influence Mechanism of Chinese Venture Capital Spatial Agglomeration" International Journal of Environmental Research and Public Health 18, no. 6: 2974. https://doi.org/10.3390/ijerph18062974

APA StyleYao, L., Singleton, A., Sun, P., & Dong, G. (2021). The Evolution Characteristics and Influence Mechanism of Chinese Venture Capital Spatial Agglomeration. International Journal of Environmental Research and Public Health, 18(6), 2974. https://doi.org/10.3390/ijerph18062974