Assessment of the Financial Autonomy of Rural Municipalities

Abstract

1. Introduction

2. Literature Review

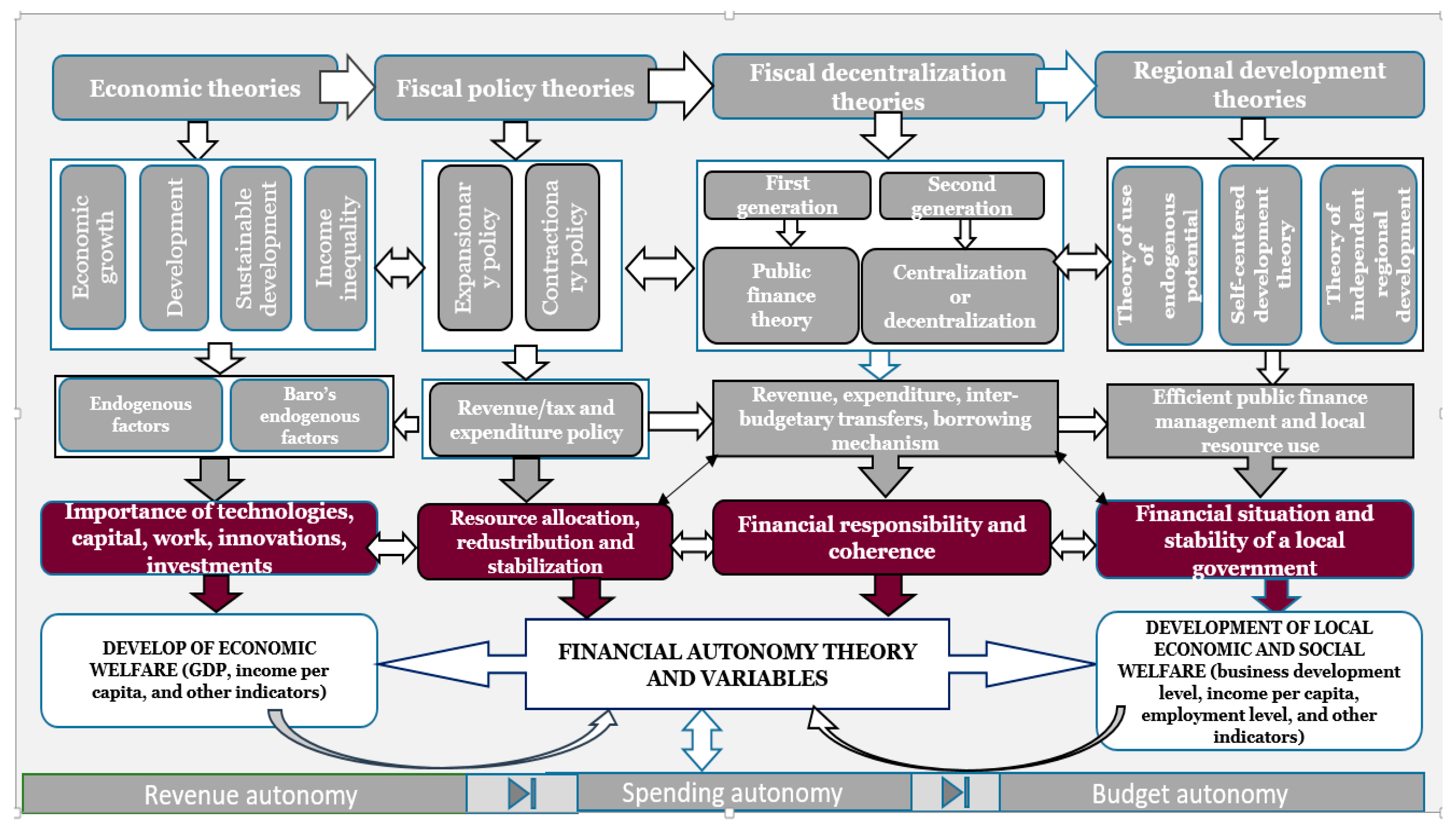

2.1. Relation between the Phenomenon of Financial Autonomy of LGUs and Economic Theories, and Complexity of the Assessment

2.2. Analysis of the Multi-Criteria Methods and Selection of the Most Appropriate Method for FA Assessment of Rural Municipalities

- is the most widely and frequently (30%) applied for assessment of the majority of phenomena, activities, compared to other methods (AHP—20%; VIKOR—6.67%, ELECTRE—16.67%; other methods—10%) (Aruldoss et al. 2013);

- is applicable to dealing with economic, financial issues in international practice;

- has been employed in the most recent empirical studies assessing FA of LGUs and, in particular, rural municipalities (Vavrek and Pukala 2019; Satoła et al. 2019; Standar and Kozera 2019; Łuczak et al. 2018a; Łuczak et al. 2018b; Głowicka-Wołoszyn and Satoła 2018; Kozera et al. 2017; Kozera and Głowicka-Wołoszyn 2016).

3. Methodology

- the municipalities with more than 50% of the population living in the rural type residential areas were considered to be rural municipalities;

- the municipalities with 15 to 50% of the population living in the rural residential areas were attributed to semi-rural municipalities.

- The indicators had been used by more than one author in their studies (Vavrek and Pukala 2019; Satoła et al. 2019; Standar and Kozera 2019; Łuczak et al. 2018a; Łuczak et al. 2018b; Głowicka-Wołoszyn and Satoła 2018; Kozera et al. 2017; Kozera and Głowicka-Wołoszyn 2016).

- Statistical data collected and published periodically were available for calculation of the indicators.

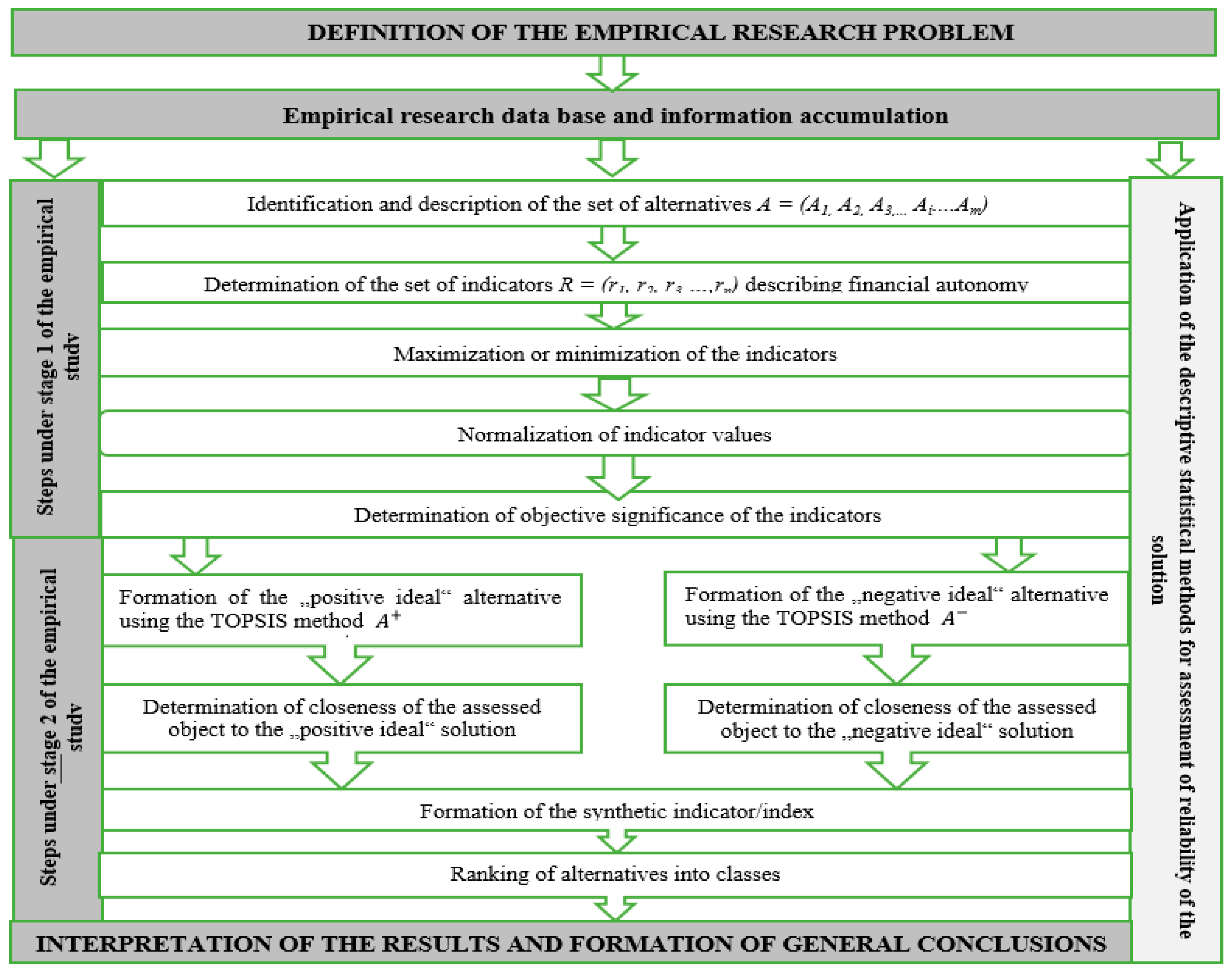

- problem formulation (definition of the problem, gathering of database and information);

- problem solving consisting of the steps comprising the first stage (decision making, formulation of the task) and second stage (task solution using the TOPSIS method) of the model design process;

- decision making in relation to the problem (interpretation of the results generated and formulation of the general conclusions).

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Aruldoss, Martin, T. Miranda Lakshmi, and V. Prasanna Venkatesan. 2013. A survey on multi criteria decision making methods and its applications. American Journal of Information Systems 1: 31–43. [Google Scholar]

- Atkočiūnienė, Vilma. 2008. Kaimo vietovės pokyčių valdymas pagal principą “iš apačios į viršų”. Ekonomika ir Vadyba: Aktualijos ir Perspektyvos 2: 50–62. (In Lithuanian). [Google Scholar]

- Beer-Tóth, Krisztina. 2009. Local Financial Autonomy in Theory and Practice. Doctoral dissertation, Université de Fribourg, Fribourg, Switzerland. [Google Scholar]

- Cigu, Elena. 2014. An aproach of local financial autonomy and implication over sustainable development in the knowledge society. Journal of Public Administration, Finance and Law 6: 44–53. [Google Scholar]

- Copus, Andrew, and Marsaili Macleod. 2006. Taking a fresh look at peripherality. In Marginality in the Twenty-first Century: Theory and Recent Trends. Edited by Gareth Jones and Walter Leimgruber. Ashgate: Aldershot. [Google Scholar]

- European Charter of Local Self-Government. 1985. Available online: https://rm.coe.int/168007a088 (accessed on 28 December 2020).

- Ginevičius, Romualdas, and Valentinas Podvezko. 2008. Daugiakriterinio vertinimo būdų suderinamumas. Business: Theory and Practice 9: 73. (In Lithuanian). [Google Scholar]

- Głowicka-Wołoszyn, Romana, and Łukasz Satoła. 2018. Financial self-sufficiency of rural communes in Poland. International Scientific Days, 1493–95. [Google Scholar]

- Hajilou, Mahran, Mohammad Mirehei, Sohrab Amirian, and Mehdi Pilehvar. 2018. Financial Sustainability of Municipalities and Local Governments in Small-Sized Cities; a Case of Shabestar Municipality. Lex Localis 16: 77–106. [Google Scholar] [CrossRef]

- Horlings, Lummina G., and Terry K. Marsden. 2014. Exploring the ‘New Rural Paradigm’ in Europe: Eco-economic strategies as a counterforce to the global competitiveness agenda. European Urban and Regional Studies 21: 4–20. [Google Scholar] [CrossRef]

- Hwang, Ching Lai, and Kwangsun Yoon. 1981. Methods for multiple attribute decision making. In Multiple Attribute Decision Making. Berlin/Heidelberg: Springer, pp. 58–191. [Google Scholar]

- Jakovljevic, Mihajlo, Melitta Jakab, Ulf Gerdtham, David McDaid, Seiritsu Ogura, Elena Varavikova, Joav Merrick, Roza Adany, Albert Okunade, and Thomas E. Getzen. 2019. Comparative financing analysis and political economy of noncommunicable diseases. Journal of Medical Economics 22: 722–27. [Google Scholar] [CrossRef]

- Jakovljevic, Mihajlo B. 2013. Resource allocation strategies in Southeastern European health policy. The European Journal of Health Economics 14: 153–59. [Google Scholar] [CrossRef]

- Jemna, Danut Vasile, Mihaela Onofrei, and C. I. G. U. Elena. 2013. Demographic and Socio-Economic Determinants of Local Financial Autonomy in Romania. Transylvanian Review of Administrative Sciences 9: 46–65. [Google Scholar]

- Kostov, Philip, and John Lingard. 2004. Integrated rural development-do we need a new approach? Paper presented by the 73 rd Seminar of the European Association of Agricultural Economists, Ancona, Italy, 28–30 June; Available online: http://clok.uclan.ac.uk/1418/1/0409006.pdf (accessed on 30 August 2020).

- Kozera, Agnieszka, Aleksandra Łuczak, and Feliks Wysocki. 2017. The Application of Classical and Positional TOPSIS Methods to Assessment Financial Self-sufficiency Levels in Local Government Units. In Data Science. Cham: Spinger, pp. 273–84. [Google Scholar]

- Kozera, Agnieszka, and Romana Głowicka-Wołoszyn. 2016. Spatial autocorrelation in assessment of financial self-sufficiency of communes of Wielkopolska province. Statistics in Transition New Series 17: 525–40. [Google Scholar]

- Kriaučiūnas, Edikas. 2018. Lietuvos kaimiškų teritorijų apgyvenimas: erdvinės transformacijos ir gyventojų gerovė. Geografijos Metrastis 51: 3–24. (In Lithuanian). [Google Scholar]

- Ladner, Andreas, and Nicolas Keuffer. 2018. Creating an index of local autonomy–theoretical, conceptual, and empirical issues. Regional & Federal Studies, 1–26. [Google Scholar] [CrossRef]

- Lietuvos Respublikos Finansų Ministerija [Ministry of Finance of the Republic of Lithuania]. 2020. Available online: http://finmin.lrv.lt/ (accessed on 28 December 2020). (In Lithuanian).

- Lietuvos Respublikos Statistikos Departamentas [Department of Statistics of the Republic of Lithuania]. 2020. Available online: https://osp.stat.gov.lt/statistiniu-rodikliu-analize#/ (accessed on 28 December 2020). (In Lithuanian)

- Lietuvos Respublikos Regioninės Plėtros Departamentas Prie Vidaus Reikalų Ministerijos [The Regional Development Department under the Ministry of the Interior of the Republic of Lithuania]. 2020. Available online: http://www.lietuvosregionai.lt/lt/8/kauno-apskritis-167;51.html (accessed on 15 November 2020). (In Lithuanian).

- Lietuvos Respublikos Valstybinė Mokesčių Inspekcija Prie Finansų Ministerijos [State Tax Inspectorate under the Ministry of Finance of the Republic of Lithuania]. 2020. Available online: https://www.vmi.lt/evmi/biudzeto-pajamos (accessed on 28 December 2020). (In Lithuanian).

- Łuczak, Aleksandra, Malgorzata Just, and Agnieszka Kozera. 2018a. Application of the positional POT-TOPSIS method to the assessment of financial self-sufficiency of local administrative units. Paper presented by the 10th Economics and Finance Conference, Rome, Italy, 10–13 September 2018; Edited by Cermakova Klara, Mozayeni Simin and Hromada Eduard. pp. 601–12. [Google Scholar] [CrossRef]

- Łuczak, Aleksandra, Agnieszka Kozera, and Silvia Bacci. 2018b. The application of taxonomic methods and ordered logit model in the assessment of financial self-sufficiency of local administrative units. Paper presented by the Economic Science for Rural Development Conference Proceedings (No. 49), Jelgava, Latvia, 9–11 May. [Google Scholar]

- Mueller, Keith J., Rebecca Slifkin, Michael D. Shambaugh-Miller, and Randy K. Randolph. 2004. Definition of rural in the context of MMA Access Standards for Prescription Drug Plans. RUPRI Center for Rural Health Policy Analysis. Available online: www. rupri. org/healthpolicy. (accessed on 6 July 2021).

- Normann, Roger Henning, and Mikaela Vasström. 2012. Municipalities as governance network actors in rural communities. European Planning Studies 20: 941–60. [Google Scholar] [CrossRef]

- Oulasvirta, Lasse, and Maciej Turala. 2009. Financial autonomy and consistency of central government policy towards local governments. International Review of Administrative Sciences 75: 311–32. [Google Scholar] [CrossRef]

- Podvezko, Valentinas. 2008. Sudėtingų dydžių kompleksinis vertinimas. Verslas: Teorija ir Praktika 9: 160–68. (In Lithuanian). [Google Scholar] [CrossRef]

- Psycharis, Yannis, Maria Zoi, and Stavroula Iliopoulou. 2016. Decentralization and local government fiscal autonomy: evidence from the Greek municipalities. Environment and Planning C: Government and Policy 34: 262–80. [Google Scholar] [CrossRef]

- Rudytė, Dalia, Dovilė Ruplienė, Lina Garšvienė, Roberta Bajorūnienė, and Solveiga Skunčikienė. 2018. Savivaldybių Fiskalinio Konkurencingumo Vertinimas Ekonominio Augimo Kontekste. Mokslo Studija. Available online: http://gs.elaba.lt/object/elaba:27762649/ (accessed on 30 August 2020). (In Lithuanian).

- Salm, Marco. 2014. Property Taxes in BRICS: Comparison and a First Draft for Performance Measurement. Available online: https://dopus.uni-speyer.de/frontdoor/deliver/index/docId/617/file/DP-079.pdf (accessed on 14 June 2021).

- Satoła, Łukasz, Aldona Standar, and Agnieszka Kozera. 2019. Financial Autonomy of Local Government Units: Evidence from Polish Rural Municipalities. Lex Localis-Journal of Local Self-Government 17: 321–42. [Google Scholar] [CrossRef]

- Shah, Anwar. 1994. The Reform of Intergovernmental Fiscal Relations in Developing and Emerging Market Economies. Washington: The World Bank. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.469.275&rep=rep1&type=pdf (accessed on 16 June 2021).

- Scutariu, Adrina Liviu, and Petronela Scutariu. 2015. The link between financial autonomy and local development. The case of Romania. Procedia Economics and Finance 32: 542–49. [Google Scholar] [CrossRef][Green Version]

- Simanavičienė, Rūta. 2016. The sensitivity of method TOPSIS with respect to the normalization rules. Lietuvos Matematikos Rinkinys 57: 71–76. [Google Scholar]

- Simanavičienė, Rūta. 2011. Kiekybinių Daugiatikslių Sprendimo Priėmimo Metodų Jautrumo Analizė. Doctoral dissertation, Vilnius Gediminas Technical University, Vilnius, Lithuania. (In Lithuanian). [Google Scholar]

- Skauronė, Laima, Astrida Miceikienė, and Ričardas Krikštolaitis. 2020. The Impact of Fiscal Policy Measures on the Financial Autonomy of Rural Municipalities: Case of Lithuania. Paper presented by the Entrenova-Enterprise Research Innovation Conference (Online), Janičić, Radmila, 22 September, vol. 6, pp. 157–72. [Google Scholar]

- Slavinskaitė, Neringa. 2017. Šalies fiskalinės decentralizacijos vertinimas. Doctoral dissertation, Vilnius Gediminas Technical University, Vilnius, Lithuania. (In Lithuanian). [Google Scholar]

- Standar, Aldona, and Agnieszka Kozera. 2019. The Role of Local Finance in Overcoming Socioeconomic Inequalities in Polish Rural Areas. Sustainability 11: 5848. [Google Scholar] [CrossRef]

- Vavrek, Roman, and Ryszard Pukala. 2019. Topsis Technique in Self-Government–Case Study of Košice Region. MATEC Web of Conferences 297: 08001, EDP Sciences. [Google Scholar] [CrossRef]

- Vidickienė, Dalia, and Rasa Melnikienė. 2008. Lietuvos kaimiškųjų regionų kaip gyvenamosios vietos patrauklumo vertinimas. Žemės Ūkio Mokslai 15: 51–59. (In Lithuanian). [Google Scholar]

- Ward, Neil, and David. L. Brown. 2009. Placing the rural in regional development. Regional Studies 43: 1237–44. [Google Scholar] [CrossRef]

- Zavadskas, Edmundas Kazimieras, Zenonas Turskis, and Simona Kildienė. 2014. State of art surveys of overviews on MCDM/MADM methods. Technological and Economic Development of Economy 20: 165–79. [Google Scholar] [CrossRef]

- Žukovskis, Jan, Daiva Urmonienė, and Rasa Jodenytė. 2013. Savivaldos institucijų įtaka kaimo raidai, taikant institucinės priklausomybės modelį. Kaimo Raidos Kryptys Žinių Visuomenėje: Mokslo Darbai, 84–94. Available online: https://www.vdu.lt/cris/handle/20.500.12259/86761 (accessed on 6 July 2021). (In Lithuanian).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors, Year | Satoła, Standar, Kozera, 2019 | Standar, Kozera, 2019 | Glowicka-Woloszyn, Satola, 2018 | Luczak, Kozera, Bacci, 2018 | Kozera, Łuczak, Wysocki, 2017 | A.L. Scutariu, P. Scutariu, 2015 | Jemna, Onofre, Cigu, 2013 |

|---|---|---|---|---|---|---|---|

| Number of indicators, units | 7 | 7 | 11 | 8 | 9 | 2 | 5 |

| Attributes | Multi-Criteria, Multi-Attribute Quantitative Methods | |||||||

|---|---|---|---|---|---|---|---|---|

| AHP | Fuzzy | ELECTRE | TOPSIS | PROMETHE | SAW | VIKOR | COPRAS | |

| International practice for addressing economic objectives | Not applicable | Applicable | Applicable | Applicable | Not applicable | Applicable | Applicable | Applicable |

| Measurement dimensions for different criteria | Available | Available | Not available | Available | Available | Available | Not available | Not available |

| Complexity of the method | Average | Average | Very complex | Complex | Complex | Simple | Complex | Simple |

| Objective structure | Hierarchic | Linear | Linear | Linear Non-linea Vector | Linear Non-linear | Linear | Linear | Linear |

| Assessment of qualitative criteria | Available | Available | Available | Available | - | Available | Available | Available |

| Assessment of quantitative criteria | Not available | Not available | Available | Available | Available | Available | Available | Available |

| Method for identification of the best alternative | T. Saaty method | Alternatives priority | Dominant relationship | Closeness to the ideal solution | Alternatives priority | Weighted | Closeness to the ideal solution | Proportionate |

| Labour costs | Average | Average | High | High | High | Low | High | Low |

| Class/Cluster | Financial Autonomy Level | Mathematical Value |

|---|---|---|

| Class I/cluster | High | + S (16) |

| Class II/cluster | Medium high | Ki+ S (17) |

| Class III/cluster | Medium low | Ki < M (18) |

| Class IV/cluster | Low level | Ki S (19) |

| Indicator, Unit of Measure | Indicator Designation | Indicator Calculation Methodology | Direction of the Indicator Value |

|---|---|---|---|

| PIT per capita, EUR | r1 | PIT transferred into the municipal budget/population of the municipality | Maximizing |

| Fiscal wealth index or tax revenues per capita, EUR | r2 | Tax revenue/population of the municipality | Maximizing |

| PIT (%) in the total municipality revenues | r3 | PIT transferred into the municipal budget/total municipal revenues × 100% | Maximizing |

| Own revenues per capita, EUR | r4 | Own municipal revenues/population of the municipality | Maximizing |

| Share of own revenues in total revenues (%) | r5 | Own municipal revenues/population of the municipality × 100% | Maximizing |

| Index of financial autonomy, 1st degree/share of own revenues in total revenues, (%) | r6 | Own municipal revenues/total municipal revenues × 100% | Maximizing |

| Non-tax revenues per capita, EUR | r7 | Municipal non-tax revenues/population of the municipality | Maximizing |

| Share of grants in the total municipal revenues or State intervention ratio (%). | r8 | Transfers from the state budget (grants)/total municipal revenues × 100% | Minimizing |

| Transfers per capita, EUR | r9 | Transfers from the state budget (grants)/population of the municipality | Minimizing |

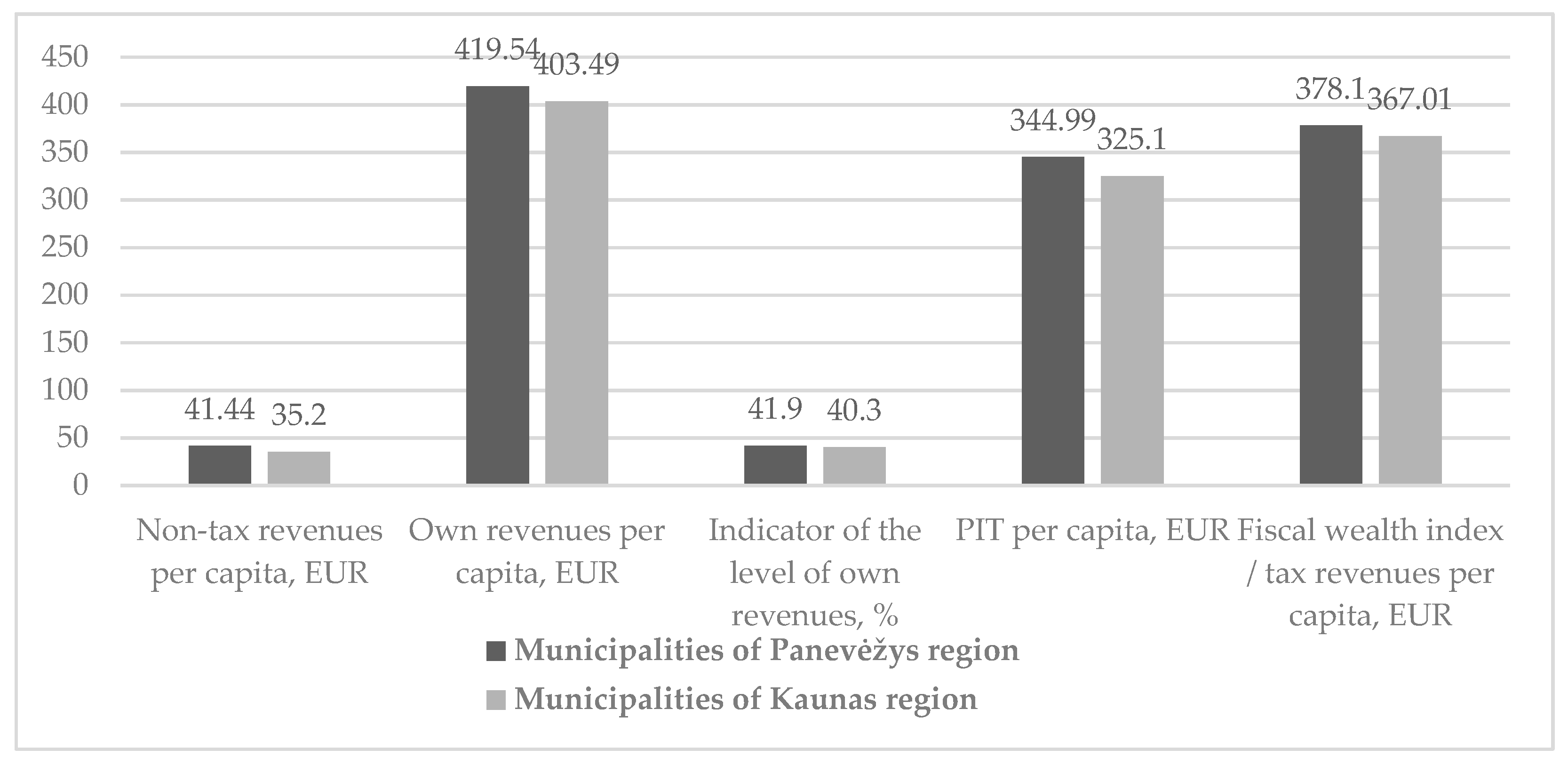

| Indicator | Mean | Median | Standard Deviation | Min | Max |

|---|---|---|---|---|---|

| PIT per capita, Eur | 344.99 | 294.71 | 121.02 | 221.04 | 591.69 |

| Fiscal wealth index or tax revenue per capita, Eur | 378.10 | 327.18 | 129.43 | 236.38 | 651.05 |

| PIT (%) in the municipality revenues | 40.64 | 40.85 | 6.28 | 30.33 | 54.65 |

| Own revenues per capita, Eur | 419.55 | 359.64 | 149.04 | 257.35 | 754.66 |

| Share of own revenues in total revenues (%) | 41.95 | 35.96 | 14.90 | 25.73 | 75.47 |

| Index of financial autonomy, 1st degree/share of own revenues in total revenues, (%) | 49.30 | 49.40 | 6.96 | 38.30 | 63.76 |

| Non-tax revenues per capita, Eur | 41.44 | 33.17 | 22.14 | 13.06 | 108.73 |

| Share of grants in the total municipal revenues or State intervention ratio, (%) | 50.71 | 50.60 | 6.96 | 36.14 | 61.70 |

| Transfer per capita, Eur | 412.74 | 403.15 | 64.69 | 273.24 | 625.05 |

| Indicator | Mean | Median | Standard Deviation | Min | Max |

|---|---|---|---|---|---|

| PIT per capita, Eur | 325.11 | 290.94 | 107.71 | 207.52 | 535.13 |

| Fiscal wealth index or tax revenue per capita, Eur | 367.01 | 331.27 | 110.42 | 227.26 | 595.80 |

| PIT (%) in the municipality revenues | 41.84 | 41.82 | 6.68 | 31.47 | 55.99 |

| Own revenues per capita, Eur | 403.50 | 365.43 | 128.99 | 244.80 | 685.65 |

| Share of own revenues in total revenues (%) | 40.35 | 36.54 | 12.90 | 24.48 | 68.57 |

| Index of financial autonomy, 1st degree/share of own revenues in total revenues, (%) | 51.87 | 51.92 | 6.47 | 40.19 | 63.95 |

| Non-tax revenues per capita, Eur | 35.91 | 27.20 | 22.07 | 14.90 | 121.07 |

| Share of grants in the total municipal revenues or State intervention ratio, (%) | 48.13 | 48.02 | 6.47 | 36.05 | 59.81 |

| Transfer per capita, Eur | 366.83 | 377.97 | 88.02 | 214.93 | 615.95 |

| Indicator Alternative | r1 | r2 | r3 | r4 | r5 | r6 | r7 | r8 | r9 |

|---|---|---|---|---|---|---|---|---|---|

| Indicator variation level (dj) | |||||||||

| Rural municipalities of Panevėžys region | |||||||||

| A1 | 0.0246 | 0.0241 | 0.0037 | 0.0243 | 0.0243 | 0.0034 | 0.0292 | 0.0038 | 0.0022 |

| A2 | 0.0248 | 0.0210 | 0.0041 | 0.0227 | 0.0227 | 0.0033 | 0.0457 | 0.0024 | 0.0042 |

| A3 | 0.0209 | 0.0198 | 0.0043 | 0.0216 | 0.0216 | 0.0043 | 0.0626 | 0.0055 | 0.0014 |

| A4 | 0.0244 | 0.0238 | 0.0042 | 0.0252 | 0.0252 | 0.0041 | 0.0389 | 0.0038 | 0.0017 |

| A5 | 0.0243 | 0.0241 | 0.0033 | 0.0258 | 0.0258 | 0.0037 | 0.0430 | 0.0038 | 0.0022 |

| Rural municipalities of Kaunas region | |||||||||

| A6 | 0.0209 | 0.0129 | 0.0040 | 0.0135 | 0.0135 | 0.0012 | 0.0270 | 0.0016 | 0.0039 |

| A7 | 0.0220 | 0.0211 | 0.0023 | 0.0207 | 0.0207 | 0.0021 | 0.0165 | 0.0035 | 0.0064 |

| A8 | 0.0217 | 0.0180 | 0.0026 | 0.0230 | 0.0230 | 0.0029 | 0.0809 | 0.0026 | 0.0022 |

| A9 | 0.0213 | 0.0182 | 0.0027 | 0.0210 | 0.0210 | 0.0024 | 0.0612 | 0.0019 | 0.0022 |

| Weight of objective significance of the indicator (qj) | |||||||||

| Rural municipalities of Panevėžys region | |||||||||

| A1 | 0.1761 | 0.1729 | 0.0268 | 0.1740 | 0.1740 | 0.0241 | 0.2095 | 0.0270 | 0.0155 |

| A2 | 0.1643 | 0.1393 | 0.0271 | 0.1506 | 0.1506 | 0.0217 | 0.3026 | 0.0160 | 0.0278 |

| A3 | 0.1290 | 0.1224 | 0.0266 | 0.1334 | 0.1334 | 0.0263 | 0.3865 | 0.0338 | 0.0084 |

| A4 | 0.1615 | 0.1570 | 0.0279 | 0.1663 | 0.1663 | 0.0273 | 0.2572 | 0.0253 | 0.0112 |

| A5 | 0.1555 | 0.1545 | 0.0214 | 0.1654 | 0.1654 | 0.0238 | 0.2754 | 0.0241 | 0.0143 |

| Rural municipalities of Kaunas region | |||||||||

| A6 | 0.2123 | 0.1314 | 0.0409 | 0.1369 | 0.1369 | 0.0118 | 0.2744 | 0.0158 | 0.0396 |

| Alternatives | Panevėžys Region | Kaunas Region | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Year | A1 | A2 | A3 | A4 | A5 | A6 | A7 | A8 | A9 |

| 2009 | 0.4507 | 0.4062 | 0.3785 | 0.4842 | 0.4442 | 0.3951 | 0.5026 | 0.3641 | 0.407 |

| 2010 | 0.4610 | 0.4125 | 0.3279 | 0.4586 | 0.4371 | 0.3723 | 0.5181 | 0.3260 | 0.333 |

| 2011 | 0.4655 | 0.4016 | 0.3133 | 0.4223 | 0.3975 | 0.3776 | 0.5270 | 0.3358 | 0.324 |

| 2012 | 0.5068 | 0.4277 | 0.3642 | 0.4360 | 0.4285 | 0.4820 | 0.5297 | 0.3623 | 0.351 |

| 2013 | 0.4594 | 0.3588 | 0.3277 | 0.3765 | 0.4055 | 0.4669 | 0.5212 | 0.3566 | 0.359 |

| 2014 | 0.5095 | 0.3818 | 0.3331 | 0.4130 | 0.4250 | 0.4309 | 0.5130 | 0.3045 | 0.339 |

| 2015 | 0.5282 | 0.4199 | 0.3367 | 0.4347 | 0.4367 | 0.4176 | 0.5183 | 0.3098 | 0.349 |

| 2016 | 0.5240 | 0.3965 | 0.3404 | 0.4343 | 0.3913 | 0.4312 | 0.5071 | 0.3101 | 0.345 |

| 2017 | 0.5254 | 0.4023 | 0.3486 | 0.4477 | 0.4179 | 0.4420 | 0.5113 | 0.3104 | 0.338 |

| 2018 | 0.4649 | 0.3466 | 0.3016 | 0.4052 | 0.3933 | 0.3956 | 0.5064 | 0.2920 | 0.304 |

| 2019 | 0.4596 | 0.3547 | 0.2959 | 0.3891 | 0.3705 | 0.3821 | 0.5051 | 0.2884 | 0.302 |

| Financial Autonomy Level | Boundaries of the Synthetic Indicator | Distribution of the Municipalities of Panevėžys Region | Distribution of the Municipalities of Kaunas Region |

|---|---|---|---|

| I (high) | [0.719; 1.00) | ||

| II (medium high) | [0.508; 0.719) | ||

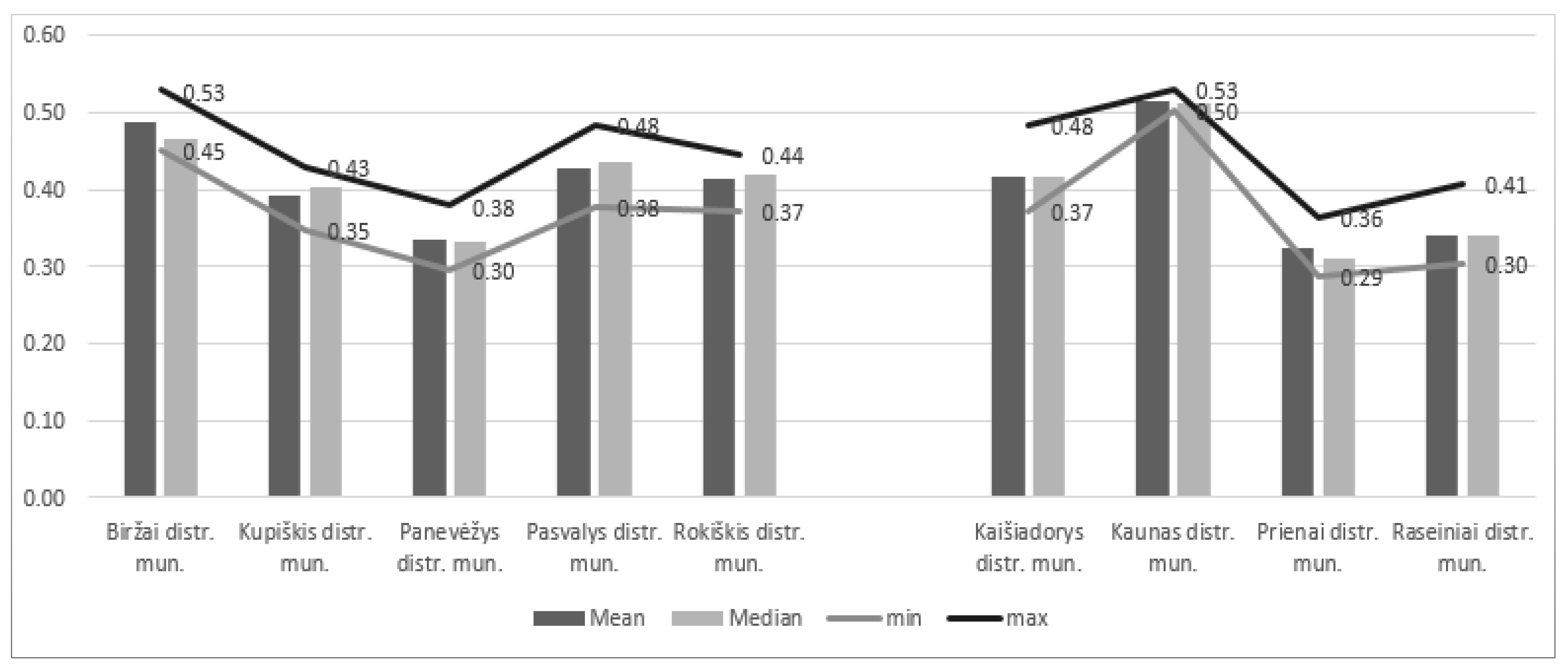

| III (medium low) | [0.297; 0.508) | Biržai distr. mun., Pasvalys distr. mun., Rokiškis distr. mun.; Kupiškis distr. mun.; Panevėžys distr. mun. | Kaišiadorys distr. mun.; Kaunas distr. mun.; Prienai distr. mun.; Raseiniai distr. mun. |

| IV (low) | [0.00; 0.297) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miceikienė, A.; Skauronė, L.; Krikštolaitis, R. Assessment of the Financial Autonomy of Rural Municipalities. Economies 2021, 9, 105. https://doi.org/10.3390/economies9030105

Miceikienė A, Skauronė L, Krikštolaitis R. Assessment of the Financial Autonomy of Rural Municipalities. Economies. 2021; 9(3):105. https://doi.org/10.3390/economies9030105

Chicago/Turabian StyleMiceikienė, Astrida, Laima Skauronė, and Ričardas Krikštolaitis. 2021. "Assessment of the Financial Autonomy of Rural Municipalities" Economies 9, no. 3: 105. https://doi.org/10.3390/economies9030105

APA StyleMiceikienė, A., Skauronė, L., & Krikštolaitis, R. (2021). Assessment of the Financial Autonomy of Rural Municipalities. Economies, 9(3), 105. https://doi.org/10.3390/economies9030105