Benefits Associated with China’s Social Health Insurance Schemes: Trend Analysis and Associated Factors Since Health Reform

Abstract

1. Introduction

2. Materials and Methods

3. Results

3.1. Characteristics of Participants

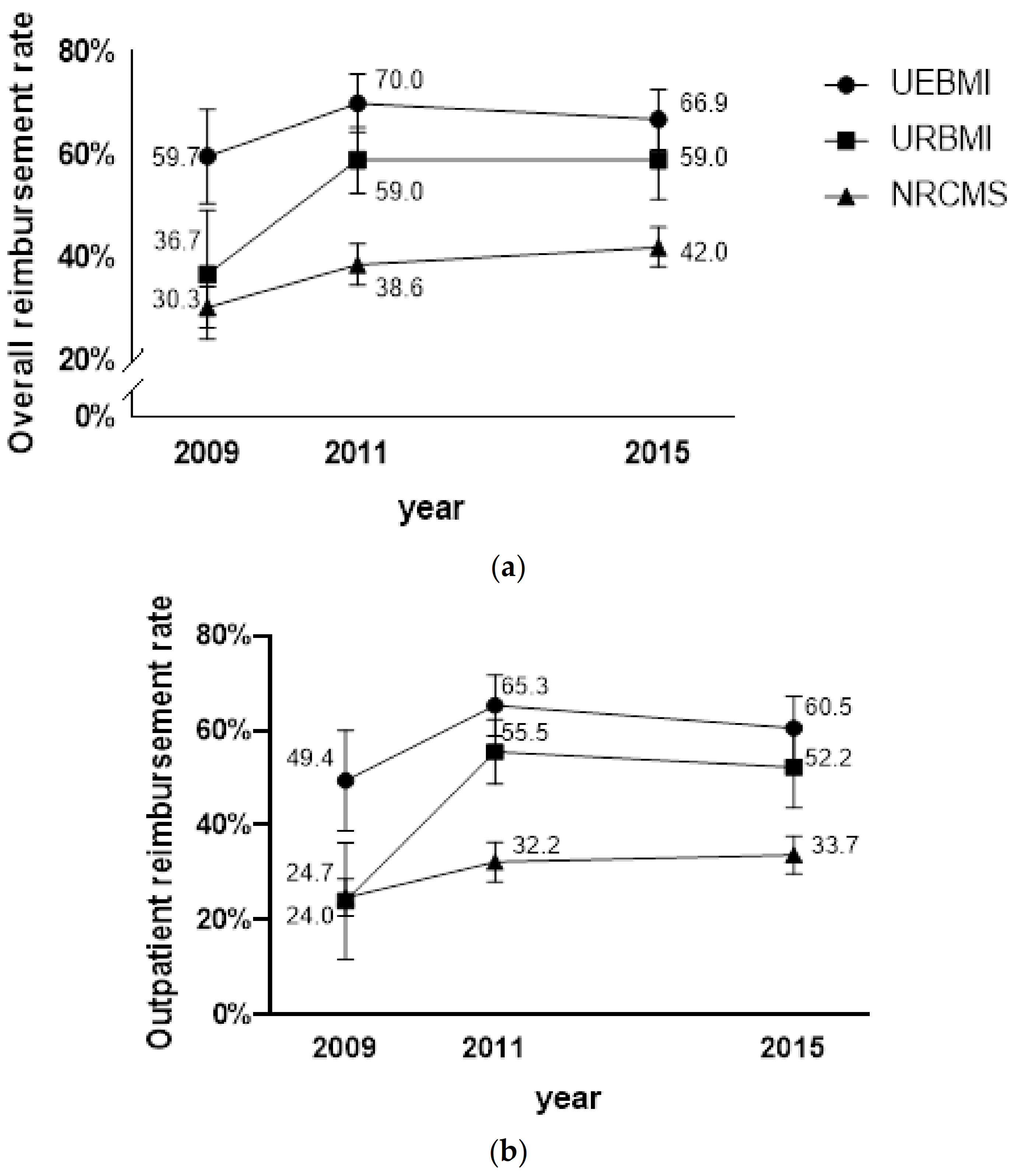

3.2. Reimbursement Rate of Different Social Health Insurance Schemes

3.3. Reimbursement Amount for the Different Social Health Insurance Schemes

3.4. Factors Associated with Benefits among Social Health Insurance Schemes

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

References

- United Nations Transforming Our World: The 2030 Agenda for Sustainable Development. Available online: https://sustainabledevelopment.un.org/post2015/transformingourworld (accessed on 5 December 2020).

- Ge, Y.F.; Gong, S. China’s Medical Reform Problem • Roots • Way Out; China Development Press: Beijing, China, 2007. [Google Scholar]

- The State Council of the People’s Republic of China The Opinions of the Communist Party of China Central Committee and the State Council on Deepening Reform of the Health Care System. Available online: http://www.gov.cn/jrzg/2009-04/06/content_1278721.htm (accessed on 17 December 2020).

- Hsiao, W.; Li, M.; Zhang, S. Universal Health Coverage: The Case of China; UNRISD Working Paper: Geneva, Switzerland, 2015. [Google Scholar]

- China’s State Council Information Office of the People’s Republic of China The Right to Development: China’s Philosophy, Practice and Contribution. Available online: http://www.scio.gov.cn/zfbps/ndhf/34120/Document/1534705/1534705.htm (accessed on 6 December 2020).

- Fang, H.; Eggleston, K.; Hanson, K.; Wu, M. China’s Health System Reforms: Review of 10 Years of Progress: Enhancing Financial Protection under China’s Social Health Insurance to Achieve Universal Health Coverage. BMJ 2019, 365, 2378. [Google Scholar] [CrossRef] [PubMed]

- Chen, G.; Liu, G.G.; Xu, F. The Impact of the Urban Resident Basic Medical Insurance on Health Services Utilisation in China. Pharmacoeconomics 2014, 32, 277–292. [Google Scholar] [CrossRef] [PubMed]

- Wang, Z.; Li, X.; Chen, M.; Si, L. Social Health Insurance, Healthcare Utilization, and Costs in Middle-aged and Elderly Community-dwelling Adults in China. Int. J. Equity Health 2018, 17, 1–13. [Google Scholar] [CrossRef] [PubMed]

- Xian, W.; Xu, X.; Li, J.; Sun, J.; Fu, H.; Wu, S.; Liu, H. Health Care Inequality under Different Medical Insurance Schemes in a Socioeconomically Underdeveloped Region of China: A Propensity Score Matching Analysis. BMC Public Health 2019, 19, 1–9. [Google Scholar] [CrossRef]

- Zhang, A.; Nikoloski, Z.; Mossialos, E. Does Health Insurance Reduce out-of-pocket Expenditure? Heterogeneity among China’s Middle-aged and Elderly. Soc. Sci. Med. 2017, 190, 11–19. [Google Scholar] [CrossRef]

- Li, C.; Yu, X.; Butler, J.R.; Yiengprugsawan, V.; Yu, M. Moving Towards Universal Health Insurance in China: Performance, Issues and Lessons from Thailand. Soc. Sci. Med. 2011, 73, 359–366. [Google Scholar] [CrossRef]

- Fu, R.; Wang, Y.; Bao, H.; Wang, Z.; Li, Y.; Su, S.; Liu, M. Trend of Urban-rural Disparities in Hospital Admissions and Medical Expenditure in China from 2003 to 2011. PLoS ONE 2014, 9, e108571. [Google Scholar] [CrossRef]

- Li, Z.; Huang, W.D. The Path for Integrating Basic Medical Insurance: An Analysis Based on the Level of Financing. Comp. Econ. Soc. Syst. 2017, 6, 138–148. [Google Scholar]

- Qiu, Y.L.; Huang, G.W. Discussion on Coordinated Development of the Urban and Rural Social Medical Insurance from the Perspective of Three Fairness. Chin. J. Health Policy 2013, 6, 4–7. [Google Scholar]

- Meng, Q.; Xu, L. Monitoring and Evaluating Progress Towards Universal Health Coverage in China. PLoS Med. 2014, 11, e1001694. [Google Scholar] [CrossRef]

- Shibuya, K.; Hashimoto, H.; Ikegami, N.; Nishi, A.; Tanimoto, T.; Miyata, H.; Takemi, K.; Reich, M.R. Future of Japan’s System of Good Health at Low Cost with Equity: Beyond Universal Coverage. Lancet 2011, 378, 1265–1273. [Google Scholar] [CrossRef]

- Meng, Q.; Fang, H.; Liu, X.; Yuan, B.; Xu, J. Consolidating the Social Health Insurance Schemes in China: Towards an Equitable and Efficient Health System. Lancet 2015, 386, 1484–1492. [Google Scholar] [CrossRef]

- Tian, L.F. Analysis of Government Regulation in the Integration of Urban and Rural Medical Insurance System. J. Dev. Reform 2018, 8, 21–24. [Google Scholar]

- Tan, Z.H. How to Establish a Fair and Sustainable Medical Security System: To Promote the Integration of Medical Insurance in Urban and Rural Areas as an Opportunity. China Health Insur. 2018, 8, 6–9. [Google Scholar]

- The State Council of the People’s Republic of China Notice of the State Council on the Establishment of Institutions. Available online: http://www.gov.cn/zhengce/content/2018-03/24/content_5277121.htm (accessed on 6 December 2020).

- National Bureau of Statistics of China National Data of Health. Available online: http://data.stats.gov.cn/easyquery.htm?cn=C01 (accessed on 18 December 2020).

- Ministry of Human Resources and Social Security of the People’s Republic of China Notice on doing a Good Job of Urban Resident Basic Medical Insurance in 2015. Available online: http://www.mohrss.gov.cn/SYrlzyhshbzb/ldbk/shehuibaozhang/yiliao/201502/t20150209_151708.htm (accessed on 18 December 2020).

- National Health Commission of the People’s Republic of China Notice on doing a Good Job of the New Rural Cooperative Medical Scheme in 2015. Available online: http://www.nhfpc.gov.cn/jws/s3581sg/201501/98d95186d494472e8d4ae8fa60e9efc5.shtml (accessed on 18 December 2020).

- Ministry of Health of the People’s Republic of China Notice on doing a Good Job of the New Rural Cooperative Medical Scheme in 2008. Available online: http://www.gov.cn/zwgk/2008-03/24/content_927289.htm (accessed on 6 December 2020).

- Shan, L.; Wu, Q.; Liu, C.; Li, Y.; Cui, Y.; Liang, Z.; Hao, Y.; Liang, L.; Ning, N.; Ding, D. Perceived Challenges to Achieving Universal Health Coverage: A Cross-sectional Survey of Social Health Insurance Managers/Administrators in China. BMJ Open 2017, 7, e014425. [Google Scholar] [CrossRef]

- World Bank. The Path to Integrated Insurance Systems in China; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Tan, S.Y.; Wu, X.; Yang, W. Impacts of the Type of Social Health Insurance on Health Service Utilisation and Expenditures: Implications for a Unified System in China. Health Econ. Policy Law 2019, 14, 468–486. [Google Scholar] [CrossRef] [PubMed]

- Dror, D.M.; Hossain, S.S.; Majumdar, A.; Pérez Koehlmoos, T.L.; John, D.; Panda, P.K. What Factors Affect Voluntary Uptake of Community-based Health Insurance Schemes in Low-and Middle-income Countries? A Systematic Review and Meta-analysis. PLoS ONE 2016, 11, e0160479. [Google Scholar] [CrossRef]

- Zhou, Q.; Liu, G. The Difference of Benefits from Health Insurance: Based on the Study of the Local Population and Migrants. Nankai Econ. Stud. 2016, 1, 77–94. [Google Scholar]

- Yang, X.; Jiang, S.; Fan, L.; Wu, W. The Influencing Factors and Countermeasures of the Actual Reimbursement Proportion of Basic Medical Insurance—Taking Guangxi as an Example. Health Econ. Res. 2013, 3, 37–39. [Google Scholar]

- Filipski, M.J.; Zhang, Y.; Chen, K.Z. Making Health Insurance Pro-poor: Evidence from a Household Panel in Rural China. BMC Health Serv. Res. 2015, 15, 210. [Google Scholar] [CrossRef]

- Duan, N.H. Smearing Estimate: A Nonparametric Retransformation Method. J. Am. Stat. Assoc. 1983, 78, 605–610. [Google Scholar] [CrossRef]

- Guo, N.; Iversen, T.; Lu, M.; Wang, J.; Shi, L. Does the New Cooperative Medical Scheme Reduce Inequality in Catastrophic Health Expenditure in Rural China? BMC Health Serv. Res. 2016, 16, 1–11. [Google Scholar] [CrossRef] [PubMed]

- Meng, Q.; Xu, L.; Zhang, Y.; Qian, J.; Cai, M.; Xin, Y.; Gao, J.; Xu, K.; Boerma, J.T.; Barber, S.L. Trends in Access to Health Services and Financial Protection in China between 2003 and 2011: A Cross-sectional Study. Lancet 2012, 379, 805–814. [Google Scholar] [CrossRef]

- Kondo, A.; Shigeoka, H. Effects of Universal Health Insurance on Health Care Utilization, and Supply-side Responses: Evidence from Japan. J. Public Econ. 2013, 99, 1–23. [Google Scholar] [CrossRef]

- Gianino, M.M.; Lenzi, J.; Martorana, M.; Bonaudo, M.; Fantini, M.P.; Siliquini, R.; Ricciardi, W.; Damiani, G. Trajectories of Long-term Care in 28 EU Countries: Evidence from a Time Series Analysis. Eur. J. Public Health 2017, 27, 948–954. [Google Scholar] [CrossRef][Green Version]

- Zhao, M.; Liu, B.; Shan, L.; Li, C.; Wu, Q.; Hao, Y.; Chen, Z.; Lan, L.; Kang, Z.; Liang, L.; et al. Can Integration Reduce Inequity in Healthcare Utilization? Evidence and Hurdles in China. BMC Health Serv. Res. 2019, 19, 654. [Google Scholar] [CrossRef]

- Center for Health Statistics and Information An Analysis Report of National Health Services Survey in China. 2013. Available online: http://www.nhfpc.gov.cn/ewebeditor/uploadfile/2016/10/20161026163512679.pdf (accessed on 10 October 2020).

- Yip, W.; Hsiao, W. China’s Health Care Reform: A Tentative Assessment. China Econ. Rev. 2009, 20, 613–619. [Google Scholar] [CrossRef]

- Su, M.; Zhou, Z.; Si, Y.; Wei, X.; Xu, Y.; Fan, X.; Chen, G. Comparing the Effects of China’s Three Basic Health Insurance Schemes on the Equity of Health-related Quality of Life: Using the Method of Coarsened Exact Matching. Health Qual. Life Outcomes 2018, 16, 1–12. [Google Scholar] [CrossRef] [PubMed]

- Ta, Y.; Zhu, Y.; Fu, H. Trends in Access to Health Services, Financial Protection and Satisfaction between 2010 and 2016: Has China Achieved the Goals of Its Health System Reform? Soc. Sci. Med. 2020, 245, 112715. [Google Scholar] [CrossRef]

- Chen, M.; Palmer, A.J.; Lei, S. Assessing Equity in Benefit Distribution of Government Health Subsidy in 2012 Across East China: Benefit Incidence Analysis. Int. J. Equity Health 2016, 15, 1–10. [Google Scholar] [CrossRef][Green Version]

- World Health Organization. Health Systems Financing: The Path to Universal Coverage; World Health Organization: Geneva, Switzerland, 2010. [Google Scholar]

- Ministry of Human Resources and Social Security of the People’s Republic of China Opinions on the General Issues Concerning the Coordination of Urban Resident Basic Medical Insurance Clinics. Available online: http://www.gov.cn/fwxx/cjr/content_2440497.htm (accessed on 18 December 2020).

- Ministry of Health of the People’s Republic of China Notice on doing a Good Job of the New Rural Cooperative Medical Scheme in 2012. Available online: http://www.gov.cn/zwgk/2012-05/25/content_2145389.htm (accessed on 18 December 2020).

- Mao, W.; Tang, Y.; Tran, T.; Pender, M.; Khanh, P.N.; Tang, S. Advancing Universal Health Coverage in China and Vietnam: Lessons for Other Countries. BMC Public Health 2020, 20, 1–9. [Google Scholar] [CrossRef] [PubMed]

- Sun, Q.; Liu, X.; Meng, Q.; Tang, S.; Yu, B.; Tolhurst, R. Evaluating the Financial Protection of Patients with Chronic Disease by Health Insurance in Rural China. Int. J. Equity Health 2009, 8, 1–10. [Google Scholar] [CrossRef] [PubMed]

- Li, Y.; Zhao, Y.; Yi, D.; Wang, X.; Jiang, Y.; Wang, Y.; Liu, X.; Ma, S. Differences Exist Across Insurance Schemes in China Post-consolidation. PLoS ONE 2017, 12, e0187100. [Google Scholar] [CrossRef] [PubMed]

- Mao, W.; Wang, H.; Wang, Z.Z.; Li, X.W.; Zhang, Y.L. Functional Positioning of Tertiary Hospitals. Foreign Med. 2015, 32, 85–87. [Google Scholar]

- Li, C.; Hou, Y.; Sun, M.; Lu, J.; Wang, Y.; Li, X.; Chang, F.; Hao, M. An Evaluation of China’s New Rural Cooperative Medical System: Achievements and Inadequacies from Policy Goals. BMC Public Health 2015, 15, 1–9. [Google Scholar] [CrossRef]

- Liu, K.; Yang, J.; Lu, C. Is the Medical Financial Assistance Program an Effective Supplement to Social Health Insurance for Low-income Households in China? A Cross-sectional Study. Int. J. Equity Health 2017, 16, 1–13. [Google Scholar] [CrossRef]

- Jiang, J.; Chen, S.; Xin, Y.; Wang, X.; Zeng, L.; Zhong, Z.; Xiang, L. Does the Critical Illness Insurance Reduce Patients’ Financial Burden and Benefit the Poor More: A Comprehensive Evaluation in Rural Area of China. J. Med. Econ. 2019, 22, 455–463. [Google Scholar] [CrossRef]

- The State Council of the People’s Republic of China Work Plan for Institutional and Governance Reform of the National Administrative Structure. Available online: http://www.gov.cn/2013lh/content_2364664.htm (accessed on 6 December 2020).

- Shan, L.; Zhao, M.; Ning, N.; Hao, Y.; Li, Y.; Liang, L.; Kang, Z.; Sun, H.; Ding, D.; Liu, B. Dissatisfaction with Current Integration Reforms of Health Insurance Schemes in China: Are They a Success and What Matters? Health Policy Plan. 2018, 33, 345–354. [Google Scholar] [CrossRef]

- Hsiao, W.; Shaw, R.P. Social Health Insurance for Developing Nations; The World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Pan, J.; Tian, S.; Zhou, Q.; Han, W. Benefit Distribution of Social Health Insurance: Evidence from China’s Urban Resident Basic Medical Insurance. Health Policy Plan. 2016, 31, 853. [Google Scholar] [CrossRef]

- Dong, K. Medical Insurance System Evolution in China. China Econ. Rev. 2009, 20, 591–597. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Features of Each Scheme | Urban Employee Basic Medical Insurance | Urban Resident Basic Medical Insurance | New Rural Cooperative Medical Scheme |

|---|---|---|---|

| (UEBMI) | (URBMI) | (NRCMS) | |

| Year established | 1998 | 2007 | 2003 |

| Target population | Urban employees | Urban unemployed, elderly, students, children | Rural residents |

| Risk-pooling unit | Municipal level | Municipal level | County level |

| Number of people insured by 2015 (millions) | 288.93 | 376.89 | 670.00 |

| Benefit package (in 2015) | Outpatient and inpatient care | Outpatient and inpatient care | Outpatient and inpatient care |

| Financing | Employer (6–8% of salary) Individual (2–3% of salary) | Government subsidy about 80% Individual about 20% | Government subsidy about 80% Individual about 20% |

| Variable | Setting | Total (n = 2773) | 2009 (n = 686) | 2011 (n = 1045) | 2015 (n = 1042) |

|---|---|---|---|---|---|

| Insurance type | UEBMI | 619 (22.32) | 114 (16.61) | 257 (24.59) | 248 (23.80) |

| URBMI | 450 (16.23) | 60 (8.75) | 229 (21.92) | 161 (15.45) | |

| NRCMS | 1704 (61.45) | 512 (74.64) | 559 (53.49) | 633 (60.75) | |

| Gender | Male | 1171 (42.23) | 287 (41.84) | 437 (41.82) | 447 (42.90) |

| Female | 1602 (57.77) | 399 (58.16) | 608 (58.18) | 595 (57.10) | |

| Age (years) | 18~44 | 516 (18.60) | 161 (23.47) | 217 (20.77) | 138 (13.24) |

| 45~59 | 976 (35.20) | 250 (36.44) | 388 (37.12) | 338 (32.44) | |

| ≥60 | 1281 (46.20) | 275 (40.09) | 440 (42.11) | 566 (54.32) | |

| Marital status | Other | 448 (16.16) | 113 (16.47) | 174 (16.65) | 161 (15.45) |

| Married | 2325 (83.84) | 573 (83.53) | 871 (83.35) | 881 (84.55) | |

| Employment | No | 1634 (58.93) | 327 (47.67) | 595 (56.94) | 712 (68.33) |

| Yes | 1139 (41.07) | 359 (52.33) | 450 (43.06) | 330 (31.67) | |

| Education | ≤Primary school | 1304 (47.02) | 391 (57.00) | 453 (43.35) | 460 (44.15) |

| Middle school | 1171 (42.23) | 248 (36.15) | 469 (44.88) | 454 (43.57) | |

| ≥Technical school | 298 (10.75) | 47 (6.85) | 123 (11.77) | 128 (12.28) | |

| Family size | ≤2 | 902 (32.52) | 226 (32.94) | 308 (29.47) | 368 (35.32) |

| 3–4 | 1098 (39.60) | 244 (35.57) | 455 (43.54) | 399 (38.29) | |

| ≥5 | 773 (27.88) | 216 (31.49) | 282 (26.99) | 275 (26.39) | |

| Household income per capita | Poorest | 546 (19.69) | 177 (25.80) | 196 (18.76) | 173 (16.60) |

| Poorer | 550 (19.83) | 192 (27.99) | 208 (19.90) | 150 (14.40) | |

| Medium | 579 (20.88) | 173 (25.22) | 210 (20.10) | 196 (18.81) | |

| Richer | 551 (19.87) | 95 (13.85) | 236 (22.58) | 220 (21.11) | |

| Richest | 547 (19.73) | 49 (7.14) | 195 (18.66) | 303 (29.08) | |

| Supplementary insurance | No | 2661 (95.96) | 665 (96.94) | 986 (94.35) | 1010 (96.93) |

| Yes | 112 (4.04) | 21 (3.06) | 59 (5.65) | 32 (3.07) | |

| Severity of illness | Not severe | 872 (31.44) | 236 (34.40) | 317 (30.34) | 319 (30.61) |

| Somewhat severe | 1540 (55.54) | 353 (51.46) | 594 (56.84) | 593 (56.91) | |

| Quite severe | 361 (13.02) | 97 (14.14) | 134 (12.82) | 130 (12.48) | |

| Medical institution level | Clinic | 1163 (41.94) | 314 (45.77) | 424 (40.58) | 425 (40.79) |

| Township/community health centers | 565 (20.38) | 123 (17.93) | 228 (21.82) | 214 (20.54) | |

| County hospitals | 396 (14.28) | 115 (16.76) | 143 (13.68) | 138 (13.24) | |

| Municipal hospitals and above | 649 (23.40) | 134 (19.54) | 250 (23.92) | 265 (25.43) | |

| Service type | Outpatient | 2408 (86.84) | 608 (88.63) | 915 (87.56) | 885 (84.93) |

| Inpatient | 365 (13.16) | 78 (11.37) | 130 (12.44) | 157 (15.07) | |

| Diagnosed by doctor | No | 274 (9.88) | 45 (6.56) | 75 (7.18) | 154 (14.78) |

| Yes | 2499 (90.12) | 641 (93.44) | 970 (92.82) | 888 (85.22) |

| Type | 2009 | 2011 | 2015 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Median | IQR | Median | IQR | Median | IQR | ||||

| P25 | P75 | P25 | P75 | P25 | P75 | ||||

| UEBMI | 950 | 210 | 3750 | 340 | 100 | 1700 | 450 | 100 | 3230 |

| URBMI | 480 | 90 | 1100 | 225 | 90 | 600 | 300 | 78 | 1500 |

| NRCMS | 101 | 31.5 | 750 | 205 | 40 | 1350 | 400 | 64 | 1890 |

| p-value | <0.001 | 0.007 | 0.393 | ||||||

| Type | 2009 | 2011 | 2015 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Median | IQR | Median | IQR | Median | IQR | ||||

| P25 | P75 | P25 | P75 | P25 | P75 | ||||

| UEBMI | 280 | 127.5 | 1000 | 218 | 89 | 640 | 180 | 80 | 800 |

| URBMI | 90 | 36 | 480 | 180 | 80 | 425 | 187.5 | 60 | 350 |

| NRCMS | 70 | 22.5 | 153 | 91 | 30 | 335 | 130 | 40 | 500 |

| p-value | <0.001 | <0.001 | 0.038 | ||||||

| Type | 2009 | 2011 | 2015 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Median | IQR | Median | IQR | Median | IQR | ||||

| P25 | P75 | P25 | P75 | P25 | P75 | ||||

| UEBMI | 3825 | 1995 | 5300 | 4000 | 1600 | 8000 | 4550 | 1700 | 8400 |

| URBMI | 1230 | 600 | 2400 | 3770 | 480 | 6800 | 5100 | 2800 | 8400 |

| NRCMS | 1320 | 420 | 2730 | 1700 | 850 | 3600 | 3200 | 1350 | 5700 |

| p-value | <0.001 | 0.011 | 0.131 | ||||||

| Model Specification | Logit | Ordinary Least Squares | ||||

|---|---|---|---|---|---|---|

| 2009 | 2011 | 2015 | 2009 | 2011 | 2015 | |

| URBMI | −0.951 ** | −0.219 | −0.191 | −0.653 * | −0.193 | −0.0700 |

| (−2.25) | (−0.94) | (−0.77) | (−1.79) | (−1.08) | (−0.31) | |

| NRCMS | −1.165 *** | −0.111 | −0.741 *** | −0.711 ** | −0.173 | −0.0913 |

| (3.65) | (−0.47) | (−3.40) | (−2.55) | (−0.81) | (−0.42) | |

| Somewhat severe | −0.0548 | 0.0285 | −0.0891 | 0.722 *** | 0.468 *** | 0.351 * |

| (−0.26) | (0.17) | (−0.53) | (3.30) | (2.93) | (1.95) | |

| Quite severe | 0.115 | 0.556 ** | 0.210 | 1.047 *** | 1.166 *** | 0.849 *** |

| (0.35) | (2.00) | (0.75) | (3.63) | (5.17) | (3.31) | |

| Township/community health centers | 1.328 *** | 1.221 *** | 0.987 *** | 0.381 | −0.0789 | −0.188 |

| (5.17) | (6.14) | (5.06) | (1.44) | (−0.42) | (−0.88) | |

| County hospitals | 1.067 *** | 0.381 | 0.808 *** | 1.571 *** | 0.961 *** | 0.946 *** |

| (3.76) | (1.62) | (3.30) | (5.47) | (4.19) | (3.88) | |

| Municipal hospitals and above | 0.215 | 0.886 *** | 0.322 | 1.613 *** | 1.040 *** | 0.984 *** |

| (0.70) | (3.92) | (1.53) | (5.27) | (5.17) | (4.37) | |

| Inpatient | 3.354 *** | 2.251 *** | 2.957 *** | 1.573 *** | 1.926 *** | 2.035 *** |

| (6.61) | (6.97) | (7.92) | (6.96) | (10.78) | (10.64) | |

| Supplementary insurance | −0.854 | 0.525 | 0.584 | −0.926 | −0.139 | −0.625 |

| (−1.21) | (1.52) | (1.37) | (−1.24) | (−0.53) | (−1.63) | |

| Diagnosed | 0.529 | 0.674 ** | 0.378 * | 0.0483 | 0.468 | 0.704 *** |

| (1.22) | (2.12) | (1.78) | (0.09) | (1.36) | (2.60) | |

| N | 686 | 1045 | 1042 | 241 | 526 | 516 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dong, W.; Zwi, A.B.; Bai, R.; Shen, C.; Gao, J. Benefits Associated with China’s Social Health Insurance Schemes: Trend Analysis and Associated Factors Since Health Reform. Int. J. Environ. Res. Public Health 2021, 18, 5672. https://doi.org/10.3390/ijerph18115672

Dong W, Zwi AB, Bai R, Shen C, Gao J. Benefits Associated with China’s Social Health Insurance Schemes: Trend Analysis and Associated Factors Since Health Reform. International Journal of Environmental Research and Public Health. 2021; 18(11):5672. https://doi.org/10.3390/ijerph18115672

Chicago/Turabian StyleDong, Wanyue, Anthony B. Zwi, Ruhai Bai, Chi Shen, and Jianmin Gao. 2021. "Benefits Associated with China’s Social Health Insurance Schemes: Trend Analysis and Associated Factors Since Health Reform" International Journal of Environmental Research and Public Health 18, no. 11: 5672. https://doi.org/10.3390/ijerph18115672

APA StyleDong, W., Zwi, A. B., Bai, R., Shen, C., & Gao, J. (2021). Benefits Associated with China’s Social Health Insurance Schemes: Trend Analysis and Associated Factors Since Health Reform. International Journal of Environmental Research and Public Health, 18(11), 5672. https://doi.org/10.3390/ijerph18115672