The Evolution and Takeoff of the Ecuadorian Economic Groups

Abstract

:1. Introduction

2. Literature Review

2.1. The Establishment and Control of the Ecuadorian Economic Concentration

2.2. The Development and Integration of Ecuadorian Economic Groups

A Brief History of the Research Efforts on the Ecuadorian Economic Groups

3. Data Source and Methodology

- (a)

- 2015–2019 (financial and fiscal variables);

- (b)

- 2016–2020 (ranking of the economic groups).

- (a)

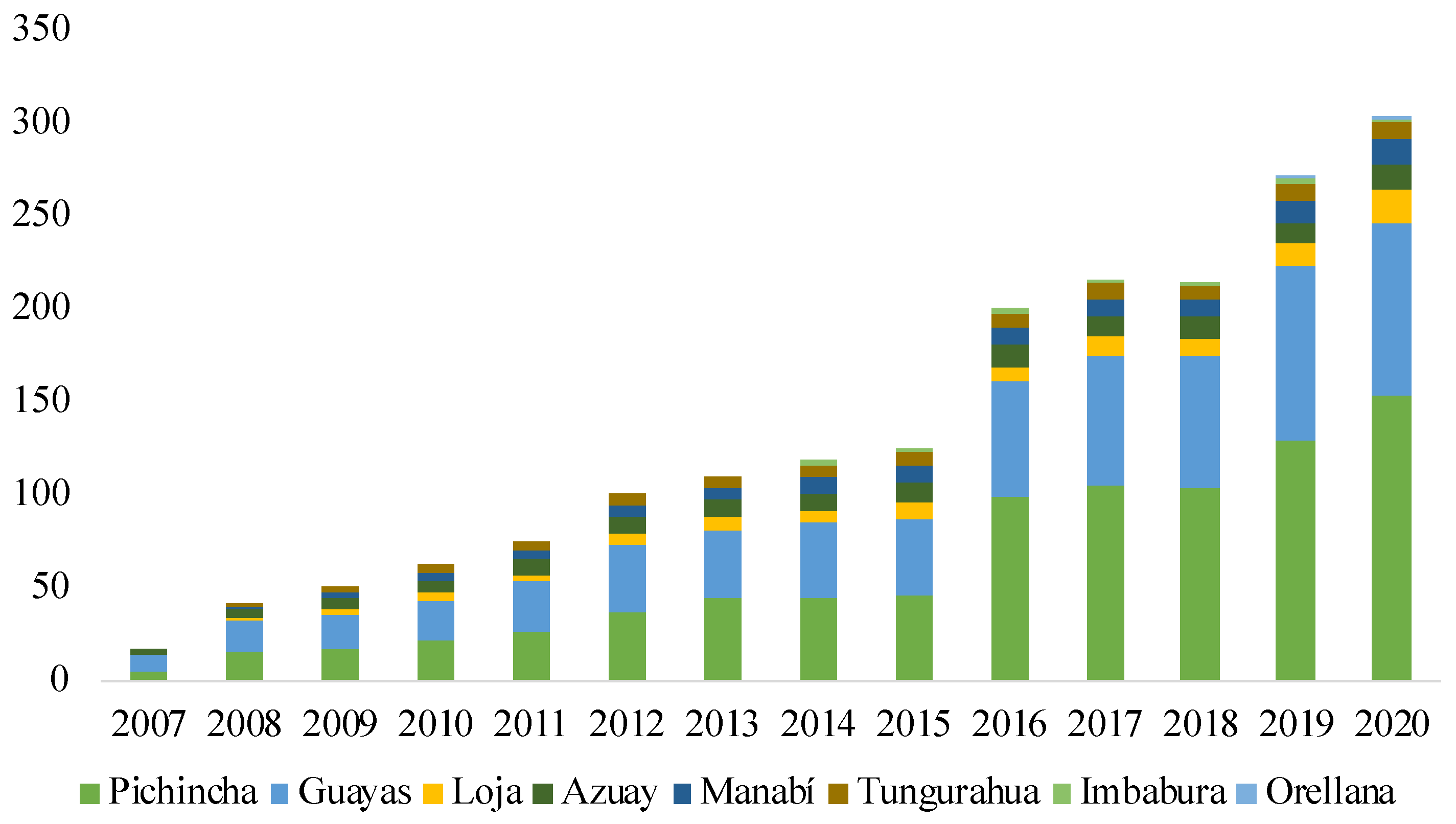

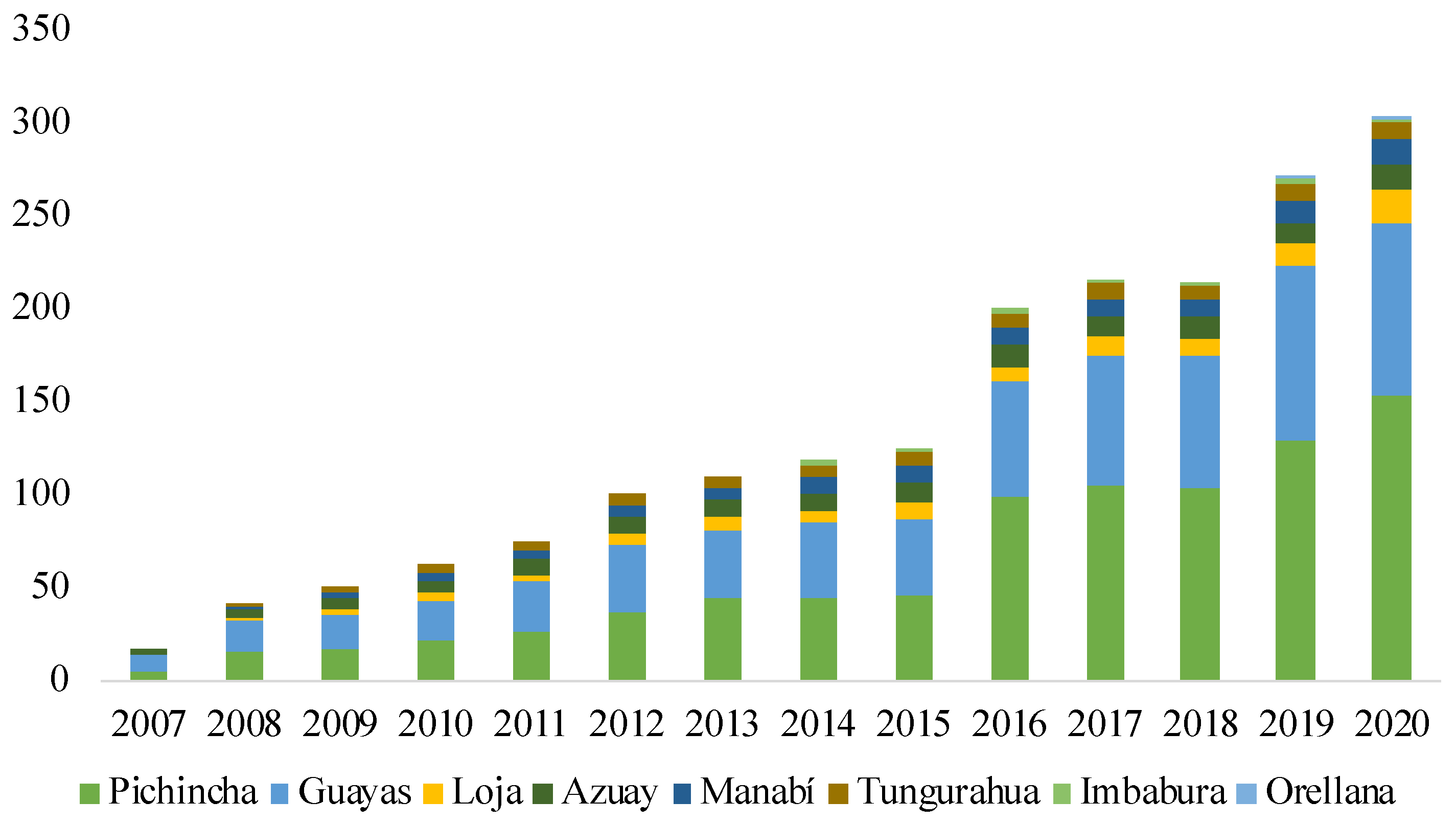

- A graphic analysis of the evolution of the Ecuadorian economic groups, and the evolution of the most representative macroeconomic and fiscal variables of Ecuador. This analysis establishes the representativeness of the Ecuadorian economic groups in the local economy.

- (b)

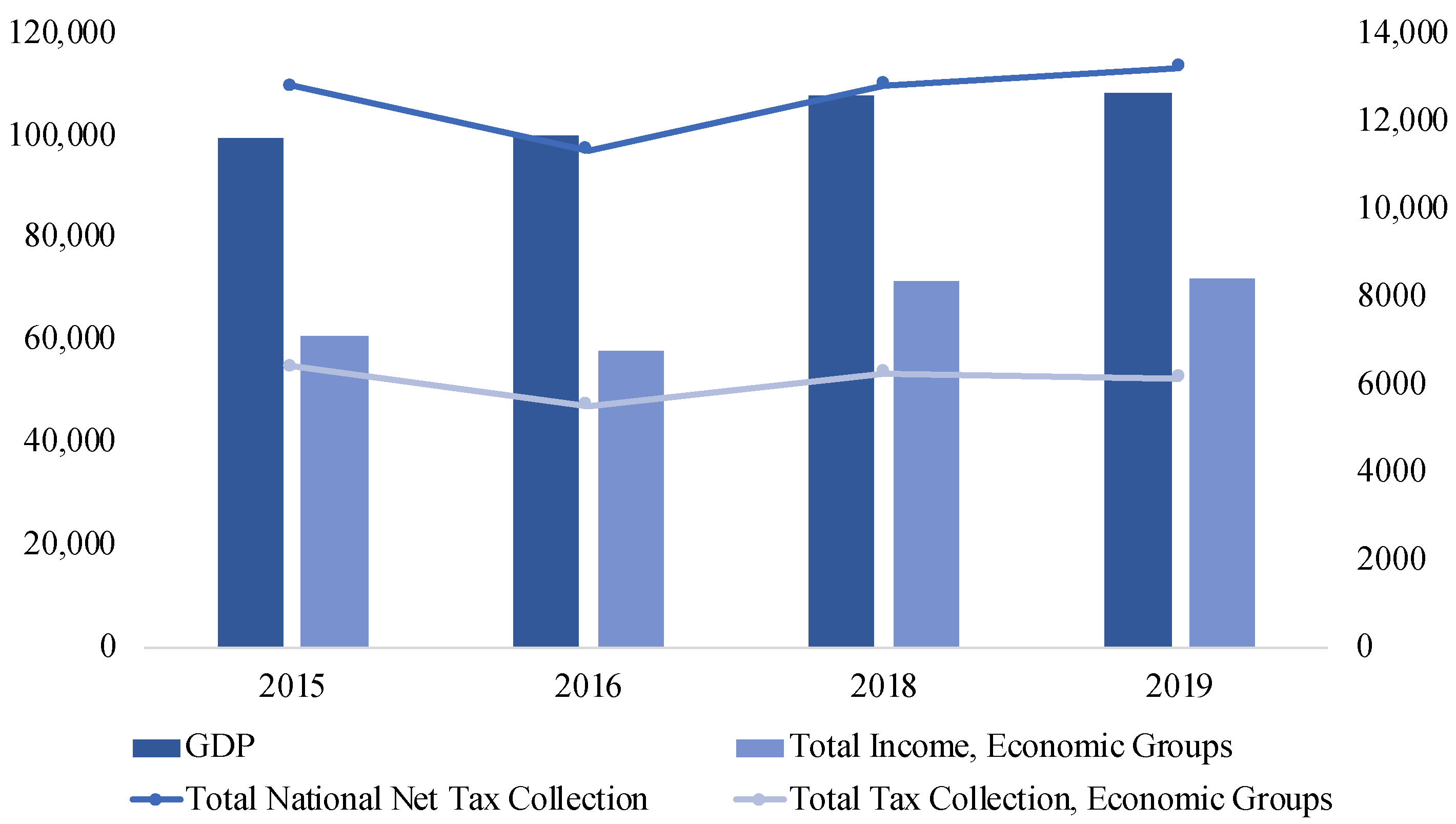

- A comparative analysis of the composition of the Ecuadorian economic groups, and the evolution of their financial and fiscal variables. This analysis compares figures from 2015 to 2019 to determine if the Ecuadorian economic groups have increased over time.

- (c)

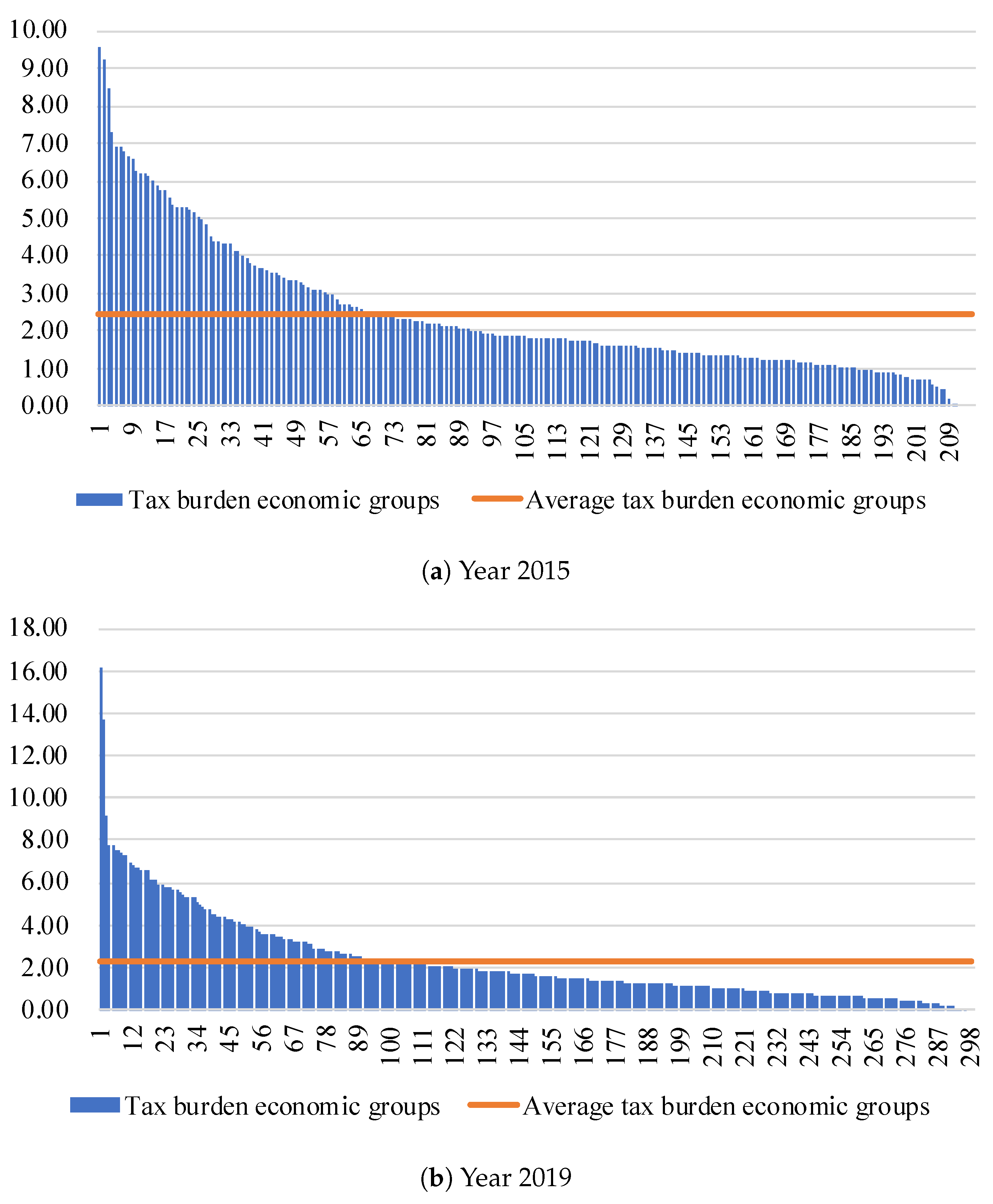

- A descriptive analysis of the tax burden of the Ecuadorian economic groups to showcase the amount of paid taxes (considered as a proportion of the total income) in a specified period.

- (d)

- An analysis of the evolution of the top-10 Ecuadorian economic groups (according to their size and tax collection). This analysis explains the tax representativeness of the top 10 Ecuadorian economic groups vs. all the remaining economic groups and compared the outcome with the total national net tax collection. Moreover, the analysis of the Ecuadorian economic groups includes the contribution on the national net tax collection to verify if their representativeness have remained stable over time.

- (e)

- A correlation analysis between the financial variables of the Ecuadorian economic groups, and the total tax collection to prove the linear association between variables.

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Acosta, Alberto. 2006. Breve Historia Económica del Ecuador. Quito: Corporación Editora Nacional. [Google Scholar]

- Anaya, Eduardo. 1990. Los Grupos de Poder Económico: Un Análisis de la Oligarquía Financiera. Lima: Editorial Horizonte. [Google Scholar]

- Banco Central del Ecuador. 2021. Información Estadística Mensual. Available online: https://contenido.bce.fin.ec/home1/estadisticas/bolmensual/IEMensual.jsp (accessed on 12 August 2021).

- Cañas, R. 2015. Caracterización de los grupos económicos en el Ecuador. Investigación Económica 8: 76–114. [Google Scholar]

- Centro de Estudios y Difusión Social (CEDIS). 1986. Los Grupos Monopólicos en el Ecuador: Un Ensayo de Difusión Popular. Accra: Centro de Estudios y Difusión Social (CEDIS). Portada. [Google Scholar]

- Chavarín, Rubén. 2011. Los grupos económicos en México a partir de una tipología de arquitectura y gobierno corporativos, Una revisión de sus explicaciones teóricas. El Trimestre Económico 30: 193–234. [Google Scholar] [CrossRef]

- Constitución de la República del Ecuador. 2008. Available online: https://www.oas.org/juridico/pdfs/mesicic4_ecu_const.pdf (accessed on 12 August 2021).

- Cueva, Agustín. 1988. El proceso de dominación política en el Ecuador. Setagaya: Planeta. [Google Scholar]

- Dahse, Fernando. 1981. Mapa de la extrema riqueza. Los grupos económicos y el proceso de concentración de capitales. NS, NorthSouth 6: 99–103. [Google Scholar] [CrossRef]

- EKOS. 2012. Los colosos de la economía nacional. EKOS Negocios 215: 28–70. [Google Scholar]

- El Comercio. 2010. 28 Entidades que Quebraron por la Crisis de 1998 Fueron Cerradas. Available online: https://www.elcomercio.com/actualidad/28-entidades-quebraron-crisis-1998.html (accessed on 12 August 2021).

- Fierro, Luis. 1991. Los Grupos Financieros en el Ecuador. Bunkyō: Centro de Educación Popular, CEDEP. [Google Scholar]

- Fierro, Luis. 2019. Financial Groups in Ecuador—25 Years Later. Revista PUCE 108: 139–75. [Google Scholar]

- Frank, Robert H. 2005. Microeconomía y Conducta. Edited by Quinta Edi. New York: McGraw-Hill. [Google Scholar]

- Furió, Elies, and Matilde Alonso. 2008. Concentración económica: Algunas consideraciones sobre su naturaleza y medida. Boletín económico de ICE, Información Comercial Española 2947: 41–54. [Google Scholar]

- Garrido, Celso, and Wilson Peres. 1996. Grandes empresas y grupos industriales latinoamericanos. Revista CEPAL 66: 127–47. [Google Scholar] [CrossRef]

- Guriev, Sergei, and Andrei Rachinsky. 2005. The Role of Oligarchs in Russian Capitalism. Journal of Economic Perspectives 19: 131–50. [Google Scholar] [CrossRef] [Green Version]

- Iturralde, Pablo. 2017. Grupo Eljuri: Paraísos Fiscales y Corruptelas: Modelo Para (Des)armar. Available online: https://lalineadefuego.info/grupo-eljuri-paraisos-fiscales-y-corruptelas-modelo-para-desarmar-por-pablo-iturralde-ruiz/ (accessed on 12 August 2021).

- Khanna, Tarun, and Yishay Yafeh. 2007. Business Groups in Emerging Markets: Paragons or Parasites? Journal of Economic Literature 45: 331–72. [Google Scholar] [CrossRef] [Green Version]

- Lagos, Ricardo. 1960. La Concentración del Poder Económico. Ph.D. Thesis, Universidad de Chile, Santiago, Chile. [Google Scholar]

- Lazzarini, Sergio G., Gary J. Miller, and Todd R. Zenger. 2008. Dealing with the Paradox of Embeddedness: The Role of Contracts and Trust in Facilitating Movement Out of Committed Relationships. Organization Science 5: 709–28. [Google Scholar] [CrossRef] [Green Version]

- Leff, Nathaniel H. 1978. Industrial Organization and Entrepreneurship in the Developing Countries: The Economic Groups. Economic Development and Cultural Change 26: 661–75. [Google Scholar] [CrossRef]

- Ley Orgánica de Regulación y Control del Poder de Mercado. 2011. Available online: https://www.planificacion.gob.ec/ley-organica-de-regulacion-y-control-del-poder-de-mercado/ (accessed on 12 August 2021).

- Llosas, Hernán. 2005. El Pensamiento Corporativo en Italia. Ph.D. Thesis, Universidad Nacional de La Plata, La Plata, Argentina. [Google Scholar]

- Manosalve, Martín. 2015. Reseñas—Schneider, Ben Ross. Hierarchical Capitalism in Latin America. Business, Labor and the Challenges of Equitable Development. Economía-Reseñas 38: 231–33. [Google Scholar]

- Marchán, Carlos. 2017. Origenes del Ecuador Republicano; Arquitectura Institucional Malograda del Estado Nacional. Quito: Editorial IAEN. [Google Scholar]

- Minaya, Manuel. 2006. Concentración Industrial en el Sector Comercio al por Menor del Ecuador: Un Análisis a Nivel de Subramas, Período 2000–2005. Quito: Pontificia Universidad Católica del Ecuador. [Google Scholar]

- Misas, Gabriel. 1975. Contribución al estudio del grado de concentración en la industria colombiana—Gabriel Misas Arango—Google Books. Edited by Tiempo Presente. Santiago de Chile: Inst. Latinoamericano de Investigaciones Sociales (ILDIS). [Google Scholar]

- Navarro, Guillermo. 1975. La Concentración de Capitales en el Ecuador. Quito: Universidad Central del Ecuador—Escuela de Sociología Editorial Universitaria. [Google Scholar]

- Navarro, Guillermo. 2006. Los Poderes Fácticos Poder Económico, Poder políTico y Poder Factico. Quito: Ediciones Zitra. [Google Scholar]

- Pástor, Carlos. 2015. Los Grupos Económicos en el Ecuador. pp. 1–82. Available online: https://repositorio.uasb.edu.ec/handle/10644/5529 (accessed on 15 July 2021).

- Peralta, Pablo Ospina. 2015. Protesta social, crisis económica y escenario político Ecuador. In Análisis de Coyuntura. Quito: Centro Ecuménico de Proyectos. [Google Scholar]

- Revista Líderes. 2017. 215 Grupos Económicos Tiene el País; 25 se Sumaron en este año. Available online: https://www.revistalideres.ec/lideres/informe-grupos-economicos-ecuador-sri.html (accessed on 15 July 2021).

- Robinson, E .A. G. 1957. La Dimensión óptima de la Empresa. Buenos Aires: El Ateneo. [Google Scholar]

- Schneider, Ben Ross. 2013. Hierarchical Capitalism: Business, Labor, and the Challenge of Equitable Development in Latin America. Cambridge: Cambridge University Press. [Google Scholar]

- Servicio de Rentas Internas del Ecuador. 2015. Reglamento Para la Aplicación de la Ley de Régimen Tributario Interno, LORTI. Quito: Servicio de Rentas Internas del Ecuador. [Google Scholar]

- Servicio de Rentas Internas del Ecuador. 2020. Catastro de Grupos Económicos 2020. Quito: Servicio de Rentas Internas del Ecuador. [Google Scholar]

- Servicio de Rentas Internas del Ecuador. 2021. Ranking of Ecuadorian Firms. Quito: Servicio de Rentas Internas del Ecuador. [Google Scholar]

- Silva, Julio. 1977. Los Verdaderos dueños del país: Oligarquía y Monopolios en Colombia—Julio Silva Colmenares—Google Books. Fondo Editorial Suramérica. Available online: https://www.worldcat.org/title/verdaderos-duenos-del-pais-oligarquia-y-monopolios-en-colombia/oclc/679746155 (accessed on 15 July 2021).

- Solano, Santiago, and Luis Tobar. 2017. Caracterización de los grupos económicos en Ecuador según el Servicio de Rentas Internas al año 2015. Observatorio Economía Latinoamericana 20. Available online: https://www.researchgate.net/publication/333659229CARACTERIZACIONDELOSGRUPOSECONOMICOSENECUADORSEGUNELSERVICIODERENTASINTERNASSRIALANO2015 (accessed on 15 July 2021).

- Strachan, Harry W. 1976. Family and Other Business Groups in Economic Development: The Case of Nicaragua. Westport: Praeger. [Google Scholar]

- Tobar, Luis, and Santiago Solano. 2017. La concentración financiero y los grupos de poder: Evidencias en la ciudad de Cuenca—Ecuador. Revista Internacional Administración y Finanzas 10: 81–90. [Google Scholar]

- Tulcanaza, Ana Belén. 2010. Concentración del Poder Económico en el Sector Comercio en Ecuador, período 2002–2008. Available online: http://repositorio.puce.edu.ec/handle/22000/742 (accessed on 15 July 2021).

- Tulcanaza-Prieto, A. 2018. Grupos Económicos Ecuatorianos: Una Mirada hacia su Comportamiento 2015–2016. Estado y Comunes—Instituto de Altos Estudios Nacionales (IAEN) 7: 181–200. [Google Scholar] [CrossRef] [Green Version]

- Tulcanaza-Prieto, A., and Younghwan Lee. 2018. Factors Associated with the Financial Performance of Commercial Firms in Ecuador. Global Business Administration Review 15: 1–26. [Google Scholar] [CrossRef]

- Tulcanaza-Prieto, Ana Belén, and Manuel Morocho-Cayamcela. 2018. Elasticity of the total production measured by the investment in information and communication technologies: Evidence from the ecuadorian manufacturing companies. X-Pedientes Económicos 2: 6–27. [Google Scholar]

- Tulcanaza-Prieto, Ana Belen, HoKyun Shin, Younghwan Lee, and Chang Won Lee. 2020. Relationship among CSR Initiatives and Financial and Non-Financial Corporate Performance in the Ecuadorian Banking Environment. Sustainability 12: 1621. [Google Scholar] [CrossRef] [Green Version]

- Unda, M., and E. Bethania. 2010. Burguesía ciudadana, nueva hegemonía, nueva alianza de clases. Revista R 69: 19–31. [Google Scholar] [CrossRef]

- Vanoni, Giuseppe, and Carlos Rodríguez. 2017. Estrategias de crecimiento implementadas por los grupos económicos del Ecuador (2007–2016). Revista Innovar Journal 27: 39–55. [Google Scholar] [CrossRef]

- Vito, Francesco. 1935. L’essenza Dell’economia Corporativa. Milano: Economía corporativa. [Google Scholar]

- Wilches, Giovanna, and Carlos Rodríguez. 2016. El proceso evolutivo de los conglomerados o grupos económicos en Colombia. Innovar 26: 11–34. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Number of Demanders | Number of Suppliers | ||

|---|---|---|---|

| One | Few | Many | |

| One | Bilateral monopoly | Partial monopsony | Monopsony |

| Few | Partial monopoly | Bilateral oligopoly | Oligopsony |

| Many | Pure monopoly | Oligopoly | Perfect competition |

| Variables | Formula / Description |

|---|---|

| Total Assets | Liabilities + Total Equity |

| Total Equity | Total Assets − Liabilities |

| Total Income | Revenue − Cost of goods sold |

| Income Tax | (Taxable base a − returns − discounts − costs − all deductions) * 25% |

| Tax Burden | (Income Tax/Total Income) * 100 |

| Total National Net Tax Collection | Total Tax Collection - credit notes − compensations − returns |

| Total Tax Collection | Sum of all Ecuadorian taxes b |

| Detail | Ranking 2017 | Ranking 2020 |

|---|---|---|

| Number of economic groups | 215 | 300 |

| Number of members of the economic group | 7126 | 9121 |

| Number of members domiciled in tax havens | 433 | 453 |

| Number of members as offshore firms (Panama Papers) a | 307 | 393 |

| Number of members related with financial institutions | 15 | 46 |

| Number of members related with media entities | 47 | 55 |

| Detail | 2015 | 2019 | Variation | |

|---|---|---|---|---|

| Income Tax | 1389 | 1772 | 382 | 27.5% |

| Total Tax Collection | 6394 | 6121 | −273 | −4.3% |

| Total Income | 60,903 | 71,744 | 10,841 | 17.8% |

| Total Assets | 95,214 | 130,262 | 35,048 | 36.8% |

| Total Debt | N.A. | 1234 | 1234 | |

| Total Equity | 35,206 | 48,216 | 13,009 | 37.0% |

| Year | Average Tax Burden | Median | Standard Deviation | Maximum |

|---|---|---|---|---|

| 2015 | 2.42 | 1.83 | 1.78 | 9.56 |

| 2019 | 2.29 | 1.64 | 2.11 | 16.17 |

| Rk. 2020 | Rk. 2019 | Rk. 2017 | Rk. 2016 | Variation 2016–2020 | Economic Group |

|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 0 | Banco Pichincha |

| 2 | 2 | 3 | 2 | 0 | Almacenes Juan Eljuri |

| 3 | 3 | 4 | 4 | 1 | Corporación Favorita |

| 4 | 4 | 2 | 5 | 1 | Schlumberger del Ecuador |

| 5 | 7 | 7 | 8 | 3 | Banco de Guayaquil |

| 6 | 6 | 6 | 7 | 1 | Produbanco |

| 7 | 5 | 5 | 3 | −4 | OCP Ecuador |

| 8 | 8 | 10 | 11 | 3 | Holdingdine Corporación Industrial y Comercial |

| 9 | 9 | 11 | 10 | 1 | Corporación El Rosado |

| 10 | 10 | 12 | 12 | 2 | Banco Bolivariano C.A. |

| 11 | 12 | 8 | 6 | −5 | Claro |

| 17 | 17 | 9 | 9 | −8 | Industria Pronaca |

| Ranking 2020 | Ranking 2019 | Ranking 2017 | Ranking 2016 | Variation 2016–2020 | Economic Group | 2015 | 2016 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 0 | Banco Pichincha | 664,261,405 | 498,739,821 | 607,395,054 | 667,872,343 |

| 2 | 2 | 2 | 2 | 0 | Dinadec | 350,974,788 | 352,100,364 | 390,791,027 | 427,107,715 |

| 3 | 3 | 3 | 4 | 1 | Produbanco | 264,294,993 | 222,306,816 | 274,261,174 | 299,941,296 |

| 4 | 5 | 7 | 8 | 4 | Banco de Guayaquil | 191,614,215 | 175,517,131 | 222,582,890 | 234,359,513 |

| 5 | 6 | 6 | 7 | 2 | Banco Bolivariano C.A. | 197,354,449 | 180,440,219 | 206,430,145 | 209,149,340 |

| 6 | 7 | 5 | 3 | −3 | Claro | 315,489,121 | 185,073,552 | 186,042,898 | 190,495,917 |

| 7 | 4 | 9 | 9 | 2 | Almacenes Juan Eljuri | 183,909,249 | 157,333,985 | 229,738,403 | 190,328,750 |

| 8 | 8 | −8 | Banco Internacional | 185,639,529 | 182,165,876 | ||||

| 9 | 9 | −9 | Arca Ecuador | 183,298,823 | 168,714,088 | ||||

| 10 | 10 | 10 | 10 | 0 | Citibank N. A., Ecuador | 179,366,431 | 144,775,146 | 179,592,586 | 166,635,702 |

| 4 | 5 | 5 | Itabsa | 239,723,714 | 205,429,092 | ||||

| 8 | 6 | 6 | Schlumberger dl Ecuador | 210,851,012 | 157,866,766 | ||||

| (a) Total Tax Collection, Top 10 Economic Groups | 2,797,839,378 | 2,279,582,892 | 2,665,772,529 | 2,736,770,540 | |||||

| (b) Total Tax Collection, Economic Groups | 6,393,835,744 | 5,499,929,764 | 6,256,788,523 | 6,120,831,840 | |||||

| (c) Total National Net Tax Collection | 12,755,076,181 | 11,309,307,282 | 12,809,502,107 | 13,180,846,182 | |||||

| (a)/(b) | 43.8% | 41.4% | 42.6% | 44.7% | |||||

| (a)/(c) | 21.9% | 20.2% | 20.8% | 20.8% | |||||

| (b)/(c) | 50.1% | 48.6% | 48.8% | 46.4% | |||||

| Economic Group | Total Income | Total Assets | Total Equity | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2015 | 2016 | 2018 | 2019 | 2015 | 2016 | 2018 | 2019 | 2015 | 2016 | 2018 | 2019 | |

| Banco Pichincha | 2055 | 2102 | 2387 | 2727 | 13,203 | 14,484 | 16,580 | 17,892 | 2658 | 2601 | 3477 | 3681 |

| Almacenes Juan Eljuri | 1894 | 1813 | 3106 | 2740 | 4294 | 4575 | 6506 | 6418 | 1244 | 1287 | 2035 | 1947 |

| Corporación Favorita | 2697 | 2508 | 2880 | 2919 | 2132 | 2245 | 2867 | 3344 | 1567 | 1690 | 2154 | 2315 |

| Schlumberger del Ecuador | 1297 | 2027 | 1724 | 1834 | 3137 | 4537 | 3968 | 3617 | 1546 | 1966 | 2397 | 2306 |

| Banco de Guayaquil | 484 | 467 | 525 | 602 | 3840 | 4190 | 4570 | 5334 | 644 | 670 | 727 | 792 |

| Produbanco | 342 | 357 | 533 | 609 | 3905 | 4324 | 4935 | 5337 | 617 | 623 | 539 | 571 |

| OCP Ecuador | 1877 | 1661 | 2013 | 1579 | 3720 | 3749 | 3771 | 3212 | 1593 | 1455 | 2004 | 1455 |

| Holdingdine | 1019 | 965 | 1030 | 2125 | 2185 | 2325 | 1693 | 1889 | 2031 | |||

| Corporación El Rosado | 1591 | 1605 | 1657 | 1635 | 1655 | 1838 | 520 | 454 | 477 | |||

| Banco Bolivariano C.A. | 289 | 342 | 3565 | 3828 | 523 | 571 | ||||||

| Claro | 1542 | 1447 | 1969 | 1968 | 521 | 555 | ||||||

| Industria Pronaca | 1754 | 1655 | 1469 | 1523 | 791 | 845 | ||||||

| (a) Total Top 10 | 15,533 | 15,057 | 16,027 | 16,039 | 39,304 | 43,720 | 50,603 | 53,145 | 11,701 | 13,386 | 16,199 | 16,145 |

| (b) Total Economic Groups | 60,903 | 57,994 | 71,455 | 71,744 | 95,214 | 102,044 | 122,032 | 130,262 | 35,206 | 36,479 | 46,525 | 48,216 |

| (a)/(b) | 25.5% | 26.0% | 22.4% | 22.4% | 41.3% | 42.8% | 41.5% | 40.8% | 33.2% | 36.7% | 34.8% | 33.5% |

| Financial Variables vs. Total Tax Collection | 2015 | 2016 | 2018 | 2019 |

|---|---|---|---|---|

| Total Income | 0.808 *** | 0.784 *** | 0.837 *** | 0.793 *** |

| Total Assets | 0.537 *** | 0.544 *** | 0.736 *** | 0.698 *** |

| Total Equity | 0.677 *** | 0.716 *** | 0.802 *** | 0.772 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tulcanaza-Prieto, A.B.; Morocho-Cayamcela, M.E. The Evolution and Takeoff of the Ecuadorian Economic Groups. Economies 2021, 9, 188. https://doi.org/10.3390/economies9040188

Tulcanaza-Prieto AB, Morocho-Cayamcela ME. The Evolution and Takeoff of the Ecuadorian Economic Groups. Economies. 2021; 9(4):188. https://doi.org/10.3390/economies9040188

Chicago/Turabian StyleTulcanaza-Prieto, Ana Belén, and Manuel Eugenio Morocho-Cayamcela. 2021. "The Evolution and Takeoff of the Ecuadorian Economic Groups" Economies 9, no. 4: 188. https://doi.org/10.3390/economies9040188

APA StyleTulcanaza-Prieto, A. B., & Morocho-Cayamcela, M. E. (2021). The Evolution and Takeoff of the Ecuadorian Economic Groups. Economies, 9(4), 188. https://doi.org/10.3390/economies9040188