Islamic Financial Depth, Financial Intermediation, and Sustainable Economic Growth: ARDL Approach

Abstract

1. Introduction

2. Literature Review

2.1. Islamic Financial Sector and Economic Growth

2.2. Financial Stability and Economic Growth

2.3. Islamic Finance-Growth Nexus

3. Data and Research Methods

3.1. Data

3.2. Model Specification

4. Empirical Results and Discussion

4.1. Bounds Testing

4.2. Long Run Elasticities and Granger Causality

4.3. Short Run and ECM

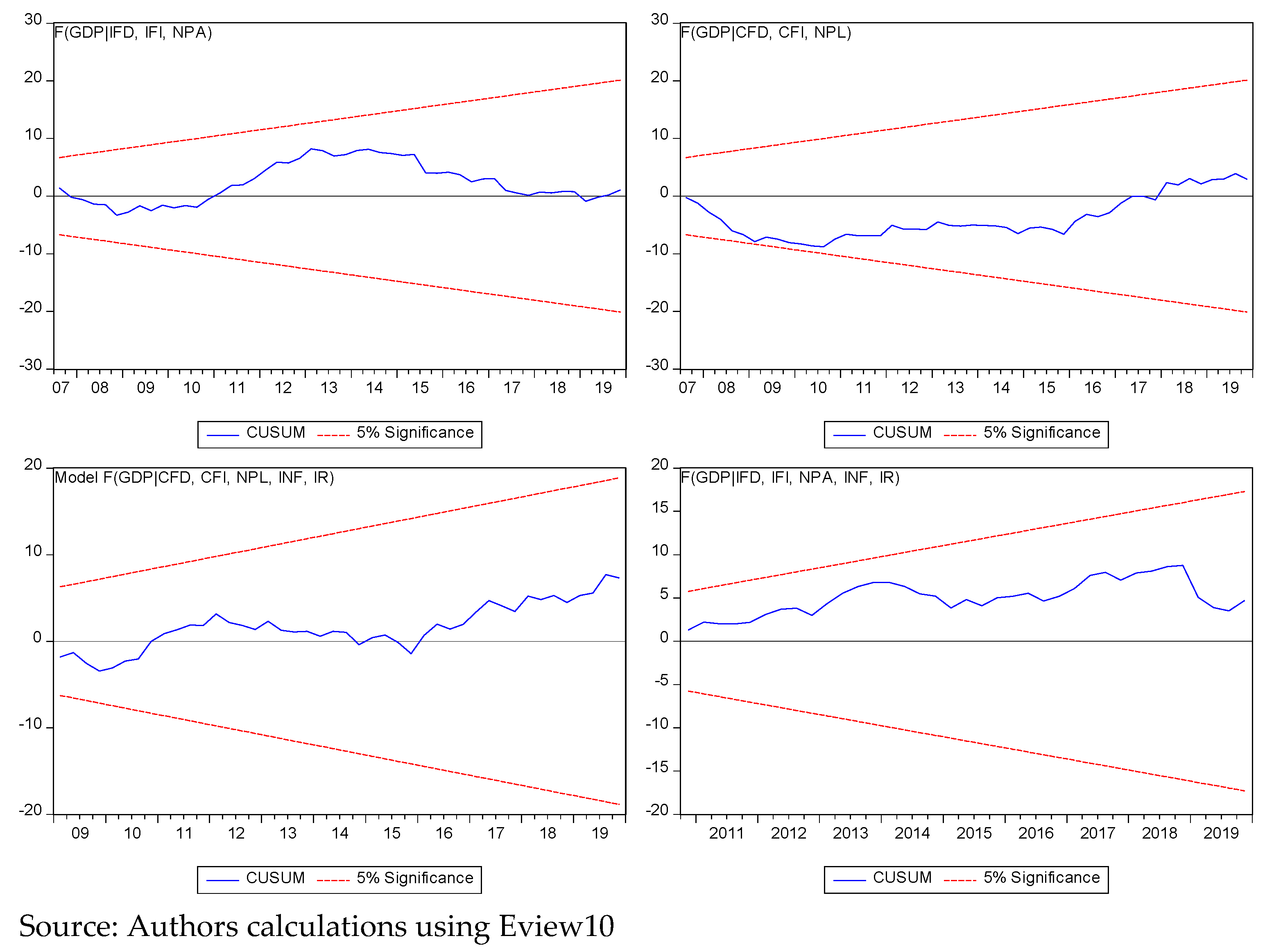

4.4. Robustness and Reliability

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Authors | Dependent Variable | Independent Variable | Model |

|---|---|---|---|

| Hachicha and Amar (2015) | Real GDP | Private = Islamic bank loans/total loan. PRIVIS = Islamic bank loans/GDP. ENVIS = Islamic bank loans/investment. Capital = GFCF. Labor force. | Engle and Granger Cointegration model (Engle and Granger 1987). |

| Shah and Raza (2020) | Real GDP | Total Islamic banking financing. Broad money. GFCF. Labor force. Trade openness. | Ordinary least square (OLS) method, and Granger causality test |

| Anwar et al. (2020) | Real GDP | Total deposit/GDP Total financing/GDP No of branches | ARDL 1, VECM 2, VDCs 3, IRFs 4 |

| Boukhatem and Moussa (2018) | Real GDP | Islamic banking development = loans/GDP. GDP per capita. Inflation. Education and human index. Government dxpenditure. Trade openness. Domestic loans to private sector/GDP. Rule of law. Regulatory quality. | Pedroni and Westerlund Panel Cointegration |

| Elmawazini et al. (2020) | GDP Per capita | Islamic banks financing/GDP. Conventional bank financing/GDP. Total financing/GDP. Interaction of rule of law. | Cross-sectionally Correlated and timewise autoregressive (CCTA) model |

| Zarrouk et al. (2017) | GDP Per capita | Financial depth = M2/GDP Financial intermediation = credit by financial sector/GDP Banking development = credit by banks/GDP Islamic banking development = Islamic financial investment/GDP. | Bivariate vector autoregressive model |

| Farahani and Dastan (2013) | Real GDP | Islamic financing GFCF Trade openness | ARDL 1, ECM 5, VAR 6 |

| Kassim (2016) | Industrial production index | Total deposit of Islamic banks Total financing of Islamic banks GFCF Government expenditure Trade openness Inflation | Engle and Granger cointegration model (Engle and Granger 1987). |

| Abduh and Omar (2012) | Ln of GDP | Ln of Deposit Ln of Financing/loans | ARDL 1, ECM 5 |

| Asif et al. (2014) | Real GDP | Advances Inflation Interest rate FDI | ARDL 1 |

| Abedifar et al. (2016) | GDP Per capita | Deposit/GDP Total deposit in the financial system Private credit/GDP Inequality and poverty = GINI index Islamic banking share | Panel Regression |

| Yusof and Bahlous (2013) | GDP Per capita | Loan/GDP Stock market development = stock/GDP GFCF/GDP Trade openness | Pedroni Panel Cointegration VDCs 3 IRFs 4 |

| Furqani and Mulyany (2009) | GDP, GFCF, TRADE | Islamic banks total financing | VECM 2 |

| Model Specification | F(IFD|GDP, IFI, NPA, INF, IR) 1 | F(IFI|GDP, IFD, NPA, INF, IR) 2 | F(NPA|GDP, IFD, IFI, INF, IR) 3 | F(INF|GDP, IFD, IFI, NPA, IR) 4 | F(IR|GDP, IFD, IFI, NPA, INF) 5 |

|---|---|---|---|---|---|

| Bounds Tests | |||||

| F-Statistics | 4.619 * | 7.477 * | 4.593 * | 2.393 | 6.751 * |

| Asymptotic Value | K-5 | K-5 | K-5 | K-5 | K-5 |

| I(0) | I(1) | I(0) | I(1) | I(0) | I(1) |

| 3.41 | 4.68 | 3.41 | 4.68 | 3.41 | 4.68 |

| 2.62 | 3.79 | 2.62 | 3.79 | 2.62 | 3.79 |

| 2.26 | 3.35 | 2.26 | 3.35 | 2.26 | 3.35 |

| Diagnostic tests | |||||

| LM BG χ2 | 0.932 | 0.060 | 0.558 | 0.245 | 0.188 |

| Ramsey RESET χ2 | 0.537 | 0.081 | 0.827 | 0.068 | 0.658 |

| JB χ2 | 0.527 | 0.045 | 0.163 | 0.993 | 0.182 |

| LM BP χ2 | 0.777 | 0.107 | 0.436 | 0.374 | 0.718 |

| Pairwise Granger causality test | |||||

| F statistics | Prob | Direction | |||

| IFD→ | GDP | 17.025 | 0.000 | IFD → GDP | |

| GDP→ | IFD | 2.379 | 0.102 | ||

| IFI→ | GDP | 1.829 | 0.170 | GDP → IFI | |

| GDP→ | IFI | 3.607 | 0.034 | ||

| NPA→ | GDP | 3.260 | 0.046 | NPA → GDP | |

| GDP→ | NPA | 0.208 | 0.813 | ||

| INF→ | GDP | 5.970 | 0.004 | INF ⇌ GDP | |

| GDP→ | INF | 7.768 | 0.001 | ||

| IR→ | GDP | 1.599 | 0.212 | IR — GDP | |

| GDP→ | IR | 0.240 | 0.787 | ||

| IFI→ | IFD | 0.484 | 0.619 | IFI — IFD | |

| IFD → | IFI | 0.907 | 0.410 | ||

| NPA→ | IFD | 0.778 | 0.464 | NPA — IFD | |

| IFD→ | NPA | 0.307 | 0.737 | ||

| INF→ | IFD | 2.076 | 0.136 | IFD → INF | |

| IFD→ | INF | 10.759 | 0.000 | ||

| IR→ | IFD | 6.461 | 0.003 | IR → IFD | |

| IFD→ | IR | 0.629 | 0.537 | ||

| NPA→ | IFI | 1.642 | 0.203 | NPA — IFI | |

| IFI→ | NPA | 1.067 | 0.351 | ||

| INF→ | IFI | 1.134 | 0.329 | IFI — INF | |

| IFI→ | INF | 3.194 | 0.049 | ||

| IR→ | IFI | 1.545 | 0.223 | IR — INF | |

| IFI→ | IR | 0.403 | 0.671 | ||

| INF→ | NPA | 1.071 | 0.349 | INF — NPA | |

| NPA→ | INF | 1.046 | 0.359 | ||

| IR→ | NPA | 8.709 | 0.001 | IR → NPA | |

| NPA→ | IR | 0.188 | 0.829 | ||

| IR→ | INF | 2.748 | 0.073 | INF → IR | |

| INF→ | IR | 3.338 | 0.043 | ||

| Model Specification | F(CFD|GDP, CFI, NPA, INF, IR) 1 | F(CFI|GDP, CFD, NPA, INF, IR) 2 | F(NPL|GDP, CFD, CFI, INF, IR) 3 | F(INF|GDP, CFD, CFI, NPA, IR) 4 | F(IR|GDP, CFD, CFI, NPA, INF) 5 |

|---|---|---|---|---|---|

| Bound Tests | |||||

| F-Statistics | 3.289 * | 2.249 | 5.369 * | 2.357 | 6.792 * |

| Asymptotic Value | k-5 | k-5 | k-5 | k-5 | k-5 |

| I(0) | I(1) | I(0) | I(1) | I(0) | I(1) |

| 3.41 | 4.68 | 3.41 | 4.68 | 3.41 | 4.68 |

| 2.62 | 3.79 | 2.62 | 3.79 | 2.62 | 3.79 |

| 2.26 | 3.35 | 2.26 | 3.35 | 2.26 | 3.35 |

| Diagnostic tests | |||||

| LM BG χ2 | 0.513 | 0.163 | 0.989 | 0.193 | 0.352 |

| Ramsey RESET χ2 | 0.536 | 0.060 | 0.141 | 0.991 | 0.859 |

| JB χ2 | 0.829 | 0.804 | 0.356 | 0.806 | 0.868 |

| LM BP χ2 | 0.097 | 0.120 | 0.385 | 0.974 | 0.139 |

| Pairwise Granger causality test | |||||

| F statistics | Prob | Direction | |||

| CFD→ | GDP | 4.052 | 0.023 | CFD → GDP | |

| GDP→ | CFD | 2.733 | 0.074 | ||

| CFI→ | GDP | 6.103 | 0.004 | GDP ⇌ CFI | |

| GDP→ | CFI | 10.484 | 0.000 | ||

| NPL→ | GDP | 1.516 | 0.229 | NPL — GDP | |

| GDP→ | NPL | 1.582 | 0.215 | ||

| INF→ | GDP | 5.970 | 0.005 | INF ⇌ GDP | |

| GDP→ | INF | 7.768 | 0.001 | ||

| IR→ | GDP | 1.599 | 0.212 | IR — GDP | |

| GDP→ | IR | 0.240 | 0.787 | ||

| CFI → | CFD | 0.528 | 0.593 | CFI — CFD | |

| CFD→ | CFI | 1.646 | 0.203 | ||

| NPL→ | CFD | 3.586 | 0.035 | NPL → CFD | |

| CFD→ | NPL | 2.592 | 0.084 | ||

| INF → | CFD | 0.161 | 0.852 | INF → CFD | |

| CFD→ | INF | 8.239 | 0.001 | ||

| IR→ | CFD | 3.640 | 0.033 | IR → CFD | |

| CFD→ | IR | 0.433 | 0.651 | ||

| NPL→ | CFI | 0.272 | 0.763 | NPL — CFI | |

| CFI→ | NPL | 1.001 | 0.375 | ||

| INF→ | CFI | 3.405 | 0.041 | INF → CFI | |

| CFI→ | INF | 2.661 | 0.079 | ||

| IR→ | INF | 0.648 | 0.527 | IR — INF | |

| INF→ | IR | 1.026 | 0.366 | ||

| INF→ | NPL | 1.537 | 0.225 | INF — NPL | |

| NPL→ | INF | 0.381 | 0.685 | ||

| IR→ | NPL | 7.256 | 0.001 | IR → NPL | |

| NPL→ | IR | 1.758 | 0.182 | ||

| IR→ | INF | 2.748 | 0.073 | INF → IR | |

| INF→ | IR | 3.338 | 0.043 | ||

References

- Abd. Majid, M. Shabri, and Salina H. Kassim. 2015. Assessing the contribution of Islamic finance to economic growth. Journal of Islamic Accounting and Business Research 6: 292–310. [Google Scholar] [CrossRef]

- Abduh, Muhamad, and Mohd Azmi Omar. 2012. Islamic banking and economic growth: The Indonesian experience. International Journal of Islamic and Middle Eastern Finance and Management 5: 35–47. [Google Scholar] [CrossRef]

- Abedifar, Pejman, Iftekhar Hasan, and Amine Tarazi. 2016. Finance-growth nexus and dual-banking systems: Relative importance of Islamic banks. Journal of Economic Behavior & Organization 132: 198–215. [Google Scholar] [CrossRef]

- Adeniyi, Oluwatosin, Abimbola Oyinlola, Olusegun Omisakin, and Festus O Egwaikhide. 2015. Financial development and economic growth in Nigeria: Evidence from threshold modelling. Economic Analysis and Policy 47: 11–21. [Google Scholar] [CrossRef]

- Adnan Hye, Qazi Muhammad, and Faridul Islam. 2013. Does financial development hamper economic growth: Empirical evidence from Bangladesh. Journal of Business Economics and Management 14: 558–82. [Google Scholar] [CrossRef]

- Ali, Mohsin, and Wajahat Azmi. 2017. Impact of Islamic Banking on Economic Growth and Volatility: Evidence from the OIC Member Countries Islamic Banking. Berlin: Springer, pp. 15–32. [Google Scholar]

- Al-Jarrah, Idries, and Philip Molyneux. 2006. Cost efficiency, scale elasticity and scale economies in arab banking. Banks & Bank Systems 1: 60–89. [Google Scholar]

- Alsamara, Mouyad, Zouhair Mrabet, Shaif Jarallah, and Karim Barkat. 2019. The switching impact of financial stability and economic growth in Qatar: Evidence from an oil-rich country. The Quarterly Review of Economics and Finance 73: 205–16. [Google Scholar] [CrossRef]

- Anwar, Suhardi M., Junaidi Junaidi, Salju Salju, Ready Wicaksono, and Mispiyanti Mispiyanti. 2020. Islamic bank contribution to Indonesian economic growth. International Journal of Islamic and Middle Eastern Finance and Management, 13. [Google Scholar] [CrossRef]

- Asif, Muhammad, Iqbal Ather, and Zaighum Isma. 2014. Impact of islamic investment trend on economic growth-A Case Study of Pakistan. Research Journal of Management Sciences 3: 8–17. [Google Scholar]

- Baber, Hasnan. 2018. How crisis-proof is Islamic finance? Qualitative Research in Financial Markets 10: 415–26. [Google Scholar] [CrossRef]

- Batuo, Michael, Kupukile Mlambo, and Simplice Asongu. 2018. Linkages between financial development, financial instability, financial liberalisation and economic growth in Africa. Research in International Business and Finance 45: 168–79. [Google Scholar] [CrossRef]

- Boukhatem, Jamel, and Fatma Ben Moussa. 2018. The effect of Islamic banks on GDP growth: Some evidence from selected MENA countries. Borsa Istanbul Review 18: 231–47. [Google Scholar] [CrossRef]

- Chandler, Nick, Balazs Heidrich, and Richard Kasa. 2017. Everything changes? A repeated cross-sectional study of organisational culture in the public sector. Evidence-Based HRM 5: 283–96. [Google Scholar] [CrossRef]

- Chapra, M. Umer. 2008. Ibn Khaldun’s theory of development: Does it help explain the low performance of the present-day Muslim world? The Journal of Socio-Economics 37: 836–63. [Google Scholar] [CrossRef]

- Cheng, Michael, Lorraine Chung, Chi-Sang Tam, Raymond Yuen, Simon Chan, and Ip-Wing Yu. 2012. Tracking the Hong Kong Economy. Occasional Paper 3: 1–29. [Google Scholar]

- Chowdhury, Mohammad Ashraful Ferdous, Chowdhury Shahed Akbar, and Mohammad Shoyeb. 2018. Nexus between risk sharing vs non-risk sharing financing and economic growth of Bangladesh. Managerial Finance 44: 739–58. [Google Scholar] [CrossRef]

- Čihák, Martin, and Klaus Schaeck. 2010. How well do aggregate prudential ratios identify banking system problems? Journal of Financial Stability 6: 130–44. [Google Scholar] [CrossRef]

- Creel, Jérôme, Paul Hubert, and Fabien Labondance. 2015. Financial stability and economic performance. Economic Modelling 48: 25–40. [Google Scholar] [CrossRef]

- Demirguc-Kunt, Asli, Luc Laeven, and Ross Levine. 2003. Regulations, Market Structure, Institutions, and the Cost of Financial Intermediation (0898-2937). Available online: https://www.nber.org/papers/w9890 (accessed on 21 January 2021).

- Duprey, Thibaut, Benjamin Klaus, and Tuomas Peltonen. 2017. Dating systemic financial stress episodes in the EU countries. Journal of Financial Stability 32: 30–56. [Google Scholar] [CrossRef]

- Elmawazini, Khaled, Khiyar Abdullah Khiyar, and Asiye Aydilek. 2020. Types of banking institutions and economic growth. International Journal of Islamic and Middle Eastern Finance and Management 13: 553–78. [Google Scholar] [CrossRef]

- Engle, Robert F., and Clive W.J. Granger. 1987. Co-integration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society 55: 251–76. [Google Scholar] [CrossRef]

- Ernst, and Young. 2016. World Islamic Banking Competitiveness Report 2016. Available online: https://ceif.iba.edu.pk/pdf/EY-WorldIslamicBankingCompetitivenessReport2016.pdf (accessed on 21 January 2021).

- European Central Bank. 2017. Financial stability review. Available online: https://www.ecb.europa.eu/pub/pdf/fsr/financialstabilityreview201705.en.pdf (accessed on 24 February 2021).

- Faisal, Faisal, Turgut Tursoy, and Niyazi Berk. 2018. Linear and non-linear impact of Internet usage and financial deepening on electricity consumption for Turkey: Empirical evidence from asymmetric causality. Environmental Science and Pollution Research 25: 11536–55. [Google Scholar] [CrossRef]

- Farahani, Yazdan Gudarzi, and Masood Dastan. 2013. Analysis of Islamic banks’ financing and economic growth: A panel cointegration approach. International Journal of Islamic and Middle Eastern Finance and Management 6: 156–72. [Google Scholar] [CrossRef]

- Foglia, Matteo, Alfredo Cartone, and Cristiana Fiorelli. 2020. Structural differences in the Eurozone: Measuring financial stability by Fci. Macroeconomic Dynamics 24: 69–92. [Google Scholar] [CrossRef]

- Furqani, Hafas, and Ratna Mulyany. 2009. Islamic banking and economic growth: Empirical evidence from Malaysia. Journal of Economic Cooperation & Development 30: 59–74. [Google Scholar]

- Geweke, John, Richard Meese, and Warren Dent. 1983. Comparing alternative tests of causality in temporal systems: Analytic results and experimental evidence. Journal of Econometrics 21: 161–94. [Google Scholar] [CrossRef]

- Goaied, Mohamed, and Seifallah Sassi. 2010. Financial Development and Economic Growth in the MENA Region: What About Islamic Banking Development. Carthage: Institut des Hautes Etudes Commerciales, pp. 1–23. [Google Scholar]

- Grassa, Rihab, and Kaouthar Gazdar. 2014. Financial development and economic growth in GCC countries. International Journal of Social Economics 41: 493–514. [Google Scholar] [CrossRef]

- Hachicha, Nejib, and Amine Ben Amar. 2015. Does Islamic bank financing contribute to economic growth? The Malaysian case. International Journal of Islamic and Middle Eastern Finance and Management 8: 349–36. [Google Scholar] [CrossRef]

- Hasan, Maher, and Jemma Dridi. 2010. Put to the Test Islamic banks were more resilient than conventional banks during the global financial crisis. Finance & Development 47: 46. [Google Scholar]

- Hassan, M. Kabir, and Khaled A. Hussein. 2003. Static and dynamic efficiency in the Sudanese banking system. Review of Islamic Economics 14: 5–48. [Google Scholar]

- Hassan, M. Kabir, Benito Sanchez, and Jung-Suk Yu. 2011. Financial development and economic growth: New evidence from panel data. The Quarterly Review of Economics and Finance 51: 88–104. [Google Scholar] [CrossRef]

- Haug, Alfred A. 2002. Temporal aggregation and the power of cointegration tests: A Monte Carlo study. Available online: https://ssrn.com/abstract=334965 (accessed on 12 March 2021).

- Jenkıns, Hatice Pehlivan, and Salih Turan Katırcıoglu. 2010. The bounds test approach for cointegration and causality between financial development, international trade and economic growth: The case of Cyprus. Applied Economics 42: 1699–707. [Google Scholar] [CrossRef]

- Johansen, Soren, and Katarina Juselius. 1990. Maximum likelihood estimation and inference on cointegration with applications to the demand for money. Oxford Bulletin of Economics and Statistics 52: 169–210. [Google Scholar] [CrossRef]

- Jouini, Jamel. 2016. Economic growth and savings in Saudi Arabia: Empirical evidence from cointegration and causality analysis. Asia-Pacific Journal of Accounting & Economics 23: 478–95. [Google Scholar] [CrossRef]

- Jung, Woo S. 1986. Financial development and economic growth: International evidence. Economic Development and Cultural Change 34: 333–46. [Google Scholar] [CrossRef]

- Kar, Muhsin, Şaban Nazlıoğlu, and Hüseyin Ağır. 2011. Financial development and economic growth nexus in the MENA countries: Bootstrap panel granger causality analysis. Economic Modelling 28: 685–93. [Google Scholar] [CrossRef]

- Kassim, Salina. 2016. Islamic finance and economic growth: The Malaysian experience. Global Finance Journal 30: 66–76. [Google Scholar] [CrossRef]

- Khan, Habibullah, and Omar KMR Bashar. 2008. Islamic Finance: Growth and Prospects in Singapore. U21Global Working Paper Series, No. 001/2008: 1–10. [Google Scholar] [CrossRef]

- Kim, Soyoung, and Aaron Mehrotra. 2017. Managing price and financial stability objectives in inflation targeting economies in Asia and the Pacific. Journal of Financial Stability 29: 106–16. [Google Scholar] [CrossRef]

- King, Robert G., and Ross Levine. 1993. Finance, entrepreneurship and growth. Journal of Monetary Economics 32: 513–42. [Google Scholar] [CrossRef]

- Lebdaoui, Hind, and Joerg Wild. 2016. Islamic banking presence and economic growth in Southeast Asia. International Journal of Islamic and Middle Eastern Finance and Management 9: 551–69. [Google Scholar] [CrossRef]

- Lentner, Csaba, László Vasa, Pál P. Kolozsi, and Zoltán Zéman. 2019. New dimensions of internal controls in banking after the GFC. Economic Annals-XXI 176: 38–48. [Google Scholar] [CrossRef]

- Love, Inessa. 2003. Financial development and financing constraints: International evidence from the structural investment model. The Review of Financial Studies 16: 765–91. [Google Scholar] [CrossRef]

- Lucas, Robert E. 1988. On the mechanics of economic development. Journal of Monetary Economics 22: 3–42. [Google Scholar] [CrossRef]

- Manu, Lordina P., Charles K.D. Adjasi, Joshua Abor, and Simon K Harvey. 2011. Financial stability and economic growth: A cross-country study. International Journal of Financial Services Management 5: 121–38. [Google Scholar] [CrossRef]

- Menegaki, Angeliki N. 2019. The ARDL method in the energy-growth nexus field; best implementation strategies. Economies 7: 105. [Google Scholar] [CrossRef]

- Misati, Roseline Nyakerario, and Esman Morekwa Nyamongo. 2012. Financial liberalization, financial fragility and economic growth in Sub-Saharan Africa. Journal of Financial Stability 8: 150–60. [Google Scholar] [CrossRef]

- Muhamad, Nazlida, and Dick Mizerski. 2013. The effects of following Islam in decisions about taboo products. Psychology & Marketing 30: 357–71. [Google Scholar] [CrossRef]

- Musa, Hussam, Viacheslav Natorin, Zdenka Musova, and Pavol Durana. 2020. Comparison of the efficiency measurement of the conventional and Islamic banks. Oeconomia Copernicana 11: 29–58. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar. 2005. The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics 37: 1979–90. [Google Scholar] [CrossRef]

- Nawaz, Huma, Maira Abrar, Asma Salman, and Syed Muhammad Hassan Bukhari. 2019. Beyond finance: Impact of Islamic finance on economic growth in Pakistan. Economic Journal of Emerging Markets 11: 8–18. [Google Scholar] [CrossRef]

- Neaime, Simon, and Isabelle Gaysset. 2018. Financial inclusion and stability in MENA: Evidence from poverty and inequality. Finance Research Letters 24: 230–37. [Google Scholar] [CrossRef]

- Odedokun, Matthew O. 1992. Supply-leading and demand-following relationship between economic activities and development banking in developing countries: An international evidence. Singapore Economic Review 37: 46–58. [Google Scholar]

- Özer, Mustafa, and Veysel Karagöl. 2018. Relative effectiveness of monetary and fiscal policies on output growth in Turkey: An ARDL bounds test approach. Equilibrium. Quarterly Journal of Economics and Economic Policy 13: 391–409. [Google Scholar] [CrossRef]

- Pappas, Vasileios, Steven Ongena, Marwan Izzeldin, and Ana-Maria Fuertes. 2017. A survival analysis of Islamic and conventional banks. Journal of Financial Services Research 51: 221–56. [Google Scholar] [CrossRef]

- Patrick, Hugh T. 1966. Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change 14: 174–89. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–26. [Google Scholar] [CrossRef]

- Robinson, Joan. 1952. The Generalization of the General Theory. The Rate of Interest and Other Essays. London: MacMillan. [Google Scholar]

- Saleem, Adil, and Muhammad Ashfaque. 2020. An Analysis of Profitability Determinants of Islamic Banks: Empirical Study of Malaysia vs Pakistan. International Journal of Business Reflections 1: 135–57. [Google Scholar]

- Samad, Abdus. 2004. Performance of Interest-free Islamic banks vis-à-vis Interest-based Conventional Banks of Bahrain. International Journal of Economics, Management and Accounting 12: 1–15. [Google Scholar]

- Samad, Abdus, and M. Kabir Hassan. 2006. The performance of Malaysian Islamic bank during 1984–1997: An exploratory study. International Journal of Islamic Financial Services 1: 1–14. [Google Scholar] [CrossRef]

- Samargandi, Nahla, Jan Fidrmuc, and Sugata Ghosh. 2014. Financial development and economic growth in an oil-rich economy: The case of Saudi Arabia. Economic Modelling 43: 267–78. [Google Scholar] [CrossRef]

- SBP. 2019a. Half-Year Performance Review of the Banking Sector. Available online: https://www.sbp.org.pk/publications/HPR/H1CY19.pdf (accessed on 16 January 2021).

- SBP. 2019b. Islamic Banking Bulletin. Available online: https://www.sbp.org.pk/ibd/bulletin/bulletin.asp (accessed on 16 January 2021).

- SBP. 2020. “Islamic Banking in Pakistan”. Available online: https://www.sbp.org.pk/70/sup-5.asp (accessed on 16 January 2021).

- Schumpeter, Joseph A. 1912. Theorie der Wirtschaftlichen Entwicklung. Leipzig: Dunker & Humblot, The Theory of Economic Development. [Google Scholar]

- Sekuloska, Jovanka Damoska. 2018. Causality between foreign direct investment in the automotive sector and export performance of Macedonian economy. Equilibrium. Quarterly Journal of Economics and Economic Policy 13: 427–43. [Google Scholar] [CrossRef]

- Shah, Syed Muhammad Abdul Rehman, and Kashif Raza. 2020. The Role of Islamic Finance in Achieving Economic Growth: An Econometric Analysis of Pakistan Enhancing Financial Inclusion through Islamic Finance. Berlin: Springer, vol. II, pp. 241–58. [Google Scholar]

- Shamsudin, Mohidin Yahya, Hussin Salamon, Mohd Fauzi Abu-Hussin, and Nasrul Hisyam Nor Muhamad. 2015. Islamic Banking and Finance: Traders not Mere Financial Intermediary. Mediterranean Journal of Social Sciences 6: 181. [Google Scholar] [CrossRef][Green Version]

- Skare, Marinko, and Małgorzata Porada-Rochoń. 2019. Financial and economic development link in transitional economies: A spectral Granger causality analysis 1991? Oeconomia Copernicana 10: 7–35. [Google Scholar] [CrossRef]

- Szegedi, Krisztina, Yahya Khan, and Csaba Lentner. 2020. Corporate Social Responsibility and Financial Performance: Evidence from Pakistani Listed Banks. Sustainability 12: 4080. [Google Scholar] [CrossRef]

- Tabash, Mosab I., and Raj S. Dhankar. 2014. Islamic finance and economic growth: An empirical evidence from United Arab Emirates (UAE). Journal of Emerging Issues in Economics, Finance and Banking 3: 1069–85. [Google Scholar] [CrossRef]

- Yüksel, Serhat, and İsmail Canöz. 2017. Does Islamic Banking Contribute to Economic Growth and Industrial Development in Turkey. Ikonomika 2: 93–102. [Google Scholar] [CrossRef]

- Yusof, Rosylin Mohd, and Mejda Bahlous. 2013. Islamic banking and economic growth in GCC & East Asia countries: A panel cointegration analysis. Journal of Islamic Accounting and Business Research 4: 151–72. [Google Scholar] [CrossRef]

- Zarrouk, Hajer, Teheni El Ghak, and Elias Abu Al Haija. 2017. Financial development, Islamic finance and economic growth: Evidence of the UAE. Journal of Islamic Accounting and Business Research 8: 2–22. [Google Scholar] [CrossRef]

| Variables | Description | Notation | Data Collected |

|---|---|---|---|

| Economic growth | Real gross domestic product | GDP | World Development Indicators (WDI) |

| Islamic financial depth | Total Islamic financings as a percentage of GDP | IFD | SBP’s Islamic Banking Bulletin |

| Islamic financial Intermediation | Represented as number of Islamic banking branches | IFI | SBP’s Islamic Banking Bulletin |

| Asset Quality Islamic | Non-performing assets/total finances | NPA | SBP’s Islamic Banking Bulletin |

| Conventional financial depth | Total loans as a percentage of GDP | CFD | SBP’s Quarterly Banking Review |

| Conventional financial intermediation | Number of conventional banking branches | CFI | SBP’s Quarterly Banking Review |

| Asset quality conventional | Non-performing loans/total loans | NPL | SBP’s Quarterly Banking Review |

| Inflation | Consumer Price Index | INF | IMF’s International Financial Statistics |

| Interest Rate | Discount Rate/KIBOR | IR | IMF’s International Financial Statistics |

| Variables | Model 1 (Islamic) | Model 2 (Conventional) | ||||||

|---|---|---|---|---|---|---|---|---|

| I(0) | I(1) | I(0) | I(1) | |||||

| c | t & c | c | t & c | c | t & c | c | t & c | |

| GDP | −0.5818 | −1.572 | −11.382 * | −11.502 * (0.000) | −0.5818 | −1.572 | −11.382 * | −11.502 * (0.000) |

| (0.866) | (0.792) | (0.000) | (0.866) | (0.792) | (0.000) | |||

| IFD/CFD | 3.891 | 0.242 | −7.396 * | −9.385 * | 0.1819 | −1.432 | −10.321 * | −10.414 * |

| (1.000) | (0.242) | (0.000) | (0.000) | (0.969) | (0.841) | (0.000) | (0.000) | |

| IFI/CFI | −5.483 * | −10.063 * | - | - | −1.366 | −3.434 | −11.587 * | −12.729 * |

| (0.000) | (0.000) | (0.592) | (0.057) | (0.000) | (0.000) | |||

| NPA/NPL | −1.626 | −1.801 | −9.727 * | −9.799 * | −1.237 | −1.540 | −6.607 * | −6.641 * |

| (0.463) | (0.691) | (0.000) | (0.000) | (0.653) | (0.803) | (0.000) | (0.000) | |

| INF | 0.982 | −1.678 | −4.022 * | −4.191 * | - | - | - | - |

| (0.996) | (0.749) | (0.003) | (0.008) | |||||

| IR | −1.565 | −1.583 | −4.337 * | −4.333 * | - | - | - | - |

| (0.494) | (0.788) | (0.001) | (0.006) | |||||

| Model Specification | F(GDP|IFD, IFI, NPA) 1 | F(GDP|IFD, IFI, NPA, INF, IR) 2 | F(GDP|CFD, CFI, NPL) 3 | F(GDP|CFD, CFI, NPL, INF, IR) 4 | ||||

|---|---|---|---|---|---|---|---|---|

| Bounds Tests | ||||||||

| F-Statistics | 4.4647 * | 43.2523 * | 12.3147 * | 14.3109 * | ||||

| Asymptotic Critical Values | K 3 | K 5 | K 3 | K 5 | ||||

| I(0) | I(1) | I(0) | I(1) | I(0) | I(1) | I(0) | I(1) | |

| 10% | 2.37 | 3.20 | 2.08 | 3.0 | 2.37 | 3.2 | 2.08 | 3.0 |

| 5% | 2.79 | 3.67 | 2.39 | 3.38 | 2.79 | 3.67 | 2.39 | 3.38 |

| 2.5% | 3.15 | 4.08 | 2.70 | 3.73 | 3.15 | 4.08 | 2.70 | 3.73 |

| Diagnostic tests | ||||||||

| LM BG χ2 | 0.751 | 0.402 | 0.761 | 1.096 | ||||

| (0.415) | (0.533) | (0.410) | (0.243) | |||||

| RESET χ2 | 1.093 | 0.069 | 2.481 | 1.831 | ||||

| (0.301) | (0.793) | (0.122) | (0.183) | |||||

| Jarque Bera χ2 | 1.506 | 0.186 | 4.911 | 0.528 | ||||

| (0.471) | (0.911) | (0.085) | (0.768) | |||||

| LM BP χ2 | 3.046 | 1.355 | 1.941 | 0.932 | ||||

| (0.061) | (0.221) | (0.088) | (0.482) | |||||

| Model Specification | F(GDP|IFD, IFI, NPA) 1 | F(GDP|IFD, IFI, NPA, INF, IR) 2 | F(GDP|CFD, CFI, NPL) 3 | F(GDP|CFD, CFI, NPL, INF, IR) 4 |

|---|---|---|---|---|

| IFD/CFD | 0.0162 | 0.0213 | −0.0015 | 0.0093 |

| (2.522) ** | (16.101) *** | (−0.588) | (2.403) ** | |

| IFI/CFI | 0.0579 | 0.0358 | 1.141 | 0.672 |

| (2.870) *** | (5.097) *** | (10.999) *** | (2.179) ** | |

| NPA/NPL | −0.014 | −0.0003 | −0.0095 | −0.0023 |

| (0.176) | (−0.140) | (−2.975) *** | (−0.425) | |

| INF | - | 0.0014 | - | 0.0001 |

| (6.430) *** | (0.098) | |||

| IR | - | −0.0097 | - | −0.0078 |

| (−3.752) *** | (−1.949) * | |||

| - | 21.247 | 21.318 | 11.352 | 15.334 |

| (154.62) *** | (371.55) *** | (13.262) *** | (5.741) *** |

| Differenced Variables | F(GDP|IFD, IFI, NPA, INF, IR) 1 | F(GDP|CFD,CFI,NPL,INF, IR) 2 | |

|---|---|---|---|

| D(GDP(-1) | −0.0103 | D(GDP(-1)) | 0.0788 |

| (−0.0646) | (0.6769) | ||

| D(GDP(-2)) | −0.1336 | D(GDP(-2)) | - |

| (−1.1915) | |||

| D(IFD) | 0.0131 | D(CFD) | 0.00045 |

| (2.7721) * | (0.3123) | ||

| D(IFD(-1)) | 0.00328 | D(CFD(-1)) | 0.00214 |

| (0.7914) | (1.4799) | ||

| D(IFI) | −0.0107 | D(CFI) | −0.6150 |

| (0.8587) | (0.0017) | ||

| D(IFI(-1)) | - | D(CFI(-1)) | - |

| D(NPA) | −0.0018 | D(NPL) | 0.00121 |

| (−0.8362) | (0.3178) | ||

| D(NPA(-1)) | - | D(NPL(-1)) | - |

| D(INF) | −0.0029 | D(INF) | −0.0038 |

| (−3.500) * | (−3.7602) | ||

| D(INF(-1)) | −0.0028 | D(INF(-1)) | - |

| (−2.9840) * | |||

| D(IR) | −0.00111 | D(IR) | 0.00305 |

| (−0.5919) | (1.1787) | ||

| D(IR(-1)) | 0.00528 | D(IR(-1)) | - |

| (2.5690) * | |||

| C | 0.0272 | 0.02352 | |

| (6.0540) * | (5.6808) * | ||

| ECT(-1) | −0.7987 | ECT(-1) | −0.4236 |

| (−4.5593) * | (−3.4756) * | ||

| Adjusted R2 | 0.8615 | 0.6800 | |

| Log likelihood | 208.7563 | 184.8972 | |

| F-statistic (prob = 0.00) | 23.8144 | 14.2236 | |

| AIC 3 | −6.8842 | −6.1367 | |

| SIC 3 | −6.3055 | −5.7783 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saleem, A.; Sági, J.; Setiawan, B. Islamic Financial Depth, Financial Intermediation, and Sustainable Economic Growth: ARDL Approach. Economies 2021, 9, 49. https://doi.org/10.3390/economies9020049

Saleem A, Sági J, Setiawan B. Islamic Financial Depth, Financial Intermediation, and Sustainable Economic Growth: ARDL Approach. Economies. 2021; 9(2):49. https://doi.org/10.3390/economies9020049

Chicago/Turabian StyleSaleem, Adil, Judit Sági, and Budi Setiawan. 2021. "Islamic Financial Depth, Financial Intermediation, and Sustainable Economic Growth: ARDL Approach" Economies 9, no. 2: 49. https://doi.org/10.3390/economies9020049

APA StyleSaleem, A., Sági, J., & Setiawan, B. (2021). Islamic Financial Depth, Financial Intermediation, and Sustainable Economic Growth: ARDL Approach. Economies, 9(2), 49. https://doi.org/10.3390/economies9020049