Has Carbon Disclosure Become More Transparent in the Global Logistics Industry? An Investigation of Corporate Carbon Disclosure Strategies Between 2010 and 2015

Abstract

1. Introduction

- RQ1.

- “To what extent have internal and external pressures led to a change in carbon management practices?”

- RQ2.

- “To what extent have internal and external pressures led to a change in carbon disclosure strategies?”

2. Strategic Internal and External Responses

2.1. Carbon Disclosure Responses and Strategies

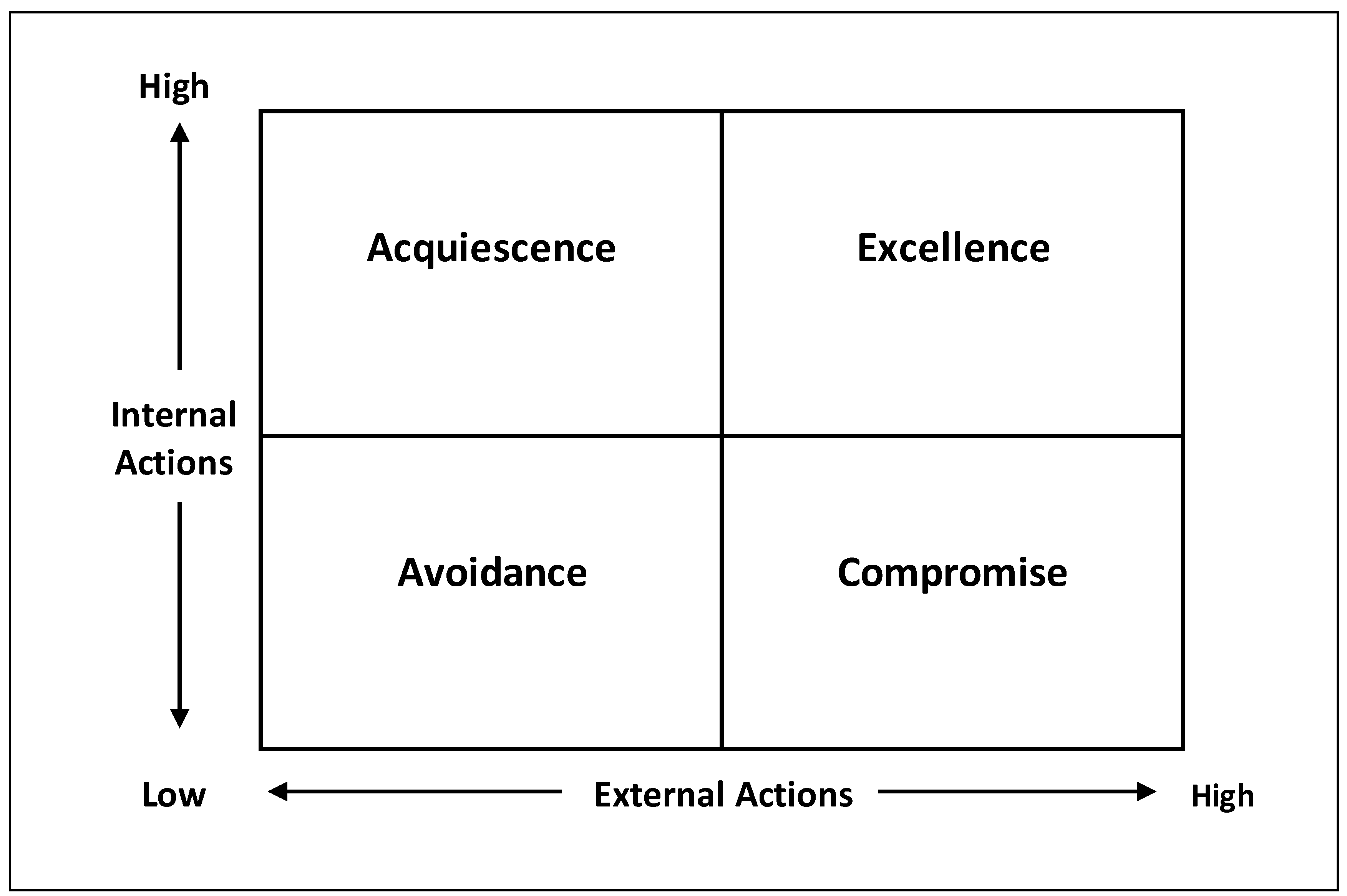

2.2. Acquiescence

2.3. Avoidance

2.4. Compromise

2.5. Excellence

3. Research Design

3.1. Sample

3.2. Carbon Disclosure Variables

3.3. Measuring Carbon Management Practices (CMPs)

3.4. Carbon Disclosure Measurement

4. Results

4.1. Descriptive Statistics of CMPs

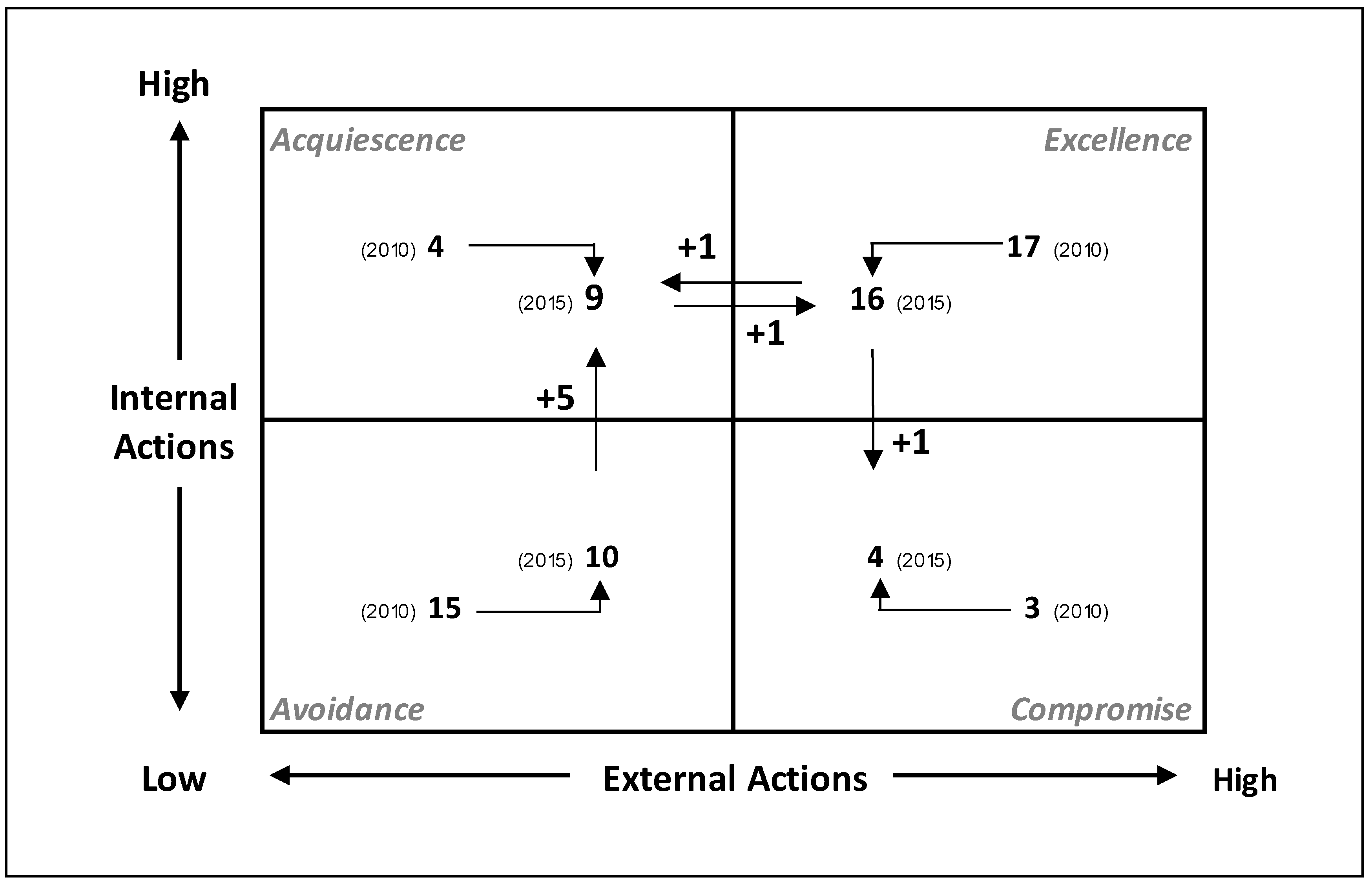

4.2. Categorization of Carbon Disclosure Behavior

5. Discussion of Results

Conclusion and Limitations

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Luo, L. The influence of institutional contexts on the relationship between voluntary carbon disclosure and carbon emission performance. Account. Financ. 2017. [Google Scholar] [CrossRef]

- Welbeck, E.E. The influence of institutional environment on corporate responsibility disclosures in Ghana. Medit. Account. Res. 2017, 25, 216–240. [Google Scholar] [CrossRef]

- De Villiers, C.; Alexander, D. The institutionalisation of corporate social responsibility reporting. Br. Account. Rev. 2014, 46, 198–212. [Google Scholar] [CrossRef]

- Pal, A.; Kant, K. A food transportation framework for an efficient and worker-friendly fresh food physical internet. Logistics. 2017, 1, 10. [Google Scholar] [CrossRef]

- Schaltegger, S.; Csutora, M. Carbon accounting for sustainability and management. Status quo and challenges. J. Clean. Prod. 2012, 36, 1–16. [Google Scholar] [CrossRef]

- Herold, D.M.; Lee, K.-H. Carbon management in the logistics and transportation sector: An overview and new research directions. Carbon Manag. 2017, 8, 79–97. [Google Scholar] [CrossRef]

- Adams, C.A.; McNicholas, P. Making a difference: Sustainability reporting, accountability and organisational change. Account. Audit. Account. J. 2007, 20, 382–402. [Google Scholar] [CrossRef]

- Kolk, A.; Levy, D.; Pinkse, J. Corporate responses in an emerging climate regime: The institutionalization and commensuration of carbon disclosure. Eur. Account. Rev. 2008, 17, 719–745. [Google Scholar] [CrossRef]

- Hrasky, S. Carbon footprints and legitimation strategies: Symbolism or action? Account. Audit. Account. J. 2011, 25, 174–198. [Google Scholar] [CrossRef]

- Lee, K.-H.; Herold, D.M. Cultural relevance in environmental and sustainability management accounting (EMA) in the Asia-Pacific region: A link between cultural values. In Accounting for Sustainability: Asia Pacific Perspectives; Lee, K.-H., Schaltegger, S., Eds.; Springer International Publishing AG: Gewerbestrasse, Cham, Switzerland, 2018; Volume 33, pp. 11–37. [Google Scholar]

- Herold, D.M. The influence of institutional and stakeholder pressures on carbon disclosure strategies: An investigation in the global logistics industry. PhD. Thesis, Griffith University, South East Queensland, Australia, January 2018. [Google Scholar]

- Tozanli, O.; Duman, G.M.; Kongar, E.; Gupta, S.M. Environmentally Concerned Logistics Operations in Fuzzy Environment: A Literature Survey. Logistics. 2017, 1, 4. [Google Scholar] [CrossRef]

- Hawn, O.; Ioannou, I. Mind the gap: The interplay between external and internal actions in the case of corporate social responsibility. Strateg. Manag. J. 2016, 37, 2569–2588. [Google Scholar] [CrossRef]

- Borghei, Z.; Leung, P.; Guthrie, J. The nature of voluntary greenhouse gas disclosure–an explanation of the changing rationale: Australian evidence. Medit. Account. Res. 2016, 24, 111–133. [Google Scholar] [CrossRef]

- Herold, D.M.; Lee, K.-H. Carbon disclosure strategies in the global logistics industry: Similarities and differences in carbon measurement and reporting. In Pathways to A Sustainable Economy; Hossain, M., Hales, R., Sarker, T., Eds.; Springer International Publishing AG: Gewerbestrasse, Cham, Switzerland, 2018; pp. 87–101. ISBN 978-3-319-67702-6. [Google Scholar]

- De Villiers, C.; Naiker, V.; Van Staden, C.J. The effect of board characteristics on firm environmental performance. J. Manag. 2011, 37, 1636–1663. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Griffiths, A. Corporate sustainability and organizational culture. J. World Bus. 2010, 45, 357–366. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Thornton, P.H.; Ocasio, W. Institutional logics. In The Sage Handbook of Organizational Institutionalism; Greenwood, R., Oliver, C., Suddaby, R., Sahlin, A., Eds.; SAGE Publications Ltd.: London, UK, 2008; Volume 840, pp. 100–129. [Google Scholar]

- Besharov, M.L.; Smith, W.K. Multiple institutional logics in organizations: Explaining their varied nature and implications. Acad. Manag. Rev. 2014, 39, 364–381. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic management: A stakeholder approach. Adv. Strateg. Manag. 1983, 1, 31–60. [Google Scholar]

- Oliver, C. Strategic responses to institutional processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized organizations: Formal structure as myth and ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef]

- Hörisch, J.; Freeman, R.E.; Schaltegger, S. Applying stakeholder theory in sustainability management: Links, similarities, dissimilarities, and a conceptual framework. Organ. Environ. 2014, 27, 328–346. [Google Scholar] [CrossRef]

- Lee, K.-H.; Herold, D.M. Cultural relevance in corporate sustainability management: A comparison between Korea and Japan. Asian J. Sustain. Soc. Responsib. 2016, 1, 1–21. [Google Scholar] [CrossRef]

- UPS. Sustainability Report–The Road Ahead; United Parcel Service: Louisville, GA, USA, 2017. [Google Scholar]

- Herold, D.M.; Lee, K.-H. The influence of the sustainability logic on carbon disclosure in the global logistics industry: The case of Dhl, Fdx and Ups. Sustainability. 2017, 9, 601. [Google Scholar] [CrossRef]

- Schuler, D.A.; Cording, M. A corporate social performance–corporate financial performance behavioral model for consumers. Acad. Manag. Rev. 2006, 31, 540–558. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Maximizing business returns to corporate social responsibility (CSR): The role of CSR communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Brundtland, G.H. Our Common Future: Report of the World Commission on Environment and Development; World Commission on Environment and Development; Oxford University Press: New York, NY, USA, 1987. [Google Scholar]

- Bob, S. Transport Report; Carbon Disclosure Project; CDP: London, UK, 2010. [Google Scholar]

- Schaltegger, S.; Hörisch, J. In search of the dominant rationale in sustainability management: Legitimacy-or profit-seeking? J. Bus. Ethics 2017, 145, 259–276. [Google Scholar] [CrossRef]

- Herold, D.M. Peak oil: Impacts on global trade and transportation. Master’s Thesis, Danube University Krems, Krems, Austria, September 2012. [Google Scholar]

- Herold, D.M.; Manwa, F.; Sen, S.; Wilde, S.J. It’s the yeast we can do: Untapping sustainability trends in australian craft breweries. J. Asia Entrep. Sustain. 2016, 12, 82–110. [Google Scholar]

- Schaltegger, S.; Burritt, R. Business cases and corporate engagement with sustainability: Differentiating ethical motivations. J. Bus. Ethics 2017, 145, 259–276. [Google Scholar] [CrossRef]

- Pålsson, H.; Kovács, G. Reducing transportation emissions: A reaction to stakeholder pressure or a strategy to increase competitive advantage. Int. J. Phys. Distribut. Logist. Manag. 2014, 44, 283–304. [Google Scholar] [CrossRef]

- John, E.; Judy, K. Trust Us: The Global Reporters 2002 Survey of Corporate Sustainability Reporting; United Nations Environment Programme (UNEP); SustainAbility: London, UK, 18 November 2002. [Google Scholar]

- Beattie, V. Accounting narratives and the narrative turn in accounting research: Issues, theory, methodology, methods and a research framework. Br. Account. Rev. 2014, 46, 111–134. [Google Scholar] [CrossRef]

- Unerman, J. Methodological issues-reflections on quantification in corporate social reporting content analysis. Account. Audit. Account. J. 2000, 13, 667–681. [Google Scholar] [CrossRef]

- Beattie, V.; McInnes, B.; Fearnley, S. A methodology for analysing and evaluating narratives in annual reports: A comprehensive descriptive profile and metrics for disclosure quality attributes. Account. Forum 2004, 28, 205–236. [Google Scholar] [CrossRef]

- Botosan, C.A. Disclosure level and the cost of equity capital. Account. Rev. 1997, 72, 323–349. [Google Scholar]

- Scott, W.R. Unpacking institutional arguments. In The New Institutionalism in Organizational Analysis; Powell, W.W., DiMaggio, P.J., Eds.; University of Chicago Press: Chicago, IL, USA, 1991; pp. 164–182. [Google Scholar]

- JOC. Top 50 Global 3pl Companies; Pittsburgh, PA, USA, 2015. Available online: https://www.joc.com/special-topics/top-50-3pls (accessed on 27 July 2018).

- Bloomberg 2016 Impact Report. Available online: https://www.bloomberg.com/company/announcements/bloomberg-publishes-2016-impact-report/ (accessed on 27 July 2018).

- Weber, R.P. Basic Content Analysis, Quantitative Applications in the Social Sciences; Sage Publications: Beverly Hills, CA, USA, 1990. [Google Scholar]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation 2010. Bus. Strateg. Environ. 2010, 19, 182–198. [Google Scholar]

- Chen, S.; Bouvain, P. Is corporate responsibility converging? A comparison of corporate responsibility reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| CMPs | Description | |

|---|---|---|

| INTERNAL | ||

| Accountability and Oversight (AO#) | ||

| CSR/Sustainability Committee | Indicates whether the company has a corporate social responsibility (CSR)/sustainability (or equivalent) committee that reports directly to the board. | |

| Responsible Body for Climate Change | Indicates if a board committee or other executive body has overall responsibility for climate change. | |

| Exec Director for Sustainability | Indicates whether there is an executive director on the board with responsibility for corporate social responsibility (CSR)/sustainability. | |

| Non-Exec Director for Sustainability | Indicates whether there is a non-executive director on the board with responsibility for corporate social responsibility (CSR)/sustainability. | |

| Climate Change Management Incentives | Indicates whether the company provides incentives for individual management of climate change issues including attainment of GHG (Greenhouse Gas) targets. | |

| Initiatives and Policies (IP#) | ||

| Climate Change Initiatives/Policy | Indicates whether the company has outlined its intention to help reduce global emissions of the Greenhouse Gases that cause climate change through its ongoing operations and/or the use of its products and services. | |

| Energy Efficiency Initiatives/Policy | Indicates whether the company has implemented any initiatives to make its use of energy more efficient. | |

| Emissions Reductions Initiatives/Policy | Indicates whether the company has implemented any initiatives to reduce its environmental emissions to air. | |

| Environmental Quality Initiatives/Policy | Indicates whether the company has introduced any kind of environmental quality management and/or environmental management system to help reduce the environmental footprint of its operations. | |

| Environmental SC Initiatives/Policy | Indicates whether the company has implemented any initiatives to reduce the environmental footprint of its supply chain. | |

| Risks and Opportunities (RO#) | ||

| Assessment of regulatory CC opportunities | Indicates if the company considers itself exposed to potential climate change regulatory opportunity. | |

| Assessment of physical CC risk | Indicates if the company considers itself exposed to climate change physical risk. | |

| Assessment of physical CC opportunities | Indicates if the company considers itself exposed to potential climate change physical opportunity. | |

| Assessment of other CC risks | Indicates if the company considers itself exposed to any other risk associated with climate change. | |

| CC Risks discussion in Annual report | Indicates whether the Management Discussion and Analysis (MD&A) or its equivalent risk section of company’s annual report discusses business risks related to climate change. | |

| CC Opportunities discussion in Annual report | Indicates whether the Management Discussion and Analysis (MD&A) and its equivalent section of company’s annual report discuss business opportunities related to climate change. | |

| EXTERNAL | ||

| Emission Verification (EV#) | ||

| Verification/Assurance Scope 1 emissions | Percentage of scope 1 reported emissions which have been verified/assured. | |

| Verification/Assurance Scope 2 emissions | Percentage of scope 2 reported emissions which have been verified/assured. | |

| Verification/Assurance Scope 3 emissions | Percentage of scope 3 reported emissions which have been verified/assured. | |

| Policy/data verification via 3rd party | Indicates whether the company’s environmental policies and data were subject to an independent assessment for the reporting period. | |

| External Engagement (EE#) | ||

| Engagement with policy makers | Indicates if the company engages with policymakers on possible responses to climate change including taxation, regulation and carbon trading. | |

| Signatory of the UNGC | Indicates whether the company is a signatory of the United Nations Global Compact (UNGC). | |

| Usage of GRI framework | Indicates whether the company has used the Global Reporting Initiative (GRI) framework for guidance in its public reporting, to varying degrees of compliance. | |

| Engagement with CDP | Indicates whether the company has disclosed their carbon emissions to the Carbon Disclosure Project (CDP). | |

| Industry Cooperation (IC#) | ||

| Extend of disclosure to Bloomberg | Proprietary Bloomberg score based on the extent of a company’s environmental disclosure as part of Environmental, Social and Governance (ESG) data. | |

| Extend of disclosure to CDP | Reflects the comprehensiveness of a company’s response in terms of the depth and breadth of its answers to the Carbon Disclosure Project (CDP) questionnaire | |

| Sections | CMPs | 2010 | 2015 | Variance | |||

|---|---|---|---|---|---|---|---|

| Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | ||

| Accountability and Oversight (AO#) | 0.35 | 0.23 | 0.38 | 0.22 | 0.03 | −0.01 | |

| CSR/Sustainability Committee | 0.03 | 0.16 | 0.08 | 0.28 | 0.05 | 0.11 | |

| Responsible Body for Climate Change | 0.65 | 0.48 | 0.24 | 0.43 | −0.41 | −0.05 | |

| Exec Director for Sustainability | 0.08 | 0.28 | 0.11 | 0.31 | 0.03 | 0.04 | |

| Non-Exec Director for Sustainability | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Climate Change Mgmt Incentives | 0.51 | 0.51 | 0.68 | 0.47 | 0.16 | −0.03 | |

| Initiatives and Policies (IP#) | 0.58 | 0.39 | 0.73 | 0.36 | 0.15 | −0.03 | |

| Climate Change Initiatives/Policy | 0.41 | 0.50 | 0.62 | 0.49 | 0.22 | −0.01 | |

| Energy Efficiency Initiatives/Policy | 0.68 | 0.47 | 0.78 | 0.42 | 0.11 | −0.06 | |

| Emissions Reductions Initiatives/Policy | 0.65 | 0.48 | 0.84 | 0.37 | 0.19 | −0.11 | |

| Envir. Quality Initiatives/Policy | 0.68 | 0.47 | 0.70 | 0.46 | 0.03 | −0.01 | |

| Environmental SC Initiatives/Policy | 0.41 | 0.50 | 0.57 | 0.50 | 0.16 | 0.00 | |

| Risks and Opportunities (RO#) | 0.35 | 0.31 | 0.50 | 0.29 | 0.15 | −0.02 | |

| Assessment of regulatory CC opportunities | 0.49 | 0.51 | 0.68 | 0.47 | 0.19 | −0.03 | |

| Assessment of physical CC risk | 0.49 | 0.51 | 0.76 | 0.43 | 0.27 | −0.07 | |

| Assessment of physical CC opportunities | 0.38 | 0.49 | 0.59 | 0.50 | 0.22 | 0.01 | |

| CC Risks discussion in Annual report | 0.24 | 0.43 | 0.27 | 0.45 | 0.03 | 0.02 | |

| CC Opportunities discussion in Annual report | 0.05 | 0.23 | 0.03 | 0.16 | −0.03 | −0.06 | |

| Internal CMPs | 0.42 | 0.24 | 0.52 | 0.21 | 0.10 | −0.03 | |

| Emission Verification (EV#) | 0.24 | 0.33 | 0.41 | 0.41 | 0.17 | 0.08 | |

| Verification/Assurance Scope 1 emissions | 0.31 | 0.46 | 0.53 | 0.49 | 0.23 | 0.03 | |

| Verification/Assurance Scope 2 emissions | 0.30 | 0.46 | 0.49 | 0.49 | 0.19 | 0.03 | |

| Verification/Assurance Scope 3 emissions | 0.09 | 0.28 | 0.32 | 0.46 | 0.23 | 0.19 | |

| Policy/data verification via 3rd party | 0.24 | 0.43 | 0.35 | 0.48 | 0.11 | 0.05 | |

| External Engagement (EE#) | 0.50 | 0.34 | 0.44 | 0.28 | −0.06 | −0.06 | |

| Engagement with policy makers | 0.51 | 0.51 | 0.59 | 0.50 | 0.08 | −0.01 | |

| Signatory of the UNGC | 0.73 | 0.65 | 0.27 | 0.51 | −0.46 | −0.14 | |

| Usage of GRI framework | 0.03 | 0.16 | 0.68 | 0.28 | 0.65 | 0.11 | |

| Engagement with CDP | 0.19 | 0.40 | 0.22 | 0.42 | 0.03 | 0.02 | |

| Industry Cooperation (IC#) | 0.44 | 0.26 | 0.53 | 0.28 | 0.08 | 0.02 | |

| Extend of disclosure to Bloomberg | 0.26 | 0.21 | 0.28 | 0.21 | 0.02 | 0.00 | |

| Extend of disclosure to CDP | 0.54 | 0.38 | 0.63 | 0.43 | 0.09 | 0.05 | |

| External CMPs | 0.41 | 0.28 | 0.46 | 0.27 | 0.06 | 0.00 | |

| Positive Drivers | Negative Drivers | |||

|---|---|---|---|---|

| ManagementSections | 2010 | 2015 | 2010 | 2015 |

| Mean | Mean | Mean | Mean | |

| Accountability and Oversight (AO#) | 0.29 | 0.43 | 0.50 | 0.50 |

| Initiatives and Policies (IP#) | 0.29 | 0.69 | 0.90 | 1.00 |

| Risks and Opportunities (RO#) | 0.29 | 0.64 | 0.00 | 0.08 |

| Internal CMPs | 0.29 | 0.59 | 0.47 | 0.51 |

| Industry Average | 0.42 | 0.52 | 0.42 | 0.52 |

| Emission Verification (EV#) | 0.06 | 0.23 | 0.52 | 0.49 |

| External Engagement (EE#) | 0.29 | 0.36 | 0.75 | 0.75 |

| Industry Cooperation (IC#) | 0.34 | 0.46 | 0.84 | 0.62 |

| External CMPs | 0.23 | 0.35 | 0.70 | 0.62 |

| Industry Average | 0.41 | 0.46 | 0.41 | 0.46 |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Herold, D.M. Has Carbon Disclosure Become More Transparent in the Global Logistics Industry? An Investigation of Corporate Carbon Disclosure Strategies Between 2010 and 2015. Logistics 2018, 2, 13. https://doi.org/10.3390/logistics2030013

Herold DM. Has Carbon Disclosure Become More Transparent in the Global Logistics Industry? An Investigation of Corporate Carbon Disclosure Strategies Between 2010 and 2015. Logistics. 2018; 2(3):13. https://doi.org/10.3390/logistics2030013

Chicago/Turabian StyleHerold, David M. 2018. "Has Carbon Disclosure Become More Transparent in the Global Logistics Industry? An Investigation of Corporate Carbon Disclosure Strategies Between 2010 and 2015" Logistics 2, no. 3: 13. https://doi.org/10.3390/logistics2030013

APA StyleHerold, D. M. (2018). Has Carbon Disclosure Become More Transparent in the Global Logistics Industry? An Investigation of Corporate Carbon Disclosure Strategies Between 2010 and 2015. Logistics, 2(3), 13. https://doi.org/10.3390/logistics2030013