Abstract

Risk management in electricity markets is essential for decision making that involve uncertainty. This article researches the dominant themes and research trends in risk management in electricity markets using descriptive analysis, literature mapping, and data mining techniques. The proposed methodology generates the clusters within the dominant themes and provides a comprehensive view of the main authors, journals, and publications, as well as the main lines of research. The results reveal that the academic production of the subject is increasing and the research trends focused on financial risk management, energy resource management, and that climate coverage mechanisms are of great interest to the scientific community.

1. Introduction

Effective risk management is fundamental for electricity market agents (Huang et al. 2012; Liu et al. 2006) because it encourages an active demand response and improves its performance (Zhang and Wang 2009). Companies that participate in energy markets are exposed to physical and financial risks due to the highly competitive environment (Das and Wollenberg 2005). Consequently, market participants require hedging strategies to manage the operations of the system, their investment portfolios (Wu 2008), and to determine the sale price that will be offered to clients (Kharrati et al. 2016). This is how different strategies have been developed that seek to improve the management of energy resources such as virtual plants or smart networks; initiatives that seek energy efficiency by incorporating information technologies to maximize the economic benefit through the programming and control of resources (Shen et al. 2016). On the other hand, there are tools that seek to mitigate the financial risks associated with fluctuations in the price of electricity, since the time series presents high volatility compared to other commodities (Li 2013). In this regard, hedging instruments have been developed such as futures, forwards, and bilateral contracts that act as an effective tool for risk management and have been widely used in the electricity markets (Anderson et al. 2007).

In reference to the above-mentioned information, interest in risk management in electricity markets has been growing in recent years and different research has focused on this topic; this way, the subject has an important and relevant academic production that needs to be studied. This work presents an analysis of the main contributions on the subject of risk management in electricity markets using bibliometric tools and systematic mapping of literature to analyze the available information and determine the main dominant themes and research trends. In this context, the main authors, journals, and impact factor of the 538 found documents are presented; however, the most important contribution of this work is the determination of the most relevant topics studied in the field of electricity market risks using group analysis.

The work is carried out as follows. Initially, the study design is presented where the methodology used is explained; subsequently, the results are presented emphasizing the predominant cluster in the investigation and finally, the article is concluded.

2. Materials and Methods

In this study, the standard scheme for the design and execution of research based on the analysis and interpretation of bibliometric databases, which consists of the following phases: (1) design; (2) data collection; (3) analysis; (4) visualization; and (5) interpretation.

The main objective of this research is to determine the dominant research themes in risk management in the electricity markets around the world, as well as to establish current research trends. Table 1 lists the parameters of the study performed. The remainder of this section expands on and discusses some of the study parameters that appear in that table.

Table 1.

Parameters of the study.

2.1. Search String Layout

An adequate construction of the search string is essential for the location and recovery of the documents that make up the study. In the first phase, the following search string was specified:

TITLE ((electricity OR Energy) AND ({risk management})) OR AUTHKEY ((electricity OR Energy) AND ({risk management}))

In order to carry out a preliminary identification of keywords; within this search string, 771 documents were recovered. Thanks to the facilities of the Scopus user interface, it was necessary to analyze the list of the author’s most frequent keywords, to determine if there were terms not considered in the initial string. In parallel, the references of the most relevant documents retrieved were also analyzed in order to establish which relevant documents had not been retrieved by the preliminary search string. Next, the titles of the recovered documents were analyzed to determine which of them should not be included in the research, and to establish why they were recovered. From the results obtained, a new search string was built:

TITLE (market* AND (electricity OR “day-ahead” OR energy) AND (hedg* OR derivativ* OR {price risk} OR {risk management} OR {risk assessment} OR {energy risk})) OR AUTHKEY (market* AND (electricity OR “day-ahead” OR energy) AND (hedg* OR derivativ* OR {price risk} OR {risk management} OR {risk assessment} OR {energy risk}))

This allowed researchers to recover a total of 557 documents. To finalize the selection process, the titles and abstracts of the automatically retrieved documents were reviewed, and in some cases, the article itself. This process allowed 19 documents to be discarded. The final database obtained consisted 538 documents.

2.2. Data Preparation

During this phase, a homogenization of the available information was carried out. This covers the processes of removal of accents, formatting, and disambiguation of author names, extraction of country names, and organization of the author affiliation field, cleaning, and homogenization of author keywords.

2.3. Clusters with Dominant Themes

To determine the author’s keyword clusters with dominant themes, it was necessary to build the author’s keyword co-occurrence matrix. This is a symmetric matrix where the rows and columns correspond to the keywords; the leading slash is the number of times each keyword appears in the database. This matrix is normalized using the association index in order to emphasize co-occurrences above the value obtained when one keyword appears randomly with another. The normalized matrix was transformed into an equivalent network, so it is possible to use community detection algorithms such as Louvain’s. A symmetric square matrix, such as keyword co-occurrence matrices, can be interpreted as a network where the rows or columns represent the nodes and the matrix elements represent the connections; thus, a higher co-occurrence value between two keywords represents a stronger relationship between them. The Louvain algorithm is a community detection algorithm in networks developed by Blondel et al. (2008) which seeks the best possible groups by optimizing the network’s modularity; that is, the method seeks the best groups of keywords, which represent terms that often appear together and, therefore, represent dominant themes. The Louvain method starts with small communities and then adds them up until the algorithm converges.

3. Results

This section presents the main bibliometric indicators obtained for the database of the final 538 selected articles.

3.1. Basic Indicators

For this study, 538 documents published in 277 journals were used, with an average of 1.94 documents per journal. The papers were written by 1231 authors belonging to 661 organizations in 53 countries, where the first authors of each paper are affiliated with 365 institutions in 38 countries. When analyzing the number of authors per document, it was found that there are 56 documents with a single author, written by 53 different authors, and 482 documents with more than one author, with an average of 3.3 co-authors per document. In terms of collaboration, a 27.6% of international co-authorship was found. In the analyzed database, there are 14,374 references, with an average of 27.43 references per document. On the other hand, there are 1345 author keywords and 2506 index keywords; after the keyword cleaning process, these go to 1152 and 2093, respectively.

3.2. Production per Year

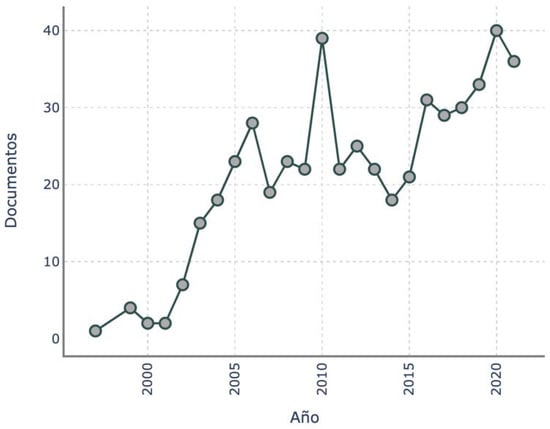

Figure 1 presents the number of articles published per year. A long-term growing trend is observed, with an average annual rate of 28.3%. There are two periods of increasing trend (2001–2006 and 2014–2021), and a stable period (2007–2013), which presents a pronounced peak of 39 publications in 2010. This figure indicates a permanent interest from the scientific community in the research area.

Figure 1.

Number of articles published per year from 1997 until 2021.

3.3. Main Journals

Table 2 lists the main indicators of the journal group made up of the ten journals with the largest number of articles and the ten most cited journals. This table shows that the most cited journal is IEEE TRANS POWER SYST with a total of 1459 citations, followed by the ENERGY ECON journal with 830 citations (56% of the citations obtained by the most cited). Given that the individual analysis of each of these indicators can bias the interpretation of the results, it is more convenient to use composite indicators such as the H index, which indicates that there are H articles with H or more citations, which quantifies both the productivity and the impact of publications. In this sense, the journal with the highest impact publications is IEEE TRANS POWER SYST, followed by ENERGY ECON and DIANLI XITONG ZIDONGHUE. On the other hand, it is found that the journal with the largest number of documents is ENERGY ECON with 39 documents, followed by DIANLI XITONG ZIDONGHUE with 28 documents and IEEE TRANS POWER SYST with 24 documents. The latter can be considered the journal with the highest impact factor since it has the highest indicators.

Table 2.

The most important journals in terms of publications and citations.

3.4. Main Countries

Table 3 shows the indicators for the group of the ten most cited countries and the ten countries with the highest productivity. It is evident that the country with the highest number of citations is the United States with 22.13% of the total citations, it also has the highest H index, followed by China with 13.48% of citations and has the largest number of documents, and then there is Iran with 6.14% of citations. Regarding the average number of citations per document, it is evident that the highest indicator is found in Finland (29.08), followed by the United States (27.68) and Iran (25.59). According to the results, the country with the greatest contribution to the research topic is the United States, since it has the highest average number of citations per document, the highest number of citations, and the highest H index. This last indicator measures the quality of scientific production.

Table 3.

Most cited countries.

When analyzing the country co-occurrence matrix for the 20 most productive countries, four groups of countries are found that frequently publish together: (a) United Kingdom, France, Iran, India, Ireland, Finland, and Turkey; (b) China, the United States, Hong Kong, Australia, Italy, and Brazil; (c) Germany, Norway, and Denmark; and (d) Portugal, Spain, and Colombia. Table 4 shows the international collaboration indicators where it is evident that the countries with the highest collaboration rate are the following: Hong Kong with 94%, the United Kingdom with 74%, and Australia with 71%. Additionally, this table presents the production of documents for the main countries, broken down by country(ies) of origin. In this sense, it is evident that countries with high levels of production, such as China and the United States, have low collaboration rates, 29% and 32%; in contrast, the countries with the highest collaboration rates are the following: Hong Kong (94%), United Kingdom (74%), and Australia (71%). Hong Kong’s production stands out as it has the highest collaboration rate and is in fourth position in the ranking of publications and has an average of 22.06 citations per document. It is concluded that collaboration between countries positively impacts the production of research.

Table 4.

International collaboration indicators for the ten most productive countries.

3.5. Authors

Table 5 lists the indicators for the authors with the largest number of publications and the most cited authors. The first two columns of the table present the ranking of publications and citations. Considering both criteria, it is concluded that the five authors with the greatest impact on the publications are the following: Shamshirband S/1, Mekhilef S, Wang J/8, Chen Z/22, and Liu H/27. In addition, the first two authors have the highest H-index.

Table 5.

Most important authors in terms of publications and citations.

On the other hand, it was necessary to analyze the groups of authors who publish frequently; for this, the 20 most frequent authors were considered, and the same procedure was applied to obtain the countries that usually publish together. Six clusters of authors were found: (1) Zhang SH, Wen F-S, Wong KP, Dong ZY, and Xue Y; (2) Zhou M, Li G-Y, and Ni Y-X; (3) Azevedo F, Vale ZA, and Lopes F; (4) Wang X-F and Zhang Q/2; (5) Xiao D and Qiao W; and (6) Wu FF and Liu M.

3.6. Most Published Citations

The article with the largest number of citations is: “Equilibrium Pricing and Optimal Hedging in Electricity Forward Markets”, in which an equilibrium model is presented to set the prices of energy derivative contracts (Bessembinder and Lemmon 2002). In second place is the document: “Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold”, which uses a VAR-GARCH model to analyze the relationship between the prices of some energy commodities and the S&P 500. In third place is the work: “An Empirical Analysis of the Impact of Hedge Contracts on Bidding Behavior in a Competitive Electricity Market”, in which the behavior of the Australian electricity market negotiations is analyzed, incorporating several sources of uncertainty and futures contracts (Wolak 2000). These articles study financial risk management in electricity markets and its alternatives for hedging purposes. The information of the main publications with their respective number of citations and DOI is shown in Table 6.

Table 6.

Most published citations.

4. Discussion

This section discusses the results obtained by applying the Louvain community detection algorithm to the author’s keyword co-occurrence matrix obtained after performing a cleaning and homogenization process of the texts. This process was carried out in order to detect the main keyword clusters to determine the main trends in risk management research in electricity markets.

Table 7 presents the detailed information for the six groups obtained. For its computation, keywords with a frequency equal to or greater than five (5) were considered. As shown in the table, the first cluster groups the largest number of keywords (29.1%) of the total words analyzed. The other five keyword clusters have a frequency between 12.7% and 16.4%.

Table 7.

Thematic groups.

Cluster 1. Risk management on financial assets and wind power generation.

The first cluster contains the works focused on financial risk management to maximize economic benefits and reduce the corresponding risk (Liu and Wu 2008) through a negotiation strategy that includes measures to risk assessment and simulation models (Jain and Srivastava 2009). In this context, there are studies that focus on portfolio theory to propose an energy purchase decision system in the bilateral market (Azevedo et al. 2003) and in the spot market (Zhou et al. 2006). Other works focus on assessing risk using VaR (value at risk) (Boroumand et al. 2015; Das and Wollenberg 2005; Huang et al. 2009), or CVaR (conditional value at risk) (Hatami et al. 2011; Kettunen et al. 2010; Kharrati et al. 2016); and they use the Montecarlo simulation to obtain the numerical series and validate the proposed model (An et al. 2010). On the other hand, optimization models are used to find the parameters that allow obtaining better forecasts such as the PSO model (particle swarm optimization) (Azevedo et al. 2010) or linear programming (Liu et al. 2008). These models search for the most efficient portfolio and validate it in the studied market; accordingly, the most appropriate hedging strategy is chosen.

Another trend that stands out in the first cluster is risk management in wind power generation. This issue has gained significant prominence in recent years due to concerns about the environmental impact and sustainability of conventional power plants (Garcia-Gonzalez 2008). By virtue of the above, many electricity systems have incorporated wind generation into their energy matrix, which generates new negotiations in the spot market. Currently, it is common to trade wind energy in competitive markets; however, market participants face risks due to the uncertainty of the wind (AlAshery and Qiao 2018). In order to mitigate these risks, there are studies that propose hedging strategies using artificial intelligence to generate electricity price scenarios (Janghorbani et al. 2014), ARIMA models to simulate the price of electricity and wind speed; (Hosseini-Firouz 2013) and models that use virtual auctions (virtual bidding) for the sale of wind energy (Xiao et al. 2022).

It is important to note that many researchers conclude that term and futures contracts with different prices should be incorporated to diversify the portfolio, and CVaR is the most commonly used risk measure in electricity market applications, as this approach employs the quantile of the profit distribution compared to other methodologies that seek the objective value of profits. The challenge for researchers is to model long-term spot prices and pricing forward contract. Regarding the topic of risks in wind energy, it is concluded that risk management strategy is directly dependent on revenue constraints; that is, the less severe the revenue constraint, the greater the economic benefits that can be obtained; therefore, the strategy should establish optimal revenue.

Cluster 2. Efficient management of energy resources.

In the second cluster there are works that propose alternatives for the management of energy resources found in the electrical network, since these sources are not always visible or can be dispatched (Kieny et al. 2009). Alternatives are presented such as a virtual power plant that forms an optimal coalition of resources incorporating bilateral and futures contracts with the stochastic programming approach (Shabanzadeh et al. 2016), or the incorporation of a microgrid together with the virtual power plant (Shen et al. 2016). Regarding microgrids, a configuration scheme is proposed for the optimization of microgrid resources (Luo et al. 2010). In this cluster, the interest in managing risk in the face of electricity shortages is highlighted. Proposals such as virtual power plants, microgrids, or smart grids can support the hedging strategy. However, virtual power plants are exposed to uncertainty since the variables of generation, consumption, price, and energy quantities have their limitations. In this sense, there are approaches that seek to reduce exposure to risk through the use of linear programming. Similarly, for microgrids, stochastic programming methods are employed for energy management; this is used to study the effect of demand response and risk management models.

Cluster 3. Application of financial instruments.

The third cluster determines the trend towards the application of financial instruments in the electricity markets, taking into account the characteristics of the price of electricity that differs from other commodities traded in the financial markets (Vehvilainen 2002). In this regard, there are studies on derivatives that propose a hedging strategy with the design of this instrument (Díaz Contreras et al. 2014) or use temperature derivatives to mitigate the risk of solar generation (Alao and Cuffe 2021). In addition, studies are reported that use Garch models to determine the value of the futures contract and to evaluate the coverage (Liu et al. 2010), or estimate the optimal levels of coverage in electricity portfolios that reduce volatility (Zanotti et al. 2010). On the other hand, time series models (regime switching models) are used to estimate the minimum variance and coverage ratios in the electricity futures market (Billio et al. 2018), or in a portfolio with crude oil and gas (Shrestha et al. 2018). The importance of validating the effectiveness of the hedge is highlighted by analyzing the variance and the value at risk, and the use of different models is recommended instead of just one to improve the hedge in different phases of the market. Finally, investment strategies are proposed including electricity futures contracts in a portfolio (Rendón-García et al. 2021); this way, the interest of the scientific community in the relationship between the financial and electricity markets is evidenced to maximize economic benefits. However, the greatest difficulty in designing hedging strategies arises from the dynamic nature of electricity prices, which exhibit high volatility. Therefore, financial market valuation models cannot be applied to electricity markets. Consequently, only electricity price forecasting models can be used, which has led to a widely studied and constantly evolving research field.

Cluster 4. Management of the demand for electricity.

The fourth cluster contains the works that analyze demand due to its influence on the electricity market; a greater demand response is essential to increase the efficiency of the electricity market (Bartusch et al. 2010). In this context, there are works that analyze the impact of the response to demand in the residential sector by monitoring demand through the Internet in real time (Blohm et al. 2021) or in the agents of the Finnish electricity market (Rautiainen et al. 2019) using a pricing model that shows that the risk of additional demand costs is significant. In order to mitigate financial risk, the electricity market has different hedging mechanisms such as bilateral, transmission, or difference contracts. In this regard, there are studies that propose bilateral contracting schemes based on forecast models (Gandelli et al. 2003) and a Monte Carlo simulation (Yucekaya 2022). In addition, there are studies that estimate the systematic risk of FTRs (financial transmission rights) (Baltaduonis et al. 2017). These instruments are used for hedging purposes for congestion charges. Finally, studies that incorporate difference contracts are reported to propose a planning model for the commercialization of energy considering the risk profile (Liu et al. 2019). It is important to highlight that the combination of futures contracts and FTRs can reduce the financial risk of electricity markets (Liu and Wu 2010), and the economic benefits of generating companies can be maximized by selecting an optimal balance between the spot and bilateral markets (Ramos et al. 2010). Similarly, through proper management of transmission rights contracts, risk coverage for congestion on electricity transmission lines can be achieved; in this case, contracts with different maturities are available to diversify the portfolio and reduce risk.

Cluster 5. Hedging tools in the electricity market.

Cluster five groups the works that analyze forward contracts and other derivatives such as the incentive that operators have to cover risk exposure regarding the quantity and price of electricity. In this sense, there are works that define, based on a CVaR model, the optimal portfolios of quantity and price of electricity for specific hours (Boroumand et al. 2015), or study the relationship between the quantity and price of electricity to propose a portfolio with forward contracts and options (Coulon et al. 2013; Oum et al. 2006), and futures contracts taking into account the variance and value at risk (Hanly et al. 2018). All of the above options improve coverage with the optimal allocation of contracts. There are also works that analyze how investment incentives are affected by introducing derivatives through a market equilibrium model (Willems and Morbee 2010) and examine the indirect effects of risk for energy and carbon futures contracts (Balcılar et al. 2016). Finally, there are works that propose models to reduce the existing operational risk in operations carried out through the internet and propose a coverage model that indicates the amount of energy to be purchased with a term contract (Rao et al. 2011). This is why there are different risk hedging tools and different ways to employ them. There are proposals that seek to optimize the amount of electricity, the number of contracts, and even the allocation of electricity for different hours. These studies have one of the main difficulties in common in designing a decision-making system that arises from simulating electricity prices. It is concluded that it is essential to know the variables that influence the price in order to simulate its behavior.

Cluster 6. Risk management in wind generation and coverage for fluctuations in weather variables.

Finally, cluster six contains the works that analyze risk management in the face of climate variations that affect the generation of renewable energies in any market structure (Shamsi and Cuffe 2022), and directly impact the price of electricity, producing high volatility. To mitigate this effect, weather derivatives have been incorporated into electricity market portfolios (Matsumoto and Yamada 2021), and an equilibrium pricing model has been proposed in a portfolio with multiple commodities (Lee and Oren 2009). Stochastic temperature models are also proposed to calculate the price of an option and determine its impact on the electricity market (Prabakaran et al. 2020). These derivatives are also used in the generation of wind (Benth et al. 2018) and solar (Matsumoto and Yamada 2019) power, which allows traders to cover themselves against the fall in low prices and the decrease in the production of power plants. On the other hand, there are works that use spread options for hedging purposes. In this sense, a modulated volatility model (Benth and Zdanowicz 2016) and a two-factor model with Levy processes (Mehrdoust and Noorani 2022) are proposed to determine the price of an electricity and gas spread option. Climate derivatives arise from the growing concern of many industries exposed to climate risk. Although they are the mechanism used to mitigate financial losses due to weather, it is difficult to have mechanisms for valuing the derivative due to climate uncertainty. Consequently, this topic has sparked the interest of different researchers and is considered a research field in full development.

5. Conclusions

This paper proposes a methodology to determine research trends on the topic of risk management in electricity markets. The results show that there are six dominant themes: (1) Risk management on financial assets and wind power generation—incorporating forward contracts to diversify the portfolio and using CVaR to measure risk. (2) Efficient management of energy resources—other models such as linear and stochastic programming are proposed to manage risk. (3) Application of financial instruments—it is difficult to have derivative and contract valuation models due to the complexity exhibited by the price series. (4) Management of the demand for electricity—using numerical simulation models, demand can be forecasted for risk management. (5) Hedging tools in the electricity market—risk can be managed through the optimization of the number of contracts, electricity, and its hourly allocation. (6) Risk management in wind generation and coverage for fluctuations in weather variables. This last topic has gained prominence thanks to the growth of renewable energies that are impacted by the climate; therefore, there is a high volatility in the price of electricity.

It is important to point out that most studies highlight the importance of risk management for decision-making systems in electricity markets. Therefore, it is essential to know the structure of the market and have electricity price models that forecast its future behavior; this way, the ideal tool for hedging purposes can be determined. In this sense, different instruments are proposed such as forward, bilateral, or futures contracts, and it is concluded that electricity futures can effectively manage risk only for certain periods of time when using hedging strategies that have been successful in financial and other commodity markets. Finally, the CVaR is widely used in studies, as it represents the risk evaluation index and is used to adjust the electricity procurement strategy in terms of purchase cost and risk level. Other methodologies focused on numerical simulation can improve the accuracy of models to quantify risk, which represents a topic for future research.

Author Contributions

This paper was written by A.A.L. and J.D.V. as indicated in the following items. The Conceptualization, A.A.L. and J.D.V.; methodology, A.A.L.; software, J.D.V.; validation, A.A.L. and J.D.V.; formal analysis, A.A.L.; investigation, A.A.L.; resources, A.A.L.; data curation, J.D.V.; writing—original draft preparation, A.A.L.; writing—review and editing, A.A.L.; visualization, J.D.V.; supervision, A.A.L.; project administration, A.A.L.; funding acquisition, A.A.L. and J.D.V. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

All results were obtained from the search string on www.scopus.com.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Alao, Olakunle, and Paul Cuffe. 2021. Towards a Blockchain Weather Derivative Financial Instrument for Hedging Volumetric Risks of Solar Power Producers. Paper presented at the 2021 IEEE Madrid PowerTech, Madrid, Spain, June 28–July 2. [Google Scholar]

- AlAshery, Mohamed Kareem, and Wei Qiao. 2018. Risk Management for Optimal Wind Power Bidding in an Electricity Market: A Comparative Study. Paper presented at the 2018 North American Power Symposium (NAPS), Fargo, ND, USA, September 9–11; pp. 1–6. [Google Scholar] [CrossRef]

- An, Xuena, Shaohua Zhang, and Xian Wang. 2010. CVaR-based decision-making model for interruptible load management. Paper presented at the 2010 Chinese Control and Decision Conference, Xuzhou, China, May 26–28; pp. 448–51. [Google Scholar] [CrossRef]

- Anderson, Edward J., Xinin Hu, and Donald Winchester. 2007. Forward contracts in electricity markets: The Australian experience. Energy Policy 35: 3089–103. [Google Scholar] [CrossRef]

- Azevedo, Filipe, Zita A. Vale, and Alberto A. Vale. 2003. Hedging using futures and options contracts in the electricity market. Renewable Energy and Power Quality Journal 1: 496–501. [Google Scholar] [CrossRef]

- Azevedo, Filipe, Zita A. Vale, Paulo B. Moura Oliveira, and H. M. Khodr. 2010. A long-term risk management tool for electricity markets using swarm intelligence. Electric Power Systems Research 80: 380–89. [Google Scholar] [CrossRef]

- Balcilar, Mehmet, Rıza Demirer, Shawkat Hammoudeh, and Duc Khuong Nguyen. 2016. Risk spillovers across the energy and carbon markets, and hedging strategies for carbon risk. Energy Economics 54: 159–72. [Google Scholar] [CrossRef]

- Baltaduonis, Rimvydas, Samuel Bonarnd, John Carnes, and Erin Mastrangelo. 2017. Risk and abnormal returns in markets for congestion revenue rights. Journal of Energy Markets. Available online: https://www.risk.net/node/5329906 (accessed on 16 March 2023). [CrossRef]

- Bartusch, Cajsa, Mikael Larsson, Fredrik Wallin, and Lars Wester. 2010. Potential of Hourly Settlements in the Residential Sector of the Swedish Electricity Market—Estimations of Risk Reduction and Economic Result. International Journal of Green Energy 7: 224–40. [Google Scholar] [CrossRef]

- Benth, Fred Espen, and Hanna Zdanowicz. 2016. Pricing and hedging of energy spread options and volatility modulated volterra processes. International Journal of Theoretical and Applied Finance 19: 1650002. [Google Scholar] [CrossRef]

- Benth, Fred Espen, Luca Di Persio, and Silvia Lavagnini. 2018. Stochastic Modeling of Wind Derivatives in Energy Markets. Risks 6: 56. [Google Scholar] [CrossRef]

- Bessembinder, Hendrik, and Michael L. Lemmon. 2002. Equilibrium Pricing and Optimal Hedging in Electricity Forward Markets. The Journal of Finance 57: 1347–82. [Google Scholar] [CrossRef]

- Billio, Monica, Roberto Casarin, and Anthony Osuntuyi. 2018. Markov switching GARCH models for Bayesian hedging on energy futures markets. Energy Economics 70: 545–62. [Google Scholar] [CrossRef]

- Bjorgan, R., Chen-Ching Liu, and J. Lawarree. 1999. Financial risk management in a competitive electricity market. IEEE Transactions on Power Systems 14: 1285–91. [Google Scholar]

- Blohm, Andrew, Jaden Crawford, and Steven A. Gabriel. 2021. Demand Response as a Real-Time, Physical Hedge for Retail Electricity Providers: The Electric Reliability Council of Texas Market Case Study. Energies 14: 808. [Google Scholar] [CrossRef]

- Blondel, Vincent D., Jean-Loup Guillaume, Renaud Lambiotte, and Etienne Lefebvre. 2008. Fast unfolding of communities in large networks. Journal of Statistical Mechanics: Theory and Experiment 2008: P10008. [Google Scholar] [CrossRef]

- Boroumand, Raphaël Homayoun, Stéphane Goutte, Simon Porcher, and Thomas Porcher. 2015. Hedging strategies in energy markets: The case of electricity retailers. Energy Economics 51: 503–9. [Google Scholar] [CrossRef]

- Botterud, Audun, Zhi Zhou, Jianhui Wang, Ricardo J. Bessa, Hrvoje Keko, Jean Sumaili, and Vladimiro Miranda. 2012. Wind Power Trading Under Uncertainty in LMP Markets. IEEE Transactions on Power Systems 27: 894. [Google Scholar] [CrossRef]

- Burger, Markus, Bernhard Klar, Alfred Müller, and Gero Schindlmayr. 2004. A spot market model for pricing derivatives in electricity markets. Quantitative Finance 4: 109–22. [Google Scholar] [CrossRef]

- Carmona, René, and Valdo Durrleman. 2003. Pricing and Hedging Spread Options. SIAM Review 45: 627. [Google Scholar] [CrossRef]

- Coulon, Michael, Warren B. Powell, and Ronnie Sircar. 2013. A model for hedging load and price risk in the Texas electricity market. Energy Economics 40: 976–88. [Google Scholar] [CrossRef]

- Das, D., and Bruce F. Wollenberg. 2005. Risk assessment of generators bidding in day-ahead market. IEEE Transactions on Power Systems 20: 416–24. [Google Scholar] [CrossRef]

- Díaz Contreras, Jhon Alexis, Gloría Inés Macías Villalba, and Edgar Luna González. 2014. Estrategia de cobertura con productos derivados para el mercado energético colombiano. Estudios Gerenciales 30: 55–64. [Google Scholar] [CrossRef]

- Gandelli, A., Stefano Marchi, and Riccardo E. Zich. 2003. Hedging through multi-resolution analysis methods in the wholesale electricity market. Paper presented at the International Conference on Financial Engineering and Applications, Banff, AB, Canada, July 2–4; pp. 15–23. [Google Scholar]

- Garcia-Gonzalez, Javier. 2008. Hedging strategies for wind renewable generation in electricity markets. Paper presented at the 2008 IEEE Power and Energy Society General Meeting—Conversion and Delivery of Electrical Energy in the 21st Century, Pittsburgh, PA, USA, July 20–24; pp. 1–6. [Google Scholar] [CrossRef]

- Hanly, Jim, Lucia Morales, and Damien Cassells. 2018. The efficacy of financial futures as a hedging tool in electricity markets. International Journal of Finance & Economics 23: 29–40. [Google Scholar] [CrossRef]

- Hatami, Alireza, Hossein Seifi, and Mohammad Kazem Sheikh-El-Eslami. 2011. A stochastic-based decision-making framework for an electricity retailer: Time-of-use pricing and electricity portfolio optimization. IEEE Transactions on Power Systems 26: 1808–16. [Google Scholar] [CrossRef]

- Hosseini-Firouz, Mansour. 2013. Optimal offering strategy considering the risk management for wind power producers in electricity market. International Journal of Electrical Power & Energy Systems 49: 359–68. [Google Scholar] [CrossRef]

- Huang, Jie, Yusheng Xue, Zhao Yang Dong, and Kit Po Wong. 2012. An efficient probabilistic assessment method for electricity market risk management. IEEE Transactions on Power Systems 27: 1485–93. [Google Scholar] [CrossRef]

- Huang, Ren-Hui, Ji Zhang, Li-Zi Zhang, and Zhao-Li Li. 2009. Price risk forewarning of electricity market based on GARCH and VaR theory. Zhongguo Dianji Gongcheng Xuebao/Proceedings of the Chinese Society of Electrical Engineering 29: 85–91. [Google Scholar]

- Jain, Arvind Kumar, and S. C. Srivastava. 2009. Strategic Bidding and Risk Assessment Using Genetic Algorithm in Electricity Markets. International Journal of Emerging Electric Power Systems 10. [Google Scholar] [CrossRef]

- Janghorbani, Mohammadreza, Seyed Mohammad Shariatmadar, Vahid Amir, Mohammad Ghanbari Jolfaei, and Ali Madanimohammadi. 2014. Risk management strategies for a wind power producer in electricity markets. Indian Journal of Science and Technology 7: 1107–13. [Google Scholar] [CrossRef]

- Kettunen, Janne, Ahti Salo, and Derek W. Bunn. 2010. Optimization of electricity retailer’s contract portfolio subject to risk preferences. IEEE Transactions on Power Systems 25: 117–28. [Google Scholar] [CrossRef]

- Kharrati, Saeed, Mostafa Kazemi, and Mehdi Ehsan. 2016. Equilibria in the competitive retail electricity market considering uncertainty and risk management. Energy 106: 315–28. [Google Scholar] [CrossRef]

- Kieny, Christophe, Boris Berseneff, Nouredine Hadjsaid, Yvon Besanger, and Joseph Maire. 2009. On the concept and the interest of virtual power plant: Some results from the European project Fenix. Paper presented at the 2009 IEEE Power & Energy Society General Meeting, Calgary, AB, Canada, July 26–30; pp. 1–6. [Google Scholar] [CrossRef]

- Lee, Yongheon, and Shmuel S. Oren. 2009. An equilibrium pricing model for weather derivatives in a multi-commodity setting. Energy Economics 31: 702–13. [Google Scholar] [CrossRef]

- Li, Jiang. 2013. The Empirical Study of Electricity Market’s Financial Risk Assessment Based on CVaR. Advanced Materials Research 805–6: 1103–6. [Google Scholar] [CrossRef]

- Liu, Hantao, Xingying Chen, and Jun Xie. 2019. Optimal Bidding Strategy for Electricity Sales Company Considering Contract for Difference and Risk. Paper presented at the 2019 IEEE 3rd Conference on Energy Internet and Energy System Integration (EI2), Changsha, China, November 8–10; pp. 2155–60. [Google Scholar] [CrossRef]

- Liu, Min, and Felix F. Wu. 2008. Risk management in a competitive electricity market. In Analytical Methods for Energy Diversity and Security. Amsterdam: Elsevier, pp. 247–62. [Google Scholar] [CrossRef]

- Liu, Min, and Felix Wu. 2010. Effect of Financial Hedging in Portfolio Selection in Electricity Markets. HKIE Transactions Hong Kong Institution of Engineers 17: 34–40. [Google Scholar] [CrossRef]

- Liu, Min, F. F. Wu, and Yixin Ni. 2006. A survey on risk management in electricity markets. Paper presented at the 2006 IEEE Power Engineering Society General Meeting, PES, Montreal, QC, Canada, June 18–22. [Google Scholar]

- Liu, Ruihua, Junyong Liu, Mai He, Minkun Wang, and Ye Chen. 2008. Power purchasing portfolio optimization and risk measurement based on semi-absolute deviation. Dianli Xitong Zidonghua/Automation of Electric Power Systems 32: 9–13. [Google Scholar]

- Liu, S. D., J. B. Jian, and Y. Y. Wang. 2010. Optimal dynamic hedging of electricity futures based on Copula-GARCH models. Paper presented at the 2010 IEEE International Conference on Industrial Engineering and Engineering Management, Macao, China, December 7–10; pp. 2498–502. [Google Scholar] [CrossRef]

- Luo, Y., B. Wang, X. Liang, and S. Xie. 2010. Configuration optimization of non-renewable energy distributed generation capacity. Dianli Zidonghua Shebei/Electric Power Automation Equipment 30: 28–36. [Google Scholar]

- Matsumoto, Takuji, and Yuji Yamada. 2019. Cross Hedging Using Prediction Error Weather Derivatives for Loss of Solar Output Prediction Errors in Electricity Market. Asia-Pacific Financial Markets 26: 211–27. [Google Scholar] [CrossRef]

- Matsumoto, Takuji, and Yuji Yamada. 2021. Simultaneous hedging strategy for price and volume risks in electricity businesses using energy and weather derivatives1. Energy Economics 95: 105101. [Google Scholar] [CrossRef]

- Mehrdoust, Farshid, and Idin Noorani. 2022. Valuation of Spark-Spread Option Written on Electricity and Gas Forward Contracts Under Two-Factor Models with Non-Gaussian Lévy Processes. Computational Economics 61: 807–53. [Google Scholar] [CrossRef]

- Mensi, Walid, Beljid Makram, Boubaker Adel, and Shunsuke Managi. 2013. Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold. Economic Modelling 32: 15–22. [Google Scholar] [CrossRef]

- Oum, Yumi, Shmuel Oren, and Shijie Deng. 2006. Hedging quantity risks with standard power options in a competitive wholesale electricity market. Naval Research Logistics (NRL) 53: 697–712. [Google Scholar] [CrossRef]

- Prabakaran, Sellamuthu, Isabel C. Garcia, and Jose U. Mora. 2020. A temperature stochastic model for option pricing and its impacts on the electricity market. Economic Analysis and Policy 68: 58–77. [Google Scholar] [CrossRef]

- Ramos, Luís, Jorge de Sousa, Tânia Silva, Rui Jerónimo, and José Allen Lima. 2010. A risk management model for trading electricity in the spot market and through bilateral contracts. Paper presented at the 2010 7th International Conference on the European Energy Market, Madrid, Spain, June 23–25; pp. 1–7. [Google Scholar] [CrossRef]

- Rao, Lei, Xue Liu, Le Xie, and Zhan Pang. 2011. Hedging Against Uncertainty: A Tale of Internet Data Center Operations Under Smart Grid Environment. IEEE Transactions on Smart Grid 2: 555–63. [Google Scholar] [CrossRef]

- Rautiainen, Antti, Pertti Järventausta, Heikki Rantamäki, and Heidi Uimonen. 2019. Impact of Demand Response on the Risk Profile of Electricity Retailers in North-European Electricity Market. Paper presented at the 2019 16th International Conference on the European Energy Market (EEM), Ljubljana, Slovenia, September 18–20; pp. 1–6. [Google Scholar] [CrossRef]

- Rendón-García, Juan Fernando, Alfredo Trespalacios, Hernan Dario Villada-Medina, and Juan Gabriel Vanegas-López. 2021. Inclusión de futuros de energía eléctrica en portafolios de acciones. Recta 22: 35–50. [Google Scholar] [CrossRef]

- Shabanzadeh, Morteza, Mohammad-Kazem Sheikh-El-Eslami, and Mahmoud-Reza Haghifam. 2016. A medium-term coalition-forming model of heterogeneous DERs for a commercial virtual power plant. Applied Energy 169: 663–81. [Google Scholar] [CrossRef]

- Shamsi, Mahdieh, and Paul Cuffe. 2022. Using Binary Prediction Markets as Hedging Instruments: Strategies for Renewable Generators. IEEE Transactions on Sustainable Energy 13: 1160–63. [Google Scholar] [CrossRef]

- Shen, Jingshuang, Chuanwen Jiang, Yangyang Liu, and Xu Wang. 2016. A Microgrid Energy Management System and Risk Management Under an Electricity Market Environment. IEEE Access 4: 2349–56. [Google Scholar] [CrossRef]

- Shrestha, Keshab, Ravichandran Subramaniam, Yessy Peranginangin, and Sheena Sara Suresh Philip. 2018. Quantile hedge ratio for energy markets. Energy Economics 71: 253–72. [Google Scholar] [CrossRef]

- Vehvilainen, Iivo. 2002. Basics of electricity derivative pricing in competitive markets. Applied Mathematical Finance 9: 45–60. [Google Scholar] [CrossRef]

- Willems, Bert, and Joris Morbee. 2010. Market completeness: How options affect hedging and investments in the electricity sector. Energy Economics 32: 786–95. [Google Scholar] [CrossRef]

- Wolak, Frank A. 2000. An Empirical Analysis of the Impact of Hedge Contracts on Bidding Behavior in a Competitive Electricity Market. International Economic Journal 14: 1–39. [Google Scholar] [CrossRef]

- Wu, Yuan-Kang. 2008. Risk assessment of trading price mechanisms in competitive electricity markets. Paper presented at the 2008 IEEE Power and Energy Society General Meeting—Conversion and Delivery of Electrical Energy in the 21st Century, Pittsburgh, PA, USA, July 20–24; pp. 1–6. [Google Scholar] [CrossRef]

- Xiao, Dongliang, Mohamed Kareem AlAshery, and Wei Qiao. 2022. Optimal Price-maker Trading Strategy of Wind Power Producer Using Virtual Bidding. Journal of Modern Power Systems and Clean Energy 10: 766–78. [Google Scholar] [CrossRef]

- Yucekaya, A. 2022. Electricity trading for coal-fired power plants in Turkish power market considering uncertainty in spot, derivatives and bilateral contract market. Renewable and Sustainable Energy Reviews 159: 112189. [Google Scholar] [CrossRef]

- Zanotti, Giovanna, Giampaolo Gabbi, and Manuela Geranio. 2010. Hedging with futures: Efficacy of GARCH correlation models to European electricity markets. Journal of International Financial Markets, Institutions and Money 20: 135–48. [Google Scholar] [CrossRef]

- Zhang, Qin, and Xifan Wang. 2009. Hedge contract characterization and risk-constrained electricity procurement. IEEE Transactions on Power Systems 24: 1547–58. [Google Scholar] [CrossRef]

- Zhao, Jun Hua, Zhao Yang Dong, Peter Lindsay, and Kit Po Wong. 2009. Flexible Transmission Expansion Planning with Uncertainties in an Electricity Market. IEEE Transactions on Power Systems 24: 479–88. [Google Scholar] [CrossRef]

- Zhou, Ming, Yan-Li Nie, Geng-Yin Li, and Yi-Xin Ni. 2006. Long-term electricity purchasing scheme and risk assessment in power markets. Zhongguo Dianji Gongcheng Xuebao/Proceedings of the Chinese Society of Electrical Engineering 26: 116–22. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).