Understanding Key Drivers of Participant Cash Flows for Individually Managed Stable Value Funds

Abstract

1. Introduction

2. Literature Review on Lapse Behavior, Contextualizing It into the Stable Value Ecosystem, and Hypothesis Development

2.1. Individually Managed Stable Value Regulation and Ecosystem

2.1.1. The 401(k) Withdrawal Treatment

2.1.2. The 401(k) Inner Transfers and Investment Options

2.2. Literature Review and Hypothesis Development

3. Methodology, and Data Collection and Cleansing

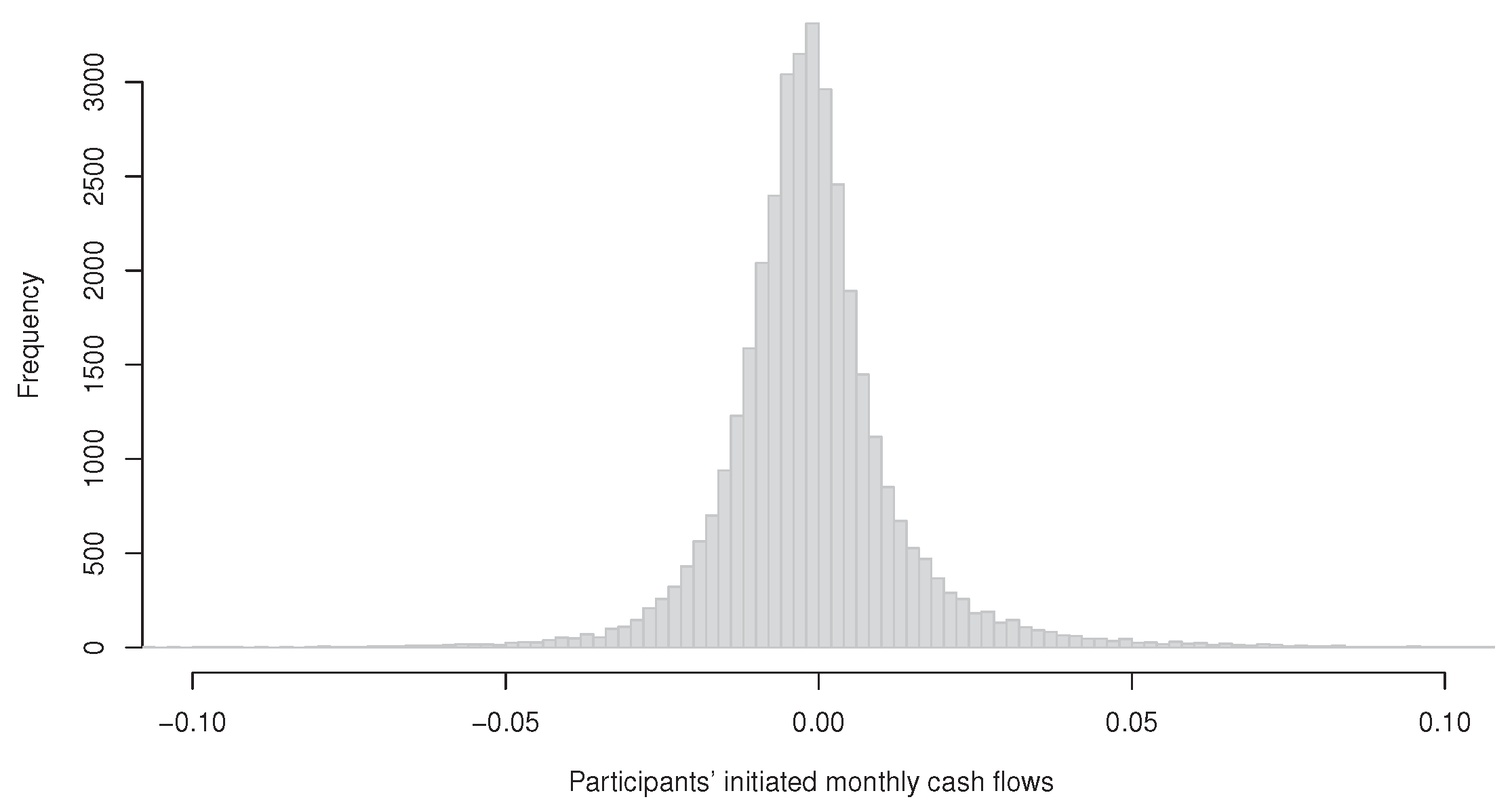

4. Observations

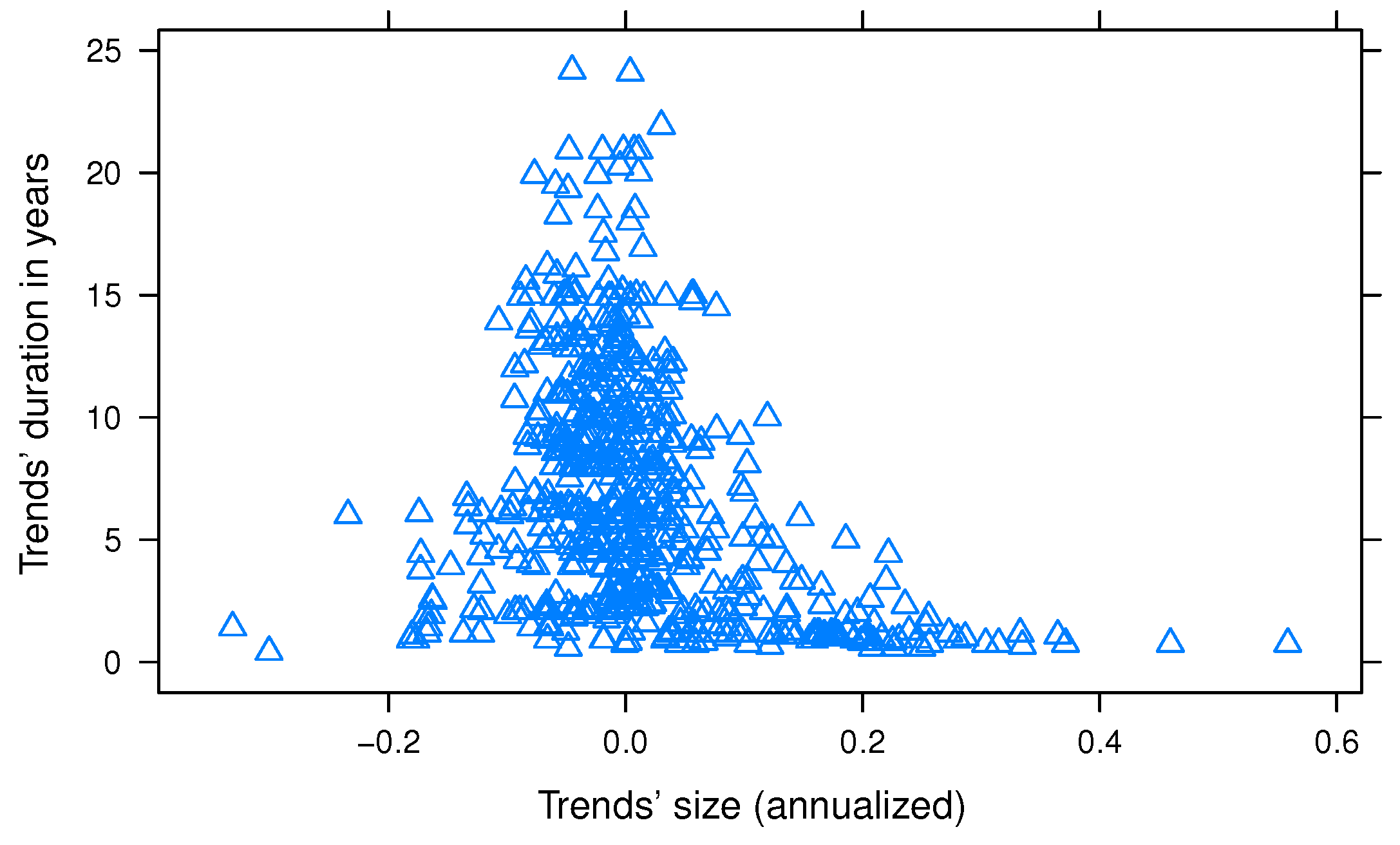

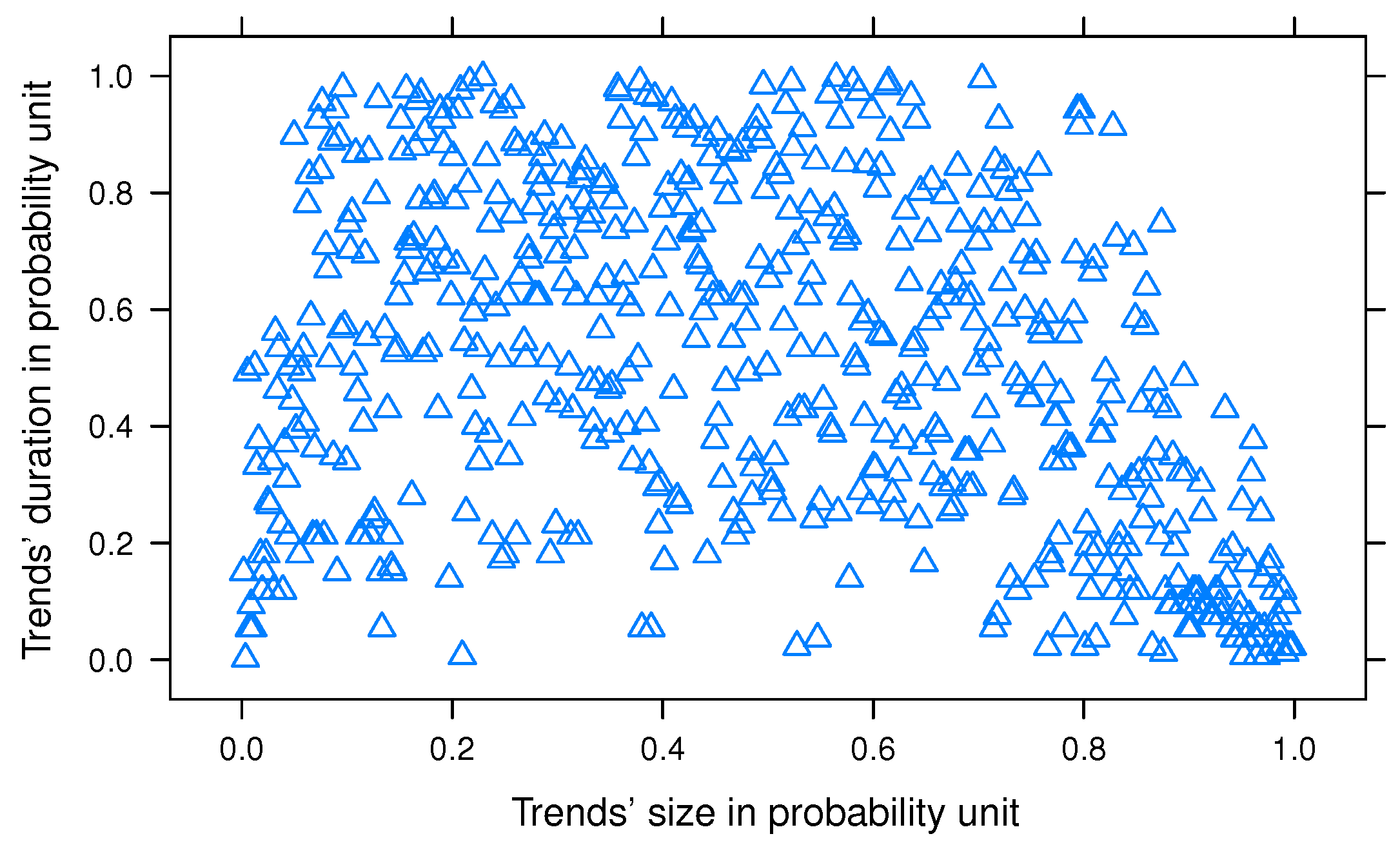

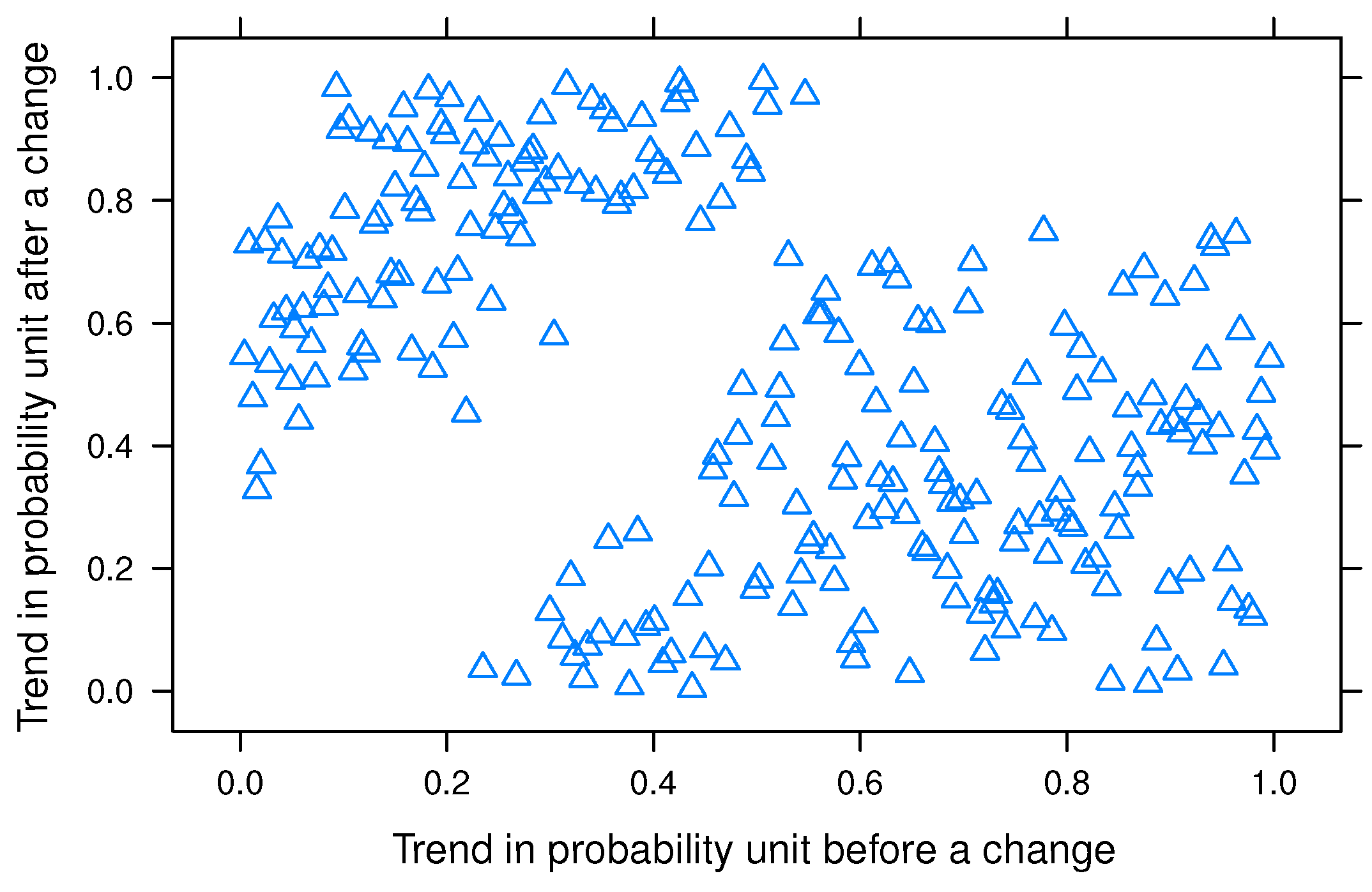

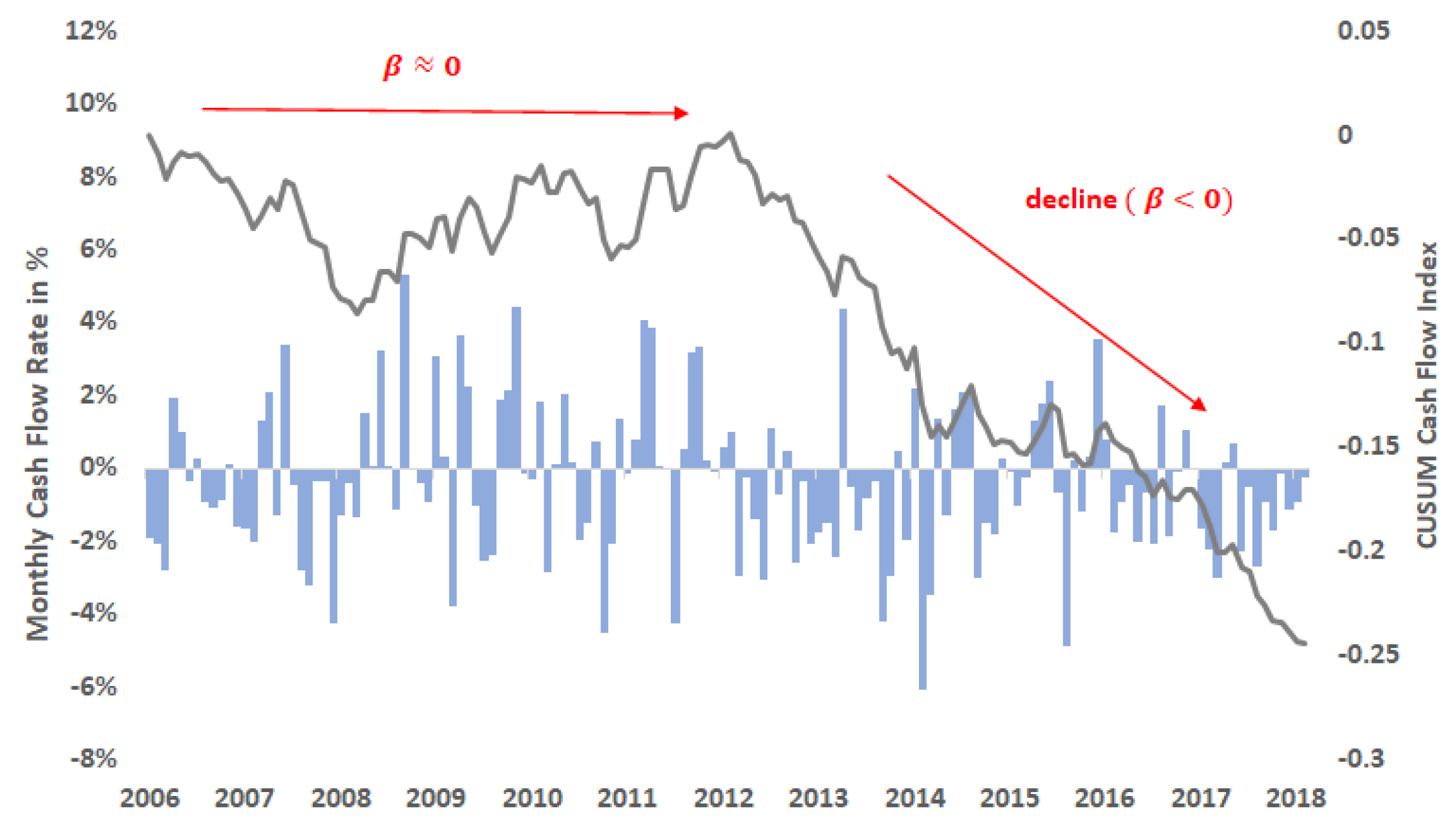

4.1. Trends

4.2. Plan Sponsor’s Ecosystem

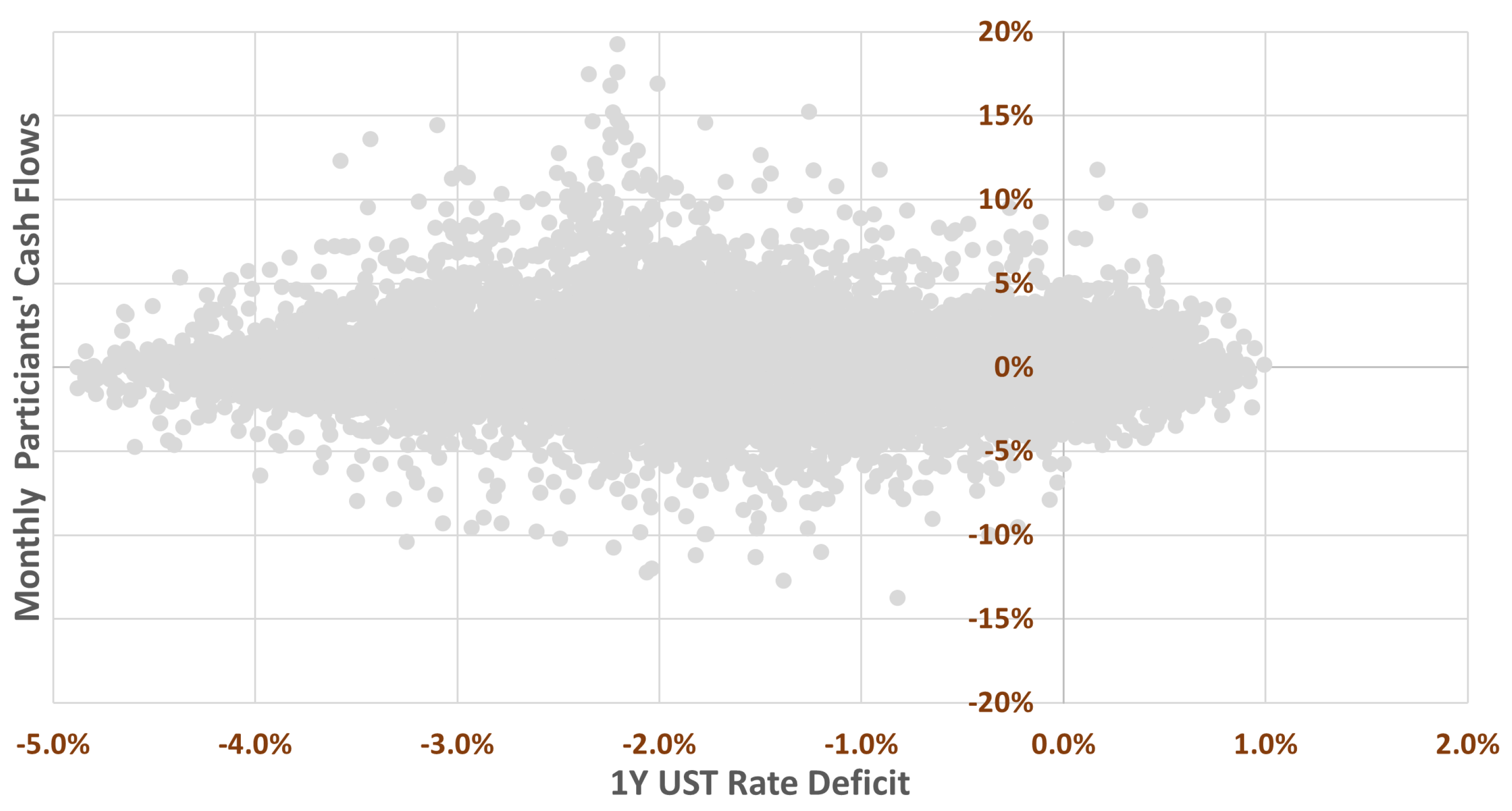

4.3. Rate Deficit Arbitrage

4.4. Herd Behavior

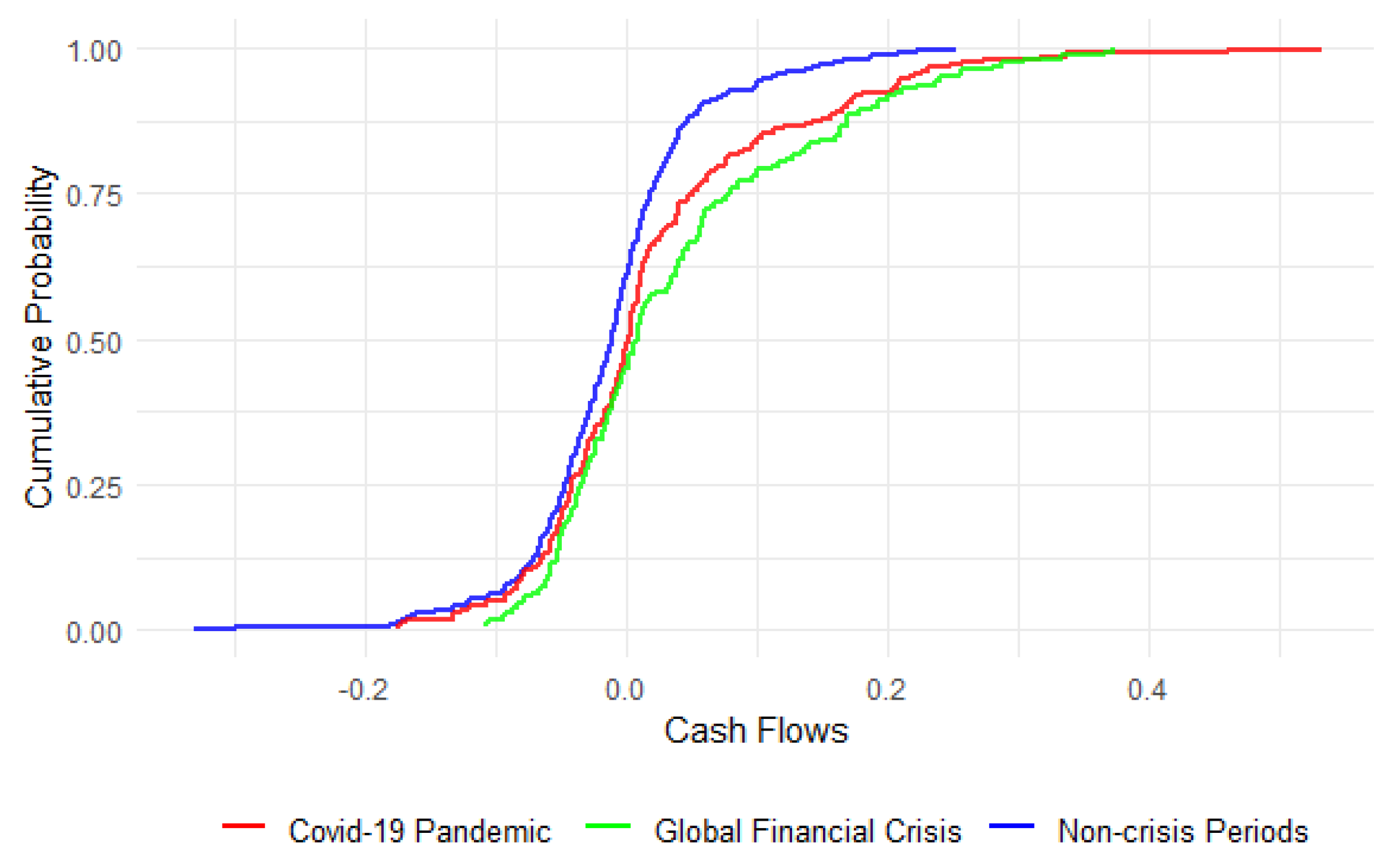

4.5. Flight-to-Safety Behavior

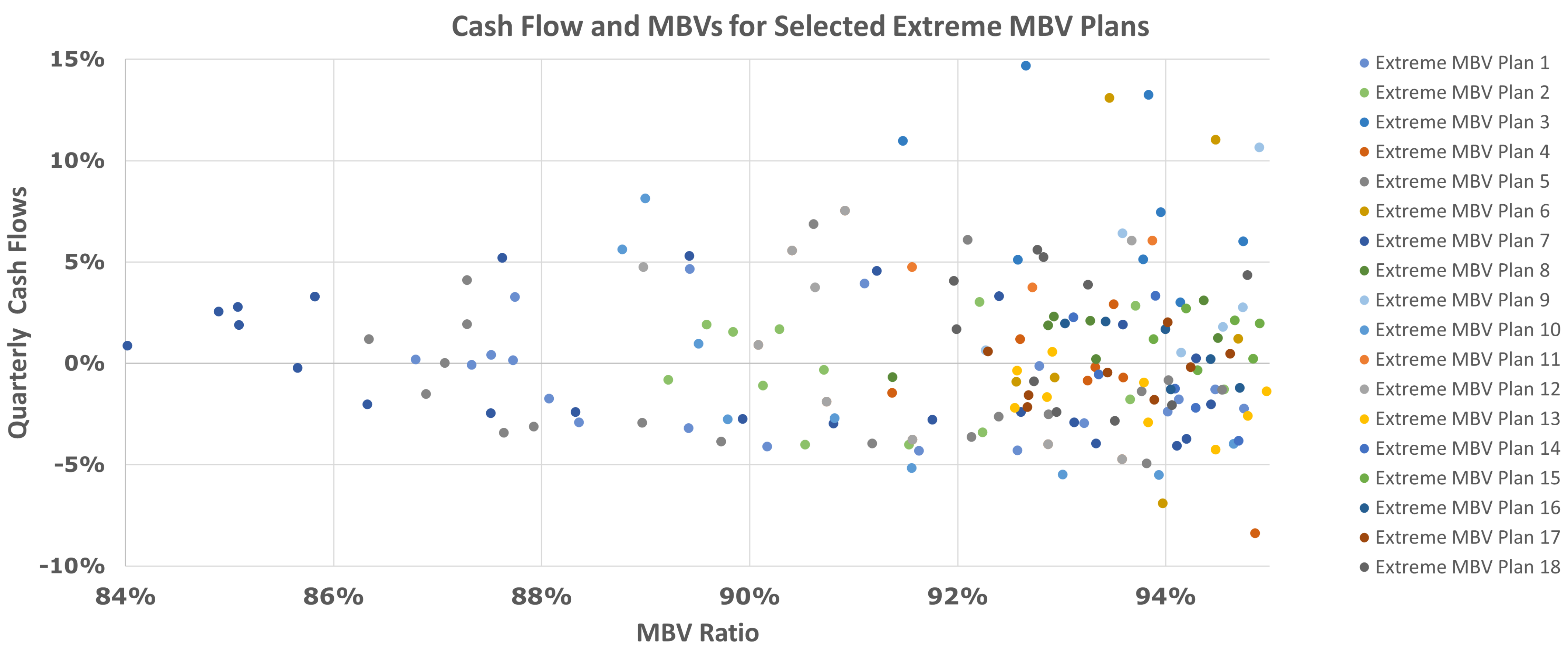

4.6. Moneyness Hypothesis

5. Discussion and Conclusions

- The trend in cash flows is related to the nature of the plan sponsors’ ecosystem, which indirectly influences participants’ behavior.

- A herd behavior component, where the plausibility of this behavior could potentially be influenced by reputational damage6.

- The cash flow risk-mitigating effect of flight-to-safety behavior during a crisis.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Basic Data Statistics

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Historical | Book Value | Number of | Number of | |

|---|---|---|---|---|

| Period | Balances (USD) | Plans | Data Points | |

| Jan. 17–Dec. 21 | 132 | billion | 172 | 27,421 |

| Jan. 14–Dec. 21 | 110 | billion | 137 | 24,416 |

| Jan. 8–Dec. 21 | 78 | billion | 38 | 15,710 |

| Nov. 97–Dec. 21 | 222 | billion | 297 | 41,742 |

| Minimum | Maximum | Average | Standard Deviation | Skewness | Kurtosis |

|---|---|---|---|---|---|

Appendix B. Example Plans’ Cash Flows with Their Respective Trends

Appendix C. ERISA Communication

ABC Corporation 401k Retirement Plan

Investment Options—January 1, 20XX

| Average Annual Total Return | ||||||||

| as of 12/31/XX | Benchmark | |||||||

| Since | Since | |||||||

| Name/Type of Option | 1 yr. | 5 yr. | 10 yr. | Inception | 1 yr. | 5 yr. | 10 yr. | Inception |

| Equity Funds | ||||||||

| A Index Fund/S&P 500 www. website address | 26.5% | 0.34% | −1.03% | 9.25% | 26.46% | 0.42% | −0.95% | 9.30% |

| S&P 500 | ||||||||

| B Fund/Large Cap www. website address | 27.6% | 0.99% | N/A | 2.26% | 27.80% | 1.02% | N/A | 2.77% |

| US Prime Market 750 Index | ||||||||

| C Fund/Int’l Stock www. website address | 36.73% | 5.26% | 2.29% | 9.37% | 40.40% | 5.40% | 2.40% | 12.09% |

| MSCI EAFE | ||||||||

| D Fund/Mid Cap www. website address | 40.22% | 2.28% | 6.13% | 3.29% | 46.29% | 2.40% | −0.52% | 4.16% |

| Russell Midcap | ||||||||

| Bond Funds | ||||||||

| E Fund/Bond Index www. website address | 6.45% | 4.43% | 6.08% | 7.08% | 5.93% | 4.97% | 6.33% | 7.01% |

| Barclays Cap. Aggr. Bd. | ||||||||

| Other | ||||||||

| F Fund/GICs www. website address | 0.72% | 3.36% | 3.11% | 5.56% | 1.8% | 3.1% | 3.3% | 5.75% |

| 3-month US T-Bill Index | ||||||||

| G Fund/Stable Value www. website address | 4.36% | 4.64% | 5.07% | 3.75% | 1.8% | 3.1% | 3.3% | 4.99% |

| 3-month US T-Bill Index | ||||||||

| Generations 2020/Lifecycle Fund www. website address | 27.94% | N/A | N/A | 2.45% | 26.46% | N/A | N/A | 3.09% |

| S&P 500 | ||||||||

| 23.95% | N/A | N/A | 3.74% | |||||

| Generations 2020 Composite Index * | ||||||||

| Name/ Type of Option | Return | Term | Other |

|---|---|---|---|

| H 200X/GIC www. website address | 4% | 2 Yr. | The rate of return does not change during the stated term. |

| I LIBOR Plus/Fixed-Type Investment Account www. website address | LIBOR +2% | Quarterly | The rate of return on 12/31/xx was 2.45%. This rate is fixed quarterly, but will never fall below a guaranteed minimum rate of 2%. Current rate of return information is available on the option’s Web site or at 1-800-yyy-zzzz. |

| J Financial Services Co./Fixed Account Investment www. website address | 3.75% | 6 Mos. | The rate of return on 12/31/xx was 3.75%. This rate of return is fixed for six months. Current rate of return information is available on the option’s Web site or at 1-800-yyy-zzzz. |

| 1 | In fact, these connections contribute to non-monotonic trends in participant cash flows, a phenomenon we will delve into in Section 4.1. |

| 2 | In regulatory terminology, the term “hardship” (IRS 2023c) refers to situations where a participant faces financial difficulties. In cases of immediate and substantial financial need, participants can withdraw a portion of their assets without incurring penalties. |

| 3 | ERISA’s requirements form the lowest bar regarding the level of detail and quality of communication expected, and plan administrators may provide more detailed information to participants. |

| 4 | In this paper, we will use the terms plan sponsor, employer, and company interchangeably, even though they may sometimes refer to different legal entities. |

| 5 | However, we should note that F-test statistics assume a normal distribution for both sets, which is not valid for cash flow trends due to their higher tail kurtosis compared to a normal distribution (as indicated in Table 4). |

| 6 | A low market-to-book value could potentially increase the chances of a reputational issue. |

References

- Alfonsi, Aurélien, Adel Cherchali, and Jose Infante. 2019. A full and synthetic model for Asset-Liability Management in life insurance, and analysis of the SCR with the standard formula. European Actuarial Journal 10: 457–98. [Google Scholar] [CrossRef]

- Babbel, David, and Miguel Herce. 2018. An Update on Stable Value Funds Performance through 2017. Journal of Financial Service Professionals 72: 6. [Google Scholar]

- Babbel, David F., and Miguel Herce. 2007. A Closer Look at Stable Value Funds Performance. Working Paper 07-21. Philadelphia: Wharton Financial Institutions Center. [Google Scholar]

- Bacinello, Anna Rita, Pietro Millossovich, Annamaria Olivieri, and Ermanno Pitacco. 2011. Variable annuities: A unifying valuation approach. Insurance: Mathematics and Economics 49: 285–97. [Google Scholar] [CrossRef]

- Barsotti, Flavia, Xavier Milhaud, and Yahia Salhi. 2016. Lapse risk in life insurance: Correlation and contagion effects among policyholders’ behaviors. Insurance: Mathematics and Economics 71: 317–31. [Google Scholar] [CrossRef]

- Barucci, Emilio, Tommaso Colozza, Daniele Marazzina, and Edit Rroji. 2020. The determinants of lapse rates in the italian life insurance market. European Actuarial Journal 10: 149–78. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Brian M. Lucey. 2010. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Butrica, Barbara A., and Karen E. Smith. 2016. 401(k) participant behavior in a volatile economy. Journal of Pension Economics & Finance 15: 1–29. [Google Scholar]

- Chen, Jie, and Arjun K. Gupta. 2011. Parametric Statistical Change Point Analysis: With Applications to Genetics, Medicine, and Finance. Berlin/Heidelberg: Springer Science & Business Media. [Google Scholar]

- Chen, Qitong, Huiming Zhu, Dongwei Yu, and Liya Hau. 2022. How does investor attention matter for crude oil prices and returns? evidence from time-frequency quantile causality analysis. The North American Journal of Economics and Finance 59: 101581. [Google Scholar] [CrossRef]

- Cheng, Chunli, Christian Hilpert, Aidin Miri Lavasani, and Mick Schaefer. 2019. Surrender Contagion in Life Insurance: Modeling and Valuation. European Journal of Operational Research 305: 1465–79. [Google Scholar] [CrossRef]

- Chiang, Thomas C., and Dazhi Zheng. 2010. An empirical analysis of herd behavior in global stock markets. Journal of Banking & Finance 34: 1911–21. [Google Scholar]

- Cumming, Douglas, and Na Dai. 2009. Capital flows and hedge fund regulation. Journal of Empirical Legal Studies 6: 848–73. [Google Scholar] [CrossRef]

- Dar, Atul, and C. Dodds. 1989. Interest rates, the emergency fund hypothesis and saving through endowment policies: Some empirical evidence for the uk. Journal of Risk and Insurance 1989: 415–33. [Google Scholar] [CrossRef]

- De Giovanni, Domenico. 2010. Lapse rate modeling: A rational expectation approach. Scandinavian Actuarial Journal 2010: 56–67. [Google Scholar] [CrossRef]

- Dorn, Daniel, and Gur Huberman. 2005. Talk and action: What individual investors say and what they do. Review of Finance 9: 437–81. [Google Scholar] [CrossRef]

- Eberhardt, Wiebke, Elisabeth Brüggen, Thomas Post, and Chantal Hoet. 2021. Engagement behavior and financial well-being: The effect of message framing in online pension communication. International Journal of Research in Marketing 38: 448–71. [Google Scholar] [CrossRef]

- El-Shagi, Makram, Tobias Knedlik, and Gregor von Schweinitz. 2013. Predicting financial crises: The (statistical) significance of the signals approach. Journal of International Money and Finance 35: 76–103. [Google Scholar] [CrossRef]

- Eling, Martin, and Michael Kochanski. 2013. Research on lapse in life insurance: What has been done and what needs to be done? The Journal of Risk Finance 14: 392–413. [Google Scholar] [CrossRef]

- Federal Reserve Bank of St. Louis. 2020. Moody’s Seasoned Baa Corporate Bond Yield. Available online: https://fred.stlouisfed.org/series/BAA (accessed on 19 July 2023).

- Floryszczak, Anthony, Olivier Le Courtois, and Mohamed Majri. 2016. Inside the solvency 2 black box: Net asset values and solvency capital requirements with a least-squares monte-carlo approach. Insurance: Mathematics and Economics 71: 15–26. [Google Scholar] [CrossRef]

- Hassani, Hossein, and Emmanuel Sirimal Silva. 2015. A kolmogorov-smirnov based test for comparing the predictive accuracy of two sets of forecasts. Econometrics 3: 590–609. [Google Scholar] [CrossRef]

- Hawkins, Douglas M. 1977. Testing a sequence of observations for a shift in location. Journal of the American Statistical Association 72: 180–86. [Google Scholar] [CrossRef]

- Hirshleifer, David, and Siew Hong Teoh. 2003. Herd behaviour and cascading in capital markets: A review and synthesis. European Financial Management 9: 25–66. [Google Scholar] [CrossRef]

- IRS. 2023a. 401k Resource Guide Plan Participants General Distribution Rules. Available online: https://www.irs.gov/retirement-plans/plan-participant-employee/401k-resource-guide-plan-participants-general-distribution-rules (accessed on 19 July 2023).

- IRS. 2023b. Retirement Plan Distributions: Exceptions to 10% Additional Tax. Available online: https://www.irs.gov/pub/irs-pdf/p5036.pdf (accessed on 19 July 2023).

- IRS. 2023c. Retirement Topics—Hardship Distributions. Available online: https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-hardship-distributions (accessed on 19 July 2023).

- Ji, Qiang, Dayong Zhang, and Yuqian Zhao. 2020. Searching for safe-haven assets during the COVID-19 pandemic. International Review of Financial Analysis 71: 101526. [Google Scholar] [CrossRef]

- Kalantonis, Petros, Christos Kallandranis, and Marios Sotiropoulos. 2021. Leverage and firm performance: New evidence on the role of economic sentiment using accounting information. Journal of Capital Markets Studies 5: 96–107. [Google Scholar] [CrossRef]

- Kim, Changki. 2005. Modeling surrender and lapse rates with economic variables. North American Actuarial Journal 9: 56–70. [Google Scholar] [CrossRef]

- Knoller, Christian, Gunther Kraut, and Pascal Schoenmaekers. 2016. On the propensity to surrender a variable annuity contract: An empirical analysis of dynamic policyholder behavior. Journal of Risk and Insurance 83: 979–1006. [Google Scholar] [CrossRef]

- Kuo, Weiyu, Chenghsien Tsai, and Wei-Kuang Chen. 2003. An empirical study on the lapse rate: The cointegration approach. Journal of Risk and Insurance 70: 489–508. [Google Scholar] [CrossRef]

- Kwun, David, Cyrus Mohebbi, Andrew Line, and Yong-Tai Tsai. 2009. A risk analysis of stable value protection for bank-owned life insurance. International Journal of Applied Decision Sciences 2: 406–21. [Google Scholar] [CrossRef]

- Kwun, David, Cyrus Mohebbi, Marc Braunstein, and Andrew Line. 2010. A risk analysis of 401k stable value funds. International Journal of Applied Decision Sciences 3: 151–67. [Google Scholar] [CrossRef]

- Loisel, Stéphane, and Xavier Milhaud. 2011. From deterministic to stochastic surrender risk models: Impact of correlation crises on economic capital. European Journal of Operational Research 214: 348–57. [Google Scholar] [CrossRef]

- Lyubchich, Vyacheslav, Yulia R. Gel, and Abdel El-Shaarawi. 2013. On detecting non-monotonic trends in environmental time series: A fusion of local regression and bootstrap. Environmetrics 24: 209–26. [Google Scholar] [CrossRef]

- Madrian, Brigitte C., and Dennis F. Shea. 2001. The power of suggestion: Inertia in 401(k) participation and savings behavior. The Quarterly Journal of Economics 116: 1149–87. [Google Scholar] [CrossRef]

- Mahdavi-Damghani, Babak. 2012. Utope-ia. Wilmott 2012: 28–37. [Google Scholar]

- Mitchell, Olivia S., and Stephen P. Utkus. 2022. Target-date funds and portfolio choice in 401 (k) plans. Journal of Pension Economics & Finance 21: 519–36. [Google Scholar]

- Mitchell, Olivia S., Gary R. Mottola, Stephen P. Utkus, and Takeshi Yamaguchi. 2006. The Inattentive Participant: Portfolio Trading Behavior in 401(K) Plans. Working Paper WP 2006-115. London: Michigan Retirement Research Center. [Google Scholar]

- Outreville, J. Francois. 1990. Whole-life insurance lapse rates and the emergency fund hypothesis. Insurance: Mathematics and Economics 9: 249–55. [Google Scholar] [CrossRef]

- Phillips, Joseph M., Jr., Barry B. Schweig, and James P. Scott. 1985. Explaining whole life insurance lapse rates. The Journal of Insurance Issues and Practices 1985: 32–40. [Google Scholar]

- Shin, Hyun Song. 2009. Reflections on northern rock: The bank run that heralded the global financial crisis. Journal of Economic Perspectives 23: 101–19. [Google Scholar] [CrossRef]

- Sierra Jimenez, Jesus A. 2012. Consumer Interest Rates and Retail Mutual Fund Flows. Available online: https://www.bankofcanada.ca/2012/12/working-paper-2012-39/ (accessed on 19 July 2023).

- SVIA. 2020a. Stable Value at a Glance. Available online: https://www.stablevalue.org/knowledge/stable-value-at-a-glance (accessed on 19 July 2023).

- SVIA. 2020b. Stable Value Quarterly Characteristic Survey. California: SVIA, December. [Google Scholar]

- Tang, Ning, Olivia S. Mitchell, Gary R. Mottola, and Stephen P. Utkus. 2010. The efficiency of sponsor and participant portfolio choices in 401 (k) plans. Journal of Public Economics 94: 1073–85. [Google Scholar] [CrossRef]

- Tobe, Christopher B. 2004. The Consultants Guide to Stable Value. Journal of Investment Consulting 7: 1. [Google Scholar]

- Tsai, Chenghsien, Weiyu Kuo, and Wei-Kuang Chen. 2002. Early surrender and the distribution of policy reserves. Insurance: Mathematics and Economics 31: 429–45. [Google Scholar] [CrossRef]

- U.S. Department of Labor. 2020. Model Comparative Chart—ABC Corporation 401k Retirement Plan. Available online: https://www.dol.gov/sites/dolgov/files/ebsa/about-ebsa/our-activities/resource-center/publications/providing-information-in-participant-directed-plans-model-chart.pdf (accessed on 19 July 2023).

- Vo, Lai Van, and Huong T. T. Le. 2023. From hero to zero-the case of silicon valley bank. Electronic Journal 2023: 1–22. [Google Scholar]

- Wang, Lan, Michael G. Akritas, and Ingrid Van Keilegom. 2008. An anova-type nonparametric diagnostic test for heteroscedastic regression models. Journal of Nonparametric Statistics 20: 365–82. [Google Scholar] [CrossRef]

- Xiong, James X., and Thomas M. Idzorek. 2012. Estimating credit risk and illiquidity risk in guaranteed investment Products. Journal of Financial Planning 25: 38–47. [Google Scholar]

- Yang, Lu. 2022. Idiosyncratic information spillover and connectedness network between the electricity and carbon markets in europe. Journal of Commodity Markets 25: 100185. [Google Scholar] [CrossRef]

- Yang, Lu, and Shigeyuki Hamori. 2021. The role of the carbon market in relation to the cryptocurrency market: Only diversification or more? International Review of Financial Analysis 77: 101864. [Google Scholar] [CrossRef]

- Yang, Lu, Shuairu Tian, Wei Yang, Mingli Xu, and Shigeyuki Hamori. 2018. Dependence structures between chinese stock markets and the international financial market: Evidence from a wavelet-based quantile regression approach. The North American Journal of Economics and Finance 45: 116–37. [Google Scholar] [CrossRef]

| Early Withdrawal | |

|---|---|

| Age | After participant/IRA owner reaches age 59½ |

| Death | After the death of the participant/IRA owner |

| Disability | Total and permanent disability of the participant |

| Domestic relations | To an alternate payee under a Qualified Domestic Relations Order |

| Medical health | Insurance premiums paid while unemployed, amount of non-reimbursed medical expenses up to a limit |

| Rollover | In-plan Roth rollovers or eligible distributions contributed to another retirement plan or IRA |

| Hardship | |

| Medical | Medical care expenses for the employee, the employee’s spouse, dependents, or beneficiary |

| Housing | Costs directly related to the purchase of an employee’s principal residence (excluding mortgage payments) Payments necessary to prevent the eviction of the employee from the employee’s principal residence or foreclosure on the mortgage on that residence Certain expenses to repair damage to the employee’s principal residence |

| Education | Tuition, related educational fees, and room and board expenses for the next 12 months of post-secondary education for the employee or the employee’s spouse, children, dependents, or beneficiary |

| Death | Funeral expenses for the employee, the employee’s spouse, children, dependents, or beneficiary |

| Loans | |

| Loans | The maximum amount a participant may borrow from the plan is 50% of the account balance or USD 50,000, whichever is less |

| Test | Number of Plans Not Rejected | Number of Plans Rejected |

|---|---|---|

| Durbin–Watson | 134 | 184 |

| Ljung–Box (Lag 12) | 185 | 133 |

| Ljung–Box (Lag 1) | 162 | 156 |

| Test | Number of Plans Not Rejected | Number of Plans Rejected |

|---|---|---|

| WAVK | 154 | 126 |

| Standard | ||||||

|---|---|---|---|---|---|---|

| Minimum | Maximum | Average | Deviation | Skewness | Kurtosis | |

| Trends’ size * | ||||||

| Trends’ duration | 6 months | 24.5 years | 7.5 years | 5.3 years |

| Test | Test Stat. | p-Value |

|---|---|---|

| F-test | 1.3243 | 0.06 |

| Bartlett’s test | 3.824 | 0.06 |

| Levene test | 1.7823 | 0.1825 |

| Chi-square test | 3.7830 | 0.2394 |

| Spearman Corr | Kendall Tau | |

|---|---|---|

| Current trend size and next trend size | −0.083 | −0.029 |

| Current duration and next trend size | 0.048 | 0.034 |

| Event Occurring during the Period of a Drastic Change in Trend | Number of Plans | Trend Sign |

|---|---|---|

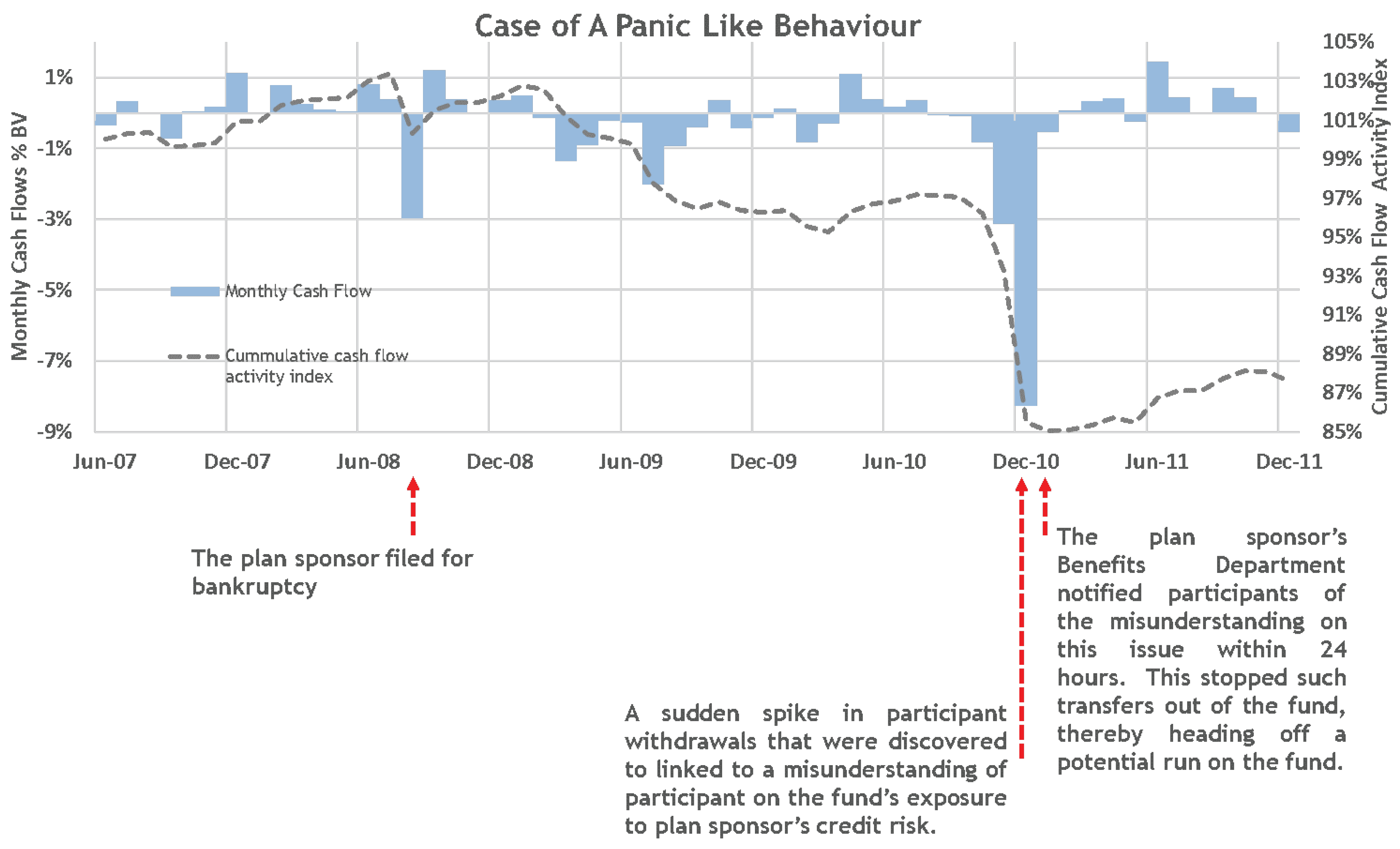

| Bankruptcy | 3 | Negative |

| Employment growth or reduction | 7 | Respectively + and − |

| Flight to safety during crisis | 11 | Positive |

| Introduction of new investment options with being the default options | 2 | Negative |

| Post spinoff/merger participant voluntary transfer to/from new investment scheme | 6 | Spinoffs: +, Mergers + or − |

| Reputational issues leading mass withdrawal | 1 | Negative |

| Coefficient | Number of | ||||

|---|---|---|---|---|---|

| Lag | Correlation | R | of Regression | p-Value | Data Points |

| 0 y | 1.8% | 0.03% | 2.9% | 0.04% | 36,259 |

| 1 y | 2.7% | 0.06% | 3.5% | 0.06% | 36,259 |

| Subgroup | Number of (Trend) Data Points |

|---|---|

| Group 1: global financial crisis | 158 |

| Group 2: COVID-19 pandemic | 207 |

| Group 3: non-crisis periods | 489 |

| Common in Group 1 and 3 | 0 |

| Common in Group 2 and 3 | 178 |

| Common in Group 1, 2, and 3 | 0 |

| Test | Comparison | Test Statistic | p-Value | Decision | |

|---|---|---|---|---|---|

| K-S (Greater) | Non-crisis vs. COVID-19 | 5.79 | Reject | ||

| K-S (Greater) | Non-crisis vs. GFC | 1.11 | Reject | ||

| K-S (Greater) | COVID-19 vs. GFC | 9.83 | Not Reject | ||

| Mann–Whitney U | Non-crisis vs. COVID-19 | 2.34 | Reject | ||

| Mann–Whitney U | Non-crisis vs. GFC | 7.44 | Reject | ||

| Mann–Whitney U | COVID-19 vs. GFC | 1.46 | Not Reject | ||

| KSPA | Non-crisis vs. COVID-19 | 9.96 | Not Reject | ||

| KSPA | Non-crisis vs. GFC | 9.83 | Not Reject | ||

| KSPA | COVID-19 vs. GFC | 4.31 | Reject |

| Coefficient of | Number of | ||

|---|---|---|---|

| Correlation | Determination | p-Value | Observations |

| 4.12 | 1.46 | 35,049 |

| Coefficient of | Number of | |||

|---|---|---|---|---|

| Period | Correlation | Determination | p-Value | Observations |

| Global Financial Crisis | −1.78 | 3.18 | 0.00 | 4893 |

| COVID-19 Pandemic | −3.40 | 1.2 | 2.97 | 4108 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alimoradian, B.; Jakubiak, J.; Loisel, S.; Salhi, Y. Understanding Key Drivers of Participant Cash Flows for Individually Managed Stable Value Funds. Risks 2023, 11, 148. https://doi.org/10.3390/risks11080148

Alimoradian B, Jakubiak J, Loisel S, Salhi Y. Understanding Key Drivers of Participant Cash Flows for Individually Managed Stable Value Funds. Risks. 2023; 11(8):148. https://doi.org/10.3390/risks11080148

Chicago/Turabian StyleAlimoradian, Behzad, Jeffrey Jakubiak, Stephane Loisel, and Yahia Salhi. 2023. "Understanding Key Drivers of Participant Cash Flows for Individually Managed Stable Value Funds" Risks 11, no. 8: 148. https://doi.org/10.3390/risks11080148

APA StyleAlimoradian, B., Jakubiak, J., Loisel, S., & Salhi, Y. (2023). Understanding Key Drivers of Participant Cash Flows for Individually Managed Stable Value Funds. Risks, 11(8), 148. https://doi.org/10.3390/risks11080148