1. Introduction

Pharmaceutical expenditures have increased rapidly in recent years in Europe, typically rising at between 4% and 13% per annum [

1,

2,

3,

4,

5,

6,

7,

8,

9]. This is generally faster than other components of healthcare spending [

6,

10,

11,

12], similar to the US [

13,

14]. As a consequence, pharmaceutical expenditures in ambulatory care are now the largest or one of the largest cost components in this segment across a number of European countries [

1,

2,

4,

6,

12]. In middle and lower income countries, expenditures on pharmaceuticals are also an appreciable component of expenditures, ranging from 20% to 60% of total spending on health [

15].

European health authorities and health insurance organisations have instigated a number of reforms and initiatives in recent years to address this unsustainable growth. Many of the measures introduced have centred on policies surrounding generics, as they can provide high quality treatment [

16] at lower costs, resulting in considerable savings [

4,

11,

17,

18,

19,

20,

21,

22,

23,

24,

25,

26].

The various reforms and initiatives have led to lower reimbursed prices for generics and originators as well as interchangeable brands within pharmacologic or therapeutic classes [

2,

4,

6,

19,

24,

25,

26,

27,

28,

29,

30]. The reforms have also increased the first line prescribing and dispensing of generics where seen as standard treatment for the condition [

1,

4,

6,

11,

12,

17,

19,

27,

28], the latter through, for instance, encouraging or mandating pharmacists to substitute less expensive generics in place of more expensive originators where pertinent, unless prohibited by physicians or health authorities [

11,

17,

19,

21,

22,

31]. Similar situations also occur in Asia. As an example, government physicians in Indonesia will soon be required to only prescribe generic drugs unless there are no generic alternatives available [

32].

In 2006, generic medicines accounted for 42% of dispensed packs among 27 European countries, but only 18% of total pharmaceutical expenditures [

33]. A recent analysis of 219 substances among the 27 Member States of the EU accounting for approximately 50% of prescription volumes calculated the market share of generics was approximately 30% at the end of the first year and 45% at the end of the second year [

24]. Preferential co-payment policies for generics in the US among the insured population and seniors have also resulted in high utilisation of generics. As a result, generics account for approximately two thirds of prescriptions, but only 13% of costs [

34,

35].

There is appreciable variation in the utilisation of generics across Europe [

36,

37]. For example, there is still limited penetration of generics in Greece, accounting for only 11.6% of total pharmaceutical expenditures in 2006 [

9]. There has also been appreciable differences in the reimbursed prices of generics across Europe [

20,

36,

37], with prices of generics varying up to 36-fold across countries, depending on the molecule [

20].

Pharmaceutical expenditures will continue to grow in Europe driven by demographic changes, rising patient expectations, stricter clinical targets and the continued launch of new premium priced drugs [

10,

24,

38,

39,

40]. Consequently, further reforms are essential to maintain comprehensive and equitable healthcare in Europe without prohibitive increases in either taxes or health insurance premiums.

Key areas for learning for European countries include additional measures to further lower prices of multiple source products where pertinent. They also include measures to increase the prescribing and dispensing of generics [

11,

12,

28,

29]. There have though been concerns with the effectiveness and safety of generics [

4,

7,

9,

11,

21,

23,

25,

33,

34,

41,

42,

43,

44,

45], with some originator companies questioning the quality of generics as part of their marketing strategies to reduce post-patent loss sales erosion [

24]. However concerns with generics generally only apply to a minority of situations [

9,

11,

34,

43]. This is endorsed by two recent comprehensive reviews comparing the outcomes between generics and originators for cardiovascular diseases and epilepsy [

22,

46]. The authors found no evidence in published trials that originator drugs had superior effectiveness and outcomes than different generic formulations. This included drugs with a narrow therapeutic index such as propafenone and warfarin [

46]. Recent studies have also shown no increase in relapse rates with generic atypical antipsychotic drugs

vs. originators apart from initial formulations of generic clozapine in the US [

47,

48,

49,

50,

51,

52,

53]. There has also been concerns with confusion when patients are dispensed multiple branded generics each with different names, which can potentially lead to medication errors [

11]. These issues must be addressed for health authorities and insurance companies to fully capitalise on future patent losses. This is especially important with estimated global sales of USD $100B per year over the next four years subject to patent losses [

54].

Consequently, the principal objective of this paper is to review additional measures that European countries can adopt to further reduce reimbursed prices for multiple source products where pertinent. Secondly, review potential approaches that governments, health authorities and health insurance agencies could instigate to address any concerns with generics when they arise to maximise savings. Potential measures to further enhance the prescribing of generics will be briefly mentioned and discussed further in future papers as it is recognised this is equally important to enhance prescribing efficiency.

We hope this article will stimulate debate on future measures that could be introduced as payers struggle to provide comprehensive and equitable healthcare within finite budgets. The various initiatives may also be of interest to payers outside of Europe as well as to other key stakeholder groups.

2. Methodology

We conducted a narrative review of articles selected from the extensive number of publications and associated references from 17 co-authors concerned with generics. These were subsequently combined with published general reviews on generics as well as additional papers and articles known to the 17 co-authors concerned with initiatives to enhance prescribing efficiency such as web-based articles that had eluded the initial selection. Finally, a targeted literature review of English language papers was subsequently undertaken by one of the authors (B.G.) across chosen European countries where the initial approaches identified no pertinent peer reviewed publications. This involved searching PubMed, MEDLINE and EMBASE between 2000 and February 2010 using key words ‘generics’, ‘generic medicines’, ‘reforms’, ‘generic reforms’, ‘generic pricing’, ‘reference pricing’ and ‘generic substitution’ and the specific country. However, no additional papers were found for possible inclusion.

The same methodological approach was adopted when collating and reviewing papers that discuss reference pricing in a class, as well as different approaches adopted by health authorities to address patient and physician concerns with generics.

There has been no review of the quality of the papers included in this paper using for instance criteria developed by the Cochrane Collaboration [

55]. This is because some of the references are from non-peer reviewed journals, internal health authority documents or web based articles. Nevertheless they have been included as they were typically written by payers or their advisers, which are the principal intended audience for this paper. Table 1A in the

Appendix contains the definitions used in this paper.

The generics and classes chosen for more in-depth analysis were generic omeprazole and the Proton Pump Inhibitors (PPIs)—Anatomical Therapeutic Chemical (ATC) A02BC [

56], and generic simvastatin and the HMG CoA reductase inhibitors (statins)—ATC group C10AA [

56]. These two classes and products were chosen as:

They are both high volume prescribing areas in ambulatory care;

They contain a mixture of generics, originators and single sourced products in a class;

They are typically the subject of initiatives within countries to enhance efficiency.

The price reductions for generic omeprazole and generic simvastatin were computed by comparing reimbursed prices per Defined Daily Dose (DDDs) in 2007 or later with originator prices in 2001 or before. These dates were chosen as generic omeprazole and generic simvastatin were typically launched after 2001 among Western European countries.

Only health authority or health insurance databases were used for the analyses in order to provide data on actual reimbursed payments for the various products in each of the two classes [

36]. The sources of the administrative databases (covering all the patient population unless stated) included:

Austria—Data Warehouse of the Federation of Austrian Social Insurance Institutions—HVB (98% of the population);

England—Information Centre for Health and Social Care;

Estonia—Estonian Health Insurance Fund;

France—Medic'am database (CNAM-TS for salaried personnel covering 75% of the population);

Germany—GAMSI-Database, the GKV Arzneimittel Schnell-Information covering all prescriptions paid by the Social Health Insurance Funds (approximately 90% of the population);

Italy—OsMed database;

Lithuania—Electronic database of the National Health Insurance Fund;

Poland—National Health Fund database;

Portugal—INFARMED (NHS) database covering approximately 75% of the population;

Serbia—Republic of Serbia’s Health Insurance Fund database;

Scotland—Prescribing Information System (PIS) from NHS National Services Scotland Corporate Warehouse;

Spain—DMART (Catalan Health Service) database;

Sweden—Apoteket AB (National Corporation of Swedish Pharmacies – monopoly up to 1 January 2010).

The concepts of ATC classification and DDDs were developed to facilitate comparisons in drug utilisation between countries [

57,

58]. The first comprehensive list of DDDs was first published in Norway in 1975, and has developed since then [

59]. As a result, DDDs are now an internationally accepted method for comparing drug utilisation across countries especially where there are different pack sizes and possibly tablet strengths [

59,

60,

61]. 2010 DDDs were used in line with recent recommendations [

61].

There has been no allowance for inflation as we wanted to compute the actual impact of different policies on reimbursed prices/DDD of generics vs. originators over time based on the local currency. In addition, expenditure figures for the PPIs and statins are presented as percentage reductions or increases rather than actual changes in reimbursed prices or changes in overall reimbursed expenditure. This is because the extent of co-payments, wholesaler and pharmacy margins as well as taxes varies considerably across Europe. As a result, making direct expenditure comparisons difficult.

Finally, details of the reforms regarding the pricing policies for generics as well as interchangeable products in a class were taken from published sources and verified by the co-authors; alternatively, provided directly by the co-authors.

Sixteen European countries and regions have been included in this paper. These countries are: Austria, Estonia, France, Germany, Italy, Lithuania, Netherlands, Norway, Portugal, Poland, Serbia, Spain (Catalonia), Sweden, Turkey and the United Kingdom (England and Scotland). The countries were chosen to reflect differences in geography, epidemiology, financing of healthcare, available resources for healthcare, approaches to the pricing of generics, originators and single sourced products, as well as measures to enhance the prescribing of generics.

Where possible, expenditure figures have been quoted in Euros. Current exchange rates are €1 = 1.3 US$, 1.33 CAN$, 7.84 NOK, 9.63 SEK, 0.86 GB£ (3 May 2010).

We accept there are limitations with the study design. These include no linking of the indications and the actual doses prescribed to calculate Prescribed Daily Doses (PDD) [

62], and reimbursed expenditure/PDD, as there was no access to prescribing databases. They also include the fact that no impact studies were undertaken as health authorities and health insurance agencies typically implemented a number of strategies between 2001 and 2007 to enhance prescribing efficiency making such analyses difficult to perform. In addition, most countries provided data on their total population.

4. Discussion

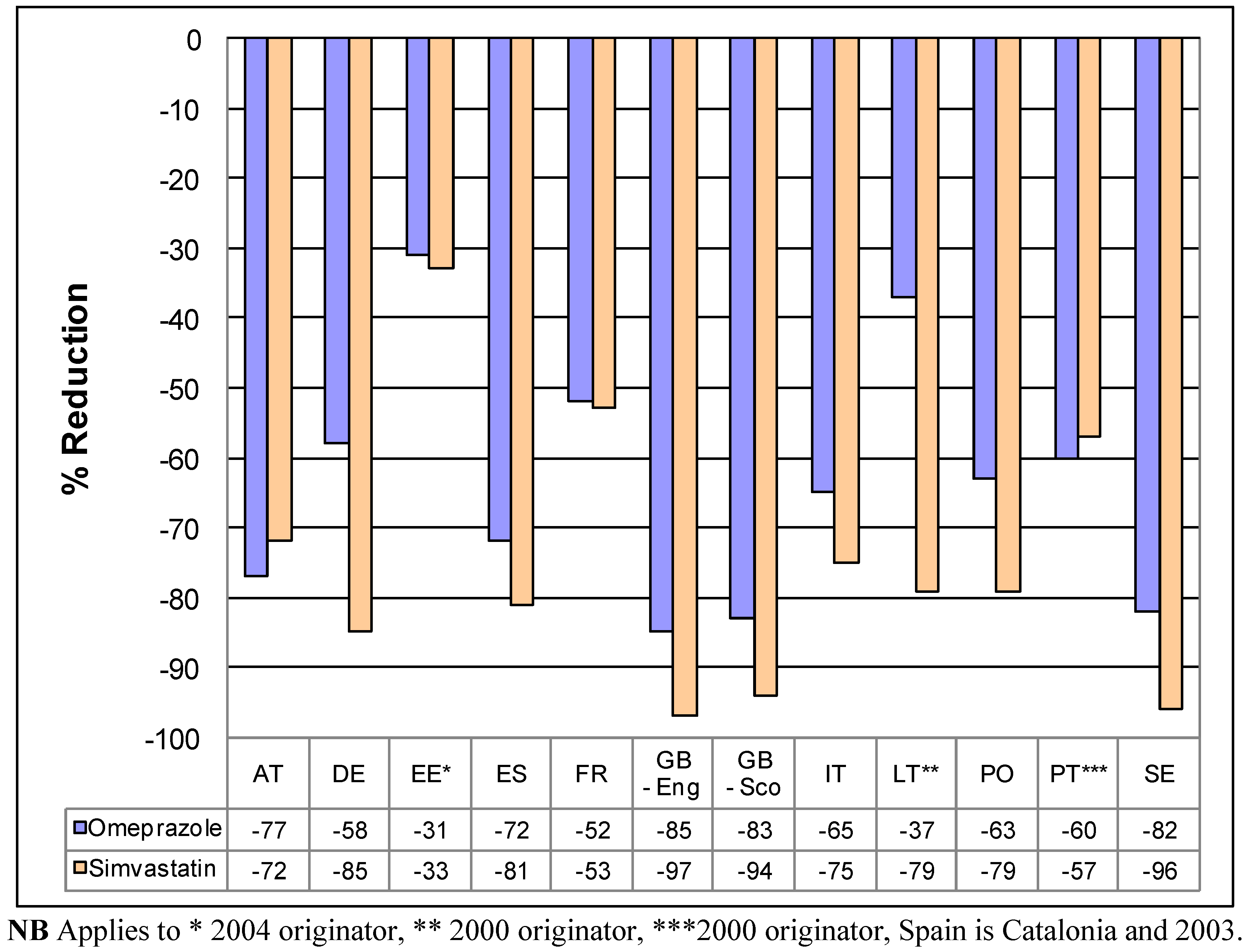

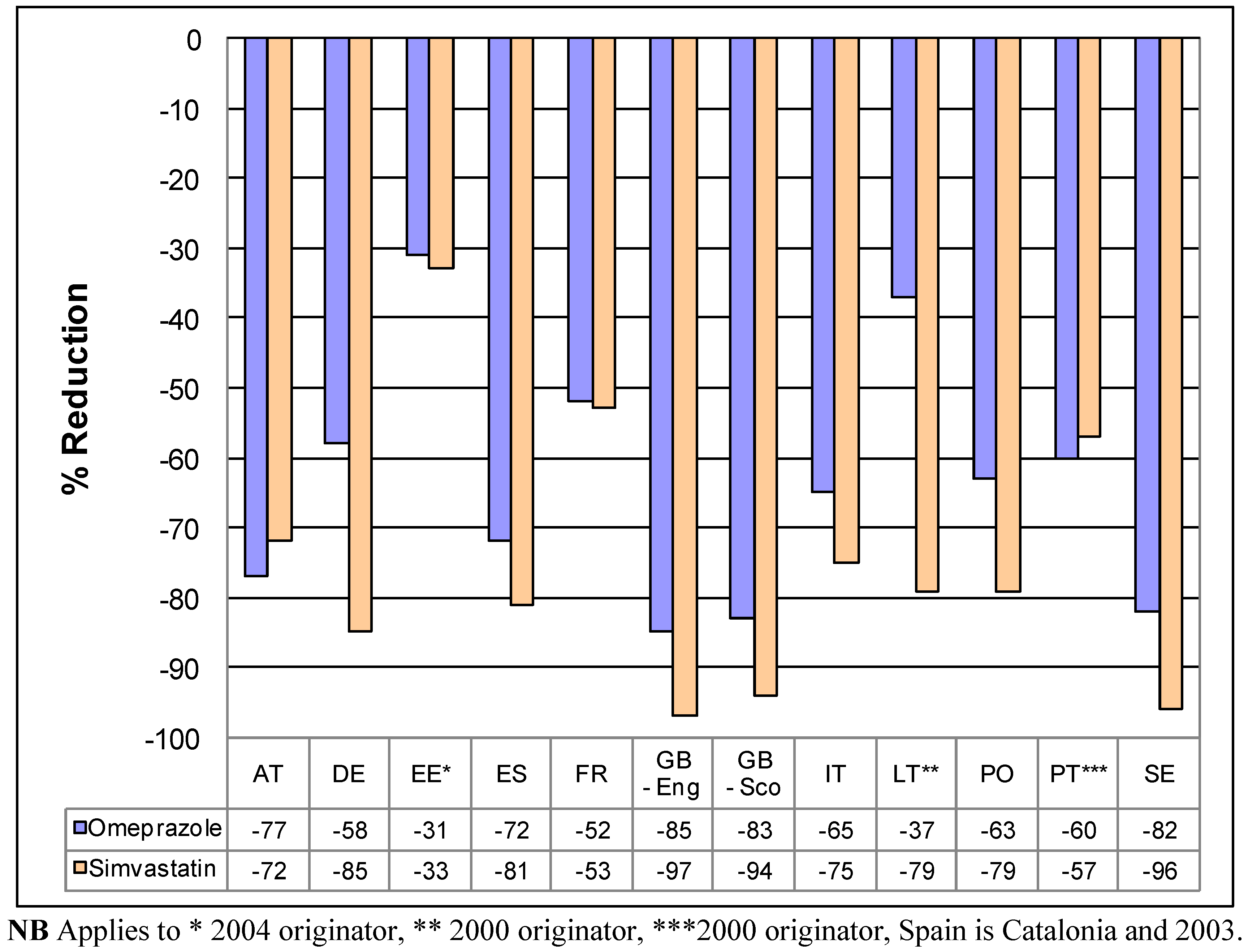

We believe a number of conclusions can be drawn from these findings, as well as provide guidance for the future. These include the fact that the various pricing policies for generics (

Table A2,

Table A3 and

Table A4) have resulted in appreciable decreases in the prices of generic omeprazole and simvastatin

vs. originator prices pre patent loss or 2000/2001 (

Figure 1) in the selected European countries. As a result, releasing considerable resources to help fund increased utilisation of PPIs and statins. Sometimes, this has been at reduced overall expenditure (

Table 2). Alongside this, there have also been more general savings from the availability of generics, which can be considerable, e.g. France, Sweden and the UK [

4,

11,

27,

64,

67]. These savings appear to be achieved without compromising care [

22,

46,

52,

53,

71]. As a result, endorsing the instigation of the various supply and demand side initiatives surrounding generics as a necessary cost containment tool to address growing budgetary pressures.

Care though is needed in a minority of situations for health authorities and health insurance agencies to fully realise the resource benefits from the availability of generics. This includes for instance limiting or discouraging substitution for different formulations of lithium, ciclosporin, and opiods as well as certain products for the management of epilepsy. It also includes instigating prescribing databases in pharmacies, or other alternative measures, to reduce the possibility of duplication when patients are dispensed different branded generics each with different names.

We acknowledge that we have not discussed biosimilars. This is in view of the appreciable difference in effectiveness and safety data requirements for registration between oral generic small molecules and biosimilars, as well as the need for post marketing pharmacovigilance studies with biosimilars. This topic will though be discussed in future articles as biosimilars are becoming increasingly important with the biopharmaceutical market expected to grow by some 12 to 15% per year over the next few years [

33,

81].

As stated, further reforms are essential to ensure continued and comprehensive healthcare in Europe. Consequently, pharmaceutical companies need to appreciate and plan for significant price decreases once drugs lose their patent. This will increasingly become a pre-requisite to fund new premium priced innovative drugs. Otherwise, future patient care and commercial goals will be compromised. Likewise, physicians also need to fully appreciate the rationale behind ongoing reforms surrounding the availability of generics and work with them to fund increased volumes and new drugs within available resources.

Alongside this, European and other countries need to learn from each other. This is already happening for health reforms in general [

82]. Future initiatives in some European countries could include measures to further lower prices of multiple sourced products where pertinent as well as accelerate reimbursement of generics with more frequent reviews of reimbursed prices. Austria and Norway provide examples of aggressive prescriptive pricing policies that can be introduced especially when taking into consideration their population sizes (

Table A2,

Table A3 and

Table A4). Sweden, the UK, and more recently Lithuania, provide examples of additional measures that could be introduced to increase transparency in the pricing of generics linked with either high INN prescribing (Lithuania and the UK) or compulsory substitution unless concerns (Sweden). High INN prescribing is in line with recommendations from the WHO and International Society of Drug Bulletins [

83]. Transparency with the pricing of generics is becoming increasingly important giving the extent of rebates and discounts that have, or still exist, to enhance the dispensing of particular generics [

4,

16,

27,

84]. As a result, demonstrate to health authorities the potential to further lower prices mindful though of the need to maintain a viable and sustainable market for generic manufacturers in Europe.

Compulsory generic substitution or INN prescribing is though not currently permitted in all European countries, and initiatives to increase the transparency for pricing generics is also not in operation across Europe. Possible approaches in these countries could include measures to lower or negate patient co-payment if particular branded generics are priced at a fixed percentage below the current reference price. This measure has been successfully applied in Germany. However, the potential impact will depend on the extent of the current co-payment per pack, and could be viewed as an alternative to more aggressive prescriptive pricing policies for generics.

Other measures to conserve valuable resources alongside pricing initiatives include policies to further enhance the prescribing of generics first line through for instance economic incentives, prescribing targets and/ or prescribing restrictions for single sourced products [

4,

11,

12,

27,

75,

85,

86]. These measures will have a direct impact in further lowering prices where market forces are used to reduce prices post patent loss. These issues will be explored in future papers.

{kind=link}