Machine Learning Algorithm for Mid-Term Projection of the EU Member States’ Indebtedness

Abstract

1. Introduction

2. A Review of the Literature Related to the Topic of Government Indebtedness

3. Description of Data and Research Methodology

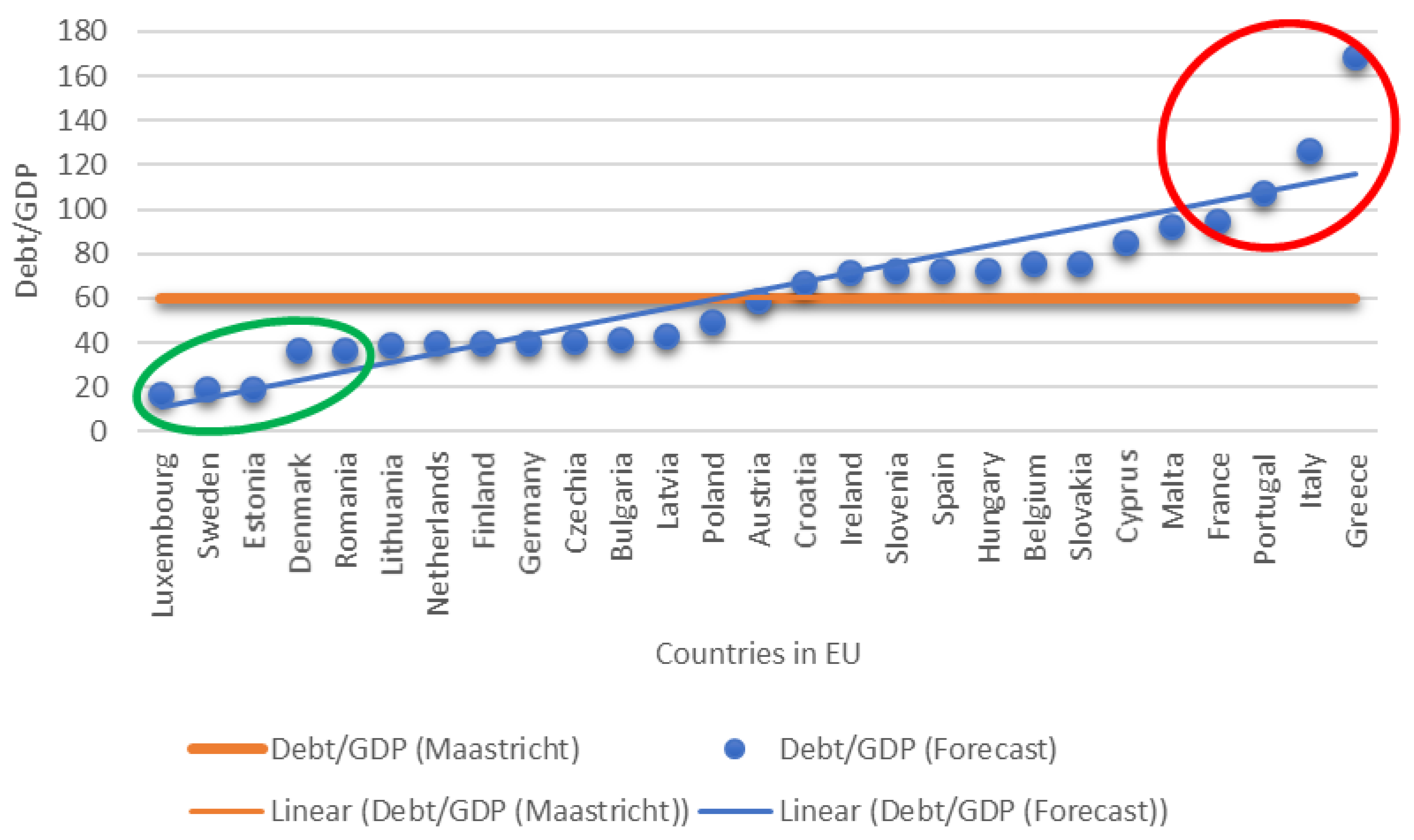

3.1. Description of Data

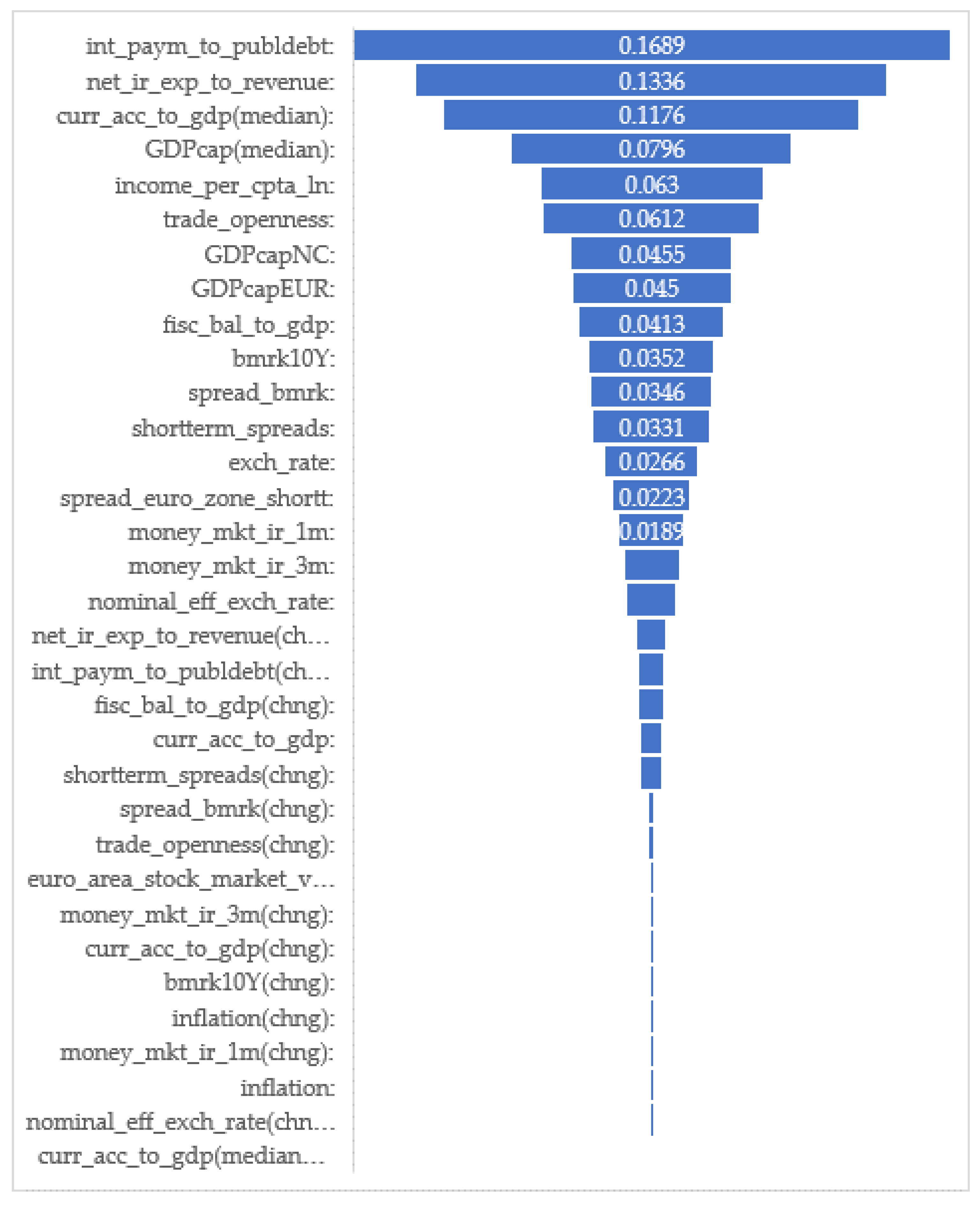

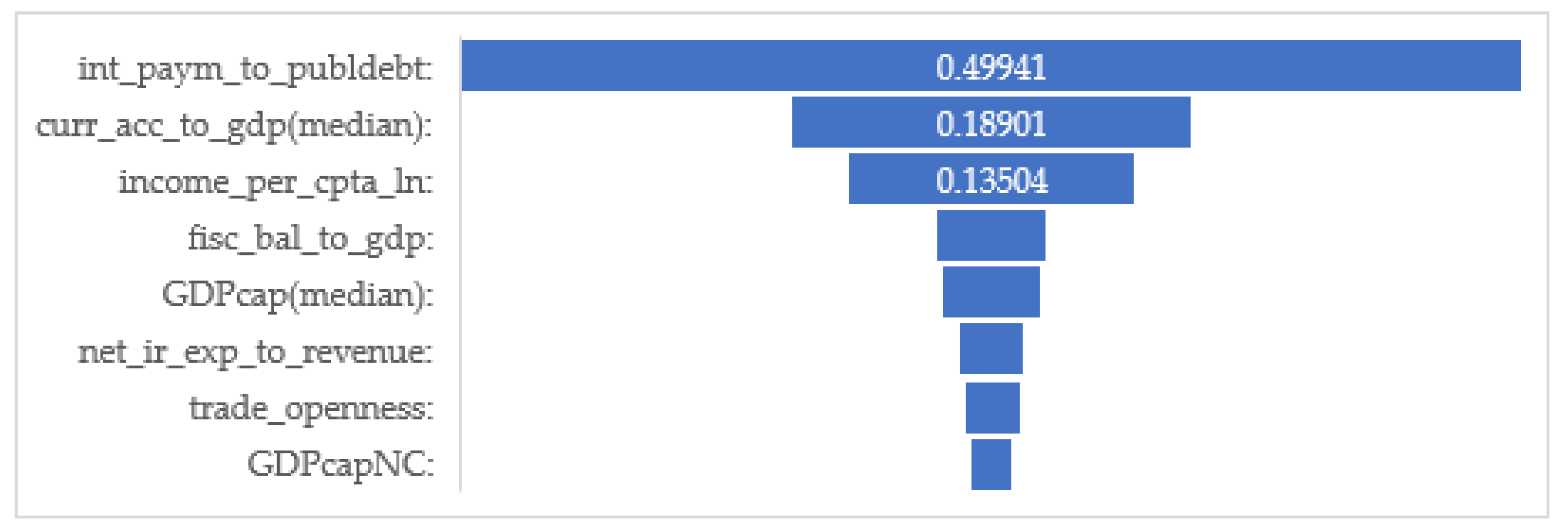

- Macroeconomic: We used two measures of nominal GDP per capita (in national currencies and in EUR) to assess the effect of changes in economic activity. The structure of the economy (Roleders et al. 2022) and its susceptibility to external shocks (Laktionova et al. 2019) is measured by means of the trade openness indicator. In macroeconomic terms, the ability to repay existing government debt and the need for new debt largely depends on the current account balance-to-GDP ratio and the gross external debt-to-GDP ratio, respectively.

- Fiscal: In this group of factors, of primary importance is the fiscal balance-to-GDP ratio indicator, as the budget balance is the main driver of debt changes (Em et al. 2022). The importance in the burden of interest payments in relation to the size of the economy and the potential capacity of the country to service its obligations are tested using the interest payments on the public debt-to-GDP ratio indicator. On the other hand, we can measure the actual current debt burden for the budget using the Net interest-payments-to-government-revenue ratio.

- Money and Bond Market rates: In order to measure the effect of changes in the monetary policy of central banks and interbank liquidity (Prodanov et al. 2022a), we tested (as a proxy) the short-term interest rates (Euribor, domestic money market rates on different time bases—day−day, monthly, etc.). Another important factor is the market’s assessment of the risk exposure of individual countries’ debt securities. The 10-year maturity for each country compared with 10-year benchmark indicators is revealed by the spread of the long-term interest rate for convergence purposes. Another aspect that affects monetary policy is the rate of inflation, measured by the inflation rates (HICP) indicator.

- Global: Global factors capture changes in investors’ risk aversion and investment expectations. For this purpose, we used Euro area stock market volatility (monthly average of EURO STOXX 50® volatility).

- Convergence: The degree of real convergence of the countries in the direction of raising the standard of living is considered an indicator (proxy) related to country-specific risks, credit ratings, and the country’s membership in a club of countries with similar parameters. For this purpose, we included the indicators of income per capita (in natural logarithm form), median values of nominal GDP per capita, and current-account-balance-to-GDP ratio for each country.

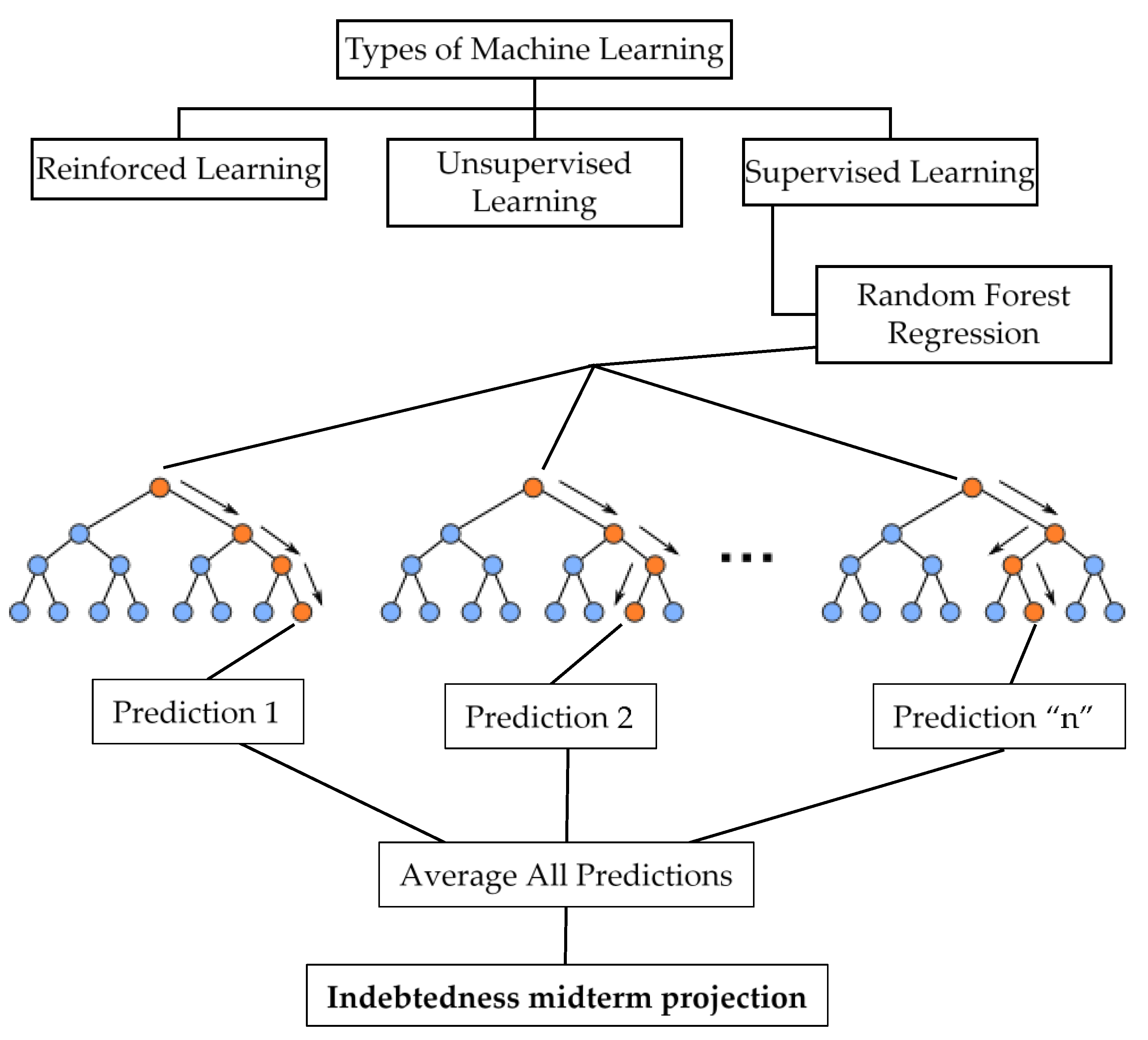

3.2. Description of Research Methodology

4. Empirical Results from Model Approbation

“#Final fit of random forest based on optimized params and cross validation on entire sample with 33 factors (ver. 1.0)model = RandomForestRegressor (n_estimators = 782, min_samples_split = 2, min_samples_leaf = 1, max_features = ‘sqrt’, max_depth = 20, bootstrap = False, random_state = 1)”

“#Final fit of random forest based on optimized params and cross validation on entire sample with most significant eight factors (ver. 2.0)model = RandomForestRegressor (n_estimators = 68, min_samples_split = 5, min_samples_leaf = 2, max_features = ‘auto’, max_depth = 10, bootstrap = True, random_state = 1)”

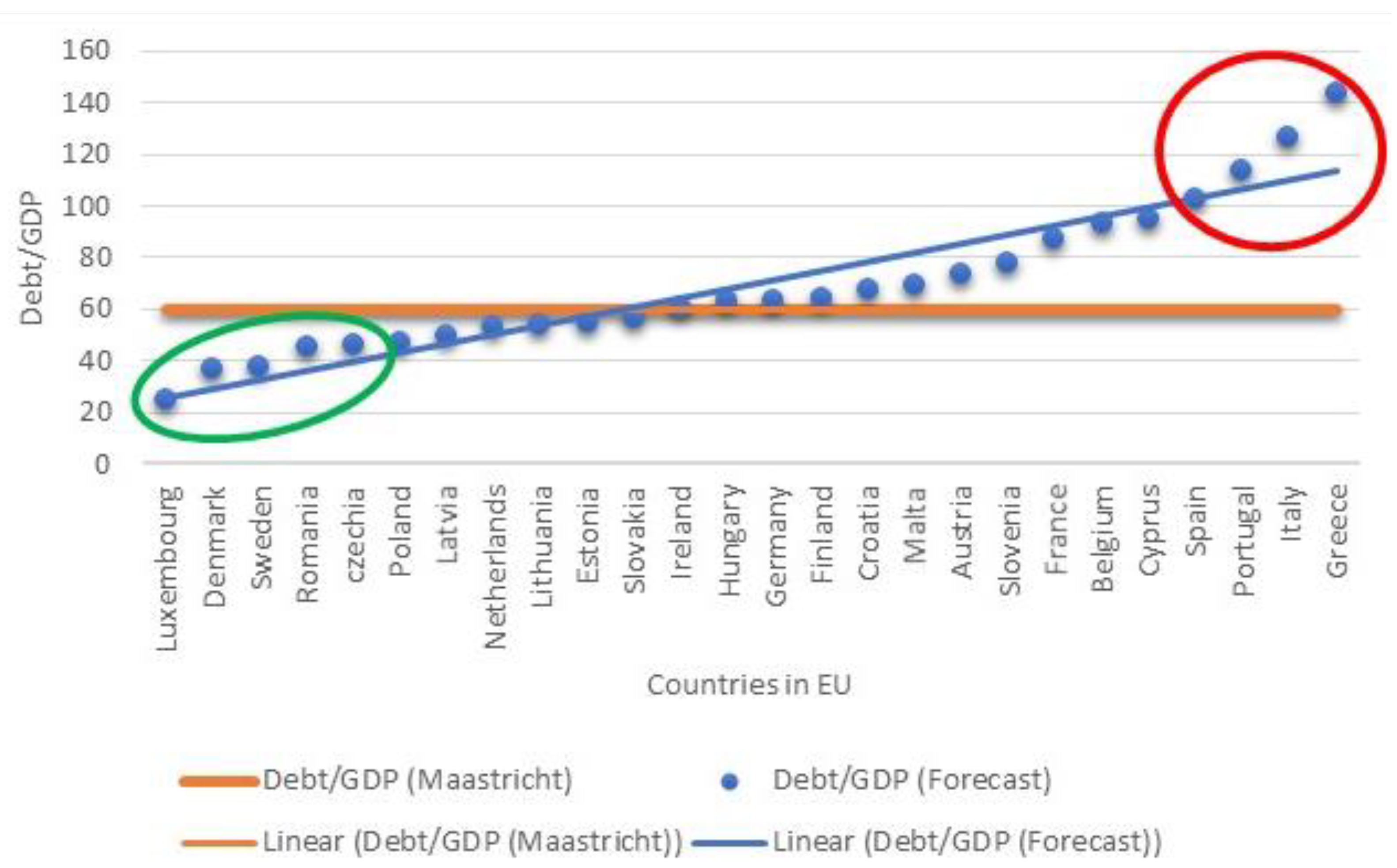

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Albonico, Alice, and Patrizio Tirelli. 2020. Financial crises and sudden stops: Was the European monetary union crisis. Economic Modelling 93: 13–26. Available online: https://bit.ly/3msydMA (accessed on 8 September 2022). [CrossRef]

- Alexopoulou, Ioana, Irina Bunda, and Annalisa Ferrando. 2010. Determinants of government bond spreads in New EU countries. Eastern European Economics 48: 5–37. [Google Scholar] [CrossRef]

- Ao, Yile, Hongqi Li, Liping Zhu, Sikandar Ali, and Zhongguo Yang. 2019. The linear random forest algorithm and its advantages in machine learning assisted logging regression modeling. Journal of Petroleum Science and Engineering 174: 776–89. [Google Scholar] [CrossRef]

- Baum, Anja, Cristina Checherita-Westphal, and Philipp Rother. 2013. Debt and growth: New evidence for the euro area. Journal of International Money and Finance, 809–21. [Google Scholar] [CrossRef]

- Bezgin, Kostiantyn, Andrey Zahariev, Larysa Shaulska, Olha Doronina, Natela Tsiklashvili, and Natalia Wasilewska. 2022. Coevolution of education and business: Adaptive interaction. International Journal of Global Environmental Issues 21: 259–75. [Google Scholar] [CrossRef]

- Caner, Mehmet, Qingliang Fan, and Thomas Grennes. 2021. Partners in debt: An endogenous non-linear analysis of the effects of the effects of public and private debt on growth. International Review of Economics and Finance 76: 694–711. [Google Scholar] [CrossRef]

- De Bruyckere, Valerie, Maria Gerhardt, Glenn Schepens, and Rudi Vander Vennet. 2013. Bank/sovereign risk spillovers in the European debt crisis. Journal of Banking & Finance 37: 4793–809. [Google Scholar]

- Dudek, Grzegorz. 2022. A Comprehensive Study of Random Forest for Short-Term Load Forecasting. Energies 15: 7547. [Google Scholar] [CrossRef]

- Eichinger, Frank, and Moritz Mayer. 2022. Predicting Salaries with Random-Forest Regression. In Machine Learning and Data Analytics for Solving Business Problems, Methods, Applications, and Case Studies. Available online: https://www.researchgate.net/publication/366340005 (accessed on 5 January 2023).

- Em, Olga, Georgi Georgiev, Sergey Radukanov, and Mariana Petrova. 2022. Assessing the Market Risk on the Government Debt of Kazakhstan and Bulgaria in Conditions of Turbulence. Risks 10: 93. [Google Scholar] [CrossRef]

- Eurostat. 2023. Third Quarter of 2022 Government Debt down to 93.0% of GDP in Euro Area Down to 85.1% of GDP in EU. January 23. Available online: https://ec.europa.eu/eurostat/documents/2995521/15725185/2-23012023-AP-EN.pdf/ (accessed on 24 January 2023).

- Ganesh, Narayanan, Paras Jain, Amitava Choudhury, Prasun Dutta, Kanak Kalita, and Paolo Barsocchi. 2021. Random Forest Regression-Based Machine Learning Model for Accurate Estimation of Fluid Flow in Curved Pipes. Processes 9: 2095. [Google Scholar] [CrossRef]

- Geldiev, Ertan Mustafa, Nayden Valkov Nenkov, and Mariana Mateeva Petrova. 2018. Exercise of Machine Learning Using Some Python Tools and Techniques. Paper presented at CBU International Conference Proceedings 2018: Innovations in Science and Education, Prague, Czech Republic, March 21–23; pp. 1062–70. [Google Scholar] [CrossRef]

- Globan, Tomislav, and Marina Matošec. 2016. Public debt-to-GDP ratio in new EU member states: Cut the numerator or increase the denominator. Romanian Journal of Economic Forecasting 19: 57–72. [Google Scholar]

- Hauptmeier, Sebastian, and Christophe Kamps. 2022. Debt policies in the aftermath of COVID-19—The SGP’s debt. European Journal of Political Economy 75: 102187. [Google Scholar] [CrossRef] [PubMed]

- He, Lingjun, Richard A. Levine, Juanjuan Fan, Joshua Beemer, and Jeanne Stronach. 2018. Random Forest as a Predictive Analytics Alternative to Regression in Institutional Research. Practical Assessment, Research & Evaluation 23: 1. [Google Scholar] [CrossRef]

- Heppke-Falk, Kirsten, and Felix P. Hüfner. 2004. Expected Budget Deficits and Interest Rate Swap Spreads-Evidence for France, Germany and Italy. Frankfurt: Deutsche Bundesbank. [Google Scholar]

- Huyugüzel Kışla, Gül, Y. Gülnur Muradoğlu, and A. Özlem Önder. 2022. Spillovers from one country’s sovereign debt to CDS (credit default swap) spreads of others during the European crisis: A spatial approach. Journal of Asset Management 23: 277–96. [Google Scholar] [CrossRef]

- Insee. 2021. Convergence Criteria (Maastricht Treaty). January 28. Available online: http://bit.ly/3ZHMOSz (accessed on 15 September 2022).

- Kharwal, Aman. 2022. Explained Variance in Machine Learning. Available online: https://thecleverprogrammer.com/2021/06/25/explained-variance-in-machine-learning/ (accessed on 25 June 2021).

- Kraft, Holger, and Mogens Steffensen. 2007. Bankruptcy, counterparty risk, and contagion. Review of Finance 11: 209–52. [Google Scholar] [CrossRef]

- Laktionova, Oleksandra, Oleksandr Dobrovolskyi, Tatyana Sergeevna Karpova, and Andrey Zahariev. 2019. Cost Efficiency of Applying Trade Finance for Agricultural Supply Chains. Management Theory and Studies for Rural Business and Infrastructure Development 41: 62–73. [Google Scholar] [CrossRef]

- Mackiewicz-Łyziak, Joanna, and Tomasz Łyziak. 2019. A new test for fiscal sustainability with endogenous sovereign bond yields: Evidence for EU economies. Economic Modelling 82: 136–51. [Google Scholar] [CrossRef]

- Maltritz, Dominik, and Sebastian Wüste. 2014. Determinants of budget deficits in Europe: The role and relations of fiscal. Economic Modelling 48: 222–36. [Google Scholar] [CrossRef]

- Ostrihon, Filip. 2020. Exploring macroeconomic imbalances through EU Alert. European Journal of Political Economy 75: 102188. [Google Scholar] [CrossRef]

- Ouedraogo, Issoufou, Pierre Defourny, and Marnik Vanclooster. 2019. Application of random forest regression and comparison of its performance to multiple linear regression in modeling groundwater nitrate concentration at the African continent scale. Hydrogeology Journal 27: 1081–98. [Google Scholar] [CrossRef]

- Posta, Pompeo Della. 2021. Government size and speculative attacks on public debt. International Review of Economics and Finance 72: 79–89. [Google Scholar] [CrossRef]

- Prodanov, Stoyan, and Lyudmil Naydenov. 2020. Theoretical, qualitative and quantitative aspects of municipal fiscal autonomy in Bulgaria. Ikonomicheski Izsledvania 29: 126–50. Available online: https://bit.ly/3rmXlTL (accessed on 10 June 2021).

- Prodanov, Stoyan, Orlin Yaprakov, and Silvia Zarkova. 2022a. CAMEL evaluation of the banks in Bulgaria. Economic Alternatives 2022: 201–19. [Google Scholar] [CrossRef]

- Prodanov, Stoyan, Petko Angelov, and Silvia Zarkova. 2022b. Real Estate in Bulgaria from the global financial crisi to the COVID-19 crisis-effects of macroprudential policy: Evidence from Bulgaria. Paper presented at 87th International Scientific Conference on Economic and Social Development—“Economics, Management, Finance and Banking”, Svishtov, Bulgaria, September 28–30; pp. 162–70. [Google Scholar]

- Roleders, Viktoriia, Tetyana Oriekhova, and Galina Zaharieva. 2022. Circular Economy as a Model of Achieving Sustainable Development. Problemy Ekorozwoju—Problems of Sustainable Development 17: 178–85. [Google Scholar] [CrossRef]

- Sakuragawaa, Masaya, and Yukie Sakuragawa. 2020. Government fiscal projection and debt sustainability. Japan & The World Economy 54: 101010. [Google Scholar] [CrossRef]

- TIBCO. 2023. What Is a Random Forest? Available online: https://www.tibco.com/reference-center/what-is-a-random-forest (accessed on 10 December 2022).

- Tyralis, Hristos, Georgia Papacharalampous, and Andreas Langousis. 2019. A Brief Review of Random Forests for Water Scientists and Practitioners and Their Recent History in Water Resources. Water 11: 910. [Google Scholar] [CrossRef]

- Zahariev, Andrey, Anelia Radulova, Aleksandrina Aleksandrova, and Mariana Petrova. 2021. Fiscal sustainability and fiscal risk in the EU: Forecasts and challenges in terms of COVID-19. Entrepreneurship and Sustainability Issues 8: 618–32. [Google Scholar] [CrossRef] [PubMed]

- Zahariev, Andrey, Mikhail Zveryakov, Stoyan Prodanov, Galina Zaharieva, Petko Angelov, Silvia Zarkova, and Mariana Petrova. 2020. Debt management evaluation through support vector machines: On the example of Italy and Greece. Entrepreneurship and Sustainability Issues 7: 2382–93. [Google Scholar] [CrossRef]

- Zahariev, Andrey, Petko Angelov, and Silvia Zarkova. 2022. Estimation of Bank Profitability Using Vector Error Correction Model and Support Vector Regression. Economic Alternatives 2022: 157–70. [Google Scholar] [CrossRef]

- Zaharieva, Galina, Onnik Tarakchiyan, and Andrey Zahariev. 2022. Market capitalization factors of the Bulgarian pharmaceutical sector in pandemic environment. Business Management XXXII: 35–51. Available online: https://www.scopus.com/record/display.uri?eid=2-s2.0-85144992057&origin=resultslist (accessed on 10 January 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Statistics | Values | |

|---|---|---|

| Ver. 1.0 (33 Indicators) | Ver. 2.0 (8 Indicators) | |

| Mean Absolute Error (MAE): | 0.973715 | 1.820823 |

| Mean Squared Error (MSE): | 3.138634 | 10.294671 |

| Root Mean Squared Error (RMSE): | 1.771619 | 3.208531 |

| Explained Variance Score: | 0.997546 | 0.992231 |

| Max Error: | 28.10818 | 27.173953 |

| Median Absolute Error: | 0.563978 | 1.026739 |

| R2: | 0.997545 ** | 0.992228 * |

| Mean explained variance: | 0.998 (0.000) ** | 0.993 (0.000) * |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zarkova, S.; Kostov, D.; Angelov, P.; Pavlov, T.; Zahariev, A. Machine Learning Algorithm for Mid-Term Projection of the EU Member States’ Indebtedness. Risks 2023, 11, 71. https://doi.org/10.3390/risks11040071

Zarkova S, Kostov D, Angelov P, Pavlov T, Zahariev A. Machine Learning Algorithm for Mid-Term Projection of the EU Member States’ Indebtedness. Risks. 2023; 11(4):71. https://doi.org/10.3390/risks11040071

Chicago/Turabian StyleZarkova, Silvia, Dimitar Kostov, Petko Angelov, Tsvetan Pavlov, and Andrey Zahariev. 2023. "Machine Learning Algorithm for Mid-Term Projection of the EU Member States’ Indebtedness" Risks 11, no. 4: 71. https://doi.org/10.3390/risks11040071

APA StyleZarkova, S., Kostov, D., Angelov, P., Pavlov, T., & Zahariev, A. (2023). Machine Learning Algorithm for Mid-Term Projection of the EU Member States’ Indebtedness. Risks, 11(4), 71. https://doi.org/10.3390/risks11040071