1. Introduction

The objective of this study is to identify possible directions of the process of transforming the system of indirect taxation on export transactions in the Russian Federation based on the analysis of legal precedents.

The objective of this article necessitated finding the solutions for the following scientific problems:

Finding the inter-relationship between the trends of development of the national economy and the emergence of risks of tax evasion in foreign trade transactions.

Analysis of main schemes used by the taxpayers for tax evasion; factors and conditions defining the indicators of legitimate tax minimization.

Development of proposals for improvement of the VAT taxation mechanism of export operations.

Our analysis of a sizeable volume of available statistical data on foreign trade confirms the existence of significant and sustainably positive impacts made by foreign trade on economic growth and incomes. The study (

Frankel and Romer 1999) identified the following channels through which trade influences economic growth: specialization based on comparative advantages and spreading of technologies via investment activity. (

Lederman and Maloney 2003) note that, as a rule, growth rates tend to be higher in countries with a more diversified export structure or that improve the quality of their exports irrespective of the level of value added (

Henn et al. 2017), or in countries that are deeply integrated into global manufacturing and commodity exchange processes (

Didier and Pinat 2017).

Factor analysis explains the many components influencing the modern-day restructuring of the system of exports. Here we mean the system of privileges and preferences for exports, offered both by exporting states and by the counterparty states (

Abshari et al. 2021). For example, VAT tax privileges serve as a stimulus for foreign trade participants to boost their export activities (

Ainsworth and Alwohaibi 2016;

Zu et al. 2020). As the burden of VAT is borne by the final consumer, the key issue here is the interaction between the state (represented by its controlling authorities) and the business actors in the process of tax administration (

de la Feria and Schoeman 2019).

On the one hand, exporters receive state support; customs formalities are streamlined and computerized to the maximum extent possible. On the other hand, each year the number of disputes concerning VAT reimbursement increases, with the most relevant of those being the disputes that fail to be reconciled via pre-trial procedures (

Statistic of Courts 2021). The international scientific community actively debates various models of combatting fraudulent actions of entities leading to VAT gaps (

van Doesum and Nellen 2020,

2021). In particular, a team of authors analyzed the factors defining the parameters of VAT gap in an economy and concluded that three key categories of actors—final consumers, sellers, and the tax administration—must ensure the good-faith fulfillment of their duties (

Poniatowski et al. 2020). Noting the negative impact of VAT fraud, certain researchers concluded that this illegal activity creates some of the most dangerous consequences for an economy (

Fjeldstad et al. 2020;

Pouwels 2021), and also concluded that such activity could be implicated in direct or indirect financing of terrorism (

Frunza 2018); the most important instrument for combatting VAT fraud is the development of international cooperation (

Ding et al. 2021) and use of modern technologies (

Kowal and Przekota 2021).

Research in the field of VAT application in recent years is focused more on improving the efficiency of tax control (

Mitusova 2021), improving the quality and efficiency of tax administration (

Zhirova 2017;

de la Feria 2021), and minimizing the risks of tax fraud and developing methods of reducing the scope of shadow business in general (

Gurdgiev 2019). A number of studies indicated that transformations in the field of taxation, including international taxation, ensure a sustainable development trend (

de Wilde and Wisman 2019;

Báez and Brauner 2019). In particular, VAT reforms underway in China promote the implementation of innovations in export-oriented industries including via an increase in corporate investments in fixed capital while simultaneously decreasing the corporate debt ratios (

Ding et al. 2021;

Cui and Wu 2012;

Zhao and Zhang 2021). In their turn, Kowal and Przekota highlighted the demonstrated efficiencies of a tax system through the degree of resistance that system poses to tax evasion. The authors underscored the thesis that “a tax system with a few taxes set at lower rates, and preferably—with one relatively low standard tax rate—is a system that’s the least susceptible to tax fraud.” In the authors’ view, the scale of the VAT gap is closely correlated with the level of the base tax rate of VAT and with the number of reduced VAT rates available. Certain positive aspects are also seen in the further implementation of the risk management system in the tax domain (

Goncharenko et al. 2019). Specifically, this relates to modeling standard schemes of tax evasion based on the intrinsic processes of information analysis—including information obtained through pre-clearance customs control.

In the above-mentioned studies, the matters related to VAT administration tend, with increasing frequency, to transcend the concept of tax sovereignty as the VAT is levied on both imported and exported goods. In addition, VAT is applied in domestic trading within the member states of transnational integration associations. The only difference is that export VAT is subject to strict application of the neutrality principle by the relevant states (

Sidorova 2020); that principle is also closely connected to the resolution of the double taxation issue.

In studies focusing on the formation of an export VAT taxation mechanism, a specific mention should be made of the trends in development of Russian foreign trade in the environment of sanctions-imposed restrictions. Statistical data on Russian foreign trade for recent years reflects not simply the challenges of diversification of this trade or the complicated trade and political relations Russia has with its major sovereign trading partners, but also the urgent need for economic reforms in general.

2. Methodology

In order to identify trends in Russia’s foreign trade, we analyzed the volume, dynamics, geography, and structure of export and import shipments of goods. According to customs statistics, Russia’s foreign trade turnover in 2020 amounted to US

$568 bn. In 2020, it decreased by 34.3% compared to the last pre-crisis year (2013); 2020 exports were US

$336 bn, a decrease of 35.8%, and 2020 imports were US

$231 bn, a decrease of 37.0% (

Table 1) (

Foreign Trade of the Russian Federation 2021).

Traditionally, Russian net exports are positive—despite a certain crisis in foreign trade and unfavorable market conditions for Russia’s main exports (

Zasko et al. 2021). Currently, Russian exports have fallen to the levels last seen after the imposition of economic sanctions against Russia in 2014. Most measures taken by the Russian government post-2014 aimed to overcome the negative developments in relations with key sovereign trade counterparties that initiated the above-mentioned economic restrictions. These measures led to some improvements, but a new challenge for the global economy as a whole, and for Russia in particular, was presented by the COVID-19 pandemic, which led to a slowdown in global trade and to significant changes (

Bejger 2021;

Korauš et al. 2021). Energy commodities, food commodities, medical products, etc. again enjoyed top demand worldwide. These changes favorably affected Russian exports, but the impact of economic sanctions should also be borne in mind, given that these sanctions tend to become stricter with time.

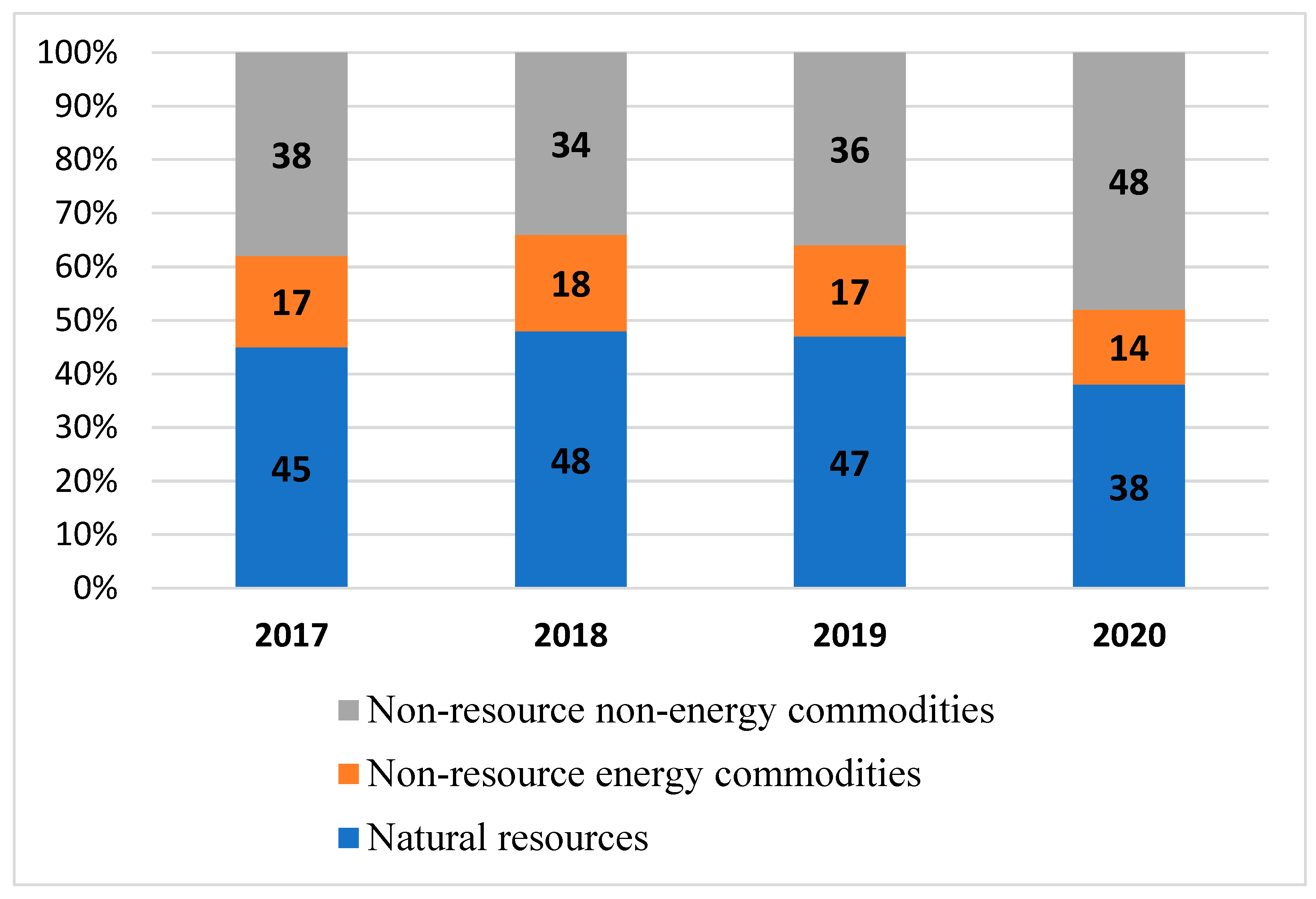

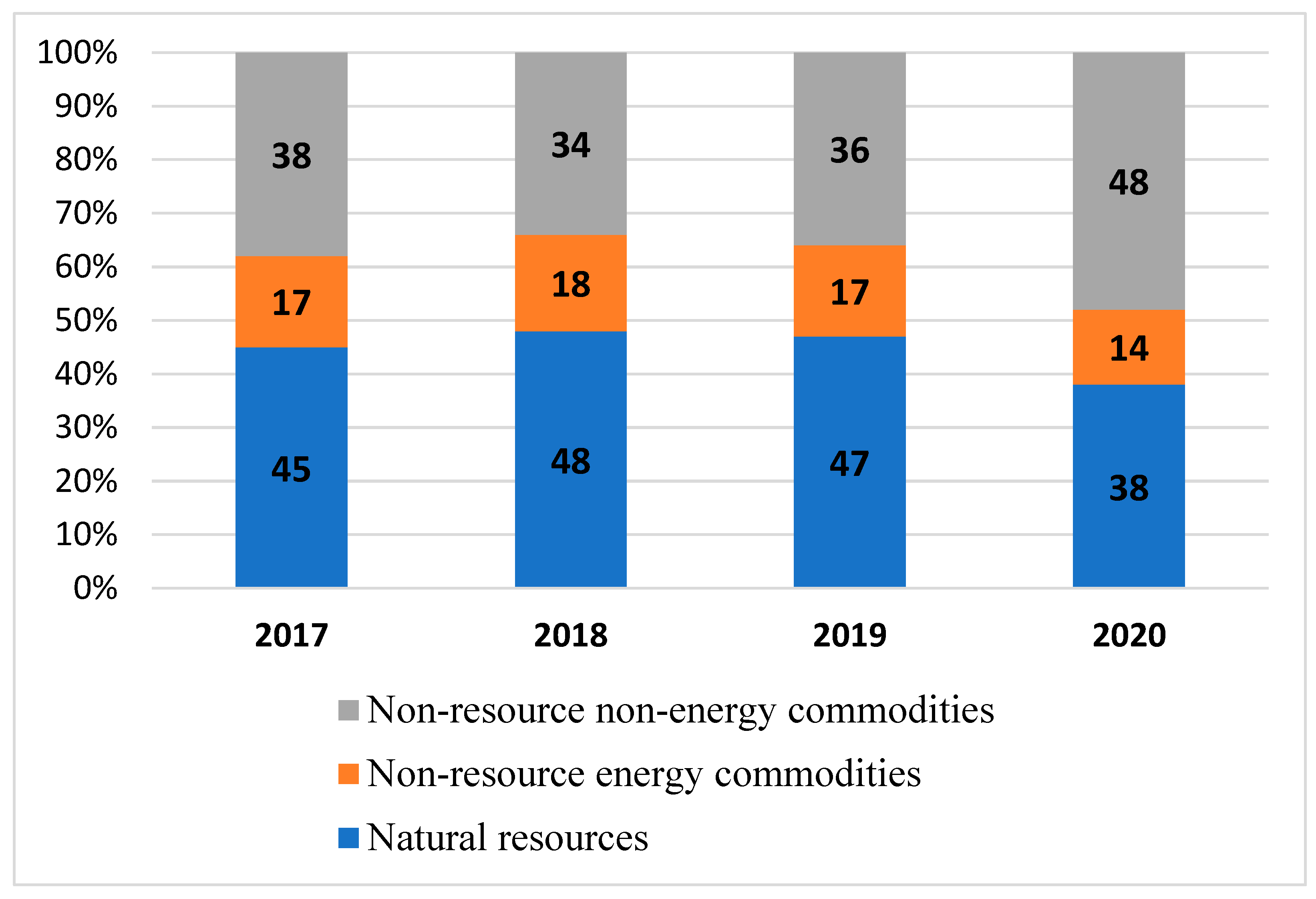

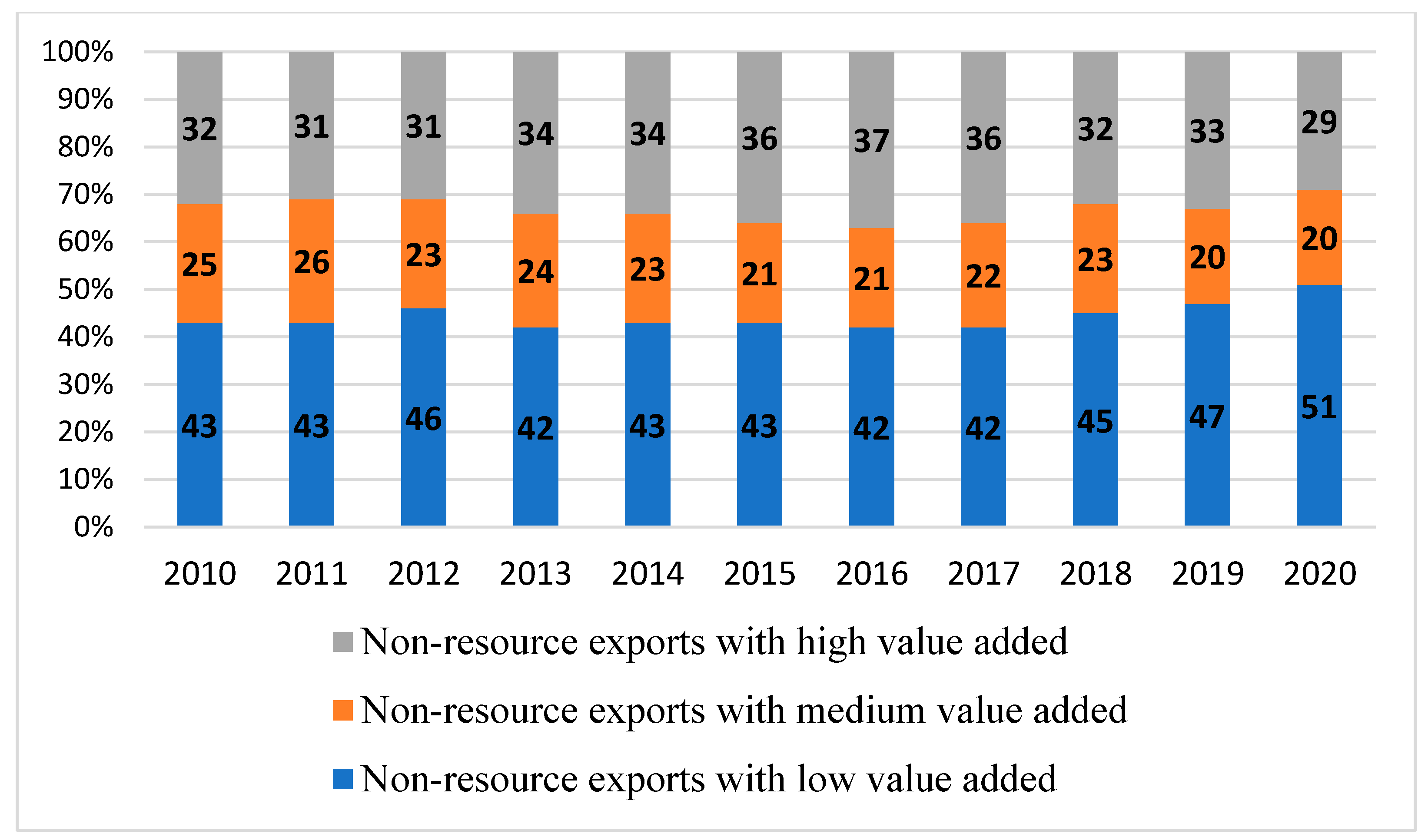

Analyzing the structure of Russian exports (

Russian Export Analytics 2021) over the last three years, a pronounced shift is clearly visible in the diversification of Russian exports (

Figure 1); in our opinion, these export levels are an indisputable indicator of the level of competitiveness of the Russian economy.

In particular, during 2020 the share of non-resource non-energy commodities increased by 10 percentage points compared to 2017.

In an environment of declining exports of Russian energy commodities, it became possible to increase the exports of finished goods and, just as important, high value-added commodities, which account for 48% of total non-resource non-energy exports (according to the classification of the Russian Export Center, non-resource high value-added products include finished goods that underwent extensive processing of raw materials: machine-building industry products, pharmaceutical products, household chemical products, garments, footwear, furniture, toys, printed materials, many food products (canned foods, confectionery and baked goods, cheese etc.); this category also includes a number of high-technology materials and semi-finished products, such as radioactive compounds and drug ingredients (

Figure 2) (

Classification of Export Goods 2021).

Analysis and assessment of the above-mentioned statistical and analytical materials lead to the following conclusions: first, Russian exports are rapidly contracting—this necessitates radical changes in its structure; second, currently, exports of raw materials and finished goods in most cases are exempt from VAT, or there are various tax privileges for such exports; third, the Russian government’s intention to stimulate growth of exports of high value-added products (using various privileges and exemptions) shall inevitably lead to abuse and irregularities.

Value-added tax is a key budget-forming tax: the share of VAT collections in the consolidated budget of the Russian Federation is ca. 20%, and the share of VAT in national GDP is 3–5%. VAT is also the most complicated tax in the Russian tax system in terms of its forecasting and administration.

Fundamentally, the tax basis for VAT calculation at the macrolevel is the volume of final consumption in the domestic market, less applicable privileges, and exemptions. For example, in international practice, the C-efficiency indicator is widely used; it is defined as the ratio of VAT collected and divided by the volume of final consumption obtained from the system of national accounts multiplied by the average tax rate—which, in its turn, is an indicator reflecting the quality of tax administration (

Ueda 2017). According to this methodology, the C-efficiency indicator in Russia increases annually and currently is at ca. 0.3. The average level of this indicator for The Organisation for Economic Co-operation and Development (OECD) countries is 0.6. New Zealand has the world’s highest C-efficiency ratio at ca. 1.0.

Such comparisons, however, are not always justified, because they do not take the legislative environment into account: the tax rates and privileges may differ significantly even between countries that have a comparable level of economic development. In addition, the domestic final consumption as a metric does not account for an important time factor—tax receipts that occur at different intermediate consumption stages involved in the creation of the final product’s added value. Said final product is subsequently exported. It is important to note here that in Russia, the volume of export transactions is taxed at a 0% VAT rate and on the macrolevel, exports have a neutral impact on total VAT receipts, because in an ideal model of administration the VAT reimbursement claimed by exporters should be equal in value to the VAT payable accrued at the exporter’s counterparty.

Similar to export transactions, import volumes also have no impact on total VAT receipts, since in a general case the importer pays “import” VAT to the customs authorities, which subsequently is deducted as input VAT on the importer’s VAT return upon the subsequent onward sale of goods into the domestic market.

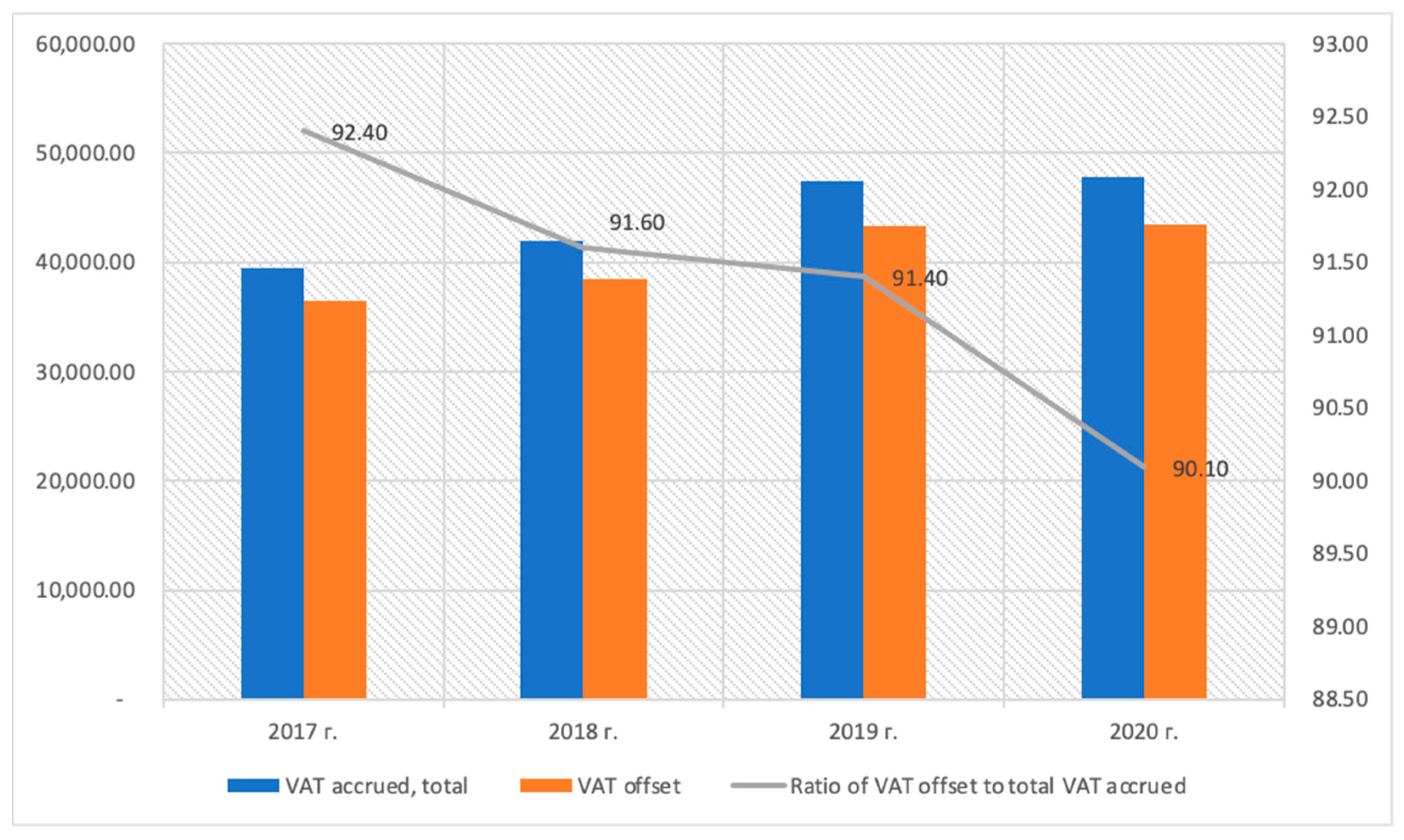

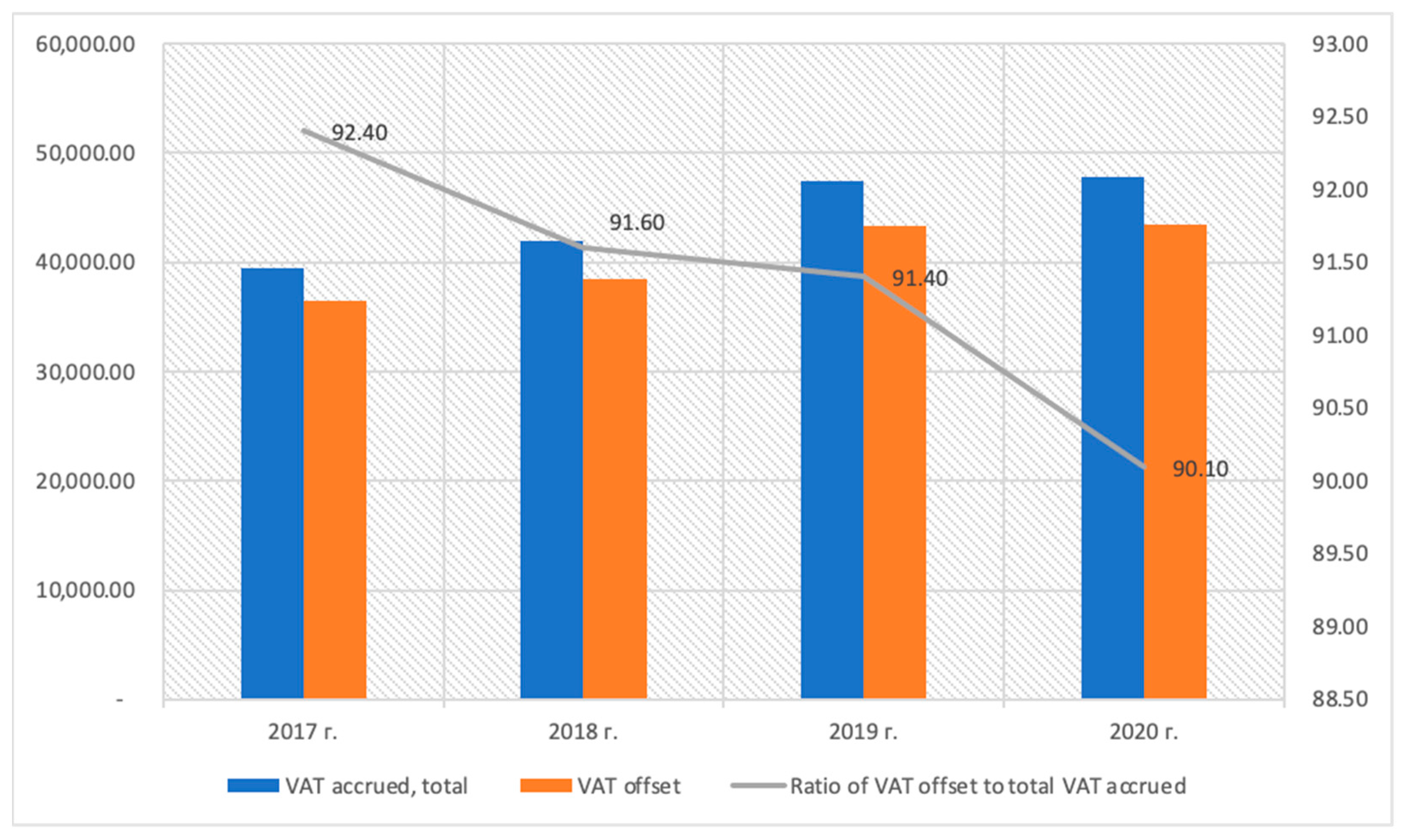

In recent years, VAT receipts show faster growth rates compared to key indicators of domestic macroeconomic activity. In particular, if we compare VAT receipt growth rates to total retail turnover growth rates, VAT receipts increase by 40% to 50% faster in different years.

This difference in growth rates is explained via the metric of the weighted impact of tax privileges: between 2017 and 2020, this metric decreased by 2.3 percentage points (

Figure 3). Reduction of this metric is defined by the Russian Federal Tax Service as one of the main drivers of an increase in VAT collections that also minimizes the risk of a taxpayer’s failure to fulfill its tax obligations.

In this situation, we must pay special attention to the practice of VAT reimbursement which indicates a significant proportion of cases when taxpayers wrongfully apply tax deductions and cases of unjustified VAT reimbursement. The main reasons include failure to submit a complete set of documents confirming the right to apply the 0% VAT rate in compliance with Article 165 of the Russian Federation Tax Code and wrongful application of VAT deductions for goods allegedly purchased because of formal documentation (in order to significantly increase the cost of goods passing through a sequence of suppliers in artificially created schemes of the procurement of goods). Export operations account for the majority of such cases.

The analysis of the problem of VAT-exempt exports from the Russian Federation via application of the 0% VAT rate shall be based on a review of the court cases involving a denial of recognition of export transactions as having taken place (

Judicial Department of the Russian Federation 2021) (

Table 2).

This practice came into active use after the introduction of Article 54.1 of the Russian Federation Tax Code that allows tax authorities to challenge transactions aimed at obtaining an unjustified tax benefit. Since the introduction of this Article, Russian tax authorities received an opportunity to view transactions of taxpayers not only according to formal criteria, but also based on the economic essence of such transactions, thus discovering the premeditated tax schemes.

We used qualitative analysis of court cases in order to highlight the main problems in the tax administration of export VAT. The standard procedure for analyzing qualitative data includes three stages, which are not necessarily carried out sequentially (they may overlap each other):

Data reduction (coding)—reduction of text volumes to a key phrase (word) based on the selection of semantic units. So, a rather verbose description can be coded according to the key word.

Reconstruction of subjective semantic systems—the search for regular connections between different semantic units.

Putting hypotheses about possible basic generalizations and conclusions based on the establishment of regular connections between various semantic units (

Artemenko and Razogreeva 2021).

This method was chosen as the most suitable for analyses of court cases.

3. Results

Analysis of the current legislation of the Russian Federation showed that the tax authorities can inspect the taxpayers’ transactions using the following criteria:

Test for distortion of information about economic transactions/taxable assets: taxpayer may not decrease their tax basis and/or amounts of taxes payable by distorting the information regarding their economic activity and tax basis in their tax and financial reporting and/or in their tax returns.

Test for the main purpose: reduction of the tax basis is not allowed to be one of the main objectives of the transaction.

Verification of actual completion of an economic transaction: a contractual obligation shall be fulfilled by the party to the contract and/or by its successor/assign.

In cases where one of the above-mentioned conditions is not complied with, the taxpayer may not include the transaction in question in their tax accounting records, i.e., VAT offset is not allowed and costs are taxes disallowed for the corporate income tax calculation.

For export transactions, three major schemes used by the taxpayers were singled out:

- (1)

the goods declared for exports do not cross the customs border as said goods do not exist or have been sold domestically, within the Russian Federation for cash, and incoming VAT related to acquisition of such allegedly “exported” goods was used by the taxpayer to offset their VAT liability (“false exports”);

- (2)

additional layers of vendors are added to the transaction for acquisition of exported goods for the exporter to be able to offset the incoming VAT;

- (3)

the taxpayer de facto is not an exporter but provides agency services for the seller/exporter, which changes the approach to VAT taxation of its operations.

In addition to schemes that are employed by the taxpayer to wrongfully offset an amount of VAT, certain scenarios are possible when real-life, bona fide transactions fall under the definition of such schemes. In addition, the reverse is also possible—when bona fide transactions are highlighted by the tax authorities as allegedly having the signs of tax minimization. That’s why we would like to mention two further problem scenarios which we include in the same list with the above-mentioned schemes:

- (1)

reclassification by the tax authorities of services contracts—entered into with foreign counterparties—to challenge the deductibility of incoming VAT;

- (2)

specifics of VAT taxation of transactions of compensation-free goods transferred to foreign legal entities.

3.1. False Exports

With the development of the tax and customs administration systems, the first item on our list became a rare occurrence in our days. Presently, verification methods for export operations and for physical exportation of goods from the territory of the Union (i.e., the Eurasian Economic Union, or EAEU) are sufficiently developed—and this prevents taxpayers from obtaining tax benefits in the form of VAT offsets for false exports of goods. One of those verification methods is the requirement to file the documents confirming the goods have physically crossed the border of the Union and an option for the automatic exchange of documents between customs and tax authorities. However, in some cases, the scheme of false exports could still be successfully implemented even today—but this requires the involvement of employees of controlling entities (

Leonov 2019). It is worth noting that development of new methods to combat false exports is still underway. For example, there are plans to equip certain types of vehicles with satellite navigation-enabled door seals capable of tracking the movements of the vehicle loaded with a specific shipment of goods, including its stops and deviations from the approved route (

FCS of Russia 2020). At the same time, many vehicles are already equipped with GLONASS satellite navigation devices; information from those trackers could assist customs and tax authorities in pinpointing the actual route of vehicles that were listed in the shipping documents for the goods.

It is necessary to mention the close connection between false exports and the concept of fictitious transactions which is derived from the analysis of provisions of Russian civil law (

The Civil Code of the Russian Federation 2021).

A fictitious transaction is characterized by its specific feature, i.e., the absence of the parties’ intent to create rights and obligations for counterparties of that specific economic activity, and the lack of intention to perform their obligations according to the terms of the transaction in line with its civil law construct. Fictitious transactions are frequently chosen by entities participating in economic activities because fictitious transactions create the appearance of a party’s performance of its obligations; this leads to systematic use of fictitious transactions in the current environment characterized by the convergence of civil, customs, and tax legal relationships.

The parties of a fictitious transaction enter into it intentionally; therefore, they shall be deemed fully aware of the legal consequences of their actions. Said parties create the appearance of a transaction being completed in strict compliance with the rules set forth in the legislation. Counterparties involved in fictitious transactions provide everything necessary at the time of entry into such transactions; sometimes they act with excessive fastidiousness, being extremely accurate with the smallest details, avoiding errors and typos, and even notarizing their actions that do not require notarial certification, etc. In such situations, the purpose for which a fictitious transaction was entered into becomes especially important. As a rule, a fictitious transaction is characterized by the “defect of will”, i.e., its parties did not express their freedom in favor of establishing, changing, or terminating the civil rights and obligations created by the contract; to the contrary, the parties would prefer that the consequences of such a fictitious transaction stipulated by its terms never materialize.

Getting back to the analysis of problems related to “false exports”, it must be pointed out that the decisions of arbitrazh courts of the Russian Federation in recent years provide a comprehensive assessment of the full body of evidence, with items of evidence being assessed both individually and in conjunction with one another—in order to eliminate internal contradictions and discrepancies between such pieces of evidence; among other things, the arguments put forward by the tax authorities are also taken into consideration (Decision of the Arbitration Court of the Rostov Region 2018).

1 A decision on whether a transaction is fictitious must be made by taking into account the circumstances under which the counterparties entered into that transaction and how the contractual obligations were performed; the motives for the selection of a particular counterparty must also be reviewed. After all the above-mentioned types of analysis, it should follow from the circumstances of entering and performing the contract, that the taxpayer had taken all reasonable measures to verify the legitimacy of the counterparty’s entry into civil law relations (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation of 02.10.2007 № 3355/07).

2According to the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated 12 October 2006 No. 53,

3 the fictitious nature of a transaction could be evidenced, in particular, by “the arguments (substantiated by evidence) of a tax authority concerning the existence of the following circumstances:

impossibility of real performance of economic transactions given the time limitations, location of property, or volume of material resources that were economically necessary for performance of work;

absence of required conditions for achievement of results of the relevant economic activity due to lack of administrative or technical personnel, fixed assets, production assets, warehousing facilities, or vehicles;

provision of payment documents with details of non-existent legal entities as well as identifying information for cash registers that have been registered to entities that are not a party to the transaction, etc.”.

The above-mentioned considerations allow us to conclude that the existence of a documented relationship between the counterparties does not present sufficient evidence to prove that real business transactions occurred between them.

Organizations should not distort the facts of their activity in an attempt to reduce the amounts of taxes payable or their tax basis (Article 54.1. of the Russian Federation Tax Code). For such a reduction to be legitimate, the following “two conditions must simultaneously be met:

the objective of the transaction is the subject matter of that transaction itself and not the subsequent non-payment or reimbursement/offset of taxes;

the obligations arising from the transaction must be fulfilled by the entity that entered into the transaction or to which said obligations were transferred under the contract.”

A significant problem of engaging in economic activities in the Russian Federation and of the related customs and tax control of economic activity still consists of the frequency of fictitious export transactions. Counterparties enter into transactions by prior agreement, while the performance of said transactions is not anticipated. The main purpose of such transactions is illegal VAT reimbursement for exports of goods. The scheme of so called “false exports” is quite simple: counterparties enter into a deal, filling out the necessary documents to place goods under the customs procedure of exports and the tax authorities in order to file a request for VAT reimbursement, but the goods that are the subject matter of the contract do not physically cross the customs border of the Russian Federation. As a rule, this scheme utilizes alleged exports of goods.

Member-states of the EAEU are working to maximize the simplification of customs and tax rules for exporters—as evidenced by the latest customs technologies—such as electronic declaration, automatic release of goods without involvement of customs inspectors, etc. In addition, (Federal Law of the Russian Federation of 3 August 2018 № 289-FZ)

4 and, subsequently, (Decision of the Eurasian Intergovernmental Council of 17 July 2020 № 5),

5 amended the regulatory process aimed at releasing participants of foreign economic activity from the obligation to submit transportation, shipping, commercial, and other documents marked with the “Release permitted” and “Goods exported” stamps to the tax authorities.

In its clarification, the Ministry of Finance of Russia (Letter of the Ministry of Finance of Russia dated 2 November 2020 No. 03-07-13/95436)

6 pointed out the necessity to confirm the export of goods from the Russian Federation by presenting any type of forwarding documents, provisions of which could be requested by the tax authorities. Said documents must prove that the goods were accepted for transportation and must contain the information about the place where the goods were unloaded outside of the customs territory of the EAEU. Such a request from the tax authorities is only possible if there is a discrepancy between the information provided by the exporter and the information in the tax authorities’ database, or if such information was not provided at all. In this case, marking the documents with the “Goods exported” stamp is also not required. Thus, it is very difficult to confirm the actual exportation of the goods in question, and this, in turn, makes it very difficult to prove the fictitious nature of the disputed transaction.

The importance of this problem increases given the course taken by the national government to change the structure of Russian exports and to significantly increase the share of high value-added finished products in total exports.

3.2. Additional Layers of Intermediaries—Resellers of Exported Goods

The second scheme can be analyzed based of one of the most important court cases concerning the exclusion of additional layers of intermediaries—i.e., the case of OOO “Emmer Trade”, case No. A32-16300/2018 (Supreme Court Ruling No. A32-16300/2018).

7 It is worth mentioning that the case was heard by several instances, but at every level the judges remained on the side of the tax authorities, recognizing that the taxpayer intentionally created conditions for extracting an unsubstantiated tax benefit. The essence of the tax scheme was that the company exporting agricultural products actually purchased its goods for resale from suppliers which enjoyed a special tax regime based on the payment of a single agricultural tax, which made them exempt from paying VAT on their sales. In order to be able to offset the incoming VAT, additional intermediaries were added to the scheme; these entities used the basic system of taxation, which made them payers of VAT. As a result, VAT amounts were not paid to the budget because the intermediate counterparties were fraudulently evading payments of tax, but the amount of VAT was offset by the exporting entity (see

Figure 4).

As part of the court hearings, the taxpayer cited the following arguments in its defense: all required documents justifying the taxpayer’s right to a VAT offset were provided; in case of bad faith actions by the counterparties, there shall be no liability on behalf of a good-faith counterparty.

The arguments of the tax authority were found to be decisive in this case and were fully supported by the court as both substantiated and proved the guilt of the taxpayer:

The documents provided by the taxpayer did not prove the real, good-faith nature of business transactions.

Intermediate vendor companies were registered just a short time before the start of the taxpayer’s contested activity.

The counterparties’ lack of the required resources for performance of their activities, as well as their physical absence at their registered addresses.

Nominee heads of counterparty entities, given the fact that the actual management of all counterparty entities was performed by a single entity affiliated with the taxpayer, as confirmed by the fact of operation of all the counterparties’ current bank accounts from one technical device/computer.

Incomplete payment of taxes by counterparty entities.

Actual goods were purchased from agricultural producers using the ESKHN (Uniform Agricultural Taxation System) and were transported directly from the producer to the taxpayer without any intermediate unloading.

Acceptance certificates for transportation services were filled in improperly, while the shipping documents were not submitted.

On the basis of the above-listed facts, it was concluded that the transactions involving additional intermediary vendors were, in fact, fictitious transactions—and on that basis, the VAT offsets previously made were challenged. It is worth mentioning that there is a large number of court cases in which transactions with bad-faith counterparties are challenged; such cases are mostly adjudicated in favor of the tax authorities. The latter have a sufficiently large data set and tools to verify the essence of business transactions. This allows the tax authorities to analyze transactions, e.g., by tracking the movement of vehicles, obtaining access to bank account information, interviewing the employees, etc.

Some court cases involving tax authorities and concerning fraudulent schemes with fictitious counterparties aiming to wrongfully claim VAT offsets have a more complicated body of evidence. The above-mentioned case is one of the first heard after the enforcement of Article 54.1 of the Russian Federation Tax Code. Since then, taxpayers began structuring such schemes more carefully in order to have convincing arguments in their favor, but the tax authorities have learned to more thoroughly study the sequence of vendors in the supply chain.

To further develop a transparent system of administration of export VAT reimbursement, it would be expedient to highlight the key arguments put forward by the tax authorities when they decline recognition of VAT amounts. This would give the taxpayers an opportunity to avoid future tax disputes at the stage of planning their activity; by the same token, the tax authorities would benefit from the reduction of litigation-related costs.

3.3. Agency Services Provided to An Exporting Seller

The third type of VAT minimization scheme designs involving exports is the substitution of the subject matter of the contract. In particular, a burning problem is the applicability of a reduced VAT rate of 0% on sales of goods to foreign counterparties by entities that could be recognized as agents in a purchase and sale transaction between a foreign entity and another Russian entity.

An example of this type of tax-related court case is the case of OOO “RosTsvetMet” (Resolution No. A56-66370/2014).

8 During the hearings of this case, the following circumstances were ascertained:

The taxpayer entered into purchase and sales agreements with a foreign entity—in this contract the taxpayer acted as a seller, and with a Russian entity—the taxpayer here acted as a buyer.

A Russian entity leased the warehouse to store goods; it possessed specialized machinery for manufacturing goods and motor vehicles for the transportation of goods. At the same time, the taxpayer did not own any working capital or other technical capabilities for performing the obligations under a transaction for purchase and sale of goods.

The taxpayer’s obligations under the contracts did not include manufacturing, loading, delivery, or insurance of the goods. In fact, its functions were limited to entering a contract with a foreign entity.

Source documents of the taxpayer did not include the shipping documents; the waybill (Russian official form TORG-12) did not include information about delivery address, weight of the cargo, or any transportation delivery notes. This confirmed the conclusions about the limited scope of functions and risks borne by the taxpayer in these transactions.

Performing outward delivery from the warehouse, in compliance with the contract, was the obligation of the foreign counterparty. In its turn, the foreign entity entered a contract with the Russian entity—which was the initial supplier of the goods—for delivery of the goods from the warehouse leased by that Russian entity.

The shareholders, heads of companies, and certain employees of the Russian companies participating in the tax scheme were listed as employees at both above-mentioned companies—which indicated their interrelated nature.

As a result, the court took the side of the tax authority because the formal fulfillment of requirements to enter into a contract for purchase and sales, and the transfer of title to the goods, are not sufficient to recognize as a legitimate VAT exemption of exports. Accordingly, a counterparty must monitor not only the formal compliance with legal norms, but also the actual contents and the substance of operations being performed, including the functions and risks borne by the taxpayer.

A similar conclusion was made during the court hearings of the case of OOO “Step” (Resolution No. A40-206968/2018).

9 In those proceedings, the only function of the taxpayer that formally performs exports was maintaining the document flow with foreign counterparties. The remaining functions—manufacturing and storage of goods—were assigned to an interrelated organization that uses a simplified taxation system and is located at the same address as the taxpayer itself. The situation was further aggravated by the fact that the taxpayer acquired raw materials to be used for manufacturing the goods using funds transferred by an interrelated organization in the form of financial assistance. As a result, the tax authorities challenged the VAT deductions made; the tax authorities referred to the concept of the intentional splitting-up of the business to obtain an unsubstantiated tax benefit.

Thus, in practice, taxpayers intentionally employ tax schemes for taxation evasion related to the specifics of the application of the 0% VAT rate for export of goods—the potential deductibility of incoming VAT. At the same time, according to the current legislation, the tax authorities have both the right to perform a formal review of the transactions entered and performed by the taxpayers and also the right to analyze the actual substance of those transactions. Currently, we see an active development of methods to discover the inter-relationship between the counterparties and their possible collusion to obtain a tax benefit.

However, we have to bear in mind that, in this situation, the good-faith taxpayers remain in an unfavorable position; they are forced to spend additional funds and their employees’ time on the preparation of sufficient document sets proving their compliance with the tax legislation and the lack of their intent to obtain any tax benefits.

3.4. Reclassification by the Tax Authorities of Services Contracts Entered with Foreign Counterparties to Challenge the Deductibility of Incoming VAT

Prior to amendments to the Russian Federation Tax Code coming into force on 1 July 2019 that allowed taxpayers to offset the input VAT on the provision of any services to foreign counterparties, there were widespread court precedents where judges reclassified the subject matter of the contract and the new subject matter was not covered by the provisions of the Russian Federation Tax Code. Based on that judicial decision, the taxpayer lost grounds for offsetting the input VAT.

A scenario that is among the most frequently reviewed in the court hearings is a reclassification of an export contract for sale and purchase into two standalone contracts: a contract for the export of goods and another contract for the provision of services related to an export transaction. Accordingly, the amounts of taxpayer’s revenue associated with the provision of services were classified as activities not subject to VAT—this led to the loss of justification for offsetting the input VAT. We can mention such examples as the cases of AO “TVEL” and OOO “Materik” (Resolution No. A44-1329/2019).

10 The court in both cases decided in favor of the tax authority challenging the VAT offsets; the court decisions referred to the need to separate the provision of R&D services and the sale of goods for the creation and further utilization of which said services were purchased. The main arguments of the court and the tax authorities were as follows:

The price of the contested services/works was determined separately from the price of the goods and was not included in the latter.

A realizable engineering model could not be deemed a standalone good, but instead shall be recognized to be the result of the provision of R&D work.

The taxpayer’s arguments explaining the auxiliary nature of the services provided with reference to the goods being exported were declined by the court and recognized to be insignificant.

Another option also involved a reclassification of one type of service into another that does not meet the requirements of the Russian Federation Tax Code. allowing input VAT to be offset. An illustration of this situation is the court case of OOO “PAREXEL International” (Moscow) (Determination No. A40-194412/2015);

11 in this case, consulting services provided to a foreign entity were recognized to be the services for organizing clinical trials. According to the content of the Decision, the taxpayer entered into contracts with a foreign company for the following services: consulting, information collection, and organization and coordination of clinical trials. However, the tax authorities stipulated that all those types of services provided under the said contact were in fact equal to agency services for organizing clinical trials. The court decided in favor of the tax authority, quoting the following arguments: the true purpose of all services under the contract was to conduct the clinical trials; the cost of agency services under the contract was significantly lower than the cost of other services; the main type of the taxpayer’s activity was conducting clinical trials.

Analyzing the court decisions quoted above, we can notice the contradictory nature of the conclusions made: in one case, there was a division of the subject of the contract into several separate and standalone components, and in the other case, all types of services, to the contrary, were united into one comprehensive service. The common denominator for all the decisions is the point that reclassification of the contracts allowed the tax authorities to assess an additional tax to be paid by the taxpayer to the budget. On the one hand, the provisions of Article 54.1 of the Russian Federation Tax Code allow the tax authorities to approach the analysis of the contracts from the viewpoint of applying the concept of unjustified tax benefit. On the other hand, civil law does not preclude the parties from entering several contracts with different subject matters—all with one and the same counterparty, or to enter into framework contracts and subsequently setting forth the specific conditions within the scope of one additional agreement. As a result, the reclassification of contracts is an approach based on a subjective evaluation of an entity’s activities; this approach has no precise legislative foundation. In this situation, taxpayers cannot act freely within the framework of the law when selecting the terms of their interaction with their counterparties. Instead, the taxpayers must mind the existing gaps in the provisions of the law that allow the authorities to challenge the taxpayers’ actions.

From this point of view, the introduction of amendments allowing the offsetting of incoming VAT for almost all types of services provided to foreign entities brings positive consequences; it removes subjective aspects from assessment of the taxpayers’ actions and also corrects the vagueness of the legislative provisions which previously led to different interpretations of tax liabilities and, correspondingly, to disputes between the taxpayers and the tax authorities.

Currently the disputes concerning R&D work may stay relevant (subparagraph 16.1 of part 3 of Article 149 of the Russian Federation Tax Code) in situations where said work was performed by the taxpayer as an auxiliary service in relation to sales of goods to a foreign entity. In addition, a similar dispute may arise about the transfer of exclusive rights or rights of use of said R&D results if those results were transferred—again, as an auxiliary step—together with the sale of the goods and provided that the goods are required for enjoyment of said right to use (subparagraphs 26 and 26.1 of part 2 of Article 149 of the Russian Federation Tax Code).

3.5. Specifics of VAT Taxation of Transactions of Compensation-Free Transfer of Goods to Foreign Legal Entities

The legal norms governing taxation of compensation-free transfer of property to third parties are laid down in the Russian Federation Tax Code and are interpreted as follows: the transfer of property rights on a compensation-free basis is deemed a sale of property and, correspondingly, is subject to taxation with VAT.

The use of a reduced VAT rate of 0% is allowed in situations where the export sale of goods is performed using the customs procedure of exportation—part 1, Article 164 of the Russian Federation Tax Code (

Russian Federation Tax Code 2021). In such a situation it is necessary to correctly define the terms used in interpreting this legislative provision. Exportation is defined as the procedure in which goods are delivered from the territory of the Russian Federation and remain permanently outside of said territory, as defined in part 1 of Article 139 of the EAEU Customs Code (

The Customs Code of the EAEU 2021). Realization is defined as a transaction of the transfer of ownership rights to goods, work, or services to a third party that occurs in return for compensation. In such a case, the exchange of goods between two entities is also recognized to be a method of realization. In certain cases, realization also includes compensation-free transfers, as mentioned above, including for the purposes of VAT taxation (part 1 of Article 39 of the Russian Federation Tax Code).

Accordingly, in a standard situation of compensation-free transfer of goods to a foreign entity, the Russian organization carries out activities that are taxable with VAT, to which it may apply a reduced VAT rate of 0% when the required set of documents can be provided. At the same time, the company has a possibility to offset the input VAT related to this transaction of the transfer of goods.

In the process of researching, a specific case of compensation-free transfer of property to a foreign entity was considered. The approach to the situation we describe below is not as straightforward as defined above. One of such special situations is the transfer of raw materials to a third party for production of the finished product that shall be returned or sold to a Russian entity.

In most cases, such relationships are formalized by a tolling contract, which is regarded as being equivalent to a contract for work and services by the provisions of Article 713 of the Civil Code of the Russian Federation (hereinafter—the Civil Code). In this scenario, transaction documentation consists of a work order for performance of certain work to manufacture finished products using the raw materials provided by the customer. In this situation, the title to the raw materials does not transfer to the entity performing the work when the raw materials are physically handed over to the foreign entity, while the manufactured finished product is the property of the customer. As a result of the above, we can conclude that the subject matter of the contract is not the realization of goods but rather the performance of work aimed at producing things or processing raw materials.

These circumstances justify the absence of grounds for the approach used in the usual compensation-free transfer of property. In saying so, we refer to the following facts:

In the absence of title transfer for property being physically transferred, such transactions cannot be recognized as a realization of goods.

The reduced VAT rate shall only apply to realization transactions entered into in the course of an exportation procedure.

As there is no realization, the taxable object for VAT does not emerge.

Correspondingly, in cases of the compensation-free transfer of raw materials to a foreign entity under a processing contract and without transfer of title to said raw materials, the Russian counterparty does not create any VAT liabilities on its side.

At the same time, it must be understood that raw materials could be transferred to the counterparty performing the work in a greater volume than required as a safety stock, to rule out the risk of a raw materials shortage that could delay the manufacturing process. In this case, there are several options for treatment of such excessive raw materials:

The counterparty performing the work could keep said raw materials and count these towards the next delivery of raw materials. In such a scenario, the Russian entity, when placing its next work order, shall transfer to the foreign counterparty a lower volume of raw materials. This option is the most preferable one provided that the two counterparties engage in similar transactions on a stable and repetitive basis.

The counterparty performing work could return the excess materials to the Russian entity. Such transaction shall not create any tax consequences as there also will be no transfer of title—and that means there is no realization of goods in this transaction as well. However, this approach would be less beneficial for the companies involved due to extra costs of the return transportation of raw materials.

The counterparty performing work could acquire the remainder of the raw materials by decreasing its fee for manufacturing services, a discount subject to approval from the customer. In this scenario, it is important to note that the nature of the transaction changes and an object of taxation emerges, as a compensation-based transfer of title now takes place.

The first option is the most frequent, as economic relations between manufacturing companies usually have a stable character to ensure permanent operation of the manufacturing and sales cycle. However, the second and third situations also do occur in practice, for example, in cases of one-time orders, the manufacturing of exclusive models, or when a specific product is discontinued and therefore the last order of that product is placed, provided that the discontinued product required some specific raw materials for its manufacturing.

The contractual relations involving the transfer of the customer’s raw materials between Russian and foreign entities could also be based on a transfer of property rights from one entity to the other. Such an agreement is also stipulated by Russia’s civil legislation: if the cost of processing is significant in relation to the original value of raw materials received, the title to the goods produced transfers to the manufacturer. In this case, the manufacturer reimburses the customer for the cost of the raw materials. However, even in cases when processing is insignificant, the contract may provide for the transfer of title as envisaged by the Civil Code of the Russian Federation. In addition to this form of cooperation involving reimbursement of costs, the second most common practice is the scenario where the manufacturer receives the title to the raw materials in exchange for a reduction in the cost of the finished goods to the customer.

In the situation described above, the nature of the transfer of raw materials could not be called compensation-free because there is reciprocity—a discount is granted for purchase of other goods. However, at the same time, this transfer of materials is based not on the contract of sale, but on another type of an agreement between the parties.

At the same time, the customer may transfer raw materials to the manufacturer not in order to receive a reciprocal reimbursement, but due to the specifics of its own order: e.g., the need to use specific raw materials to obtain a higher-quality product meeting the required standards. In this situation, the nature of the transfer of raw materials will be compensation-free and the title to said materials also passes onwards to the foreign entity.

The approach to VAT taxation of raw materials transfers in both cases will be the same: these operations fall under the definition of the object of taxation since they are recognized as a realization due to the transfer of title. However, the question of the legitimacy of categorizing operations as exports arises in such scenarios.

The key factor for solving this issue is the correct interpretation of the definition of “exportation”, i.e., understanding of the condition requiring outward transportation of goods from the territory of the Russian Federation and that the permanent location of the goods being outside of the Russian Federation territory. On the one hand, the abovementioned transactions could be considered export transactions, given that the specific commodity, “raw materials”, is being exported outside of the Russian Federation and is consumed in the manufacturing process in another state. On the other hand, the raw materials are exported outside the territory of the Russian Federation to be processed—and are subsequently returned in a modified form. Consequently, entities engaged in economic activity risk misunderstanding the norms of law—while said norms are key to determining the approach to taxation of said entities’ activities. When analyzing the core issue of a dispute, no clarifications by state authorities, no law enforcement practice, nor court precedents related to this topic have been found.

4. Discussion

In our analysis of the practice of applying a reduced VAT rate of 0% to goods exports, it was found that Russian tax legislation is periodically amended—which eliminates the inaccuracies that previously caused disputes and issues between taxpayers and tax authorities. At the same time, currently, there are certain legal provisions that may be ambiguously interpreted by the taxpayers intending to legally minimize their tax liabilities; on the other hand, such ambiguity could be an obstacle for good-faith taxpayers willing to build the most favorable business relationships with foreign counterparties for manufacturing projects.

Tax authorities have an opportunity to analyze transactions not only from a formal point of view, but also based on the investigation of the substance of transactions. This opportunity facilitates tax authorities’ identification of premeditated counterparties’ actions aimed at obtaining unjustified tax benefits. The other side of this approach consists of the subjective approach to assess a taxpayers’ actions—this may lead tax disputes even in situations where the actions of an organization were in fact motivated by business reasons.

In order to improve the Russian system of VAT taxation of export operations, provisions of EU regulations in this area have also been analyzed. In the EU, exportation of goods is subject to VAT at the rate of 0%, and the input VAT on goods, work, and services used for exports could be offset in full. The primary document regulating VAT taxation in the EU is the relevant EU Directive (The Council Directive of the EU on the Common System of VAT 2006).

12 The provisions contained in that Directive apply in all EU countries and are similar to legal provisions that apply in the Russian Federation. However, it is worth mentioning the key differentiating factor, specifically—the requirements for proof of transactions. According to Chapter 10 of the Directive, input VAT amounts could be offset, in a general case, if the following conditions are met:

goods, work, and services being acquired must be used in an activity that is taxable with VAT or in some certain specific types of activities, including exports;

the taxpayer has a VAT invoice filled in according to the provisions of the legislation;

the taxpayer has filed the VAT report containing the information on volumes of transactions, the applicable VAT rate for said transactions, and the tax basis for the tax reporting period.

At the same time, in the EU regulations, there are no requirements regarding the filing of any supporting documents proving the legitimacy of an application of a reduced VAT rate for exports. This partially confirms the problem of documentary proof of reduced VAT rates for exporters in a situation when control over its administration is tightened—it is precisely that problem which the present study attempts to resolve.

Most countries with a significant share of the global exports volume share certain common fundamentals of export VAT taxation, but each jurisdiction has its own specifics. Legislative provisions of the Russian Federation have the highest similarity to the European approach of export regulation—this is explainable by the fact that both regulatory systems have been generally guided by the OECD recommendations (

van Doesum and Nellen 2021). At the same time, the Russian Federation employs an approach that is more demanding from the taxpayer’s viewpoint in terms of documenting the fact of exportation. Thus, there is a need for transparent procedures enabling the sustainable operation of exporters and their interaction with foreign counterparties.

In the current situation, it is necessary to develop more detailed requirements for the taxpayers’ confirmation of the fact that a service has been rendered, so that the taxpayers could efficiently interact with foreign counterparties to obtain the documents required. Such rules could be specified directly in the Russian Federation Tax Code; these rules could be introduced in part 4 of Article 148 of the Russian Federation Tax Code or alternatively, an official detailed clarification from the Federal Tax Service (FTS of Russia) could be developed, similar to the document referred below and listing detailed requirements for confirmation of a taxpayer’s compliance with counterparty verification rules (Letter of the Federal Tax Service of 10 March 2021. No BV-4-7/3060).

13Taking into consideration the established practice, in addition to the contract with the counterparty, the following documents should be included in the list of required documents: the acceptance certificate describing the services rendered with detailed breakdown by each specific type of service, the service provider’s report with a description of services and forms of provision of deliverables of services rendered, and other documents confirming provision of services using the template provided in the report. Additionally, the official clarification of the Russian Federation Federal Tax Service should provide examples of other potentially suitable documents: a service order from a foreign entity; files containing consultations, research results, and other information in text form; a schedule of events and presentation materials for such events; materials for training sessions conducted; screenshots of software programs provided for use, etc.

The revision of tax legislation is necessary for taxpayers to be able to efficiently and correctly draft and execute their contracts with foreign counterparties. Currently, this process is complicated by the imprecise wording in the legislation and by the possibility of the reclassification of one type of contract into another type by Russian tax authorities.

As we established earlier, exports of goods for which R&D work was required or for which a transfer of usage rights from the performer of work to the end user is necessary, may still be subject to tax disputes—specifically in the aspect of offsetting the input VAT. Russian tax legislation stipulates that any R&D work, including certain pre-defined elements of work, and the transfer of usage rights performed on the basis of a licensing agreement, are exempt from taxation.

Due to specifics of subjective interpretation of Russian tax legislation, certain taxpayers offset the full amount of input VAT on R&D work performed, provided said work was required for the creation and further sale of goods being exported, and also on a transfer of rights of use of intellectual property. Such a transfer was performed under the contract for sale and purchase as a measure to ensure that the goods have their required functionality and are capable to be used for a specific purpose.

On the one hand, this approach is in stark contradiction to the legal norms established by the Russian Federation Tax Code. On the other hand, taxpayers perform these operations under a sale-purchase agreement, taking the other parties of this agreement only as a manufacturing process to create export goods for which there is a zero rate of VAT. As a result, both sides of the tax dispute have grounds for defending their own positions based on subjective understanding of the rules of the tax legislation.

With the purpose of establishing a unified approach to understanding the rules of tax legislation, we hereby suggest to amend a number of articles of the Russian Federation Tax Code; these amendments would more precisely define, for the taxpayers’ benefit, the interpretation of the approach, which is also supported by the application and interpretation of tax law. Specifically, the approach consists of identifying the costs of R&D work carried out or of the usage rights transferred under the contract for sale and purchase; afterwards the amount of such separate costs is subsequently used to correctly determine the amount of input VAT that could be offset.

Another controversial VAT taxation issue that was examined in our study is the taxation of transactions in which the transfer of goods to a foreign counterparty is performed under a processing contract involving customer-supplied raw materials.

International organizations with manufacturing cycles divided into separate companies located in different countries are frequently encountered in the business world today (

van Doesum and Nellen 2021). Thus, it is important to have sufficiently detailed legislative provisions defining the nature of work in this area, including the provisions of the tax law. We posit that it is necessary to provide more details in the provisions of the Russian Federation Tax Code to facilitate an understanding of methods used for VAT taxation of operations involving the transfer of customer-owned raw materials to a foreign entity with any possible type of documentation.

As was already established, such transactions could be documented in different ways, and may have a key impact on the tax treatment of that transaction. At the same time, there is no clarity regarding the taxation of certain types of operations involving the transfer of customer-owned raw materials because of the ambiguity of the term “exportation”. There is no certainty whether the raw materials, that were earlier transferred to a foreign entity, could be considered exported and have their permanent location outside of the territory of the Russian Federation.

In view of the above considerations, we propose to introduce a separate type of agreement—a “services contract for processing of raw materials transferred by a customer”. This type of contract must be introduced in Chapter 37 of the Russian Federation Civil Code. In the Articles forming that Chapter of the Russian Federation Civil Code, the main rules for documenting such types of transactions must be provided. At the same time, it is necessary to also amend the Russian Federation Tax Code; proposed amendments would set the general rules for VAT taxation of transactions involving the transfer of customer-owned raw materials:

To amend Subparagraph 1 of paragraph 1 of Article 164 of the Russian Federation Tax Code with paragraph No.6: “…exported outside the territory of the Russian Federation according to the contract for transfer of customer-owned raw materials”.

These amendments would allow taxpayers to properly maintain the document flow with their foreign counterparts, taking into consideration the requirements of the Russian Federation Civil Code. This will also give taxpayers an accurate understanding of their VAT tax obligations for the above-mentioned transactions, whether the 0% VAT rate could be used when the title to raw materials is transferred to a foreign entity, or whether VAT-exempt status is available in situations when there is no transfer of title.

5. Conclusions

The economic substance of applying a reduced VAT rate to exports can be estimated by comparing it to other countries’ experience—or by analyzing it at the national level. First, OECD has introduced recommendations for VAT taxation of international transactions, one of the principles of which is collecting tax at the purchaser’s location. Despite the advisory rather than mandatory nature of this principle, it is observed by the majority of the world’s countries. Such a situation could be explained by the wish to harmonize national legislations in order to eliminate double taxation. Second, at the national level, the introduction of a reduced VAT rate for exports, while imports are still taxed, facilitates support of domestic producers’ competitiveness in the national market.

As for legal specifics, we described the main provisions of the tax legislation regarding VAT on exports of goods outside the territory of the Russian Federation in the exportation procedure, as well as VAT on services provided to foreign entities, including the permission to offset input VAT, specific features of taxation in transactions with tax-exempt suppliers, and the requirement for provision of documentary proof.

We reviewed the statistical data characterizing the trends of foreign trade development, including exports and imports; we assessed their impact on economic by growth taking certain factors into account, such as the use of tax incentives for exports of goods, work, and services. We analyzed the practice of law interpretation and law enforcement, and in particular we examined arbitration cases in which tax authorities attempted to identify schemes intentionally created by exporters in order to obtain tax benefits. The most frequent situations of “false exports” of goods were found, which included the following: application for exporting goods across the border of the customs territory using the customs procedure of exportation, but without actually moving the goods across the border—goods were subsequently sold within the Russian Federation with payments received electronically; introduction of bad-faith counterparties into the supply chain in order to obtain tax benefits by offsetting the input VAT; and performance of activities, which for all purposes could be classified as agency services through entry into contracts for sale and purchase in order for the taxpayer to apply for application of a reduced VAT rate.

To minimize the number of tax disputes, we suggest amending the provisions of Russian legislation and making them more detailed. Specifically, we wish to clarify the list of documents required to confirm the fact of rendering services to foreign entities, and to differentiate the cost of exported goods and costs of auxiliary services rendered additionally under the contract for sale and purchase. Such differentiation must be made either in the text of the contract and/or in the source documents relating to it; to set in the Russian Federation Civil Code the definition of the services contract for processing of raw materials transferred by the customers, the main terms and conditions of such a contract, and also to introduce with a standalone legislative act an option for applying a 0% VAT rate for the sale of goods exported outside of the territory of the Russian Federation under the contracts for transfer of customer-owned raw materials.

The suggested innovations could make a positive impact on international trade as they would improve the clarity and stability of conditions for developing Russian businesses offering their services internationally. At the same time, a decline in the number of disputes based on subjective judgments concerning the taxpayers’ actions would allow the tax authorities to focus on clearer and more objective criteria of tax compliance by Russian companies. This would simplify the administration of taxation in one of the areas of tax law. This study showed that there are still legal provisions that need a more precise and more detailed definition to rule out potential disputes arising from gaps in the existing legislation.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}