Behavioural Effects and Market Dynamics in Field and Laboratory Experimental Asset Markets

Abstract

1. Introduction

2. Laboratory and Field Economic Experiments—A Literature Review

3. Preliminary Considerations

3.1. Between the Laboratory and the Field

3.2. Incentive Compatibility

4. Method

4.1. Field Study

4.2. Laboratory Experiment

4.2.1. Participants

4.2.2. Procedure

4.2.3. Compensation

5. Presentation of the Main Results

5.1. Comparison and Quantification Criteria for Assessing Similarities and Differences between Experimental Environments

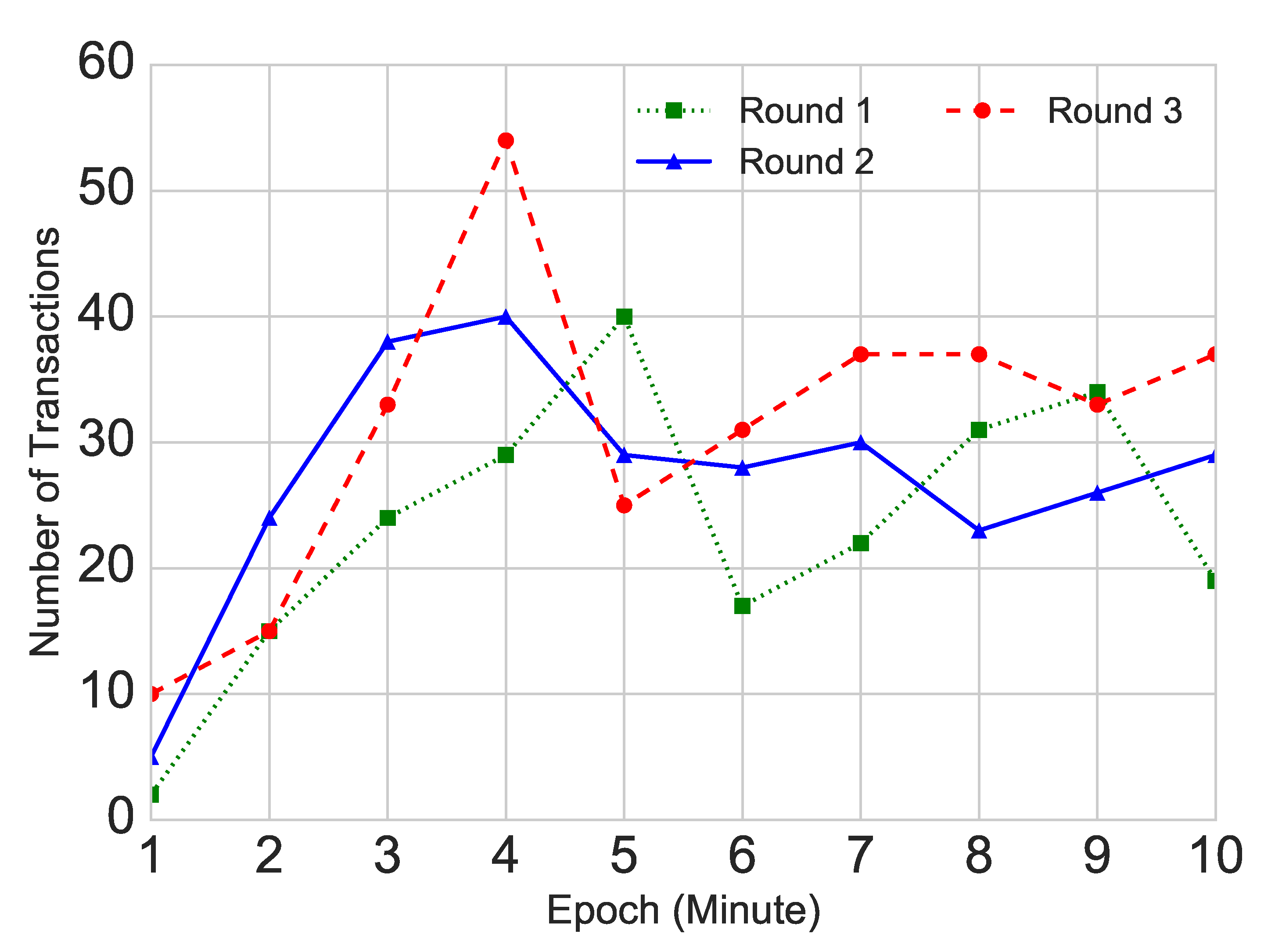

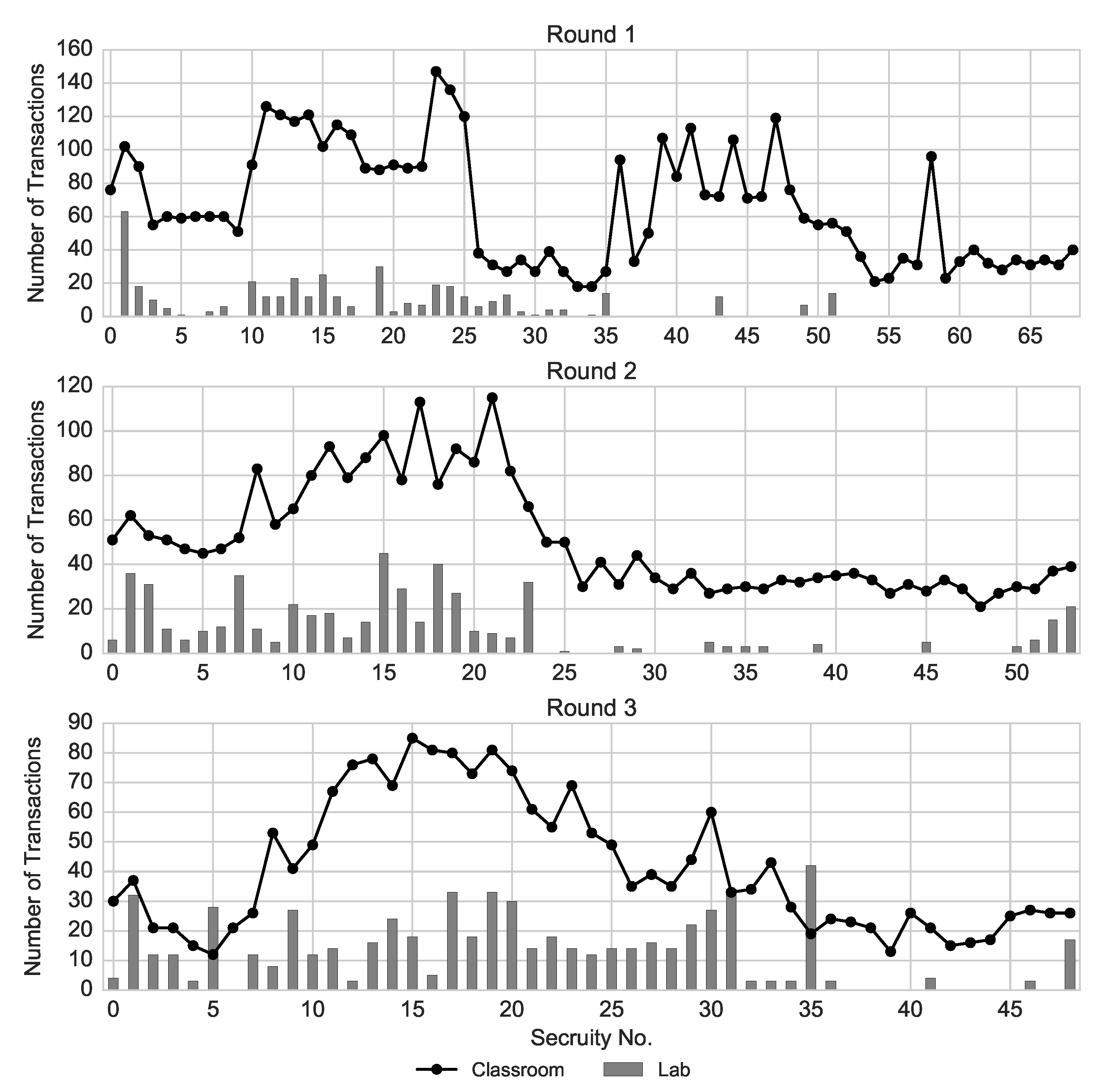

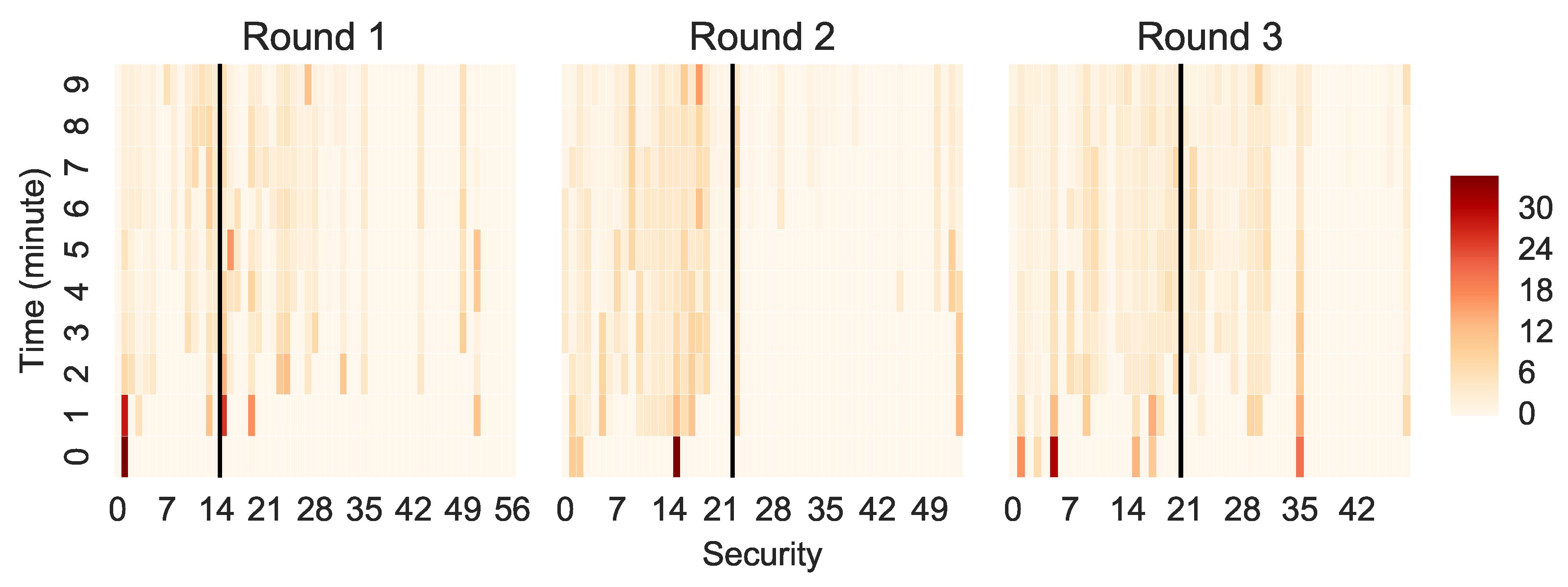

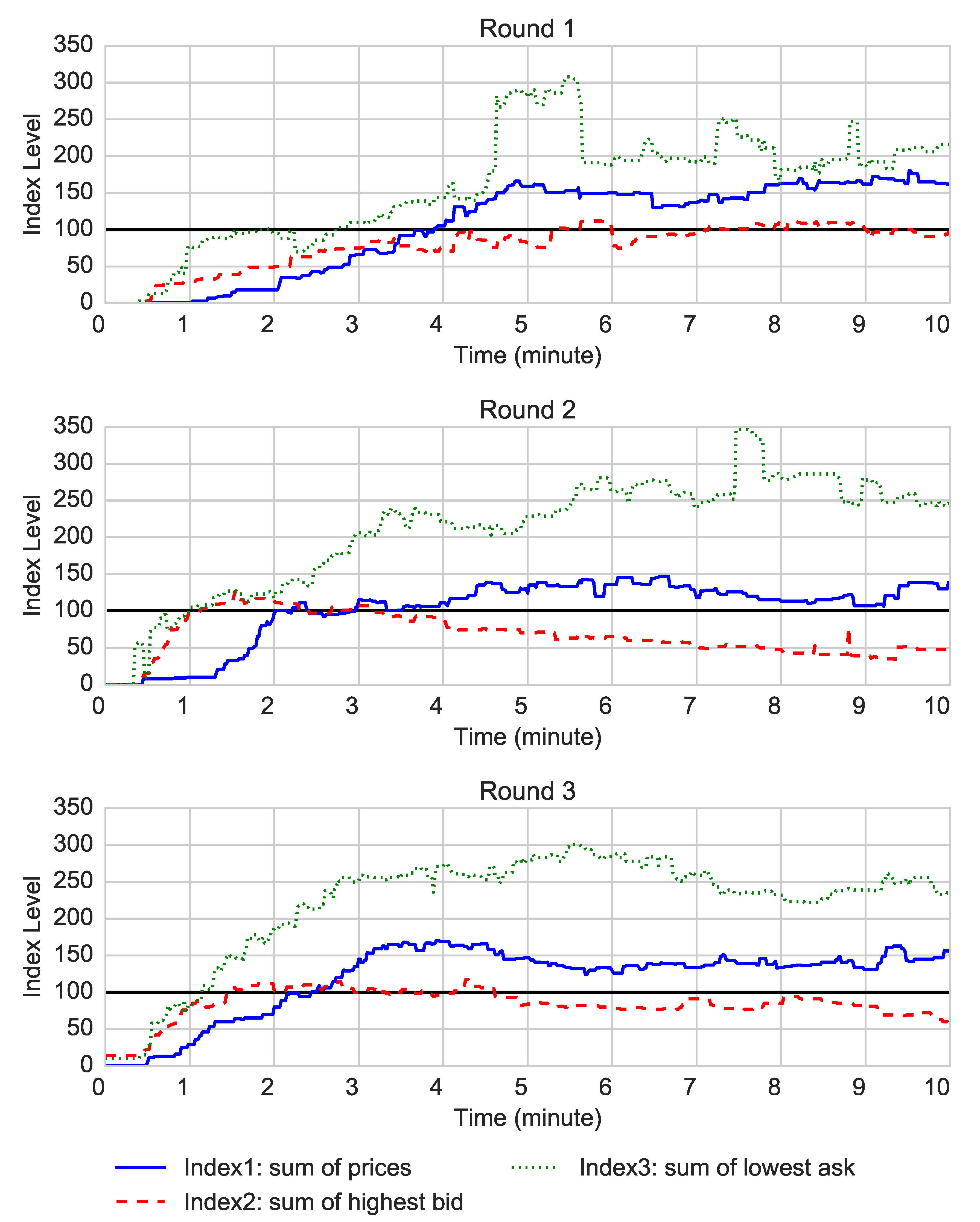

5.2. Trading Activity

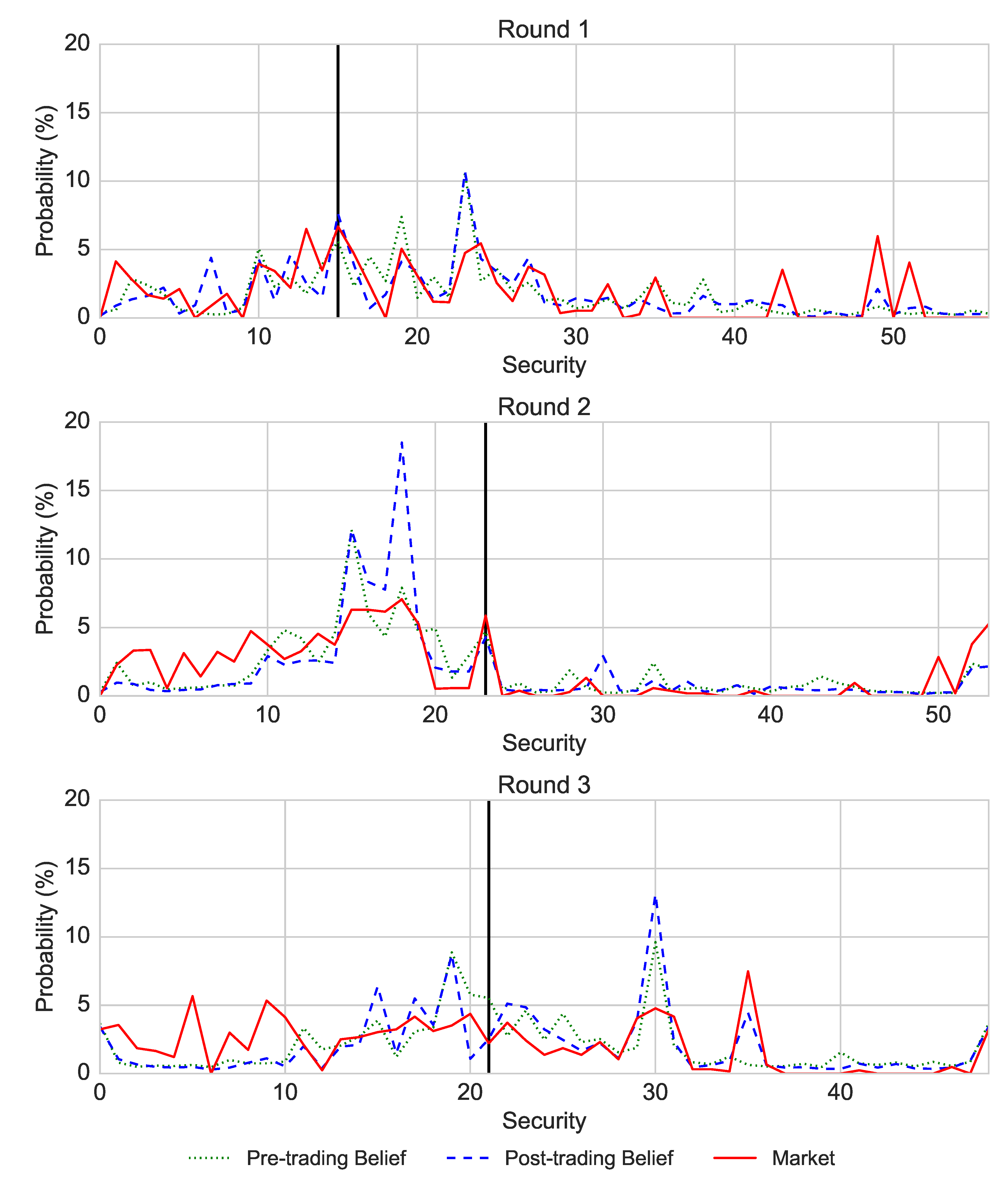

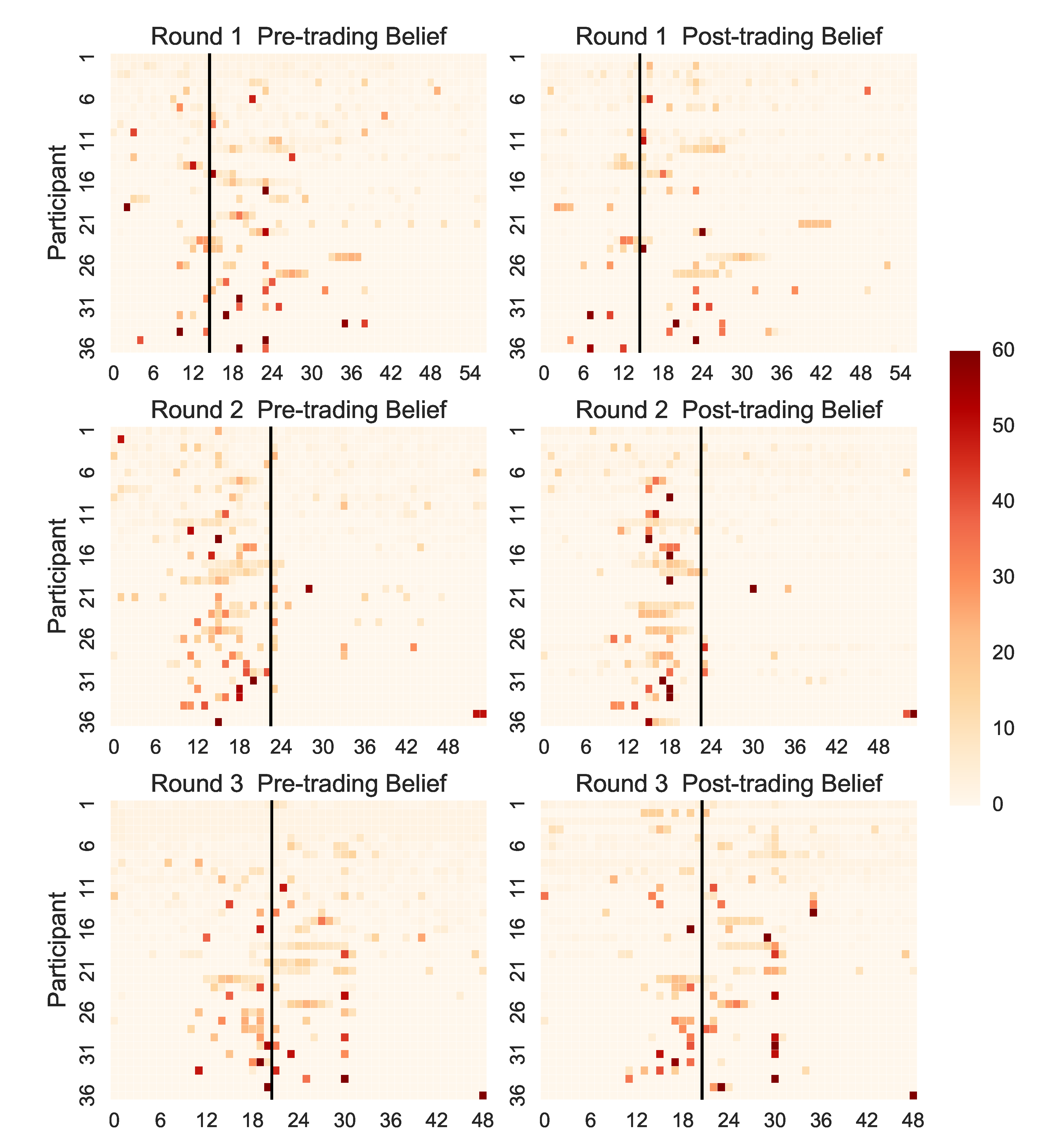

5.3. Market Prices and Participants’ Beliefs

5.4. Mispricing and Market Rationality

5.5. Trading Performance and the Illusion of Control

6. Discussion

6.1. Common Findings in the Laboratory and Field Experiments

6.2. Observed Differences between the Laboratory and Field Setting

6.3. Motivation for the Changes between the Field and Laboratory Setting

7. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Details of the Experimental Method

Appendix A.1. Materials and Apparatus

Appendix A.2. Summary of the Lecturing Style of Prof. Sornette, as Displayed in the Movie

- This movie presents Prof. Didier Sornette’s lecturing style. He prepares more slides than needed and he does not know how much material he will cover.

- Slides that were prepared for a given lecture but were not presented, are presented in a consecutive lecture.

- You will predict the final slide of the lectures that took place in weeks 5–7 of the semester.

- The slides prepared for week 4 will be used in the practice round.

- In weeks 1–3, the professor covered 45, 35 and 30 slides consecutively which corresponds to 69%, 39% and 54% of the available slides.

- There are a few characteristics of the professor’s lecturing style.

- The professor sometimes stops the flow of the lecture to provide a more detailed mathematical derivation of a problem on the blackboard.

- He jumps to a different slide or a topic that either has been shown previously or has not been shown at all.

- Professor Sornette has two lecture ending styles:

- (1)

- He finishes a topic and ends on the last slide of that topic.

- (2)

- He finishes a lecture by showing the first slide of the next topic to give an overview on what he will be talking about in the next lecture.

- Some lectures might start a few minutes later due to organisational issues, important announcements or presentation of an assignment.

- Now, you will see samples of the professor’s lecturing style, based on material recording during two consecutive lectures in the Fall 2015.

Appendix B. Summary of the Self-Reported Measures

References

- Nuzzo, S.; Morone, A. Asset markets in the lab: A literature review. J. Behav. Exp. Financ. 2017, 13, 42–50. [Google Scholar] [CrossRef]

- Hirsh, J.B.; Mar, R.A.; Peterson, J.B. Psychological entropy: A framework for understanding uncertainty-related anxiety. Psychol. Rev. 2012, 119, 304–320. [Google Scholar] [CrossRef] [PubMed]

- Spielberger, C.D. Chapter State-Trait Anxiety Inventory. In The Corsini Encyclopedia of Psychology; John Wiley & Sons: Hoboken, NJ, USA, 2010; p. 1. [Google Scholar]

- Blanchette, I.; Richards, A. The influence of affect on higher level cognition: A review of research on interpretation, judgement, decision making and reasoning. Cognit. Emot. 2010, 24, 561–595. [Google Scholar] [CrossRef]

- Hartely, C.A.; Phelps, E.A. Anxiety and Decision-Making. Biol. Psychiatry 2011, 72, 113–118. [Google Scholar] [CrossRef] [PubMed]

- Palan, S. A review of bubbles and crashes in experimental asset markets. J. Econ. Surv. 2013, 27, 570–588. [Google Scholar] [CrossRef]

- Eckel, C.C.; Füllbrunn, S. Thar she blows? Gender, competition, and bubbles in experimental asset markets. Am. Econ. Rev. 2015, 105, 906–920. [Google Scholar] [CrossRef]

- Cronson, R.; Gneezy, U. Gender differences in preferences. J. Econ. Lit. 2009, 47, 448–474. [Google Scholar] [CrossRef]

- Bruch, E.; Feinberg, F. Decision-making processes in social contexts. Annu. Rev. Sociol. 2017, 43, 207–227. [Google Scholar] [CrossRef]

- Giegerenzer, G.; Gaissmaier, W. Heuristic decision making. Annu. Rev. Psychol. 2011, 62, 451–482. [Google Scholar] [CrossRef]

- Payne, J.W.; Bettman, J.R.; Johnson, E.J. Behavioral decision research: A constructive processing perspective. Annu. Rev. Psychol. 1992, 43, 87–131. [Google Scholar] [CrossRef]

- Dinga, E.; Tanasescu, C.R.; Ioanescu, G.M. Social Entropy and Normative Network. Entropy 2020, 22, 1051. [Google Scholar] [CrossRef]

- Askar, S.S.; Al-khedhairi, A. Dynamic Effects Arise Due to Consumers’ Preferences Depending on Past Choices. Entropy 2020, 22, 173. [Google Scholar] [CrossRef]

- Maldonado, A.D.; Morales, M.; Aquilera, P.A.; Salmeron, A. Analyzing uncertainty in comples socio-ecological networks. Entropy 2020, 22, 123. [Google Scholar] [CrossRef]

- Adams, B.; Lipson, H. A Universal Framework for Aanalysis of Self-Replication Phenomena. Entropy 2009, 11, 295–325. [Google Scholar] [CrossRef]

- Harrison, G.W.; List, J.A. Field Experiments. J. Econ. Lit. 2004, 42, 1009–1055. [Google Scholar] [CrossRef]

- Sornette, D.; Andraszewicz, S.; Wu, K.; Murphy, R.O.; Rindler, P.; Sanagdol, D. Overpricing persistence in exprimental asset markets with intrinsic uncertainty. Econ. E-J. 2020. [Google Scholar] [CrossRef]

- Schram, A. Artificiality: The tension between internal and external validity in economic experiments. J. Econ. Methodol. 2005, 12, 225–237. [Google Scholar] [CrossRef]

- Plott, C.R. Industrial Organization Theory and Experimental Economics. J. Econ. Lit. 1982, 20, 1485–1527. [Google Scholar]

- Loewenstein, G. Experimental economics from the vantage-point of behavioural economics. Econ. J. 1999, 109, 25–34. [Google Scholar] [CrossRef]

- Ledyard, J.O. Chapter Public Goods: A Survey of Experimental Research. In Handbook of Experimental Economics; Princeton University Press: Princeton, NJ, USA, 1995; pp. 111–194. [Google Scholar]

- Nosek, O.S.C.B.A.; Alter, G.; Banks, G.C.; Borsboom, D.; Bowman, S.D.; Breckler, S.J.; Buck, S.; Chambers, C.D.; Chin, G.; Christensen, G.; et al. Promoting and open research culture. Science 2015, 348, 1422–1425. [Google Scholar] [CrossRef]

- Camerer, C.F.; Dreber, A.; Forsell, E.; Ho, T.H.; Huber, J.; Johannesson, M.; Kirchler, M.; Almenberg, J.; Altmejd, A.; Chan, T.; et al. Evaluating replicability of laboratory experiments in economics. Science 2016, 351, 1433–1436. [Google Scholar] [CrossRef]

- Chen, D.; Schonger, M.; Wickens, C. oTree—An open-source platform for laboratory, online, and field experiments. J. Behav. Exp. Financ. 2016, 9, 88–97. [Google Scholar] [CrossRef]

- List, J.A. Do explicit warnings eliminate the hypothetical bias in elicitation procedures? Evidence from field auctions for sportscards. Am. Econ. Rev. 2001, 91, 1498–1507. [Google Scholar] [CrossRef]

- Cummings, R.G.; Harrison, G.W.; Rutström, E.E. Homegrown values and hypothetical surveys: Is the dichotomous choice approach incentive compatible? Am. Econ. Rev. 1995, 95, 260–266. [Google Scholar]

- Cummings, R.G.; Taylor, L.O. Unbiased value estimates for environmental goods: A cheap talk design for the contingent valuation method. Am. Econ. Rev. 1999, 89, 649–665. [Google Scholar] [CrossRef]

- Benz, M.; Meier, S. Do people behave in experiments as in the field?—Evidence from domains. J. Exp. Econ. 2008, 11, 268–281. [Google Scholar] [CrossRef]

- Levitt, S.; List, J.A.; Railey, D. What happens in the field stays in the field: Professionals do not play minimax in laboratory experiments. Econometrica 2010, 78, 1413–1434. [Google Scholar]

- Levitt, S.; List, J.A. Viewpoint: On the generalizability of lab behaviour to the field. Can. J. Econ. 2007, 40, 347–370. [Google Scholar] [CrossRef]

- Levitt, S.; List, J.A. What do laboratory experiments measuring social preferences reveal about the real world. J. Econ. Perspect. 2007, 21, 153–174. [Google Scholar] [CrossRef]

- Levitt, S.; List, J.A. Homo Oeconomicus Evolves. Science 2008, 319, 909–910. [Google Scholar] [CrossRef]

- Camerer, C.F. The promise and success of lab-field generalizability in experimental economics: A critical reply to Levitt and List. In Handbook of Experimental Economic Methodology; Frechette, G.R., Schotter, A., Eds.; Oxford Scholarship Online: Oxford, UK, 2015; pp. 1–64. [Google Scholar]

- Smith, V.L.; Suchanek, G.L.; Williams, A.W. Bubbles, crashes, and endogenous expectations in experimental spot asset markets. Econometrica 1988, 56, 1119–1151. [Google Scholar] [CrossRef]

- Hertwig, R.; Erev, I. The description-experience gap in risky choice. Trends Cognit. Sci. 2009, 13, 517–523. [Google Scholar] [CrossRef]

- Powell, O.; Shestakova, N. Experimental asset markets: A survey of recent developments. J. Behav. Exp. Financ. 2016, 12, 14–22. [Google Scholar] [CrossRef]

- Trautman, S.T.; van de Kuilen, G. Belief Elicitation: A horse race among truth serums. Econ. J. 2015, 125, 2116–2135. [Google Scholar] [CrossRef]

- Camerer, C.F.; Hogarth, R. The effects of financial incentives in experiments: A Review and Capital-Labour- Production Framework. J. Risk Uncertain. 1999, 19, 7–42. [Google Scholar] [CrossRef]

- Gneezy, U.; Rustichini, A. Pay enough or don’t pay at all. Q. J. Econ. 2000, 115, 791–810. [Google Scholar] [CrossRef]

- Nieuwenhuis, S.; Heslenfeld, D.J.; von Geusau, N.J.A.; Mars, R.B.; Holroyd, C.B.; Yeung, N. Activity in human reward-sensitive brain areas is strongly content dependent. NeuroImage 2005, 25, 1302–1309. [Google Scholar] [CrossRef] [PubMed]

- Miyapuram, K.P.; Tobler, P.N.; Gregorios-Pippas, L.; Schulz, W. BOLD responses in reward regions to hypothetical and imaginary monetary rewards. NeuroImage 2012, 59, 1692–1699. [Google Scholar] [CrossRef]

- Bray, S.; Shimojo, S.; O’Doherty, J.P. Human medial orbitofrontal cortex is recruited during experience of imagined and real rewards. J. Neurophysiol. 2010, 103, 2506–2512. [Google Scholar] [CrossRef]

- Lin, A.; Adoplhs, R.; Rangel, A. Social and monetary reward learning engage overlapping neural substrates. Soc. Cognit. Affect. Neurosci. 2012, 7, 274–281. [Google Scholar] [CrossRef]

- Domenico, S.I.D.; Ryan, R.M. The emerging neuroscience of intrinsic motivation: A new frontier in self-determination research. Front. Hum. Neurosci. 2017, 11, 1–14. [Google Scholar] [CrossRef]

- Kruse, J.B.; Thompson, M.A. A comparison of salient rewards in experiments: Money and class points. Econ. Lett. 2001, 74, 113–117. [Google Scholar] [CrossRef]

- Ding, S.; Lugovskyy, V.; Puzzello, D.; Tucker, S.; Williams, A. Cash versus extra-credit incentives in experimental asset markets. J. Econ. Behav. Organ. 2018, 150, 19–27. [Google Scholar] [CrossRef]

- Charness, G.; Gneezy, U.; Halladay, B. Experimental methods: Pay one or pay all. J. Econ. Behav. Organ. 2016, 131, 141–150. [Google Scholar] [CrossRef]

- Beatty, J. Grades as money and the role of the market metaphor in management education. Acad. Manag. Learn. Educ. 2004, 3, 187–196. [Google Scholar] [CrossRef]

- Knight, F.H. Risk, Uncertainty and Profit; Houghton Mifflin Company: Boston, MA, USA; New York, NY, USA, 1921. [Google Scholar]

- Johnson, S.R.; Tomlinson, G.A.; Hawker, G.A.; Granton, J.T.; Grosbein, H.A.; Feldman, B.M. A valid and reliable belief elicitation method for Bayesian priors. J. Clin. Epidemiol. 2010, 63, 370–383. [Google Scholar] [CrossRef]

- Morris, D.E.; Oakley, J.O.; Crowe, J.A. A web-based tool for eliciting probability distributions from experts. Environ. Model. Softw. 2014, 52, 1–4. [Google Scholar] [CrossRef]

- Ejova, A.; Delfabbro, P.H.; Navarro, D.J. The illusion of control: Structure, measurement and dependence on reinforcement frequency in the context of a laboratory gambling. In ASCS09: Proceeding of the 9th Conference of the Australasian Society for Cognitive Science; University of Adelaide: Adelaide, Australia, 2009; pp. 84–92. [Google Scholar]

- Majtey, A.; Lamberti, P.; Prato, D. Jensen-Schannon divergence as a measure of distinguishability between mixed quantum states. Phys. Rev. A 2005, 72, 052310. [Google Scholar] [CrossRef]

- Stöckl, T.; Huber, J.; Kirchler, M. Bubble measures in experimental asset markets. Exp. Econ. 2010, 13, 284–298. [Google Scholar] [CrossRef]

- Lei, V.; Noussair, C.N.; Plott, C.R. Non-speculative bubbles in experimental asset markets: Lack of common knowledge of rationality vs. actual irrationality. Econometrica 2001, 69, 831–859. [Google Scholar] [CrossRef]

- Tourangeau, R.; Rasinski, K.A. Cognitive processes underlying context effects in attitude measurement. Psychol. Bull. 1988, 103, 299–314. [Google Scholar] [CrossRef]

- Binmore, K. Does Game Theory Work? The Bargaining Challenge; MIT Press: Cambridge, MA, USA, 2007. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Minute | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Round | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| 1 | 0.89 | 0.61 | 0.28 | 0.23 | 0.08 | 0.11 | 0.12 | 0.09 | 0.07 | 0.08 |

| 2 | 0.86 | 0.60 | 0.13 | 0.04 | 0.15 | 0.09 | 0.10 | 0.06 | 0.11 | 0.03 |

| 3 | 0.73 | 0.34 | 0.29 | 0.08 | 0.02 | 0.06 | 0.03 | 0.04 | 0.07 | 0.04 |

| Round 1 | Round 2 | Round 3 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Lab | Field | Lab | Field | Lab | Field | ||||

| Pre-trading Belief | 3.59 | 3.76 | 0.13 | 3.44 | 3.46 | 0.08 | 3.51 | 3.55 | 0.06 |

| Post-trading Belief | 3.59 | 3.62 | 0.17 | 3.18 | 3.25 | 0.07 | 3.38 | 3.51 | 0.08 |

| Market | 3.34 | 3.16 | 0.36 | 3.29 | 2.78 | 0.3 | 3.43 | 3.11 | 0.27 |

| Round 1 | Round 2 | Round 3 | ||||

|---|---|---|---|---|---|---|

| RD | Lab | Field | Lab | Field | Lab | Field |

| Index 1 | 45% | 30% | 19% | 42% | 30% | 27% |

| Index 2 | −7% | −50% | −51% | 28% | −25% | 6% |

| Index 3 | 101% | 178% | 150% | 87% | 139% | 82% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Andraszewicz, S.; Wu, K.; Sornette, D. Behavioural Effects and Market Dynamics in Field and Laboratory Experimental Asset Markets. Entropy 2020, 22, 1183. https://doi.org/10.3390/e22101183

Andraszewicz S, Wu K, Sornette D. Behavioural Effects and Market Dynamics in Field and Laboratory Experimental Asset Markets. Entropy. 2020; 22(10):1183. https://doi.org/10.3390/e22101183

Chicago/Turabian StyleAndraszewicz, Sandra, Ke Wu, and Didier Sornette. 2020. "Behavioural Effects and Market Dynamics in Field and Laboratory Experimental Asset Markets" Entropy 22, no. 10: 1183. https://doi.org/10.3390/e22101183

APA StyleAndraszewicz, S., Wu, K., & Sornette, D. (2020). Behavioural Effects and Market Dynamics in Field and Laboratory Experimental Asset Markets. Entropy, 22(10), 1183. https://doi.org/10.3390/e22101183