The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan

Abstract

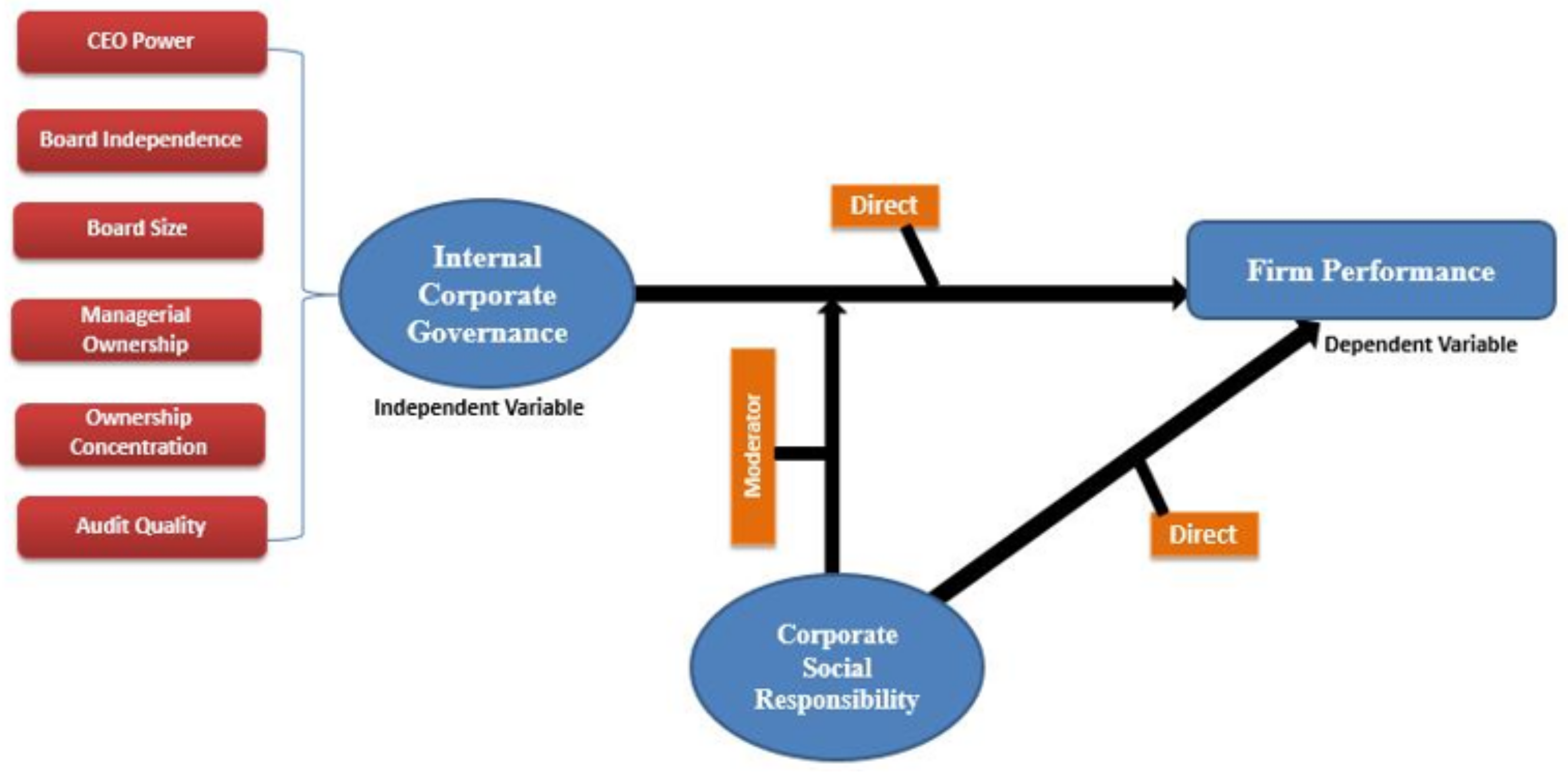

1. Introduction

2. Theoretical Analysis

3. Literature Review and Hypothesis Development

3.1. Internal Corporate Governance Factors and Firm Performance

3.2. Corporate Social Responsibility (CSR) and Firm Performance

3.3. The Moderating Role of CSR

4. Research Approach

4.1. Description of the Sample

4.2. CSR and Corporate Governance Practices in Pakistan

4.3. Variable Measurement

4.4. Analysis Techniques

4.4.1. Panel Data Issues

4.4.2. Solution for Panel Data Issues

4.5. Empirical Estimation Procedure

4.5.1. Model Construction

ICG and Firm Performance

CSR and Firm Performance

The Moderating Role of CSR

5. Results and Discussion

5.1. Results

5.2. Additional Test

5.3. Discussion

6. Conclusions

6.1. Policy Implications

6.2. Limitation and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Liao, Z. Market orientation and FIRMS’ environmental innovation: The moderating role of environmental attitude. Bus. Strat. Environ. 2018, 27, 117–127. [Google Scholar] [CrossRef]

- Song, M.; Zhang, L.; An, Q.; Wang, Z.; Li, Z. Statistical analysis and combination forecasting of environmental efficiency and its influential factors since China entered the WTO: 2002–2010–2012. J. Clean. Prod. 2013, 42, 42–51. [Google Scholar] [CrossRef]

- Adnan, S.M.; Hay, D.; van Staden, C.J. The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. J. Clean. Prod. 2018, 198, 820–832. [Google Scholar] [CrossRef]

- Contrafatto, M.; Ferguson, J.; Power, D.; Stevenson, L.; Collison, D. Understanding power-related strategies and initiatives. Account. Audit. Acc. J. 2019, 33, 559–587. [Google Scholar] [CrossRef]

- Bhagat, S.; Bolton, B. Corporate governance and firm performance. Sequel 2019, 58, 142–168. [Google Scholar]

- Bhatt, P.R.; Bhatt, R.R. Corporate governance and firm performance in Malaysia. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 896–912. [Google Scholar] [CrossRef]

- Hutchinson, M.; Gul, F.A. Investment opportunity set, corporate governance practices and firm performance. J. Corp. Financ. 2004, 10, 595–614. [Google Scholar] [CrossRef]

- Prevost, A.K.; Rao, R.P.; Hossain, M. Determinants of board composition in New Zealand: A simultaneous equations approach. J. Empir. Financ. 2002, 9, 373–397. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility. J. Bus. Ethic. 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Wu, S.; Quan, X.; Xu, L. CEO power, disclosure quality and the variability of firm performance. Nankai Bus. Rev. Int. 2011, 2, 79–97. [Google Scholar] [CrossRef]

- Bolourian, S.; Angus, A.; Alinaghian, L. The impact of corporate governance on corporate social responsibility at the board-level: A critical assessment. J. Clean. Prod. 2021, 291, 125752. [Google Scholar] [CrossRef]

- SECP. Rules and Regulations for Firms; Pakistan Stock Exchange: Islamabad, Pakistan, 2017.

- Sah, R.K.; Stiglitz, J. The Architecture of Economic Systems: Hierarchies and Polyarchies. Archit. Econ. Syst. Hierarchies Polyarchies 1984, 716–727. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder Perspective; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Wiseman, R.M.; Cuevas-Rodríguez, G.; Gomez-Mejia, L.R. Towards a social theory of agency. J. Manag. Stud. 2012, 49, 202–222. [Google Scholar] [CrossRef]

- Hill, C.W.; Jones, T.M. Stakeholder-agency theory. J. Manag. Stud. 1992, 29, 131–154. [Google Scholar] [CrossRef]

- Jizi, M.; Nehme, R. Board monitoring and audit fees: The moderating role of CEO/chair dual roles. Manag. Audit. J. 2018, 33, 217–243. [Google Scholar] [CrossRef]

- Calton, J.M.; Payne, S.L. Coping with paradox: Multistakeholder learning dialogue as a pluralist sensemaking process for addressing messy problems. Bus. Soc. 2003, 42, 7–42. [Google Scholar] [CrossRef]

- Brown, J.A.; Forster, W.R. CSR and stakeholder theory. Tale Adam Smith 2013, 112, 301–312. [Google Scholar]

- Berger, R.; Dutta, S.; Raffel, T.; Samuels, G. Innovating at the Top: How Global CEOs Drive Innovation for Growth and Profit; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Papadakis, V.M. Do CEOs shape the process of making strategic decisions? Evidence from Greece. Manag. Decis. 2006, 44, 367–394. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.; Wang, A.Y. Industry tournament incentives. Rev. Financ. Stud. 2017, 31, 1418–1459. [Google Scholar] [CrossRef]

- Javeed, S.A.; Lefen, L. An Analysis of Corporate Social Responsibility and Firm Performance with Moderating Effects of CEO Power and Ownership Structure: A Case Study of the Manufacturing Sector of Pakistan. Sustainability 2019, 11, 248. [Google Scholar] [CrossRef]

- Daily, C.M.; Johnson, J.L. Sources of CEO power and firm financial performance. Longitud. Assess. 1997, 23, 97–117. [Google Scholar]

- Garcia-Sanchez, I.-M.; Raimo, N.; Vitolla, F. CEO power and integrated reporting. Meditari Acc. Res. 2020. [Google Scholar] [CrossRef]

- Busco, C.; Frigo, M.L.; Quattrone, P.; Riccaboni, A. Towards Integrated Reporting: Concepts, Elements and Principles. In Integrated Reporting; Springer: Berlin/Heidelberg, Germany, 2013; pp. 3–18. [Google Scholar]

- Muttakin, M.B.; Khan, A.; Mihret, D.G. The Effect of Board Capital and CEO Power on Corporate Social Responsibility Disclosures. J. Bus. Ethics 2016, 150, 41–56. [Google Scholar] [CrossRef]

- Raheja, C.G. Determinants of board size and composition: A theory of corporate boards. J. Financ. Quant. Anal. 2005, 40, 283–306. [Google Scholar] [CrossRef]

- Bennedsen, M.; Kongsted, H.C.; Nielsen, K.M. The causal effect of board size in the performance of small and medium-sized firms. J. Bank. Financ. 2008, 32, 1098–1109. [Google Scholar] [CrossRef]

- Pearce, J.A.; Zahra, S.A. Board Composition from a strategic contingency perspective. J. Manag. Stud. 1992, 29, 411–438. [Google Scholar] [CrossRef]

- Ansari, B.; Gul, K.; Ahmad, N. Corporate Governance and Firm Performance: Automobile Assemblers Listed in Pakistan Stock Exchange (Psx). J. Bus. Strateg. 2017, 11, 125–140. [Google Scholar]

- Leung, S.; Richardson, G.; Jaggi, B. Corporate board and board committee independence, firm performance, and family ownership concentration: An analysis based on Hong Kong firms. J. Contemp. Acc. Econ. 2014, 10, 16–31. [Google Scholar] [CrossRef]

- Abbas, A.; Naqvi, H.A.; Mirza, H.H. Impact of large ownership on firm performance: A case of non-financial listed companies of Pakistan. World Appl. Sci. J. 2013, 21, 1141–1152. [Google Scholar]

- Yasser, Q.R.; Mamun, A.A. The impact of ownership concentration on firm performance: Evidence from an emerging market. Emerg. Econ. Stud. 2017, 3, 34–53. [Google Scholar] [CrossRef]

- Leung, S.C.M.; Horwitz, B. Corporate governance and firm value during a financial crisis. Rev. Quant. Financ. Acc. 2009, 34, 459–481. [Google Scholar] [CrossRef]

- Kapopoulos, P.; Lazaretou, S. Corporate Ownership Structure and Firm Performance: Evidence from Greek firms. Corp. Gov. Int. Rev. 2007, 15, 144–158. [Google Scholar] [CrossRef]

- Demsetz, H. The structure of ownership and the theory of the firm. J. Law Econ. 1983, 26, 375–390. [Google Scholar] [CrossRef]

- Raimo, N.; Vitolla, F.; Marrone, A.; Rubino, M. The role of ownership structure in integrated reporting policies. Bus. Strat. Environ. 2020, 29, 2238–2250. [Google Scholar] [CrossRef]

- Waweru, N. Determinants of quality corporate governance in Sub-Saharan Africa: Evidence from Kenya and South Africa. Manag. Audit. J. 2014, 29, 455–485. [Google Scholar] [CrossRef]

- Masood, A.; Afzal, M. Determinants of Audit Quality in Pakistan. J. Qual. Technol. Manag. 2016, 12, 25–49. [Google Scholar]

- Matoke, V.; Omwenga, J. Audit Quality and Financial Performance of Companies Listed in Nairobi Securities Exchange. Int. J. Sci. Res. Publ. 2016, 6, 372–381. [Google Scholar]

- Al Ani, M.K.; Mohammed, Z.O. Auditor quality and firm performance: Omani experience. Eur. J. Econ. Financ. Adm. Sci. 2015, 74, 13–23. [Google Scholar]

- Sattar, U.; Javeed, S.A.; Latief, R. How Audit Quality Affects the Firm Performance with the Moderating Role of the Product Market Competition: Empirical Evidence from Pakistani Manufacturing Firms. Sustainability 2020, 12, 4153. [Google Scholar] [CrossRef]

- Jacoby, G.; Liu, M.; Wang, Y.; Wu, Z.; Zhang, Y. Corporate governance, external control, and environmental information transparency: Evidence from emerging markets. J. Int. Financ. Mark. Inst. Money 2019, 58, 269–283. [Google Scholar] [CrossRef]

- King, A.A.; Lenox, M.J.; Terlaak, A. The Strategic Use of Decentralized Institutions: Exploring Certification with the ISO 14001 Management Standard. Acad. Manag. J. 2005, 48, 1091–1106. [Google Scholar] [CrossRef]

- Alexander, G.J.; Buchholz, R.A. Corporate social responsibility and stock market performance. Acad. Manag. J. 1978, 21, 479–486. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Oeyono, J.; Samy, M.; Bampton, R. An examination of corporate social responsibility and financial performance. J. Glob. Responsib. 2011, 2, 100–112. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Corporate environmental disclosure, financial markets and the media: An international perspective. Ecol. Econ. 2008, 64, 643–659. [Google Scholar] [CrossRef]

- Kong, Y.; Antwi-Adjei, A.; Bawuah, J. A systematic review of the business case for corporate social responsibility and firm performance. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 444–454. [Google Scholar] [CrossRef]

- Naseem, T.; Shahzad, F.; Asim, G.A.; Rehman, I.U.; Nawaz, F. Corporate social responsibility engagement and firm performance in Asia Pacific: The role of enterprise risk management. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 501–513. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A.J. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Jizi, M.I.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef]

- Khan, A.; Muttakin, M.B.; Siddiqui, J. Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. J. Bus. Ethics 2013, 114, 207–223. [Google Scholar] [CrossRef]

- Jamali, D.; Safieddine, A.M.; Rabbath, M. Corporate Governance and Corporate Social Responsibility Synergies and Interrelationships. Corp. Gov. Int. Rev. 2008, 16, 443–459. [Google Scholar] [CrossRef]

- Said, R.; Zainuddin, Y.H.; Haron, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef]

- Zhuang, Y.; Chang, X.; Lee, Y. Board Composition and Corporate Social Responsibility Performance: Evidence from Chinese Public Firms. Sustainability 2018, 10, 2752. [Google Scholar] [CrossRef]

- Guerrero-Villegas, J.; Pérez-Calero, L.; Hurtado-González, J.M.; Giráldez-Puig, P. Board Attributes and Corporate Social Responsibility Disclosure: A Meta-Analysis. Sustainability 2018, 10, 4808. [Google Scholar] [CrossRef]

- Lone, E.J.; Ali, A.; Khan, I. Corporate governance and corporate social responsibility disclosure: Evidence from Pakistan. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 785–797. [Google Scholar] [CrossRef]

- Sharif, M.; Rashid, K. Corporate governance and corporate social responsibility (CSR) reporting: An empirical evidence from commercial banks (CB) of Pakistan. Qual. Quant. 2013, 48, 2501–2521. [Google Scholar] [CrossRef]

- Majeed, S.; Aziz, T.; Saleem, S. The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Disclosure: An Empirical Evidence from Listed Companies at KSE Pakistan. Int. J. Financ. Stud. 2015, 3, 530–556. [Google Scholar] [CrossRef]

- Gul, S.; Muhammad, F.; Rashid, A. Corporate governance and corporate social responsibility: The case of small, medium, and large firms. Pak. J. Commer. Soc. Sci. 2017, 11, 1–34. [Google Scholar]

- Naseem, M.A.; Rehman, R.U.; Ikram, A.; Malik, F. Impact of board characteristics on corporate social responsibility disclosure. J. Appl. Bus. Res. 2017, 33, 801–810. [Google Scholar]

- Cong, Y.; Freedman, M. Corporate governance and environmental performance and disclosures. Adv. Acc. 2011, 27, 223–232. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.-Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Acc. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef]

- Freedman, M.; Park, J.D.; Romero, J. Recognizing Environmental Liabilities Surrounding CEO Turnovers. In Managing Reality: Accountability and the Miasma of Private and Public Domains; Emerald Group Publishing Limited: Bingley, UK, 2014. [Google Scholar]

- Kock, C.J.; Santaló, J.; Diestre, L. Corporate Governance and the Environment: What Type of Governance Creates Greener Companies? J. Manag. Stud. 2011, 49, 492–514. [Google Scholar] [CrossRef]

- Javeed, S.A.; Latief, R.; Lefen, L. An analysis of relationship between environmental regulations and firm performance with moderating effects of product market competition: Empirical evidence from Pakistan. J. Clean. Prod. 2020, 254, 120197. [Google Scholar] [CrossRef]

- Shahab, Y.; Ntim, C.G.; Chen, Y.; Ullah, F.; Li, H.-X.; Ye, Z. CEO Attributes, Sustainable Performance, Environmental Performance, and Environmental Reporting: New Insights from Upper Echelons Perspective. SSRN Electron. J. 2019. [Google Scholar] [CrossRef]

- Welford, R. Corporate governance and corporate social responsibility: Issues for Asia. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 42–51. [Google Scholar] [CrossRef]

- Lenssen, G.; Blagov, Y.; Bevan, D.; Peters, S.; Miller, M.; Kusyk, S. How Relevant is Corporate Governance and Corporate Social Responsibility in Emerging Markets? Available online: https://www.emerald.com/insight/content/doi/10.1108/14720701111159262/full/html?queryID=57%2F5412077 (accessed on 28 May 2021).

- Odoemelam, N.; Ofoegbu, G. Corporate Board Characteristics and Environmental Disclosure Quantity: A Comparative Analysis of Traditional and Integrated Reporting Evidence. Preprints 2018. [Google Scholar] [CrossRef]

- Osazuwa, N.P.; Che-Ahmad, A.; Che-Adam, N. Political Connection, Board Characteristics and Environmental Disclosure in Nigeria. Adv. Sci. Lett. 2017, 23, 9356–9361. [Google Scholar] [CrossRef]

- Rabi, A.M. Board Characteristics and Environmental Disclosure: Evidence from Jordan. Int. J. Bus. Manag. 2019, 14, 57. [Google Scholar] [CrossRef]

- Uwuigbe, U. An examination of the relationship between management ownership and corporate social responsibility disclosure: A study of selected firms in Nigeria. Res. J. Financ. Account. 2011, 2, 23–30. [Google Scholar]

- García-Meca, E.; Sánchez-Ballesta, J.P. The Association of Board Independence and Ownership Concentration with Voluntary Disclosure: A Meta-analysis. Eur. Acc. Rev. 2010, 19, 603–627. [Google Scholar] [CrossRef]

- Sufian, M.A.; Zahan, M. Ownership structure and corporate social responsibility disclosure in Bangladesh. Int. J. Econ. Financ. Issues 2013, 3, 901–909. [Google Scholar]

- Power, M. Expertise and the construction of relevance: Accountants and environmental audit. Account. Organ. Soc. 1997, 22, 123–146. [Google Scholar] [CrossRef]

- Ahmad, N.B.J.; Rashid, A.; Gow, F. Board independence and corporate social responsibility (CSR) reporting in Malaysia. Australas. Account. Bus. Financ. J. 2017, 11, 61–85. [Google Scholar] [CrossRef]

- Chang, Y.K.; Oh, W.-Y.; Park, J.H.; Jang, M.G. Exploring the Relationship Between Board Characteristics and CSR: Empirical Evidence from Korea. J. Bus. Ethics 2017, 140, 225–242. [Google Scholar] [CrossRef]

- Dewi, K.; Monalisa, M. Effect of Corporate Social Responsibility Disclosure on Financial Performance with Audit Quality as a Moderating Variable. Binus. Bus. Rev. 2016, 7, 149. [Google Scholar] [CrossRef]

- Tamimi, N.; Sebastianelli, R. Transparency among S&P 500 companies: An analysis of ESG disclosure scores. Manag. Decis. 2017, 55, 1660–1680. [Google Scholar] [CrossRef]

- SECP. Corporate Social Responsibility Voluntary Guidelines. 2013. Available online: http://www.secp.gov.pk/notification/pdf/2013/VoluntaryGuidelinesforCSR_2013.pdf (accessed on 10 July 2013).

- Cheema, K.U.R.; Din, M.S. Impact of corporate governance on performance of firms: A case study of cement industry in Pakistan. J. Bus. Manage. Sci. 2013, 4, 44–46. [Google Scholar]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef]

- Ahmad, N.; Taiba, S.; Kazmi, S.M.A.; Ali, H.N. Concept and Elements of Corporate Social Responsibility (CSR) and its Islamic Perspective: Mainstream Business Management Concern in Pakistan. Pak. J. Soc. Sci. 2015, 35, 925–934. [Google Scholar]

- Ali, W.; Frynas, J.G. The Role of Normative CSR-Promoting Institutions in Stimulating CSR Disclosures in Developing Countries. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 373–390. [Google Scholar] [CrossRef]

- Dawn. Pakistan Stock Exchange. Dawn Newspaper. Available online: https://www.dawn.com/ (accessed on 25 June 2020).

- Yusuf, F.; Yousaf, A.; Saeed, A. Rethinking agency theory in developing countries: A case study of Pakistan. Acc. Forum 2018, 281–292. [Google Scholar] [CrossRef]

- Liao, Z. Is environmental innovation conducive to corporate financing? The moderating role of advertising expenditures. Bus. Strategy Environ. 2020, 29, 954–961. [Google Scholar] [CrossRef]

- Kramer, J.K. Peters An Interindustry Analysis of Economic Value Added as a Proxy for Market Value Added. Available online: http://www.cunyspsc.org/files/papers_o/p_ECO_2001_jaf5899650_o.pdf (accessed on 19 May 2021).

- Zaid, M.A.; Abuhijleh, S.T.; Pucheta-Martínez, M.C. Ownership structure, stakeholder engagement, and corporate social responsibility policies: The moderating effect of board independence. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1344–1360. [Google Scholar] [CrossRef]

- Vitolla, F.; Raimo, N.; Rubino, M. Board characteristics and integrated reporting quality: An agency theory perspective. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1152–1163. [Google Scholar] [CrossRef]

- Sun, J.; Wang, J.; Kent, P.; Qi, B. Does sharing the same network auditor in group affiliated firms affect audit quality? J. Acc. Public Policy 2020, 39, 106711. [Google Scholar] [CrossRef]

- Hubbard, R.; Palia, D. Executive pay and performance Evidence from the U.S. banking industry. J. Financ. Econ. 1995, 39, 105–130. [Google Scholar] [CrossRef]

- Hermalin, B.E.; Weisbach, M.S. The Effects of Board Composition and Direct Incentives on Firm Performance. Financ. Manag. 1991, 20, 101. [Google Scholar] [CrossRef]

- Demsetz, H.; Lehn, K. The Structure of Corporate Ownership: Causes and Consequences. J. Polit. Econ. 1985, 93, 1155–1177. [Google Scholar] [CrossRef]

- Boone, A.L.; Field, L.C.; Karpoff, J.M.; Raheja, C.G. The determinants of corporate board size and composition: An empirical analysis. J. Financ. Econ. 2007, 85, 66–101. [Google Scholar] [CrossRef]

- DeAngelo, H.; DeAngelo, L.; Whited, T.M. Capital structure dynamics and transitory debt. J. Financ. Econ. 2011, 99, 235–261. [Google Scholar] [CrossRef]

- Antonakis, J.; Bendahan, S.; Jacquart, P.; Lalive, R. On making causal claims: A review and recommendations. Lead. Q. 2010, 21, 1086–1120. [Google Scholar] [CrossRef]

- Hamilton, B.H.; Nickerson, J.A. Correcting for Endogeneity in Strategic Management Research. Strat. Organ. 2003, 1, 51–78. [Google Scholar] [CrossRef]

- Aitken, A.C., IV. On Least Squares and Linear Combination of Observations. In Proceedings of the Royal Society of Edinburgh; Cambridge University Press (CUP): Cambridge, UK, 1936. [Google Scholar]

- Li, F. Endogeneity in CEO power: A survey and experiment. Invest. Anal. J. 2016, 45, 149–162. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277. [Google Scholar] [CrossRef]

- Blundell, R.; Griffiths, R.; Van Reenen, J. Market Share, Market Value and Innovation in a Panel of British Manufacturing Firms. Rev. Econ. Stud. 1999, 66, 529–554. [Google Scholar] [CrossRef]

- Feng, Y.; Chen, H.H.; Tang, J. The Impacts of Social Responsibility and Ownership Structure on Sustainable Financial Development of China’s Energy Industry. Sustainability 2018, 10, 301. [Google Scholar] [CrossRef]

- Ullah, S.; Akhtar, P.; Zaefarian, G. Dealing with endogeneity bias: The generalized method of moments (GMM) for panel data. Ind. Mark. Manag. 2018, 71, 69–78. [Google Scholar] [CrossRef]

- Wintoki, M.B.; Linck, J.S.; Netter, J.M. Endogeneity and the dynamics of internal corporate governance. J. Financ. Econ. 2012, 105, 581–606. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Inverse probability weighted M-estimators for sample selection, attrition, and stratification. Port. Econ. J. 2002, 1, 117–139. [Google Scholar] [CrossRef]

- Baltagi, B. Econometric Analysis of Panel Data; John Wiley & Sons: Hoboken, NJ, USA, 2008. [Google Scholar]

- Greene, W.H. Heteroscedasticity. Econometric Analysis, 4th ed.; Upper Saddle River, Prentice-Hall Inc.: Hoboken, NJ, USA, 2000; pp. 499–524. [Google Scholar]

- Mayur, M.; Saravanan, P. Performance implications of board size, composition and activity: Empirical evidence from the Indian banking sector. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 466–489. [Google Scholar] [CrossRef]

- Singh, S.; Guha, M. Experiential learning: Analyzing success and failures in Indian telecom sector. Benchmarking Int. J. 2018, 25, 3702–3719. [Google Scholar] [CrossRef]

- Chen, H.; Li, X.; Zeng, S.; Ma, H.; Lin, H. Does state capitalism matter in firm internationalization? Pace, rhythm, location choice, and product diversity. Manag. Decis. 2016, 54, 1320–1342. [Google Scholar] [CrossRef]

- Beiner, S.; Drobetz, W.; Schmid, M.M.; Zimmermann, H. An integrated framework of corporate governance and firm valuation. Eur. Financ. Manag. 2006, 12, 249–283. [Google Scholar] [CrossRef]

- Schultz, E.L.; Tan, D.T.; Walsh, K.D. Endogeneity and the corporate governance performance relation. Aust. J. Manag. 2010, 35, 145–163. [Google Scholar] [CrossRef]

- Gujarati, D.N. Basic Econometrics; Tata McGraw-Hill Education: New York, NY, USA, 2009. [Google Scholar]

- Weisbach, M.S. Outside directors and CEO turnover. J. Financ. Econ. 1988, 20, 431–460. [Google Scholar] [CrossRef]

- Brickley, J.A.; Coles, J.L.; Jarrell, G. Leadership structure: Separating the CEO and Chairman of the Board. J. Corp. Financ. 1997, 3, 189–220. [Google Scholar] [CrossRef]

- Cotter, J.F.; Shivdasani, A.; Zenner, M. Do independent directors enhance target shareholder wealth during tender offers? J. Financ. Econ. 1997, 43, 195–218. [Google Scholar] [CrossRef]

- Sah, R.K.; Stiglitz, J.E. The architecture of economic systems: Hierarchies and polyarchies. Am. Econ. Rev. 1986. [Google Scholar] [CrossRef]

- Malik, M.; Wan, D.; Ahmad, M.I.; Naseem, M.A.; Rehman, R.U. Role of Board Size in Corporate Governance and Firm Performance Applying Pareto Approach, Is It Cultural Phenomena? J. Appl. Bus. Res. 2014, 30, 1395. [Google Scholar] [CrossRef]

- Bhagat, S.; Bolton, B. Corporate governance and firm performance. J. Corp. Financ. 2008, 14, 257–273. [Google Scholar] [CrossRef]

- Liu, Y.; Miletkov, M.K.; Wei, Z.; Yang, T. Board independence and firm performance in China. J. Corp. Financ. 2015, 30, 223–244. [Google Scholar] [CrossRef]

- Nazir, M.S.; Afza, T. Does managerial behavior of managing earnings mitigate the relationship between corporate governance and firm value? Evidence from an emerging market. Futur. Bus. J. 2018, 4, 139–156. [Google Scholar] [CrossRef]

- Adhikary, B.; Huynh, L.; Hoang, G. Board structure and firm performance in emerging economies: Evidence from Vietnam. Ruhuna J. Manag. Financ. 2014, 1, 53–72. [Google Scholar]

- Coles, J.L.; Daniel, N.D.; Naveen, L. Boards: Does one size fit all? J. Financ. Econ. 2008, 87, 329–356. [Google Scholar] [CrossRef]

- Fauzi, F.; Locke, S. Board structure, ownership structure and firm performance: A study of New Zealand listed-firms. Manag. J. Account. Financ. 2012, 8, 43–67. [Google Scholar]

- Jackling, B.; Johl, S. Board structure and firm performance: Evidence from India’s top companies. Corp. Gov. Int. Rev. 2009, 17, 492–509. [Google Scholar] [CrossRef]

- Li, D.; Moshirian, F.; Nguyen, P.; Tan, L.-W. Managerial ownership and firm performance: Evidence from China’s privatizations. Res. Int. Bus. Financ. 2007, 21, 396–413. [Google Scholar] [CrossRef]

- Chen, C.R.; Guo, W.; Mande, V. Managerial ownership and firm valuation: Evidence from Japanese firms. Pac. Basin Financ. J. 2003, 11, 267–283. [Google Scholar] [CrossRef]

- Uwuigbe, U.; Olusanmi, O. An Empirical Examination of the Relationship between Ownership Structure and the Performance of Firms in Nigeria. Int. Bus. Res. 2011, 5, 208. [Google Scholar] [CrossRef]

- Kim, K.A.; Kitsabunnarat, P.; Nofsinger, J.R. Ownership and operating performance in an emerging market: Evidence from Thai IPO firms. J. Corp. Financ. 2004, 10, 355–381. [Google Scholar] [CrossRef]

- Claessens, S.; Djankov, S.; Pohl, G. Ownership and Corporate Governance: Evidence from the Czech Republic; World Bank Publications: Washington, DC, USA, 1997; Volume 1737. [Google Scholar]

- Hanousek, J.; Kočenda, E.; Svejnar, J. Origin and concentration: Corporate ownership, control and performance in firms after privatization. Econ. Transit. 2007, 15, 1–31. [Google Scholar] [CrossRef]

- Omran, M. Post-privatization corporate governance and firm performance: The role of private ownership concentration, identity and board composition. J. Comp. Econ. 2009, 37, 658–673. [Google Scholar] [CrossRef]

- Bonazzi, L.; Islam, S.M. Agency theory and corporate governance: A study of the effectiveness of board in their monitoring of the CEO. J. Model. Manag. 2007, 2, 7–23. [Google Scholar] [CrossRef]

- Agyemang-Mintah, P. Remuneration Committee governance and firm performance in UK financial firms. Invest. Manag. Financ. Innov. 2016, 13, 176–190. [Google Scholar] [CrossRef][Green Version]

- Crespi-Cladera, R.; Gispert-Pellicer, C. Board Remuneration, Performance and Corporate Governance in Large Spanish Companies. SSRN Electron. J. 1999. [Google Scholar] [CrossRef]

- Farrukh, K.; Irshad, S.; Khakwani, M.S.; Ishaque, S.; Ansari, N.Y. Impact of dividend policy on shareholders wealth and firm performance in Pakistan. Cogent Bus. Manag. 2017, 4, 1408208. [Google Scholar] [CrossRef]

- Arnott, R.D.; Asness, C.S. Surprise! Higher Dividends = Higher Earnings Growth. Financ. Anal. J. 2003, 59, 70–87. [Google Scholar] [CrossRef]

- Ouma, O.P. The relationship between dividend payout and firm performance: A study of listed companies in Kenya. Eur. Sci. J. 2012, 8, 9. [Google Scholar]

- Birindelli, G.; Dell’Atti, S.; Iannuzzi, A.P.; Savioli, M. Composition and activity of the board of directors: Impact on ESG performance in the banking system. Sustainability 2018, 10, 4699. [Google Scholar] [CrossRef]

- Valls Martínez, M.d.C.; Martín Cervantes, P.A.; Cruz Rambaud, S.E. Women on corporate boards and sustainable development in the American and European markets: Is there a limit to gender policies? JCSR Manag. 2020, 27, 2642–2656. [Google Scholar] [CrossRef]

{kind=link}

| Dependent Variables | Abbreviations | Measures |

|---|---|---|

| Economic Value Added | EVA | Net operational profit after tax minus cost of capital into the capital invested [94]. |

| Sustainable Growth Rate | SGR | PM × (1 − D) × (1 + L)/(T − (PM ×(1 − D) × (1 + L))) 1 [24]. |

| Independent Variables | ||

| Chief Executive Officer Power | CEO Power | CEO annual compensations/ Whole board of directors compensations [68]. |

| Board Independence | BI | Independent directors on board/Total number of board of directors on board [95]. |

| Board Size | BS | The total member of board members on the board [96]. |

| Ownership Concentration | OC | The major shareholding portion or Top 5 shareholders [24]. |

| Managerial Ownership | MO | The portion of shares held by the management [24]. |

| Audit Quality | AQ | The statutory audit fees to the number of sales [97]. |

| Corporate Social Responsibility | CSR | The addition of Earning Per Share (EPS), total taxes, staff salaries, interests, and public expenses minus social cost divided by total equity [24]. |

| Control Variables | ||

| Property, Plant, and Equipment | PPE | The ratio of property, plant, and equipment to total sales [71]. |

| Firm Size | LNTA | The natural log of total assets [71]. |

| Asset turnover | ATO | The ratio of total sales to total asset [71]. |

| Environmental Awareness | EA | The ratio of an average green investment divided by No. of employees [71]. |

| Variables | M | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. EVA | 0.27 | 0.5 | 1 | ||||||||||||

| 2. SGR | 0.68 | 0.13 | 1.00 *** | 1 | |||||||||||

| 3. CEO POWER | 3.38 | 4.21 | 0.78 *** | 0.79 *** | 1 | ||||||||||

| 4. BI | 2.43 | 5.01 | 0.98 *** | 0.98 *** | 0.77 *** | 1 | |||||||||

| 5. BS | 0.2 | 0.37 | 0.52 *** | 0.53 *** | 0.71 *** | 0.50 *** | 1 | ||||||||

| 6. MO | 5.36 | 3.54 | 0.45 *** | 0.44 *** | 0.33 *** | 0.47 *** | 0.28 *** | 1 | |||||||

| 7. OC | 1.24 | 1.64 | 0.73 *** | 0.74 *** | 0.92 *** | 0.70 *** | 0.66 *** | 0.25 *** | 1 | ||||||

| 8. AQ | 0.92 | 1.72 | 0.99 *** | 0.97 *** | 0.79 *** | 0.99 *** | 0.53 *** | 0.46 *** | 0.73 *** | 1 | |||||

| 9. CSR | 0.97 | 1.36 | 0.74 *** | 0.73 *** | 0.92 *** | 0.72 *** | 0.68 *** | 0.30 *** | 0.86 *** | 0.73 *** | 1 | ||||

| 10. ATO | −0.71 | 0.59 | −0.44 *** | −0.63 *** | −0.32 *** | −0.46 *** | −0.17 *** | −0.43 *** | −0.27 *** | −0.47 *** | −0.20 *** | 1 | |||

| 11. EA | 0.29 | 0.4 | 0.06 *** | 0.02 *** | 0.29 *** | 0.09 *** | 0.24 *** | 0.42 *** | 0.21 *** | 0.07 *** | 0.21 *** | −0.25 *** | 1 | ||

| 12. LNTA | 0.11 | 0.13 | 0.25 *** | 0.24 *** | 0.29 *** | 0.28 *** | 0.22 *** | 0.66 *** | 0.24 *** | 0.26 *** | 0.18 *** | −0.49 *** | 0.72 *** | 1 | |

| 13. PPE | 1.77 | 4.18 | 0.76 *** | 0.75 *** | 0.86 *** | 0.79 *** | 0.62 *** | 0.53 *** | 0.74 *** | 0.78 *** | 0.76 *** | −0.47 *** | 0.45 *** | 0.51 *** | 1 |

| Independent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 |

|---|---|---|---|---|---|---|---|

| CEO POWER | 0.625 *** | ||||||

| BI | 1.288 *** | ||||||

| BS | 2.862 *** | ||||||

| MO | 0.051 ** | ||||||

| OC | 0.261 *** | ||||||

| AQ | 1.423 ** | ||||||

| CSR | 2.635 ** | ||||||

| ATO | |||||||

| EA | |||||||

| LNTA | |||||||

| PPE | 10.827 ** | 6.429 *** | 12.651 *** | 7.956 ** | 13.733 ** | 9.617 *** | 11.388 ** |

| Constant | 0.698 ** | 2.577 *** | 0.737 *** | 0.764 *** | 1.492 ** | 0.468 *** | 2.815 ** |

| R2 | 0.8741 | 0.9216 | 0.8563 | 0.7889 | 0.9350 | 0.8819 | 0.8931 |

| Durbin–Wu–Hausman | 25.78 *** | 31.57 *** | 27.41 *** | 28.74 *** | 36.65 *** | 33.44 *** | 32.94 *** |

| Dependent Variables | Model 1 | Model 2 | ||

|---|---|---|---|---|

| Independent Variables | EVA | SGR | ||

| FE | GMM | FE | GMM | |

| CEO POWER | 0.004 *** | 0.005 *** | 0.001 *** | 0.011 *** |

| BI | 0.015 *** | 0.018 *** | 0.003 *** | 0.004 *** |

| BS | 0.008 *** | 0.004 ** | 0.002 *** | 0.001 ** |

| MO | 0.006 *** | 0.005 *** | 0.001 *** | 0.002 *** |

| OC | 0.012 *** | 0.009 *** | 0.003 *** | 0.003 *** |

| AQ | 0.240 *** | 0.237 *** | 0.060 *** | 0.059 *** |

| ATO | −0.004 *** | −0.005 ** | −0.001 | −0.002 ** |

| EA | −0.007 | −0.003 | −0.015 | −0.008 |

| LNTA | −0.004 | 0.006 | −0.002 | −0.001 |

| PPE | 0.009 *** | −0.010 *** | −0.002 *** | −0.003 *** |

| Constant | −0.033 *** | −0.025 *** | −0.008 *** | −0.006 *** |

| R2 | 0.9920 | 0.9921 | ||

| F | 31.54 *** | 31.54 *** | ||

| N | 3686 | 2891 | 3686 | 2891 |

| Hausman Test | 58.86 *** | 56.87 *** | ||

| Wald Chi2 | 381,653.42 *** | 382,654.44 *** | ||

| Dependent Variables | Model 3 | Model 4 | ||

|---|---|---|---|---|

| Independent Variables | EVA | SGR | ||

| FE | GMM | FE | GMM | |

| CSR | 0.155 *** | 0.144 *** | 0.038 *** | 0.035 *** |

| ATO | 0.011 | −0.009 | 0.002 | −0.003 |

| EA | −0.840 *** | −1.092 *** | −0.209 *** | −0.272 *** |

| LNTA | 0.749 *** | 0.655 *** | 0.188 *** | 0.164 *** |

| PPE | 0.052 *** | 0.054 *** | 0.012 *** | 0.013 *** |

| Constant | 0.126 *** | 0.229 *** | 0.051 *** | 0.058 *** |

| R2 | 0.6355 | 0.6412 | ||

| F | 13.42 *** | 13.54 *** | ||

| N | 3686 | 2891 | 3686 | 2891 |

| Hausman Test | 83.86 *** | 84.85 *** | ||

| Wald Chi2 | 4657.13 *** | 4655.14 *** | ||

| Dependent Variables | Model 5 | Model 6 | ||

|---|---|---|---|---|

| Independent Variables | EVA | SGR | ||

| FE | GMM | FE | GMM | |

| CEO POWER | 0.002 *** | 0.003 *** | 0.006 *** | 0.007 *** |

| BI | −0.008 *** | −0.007 *** | −0.002 *** | −0.003 *** |

| BS | 0.004 | 0.005 ** | 0.001 | 0.004 |

| MO | 0.005 *** | 0.004 *** | 0.002 *** | 0.001 *** |

| OC | 0.008 *** | 0.008 *** | 0.001 *** | 0.002 *** |

| AQ | 0.050 *** | 0.052 *** | 0.012 *** | 0.013 *** |

| CSR | −0.006 *** | −0.007 *** | −0.001 *** | −0.001 *** |

| CEO POWER × CSR | 0.001 *** | 0.002 ** | 0.009 *** | 0.002 *** |

| BI × CSR | 0.471 *** | 0.524 *** | 0.117 *** | 0.131 *** |

| BS × CSR | 0.856 *** | 0.875 *** | 0.214 *** | 0.218 *** |

| MO × CSR | 2.153 *** | 1.976 *** | 0.538 *** | 0.494 *** |

| OC × CSR | 1.935 *** | 1.760 *** | 0.483 *** | 0.440 *** |

| AQ × CSR | 10.88 *** | 11.87 *** | 2.722 *** | 2.968 *** |

| ATO | −0.001 | −0.003 | -0.004 | −0.007 |

| EA | −0.002 | −0.002 * | −0.006 *** | −0.009 *** |

| LNTA | −0.006 *** | −0.007 ** | −0.001 ** | −0.007 ** |

| PPE | −0.001 *** | −0.001 *** | −0.003 *** | −0.004 *** |

| Constant | −0.008 ** | −0.005 | −0.002 | −0.002 |

| R2 | 0.9999 | 0.9998 | ||

| F | 25.38 *** | 26.37 *** | ||

| N | 3686 | 2891 | 3686 | 2891 |

| Hausman Test | 44.03 *** | 45.44 *** | ||

| Wald Chi2 | 29,303.31 *** | 35,768.19 *** | ||

| Dependent Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

|---|---|---|---|---|---|---|

| Independent Variables | EVA | SGR | EVA | SGR | EVA | SGR |

| FGLS | FGLS | FGLS | FGLS | FGLS | FGLS | |

| CEO POWER | 0.009 *** | 0.002 *** | 0.003 *** | 0.008 *** | ||

| BI | 0.007 *** | 0.001 *** | −0.006 *** | −0.001 *** | ||

| BS | 0.003 *** | 0.002 *** | 0.001 | 0.002 | ||

| MO | 0.002 ** | 0.0001 ** | 0.002 *** | 0.004 *** | ||

| OC | 0.001 *** | 0.004 *** | −0.003 ** | −0.005 ** | ||

| AQ | 0.264 *** | 0.066 *** | 0.036 *** | 0.009 *** | ||

| CSR | 0.141 *** | 0.035 *** | −0.001 *** | −0.001 *** | ||

| CEO POWER × CSR | 0.003 *** | 0.004 *** | ||||

| BI × CSR | 0.304 *** | 0.076 *** | ||||

| BS × CSR | 0.626 *** | 0.156 *** | ||||

| MO × CSR | 2.761 *** | 0.691 *** | ||||

| OC × CSR | 3.148 *** | 0.787 *** | ||||

| AQ × CSR | 9.272 *** | 2.318 *** | ||||

| ATO | −0.002 *** | 0.001 *** | −0.072 *** | −0.018 *** | −0.001 *** | −0.001 *** |

| EA | −0.005 *** | −0.012 *** | −0.356 *** | −0.090 *** | 0.006 *** | 0.002 *** |

| LNTA | −0.027 *** | 0.006 *** | 0.314 *** | 0.078 *** | 0.005 *** | −0.005 *** |

| PPE | 0.011 *** | −0.002 *** | 0.070 *** | 0.017 *** | −0.001 *** | 0.004 *** |

| Constant | −0.001 *** | −0.003 *** | 0.025 *** | 0.006 *** | −0.009 *** | −0.002 *** |

| N | 3686 | 3686 | 3686 | 3686 | 3686 | 3686 |

| Wald Chi2 | 972,427 *** | 98,403.85 *** | 52,988.46 *** | 21,598.47 *** | 63,849.06 *** | 224,869.16 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lu, J.; Javeed, S.A.; Latief, R.; Jiang, T.; Ong, T.S. The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan. Int. J. Environ. Res. Public Health 2021, 18, 5830. https://doi.org/10.3390/ijerph18115830

Lu J, Javeed SA, Latief R, Jiang T, Ong TS. The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan. International Journal of Environmental Research and Public Health. 2021; 18(11):5830. https://doi.org/10.3390/ijerph18115830

Chicago/Turabian StyleLu, Jihai, Sohail Ahmad Javeed, Rashid Latief, Tao Jiang, and Tze San Ong. 2021. "The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan" International Journal of Environmental Research and Public Health 18, no. 11: 5830. https://doi.org/10.3390/ijerph18115830

APA StyleLu, J., Javeed, S. A., Latief, R., Jiang, T., & Ong, T. S. (2021). The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan. International Journal of Environmental Research and Public Health, 18(11), 5830. https://doi.org/10.3390/ijerph18115830