3.1. Historical Agribusiness Trajectories

Tobacco was first introduced in Mozambique in colonial times by Portuguese traders and was traditionally grown by African peasants for domestic consumption. At the beginning of the 20th-century, tobacco became a commodity in Mozambique that could be exchanged for clothing and other consumer goods on the market as well as a source of income to pay mussoco, the colonial tax. The districts of Malema and Ribàué in the province of Nampula, today is known as two of the most agriculturally productive districts in the country, became the center of tobacco production in settlers’ farms, a production that reached an average of approximately 3000 tons per annum at that time. Without agricultural assistance or access to credit, the relative success of tobacco production was largely dependent on the mobilization of forced labor for Portuguese farms. Navohola [

12] calculated that in 1948 most of the workers came to work on the tobacco plantations through chibalo (forced labor during the colonial regime) in Ribàué and Malema. However, the volumes produced were limited, and Mozambique was a net tobacco importer, mainly from Angola and the USA [

7]. Between 1941 and 1960, tobacco production increased, and the land-used to grow tobacco expanded. Those charged with the colonial agricultural strategy began to take an interest in ensuring that local production grew to replace imports and to supply the Portuguese metropolis.

Prior to obtaining independence from the Portuguese regime in 1975, tobacco farms flourished in central Mozambique due to the inexpensive forced labor and expropriated land [

13]. Tobacco cultivation continued, mainly in the nationalized state farms of Manica and Nampula. In the following decade after independence, however, state tobacco farms were malfunctioning due to the impact of the civil war in 1977, which aggravated problems of poor coordination and mobilization. Aspects such as prices, financing and conditions for recruiting labor were managed by central authorities in many cases, not effectively managing problems that arose. As a result, the state initiated the selling of state farms in 1985, selling over 40,000 acres of land to the private sector by 1993 [

7]. In the period following the end of the civil war, tobacco cultivation expanded in Mozambique in terms of production volume and was also introduced in provinces and districts where it had not previously been cultivated. In contrast to the colonial period, and in which commercial tobacco production had been restricted to state farms, after independence, tobacco was adopted mainly by Mozambican farmers using family labor and private land [

7]. After the civil war that took place immediately after independence and following the process of divestment of state farms and the reform of seed supply organizations, producers who needed credit and assistance for the production of cash crops had to stop production due to the lack of capital and underdevelopment of local private credit unions. In order to deal with the existing bottleneck caused by the lack of financing and access to markets, a variation of the old system of concessions was adopted, this time in the form of interconnected input and production markets, in which cash crop traders provided credit to producers. In some regions of Mozambique, and for cultures such as tobacco and cotton, the only channel of access to credit assistance was the private sector [

7]. The largest distribution of private credit and extension services in Mozambique in the past few years has been for tobacco producers. According to a recent survey from the Ministry of Agriculture and Rural Development, in 2017, only 2 percent of non-tobacco-producing farmer households had access to credit compared to 21.7 percent of tobacco-producing farmer households [

14].

3.2. Current Country Context

The Republic of Mozambique is located in South-East Africa and is utilized by neighboring landlocked countries to access external markets. Mozambique has a population of 28.9 million, of which 84.9% are active in the formal economy. Smallholder farmers (SHFs) account for 86.2% of the rural population. Mozambique’s arable land accounts for about 36 million acres, and agriculture accounts for up to 80% of the nation’s economic workforce, though it only accounts for 25% of the nation’s GDP [

15]. In this context, accounting for over a quarter of the total export value of agricultural commodities in Mozambique, tobacco is considered to be one of the country’s most important cash crops. The tobacco industry in Mozambique contributes to more than 1.9 billion

Meticais annually in tax revenue to the state [

16].

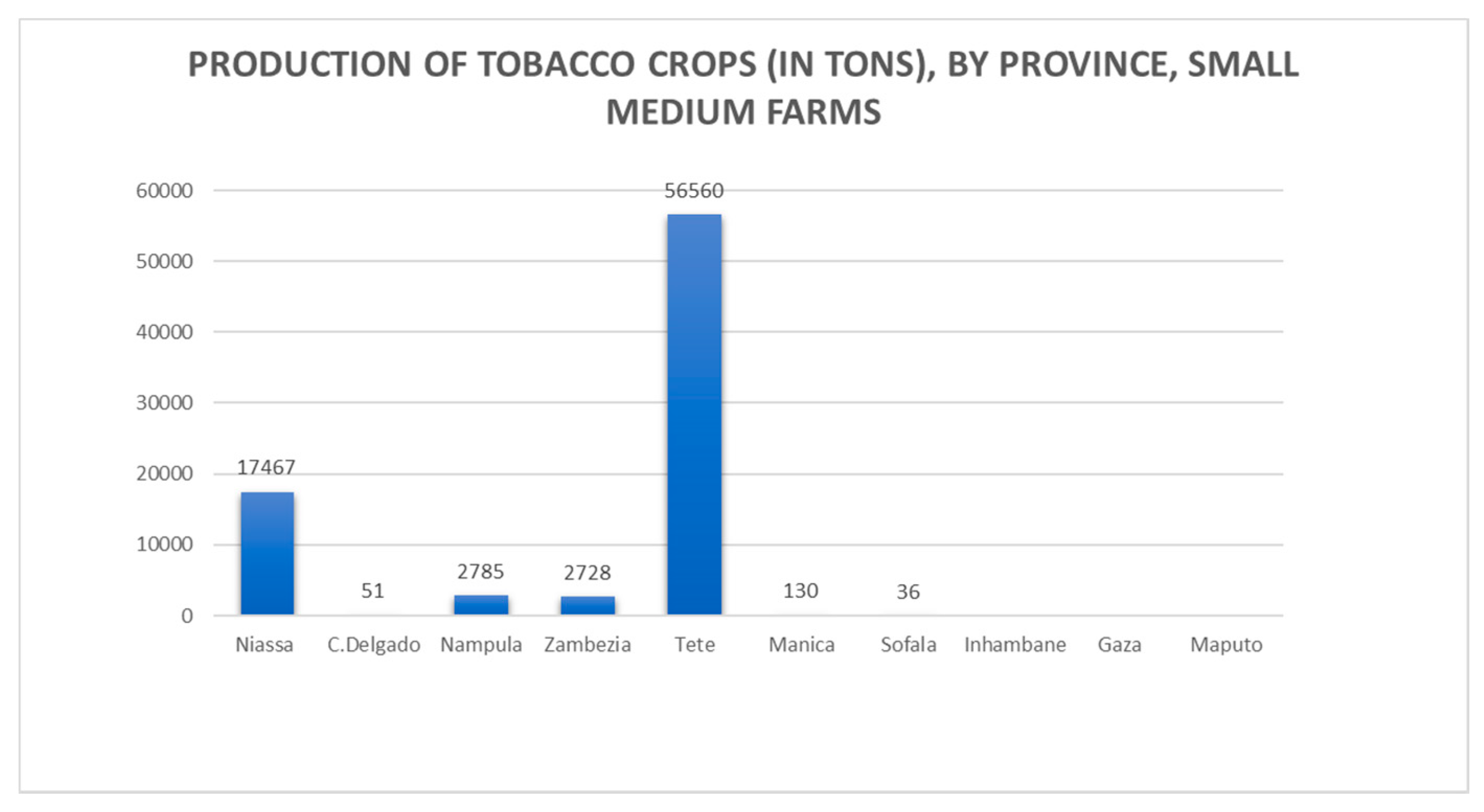

With roughly 98% of tobacco being produced by SHFs [

9], the crop is grown in a concession system with Mozambique Leaf Tobacco (MLT), a local subsidiary of the multinational Universal Corp [

17]. The company operates in four provinces in central and northern Mozambique: Zambézia, Manica, Niassa, and Tete (See

Figure 2 for production by province).

Between 72,000 and 124,000 households grow tobacco out of 3.9 million farming households total nationwide, with higher concentrations of tobacco farmers in the Tete and Niassa provinces, which together in 2017 accounted for approximately 78% of the total number of growers. The total number of farmers varies considerably annually, however, and data from national agricultural surveys conducted by MADER show a consistent decline in Zambézia where alternative livelihoods have been promoted. The export data presented in

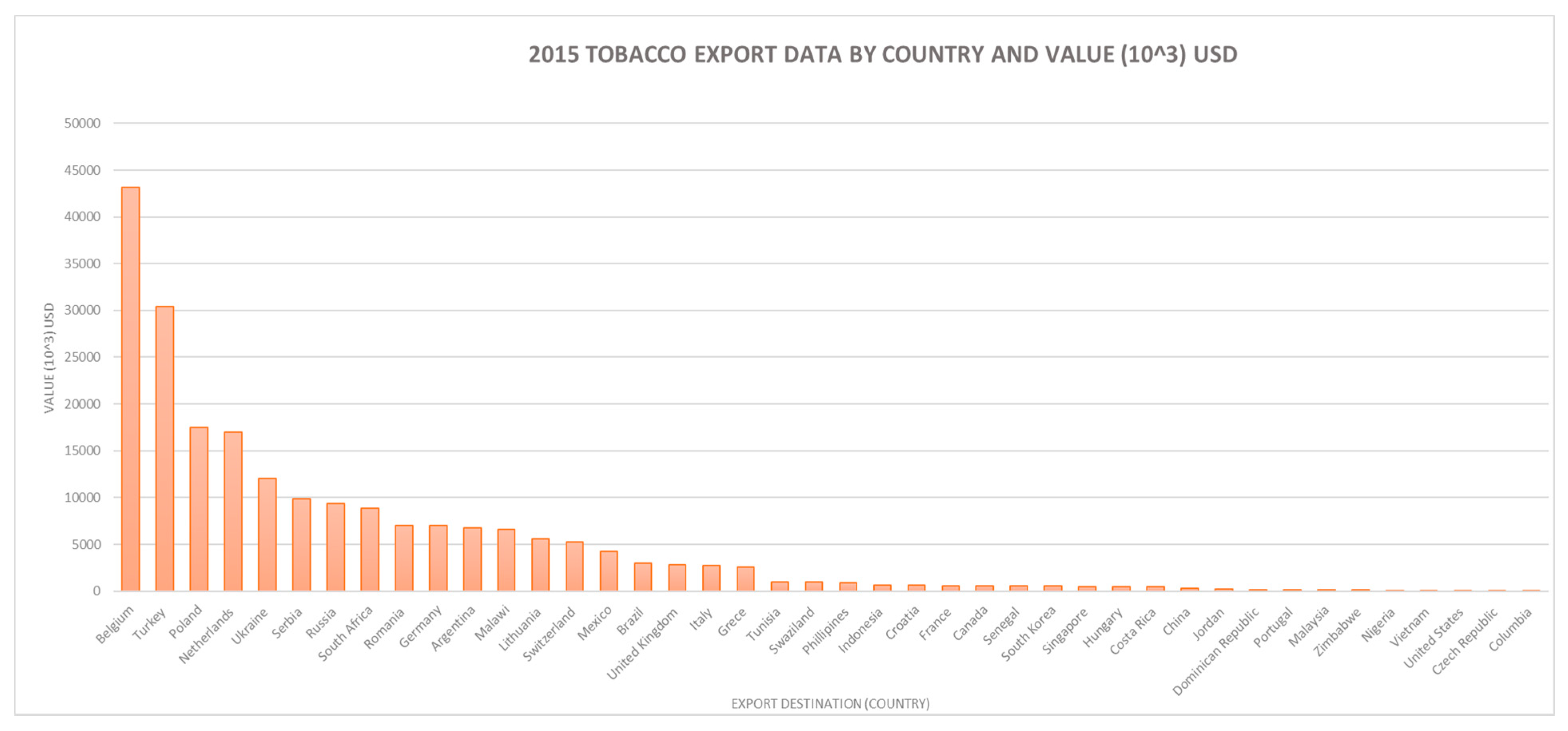

Figure 3 illustrates that, as of 2015, Mozambique had a diverse international market for raw tobacco, with Belgium, Turkey, Poland, Netherlands and Ukraine having the highest tobacco export values.

According to data from the Ministry of Agriculture [

19], which also measured data for other cash crops, such as cotton, sugarcane, sunflower, sesame and soy, most medium to small holdings that produced tobacco sold 100 percent of their crop, with the exception of Cabo Delgado and Tete, reflecting the crop’s high demand, and possibly, an efficient supply chain (

Figure 4).

3.3. Production Incentives for Smallholder Farmers

In addition to job creation opportunities and high demand from a diverse market, the incentives of tobacco production, specifically for rural smallholder household welfare and farming systems, have been plentiful. Data by the national agricultural sample survey (TIA) in 2002 revealed that at the time, the incomes of tobacco growers were much higher than those who did not produce tobacco [

20]. In the same study, controlling for a set of characteristics including the gender of household head, age, and education, researchers compared the total household income of tobacco smallholders to those who do not grow tobacco and did the same for those who grow cotton as a cash crop. The results demonstrated that this period saw a rise in income of SHFs who grew tobacco, about 29% higher than that of non-growers, while the income of cotton growers was only 5% higher than those that did not farm it. Given the high involvement of family labor in tobacco growing, this figure likely does not reflect the true profit of tobacco growing in relation to other crops, given that the analysis did not account for household labor. The findings also indicated that tobacco SHFs were less likely to be poor and to show improvement in their well-being over the past 3 years compared to households that did not grow tobacco. Preliminary empirical data suggests that the additional income from sales, as well as the additional fertilizer residuals left in the soil from tobacco production, can improve food security [

21,

22]. The additional income garnered from tobacco sales as well as effective agricultural practices, such as crop rotation, has increased the productivity of maize after tobacco production. In general terms, tobacco producers tend to benefit from better access to extension services, including inputs, pesticides and fertilizer, which tends to contribute to the positive yields, including that of non-tobacco crops. The combined direct and indirect effects of tobacco production are stated as one of the reasons why Tete province managed to achieve the fastest rate of increase in rural household incomes in Mozambique in the few years following 1996 [

21]. Access to such services for tobacco producers were of national interest and in alignment with the Strategic Plan for Agrarian Sector Development 2011–2019 (PEDSA, in Portuguese) [

23]. To support the implementation of the PEDSA, there are additional strategic documents that operationalize the PEDSA, including the Agricultural Livestock Marketing Integral Plan (PICA, in Portuguese) [

24] and Agricultural Sector National Investment Plan (PNISA, in Portuguese) [

25]. We have included a

Supplemental Table S1 highlighting the political framework listing relevant agricultural policies/programs (2000–onwards), including policies that promote tobacco.

3.4. Regulation and the Tobacco Market

Tobacco production in Mozambique is regulated by the Tobacco Promotion, Production and Marketing Regulation (Ministerial Diploma 176/2001) [

26] and by the contracts established between the national government and the tobacco concession companies. This concessionary system was implemented after the divestment of state farms. The Tobacco Regulation sets out the principles that govern concessions and establishes the role of the various stakeholders involved. The Mozambican model is composed of three interrelated elements: (1) the interconnected input and production markets, (2) a production scheme under contract as the predominant form of production, and (3) the adoption of monopsonistic territorial concessions.

The first of these elements, the interconnection between the input and production markets, served as a solution to the lack of credible sources for agricultural producers [

27,

28]. The background to this situation was that traditional financial institutions were unable to offer commercial credit to producers because the small scale of the credit that farmers asked for increased overall transaction costs; the lack of markets prevented the use of land as collateral generally, and debts were difficult to collect. One way around this problem was for agricultural traders to directly offer producers credits for production and deduct payments when buying the harvest. Unlike banks, agricultural traders have a direct link with producers, and traders would thus benefit from improved quality and production generated by access to agricultural credit. Therefore, the interconnected markets allow the use of the future harvest as a guarantee for the repayment of production credit [

28]. To this end, traders sign production contracts with each of the producers, in which they advance in-kind credit in the form of inputs for production (seeds, fertilizer, pesticides and other production materials) and commit to buying the final product, even though often not all the tobacco is purchased leaving farmers with a surplus. At the time of the purchase, the merchant deducts the initial credit amount from the payment the farmer receives for tobacco. Competition between companies creates an incentive for traders to offer attractive prices to producers to whom they have not provided credits, taking advantage if so, free of charge, of the lenders’ investment. With alternative buyers, the interconnected markets have higher rates of strategic default, as has been documented in the case of the cotton sectors in Ghana and Mozambique [

28,

29]. To avoid the negative effects of strategic non-compliance, some county governments have opted for the creation of territorial concessions, in which traders receive concessions in different regions, eliminating competition between operators [

7].

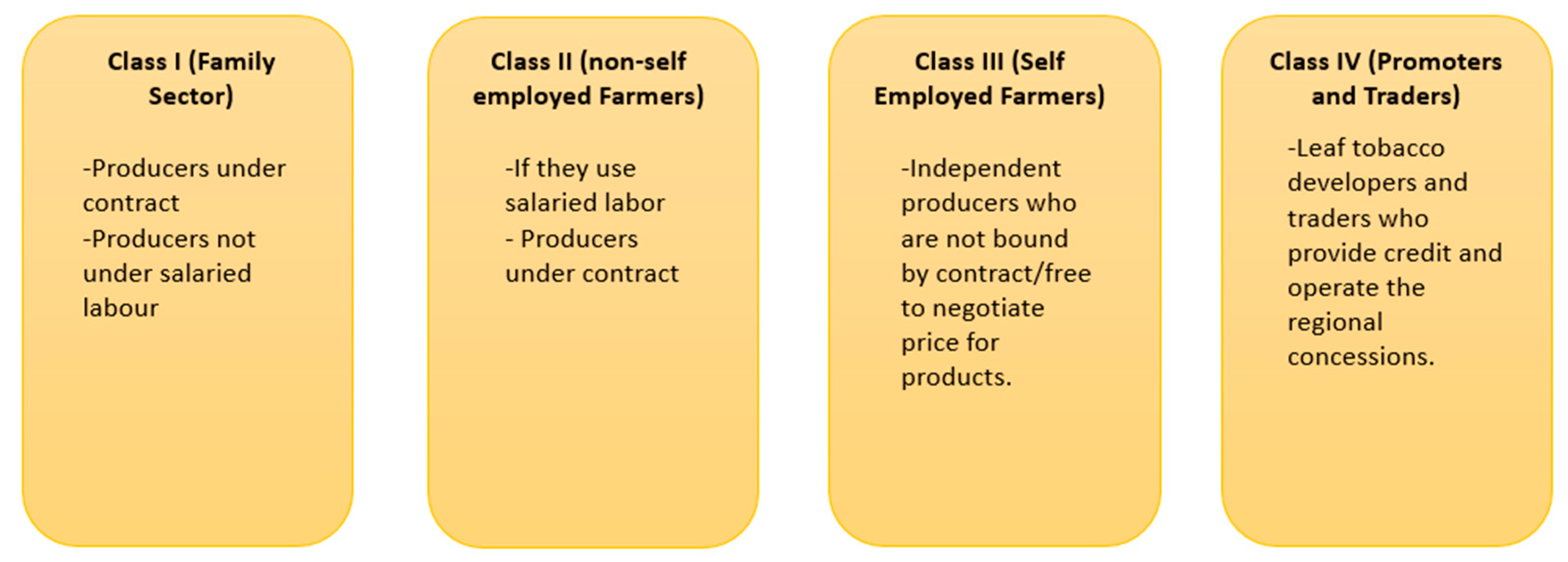

In 2005, there were about 129,000 agricultural producers with tobacco production contracts. Of these, there were 34,813 producers in Niassa and 43,464 in Tete. MLT was the main buyer and had concessions in Tete and Manica. According to the 2001 Tobacco Regulation, under article 2, there are four classes of economic operators in the tobacco production space (see

Figure 5 for classification details): Class I (family sector), Class II (non-self-employed farmers), Class III (self-employed farmers) and Class IV (promoters and traders). Producers engaged in agriculture under contract are classified in “Class I” if they do not use salaried labor and in “Class II” if they do. Independent farmers who are not bound by production contracts and are free to negotiate the price for their products are part of “Class III,” and leaf tobacco developers and traders who provide credit and operate the regional concessions comprise “Class IV”. Tobacco trading companies of “Class IV” apply annually to renew their concessions to the Provincial Directorates of Agriculture. Operators must submit a production proposal and specify inputs, investment and reforestation plans, as well as a final execution report after the harvest and the marketing season. Contract signatories are strictly prohibited from selling their tobacco to third parties not included in the contract. Tobacco sold outside the contract can be confiscated and handed over to its legitimate dealer in accordance with Ministerial Diploma 176/2001. Tobacco is sold by farmers at different price levels, with “premium price” being the highest. In Mozambique, the price set by the largest tobacco concessionaire, MLT, for the purchase of tobacco from SHFs is automatically never sold at a premium price and therefore is, by default, set to sell at lower prices [

30].

In all tobacco producing districts, it is stipulated that an arbitration committee must be formed, with representatives of all producers, buyers, district government and community, to resolve differences between farmers and companies regarding the sorting, classification and marketing of tobacco. The MADER has an inspection body to ensure compliance with the tobacco regulation by all parties. By the mid-1990s, there were 8 main companies in the tobacco trading space in Mozambique, including DIMON, STANCOM, MLT, SONIL, JFS, Mosagrius, as well as two joint venture companies, Shancom and Stancom. Three large multinational tobacco trading companies, Dimon Inc., Stancom and MLT (the local subsidiary of Universal Corp.), started operating in Mozambique in the mid-1990s, joining companies such as JFS and SONIL, which have worked in Mozambique since the colonial period but were new to the tobacco trade. Stancom was present in Manica, and as a subcontractor for SONIL and Mosagrius, in both Niassa and Cabo Delgado province. Dimon worked in Tete, Manica and Sofala. The other major player, JFS, was a Portuguese Mozambican business group with tobacco and cotton contracts in Nampula, Niassa and Cabo Delgado province [

7]. Although the Mozambican model started with several operators as described above, in 2006, it was reduced to a de facto national monopoly, in which a single company, Universal’s subsidiary MLT, dominates the purchase and processing of tobacco leaf, although marginal traders remain.

The mid-2000s marked a turning point in the trajectory of the tobacco market in Mozambique. There were three developments that determined, from then on, the evolution of the sector: technological developments such as the creation of a processing factory in Tete province, which ended the need to send raw tobacco to Malawi for processing; the withdrawal of the Chifunde concession, which led to the departure of Dimon Inc. from Mozambique; and the failure of tobacco production in the province of Manica. In the early 2000s, tobacco from Mozambique had a consolidated presence in the international market, but it had to be exported to Malawi or Zimbabwe, to be processed, and reexported through the port of Beira city in Sofala province since there were no processing facilities in Mozambique. This resulted in additional transport costs and loss of revenue. An internal proposal was studied at the MADER to introduce an export tax of 20% on the value of raw tobacco to force commercial companies to invest in a leaf-cutting infrastructure in Mozambique [

21].

An internal document from 2004, prepared by the National Directorate of Agrarian Services of MADER was quoted by Benfica and colleagues [

21] and argued that this tax would lead buying companies to invest in processing facilities and thus create job opportunities and new sources of tax revenue from the income tax paid for additional processing labor. The export tax proposal, however, had a more complex context. In February 2003, MLT, the largest purchasing concessionaire, had started the construction of a 50 million USD processing unit in Tete province, with a capacity to process 50 thousand tons per year [

21]. Considering that MLT was, at the time, the biggest buyer and that total production in 2003 was 37,051 tones, it is likely that MLT wanted to ensure that the installed capacity would not be underutilized. Other tobacco companies did not buy tobacco on a scale that justified the installation of processing infrastructure. The introduction of an export tax in this context would have forced all tobacco producers to process tobacco at the unit built by MLT. The MLT processing unit was opened in 2006, and the export tax policy ended, but in 2005, the government announced that the tobacco concession in Chifunde, in Tete province, would be transferred from Dimon, at that time already merged with Alliance One, to MLT. Chifunde was the largest concession controlled by Alliance One, and its loss jeopardized the viability of its work in Mozambique. In May 2006, Alliance One announced that it would abandon all its concessions as of the 2007 agricultural season and began to close activities invoking political interference. At the time, 500 direct workers lost their jobs, although many ended up being reabsorbed by MLT. The decision to transfer the concession to MLT was initially seen as a reward for the willingness to invest in processing [

31,

32]. Only in 2010 did it go public that the MLT was behind the proposed export tax and the transfer of the Chifunde concession. In the following years, Mozambique stopped exporting raw tobacco material to neighboring countries for processing and became a country that exported processed tobacco ready to send for cigarette manufacturing. Additionally, Mozambique no longer has the initial eight registered companies, as only two, MLT and SONIL, remain in-country [

7].

In 2019, a media source published that China was due to import approximately 60,000 tons of tobacco from Mozambique until February 2020, making them the second-largest tobacco importer. Mozambique’s current President, Filipe Nyusi, stated that the sale of these products would improve the livelihood of local farmers [

33]. To confirm where this is, in fact, true requires further research. To date, there have not been any publications analyzing the economic livelihoods of tobacco farmers after this new market for tobacco leaf grown in Mozambique. Findings from Zimbabwe suggest that the China National Tobacco Company has renewed and facilitated the expansion of tobacco growing there [

34,

35]. It is likely that CNTC could have a similar impact in Mozambique.

3.5. Alternative Cash Crops for Farmer Livelihoods

As stated in earlier sections, the general consensus for producing tobacco is to improve farmer livelihoods. Although cotton and tobacco have a long history as cash crops in Mozambique, there are other cash crops that have recently been introduced to farmers. Soybeans are one example of a crop grown as an alternative to tobacco. The percentage of growers of tobacco at the national level declined slightly (

Table 1) as farmers embraced new alternatives. TechnoServe, funded by the Embassy of the Kingdom of the Netherlands (EKN), implemented the Seed Multiplication project to Empower Small Commercial Farmers (SM4ESCF) from 1 March 2016 to 31 January 2019. The overall objective of the project was to increase the productivity and profitability of SHFs and small commercial farmers (SCFs) in Zambézia Province, resulting in financial benefits for these rural farming communities. Specifically, the project sought to build a strong and sustainable local seed and service provider network in Upper Zambézia.

The project invested heavily in extension services, machinery, post-harvesting technologies, and a seed factory. In 2002 about 3.5% of farmers in Zambezia cultivated tobacco, and no one grew soybeans. By 2017 the percentage of tobacco growers in Zambezia had declined to 0.8%, and there was a shift to soybean production (0% in 2002; 4.6% in 2017) attributed to the guaranteed market for soybean seeds, which, unlike tobacco, sells at a premium price at the factory, and due to demand for soybean that is sold to the poultry industry both locally and in neighboring Malawi. As previously stated, the tobacco contribution to farmer livelihoods in Mozambique is unknown. From both a public health and economic perspective, the cash crops outlined in

Table 1 could be explored as healthier alternatives to tobacco, especially since there is a guaranteed market for some of these crops. Additionally, in accordance with the agricultural operational marketing plans (2018) developed by the Government for Zambézia province, the production of these alternative crops, such as sunflower, sesame and cotton, is, indeed, of government interest.

3.6. Tobacco Control (Ministry of Health)

The Ministry of Health, under the mental health department, has outlined tobacco control strategies in both national decrees and strategic documents. Under the decree for Consumption and Commercialization of Tobacco (Decree 11/2007), there are various limitations relating to the commercialization, consumption, as well as demand and supply reduction for tobacco, including the banning of partnerships/cooperation between tobacco companies and public health campaigns of any kind (Article 13). Relevant articles limiting the supply and sales of tobacco under Decree 11/2007 include Article 10, which explicitly prohibits the sale and publicity of tobacco in various establishments, including, but not limited to, health, education and public administration institutions; and Article 12, which prohibits the sale of tobacco products to minors (anyone under the age of 18). Relevant articles to decrease tobacco demand include the following: Article 3 provides for a modest increase in tobacco taxes; Articles 7 and 8, which outlaw general tobacco advertising as well as false marketing that outline false benefits related to tobacco; and lastly, Article 9, which highlights demand reduction measures related to tobacco dependence and cessation as the focus.

A common government interest that has been consistent in the decree and later translated in relevant national strategic documents concerning tobacco is the importance of awareness-raising of the negative impacts of tobacco use to the general public. Key policy documents including the Strategic Plan for the Health Sector (2014–2019) [

36], National Strategic Plan for the Prevention and Control of Non-Communicable Disease (2008–2014) [

37], National Plan for Cancer Control (2019–2029) [

38] and the Mental Health Action Plan and Strategy (2007–2015) [

39] have awareness-raising activities in relation to tobacco use included in their narratives and/or strategic objectives. In accordance with the indicators highlighted in the policy documents, the expected impact is to increase awareness surrounding the risks and negative impacts of tobacco.

The concessionaire that dominates the growing and processing of tobacco in Mozambique, MLT, has various social corporate responsibility programs. However, most are related to discouraging child labor practices, enhancing good agricultural labor practices, financial literacy, and increasing access to clean water. The program most related to tobacco control policy in Mozambique is an HIV program [

17], due to the fact that it also focuses on tuberculosis as tobacco smoking often causes health problems in tuberculosis patients. However, it is unclear whether the messaging is around tobacco control, and while tuberculosis awareness seems to be a component of the program, it is not its central focus.

According to the government officials responsible for leading the multi-sectoral tobacco control working group under the Ministry of Health, and the mandate of the National Inspection of Economic Activities (INAE, in Portuguese), INAE ensures that all economic activities are completed in compliance with the law in order to create a good business environment in the country. INAE has been granted authority to work together with the Ministry of Health, through inspections, in order to ensure that the in-country tobacco control regulations are followed. It is also relevant to highlight that there is not much information about economic sectors taking up tobacco control from the health perspective, nor are there regular inspections by the Health Ministry or in collaboration with INAE to ensure consistent implementation of tobacco control regulations in economic sectors. Therefore, further stakeholder consultations with the private sector are advised to gather more data. In-depth interviews with decision-makers are also needed to explore this dynamic.

Under the auspices of the Ministry of Health, the aforementioned multi-sectorial working group for tobacco control was created to regulate the consumption and commercialization of tobacco in Mozambique. The working group which was mostly responsible for the creation of Decree 11/2007, which aimed to follow the FCTC framework, consists of focal points from all government ministries, civil society, UN (WHO, UNDP) and customs, was formed, and later became functional in 2005 after Mozambique signed the FCTC in 2003. Although Mozambique was indeed a signatory to the convention, it would be years to come until the government officially ratified the FCTC. Being one of the few tobacco-producing countries that had an existing tobacco control instrument prior to the ratification of the convention, the multi-sectoral working group continued to work with decree 11/2007 as a base for tobacco control advocacy, which led to the eventual accession to the FCTC on 2 November 2017. Granted that the ratification of the FCTC was a success, a high-level government official we spoke with emphasized that although the tobacco leaf MLT purchases are intended for exportation, it still returns Mozambique as manufactured cigarettes making them readily available for consumption [

30]. It is also important to note that all neighboring countries have much higher cigarette prices and taxes than Mozambique. Due to this fact, cigarette smuggling out of Mozambique is a common occurrence [

40]. Given the shift of general consumption of tobacco from high-income countries to low and middle-income countries (LMICs); as well as the projection that by 2030 more than 80 percent of the disease burden from tobacco will fall on LMICs [

10], it is important to keep in mind that the supply of tobacco that stems from production may pose potential competing pressures on health sectors goals as it relates to tobacco control not only in Mozambique but in other LMICs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}