An Endowment Effect Study in the European Union Emission Trading Market based on Trading Price and Price Fluctuation

Abstract

1. Introduction

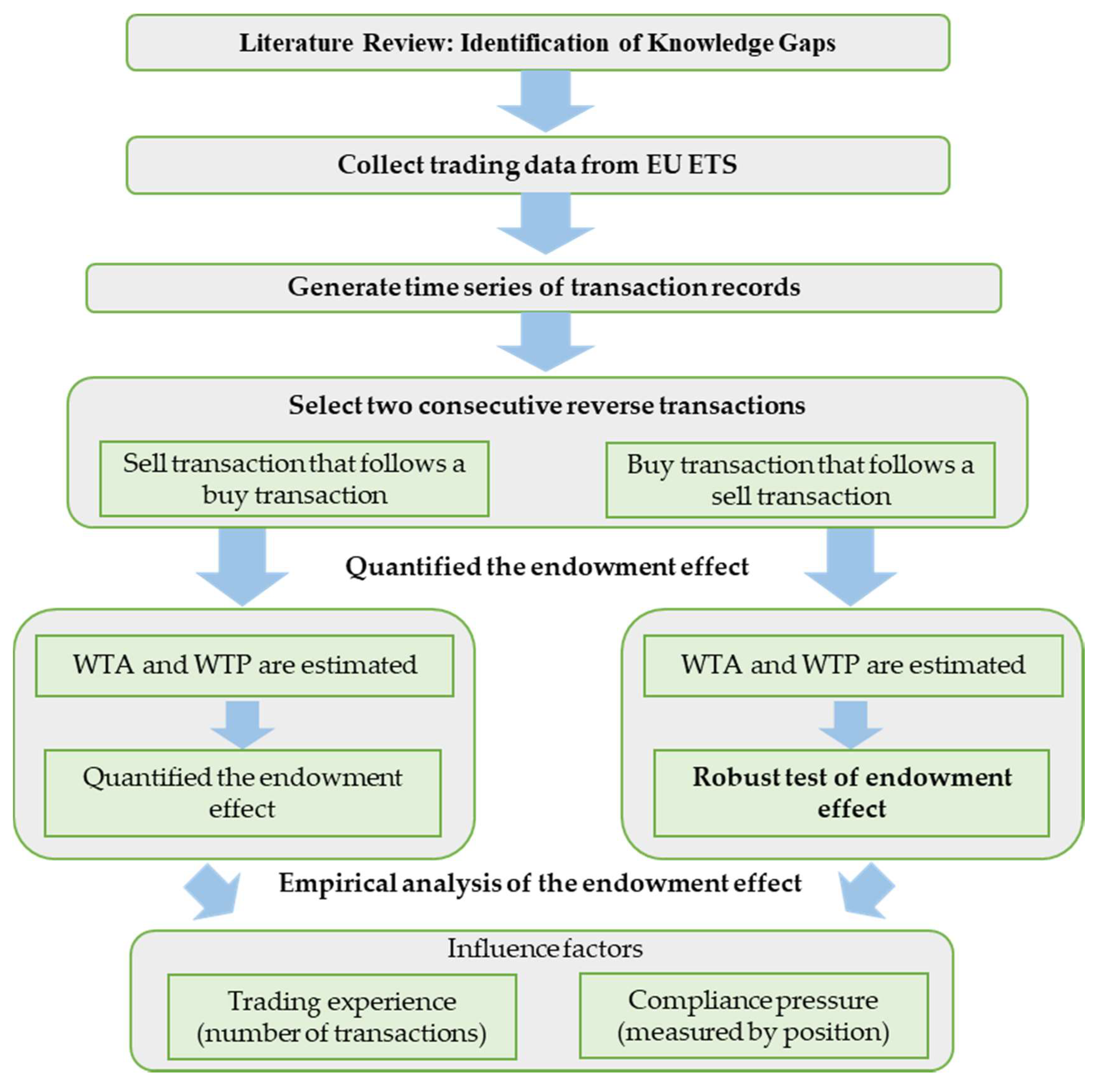

2. Research Framework

3. Data and Methodology

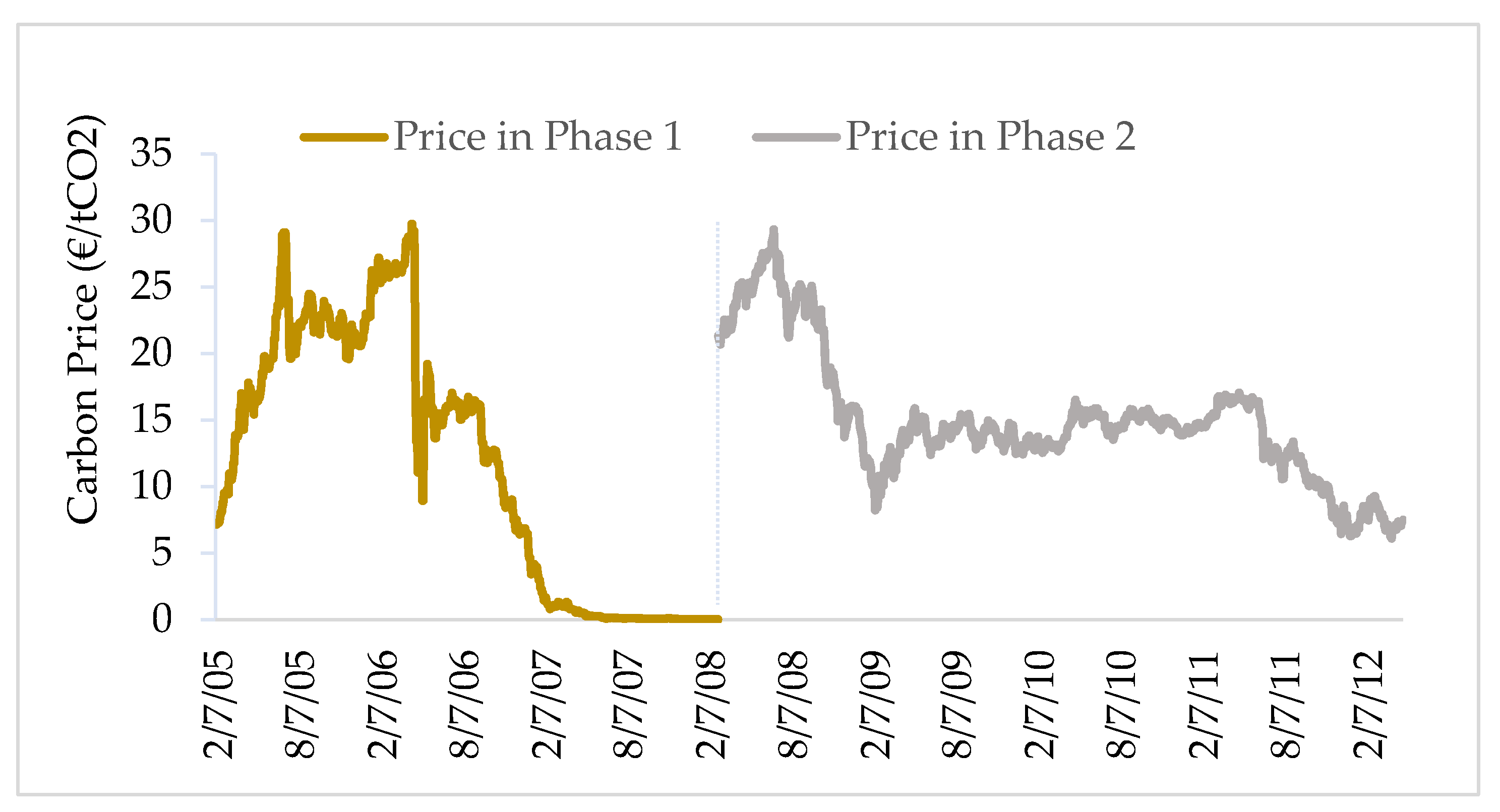

3.1. Data

3.2. Methodology

3.2.1. ARMA-EGARCH Model for Carbon Price

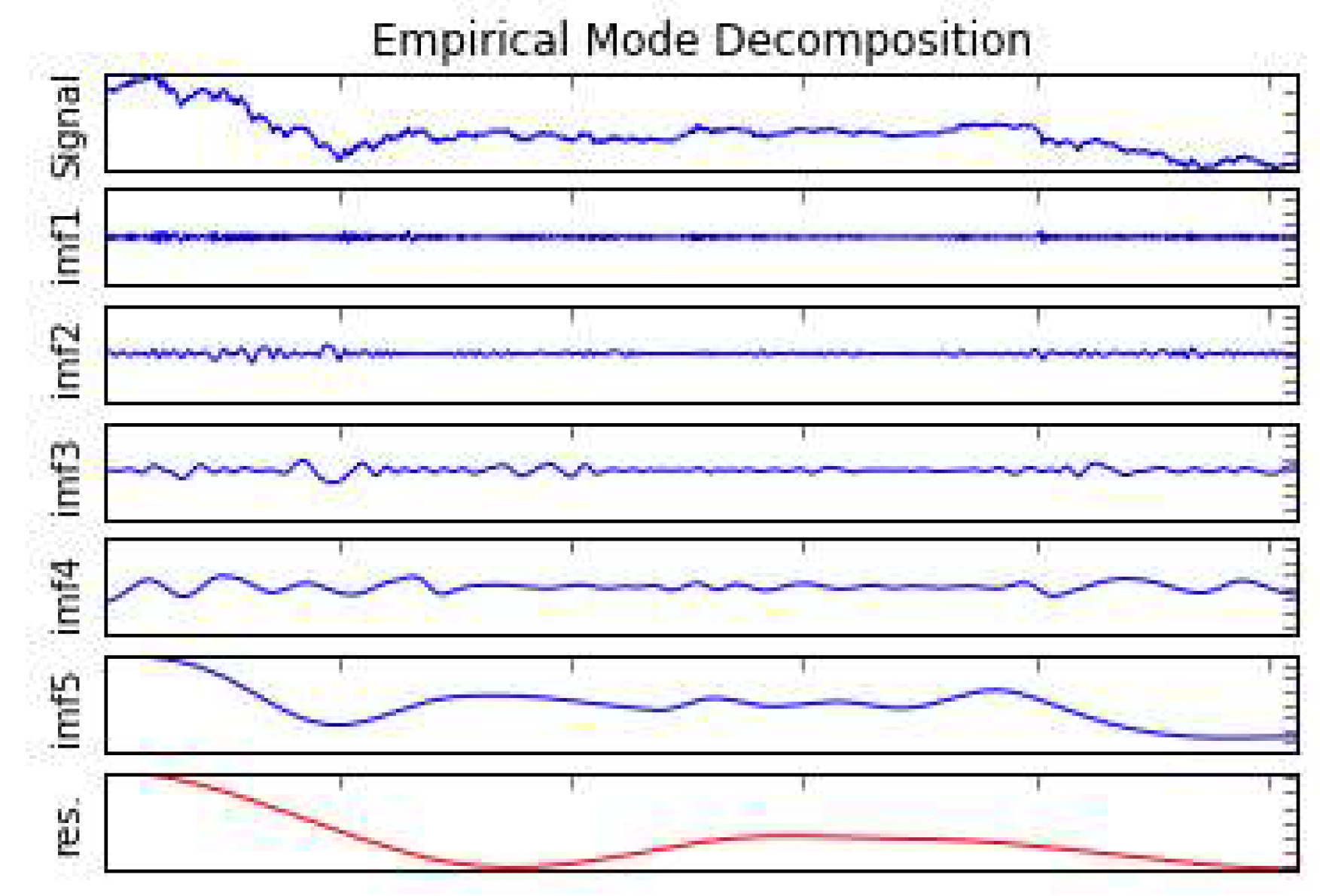

3.2.2. Empirical Mode Decomposition (EMD) Model for Carbon Price

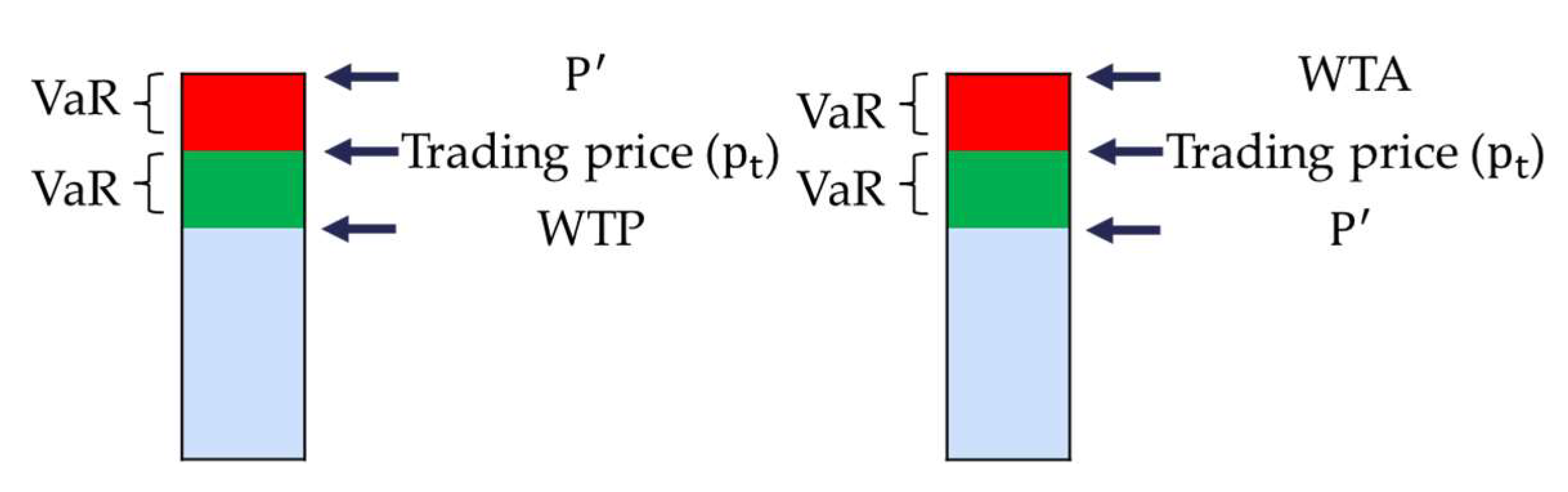

3.2.3. Quantify the Endowment Effect

3.2.4. Model the Influences of Trading Experience and Compliance Pressure on the Endowment Effect

4. Results

4.1. ARMA-EGARCH Results

4.2. EMD Results

4.3. Quantitively Assessed Results of Endowment Effect

4.4. The Influences of Trading Experience and Compliance Pressure on the Endowment Effect

5. Conclusions

Shortcomings and Future Work

Author Contributions

Funding

Conflicts of Interest

References

- Thaler, R. Toward a positive theory of consumer choice. J. Econ. Behav. Organ. 1980, 1, 39–60. [Google Scholar] [CrossRef]

- Shogren, J.F.; Cho, S.; Koo, C.; List, J.; Park, C.; Polo, P.; Wilhelmi, R. Auction mechanisms and the measurement of WTP and WTA. Resour. Energy Econ. 2001, 23, 97–109. [Google Scholar] [CrossRef]

- Loewenstein, G.; Issacharoff, S. Source dependence in the valuation of objects. J. Behav. Decis. Mak. 1994, 7, 157–168. [Google Scholar] [CrossRef]

- Knetsch, J.L.; Sinden, J.A. Willingness to pay and compensation demanded: Experimental evidence of an unexpected disparity in measures of value. Q. J. Econ. 1984, 99, 507. [Google Scholar] [CrossRef]

- Kahneman, D.; Knetsch, J.L.; Thaler, R.H. Experimental tests of the endowment effect and the coase theorem. J. Politi- Econ. 1990, 98, 1325–1348. [Google Scholar] [CrossRef]

- List, J.A. Does market experience eliminate market anomalies? Q. J. Econ. 2003, 118, 41–71. [Google Scholar] [CrossRef]

- List, J.A. Neoclassical theory versus prospect theory: Evidence from the marketplace. Econ. 2004, 72, 615–625. [Google Scholar] [CrossRef]

- Plott, C.R.; Zeiler, K. The willingness to pay—willingness to accept gap, the “Endowment effect,” Subject misconceptions, and experimental procedures for eliciting valuations. Am. Econ. Rev. 2005, 95, 530–545. [Google Scholar] [CrossRef]

- Plott, C.R.; Zeiler, K. Exchange asymmetries incorrectly interpreted as evidence of endowment effect theory and prospect theory? Am. Econ. Rev. 2007, 97, 1449–1466. [Google Scholar] [CrossRef]

- Fehr, D.; Hakimov, R.; Kübler, D. The willingness to pay–willingness to accept gap: A failed replication of Plott and Zeiler. Eur. Econ. Rev. 2015, 78, 120–128. [Google Scholar] [CrossRef]

- Bartling, B.; Engl, F.; Weber, R. Game form misconceptions are not necessary for a willingness-to-pay vs. willingness-to-accept gap. J. Econ. Sci. Assoc. 2015, 1, 72–85. [Google Scholar] [CrossRef]

- Cason, T.N.; Plott, C.R. Misconceptions and game form recognition: Challenges to theories of revealed preference and framing. J. Politi- Econ. 2014, 122, 1235–1270. [Google Scholar] [CrossRef]

- Horowitz, J.K.; McConnell, K.E. A review of WTA/WTP Studies. J. Environ. Econ. Manag. 2002, 44, 426–447. [Google Scholar] [CrossRef]

- Tuncel, T.; Hammitt, J.K. A new meta-analysis on the WTP/WTA disparity. J. Environ. Econ. Manag. 2014, 68, 175–187. [Google Scholar] [CrossRef]

- Isoni, A.; Loomes, G.; Sugden, R. The willingness to Pay—willingness to accept gap, the ‘Endowment Effect’,subject misconceptions, and experimental procedures for eliciting valuations: Comment. Am. Econ. Rev. 2011, 101, 991–1011. [Google Scholar] [CrossRef]

- Hossain, T.; List, J.A. The Behavioralist Visits the Factory: Increasing Productivity Using Simple Framing Manipulations. Manag. Sci. 2012, 58, 2151–2167. [Google Scholar] [CrossRef]

- Palao, F.; Pardo, Á. What makes carbon traders cluster their orders? Energ. Econ. 2014, 43, 158–165. [Google Scholar] [CrossRef]

- Palao, F.; Pardo, Á. Do carbon traders behave as a herd? North Am. J. Econ. Financ. 2017, 41, 204–216. [Google Scholar] [CrossRef]

- Palao, F.; Pardo, Á. Do prices barriers exist in the European carbon market? J. Behav. Financ. 2017, 1–14. [Google Scholar] [CrossRef]

- Lin, B.; Jia, Z. The impact of Emission Trading Scheme (ETS) and the choice of coverage industry in ETS: A case study in China. Appl. Energy 2017, 205, 1512–1527. [Google Scholar] [CrossRef]

- Daskalakis, G. Temporal restrictions on emissions trading and the implications for the carbon futures market: Lessons from the EU emissions trading scheme. Energy Policy 2018, 115, 88–91. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica. 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econ. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Fan, Y.; Liu, Y.P.; Guo, J.F. How to explain carbon price using market micro-behavior? Appl. Econ. 2016, 48, 1–16. [Google Scholar] [CrossRef]

- Montagnoli, A.; De Vries, F.P. Carbon trading thickness and market efficiency. Energy Econ. 2010, 32, 1331–1336. [Google Scholar] [CrossRef]

- Huang, N.E.; Shen, Z.; Long, S.R.; Wu, M.C.; Shih, H.H.; Zheng, Q.; Yen, N.-C.; Tung, C.C.; Liu, H.H. The empirical mode decomposition and the Hilbert spectrum for nonlinear and non-stationary time series analysis. Proc. R. Soc. A: Math. Phys. Eng. Sci. 1998, 454, 903–995. [Google Scholar] [CrossRef]

- Li, H.; Zhu, H.; Xu, C. Subsample time delay estimation of chirp signals using frft. Signal Process. 2014, 96, 110–117. [Google Scholar] [CrossRef]

- Chiementin, X.; Kilundu, B.; Dron, J.P.; Dehombreux, P.; Debray, K. Effect of cascade methods on vibration defects detection. J. Vib. Control 2011, 17, 567–577. [Google Scholar] [CrossRef]

- Rai, V.; Mohanty, A. Bearing fault diagnosis using FFT of intrinsic mode functions in Hilbert–Huang transform. Mech. Syst. Signal Process. 2007, 21, 2607–2615. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Coefficient | Std. Error | z-Statistic | Prob. |

|---|---|---|---|---|

| θ1 | −5.88E-05 | 0.001 | −0.106 | 0.916 |

| θ2 | −0.894 | 0.042 | −21.388 | 0.000 *** |

| θ3 | 0.926 | 0.033 | 28.170 | 0.000 *** |

| β1 | −8.955 | 0.436 | −20.537 | 0.000 *** |

| β2 | 0.438 | 0.033 | 13.095 | 0.000 *** |

| β3 | 0.048 | 0.024 | 2.039 | 0.042 ** |

| β4 | −0.135 | 0.057 | −2.353 | 0.019 ** |

| Parameter | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| 1.312 | 0.007 | 178.874 | 0.000 *** | |

| −2.22 × 10−5 | 2.75 × 10−6 | −8.085 | 0.000 *** | |

| −5.33 × 10−9 | 1.03 × 10−9 | −5.161 | 0.000 *** | |

| −1.372 | 0.006 | −245.969 | 0.000 *** | |

| −3.47 × 10−6 | 4.30 × 10−7 | −8.084 | 0.000 *** | |

| −7.05 × 10−9 | 1.18 × 10−9 | −5.998 | 0.000 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, J.; Gu, F.; Liu, Y.; Fan, Y.; Guo, J. An Endowment Effect Study in the European Union Emission Trading Market based on Trading Price and Price Fluctuation. Int. J. Environ. Res. Public Health 2020, 17, 3343. https://doi.org/10.3390/ijerph17093343

Wang J, Gu F, Liu Y, Fan Y, Guo J. An Endowment Effect Study in the European Union Emission Trading Market based on Trading Price and Price Fluctuation. International Journal of Environmental Research and Public Health. 2020; 17(9):3343. https://doi.org/10.3390/ijerph17093343

Chicago/Turabian StyleWang, Jiqiang, Fu Gu, Yingpeng Liu, Ying Fan, and Jianfeng Guo. 2020. "An Endowment Effect Study in the European Union Emission Trading Market based on Trading Price and Price Fluctuation" International Journal of Environmental Research and Public Health 17, no. 9: 3343. https://doi.org/10.3390/ijerph17093343

APA StyleWang, J., Gu, F., Liu, Y., Fan, Y., & Guo, J. (2020). An Endowment Effect Study in the European Union Emission Trading Market based on Trading Price and Price Fluctuation. International Journal of Environmental Research and Public Health, 17(9), 3343. https://doi.org/10.3390/ijerph17093343