How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe

Abstract

:1. Introduction

- -

- that the initial COVID-19 impact on banks in the analyzed region studied was heterogeneous, affecting certain countries strongly, while leaving others initially unaffected,

- -

- that the pandemic has intensified the challenges of digitalization and forced banks to speed up the digital transformations in their business models.

2. COVID-19 Shock and Bank Resilience in CENE

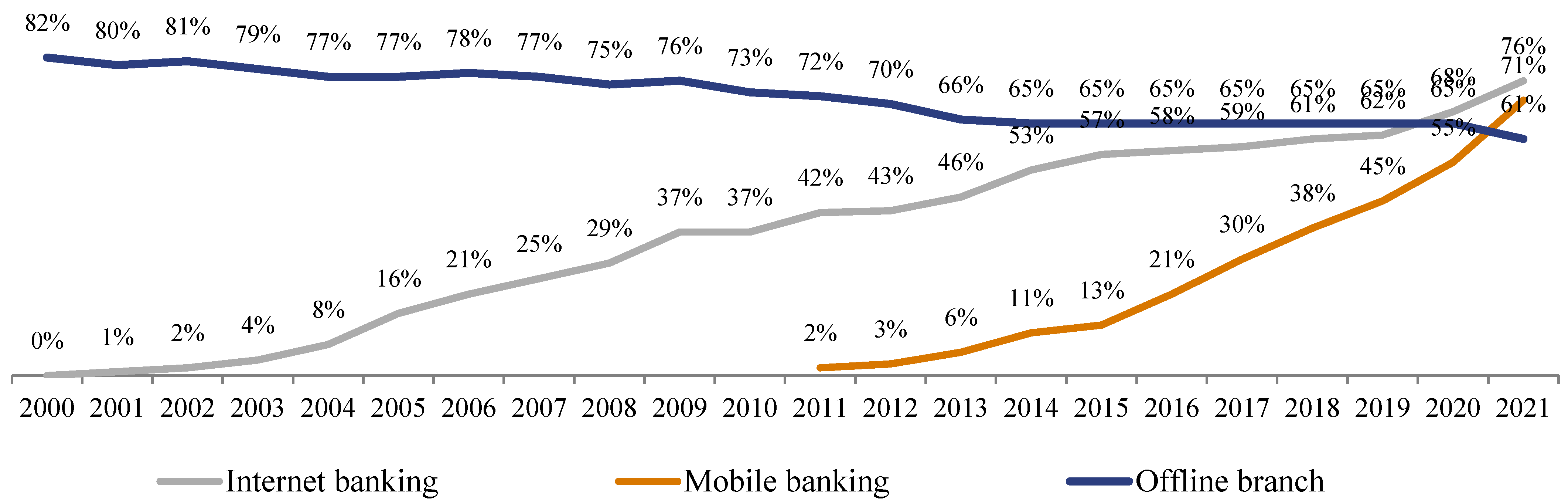

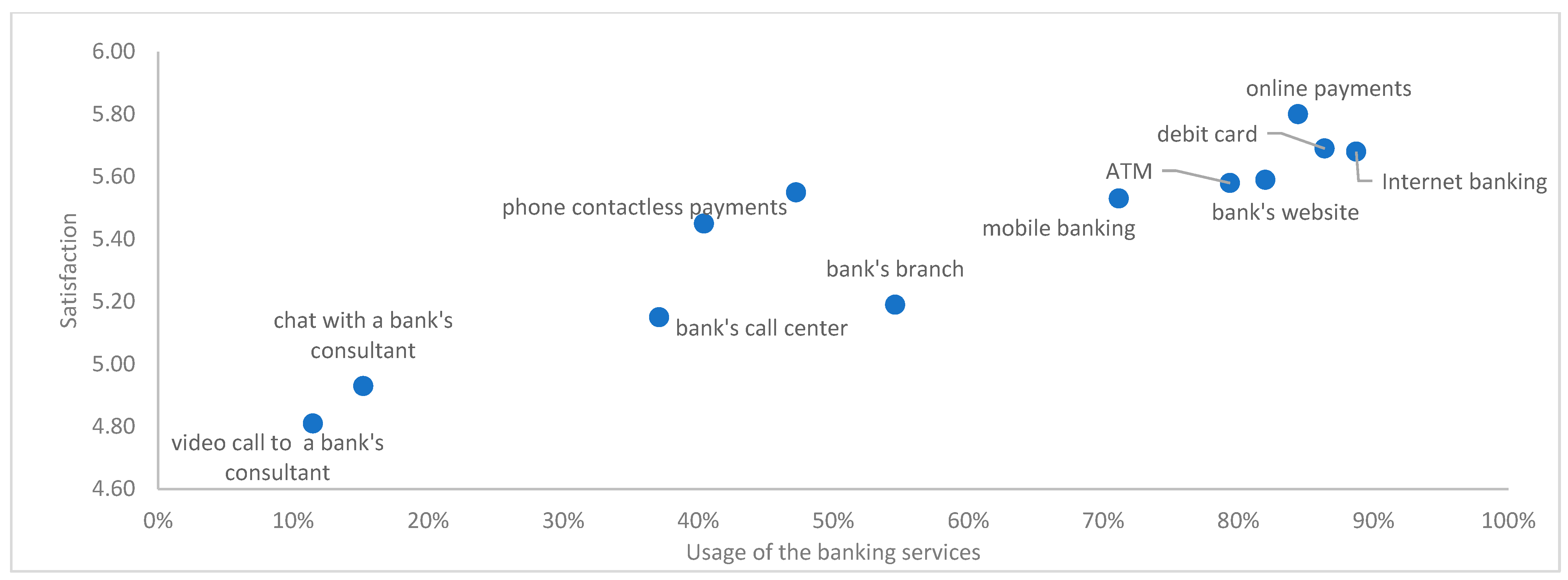

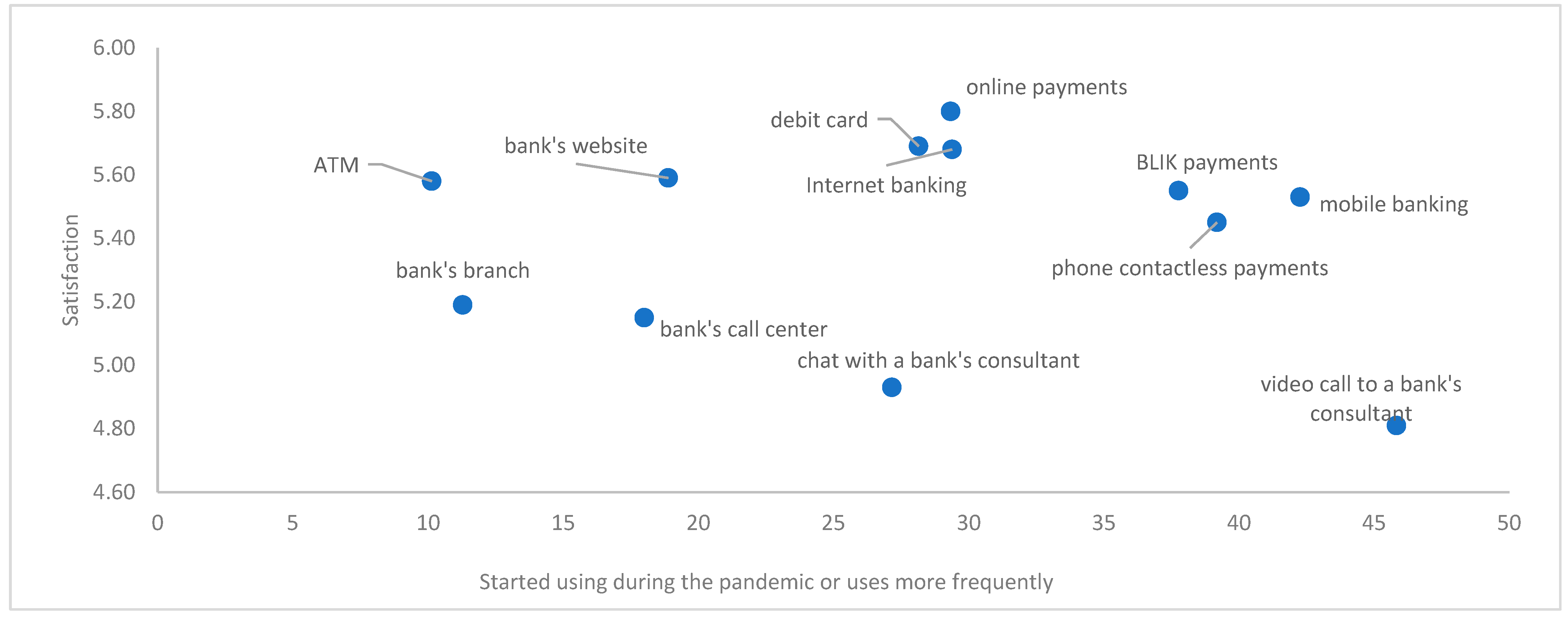

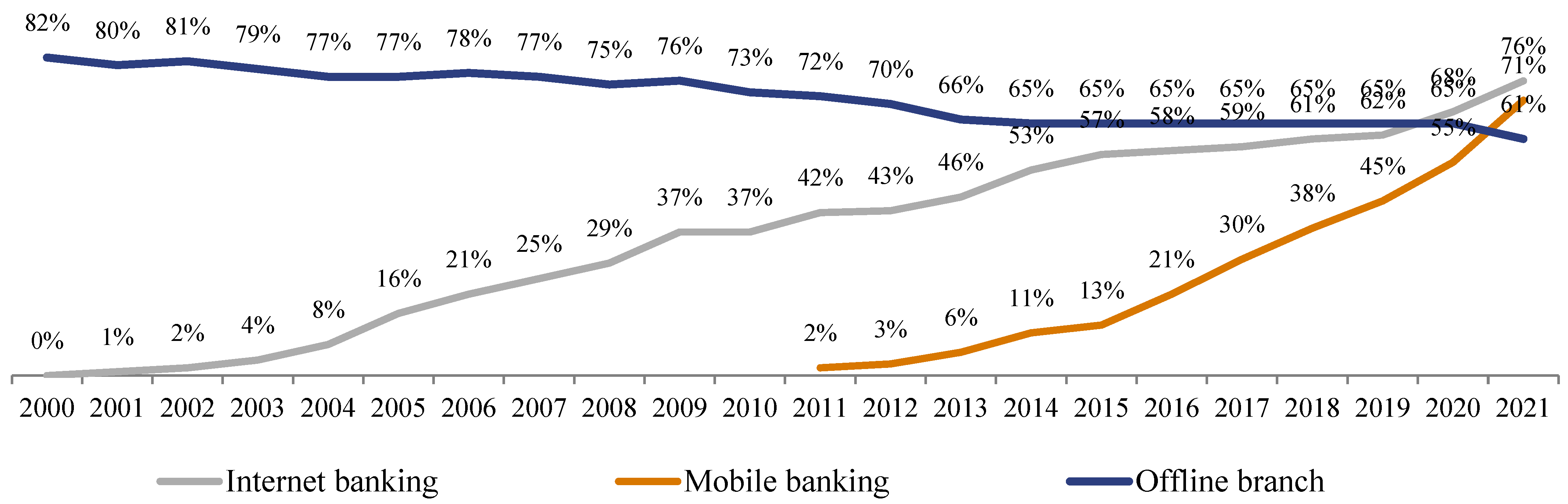

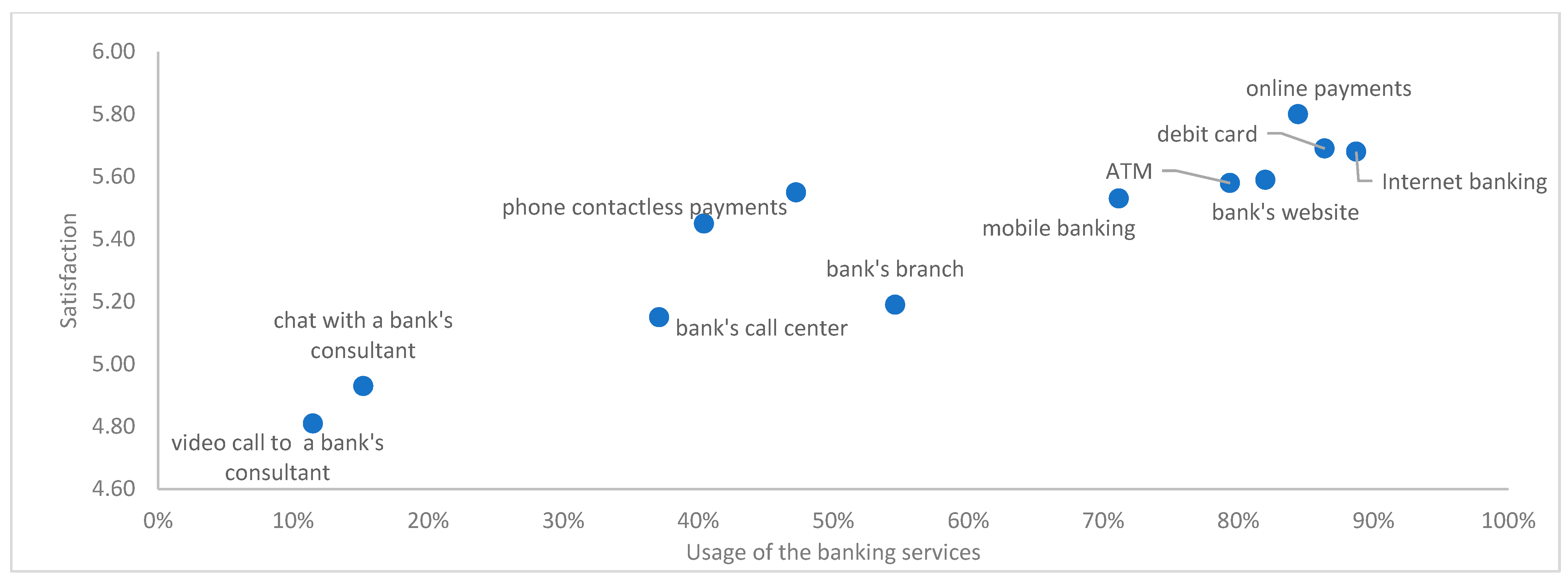

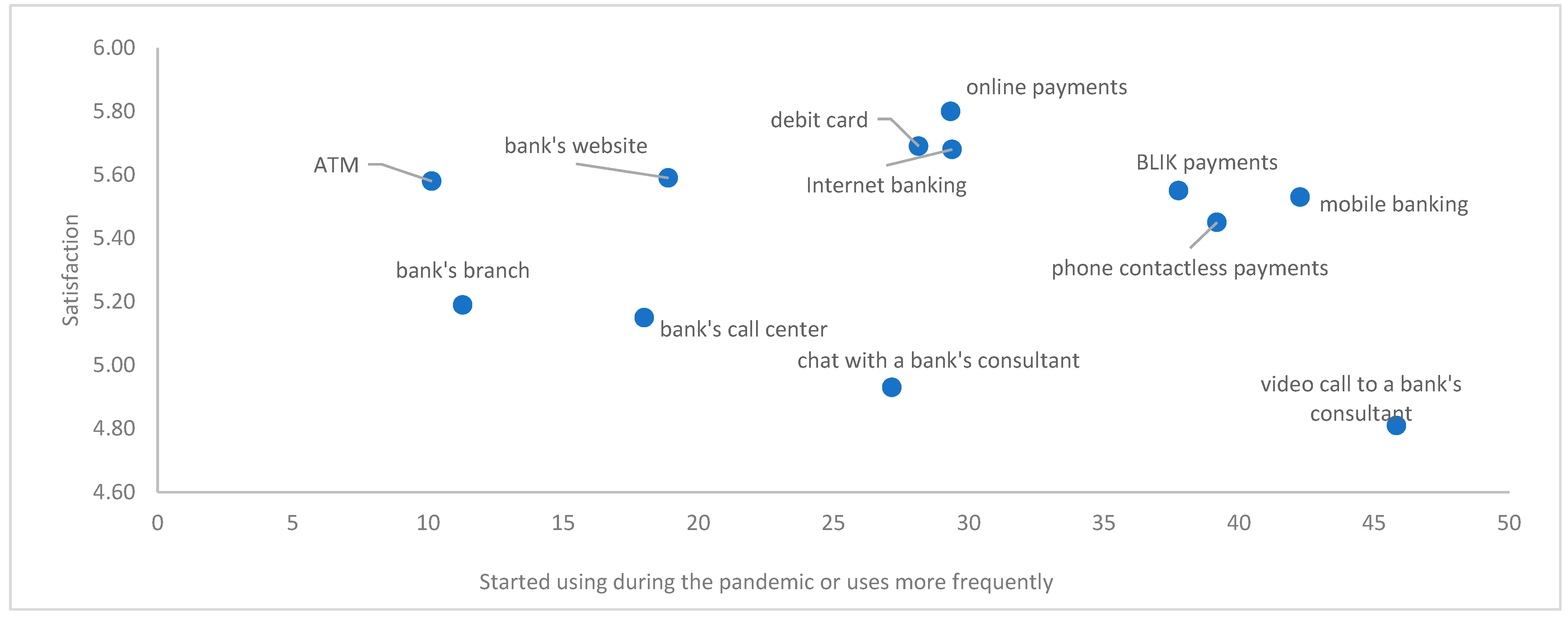

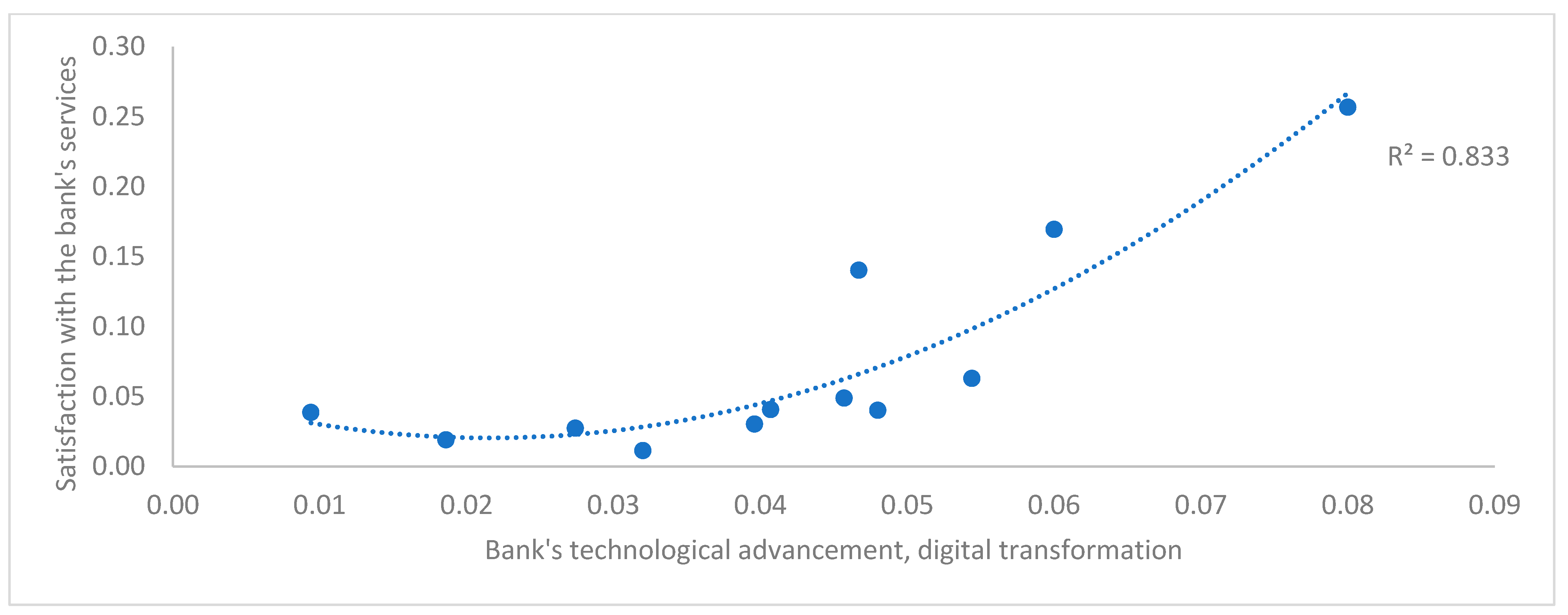

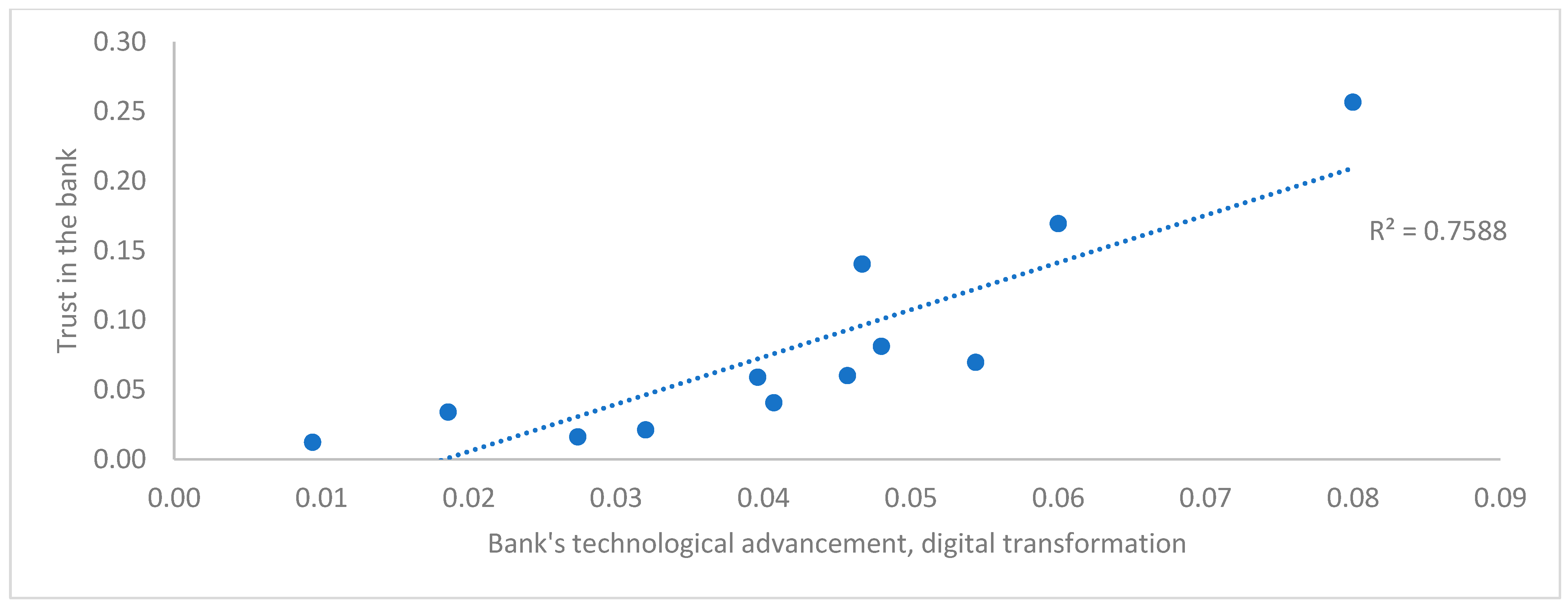

3. The Impact of the Pandemic on Consumer Preferences

4. CENE Banks’ Attitude to Digitalization: The Results of the 2020 Bank Survey

5. Factors Influencing Bank Performance in CENE: Comparison of Aggregate Bank Stability and Performance Measures

5.1. Z-Score Stability Index

5.2. Multi-Level Performance Score Index (MLPS)

5.3. Financial Stability Indicator (FSI)

- -

- ETA stands for equity to total assets, representing capital adequacy;

- -

- ROA stands for return on assets, representing profitability;

- -

- LAF stands for liquid assets to total funding, representing liquidity;

- -

- LD stands for loans to customers to deposits from customers, representing liquidity;

- -

- LITA stands for impairment charges to total assets, representing asset quality.

- comparing the results for the Z-score in the 2004–2014 and the 2016–2019 periods, the overall improvement of CENE bank stability can be observed, which was not affected by the pandemic in 2020. The only exceptions were Hungary, with a result much below the average, and Slovakia, with a very high bank stability score;

- for the aggregate MLPS index, the conclusion can be formed that banks in some countries, such as the Czech Republic, Estonia, and, to some extent, Slovakia, have managed to demonstrate steady high performance values. At the other end of the spectrum, there was a steady worsening performance in Hungary and Latvia. The two remaining cases are Poland, which had a very high performance score in the 2004–2014 period, rapidly deteriorating in the 2016–2019 period, and the worst score of the whole group in 2020; and Lithuania, with a low score in 2004–2015, and the highest score after 2016, including in 2020;

- for the FSI, values were quite harmonized within the group, and for all countries were higher in 2020 than in the preceding years, indicating the stable funding and liquidity position of banks in the analysed countries, and the lack of a substantial credit risk related to the NPL portfolio;

- one of the most affected banking sectors in terms of bank profitability were those of Hungary, Latvia, and Poland. Polish banks were seriously affected by regulatory burdens: high bank tax, macroeconomic trends (low interest rates), and legal risk (large portfolio of foreign denominated mortgage loans) (Raiffeisen Research 2020;)

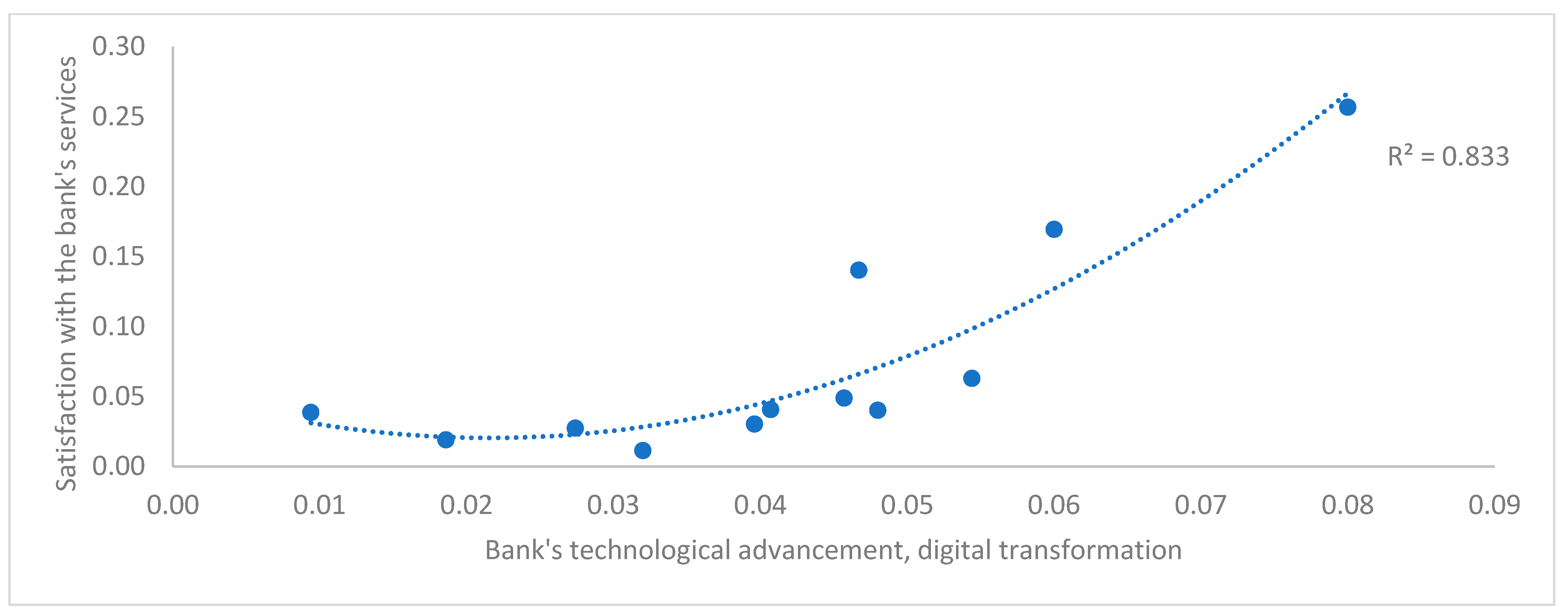

- the countries with the most stable and positive performance were the Czech Republic, Estonia, and Slovakia; and the country which seemed to be least affected by the pandemic was Lithuania—all with an environment very favourable to technology-based transformation. As Deloitte pointed out, banks that invested heavily in technology managed to offset the pandemic effect, at least in the short run (Deloitte 2020a, 2020b);

- in all the analysed countries the crisis mostly affected profitability, while stability indicators and bank capitalisation remained strong.

6. The Impact of the COVID-19 Pandemic on Bank Performance: Panel Data Analysis

- BP—measure of bank financial performance (ROA, ROE; C/I, MLPS, FSI);

- BC—measure of bank capital stability (Z-SC, CAR, TCR);

- MACRO.VAR—the vector of values of macroeconomic variables in period t or t − 1; MICRO.VAR—a vector of control variables characterizing the specific operation of a particular cooperative bank in the period t; vit—the random component, which is the sum of the individual, unchanged in time effect and the pure random error ε.

7. Conclusions: COVID-19 and CENE Bank Business Model Reorientation

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

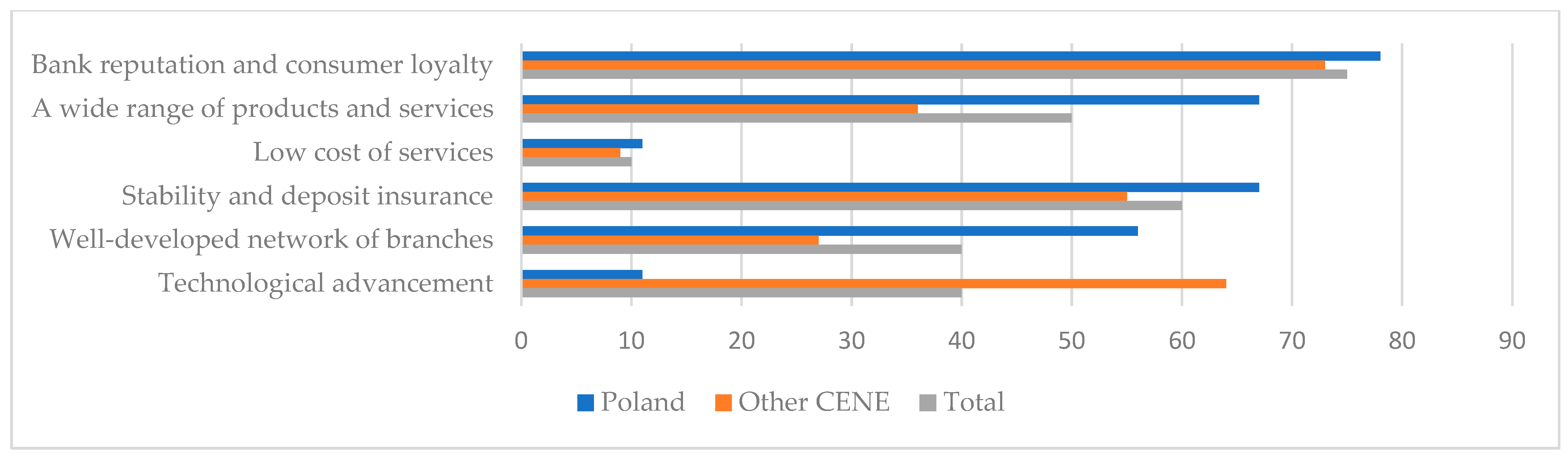

| Survey Questions | Answering Options | Answers CENE (without Poland) | Answers Poland | Total CENE |

|---|---|---|---|---|

| 1. What is the impact of technological changes and competition from the fintech sector on the banking market in your country? | Neutral—they will not threaten the existing market structure and products | 11 | 0 | 5 |

| Positive, evolutionary—improving customer satisfaction | 67 | 73 | 70 | |

| Positive, revolutionary—changes market functioning and the products’ offer | 22 | 27 | 25 | |

| Negative—changing market structure and displacing some products | 0 | 0 | 0 | |

| 2. Which banking market segment is most affected as a result of new technologies? | Robotization | 11 | 18 | 15 |

| Payment services | 45 | 55 | 50 | |

| Big data/cloud computing | 22 | 9 | 15 | |

| Credit services | 22 | 18 | 20 | |

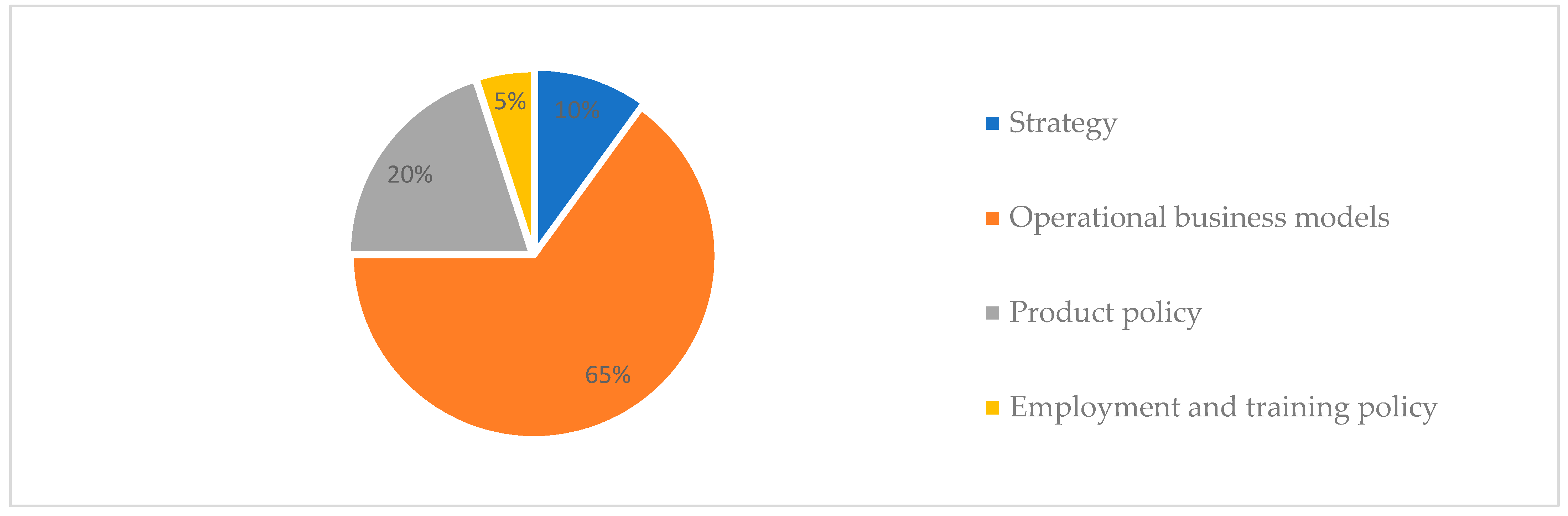

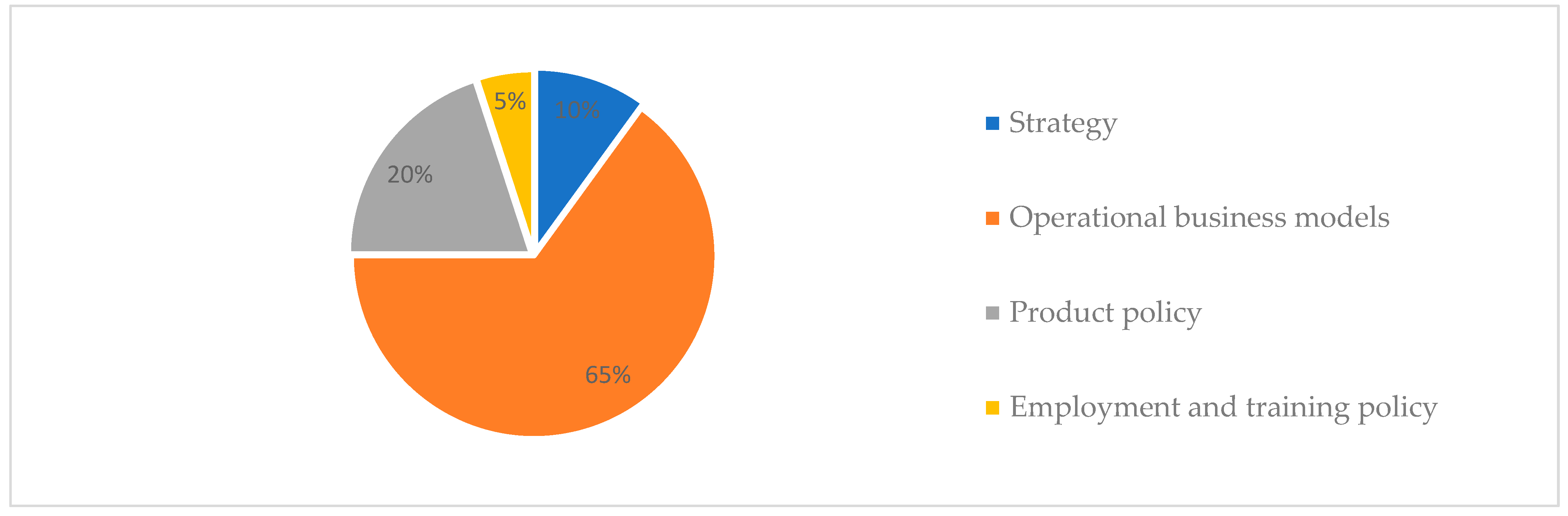

| 3. Which area of banks’ operations will be most impacted as a result of new technologies? | Strategy | 11 | 9 | 10 |

| Operational business models | 67 | 64 | 65 | |

| Product policy | 22 | 18 | 20 | |

| Employment and training policy | 0 | 9 | 5 | |

| 4. What are the main challenges for banks in implementing innovation? (up to 3 answers) | Cybersecurity | 56 | 100 | 80 |

| Cost barriers | 0 | 27 | 15 | |

| Managing complexity and integration of technological processes | 78 | 18 | 45 | |

| Regulatory barriers | 56 | 18 | 35 | |

| Customer education | 22 | 55 | 40 | |

| Employee competences | 33 | 36 | 35 | |

| 5. What are the outlays in your bank for digital transformation (in % of total investments)? | Significant—this is the main investment priority | 67 | 73 | 70 |

| On par with other investment priorities | 33 | 18 | 25 | |

| Low, mainly for reconstruction projects | 0 | 9 | 5 | |

| 6. How does your bank define its competitive position in the field of digitization? | We are market leaders, advanced in implementing new technologies | 56 | 82 | 70 |

| We are moderately advanced, similarly like our main competitors | 33 | 18 | 25 | |

| We are at an early stage of technological changes | 11 | 0 | 5 | |

| It is hard to say—we do not have a specific digitization strategy | 0 | 0 | 0 | |

| 7. Does your bank have a clearly articulated digitization strategy? | Yes, developed and implemented | 100 | 91 | 95 |

| Yes, but at the conceptual stage | 0 | 0 | 0 | |

| Yes, but the implementation was interrupted by the pandemic | 0 | 9 | 5 | |

| We do not see the need to prepare such a strategy | 0 | 0 | 0 | |

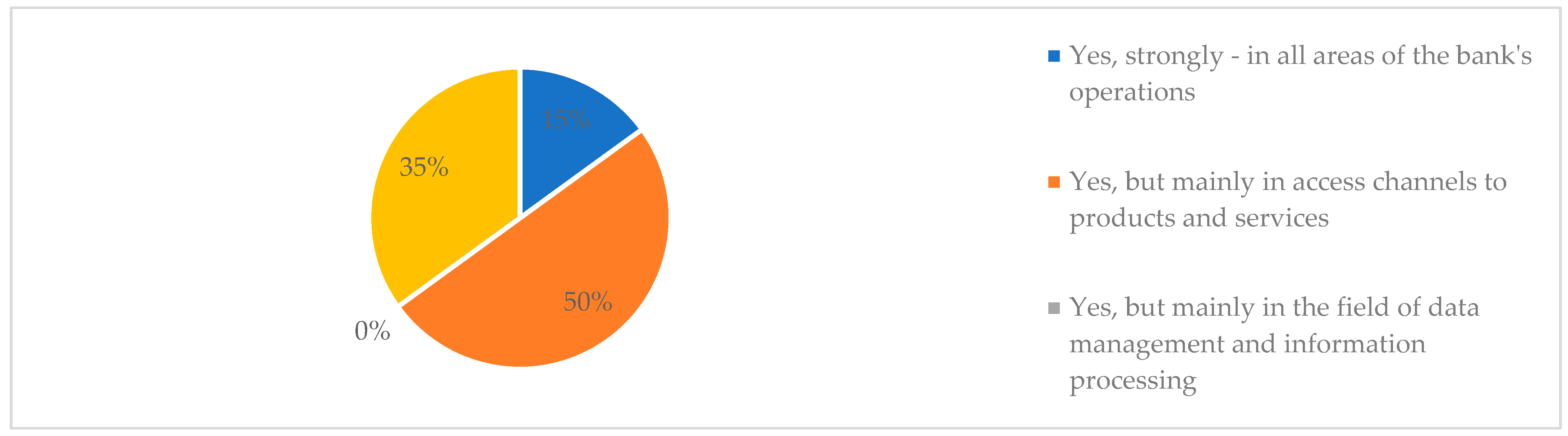

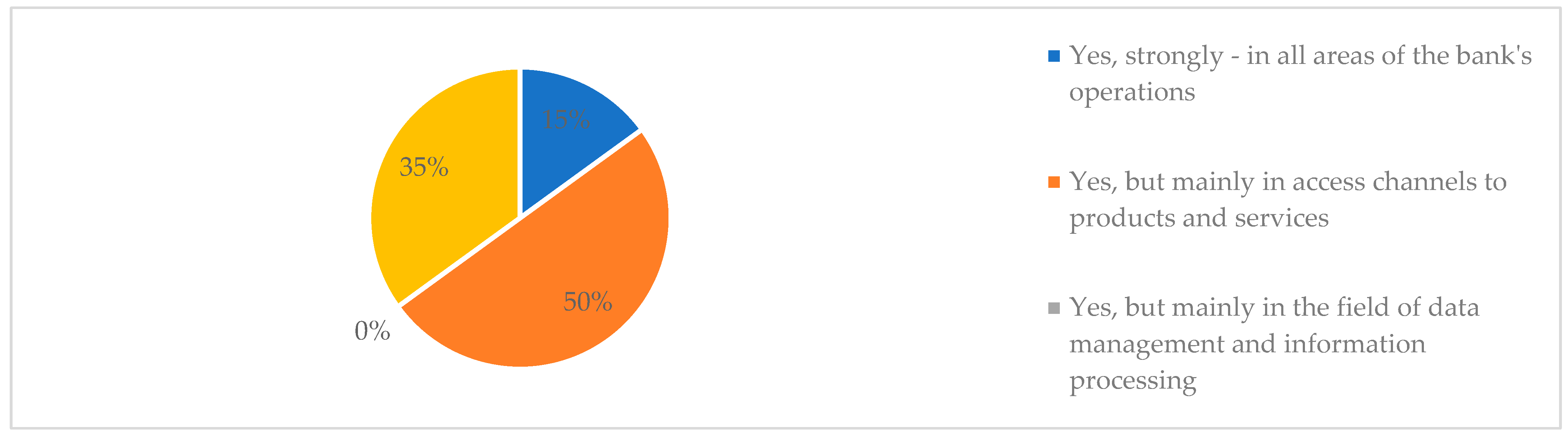

| 8. Has the COVID-19 pandemic revealed the need to change technological solutions in your bank? | Yes, strongly—in all areas of the bank’s operations | 11 | 18 | 15 |

| Yes, but mainly in access channels to products and services | 56 | 46 | 50 | |

| Yes, but mainly in the field of data management and information processing | 0 | 0 | 0 | |

| No | 33 | 36 | 35 | |

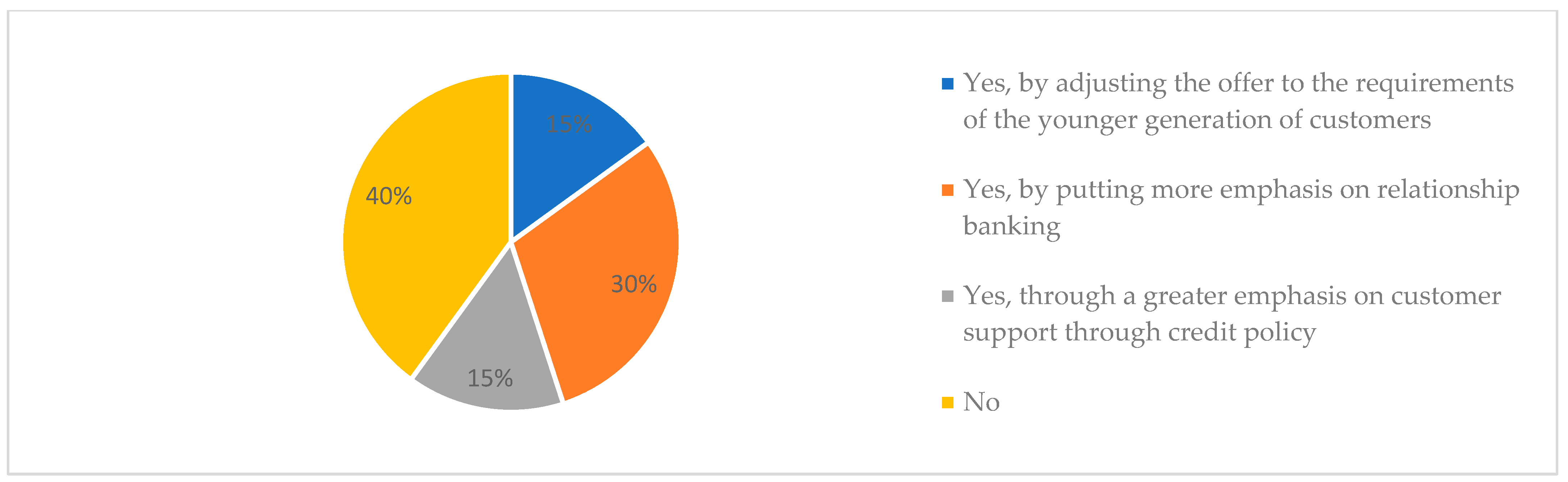

| 9. Has the COVID-19 pandemic revealed the need to change customer relations in your bank? | Yes, by adjusting the offer to the requirements of the younger generation of customers | 11 | 18 | 15 |

| Yes, by putting more emphasis on relationship banking | 22 | 36 | 30 | |

| Yes, through a greater emphasis on customer support through credit policy | 22 | 9 | 15 | |

| No | 44 | 36 | 40 | |

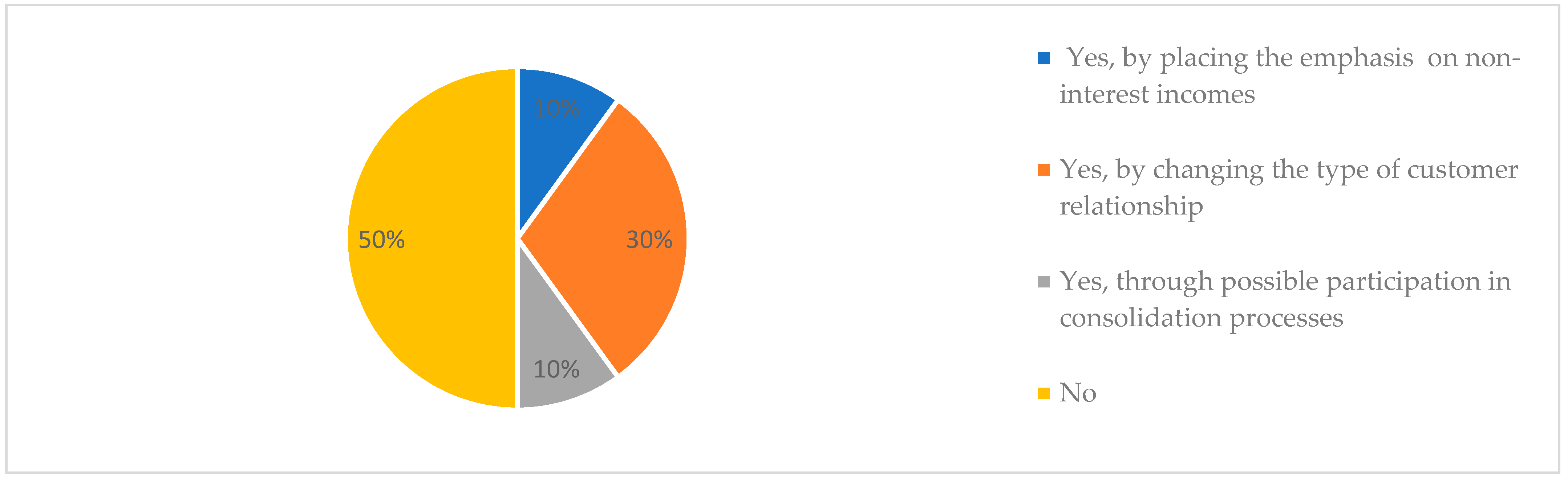

| 10.Has COVID-19 revealed the need for a fundamental change in your bank’s strategy? | Yes, by placing the emphasis on non-interest incomes | 0 | 18 | 10 |

| Yes, by changing the type of customer relationship | 11 | 46 | 30 | |

| Yes, through possible participation in consolidation processes | 22 | 0 | 10 | |

| No | 67 | 36 | 50 | |

| No. of banks | 9 | 11 | 20 |

| Var. | DEP_GR | GS_TA | NII_OR | NPL | LO_GR | LO_DEP | LO_TA | LN_TA | LTIR | HHI | C_GDP | GDP_GR | TCR | E_TA | FSI | MLPS | Z-SC | C/I | ROE | ROA |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 0.04 | −0.02 | 0.02 | −0.39 | 0.05 | −0.02 | 0.15 | 0.12 | −0.03 | 0.18 | 0.06 | 0.17 | 0.06 | 0.07 | −0.30 | 0.62 | −0.01 | −0.39 | 0.63 | 1.00 |

| ROE | 0.02 | −0.06 | −0.01 | −0.39 | 0.03 | −0.04 | −0.07 | 0.13 | −0.02 | 0.08 | 0.03 | 0.10 | 0.03 | −0.13 | −0.10 | 0.45 | −0.14 | −0.29 | 1.00 | |

| C/I | −0.01 | 0.02 | −0.11 | 0.41 | −0.05 | 0.14 | −0.04 | −0.26 | −0.03 | 0.02 | −0.17 | −0.03 | −0.14 | −0.11 | 0.20 | −0.41 | −0.07 | 1.00 | ||

| Z-SC | 0.08 | 0.27 | 0.08 | 0.09 | 0.08 | 0.02 | 0.10 | −0.06 | 0.01 | −0.05 | 0.18 | 0.05 | 0.11 | 0.38 | 0.01 | −0.03 | 1.00 | |||

| MLPS | 0.00 | −0.23 | 0.26 | −0.53 | 0.06 | −0.07 | 0.45 | 0.37 | −0.11 | 0.16 | 0.17 | −0.01 | 0.15 | −0.01 | −0.23 | 1.00 | ||||

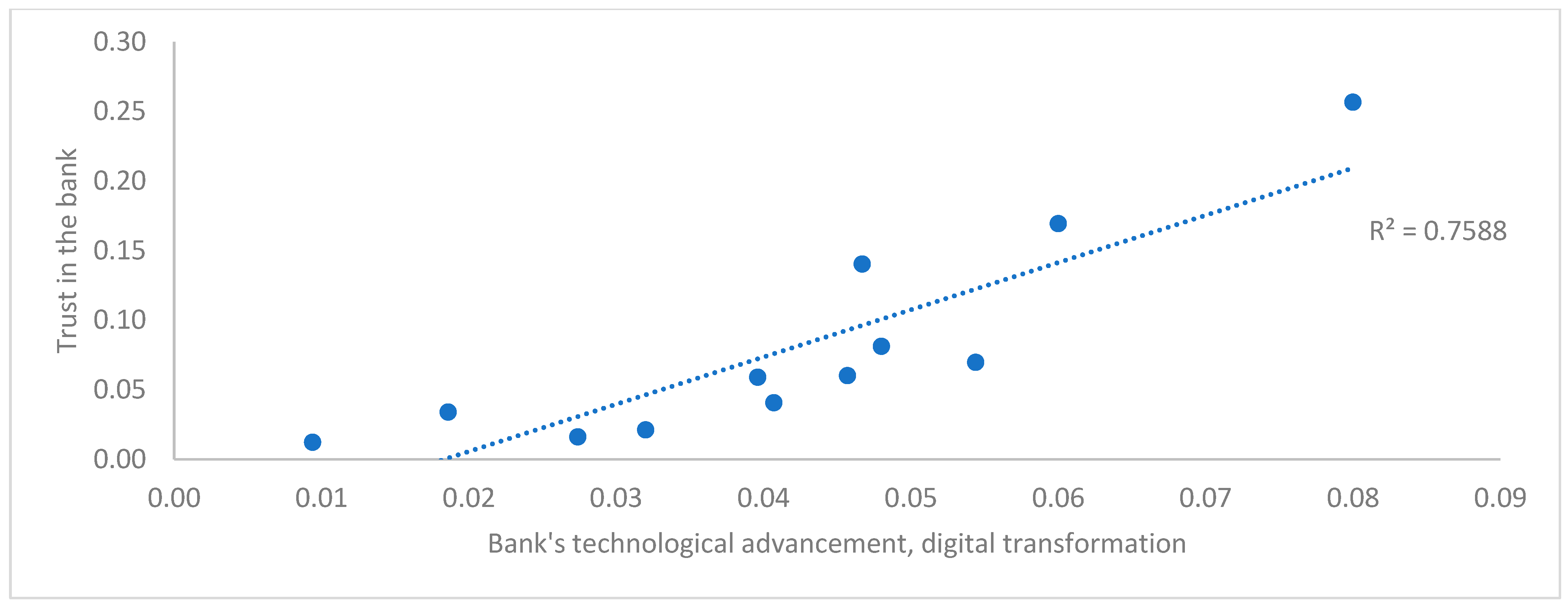

| FSI | 0.04 | −0.18 | 0.10 | 0.20 | −0.06 | −0.43 | −0.07 | −0.09 | 0.00 | 0.06 | −0.02 | −0.05 | 0.07 | 0.03 | 1.00 | |||||

| E_TA | 0.00 | 0.04 | −0.06 | 0.06 | 0.03 | −0.10 | 0.01 | −0.14 | −0.08 | 0.09 | 0.13 | 0.04 | 0.44 | 1.00 | ||||||

| TCR | −0.03 | −0.04 | 0.10 | 0.17 | −0.07 | −0.12 | −0.15 | −0.12 | −0.02 | 0.01 | −0.10 | −0.03 | 1.00 | |||||||

| GDP_GR | 0.04 | −0.05 | 0.00 | 0.08 | 0.05 | 0.14 | 0.05 | −0.06 | 0.35 | −0.14 | −0.08 | 1.00 | ||||||||

| C_GDP | 0.07 | −0.05 | 0.39 | −0.19 | 0.11 | 0.12 | 0.34 | 0.11 | −0.26 | 0.20 | 1.00 | |||||||||

| HHI | 0.09 | −0.28 | −0.11 | −0.07 | 0.09 | −0.13 | −0.04 | −0.31 | −0.61 | 1.00 | ||||||||||

| LTIR | 0.04 | 0.24 | 0.15 | −0.03 | 0.05 | 0.20 | 0.06 | 0.26 | 1.00 | |||||||||||

| LN_TA | 0.02 | 0.20 | 0.23 | −0.35 | 0.00 | 0.05 | 0.14 | 1.00 | ||||||||||||

| LO_TA | 0.07 | −0.23 | 0.44 | −0.31 | 0.15 | 0.20 | 1.00 | |||||||||||||

| LO_DEP | 0.02 | 0.11 | 0.11 | −0.08 | 0.05 | 1.00 | ||||||||||||||

| LO_GR | 0.36 | −0.05 | 0.14 | −0.25 | 1.00 | |||||||||||||||

| NPL | −0.06 | −0.01 | −0.29 | 1.00 | ||||||||||||||||

| NII_OR | 0.10 | −0.18 | 1.00 | |||||||||||||||||

| GS_TA | −0.03 | 1.00 | ||||||||||||||||||

| DEP_GR | 1.00 |

| Variable | Av. | Med. | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| ROA | 0.80 | 0.74 | 1.19 | −8.17 | 7.11 |

| ROE | 8.52 | 7.72 | 14.9 | −70.1 | 134.2 |

| C/I | 63.0 | 57.7 | 42.2 | 6.00 | 799.6 |

| Z-SC | 49.3 | 36.0 | 48.0 | −6.76 | 333.1 |

| MLPS | 0.50 | 1.00 | 9.51 | −25.0 | 21.0 |

| FSI | 0.05 | 0.05 | 0.06 | −0.19 | 0.256 |

| E_TA | 11.3 | 10.0 | 9.13 | −59.2 | 82.2 |

| TCR | 21.7 | 18.5 | 13.2 | 4.69 | 129.3 |

| GDP_GR | 2.12 | 3.14 | 3.35 | −5.60 | 5.50 |

| C_GDP | 49.0 | 50.9 | 9.92 | 32.4 | 68.9 |

| HHI | 0.12 | 0.11 | 0.05 | 0.06 | 0.27 |

| LTIR | 1.50 | 1.29 | 1.10 | −0.53 | 3.54 |

| LN_TA | 7.94 | 8.04 | 1.55 | 4.44 | 11.2 |

| LO_TA | 57.6 | 59.8 | 22.3 | 2.28 | 99.7 |

| LO_DEP | 84.1 | 77.2 | 66.6 | 0.000 | 646.4 |

| LO_GR | 11.5 | 5.53 | 59.3 | −100.0 | 0.00 |

| NPL | 8.43 | 4.50 | 11.2 | 0.00 | 79.8 |

| NII_OR | 64.9 | 67.2 | 22.6 | −4.76 | 161.0 |

| GS_TA | 13.5 | 11.6 | 11.4 | 0.00 | 68.6 |

| DEP_GR | 13.6 | 6.15 | 62.9 | −93.5 | 961.2 |

References

- Allen, Franklin, Ana Babus, and Elena Carletti. 2009. Financial Crises: Theory and Evidence. European University Institute. Available online: http://apps.eui.eu/Personal/Carletti/ARFE-Crises-08June09-final.pdf (accessed on 5 June 2021).

- Allen, Franklin, and Elena Carletti. 2013. What is systemic risk? Journal of Money, Credit and Banking 45: 121–27. [Google Scholar] [CrossRef]

- Andreß, Hans-Jürgen, Katrin Golsch, and Alexander W. Schmidt. 2013. Applied Panel Data Analysis for Economic and Social Surveys. Berlin: Springer. [Google Scholar]

- Baltagi, Badi H. 2005. Econometric Analysis of Panel Data. Chichester: John Wiley and Sons. [Google Scholar]

- Beck, Thorsten, Ross Levine, and Norman Loayza. 2000. Finance and sources of growth. Journal of Financial Economics 58: 261–300. [Google Scholar] [CrossRef] [Green Version]

- Berger, Allen N., and David Humphrey. 1997. Efficiency of Financial Institutions: International Survey and Direction for Future Research. Journal of Operational Research 98: 175–212. [Google Scholar] [CrossRef] [Green Version]

- Bhagat, Sanjai, Brian Bolton, and Jun Lu. 2015. Size, leverage, and risk-taking of financial institutions. Journal of Banking & Finance 59: 520–37. [Google Scholar]

- BIS. 2018. Structural Changes in Banking after the Crisis, CGFS Papers No 60. Available online: https://www.bis.org/publ/cgfs60.pdf (accessed on 5 June 2021).

- BIS. 2019. BigTech in Finance: Opportunities and Risks. Annual Economic Report. Available online: https://www.bis.org/publ/arpdf/ar2019e3.htm (accessed on 5 June 2021).

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel model data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Bond, Stephen R. 2002. Dynamic Panel Data Models: A Guide to Micro Data Methods and Practice. Cemmap Working Paper 09/02. London: Institute for Fiscal Studies. [Google Scholar]

- Boot, Arnoud, Peter Hoffmann, Luc Laeven, and Lev Ratnovski. 2020. Financial intermediation and technology: What’s old, what’s new? ECB Discussion Paper 2438: 1–33. [Google Scholar] [CrossRef]

- Carletti, Elena, Stijn Claessens, Antonio Fatás, and Xavier Vives. 2020. The Bank Business Model in the Post-Covid-19 World. London: CEPR. [Google Scholar]

- Coles, Jeffrey L., and Zhichuan Frank Li. 2020. Managerial Attributes, Incentives, and Performance. The Review of Corporate Finance Studies 2: 256–301. [Google Scholar]

- Dang, Chongyu, Zhichuan Li, and Chen Yang. 2018. Measuring firm size in empirical corporate finance. Journal of Banking & Finance 86: 159–76. [Google Scholar]

- Dang, Van Dan. 2019. The effects of loan growth on bank performance: Evidence from Vietnam. Management Science Letters 9: 899–910. [Google Scholar] [CrossRef]

- Dańska-Borsiak, Barbara. 2009. Zastosowania panelowych modeli dynamicznych w badaniach mikroekonomicznych i makroekonomicznych. Przegląd Statystyczny 56: 25–41. [Google Scholar]

- De Haas, Ralph, Daniel Ferreira, and Anita Taci. 2010. What determines the composition of banks’ loan portfolios? Evidence from transition countries. Journal of Banking & Finance 34: 388–98. [Google Scholar]

- Deloitte. 2020a. CEE Banks Facing Challenging Times. Economic Turbulence to Boost Consolidation. Available online: https://www2.deloitte.com/content/dam/Deloitte/ce/Documents/finance/MA_Banking_study_2020_digital.pdf (accessed on 25 June 2021).

- Deloitte. 2020b. Digital Banking Maturity 2020. Available online: https://www2.deloitte.com/content/dam/Deloitte/ce/Documents/financial-services/ce-digital-banking-maturity-2020.pdf (accessed on 21 June 2021).

- Demirgüç-Kunt, Asli, and Harry Huizinga. 2010. Bank activity and funding strategies: The impact on risk and return. Journal of Financial Economics 98: 625–50. [Google Scholar] [CrossRef] [Green Version]

- Demirguc-Kunt, Asli, Enrica Detragiache, and Ouarda Merrouche. 2010. Bank Capital: Lessons from the Financial Crisis. IMF Working Paper 286: 1–35. [Google Scholar]

- Dinesen, Christian. 2020. Absent Management in Banking: How Banks Fail and Cause Financial Crisis. Cham: Palgrave Macmillan. [Google Scholar]

- European Parliament. 2021. Impacts of the COVID-19 Pandemic on EU Industries. Available online: https://www.europarl.europa.eu/thinktank/en/document.html?reference=IPOL_STU2021.662903 (accessed on 18 June 2021).

- EY. 2018. Global Banking Outlook. Available online: www.ey.com/en_gl/digital/banking-innovation (accessed on 10 June 2021).

- Fiordelisi, Franco. 2007. Shareholder value efficiency in European banking. Journal of Banking & Finance 31: 2151–71. [Google Scholar]

- Haq, Mamiza, and Richard Heaney. 2012. Factors determining European bank risk. Journal of International Financial Markets, Institutions & Money 22: 696–718. [Google Scholar]

- Horobet, Alexandra, Magdalena Radulescu, Lucian Belascu, and Sandra M. Dita. 2021. Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates. Journal of Risk and Financial Management 14: 307. [Google Scholar] [CrossRef]

- Iwanicz-Drozdowska, Małgorzata, Paweł Smaga, and Bartosz Witkowski. 2017. Role of Foreign Capital in Stability of Banking Sectors in CESEE Countries. Czech Journal of Economics and Finance 67: 492–511. [Google Scholar]

- Kantar. 2021. Zoom Finance 2021. Warsaw: Kantar. [Google Scholar]

- Keen, Steve. 2017. Can We Avid Another Financial Crisis? Cambridge: Polity Press. [Google Scholar]

- Kocisova, Kristina. 2015. Banking Stability Index: A Cross-Country Study. Paper presented at 15th International Conference of Finance and Banking Proceedings, Prague, Czech Republic, October 13–14; Available online: http://icfb2015.cms.opf.slu.cz/sites/icfb.rs.opf.slu.cz/files/kocisova.pdf (accessed on 25 June 2021).

- Lepetit, Laetitia, and Frank Strobel. 2015. Bank insolvency risk and Z-score measures: A refinement. Finance Research Letter 13: 214–24. [Google Scholar] [CrossRef] [Green Version]

- Miklaszewska, Ewa, and Krzysztof Kil. 2016. The Impact of 2007–9 Crisis on the Assessment of Bank Performance: The Evidence from CEE-11 Countries. Transformations in Business & Economics 2A: 459–79. [Google Scholar]

- NBP. 2020. Financial System in Poland 2019. Warsaw: NBP. [Google Scholar]

- Neves, Maria E. D., Maria D. C. Gouveia, and Catarina A. N. Proença. 2020. European Bank’s Performance and Efficiency. Journal of Risk and Financial Management 13: 67. [Google Scholar] [CrossRef] [Green Version]

- Oliver Wyman. 2019. Time to Start Again: The State of the Financial Services Industry. Available online: https://www.oliverwyman.com/content/dam/oliver-wyman/v2/publications/2019/January/The-State-Of-Financial-Services-2019-Time-to-start-again.pdf (accessed on 5 June 2021).

- Oliver Wyman. 2021. Ready to Lead: How Banks Can Drive the European Recovery. Available online: https://www.oliverwyman.com/content/dam/oliver-wyman/v2/publications/2021/jul/European-Banking-Outlook-2021.pdf (accessed on 5 June 2021).

- Raiffeisen Research. 2020. CEE Banking Sector Report. Available online: http://www.rbinternational.com/eBusiness/services/resources/media/829189266947841370829189181316930732_829602947997338151_829603177241218127-164075872827402397-1-2-EN.pdf (accessed on 25 June 2021).

- Samson, Kirk, and Gabriella Kusz. 2019. The Silver Lining of the Baltic Banking Crisis, Global Trade Magazine. Available online: https://www.globaltrademag.com/the-silver-lining-of-the-baltic-banking-crisis (accessed on 25 June 2021).

- ZBP. 2021. Reputation of the Polish Banking Sector 2021. Warsaw: ZBP. [Google Scholar]

| Bank/Country | Europe Assets in Billions EUR | Bank/Country | CEE Assets in Billions EUR |

|---|---|---|---|

| BNP Paribas/France | 2521 | PKO BP/Poland | 81.737 |

| HSBC/the UK | 2440 | ČSOB/Czech Republic | 66.927 |

| Credit Agricole/France | 2241 | OTP Bank/Hungary | 63.953 |

| Banco Santander/Spain | 1508 | Česká Spořitelna/Czech Rep. | 58.596 |

| Barclays/the UK | 1506 | Bank Pekao/Poland | 50.568 |

| Country | ROA | ROE | C/I | TCR | CAR | RWA_GR | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2016–2019 | 2020 | 2016–2019 | 2020 | 2016–2019 | 2020 | 2016–2019 | 2020 | 2016–2019 | 2020 | 2016–2019 | 2020 | |

| CZ | 0.98 | 0.52 | 15.06 | 9.04 | 54.73 | 55.60 | 21.96 | 26.05 | 11.85 | 9.00 | 3.24 | 1.84 |

| EE | 2.08 | 0.79 | 14.25 | 6.95 | 58.37 | 72.36 | 22.01 | 23.12 | 12.22 | 12.53 | 51.06 | 10.93 |

| HU | 1.16 | 0.35 | 11.99 | 2.70 | 78.52 | 68.73 | 20.00 | 20.29 | 11.93 | 9.41 | 6.61 | 6.47 |

| LT | 1.46 | 1.07 | 14.40 | 11.04 | 48.47 | 48.54 | 20.40 | 21.84 | 12.24 | 9.24 | 8.27 | 10.04 |

| LV | 0.90 | −0.12 | 5.65 | −0.67 | 74.46 | 95.68 | 20.86 | 22.93 | 12.82 | 13.20 | 1.92 | 1.50 |

| PL | 0.55 | −0.08 | 3.58 | −1.74 | 58.47 | 69.56 | 20.51 | 19.59 | 13.38 | 10.04 | 17.38 | 0.12 |

| SK | 0.74 | 0.50 | 7.28 | 5.24 | 60.71 | 62.67 | 21.55 | 18.40 | 14.59 | 9.71 | 5.67 | 1.12 |

| Av. CENE | 0.91 | 0.35 | 9.45 | 4.33 | 62.20 | 67.47 | 21.47 | 22.36 | 11.56 | 10.26 | 12.08 | 3.16 |

| Country | Z-SC | MLPS | FSI | |||||

|---|---|---|---|---|---|---|---|---|

| 2004–2014 * | 2016–2019 | 2020 | 2004–2014 * | 2016–2019 | 2020 | 2016–2019 | 2020 | |

| CZ | 19.05 | 43.60 | 41.79 | 4.79 | 3.33 | 4.2 | 0.04 | 0.06 |

| EE | 21.87 | 41.67 | 44.66 | 3.18 | 4.93 | 4.4 | 0.06 | 0.08 |

| HU | 10.38 | 34.82 | 27.62 | 1.89 | −1.95 | −3.8 | 0.04 | 0.05 |

| LT | 11.96 | 43.71 | 40.11 | −0.08 | 7.53 | 9.0 | 0.02 | 0.07 |

| LV | 12.89 | 35.49 | 34.56 | −4.09 | −3.78 | −5.1 | 0.02 | 0.06 |

| PL | 18.66 | 59.09 | 44.87 | 5.00 | −1.53 | −4.8 | 0.04 | 0.09 |

| SK | 22.61 | 73.41 | 75.19 | 3.72 | 0.55 | 3.8 | 0.01 | 0.05 |

| Av. CEE | 16.22 | 50.54 | 43.67 | - | - | - | 0.03 | 0.07 |

| Variable | Characteristics | Rationale |

|---|---|---|

| ROA | Return on assets | Profitability indicator |

| ROE | Return on equity | Profitability indicator |

| C/I | Cost to income ratio | Cost-efficiency indicator |

| Z-SC | Bank distnce from banktruptcy: compares the capitalization (CAR) and return (ROA) buffers with risk, represented by volatility of returns and measured by standard deviation of ROA | Bank stability indicator |

| MLPS | Multi-level performance score composed of three efficiency ratios (ROE, C/I, and loan accessibility measured by loans to asset ratio) and two stability indicators (Z-score and NPL level), interpreted relatively to the whole analysed group | An aggregate performance idicator |

| FSI | Financial stability indicator Composed of five performance indicators, representing profitability, capital adequacy, asset quality, and two liquidity measures | An aggregate financial stability indicator |

| E_TA | Equity to assets ratio | An indicator of financial leverage |

| TCR | Total capital ratio | The regulatory capital adequacy indicator |

| Variable | Characteristics | Rationale/Explaining Factor | Source of Data |

|---|---|---|---|

| Bank Level Variables | |||

| LN_TA | Ln of total assets | Bank scale | BankFocus (or own culations based on Bankfocus) |

| LO_TA | Loans to assets ratio | Bank credit policy | |

| LO_GR | Non-financial loan growth (annual % change) | Changes in demand and supply of loans | |

| NPL | Non-performing loans ratio | Credit risk | |

| LO_DE | Loans to deposit ratio | Bank financial strategy | |

| NII_OR | Non-interest income ratio | Diversification of incomes | |

| GS_TA | Government debt securities as a share of total assets | Bank involvement in financing of public debt | |

| DEP_GR | The annual growth rate of deposits placed by non-financial sector | Supply of deposits | |

| Macro-Level Variables | |||

| GDP_GR | GDP growth | Economic growth | Eurostat |

| C_GDP | Domestic credit to private sector as % of GDP | Banking sector development indicator | World Bank |

| HHI | Herfindahl–Hirschman Index | Concentration index | ECB: consolidated banking data |

| LTIR | Long-term interest rate (yield to maturity on long-term government bonds) | Interest rate risk | ECB: financial markets and interest rates data |

| Variable | ROA | ROE | C/I |

|---|---|---|---|

| BP(-1) | 0.509 *** (0.187) | 0.634 *** (0.175) | 0.365 * (0.218) |

| Const | −0.818 (1.324) | 3.528 (9.22) | 101.89 * (56.358) |

| GDP_GR | 0.077 *** (0.015) | 0.717 *** (0.124) | −0.848 ** (0.411) |

| C_GDP | 0.005 (0.006) | 0.063 (0.056) | −0.21 (0.186) |

| HHI | 3.345 * (1.913) | 3.371 (14.23) | −72.48 * (42.132) |

| LTIR | 0.064 (0.063) | 0.165 (0.521) | −2.025 (1.344) |

| LN_TA | 0.032 (0.05) | 0.205 (0.288) | −3.741 (2.419) |

| LO_TA | −0.003 (0.003) | −0.066 (0.046) | 0.124 * (0.07) |

| LO_DEP | −0.001 (0.001) | −0.009 (0.01) | 0.015 (0.021) |

| LO_GR | 0.005 (0.004) | 0.045 * (0.024) | −0.166 ** (0.069) |

| NPL | −0.027 ** (0.011) | −0.255 *** (0.084) | 0.387 (0.264) |

| NII_OR | 0.002 (0.005) | −0.025 (0.032) | −0.199 (0.16) |

| GS_TA | −0.005 (0.005) | −0.146 * (0.081) | 0.087 (0.136) |

| DEP_GR | −0.002 *** (0.001) | −0.019 *** (0.007) | 0.08 ** (0.039) |

| No. observation | 228 | 228 | 249 |

| AR (1) test | −1.74442 (0.0211) | −2.00929 (0.0445]) | −2.55095 (0.0107) |

| AR (2) test | 0.877989 (0.3799) | −0.748511 (0.4542) | −1.48856 (0.1366) |

| Hansen test | 4.46435 (0.8130) | 10.5678 (0.2274) | 7.69091 (0.4642) |

| Variable | Z-SC | MLPS | FSI |

|---|---|---|---|

| BP(-1) | 0.864 *** (0.056) | 0.827 *** (0.114) | 0.102 *** (0.020) |

| Const | −0.513 (6.755) | −7.705 (4.690) | 0.075 * (0.044) |

| GDP_GR | 0.276 ** (0.114) | 0.241 ** (0.095) | −0.001 (0.001) |

| C_GDP | 0.142 ** (0.067) | −0.026 (0.028) | 0.000 (0.000) |

| HHI | 2.171 (16.311) | 15.549 * (9.360) | −0.129 (0.096) |

| LTIR | 0.186 (0.709) | −0.088 (0.660) | 0.003 (0.004) |

| LN_TA | −1.251 ** (0.544) | 0.547 (0.481) | 0.001 (0.003) |

| LO_TA | 0.082 (0.053) | - | 0.000 (0.000) |

| LO_DEP | −0.013 (0.028) | 0.009 (0.008) | - |

| LO_GR | −0.006 (0.05) | 0.026 (0.031) | −0.001 *** (0.000) |

| NPL | 0.037 (0.089) | - | - |

| NII_OR | 0.037 (0.055) | 0.029 (0.024) | 0.000 (0.000) |

| GS_TA | 0.187 (0.155) | −0.028 (0.035) | −0.001 ** (0.000) |

| DEP_GR | −0.033 (0.031) | −0.028 ** (0.011) | 0.000 (0.000) |

| No. observation | 228 | 260 | 206 |

| AR (1) test | −1.99955 (0.0455) | −3.76847 (0.0002) | 0.279244 (0.0401) |

| AR (2) test | 0.67514 (0.4996) | 0.682279 (0.4951) | −1.46015 (0.1442) |

| Hansen test | 11.4202 (0.1790) | 15.1513 (0.1563) | 13.5978 (0.2127) |

| Variable | E_TA | TCR |

|---|---|---|

| BC(-1) | 0.852 *** (0.074) | 1.027 *** (0.052) |

| Const | 0.177 (1.13) | −1.111 (2.585) |

| GDP_GR | 0.062 ** (0.031) | −0.128 ** (0.053) |

| C_GDP | 0.011 (0.012) | −0.025 (0.03) |

| HHI | 4.681 (3.795) | −2.225 (5.381) |

| LTIR | 0.193 (0.184) | −0.274 (0.326) |

| LN_TA | −0.233 ** (0.104) | 0.177 (0.16) |

| LO_TA | 0.005 (0.015) | −0.011 (0.016) |

| LO_DEP | 0.007 (0.012) | 0.001 (0.007) |

| LO_GR | −0.019 * (0.011) | −0.038 ** (0.018) |

| NPL | 0.016 (0.021) | −0.059 * (0.03) |

| NII_OR | 0.007 (0.01) | 0.041 *** (0.013) |

| GS_TA | 0.027 (0.02) | 0.03 (0.033) |

| DEP_GR | −0.008 (0.008) | −0.017 (0.015) |

| No. of observation | 249 | 233 |

| AR (1) test | −2.81652 (0.0049) | −2.39085 (0.0168) |

| AR (2) test | 0.460254 (0.6453) | −0.681621 (0.4955) |

| Hansen test | 8.00543 (0.4329) | 5.8789 (0.6608) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miklaszewska, E.; Kil, K.; Idzik, M. How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe. Risks 2021, 9, 180. https://doi.org/10.3390/risks9100180

Miklaszewska E, Kil K, Idzik M. How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe. Risks. 2021; 9(10):180. https://doi.org/10.3390/risks9100180

Chicago/Turabian StyleMiklaszewska, Ewa, Krzysztof Kil, and Marcin Idzik. 2021. "How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe" Risks 9, no. 10: 180. https://doi.org/10.3390/risks9100180

APA StyleMiklaszewska, E., Kil, K., & Idzik, M. (2021). How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe. Risks, 9(10), 180. https://doi.org/10.3390/risks9100180