2.1. A Brief History of FSI

The financial stress index (FSI) aims to reveal the functionality of the financial system due to uncertainty or stress and to provide an aggregate measure of financial stress in the financial system as a whole which includes the money market, bond market, foreign exchange market etc. (

Huotari 2015). In order words, developing FSI will enable regulatory authorities, government, policymakers and other stakeholders to understand the general condition of the financial sector. The FSI is a composite index that aggregates information from these markets to provide a single measure of stress for the whole financial system (

Huotari 2015). This makes it easier to monitor the financial system and determine the likelihood of the occurrence of any financial crises. The FSI is a highly useful and appropriate dependent variable in an early signal warning model. It is also useful by macroprudential authorities during their macroprudential decision making process. Generally, FSIs are mostly calculated on a monthly basis for developed countries like the USA.

There have been numerous indicators that have been developed since the 1980s, such as the slope of the yield curve, which is based on the difference between long-term and short-term interest rates, credit risk as measured by commercial paper-Treasury bill spread and stock market trends (

Ekinci 2013). The first broader financial condition, measure introduced by the Bank of Canada in the mid-1990s was named the monetary condition index (MCI), which is the weighted average changes in interest rates and exchange rates relative to their value during the base period (

Ekinci 2013). MCIs are now used by policymakers as measures of monetary conditions in the economy. Soon after that, several similar indexes began to be used for monetary policy decisions by several central banks such as that of Canada, New Zealand and Sweden (

Ekinci 2013). Several other indicators such as stock prices and real estate prices were also incorporated into the MCI, which made it broader; this new index became referred to as the FSI.

In 2009, the Bloomberg FCI was calculated using ten variables covering the money market, bond market as well as the equity market; it is believed to be a suitable indicator for monitoring financial conditions since it is accessible to many financial markets and has been updated daily from 1991 (

Rosenberg 2009). In contrast to the Bloomberg FCI, the Citi FCI developed in 2008, which has been available from 1983, was calculated using six (6) variables. These variables include corporate spreads, money supply, equity values, mortgage rates, the trade-weighted dollar and energy prices (

D’Antonio 2008). Similarly, the Deutsche Bank FCI also starts in 1983, although it differs with respect to the number of variables and methodology used. The index is made up of seven (7) variables which include the exchange rate as well as bond, stock and housing market indicators, and is calculated using principal component analysis (

Hooper et al. 2010). In 2008, the OECD developed its own FCI which starts from 1995 by aggregating six financial variables. The weights were calculated based on the effects of each variable on GDP and this was done by regressing the output gap on a distributed lag of the financial indicators (

Ekinci 2013). The FCI developed by the OECD differs from other FCIs in that it included variables for tightening of credit standards. In May 2009, a FSI was constructed for Turkey comprising five sub-market indexes which are the “foreign exchange market pressure index, the riskiness of the banking sector, equity markets and perceptions of uncertainty towards this market” (

CBRT 2009, pp. 76–78).

Several other attempts (

Illing and Liu 2006;

Hakkio and Keeton 2009;

Holló et al. 2012;

Islami and Kurz-Kim 2014) have been made to develop a composite index for measuring financial stress. Researchers developed FSIs for the Canadian financial system, Kansas City and the Euro area. The construction of a FSI is based on the aggregation of market-specific sub-indexes which reflect the stress within a market segment though varying aggregation techniques and the number of variables used. Market segments include the equity markets, bond markets, foreign exchange markets as well as the banking sector. Major findings of these studies include the fact that FSIs can predict developments in the real economy and select risk variables based on their correlation with economic activities. More specifically, the findings of

Illing and Liu (

2006) captured previous stress events such as the 1992 credit losses as well as the 1998 Long-Term Capital Management (LTCM) among others.

In the same vein,

Cardarelli et al. (

2011) and

Balakrishnan et al. (

2011) developed a FSI to identify periods of financial turmoil and suggested a framework to investigate the impact of financial stress on the real economy for 17 advanced economies and emerging economies, respectively. They show that stress in the banking sector has greater effects on creating financial stress compared to the two other market segments (securities and foreign exchange) considered in the study. Also,

Oet et al. (

2011) developed a FSI for the United States called the Cleveland Financial Stress Index (CFSI). The CFSI was developed using daily data from 11 components reflecting four financial sectors: credit markets, equity markets, foreign exchange markets, and interbank markets. Most of the CFSI components are spreads (i.e., the interbank liquidity spread, corporate bond spread and liquidity spread) and two of the remaining CFSI components are ratios, and one is a measure of stock market volatility.

Iachini and Nobili (

2016) introduced an indicator for measuring systemic risk in the Italian financial market using the portfolio aggregation theory method. This portfolio aggregation was used to capture the systemic dimension of liquidity stress. The result shows that the systemic liquidity risk indicator adequately captured extreme events that were characterized by high systemic risk.

In the case of emerging markets,

Stolbov and Shchepeleva (

2016) employed the PCA approach to calculate the FSI for emerging markets including Russia, China, India, Brazil, South Africa, Indonesia, Turkey, Mexico, Malaysia, Thailand, Philippines, Chile, Columbia as well as Peru. Using six variables, the results of the study show that the FSI for most emerging markets exhibited a surge around September—October 2008 and this is assumed to have been caused by the emergence of the GFC (

Stolbov and Shchepeleva 2016). In this study, following the studies of

Holló et al. (

2012),

Huotari (

2015) and

Ilesanmi and Tewari (

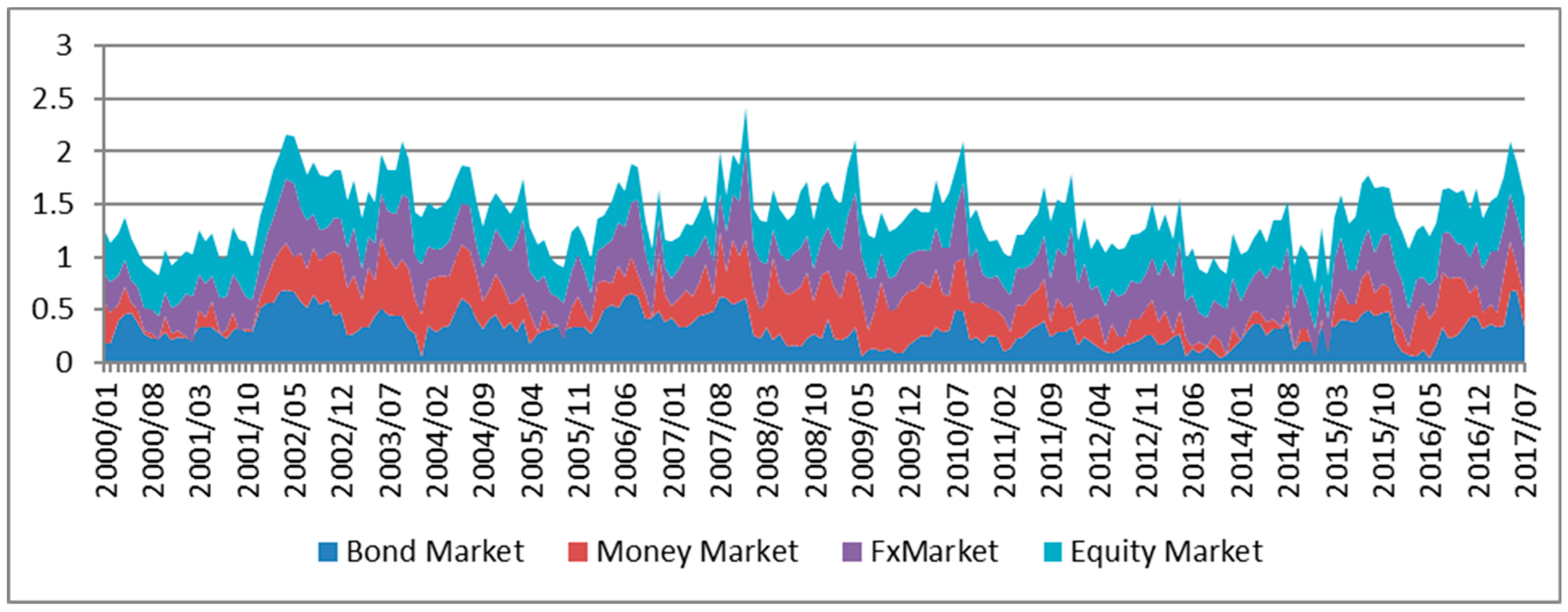

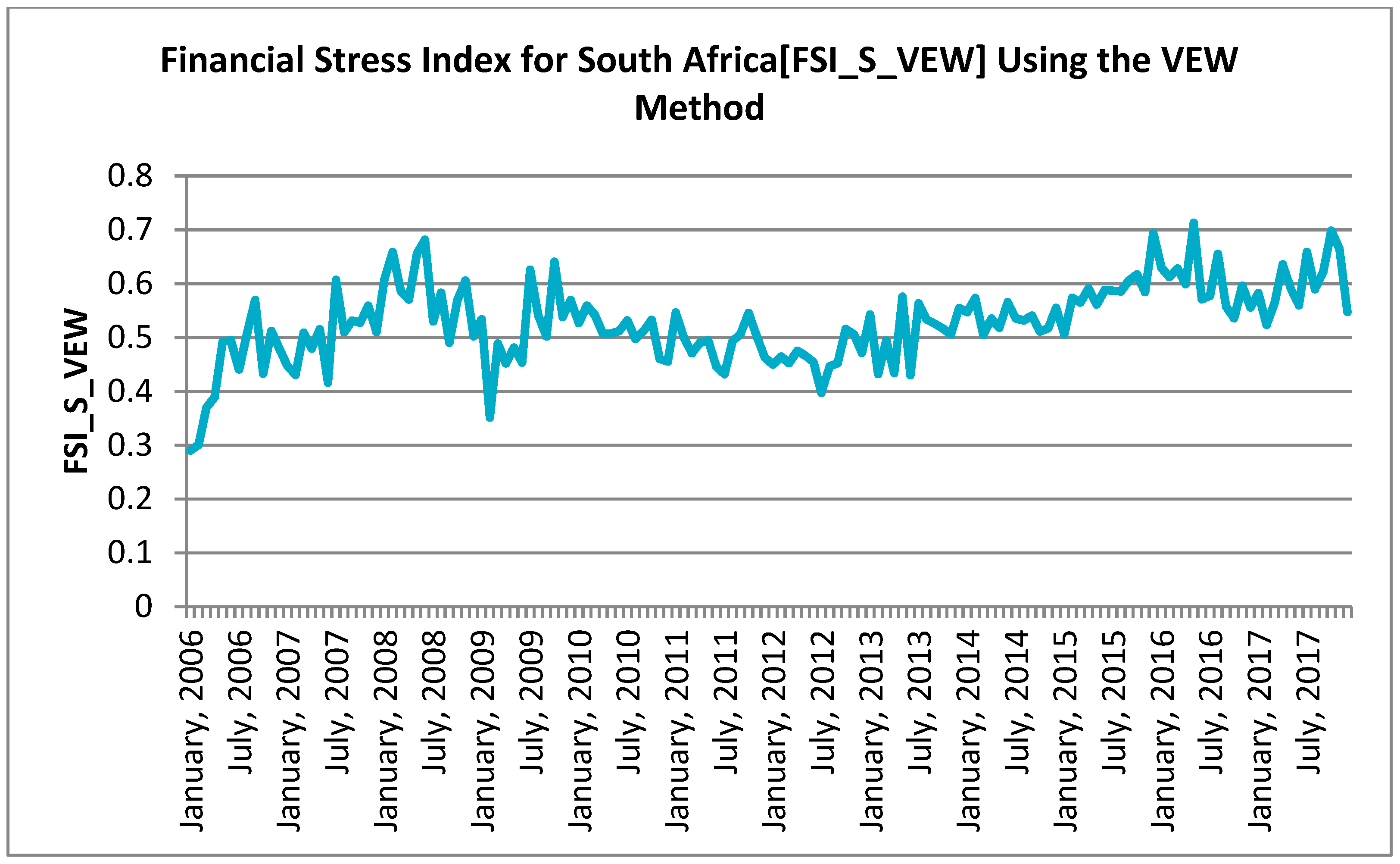

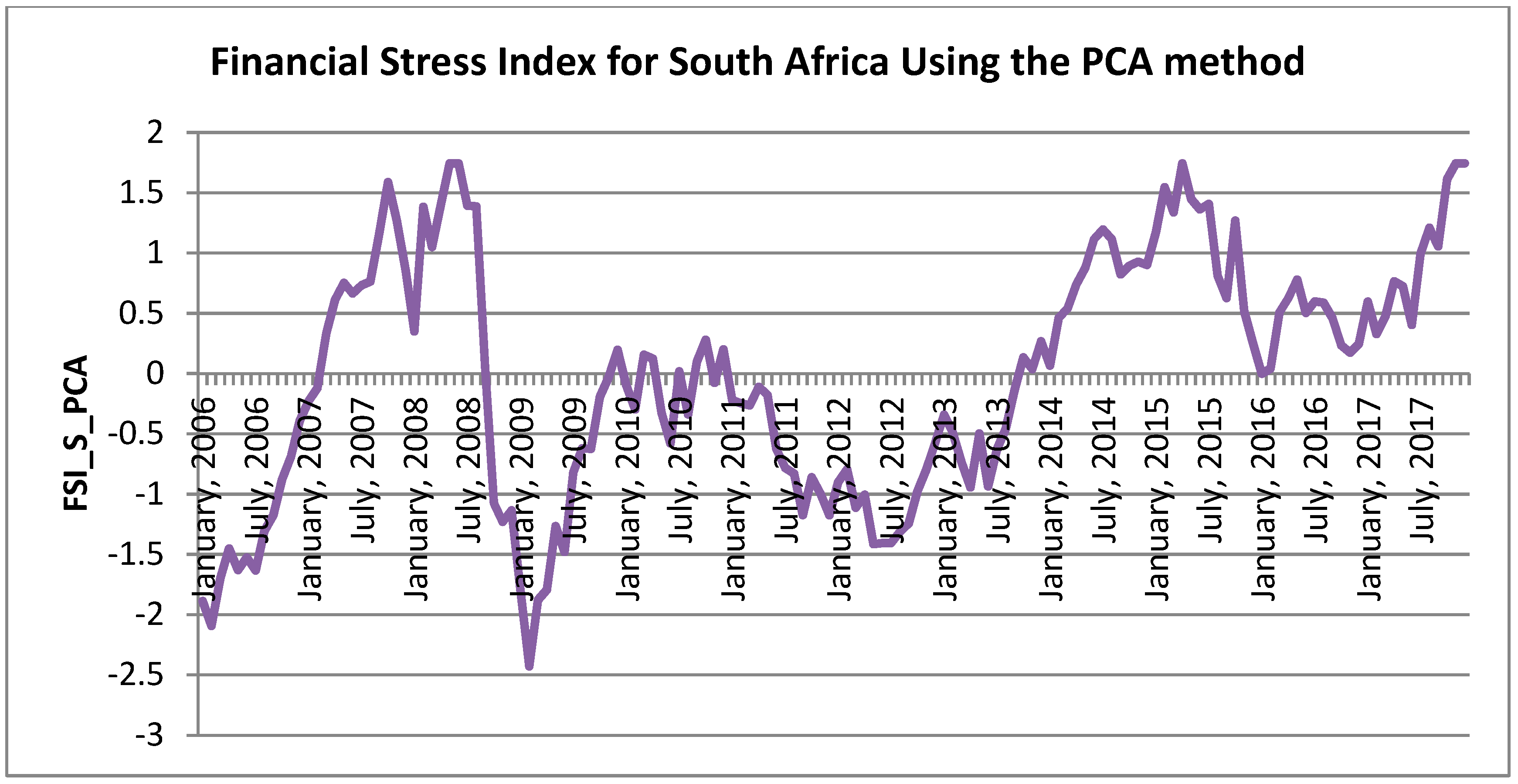

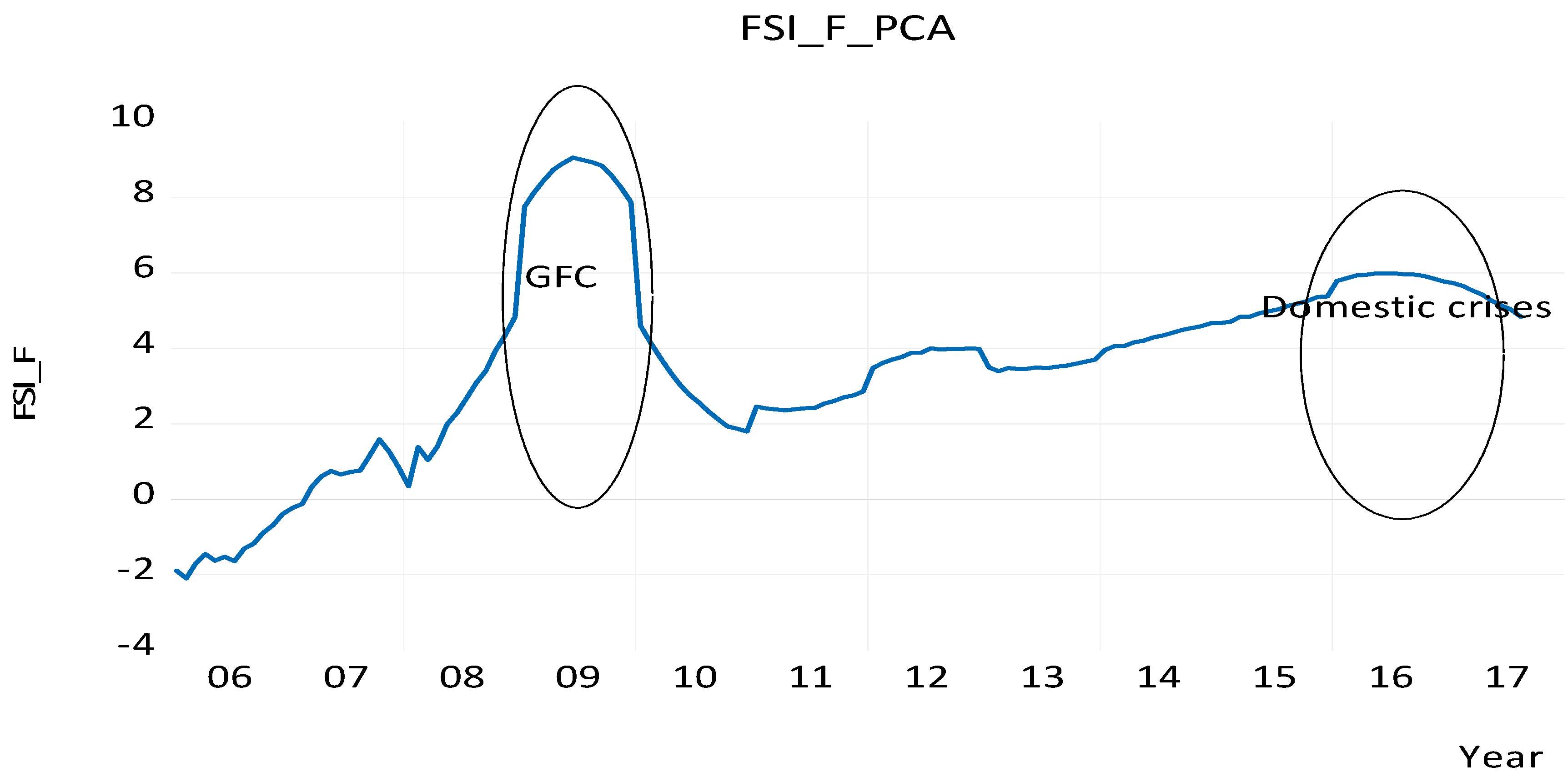

2019a), a financial stress index for South Africa was developed by aggregating individual stress indicators from four different markets: the money market, bond market, equity market, and the foreign exchange market. Different aggregation methods have been used in literature such as the equal weighting method; correlation-based weighing method, principal component analysis, market size weight etc. This study employed the equal-variance and principal component analysis methods to develop a composite index for monitoring the financial system.

2.2. Financial Stress and Systemic Risk Indicators

Although it might be difficult to identify what systemic risk is since it is difficult to define and quantify, several attempts have been made to define it. According to

De Bandt and Hartmann (

2000) “systemic risk is defined as the systemic event that causes a particularly strong propagation of failures from one institution, market or system to another.” In the words of

Illing and Liu (

2006), it can be referred to as shocks with negative effects on the real economy.

It is also defined as the disruption or obstruction of the financial system’s ability to provide credit to all stakeholders within the economic system (

Brockmeijer et al. 2011;

Yellen 2010).

Although there is no consensus on the definition of financial stress, it is commonly accepted as referring to the disruption of the functioning of the financial market (

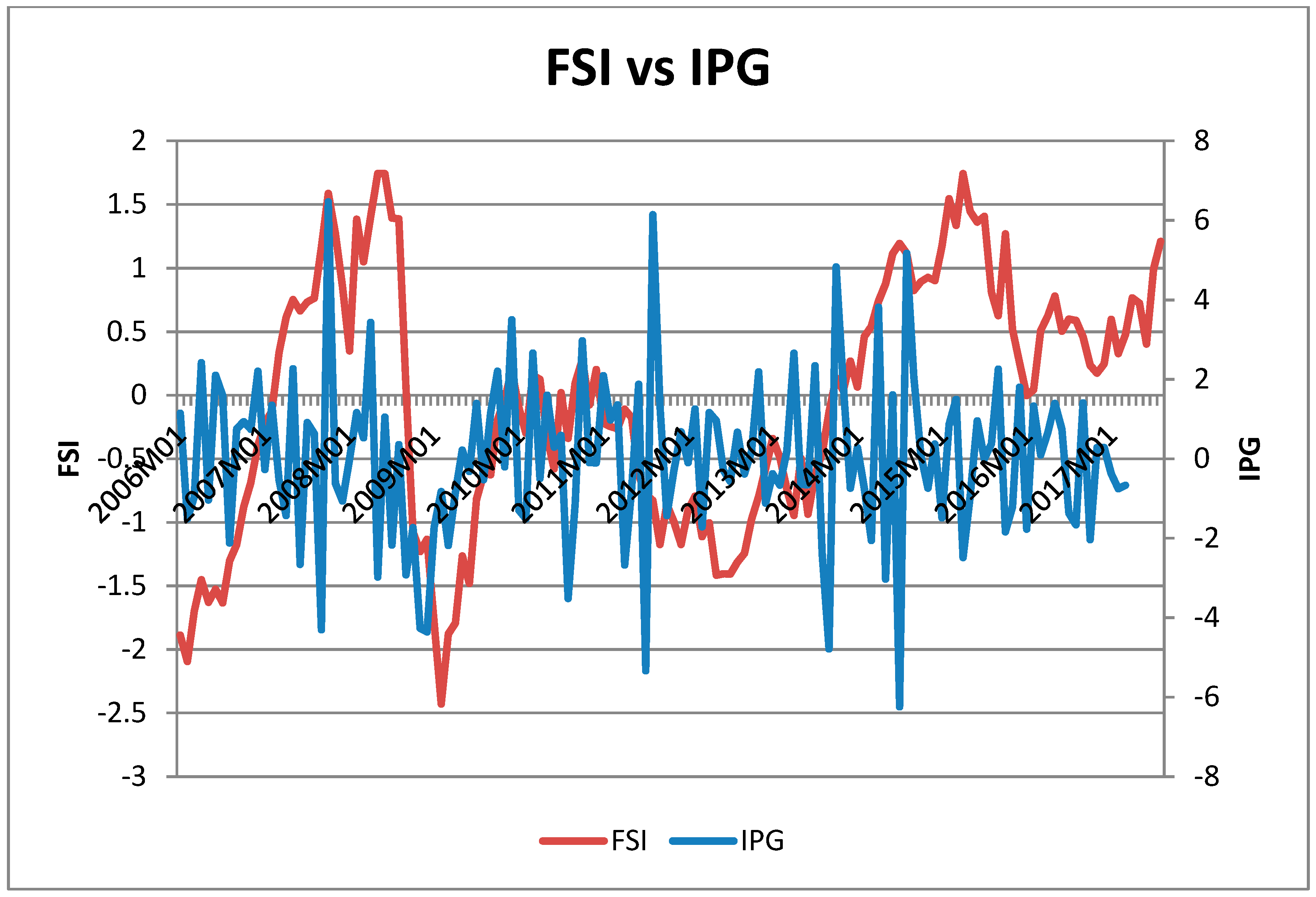

Aklan et al. 2015). In order words, it is the emergence of an event or events that impair the smooth functioning of the financial system’s ability to provide financial services, with attendant negative effects on the overall functioning of the entire economy. One common characteristic of financial stress is the increasing uncertainty of creditors and investors about the real value of financial assets, which in turn leads to increased volatility of asset prices. The computation of the FSI is important not only for evaluating macroeconomic conditions, but also to determine the source(s) of fragility in the financial sector.

As noted earlier, there is an increasing number of studies on FSI; however, these studies differ based on methodologies, frequency and countries. For example,

Huotari (

2015) in his study proposed a FSI for the Finnish financial system using the variance-equal weight (VEW), principal component analysis (PCA) and portfolio theory aggregation methods (PAM). The study utilized a formation which included the country’s money market, bond market, equity market and foreign exchange markets and the banking sector. This FSI developed using the PCA and PAM captured previously known stress periods, although an FSI index produced by the VEW methods differs from the PCA and PAM by only showing stress events at the end of the sample.

Kabundi and Mbelu (

2020) developed a financial condition index (FCI) for the South African economy using 41 indicators, and their result revealed the strength of the FCI in signaling both domestic and foreign risk. However, as noted by

Huotari (

2015) using too many indicators that could constitute adding noise in the index.

Siņenko et al. (

2013) developed a methodology for measuring the Latvian financial stress index and also analyzed the nature of financial stress. These results captured the changes in the Latvian financial system, as well as signaling periods of elevated stress and periods of excessively vigorous and imbalanced development of the financial system. Similar to the study of

Siņenko et al. (

2013),

Kondratovs (

2014) examined the fragility of the financial system of Latvia in comparison to the fluctuations in the global economy and changes in direction of international capital flows by creating a complex financial system stability index. The findings of the study revealed that a fall in the stability level of the Latvian financial system started in 2002 and became worse in 2005, which informed the need for policymakers to be more actively involved in preventing growing risks to the economy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}