Consumer Acceptance of Fintech App Payment Services: A Systematic Literature Review and Future Research Agenda

Abstract

:1. Introduction

- RQ1:

- How many studies have been done relating to consumers’ adoption of fintech payment services?

- RQ2:

- What are the contexts used by researchers in previous studies?

- RQ3:

- What are the methods applied by researchers in previous studies?

- RQ4:

- What are the theories used by researchers in previous studies?

- RQ5:

- What are the factors that influenced consumers’ adoption of fintech payment services?

- RQ6:

- What are the recommendations for future studies in this field?

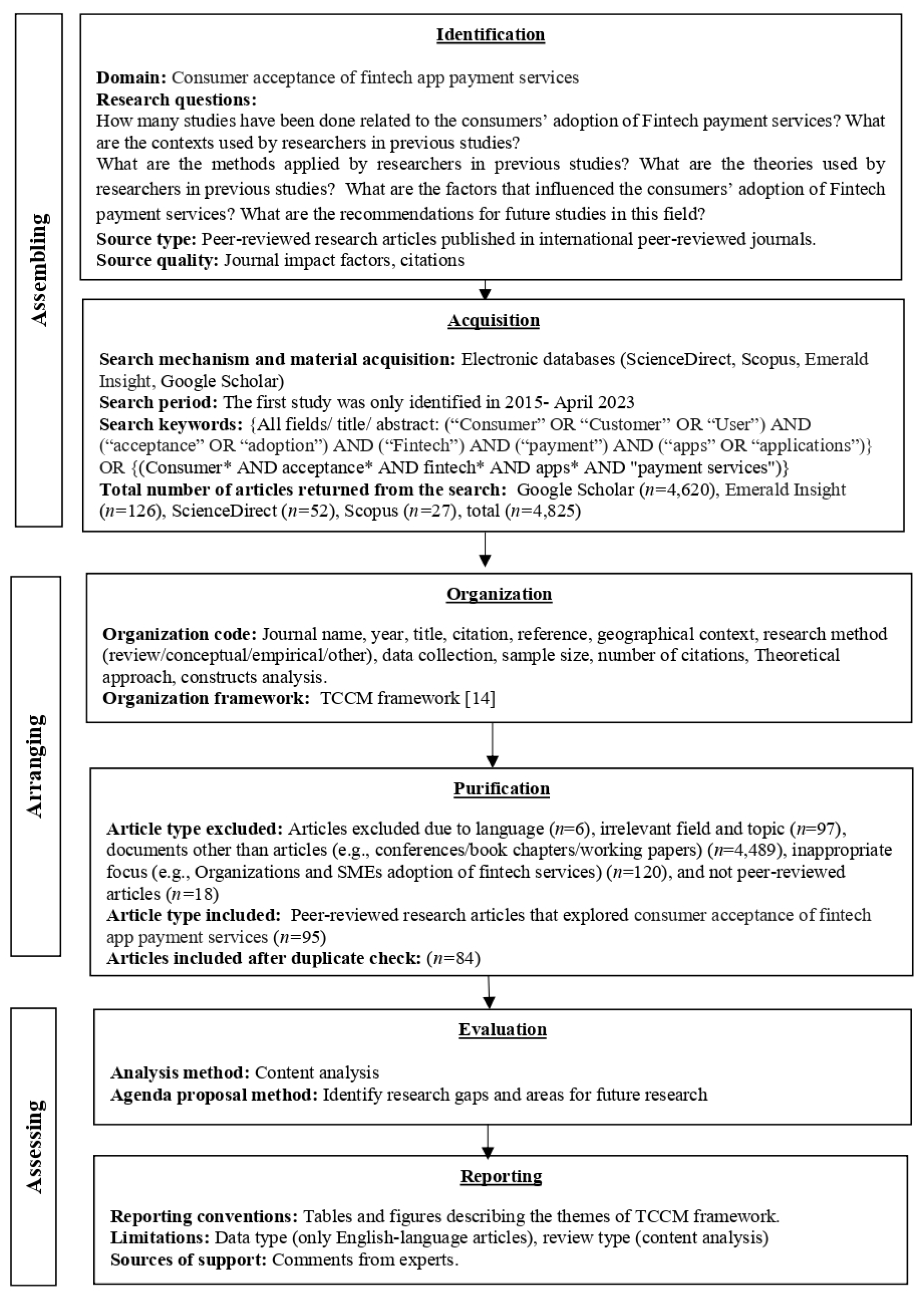

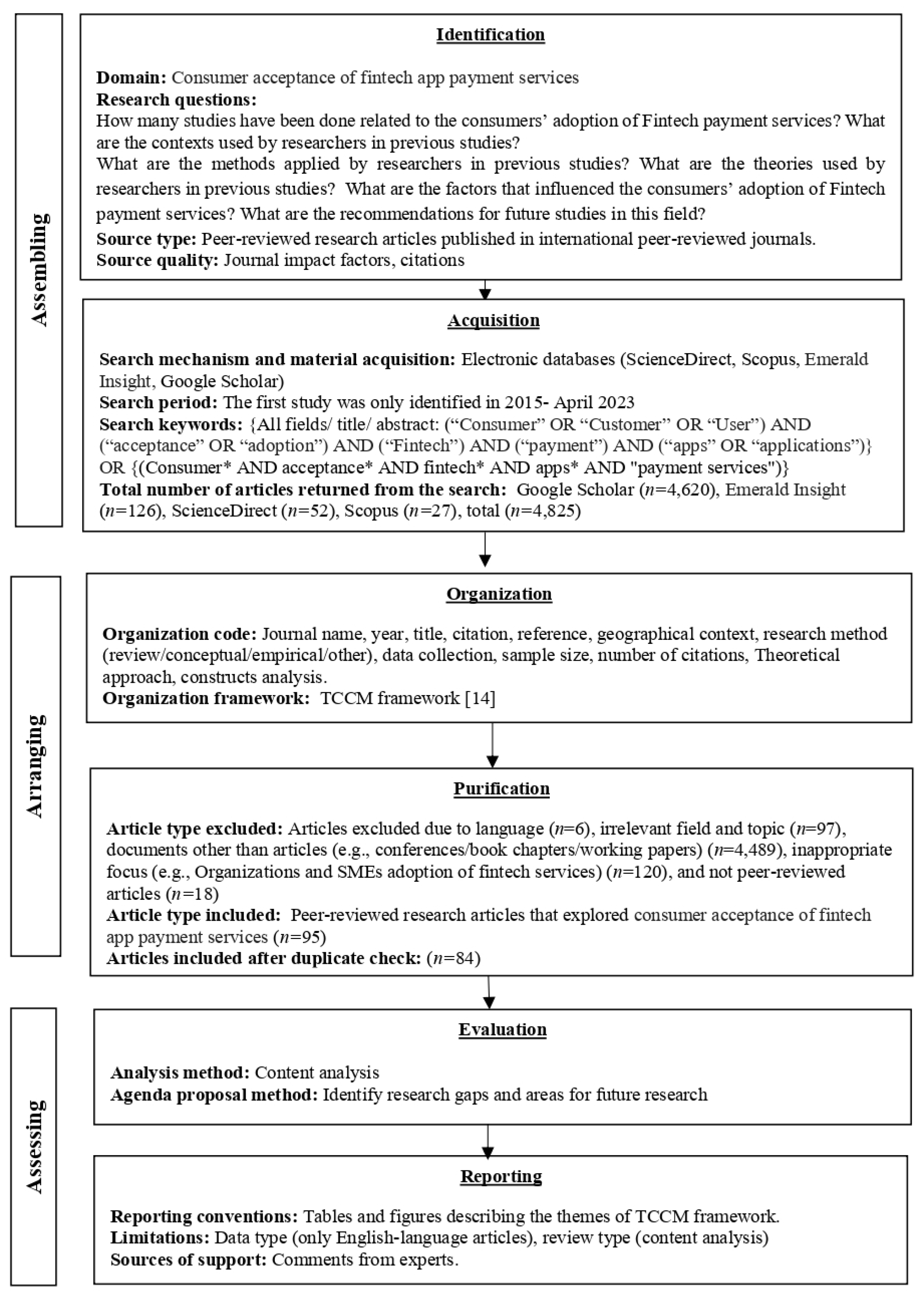

2. Methodology

2.1. Assembling

2.2. Arranging

2.3. Assessing

3. Results

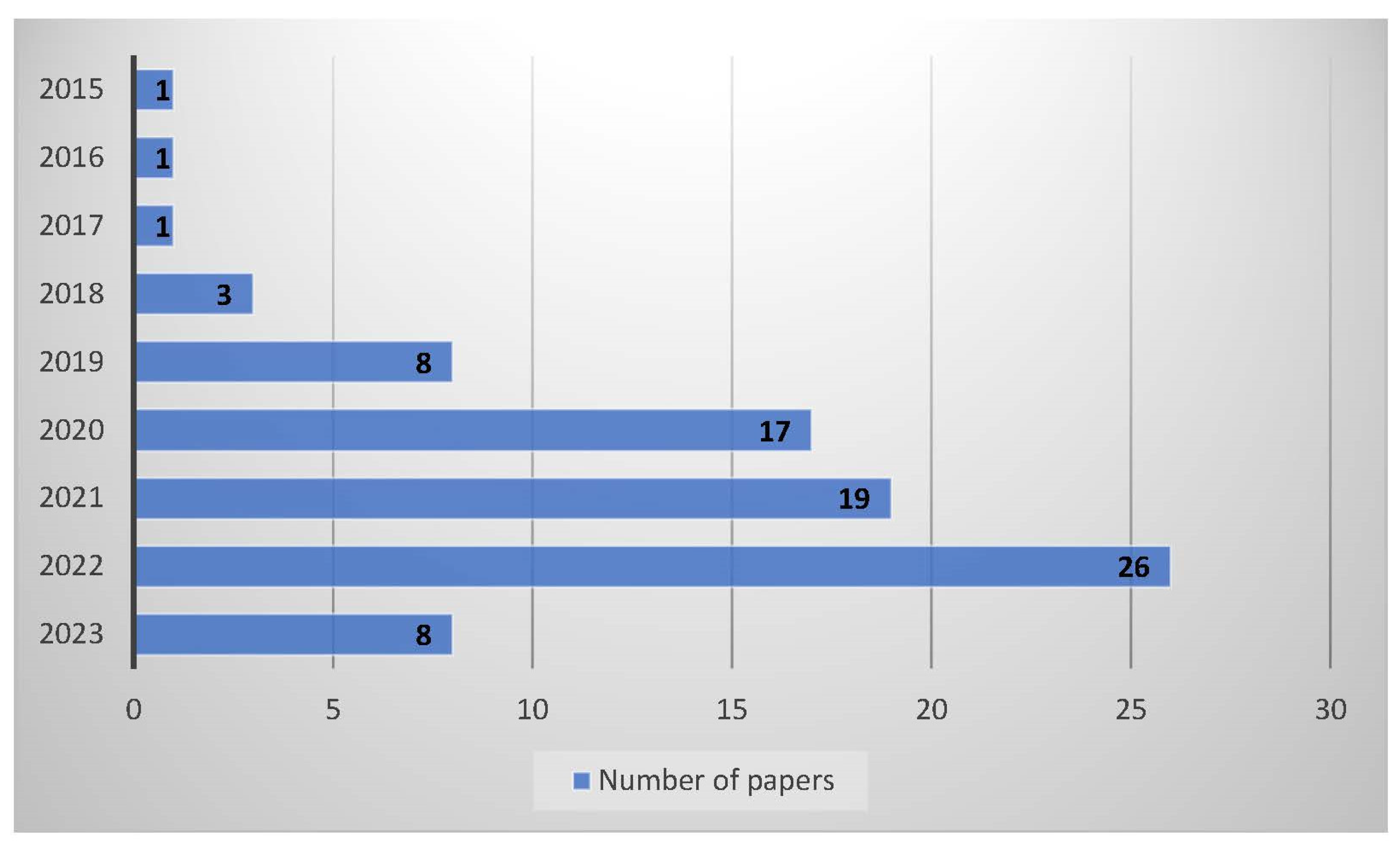

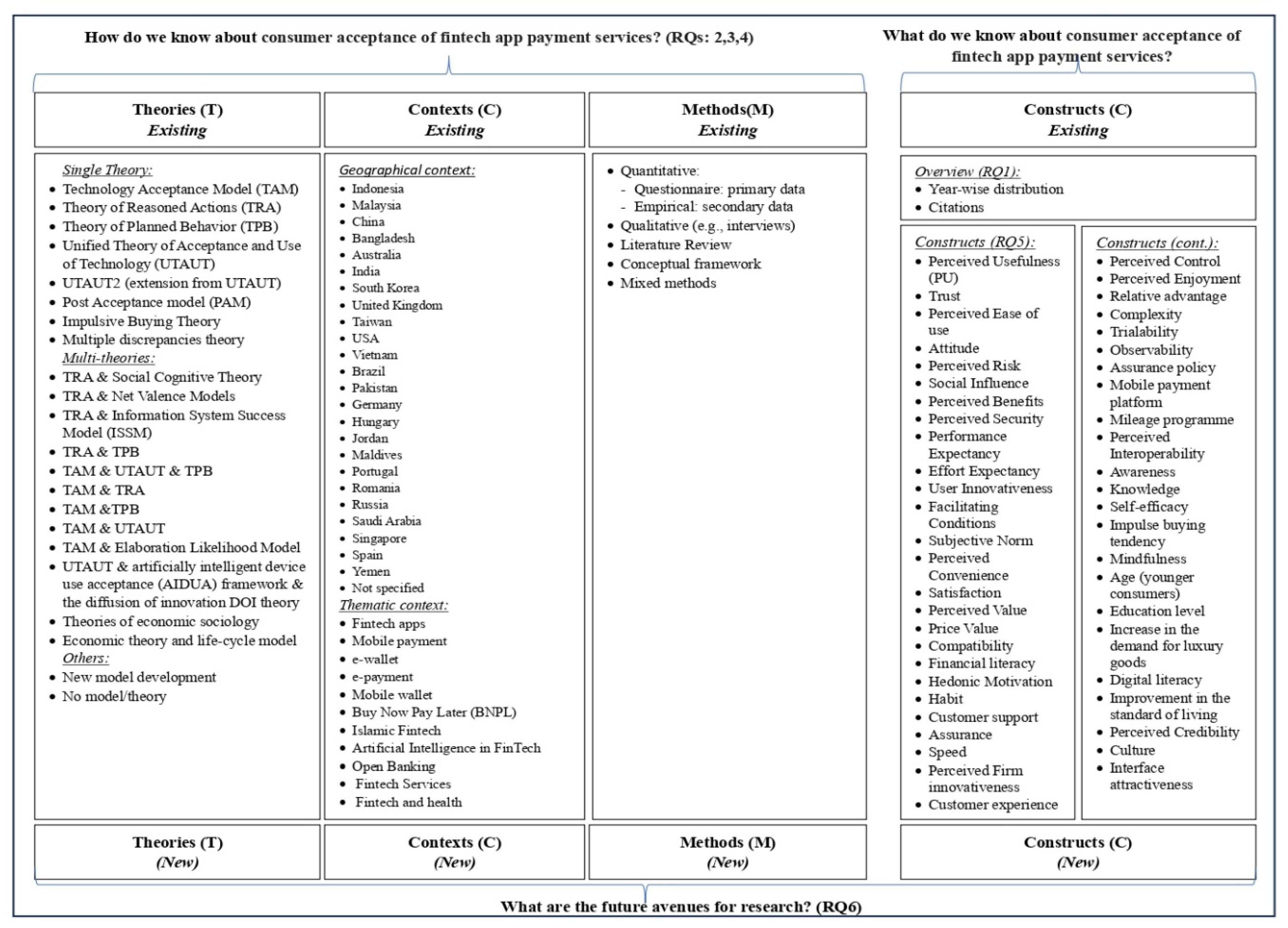

3.1. A General Overview of the Results

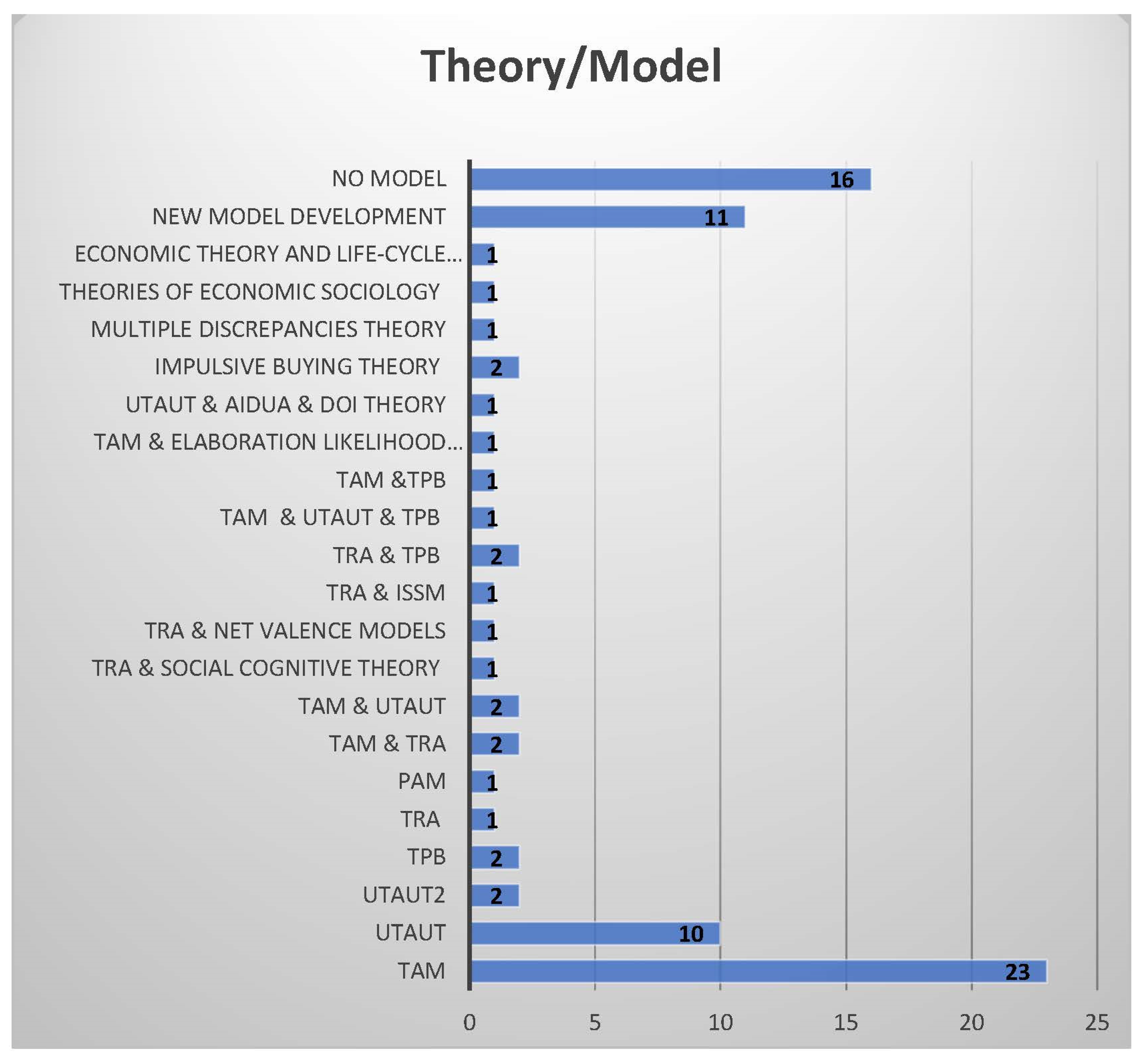

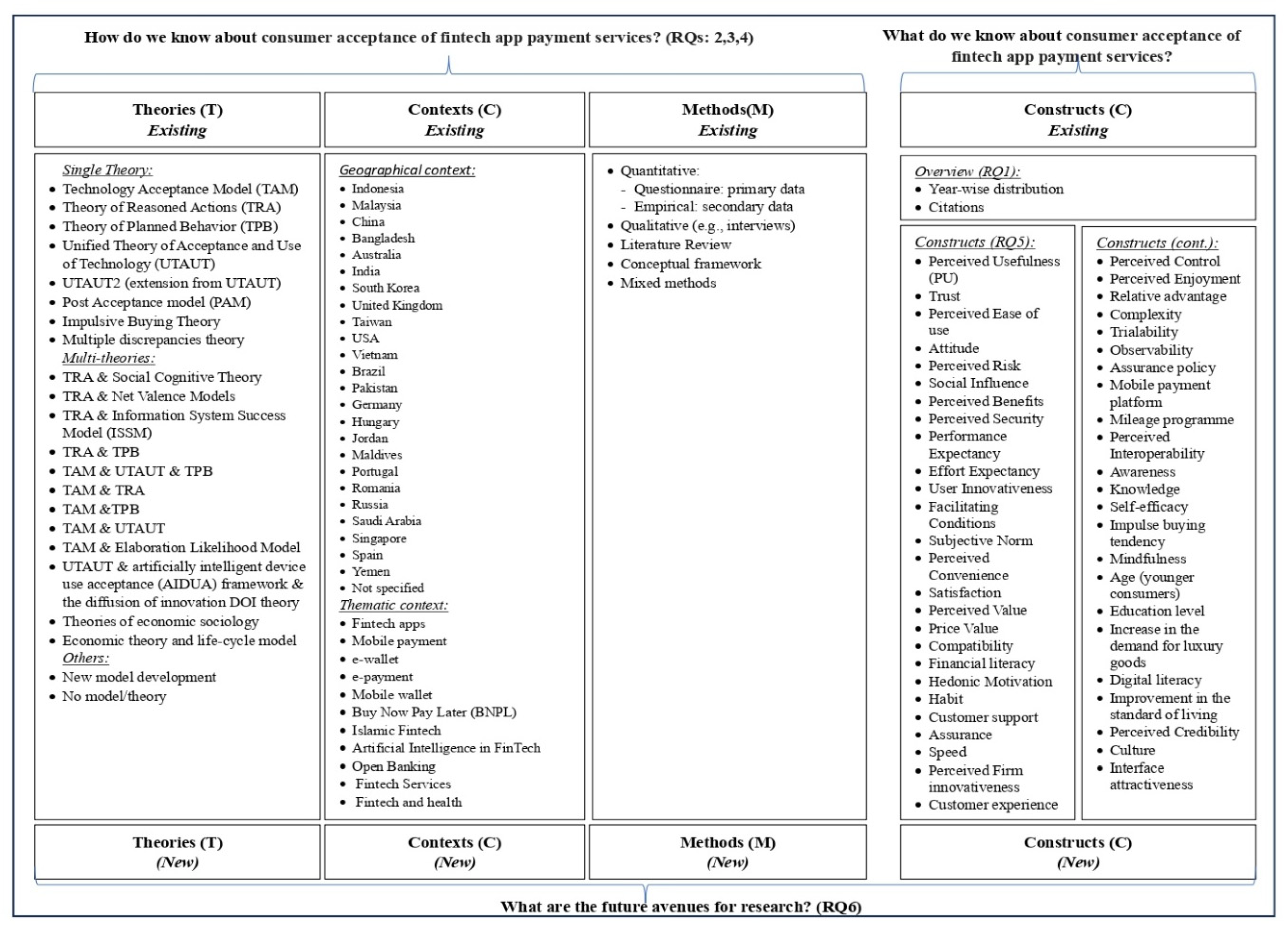

3.2. Theories (T)

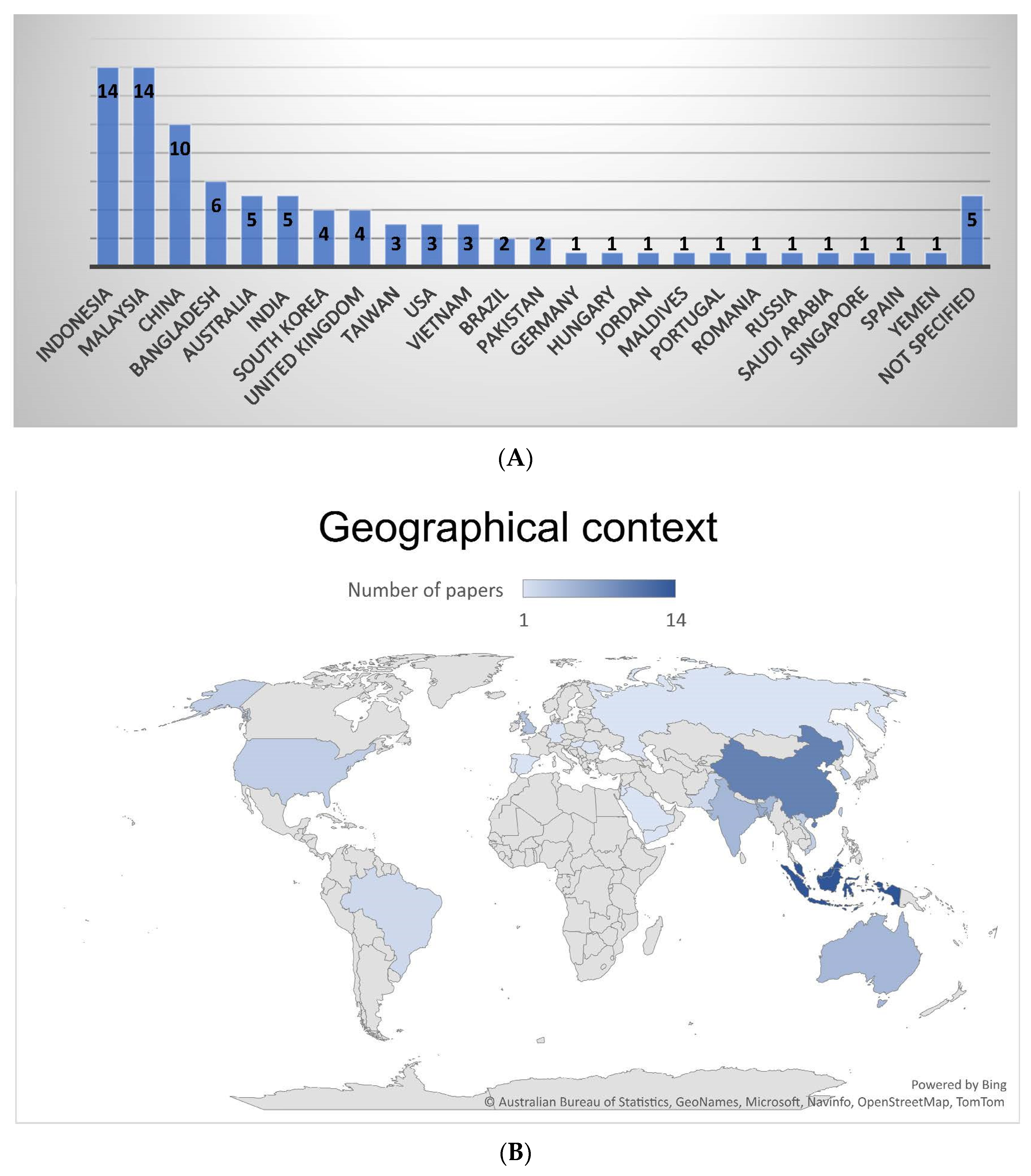

3.3. Context (C)

3.4. Construct (C)

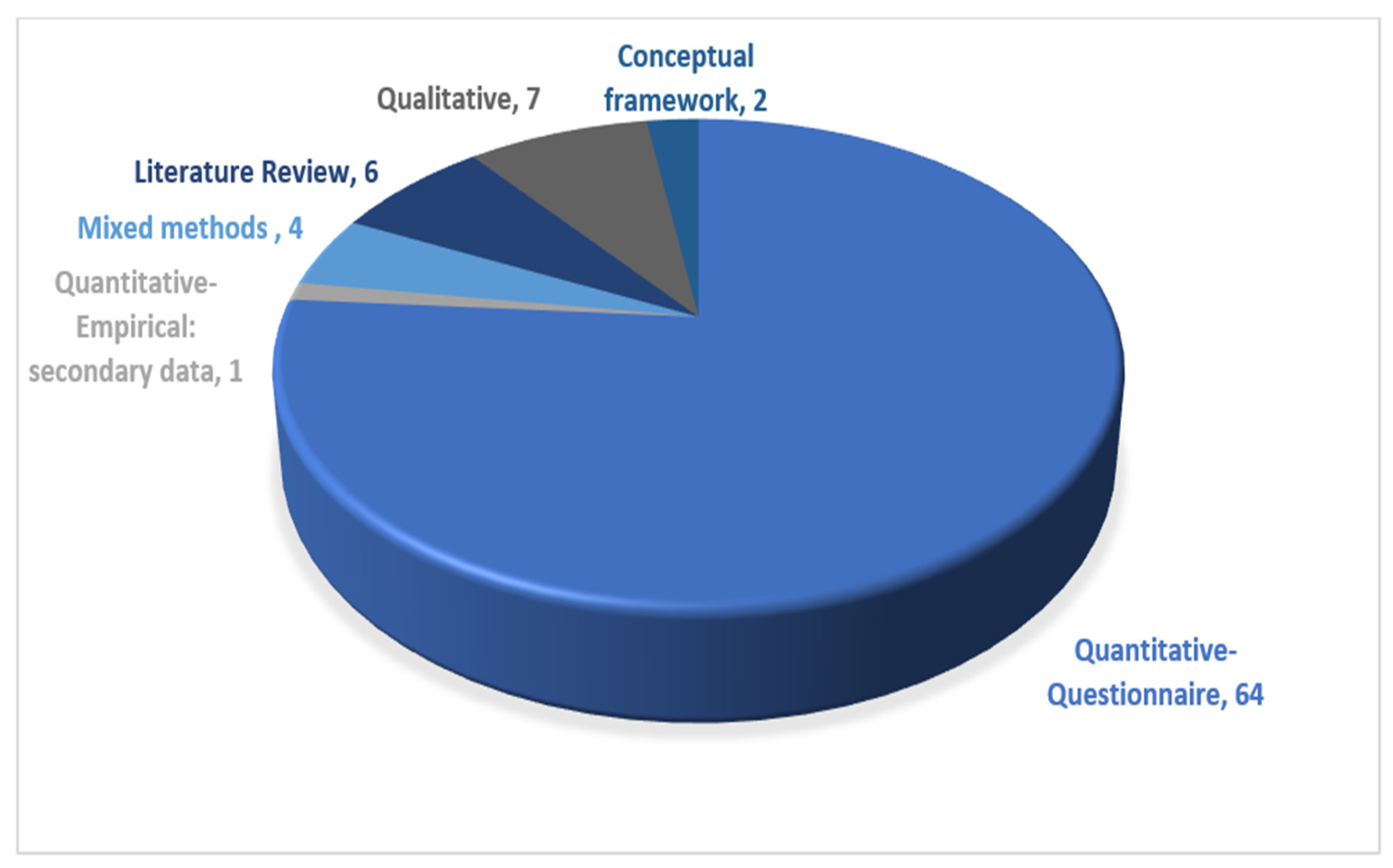

3.5. Methods (M)

4. Discussion

4.1. Managerial Level Implications

4.2. Policy Implications

4.3. Academic Research Implications

5. Research Gaps and Future Research Agenda

5.1. Theories—Future Agenda

- Most of the studies have examined technology acceptance theories and models in the fintech adoption context. This includes TAM and UTAUT. Future research could combine these theories with other models, such as The DeLone and McLean Model of Information Systems (IS) Success Model [102], to provide a better understanding of the most significant factors that affect fintech adoption by consumers.

- The electronic Word of Mouth (eWOM) theory is considered a multi-disciplinary theory that combines sociology, marketing, and IS literatures. Ref. [103] found that there is an association between eWOM and consumers’ purchasing intention. Hence, examining the eWOM impact or association with the acceptance of fintech app payment services can be considered in future research.

- The impulsive buying behaviour theory has been employed by some recent studies, particularly on the BNPL service e.g., [17,44]. Studies on other themes (i.e., e-wallet, mobile payment) have also considered this theory. Future studies can examine consumers’ acceptance of one of the fintech app payment services based on impulsive buying behaviour. This is particularly important, as the world is becoming a cashless society and fintech payment services may stimulate impulsive purchasing behaviour.

- Understanding the acceptance of fintech payment services is complicated, as it includes different stakeholders. Hence, future researchers are advised to develop new models that incorporate moderating and mediating effects for better understanding [56].

5.2. Context—Future Agenda

- Conducting more studies targeting countries other than the widely investigated ones. The MENA region is also one of the areas that have not been considered, although some of its countries’ governments (i.e., Saudi Arabia) have injected massive investments into fintech services. Hence, those countries can be considered in future research. Moreover, EU countries have been considered by a very limited number of studies, though some EU countries can be potential contexts for future studies (e.g., France, Sweden, and Austria).

- In terms of demographic context, most of the studies focused on young adults (Millennials) [10,29,92]. Older adults (above 50) commonly have different preferences, and this segment is highly neglected in the literature. It is recommended that future studies examine the challenges faced by the older generation (above 50) in accepting the usage of fintech payment services.

- Additionally, there is different technology acceptance behaviour between male and female consumers. Very few studies have considered the difference between male and female acceptance of fintech payment services e.g., [74]. Future studies are encouraged to differentiate between the acceptance of fintech payment services between males and females.

- Furthermore, variation in education level has not been considered widely, i.e., only considered by [17]. Future studies may consider how different educational levels influence the acceptance of fintech payment services.

- In terms of the themes/topics, it was found that the majority of studies have examined the fintech apps as a whole, with no specification of a certain app or payment service. Future studies may consider specification and focus on examining the acceptance of a particular fintech payment service. For instance, the BNPL is one of the themes that can be highly considered in future research, particularly using a quantitative approach for testing the factors influencing the consumer acceptance of the BNPL mechanism. To the best of our knowledge, only [17] examined some factors in Dhaka city (Bangladesh). Hence, this theme can be highly considered in the future.

5.3. Construct—Future Agenda

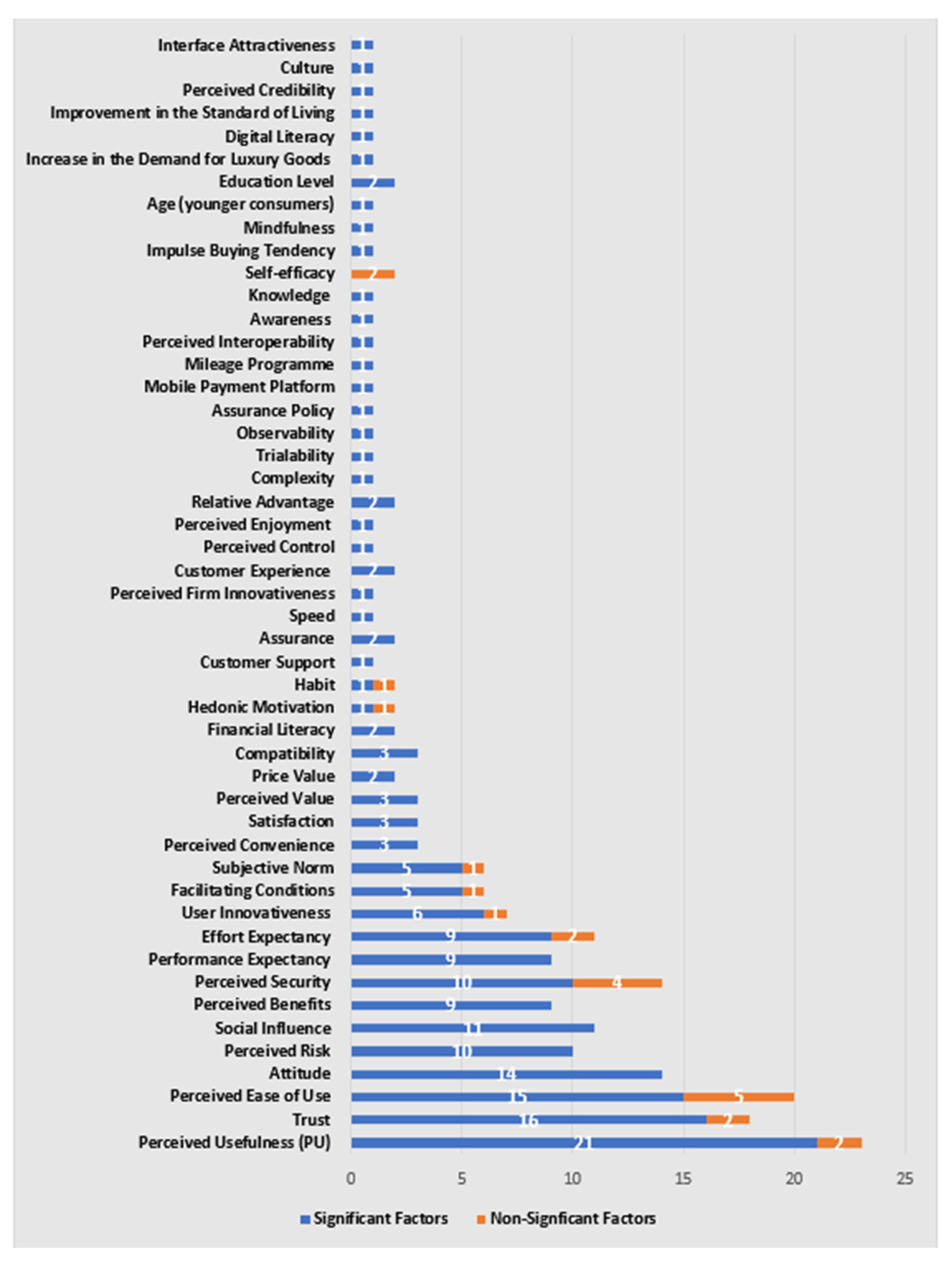

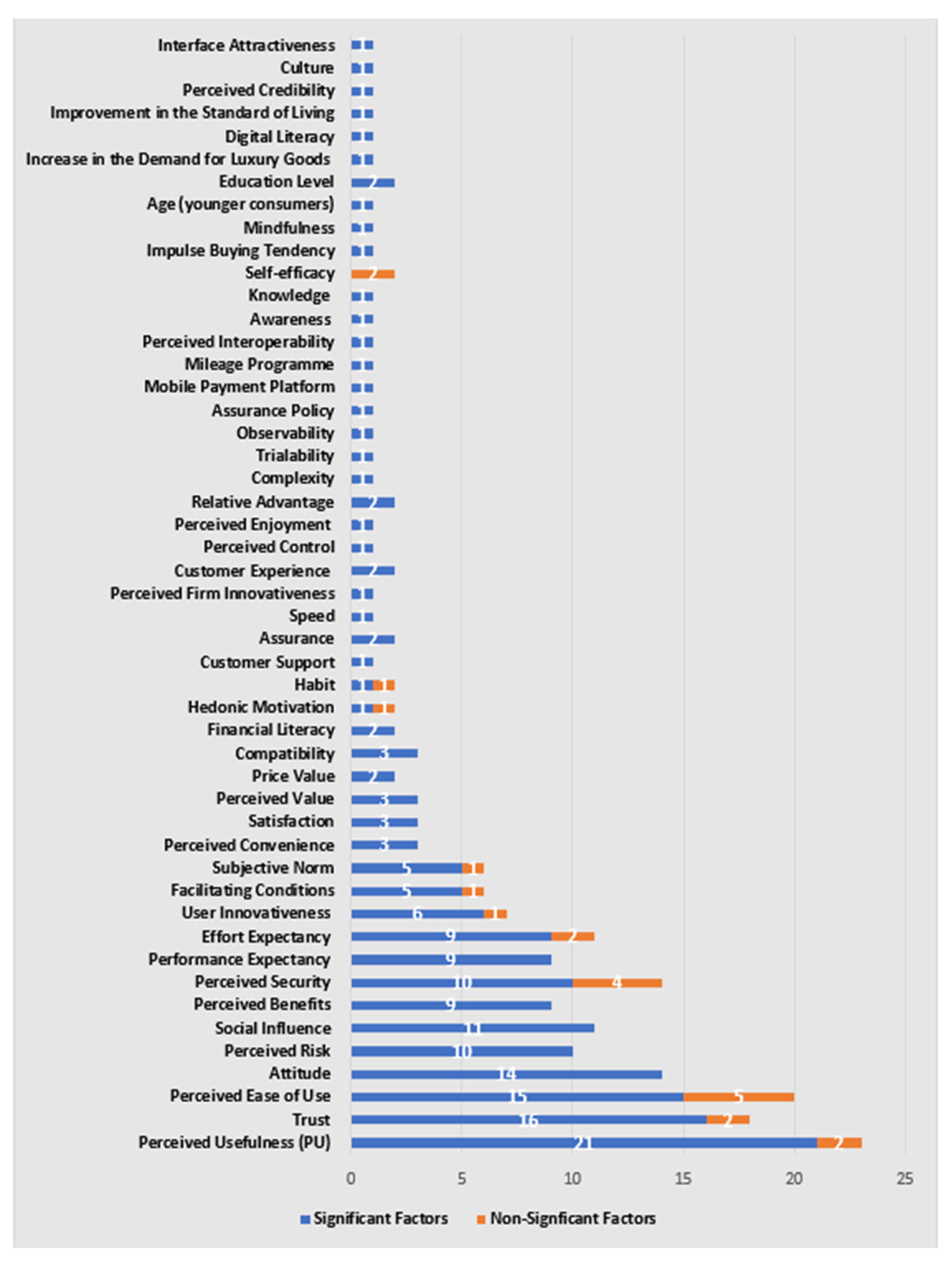

- Examine the factors that have been considered in other fintech payment services acceptance in the BNPL context (i.e., perceived usefulness, trust, perceived ease of use, perceived security, perceived convenience, awareness, etc.) (Figure 6 gives more factors).

- Impulsive buying behaviour can be a factor to be studied in e-wallet and mobile payment acceptance, especially as these themes have a low number of articles, based on the reviewed literature. This factor is essential, as some studies argue that once an individual puts money into his/her e-wallet, it is regarded as spent [104]. Hence, consumers may believe that e-wallet money must be spent (impulsive buying behaviour).

5.4. Methods—Future Agenda

- Future research may consider secondary data, for instance, using the number of transactions by each fintech payment service provider [16]. More importantly, secondary data can be used in examining causality between some factors and consumer acceptance of fintech payment services by applying Difference-in-Differences (DiD) tests.

- It was also noticed that use of a qualitative approach is very limited; hence gathering an in-depth understanding of consumers’ beliefs and experience is recommended. In such cases NVivo and other tools can be utilized.

- A mixed-methods approach is rarely used in the reviewed literature. While it is a more complex approach, it can be considered in future research, as it provides a thorough understanding of consumers’ acceptance.

6. Research Contributions

- First, the present paper can be followed in the phase of collecting data from databases, i.e., the SPAR-4-SLR protocol [13]. This approach has not been followed in the literature review studies in the consumer adoption of fintech services. Applying this protocol can guide future researchers in conducting literature reviews.

- Second, the paper is distinctive as it followed the TCCM framework presented by [14] in the analysis and results, which has not been followed in the literature review studies in the consumer adoption of fintech services. This can also guide future researchers to follow a framework in conducting literature reviews.

- Third, the current study is unique as it synthesizes recent studies by covering the period from the beginning of the emergence of studies related to fintech payment services and consumer acceptance (2015) until April 2023. Future researchers who are interested in this subject can benefit from this literature, as it covers the studies from the beginning of the emergence of this context.

- Fourth is the inclusion of a newly established fintech payment service, i.e., BNPL, which has been one of the trending fintech solutions that have received recent attention in academic studies [15,16,17,18]. Due to its recent emergence, we found that there has been no systematic review, until now, that has covered this fintech payment service. The current study includes this new fintech service and its acceptance by consumers in its review to provide a better understanding for future researchers.

- Fifth, the study contributes conceptually by identifying and summarizing the theories and factors influencing the adoption and acceptance of fintech apps in payment services. As a result, future researchers can examine other theories and factors in different geographical contexts.

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ferraz, R.M.; da Veiga, C.P.; da Veiga, C.R.P.; Furquim, T.S.G.; da Silva, W.V. After-Sales Attributes in E-Commerce: A Systematic Literature Review and Future Research Agenda. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 475–500. [Google Scholar] [CrossRef]

- Bălan, C. Chatbots and Voice Assistants: Digital Transformers of the Company–Customer Interface—A Systematic Review of the Business Research Literature. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 995–1019. [Google Scholar] [CrossRef]

- Yang, X.; Yang, J.; Hou, Y.; Li, S.; Sun, S. Gamification of mobile wallet as an unconventional innovation for promoting Fintech: An fsQCA approach. J. Bus. Res. 2023, 155, 113406. [Google Scholar] [CrossRef]

- Bommer, W.H.; Milevoj, E.; Rana, S. A meta-analytic examination of the antecedents explaining the intention to use fintech. Ind. Manag. Data Syst. 2023, 123, 886–909. [Google Scholar] [CrossRef]

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An empirical study of the impacts of perceived security and knowledge on continuous intention to use mobile fintech payment services. Int. J. Hum. Comput. Interact. 2019, 35, 886–898. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola, M.D.M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Schueffel, P. Taming the beast: A scientific definition of fintech. J. Innov. Manag. 2016, 4, 32–54. [Google Scholar] [CrossRef]

- Alwi, S. Fintech as financial inclusion: Factors affecting behavioral intention to accept mobile e-wallet during COVID-19 outbreak. Turk. J. Comput. Math. Educ. 2021, 12, 2130–2141. [Google Scholar]

- Ernst & Young Global Fintech Adoption Index 2019. 2019. Available online: https://www.ey.com/en_gl/ey-global-fintech-adoption-index (accessed on 11 February 2023).

- Daragmeh, A.; Lentner, C.; Sági, J. FinTech payments in the era of COVID-19: Factors influencing behavioral intentions of “Generation X” in Hungary to use mobile payment. J. Behav. Exp. Finance 2021, 32, 100574. [Google Scholar] [CrossRef] [PubMed]

- Kajol, K.; Singh, R.; Paul, J. Adoption of digital financial transactions: A review of literature and future research agenda. Technol. Forecast. Soc. Chang. 2022, 184, 121991. [Google Scholar] [CrossRef]

- Furquim, T.S.G.; da Veiga, C.P.; Veiga, C.R.P.D.; Silva, W.V.D. The Different Phases of the Omnichannel Consumer Buying Journey: A Systematic Literature Review and Future Research Directions. J. Theor. Appl. Electron. Commer. Res. 2022, 18, 79–104. [Google Scholar] [CrossRef]

- Paul, J.; Lim, W.M.; O’Cass, A.; Hao, A.W.; Bresciani, S. Scientific procedures and rationales for systematic literature reviews (SPAR-4-SLR). Int. J. Consum. Stud. 2021, 45, 1–16. [Google Scholar] [CrossRef]

- Paul, J.; Rosado-Serrano, A. Gradual internationalization vs born-global/international new venture models: A review and research agenda. Int. Mark. Rev. 2019, 36, 830–858. [Google Scholar] [CrossRef]

- Aalders, R. Buy now, pay later: Redefining indebted users as responsible consumers. Inf. Commun. Soc. 2023, 26, 941–956. [Google Scholar] [CrossRef]

- Guttman-Kenney, B.; Firth, C.; Gathergood, J. Buy now, pay later (BNPL)… on your credit card. J. Behav. Exp. Finance 2023, 37, 100788. [Google Scholar] [CrossRef]

- Khan, M.; Haque, S. Impact of Buy Now-Pay Later Mechanism through Installment Payment Facility and Credit Card Usage on the Impulsive Purchase Decision of Consumers: Evidence from Dhaka City. Southeast Univ. J. Arts Soc. Sci. 2021, 3, 40–59. [Google Scholar]

- Tan, G.K.S. Buy what you want, today! Platform ecologies of ‘buy now, pay later’services in Singapore. Trans. Inst. Br. Geogr. 2022, 47, 912–926. [Google Scholar] [CrossRef]

- Păuceanu, A.M.; Văduva, S.; Nedelcuț, A.C. Social Commerce in Europe: A Literature Review and Implications for Researchers, Practitioners, and Policymakers. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 1283–1300. [Google Scholar] [CrossRef]

- Korte, A.; Tiberius, V.; Brem, A. Internet of Things (IoT) technology research in business and management literature: Results from a co-citation analysis. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2073–2090. [Google Scholar] [CrossRef]

- Prados-Castillo, J.F.; Guaita Martínez, J.M.; Zielińska, A.; Gorgues Comas, D. A Review of Blockchain Technology Adoption in the Tourism Industry from a Sustainability Perspective. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 814–830. [Google Scholar] [CrossRef]

- Mishra, R.; Singh, R.K.; Koles, B. Consumer decision-making in Omnichannel retailing: Literature review and future research agenda. Int. J. Consum. Stud. 2021, 45, 147–174. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C. Artificial Intelligence in FinTech: Understanding robo-advisors adoption among customers. Ind. Manag. Data Syst. 2019, 119, 1411–1430. [Google Scholar] [CrossRef]

- Chuang, L.M.; Liu, C.C.; Kao, H.K. The adoption of fintech service: TAM perspective. Int. J. Manag. Adm. Sci. 2016, 3, 1–15. [Google Scholar]

- Stewart, H.; Jürjens, J. Data security and consumer trust in FinTech innovation in Germany. Inf. Comput. Secur. 2018, 26, 109–128. [Google Scholar] [CrossRef]

- Shiau, W.L.; Yuan, Y.; Pu, X.; Ray, S.; Chen, C.C. Understanding fintech continuance: Perspectives from self-efficacy and ECT-IS theories. Ind. Manag. Data Syst. 2020, 120, 1659–1689. [Google Scholar] [CrossRef]

- Barbu, C.M.; Florea, D.L.; Dabija, D.C.; Barbu, M.C.R. Customer experience in fintech. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1415–1433. [Google Scholar] [CrossRef]

- Kim, Y.; Park, Y.J.; Choi, J.; Yeon, J. An empirical study on the adoption of “Fintech” service: Focused on mobile payment services. Adv. Sci. Technol. Lett. 2015, 114, 136–140. [Google Scholar] [CrossRef]

- Singh, S.; Sahni, M.M.; Kovid, R.K. What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model. Manag. Decis. 2020, 58, 1675–1697. [Google Scholar] [CrossRef]

- Nathan, R.J.; Setiawan, B.; Quynh, M.N. Fintech and financial health in Vietnam during the COVID-19 pandemic: In-depth descriptive analysis. J. Risk Financ. Manag. 2022, 15, 125. [Google Scholar] [CrossRef]

- Alshari, H.A.; Lokhande, M.A. The impact of demographic factors of clients’ attitudes and their intentions to use FinTech services on the banking sector in the least developed countries. Cogent Bus. Manag. 2022, 9, 2114305. [Google Scholar] [CrossRef]

- Aseng, A.C. Factors Influencing Generation Z Intention in Using FinTech Digital Payment Services. CogITo Smart J. 2020, 6, 155–166. [Google Scholar] [CrossRef]

- Karim, R.A.; Sobhani, F.A.; Rabiul, M.K.; Lepee, N.J.; Kabir, M.R.; Chowdhury, M.A.M. Linking Fintech Payment Services and Customer Loyalty Intention in the Hospitality Industry: The Mediating Role of Customer Experience and Attitude. Sustainability 2022, 14, 16481. [Google Scholar] [CrossRef]

- Koroleva, E. Attitude Towards Using Fintech Services: Digital Immigrants Versus Digital Natives. Int. J. Innov. Technol. Manag. 2022, 19, 2250029. [Google Scholar] [CrossRef]

- Lee, C.T.; Pan, L.Y. Smile to pay: Predicting continuous usage intention toward contactless payment services in the post-COVID-19 era. Int. J. Bank Mark. 2023, 41, 312–332. [Google Scholar] [CrossRef]

- Mainardes, E.W.; Costa, P.M.F.; Nossa, S.N. Customers’ satisfaction with fintech services: Evidence from Brazil. J. Financ. Serv. Mark. 2023, 28, 378–395. [Google Scholar] [CrossRef]

- Ngo, H.T.; Nguyen, L.T.H. Consumer adoption intention toward FinTech services in a bank-based financial system in Vietnam. J. Financ. Regul. Compliance 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Roh, T.; Yang, Y.S.; Xiao, S.; Park, B.I. What makes consumers trust and adopt fintech? An empirical investigation in China. Electron. Commer. Res. 2022, 1–33. [Google Scholar] [CrossRef]

- Souza, M.V.D.; Spers, E.E. Proposal of the FinTech’s Services Adoption Measurement Model. Rev. Adm. Dialogo 2021, 30, 96–114. [Google Scholar]

- Wang, Z.; Guan, Z.; Hou, F.; Li, B.; Zhou, W. What determines customers’ continuance intention of FinTech? Evidence from YuEbao. Ind. Manag. Data Syst. 2019, 119, 1625–1637. [Google Scholar] [CrossRef]

- Yan, C.; Siddik, A.B.; Akter, N.; Dong, Q. Factors influencing the adoption intention of using mobile financial service during the COVID-19 pandemic: The role of FinTech. Environ. Sci. Pollut. Res. 2021, 30, 61271–61289. [Google Scholar] [CrossRef] [PubMed]

- Ah Fook, L.; McNeill, L. Click to buy: The impact of retail credit on over-consumption in the online environment. Sustainability 2020, 12, 7322. [Google Scholar] [CrossRef]

- Burton, D. Digital debt collection and ecologies of consumer overindebtedness. Econ. Geogr. 2020, 96, 244–265. [Google Scholar] [CrossRef]

- Feng, L.; Teng, J.T.; Zhou, F. Pricing and lot-sizing decisions on buy-now-and-pay-later installments through a product life cycle. Eur. J. Oper. Res. 2023, 306, 754–763. [Google Scholar] [CrossRef]

- Gerrans, P.; Baur, D.G.; Lavagna-Slater, S. Fintech and responsibility: Buy-now-pay-later arrangements. Aust. J. Manag. 2022, 47, 474–502. [Google Scholar] [CrossRef]

- Johnson, D.; Rodwell, J.; Hendry, T. Analyzing the impacts of financial services regulation to make the case that buy-now-pay-later regulation is failing. Sustainability 2021, 13, 1992. [Google Scholar] [CrossRef]

- Pattamatta, P.; Dabadghao, S.S. Models for Point-of-Sale (POS) Market Entry. FinTech 2022, 1, 318–324. [Google Scholar] [CrossRef]

- Schomburgk, L.; Hoffmann, A. How mindfulness reduces BNPL usage and how that relates to overall well-being. Eur. J. Mark. 2023, 57, 325–359. [Google Scholar] [CrossRef]

- Abdillah, L.A. FinTech E-commerce payment application user experience analysis during COVID-19 pandemic. arXiv 2020, arXiv:2012.07750. [Google Scholar]

- Johan, S. Users’ acceptance of financial technology in an emerging market (An empirical study in Indonesia). J. Ekon. Dan Bisnis 2020, 23, 173–188. [Google Scholar] [CrossRef]

- Alwi, S.; Salleh, M.N.M.; Kamaruddin, H.; Alpandi, R.M.; Razak, S.E.A. The e-wallet usage as an acceptance indicator on Financial Technology in Malaysia. Relig. Rev. Cienc. Soc. Humanid. 2019, 4, 45–52. [Google Scholar]

- Karim, M.W.; Chowdhury, M.A.M.; Haque, A.A. A Study of Customer Satisfaction Towards E-Wallet Payment System in Bangladesh. Am. J. Econ. Bus. Innov. 2022, 1, 1–10. [Google Scholar] [CrossRef]

- Yeh, H. Factors in the ecosystem of mobile payment affecting its use: From the customers’ perspective in Taiwan. J. Theor. Appl. Electron. Commer. Res. 2020, 15, 13–29. [Google Scholar] [CrossRef]

- Abdul-Rahim, R.; Bohari, S.A.; Aman, A.; Awang, Z. Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability 2022, 14, 8357. [Google Scholar] [CrossRef]

- Agustiningsih, M.D.; Savitrah, R.M.; Lestari, P.C.A. Indonesian young consumers’ intention to donate using sharia fintech. Asian J. Islam. Manag. AJIM 2021, 3, 34–44. [Google Scholar] [CrossRef]

- Al Nawayseh, M.K. Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of fintech applications? J. Open Innov. Technol. Mark. Complex. 2020, 6, 153. [Google Scholar] [CrossRef]

- Darmansyah, D.; Fianto, B.A.; Hendratmi, A.; Aziz, P.F. Factors determining behavioral intentions to use Islamic financial technology: Three competing models. J. Islam. Mark. 2020, 12, 794–812. [Google Scholar] [CrossRef]

- Datta, D. The Future of Financial Inclusion Through Fintech: A Conceptual Study in Post Pandemic India. Sachetas 2023, 2, 11–17. [Google Scholar] [CrossRef] [PubMed]

- Handarkho, Y.D.; Harjoseputro, Y.; Samodra, J.E.; Irianto, A.B.P. Understanding proximity mobile payment continuance usage in Indonesia from a habit perspective. J. Asia Bus. Stud. 2021, 15, 420–440. [Google Scholar] [CrossRef]

- Lantang, A.P.; Pangemanan, S.S.; Tielung, M.V. The Influence of Ease of Use and Facility Towards Customer Satisfaction on Fintech Digital Payment. J. Ris. Ekon. Manaj. Bisnis Dan Akunt. 2021, 9, 406–414. [Google Scholar]

- Lee, Y.K. Higher innovativeness, lower technostress?: Comparative study of determinants on FinTech usage behavior between Korean and Chinese Gen Z consumers. Asia Pac. J. Mark. Logist. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Mascarenhas, A.B.; Perpétuo, C.K.; Barrote, E.B.; Perides, M.P. The influence of perceptions of risks and benefits on the continuity of use of fintech services. Braz. Bus. Rev. 2021, 18, 1–21. [Google Scholar] [CrossRef]

- Ming, K.L.Y.; Jais, M. Factors affecting the intention to use e-wallets during the COVID-19 pandemic. Gadjah Mada Int. J. Bus. 2022, 24, 82–100. [Google Scholar] [CrossRef]

- Nan, D.; Kim, Y.; Huang, J.; Jung, H.S.; Kim, J.H. Factors affecting intention of consumers in using face recognition payment in offline markets: An acceptance model for future payment service. Front. Psychol. 2022, 13, 830152. [Google Scholar] [CrossRef] [PubMed]

- Nurfadilah, D.; Samidi, S. How The COVID-19 Crisis is Affecting Customers’ Intentions to Use Islamic Fintech Services: Evidence from Indonesia. J. Islam. Monet. Econ. Finance 2021, 7, 83–114. [Google Scholar] [CrossRef]

- Oladapo, I.A.; Hamoudah, M.M.; Alam, M.M.; Olaopa, O.R.; Muda, R. Customers’ perceptions of FinTech adaptability in the Islamic banking sector: Comparative study on Malaysia and Saudi Arabia. J. Model. Manag. 2022, 17, 1241–1261. [Google Scholar] [CrossRef]

- Purba, J.; Samuel, S.; Budiono, S. Collaboration of digital payment usage decision in COVID-19 pandemic situation: Evidence from Indonesia. Int. J. Data Netw. Sci. 2021, 5, 557–568. [Google Scholar] [CrossRef]

- Shahzad, A.; Zahrullail, N.; Akbar, A.; Mohelska, H.; Hussain, A. COVID-19’s Impact on Fintech Adoption: Behavioral Intention to Use the Financial Portal. J. Risk Financ. Manag. 2022, 15, 428. [Google Scholar] [CrossRef]

- Spulbar, C.; Birau, R.; Calugaru, T.; Mehdiabadi, A. Considerations regarding FinTech and its multidimensional implications on financial systems. Rev. Stiinte Politice 2020, 68, 77–86. [Google Scholar]

- Susilo, A.Z.; Prabowo, M.I.; Taman, A.; Pustikaningsih, A.; Samlawi, A. A comparative study of factors affecting user acceptance of go-pay and OVO as a feature of Fintech application. Procedia Comput. Sci. 2019, 161, 876–884. [Google Scholar] [CrossRef]

- Tang, K.L.; Ooi, C.K.; Chong, J.B. Perceived risk factors affect intention to use FinTech. J. Account. Finance Emerg. Econ. 2020, 6, 453–463. [Google Scholar] [CrossRef]

- Tun-Pin, C.; Keng-Soon, W.C.; Yen-San, Y.; Pui-Yee, C.; Hong-Leong, J.T.; Shwu-Shing, N. An adoption of fintech service in Malaysia. South East Asia J. Contemp. Bus. 2019, 18, 134–147. [Google Scholar]

- Vaicondam, Y.; Jayabalan, N.; Tong, C.X.; Qureshi, M.I.; Khan, N. Fintech Adoption Among Millennials in Selangor. Acad. Entrep. J. 2021, 27, 1–14. [Google Scholar]

- Wang, J.S. Exploring biometric identification in FinTech applications based on the modified TAM. Financ. Innov. 2021, 7, 42. [Google Scholar] [CrossRef]

- Wardani, D.; Wulandari, N.; Baskara, C.A. Understanding Customer Acceptance To Financial Technology; Study In Indonesia. Int. J. Innov. Technol. Econ. 2021, 2, 1–10. [Google Scholar] [CrossRef]

- Weichert, M. The future of payments: How FinTech players are accelerating customer-driven innovation in financial services. J. Paym. Strategy Syst. 2017, 11, 23–33. [Google Scholar]

- Won-jun, L. Understanding consumer acceptance of Fintech Service: An extension of the TAM Model to understand Bitcoin. IOSR J. Bus. Manag. 2018, 20, 34–37. [Google Scholar]

- Zhang, L.L.; Kim, H. The influence of financial service characteristics on use intention through customer satisfaction with mobile fintech. J. Syst. Manag. Sci. 2020, 10, 82–94. [Google Scholar] [CrossRef]

- Ali, M.; Raza, S.A.; Khamis, B.; Puah, C.H.; Amin, H. How perceived risk, benefit and trust determine user Fintech adoption: A new dimension for Islamic finance. Foresight 2021, 23, 403–420. [Google Scholar] [CrossRef]

- Bakri, M.H.; Yahaya, S.N. Conceptualization of Spiritual intelligence quotient (SQ) in the Islamic Fintech adoption. Islamiyyat 2020, 42, 113–122. [Google Scholar] [CrossRef]

- Maryam, S.Z.; Ahmed, A.; Haider, S.W.; Akhter, T. Explicating the adoption of an innovation Fintech Value Chain Financing from Aarti (Middlemen) perspective in Pakistan. Afr. J. Sci. Technol. Innov. Dev. 2023, 15, 429–439. [Google Scholar] [CrossRef]

- Rahim, N.F.; Bakri, M.H.; Fianto, B.A.; Zainal, N.; Hussein Al Shami, S.A. Measurement and structural modelling on factors of Islamic Fintech adoption among millennials in Malaysia. J. Islam. Mark. 2022, 14, 1463–1487. [Google Scholar] [CrossRef]

- Shaikh, I.M.; Qureshi, M.A.; Noordin, K.; Shaikh, J.M.; Khan, A.; Shahbaz, M.S. Acceptance of Islamic financial technology (FinTech) banking services by Malaysian users: An extension of technology acceptance model. Foresight 2020, 22, 367–383. [Google Scholar] [CrossRef]

- Belanche, D.; Guinalíu, M.; Albás, P. Customer adoption of p2p mobile payment systems: The role of perceived risk. Telemat. Inform. 2022, 72, 101851. [Google Scholar] [CrossRef]

- Choi, H.; Park, J.; Kim, J.; Jung, Y. Consumer preferences of attributes of mobile payment services in South Korea. Telemat. Inform. 2020, 51, 101397. [Google Scholar] [CrossRef]

- Diana, N.; Leon, F.M. Factors affecting continuance intention of FinTech payment among Millennials in Jakarta. Eur. J. Bus. Manag. Res. 2020, 5, 1–9. [Google Scholar] [CrossRef]

- Haritha, P.H. Mobile payment service adoption: Understanding customers for an application of emerging financial technology. Inf. Comput. Secur. 2023, 31, 145–171. [Google Scholar] [CrossRef]

- Hassan, M.S.; Islam, M.A.; Sobhani, F.A.; Nasir, H.; Mahmud, I.; Zahra, F.T. Drivers influencing the adoption intention towards mobile fintech services: A study on the emerging Bangladesh market. Information 2022, 13, 349. [Google Scholar] [CrossRef]

- Hwang, Y.; Park, S.; Shin, N. Sustainable development of a mobile payment security environment using fintech solutions. Sustainability 2021, 13, 8375. [Google Scholar] [CrossRef]

- Khuong, N.V.; Phuong, N.T.T.; Liem, N.T.; Thuy, C.T.M.; Son, T.H. Factors Affecting the Intention to Use Financial Technology among Vietnamese Youth: Research in the Time of COVID-19 and Beyond. Economies 2022, 10, 57. [Google Scholar] [CrossRef]

- Laksamana, P.; Suharyanto, S.; Cahaya, Y.F. Determining factors of continuance intention in mobile payment: Fintech industry perspective. Asia Pac. J. Mark. Logist. 2023, 35, 1699–1718. [Google Scholar] [CrossRef]

- Xie, J.; Ye, L.; Huang, W.; Ye, M. Understanding FinTech platform adoption: Impacts of perceived value and perceived risk. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1893–1911. [Google Scholar] [CrossRef]

- Yahaya, M.H.; Ahmad, K. Factors affecting the acceptance of financial technology among asnaf for the distribution of zakat in Selangor-A Study Using UTAUT. J. Islam. Finance 2019, 8, 35–46. [Google Scholar]

- Chan, R.; Troshani, I.; Rao Hill, S.; Hoffmann, A. Towards an understanding of consumers’ FinTech adoption: The case of Open Banking. Int. J. Bank Mark. 2022, 40, 886–917. [Google Scholar] [CrossRef]

- Singh, A.K.; Sharma, P. A study of Indian Gen X and Millennials consumers’ intention to use FinTech payment services during COVID-19 pandemic. J. Model. Manag. 2022, 18, 1177–1203. [Google Scholar] [CrossRef]

- Jebarajakirthy, C.; Maseeh, H.I.; Morshed, Z.; Shankar, A.; Arli, D.; Pentecost, R. Mobile advertising: A systematic literature review and future research agenda. Int. J. Consum. Stud. 2021, 45, 1258–1291. [Google Scholar] [CrossRef]

- Soriano, M.; Ziegler, T.; Umer, Z.; Chen, H.; Jenweeranon, P.; Zhang, B.Z.; Donald, D.C.; Lin, L.; Alam, N.; Luo, C.S.; et al. The ASEAN Fintech Ecosystem Benchmarking Study. 2019. Available online: https://ssrn.com/abstract=3772254 (accessed on 28 January 2023).

- Dwivedi, Y.K.; Rana, N.P.; Jeyaraj, A.; Clement, M.; Williams, M.D. Re-examining the unified theory of acceptance and use of technology (UTAUT): Towards a revised theoretical model. Inf. Syst. Front. 2019, 21, 719–734. [Google Scholar] [CrossRef]

- Lashitew, A.A.; van Tulder, R.; Liasse, Y. Mobile phones for financial inclusion: What explains the diffusion of mobile money innovations? Res. Policy 2019, 48, 1201–1215. [Google Scholar] [CrossRef]

- DeLone, W.H.; McLean, E.R. The DeLone and McLean model of information systems success: A ten-year update. J. Manag. Inf. Syst. 2003, 19, 9–30. [Google Scholar] [CrossRef]

- Odilia, G.; Sulistiobudi, R.A.; Fitriana, E. Factors Contributing to Online Shopping Behavior During COVID-19 Pandemic: The Power of Electronic Word of Mouth in Digital Generation. Acad. Entrep. J. 2022, 28, 1–10. [Google Scholar]

- Alam, M.M.; Awawdeh, A.E.; Muhamad, A.I.B. Using e-wallet for business process development: Challenges and prospects in Malaysia. Bus. Process Manag. J. 2021, 27, 1142–1162. [Google Scholar] [CrossRef]

- Suryono, R.R.; Budi, I.; Purwandari, B. Challenges and trends of financial technology (Fintech): A systematic literature review. Information 2020, 11, 590. [Google Scholar] [CrossRef]

- Giglio, F. Fintech: A literature review. Eur. Res. Stud. J. 2021, 24, 600–627. [Google Scholar] [CrossRef]

- Takeda, A.; Ito, Y. A review of FinTech research. Int. J. Technol. Manag. 2021, 86, 67–88. [Google Scholar] [CrossRef]

- Firmansyah, E.A.; Masri, M.; Anshari, M.; Besar, M.H.A. Factors affecting fintech adoption: A systematic literature review. FinTech 2022, 2, 21–30. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Bibliographic Data | Description | Criteria |

|---|---|---|

| Author(s) | Who is the author? | All |

| Journal | In which journal was the paper published? | All |

| Year of publication | When was the article published? | Up to April 2023 |

| Title | What is the title of the paper? | All |

| Geographical focus | Where do the data come from? | All |

| Aim/Goals | What are the main goals of the study? | All |

| Major themes | What are the major themes of fintech studies? | All |

| Type of research article | What is the nature of the research article? | Qualitative, Quantitative, Literature Review, Conceptual Framework, or Mixed Methods |

| Data collection method | What is the data collection method? | All |

| Sample size | What is the sample size? | All |

| Data analysis method | What is the data analysis method? | All |

| Theoretical approach | Which theories has the study utilized? | All |

| Dependent variables | What dependent variables are explored in the study? | All |

| Main findings | What are the main findings of the study? | All |

| Citations | What is the number of citations, based on Google Scholar? | All |

| # | Author(s) | Journal Name | Title | Total Citations (Based on Google Scholar) |

|---|---|---|---|---|

| 1 | Gomber et al. [23] | Journal of Management Information Systems, | On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services | 1066 |

| 2 | Hu et al. [24] | Symmetry | Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model | 348 |

| 3 | Belanche et al. [25] | Industrial Management & Data Systems | Artificial Intelligence in FinTech: understanding robo-advisors adoption among customers | 341 |

| 4 | Chuang et al. [26] | International Journal of Management and Administrative Sciences | The adoption of fintech service: TAM perspective. | 278 |

| 5 | Stewart and Jürjens [27] | Information & Computer Security. | Data security and consumer trust in FinTech innovation in Germany | 207 |

| 6 | Lim et al. [5] | International Journal of Human–Computer Interaction | An empirical study of the impacts of perceived security and knowledge on continuous intention to use mobile fintech payment services | 193 |

| 7 | Shiau et al. [28] | Industrial Management & Data Systems | Understanding fintech continuance: perspectives from self-efficacy and ECT-IS theories | 157 |

| 8 | Barbu et al. [29] | Journal of Theoretical and Applied Electronic Commerce Research | Customer experience in fintech | 137 |

| 9 | Kim et al. [30] | Advanced Science and Technology Letters | An empirical study on the adoption of “Fintech” service: Focused on mobile payment services. | 120 |

| 10 | Singh et al. [31] | Management Decision | What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model | 110 |

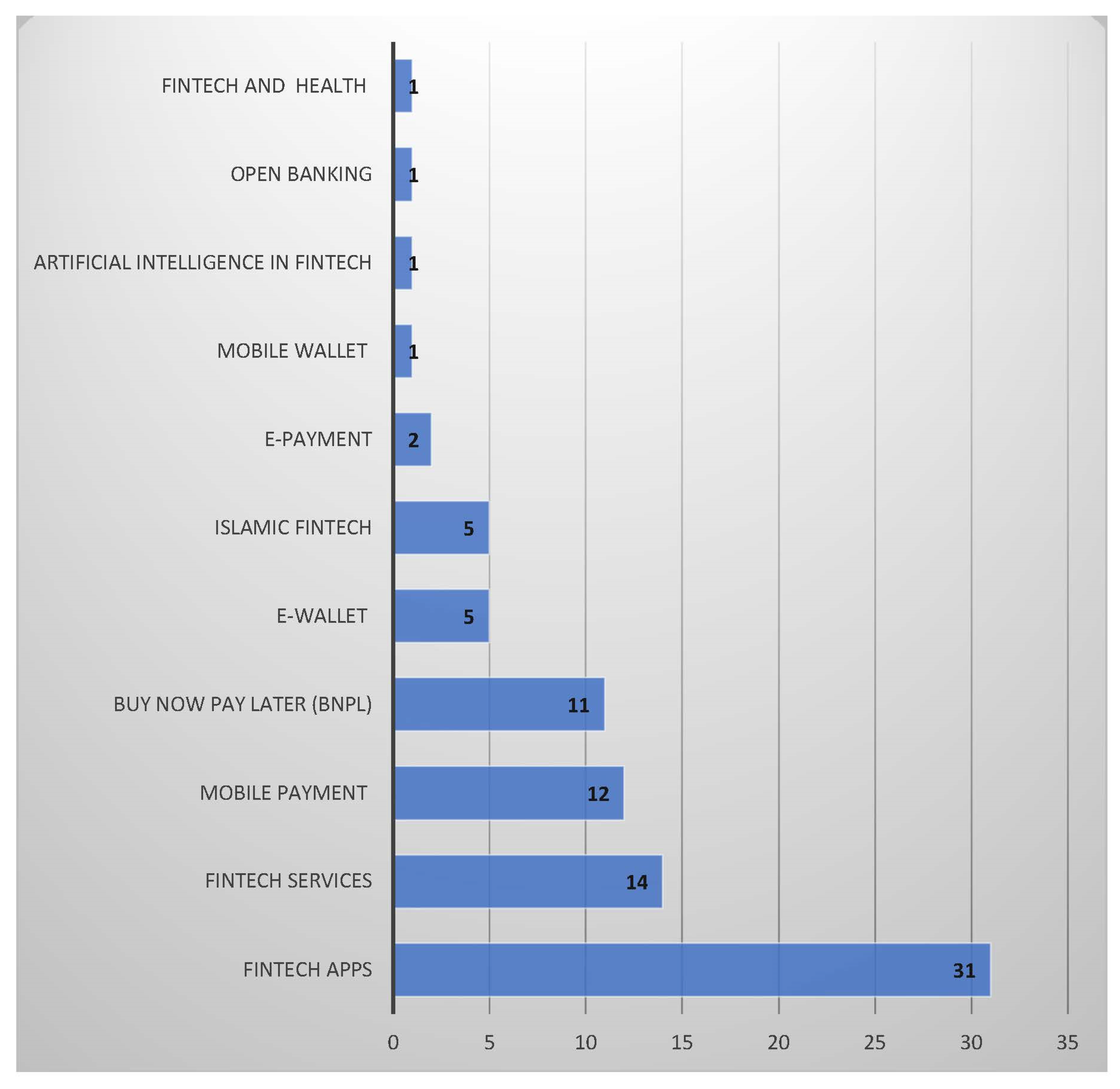

| Theme | Reference |

|---|---|

| Fintech and health | Nathan et al. [32] |

| Fintech Services | Alshari and Lokhande [33]; Aseng [34]; Chuang et al. [26]; Karim et al. [35]; Kim et al. [30]; Koroleva [36]; Lee and Pan [37]; Mainardes et al. [38]; Ngo and Nguyen [39]; Roh et al. [40]; Singh et al. [31]; Souza and Spers [41]; Wang et al. [42]; Yan et al. [43] |

| Artificial Intelligence in fintech | Belanche et al. [25] |

| Buy Now Pay Later (BNPL) | Aalders [15]; Ah Fook and McNeill [44]; DawnBurton [45]; Feng et al. [46]; Gerrans et al. [47]; Johnson et al. [48]; Khan and Haque [17]; Pattamatta and Dabadghao [49]; Schomburgk and Hoffmann [50]; Tan [18] |

| e-payment | Abdillah [51]; Johan [52] |

| e-wallet | Alwi et al. [53]; Alwi [8]; Karim et al. [54]; Lim et al. [5]; Yeh [55] |

| Fintech apps | Abdul-Rahim et al. [56]; Agustiningsih et al. [57]; Al Nawayseh [58]; Barbu et al. [29]; Daragmeh et al. [10]; Darmansyah et al. [59]; Datta [60]; Handarkho et al. [61]; Hu et al. [24]; Lantang et al. [62]; Lee [63]; Mascarenhas et al. [64]; Ming and Jais [65]; Nan et al. [66]; Nurfadilah and Samidi [67]; Oladapo et al. [68]; Purba et al. [69]; Shahzad et al. [70]; Shiau et al. [28]; Singh et al. [31]; Spulbar et al. [71]; Stewart et al. [27], Susilo et al. [72]; Tang et al. [73]; Tun-Pin et al. [74]; Vaicondam et al. [75]; Wang [76]; Wardani et al. [77]; Weichert [78]; Won-jun [79]; Zhang and Kim [80] |

| Islamic Fintech | Ali et al. [81]; Bakri and Yahaya [82]; Maryam et al. [83]; Rahim et al. [84]; Shaikh et al. [85] |

| Mobile payment | Belanche et al. [86]; Bommer et al. [4]; Choi et al. [87]; Diana and Leon [88]; Gomber et al. [23]; Haritha [89]; Hassan et al. [90]; Hwang et al. [91]; Khuong et al. [92]; Laksamana et al. [93]; Xie et al. [94]; Yahaya and Ahmad [95] |

| Mobile wallet | Yang et al. [3] |

| Open Banking | Chan et al. [96] |

| # | Factor | Supported | Not Supported |

|---|---|---|---|

| 1 | Perceived Usefulness (PU) | Agustiningsih et al. [57]; Alshari and Lokhande [33]; Chuang et al. [26]; Daragmeh et al. [10]; Handarkho et al. [61]; Haritha [89]; Hu et al. [24]; Lantang et al. [62]; Ming and Jais [65]; Nurfadilah and Samidi [67]; Shaikh et al. [85]; Singh et al. [31]; Susilo et al. [72]; Tun-Pin et al. [73]; Vaicondam et al. [74]; Won-jun [78]; Laksamana et al. [92]; Mainardes et al. [37]; Nathan et al. [31]; Shiau et al. [27]; Singh and Sharma [97] | Shahzad et al. [70]; Belanche et al. [25] |

| 2 | Trust | Ali et al. [81]; Al Nawayseh [58]; Alshari and Lokhande [33]; Chuang et al. [26]; Hassan et al. [90]; Hwang et al. [91]; Purba et al. [69]; Shahzad et al. [70]; Stewart and Jürjens [27]; Vaicondam et al. [75]; Laksamana et al. [93]; Mainardes et al. [38]; Nathan et al. [32]; Roh et al. [40]; Wang et al. [42]; Yan et al. [43] | Nan et al. [66]; Nurfadilah and Samidi [67] |

| 3 | Perceived Ease of use | Alshari and Lokhande [33]; Chuang et al. [26]; Haritha [89]; Nurfadilah and Samidi [67]; Shaikh et al. [85]; Purba et al. [69]; Shahzad et al. [70]; Singh et al. [31]; Susilo et al. [72]; Tun-Pin et al. [74]; Vaicondam et al. [75]; Koroleva [36]; Laksamana et al. [93]; Nathan et al. [32]; Singh and Sharma [97] | Barbu et al. [29]; Daragmeh et al. [10]; Hu et al. [24]; Won-jun [79]; Mainardes et al. [38] |

| 4 | Attitude | Alshari and Lokhande [33]; Belanche et al. [86]; Chuang et al. [26]; Hu et al. [24]; Karim et al. [35]; Ming and Jais [65]; Nurfadilah and Samidi [67]; Oladapo et al. [68]; Susilo et al. [72]; Belanche et al. [25]; Koroleva [36]; Laksamana et al. [93]; Nathan et al. [32]; Roh et al. [40] | |

| 5 | Perceived Risk | Ali et al. [81]; Chan et al. [96]; Diana and Leon [88]; Hassan et al. [90]; Ming and Jais [65]; Nan et al. [66]; Tang et al. [73]; Xie et al. [94]; Laksamana et al. [93]; Singh and Sharma [97] | Belanche et al. [25]; Hu et al. [24]; Khuong et al. [92]; Mascarenhas et al. [64]; Vaicondam et al. [75] |

| 6 | Social Influence | Al Nawayseh [58]; Aseng [34]; Bommer et al. [4]; Chan et al. [96]; Hassan et al. [90]; Nan et al. [66]; Tun-Pin et al. [74]; Xie et al. [94]; Yahaya and Ahmad [94]; Rahim et al. [84]; Yan et al. [43] | Khuong et al. [91]; Singh et al. [30]; Wardani et al. [76] |

| 7 | Perceived Benefits | Abdul-Rahim et al. [56]; Ali et al. [81]; Al Nawayseh [58]; Diana and Leon [88]; Hassan et al. [90]; Khuong et al. [92]; Mascarenhas et al. [64]; Zhang and Kim [80]; Maryam et al. [83] | |

| 8 | Perceived Security | Aseng [34]; Bommer et al. [4]; Lee and Pan [37]; Stewart and Jürjens [27]; Tun-Pin et al. [74]; Won-jun [79]; Zhang and Kim [80]; Laksamana et al. [93]; Roh et al. [39]; Singh and Sharma [97] | Khuong et al. [92]; Lantang et al. [62]; Purba et al. [69]; Tang et al. [73] |

| 9 | Performance Expectancy | Aseng [34]; Bommer et al. [4]; Chan et al. [96]; Lee and Pan [37]; Nan et al. [66]; Wardani et al. [77]; Xie et al. [94]; Yahaya and Ahmad [95]; Rahim et al. [84] | |

| 10 | Effort Expectancy | Aseng [34]; Bommer et al. [4]; Chan et al. [96]; Lee and Pan [37]; Nan et al. [66]; Wardani et al. [77]; Xie et al. [94]; Maryam et al. [83]; Rahim et al. [84] | Hassan et al. [90]; Yahaya and Ahmad [95] |

| 11 | User Innovativeness | Shahzad et al. [70]; Shaikh et al. [85]; Tun-Pin et al. [74]; Lee [63]; Mainardes et al. [38]; Maryam et al. [83]; Nathan et al. [32] | Nurfadilah and Samidi [67] |

| 12 | Facilitating Conditions | Bommer et al. [4]; Haritha [89]; Hassan et al. [90]; Yahaya and Ahmad [95]; Rahim et al. [84] | Xie et al. [94] |

| 13 | Subjective Norm | Belanche et al. [25]; Daragmeh et al. [10]; Oladapo et al. [68]; Singh and Sharma [98]; Wang et al. [42]; | Belanche et al. [86] |

| 14 | Perceived Convenience | Hwang et al. [91]; Khuong et al. [92]; Zhang and Kim [80] | |

| 15 | Satisfaction | Handarkho et al. [61]; Lantang et al. [62]; Shiau et al. [28] | |

| 16 | Perceived Value | Barbu et al. [29]; Xie et al. [94]; Yan et al. [43] | |

| 17 | Compatibility | Handarkho et al. [61]; Lee and Pan [37]; Yeh [55] |

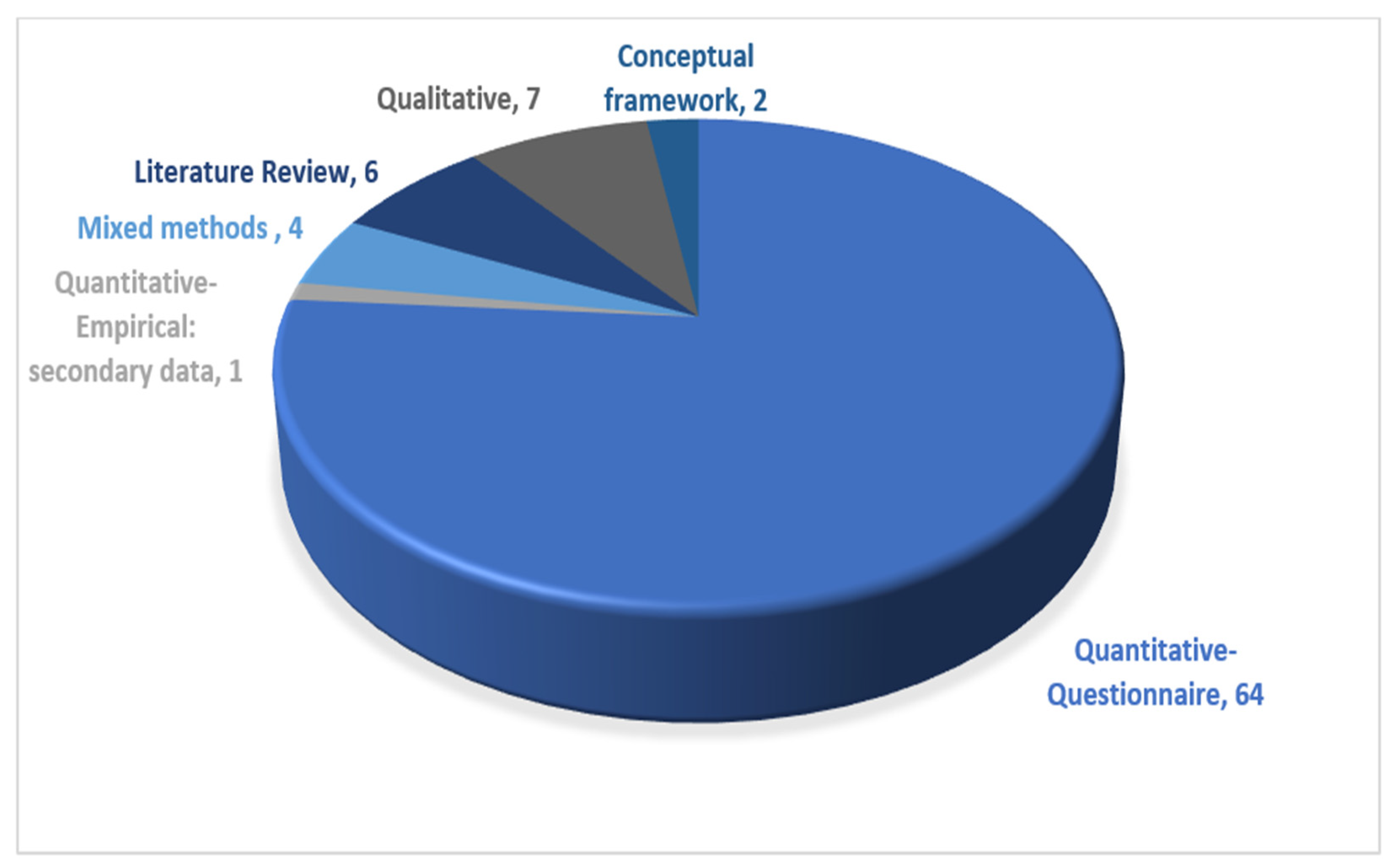

| Quantitative (Questionnaire) | Quantitative (Empirical Using Secondary Data) | Qualitative (Content Analysis) | Mixed Methods (Questionnaires and Interviews) | Literature Review | Conceptual Framework |

|---|---|---|---|---|---|

| Abdillah [51]; Abdul-Rahim et al. [56]; Agustiningsih et al. [57]; Ah Fook and McNeill [44]; Al Nawayseh [58]; Ali et al. [81]; Alshari and Lokhande [33]; Alwi et al. [53]; Aseng [34]; Barbu et al. [29]; Belanche et al. [25]; Belanche et al. [86]; Chan et al. [96]; Choi et al. [87]; Chuang et al. [26]; Daragmeh et al. [10]; Darmansyah et al. [59]; Diana and Leon [88]; Gerrans et al. [47]; Handarkho et al. [61]; Haritha [89]; Hassan et al. [90]; Hu et al. [24]; Hwang et al. [91]; Johan [52]; Karim et al. [54]; Karim et al. [35]; Khan and Haque [17]; Khuong et al. [92]; Koroleva [36]; Laksamana et al. [93]; Lantang et al. [62]; Lee [63]; Lee and Pan [37]; Lim et al. [5]; Mainardes et al. [38]; Maryam et al. [83]; Mascarenhas et al. [64]; Ming and Jais [65]; Nan et al. [66]; Nurfadilah and Samidi [67]; Oladapo et al. [68]; Purba et al. [69]; Rahim et al. [84]; Roh et al. [40]; Schomburgk and Hoffmann [50]; Shahzad et al. [70]; Shaikh et al. [85]; Shiau et al. [28]; Singh and Sharma [97]; Stewart and Jürjens [27]; Susilo et al. [72]; Tang et al. [73]; Tun-Pin et al. [74]; Vaicondam et al. [75]; Wang et al. [42]; Wardani et al. [77]; Won-jun [79]; Xie et al. [94]; Yahaya and Ahmad [95]; Yan et al. [43]; Yang et al. [3]; Yeh [55]; Zhang and Kim [80] | Guttman-Kenney et al. [16] | Aalders [15]; Bakri and Yahaya [82]; Datta [60]; DawnBurton [45]; Johnson et al. [48]; Nathan et al. [32]; Tan [18] | Alwi [8]; Ngo and Nguyen [39]; Singh et al. [31]; Wang [76] | Bommer et al. [4]; Gomber et al. [23]; Pattamatta and Dabadghao [49]; Souza and Spers [41]; Spulbar et al. [71]; Weichert [78] | Feng et al. [46]; Kim et al. [30] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alkadi, R.S.; Abed, S.S. Consumer Acceptance of Fintech App Payment Services: A Systematic Literature Review and Future Research Agenda. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 1838-1860. https://doi.org/10.3390/jtaer18040093

Alkadi RS, Abed SS. Consumer Acceptance of Fintech App Payment Services: A Systematic Literature Review and Future Research Agenda. Journal of Theoretical and Applied Electronic Commerce Research. 2023; 18(4):1838-1860. https://doi.org/10.3390/jtaer18040093

Chicago/Turabian StyleAlkadi, Rotana S., and Salma S. Abed. 2023. "Consumer Acceptance of Fintech App Payment Services: A Systematic Literature Review and Future Research Agenda" Journal of Theoretical and Applied Electronic Commerce Research 18, no. 4: 1838-1860. https://doi.org/10.3390/jtaer18040093

APA StyleAlkadi, R. S., & Abed, S. S. (2023). Consumer Acceptance of Fintech App Payment Services: A Systematic Literature Review and Future Research Agenda. Journal of Theoretical and Applied Electronic Commerce Research, 18(4), 1838-1860. https://doi.org/10.3390/jtaer18040093