Which Liquidity Proxy Measures Liquidity Best in Emerging Markets?

Abstract

1. Introduction

2. Liquidity Variables

2.1. Liquidity Benchmarks Using High-Frequency Data

2.1.1. Spread Benchmarks

2.1.2. Price Impact Benchmarks

2.2. Liquidity Proxies from Low-Frequency Data

2.2.1. Spread Proxies

2.2.2. Price Impact Proxies

3. Data and Sample

- (1)

- Quotes and transactions are used only if they are recorded during the exchange opening hours, and if the quotes or trades have positive prices and positive shares.

- (2)

- Only valid quotes and trades are used, where a valid quote or trade is defined, as follows:

- (a)

- If a quote is not the first quote of the day, its price should be within the range of 50–150% of its previous quote.

- (b)

- If a trade is not the first trade of the day, its price should be within the range of 50–150% of the price of the trade prior to it.

- (3)

- To obtain a reliable time series average of the daily average spreads, we impose a condition that there should be at least 20 valid trading days for each stock during the entire investigation window. A valid trading day is a day that has at least one valid quoted spread and one valid effective spread. A valid quoted spread is a spread whose size in currency unit is within 0.2 (quote midpoint) and a valid effective spread is an effective spread whose size in currency unit is within 0.2 (quote midpoint in effect at the time of the trade).

- (4)

- For the quoted, effective, and realized spreads, we calculate the daily average spread first (an equal weight average of all spreads, not time weighted), and then calculate the average of these daily spreads over the entire period. For each stock, these average spreads in currency units must be smaller than 10% the time series average of the daily prices during the period.

4. Empirical Results

4.1. Spread Benchmarks and Spread Proxies

4.1.1. Spread Benchmarks and Spread Proxies

4.1.2. Price Impact Benchmarks and Price Impact Proxies

4.1.3. Firm Characteristics, Market Features, Minimum Tick Size, and Foreign Exchange Rate

4.2. The Best Liquidity Proxies

4.2.1. The Best Spread Proxies

4.2.2. The Best Price Impact Proxies

4.3. Wilcoxon Rank-Sum Tests for the Effectiveness of Liquidity Proxies

4.3.1. Effectiveness of Spread Proxies

4.3.2. Effectiveness of Price Impact Proxies

4.4. Correlation Analysis

4.5. Incremental Regression R2

4.5.1. The Determinants of Spread Benchmarks

4.5.2. The Determinants of Price Impact Benchmarks

4.6. Firm and Market Characteristics and Accuracy of Liquidity Proxies

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Abdi, Farshid, and Angelo Ranaldo. 2017. A simple estimation of bid-ask spreads from daily close, high, and low prices. Review of Financial Studies 30: 4437–80. [Google Scholar] [CrossRef]

- Acharya, Viral, and Lasse Heje Pedersen. 2005. Asset pricing with liquidity risk. Journal of Financial Economics 77: 375–410. [Google Scholar] [CrossRef]

- Amihud, Yakov. 2002. Illiquidity and stock returns: Cross-section and time series effects. Journal of Financial Markets 5: 31–56. [Google Scholar] [CrossRef]

- Amihud, Yakov, and Kefei Li. 2006. The declining information content of dividend announcements and the effects of institutional holdings. Journal of Financial and Quantitative Analysis 41: 637–60. [Google Scholar] [CrossRef]

- Amihud, Yakov, and Haim Mendelson. 1986. Asset pricing and the bid-ask spread. Journal of Financial Economics 17: 223–49. [Google Scholar] [CrossRef]

- Banerjee, Suman, Vladimir A. Gatchev, and Paul A. Spindt. 2007. Stock market liquidity and firm dividend policy. Journal of Financial and Quantitative Analysis 42: 369–98. [Google Scholar] [CrossRef]

- Bekaert, Geert, and Campbell R. Harvey. 1995. Time-varying world market integration. Journal of Finance 50: 403–44. [Google Scholar] [CrossRef]

- Bekaert, Geert, Campbell R. Harvey, and Christian Lundblad. 2007. Liquidity and expected returns: Lessons from emerging markets. Review of Financial Studies 20: 1783–831. [Google Scholar] [CrossRef]

- Bharath, Sreedhar, Paolo Pasquariello, and Guojun Wu. 2009. Does asymmetric information drive capital structure decisions? Review of Financial Studies 22: 3211–43. [Google Scholar] [CrossRef]

- Brennan, Michael, and Avanidhar Subrahmanyam. 1996. Market microstructure and asset pricing: On the compensation for illiquidity in stock returns. Journal of Financial Economics 41: 441–64. [Google Scholar] [CrossRef]

- Brockman, Paul, and Dennis Y. Chung. 2003. Investor Protection and Firm Liquidity. Journal of Finance 58: 921–37. [Google Scholar] [CrossRef]

- Chalmers, John, and Gregory Kadlec. 1998. An empirical examination of the amortized spread. Journal of Financial Economics 48: 159–88. [Google Scholar] [CrossRef]

- Chiyachantana, Chiraphol, Pankaj Jain, Christine Jiang, and Robert Wood. 2004. International evidence on institutional trading behavior and price impact. Journal of Finance 59: 869–98. [Google Scholar] [CrossRef]

- Chung, Kee, and Hao Zhang. 2014. A simple approximation of intraday spreads using daily data. Journal of Financial Markets 17: 94–120. [Google Scholar] [CrossRef]

- Coller, Maribeth, and Teri Lombardi Yohn. 1997. Management forecasts and information asymmetry: An examination of bid-ask spreads. Journal of Accounting Research 35: 181–91. [Google Scholar] [CrossRef]

- Cooper, S. Kerry, John C. Groth, and William E. Avera. 1985. Liquidity, exchange listing and common stock performance. Journal of Economics and Business 37: 19–33. [Google Scholar] [CrossRef]

- Eleswarapu, Venkat R. 1997. Cost of transacting and expected returns in the NASDAQ market. Journal of Finance 52: 2113–27. [Google Scholar] [CrossRef]

- Goyenko, Ruslan Y., Craig W. Holden, and Charles A. Trzcinka. 2009. Do liquidity measures measure liquidity? Journal of Financial Economics 92: 153–81. [Google Scholar] [CrossRef]

- Hasbrouck, Joel. 2004. Liquidity in the futures pits: Inferring market dynamics from incomplete data. Journal of Financial and Quantitative Finance 39: 305–26. [Google Scholar] [CrossRef]

- Hasbrouck, Joel. 2009. Trading costs and returns for US equities: Estimating effective costs from daily data. Journal of Finance 64: 1445–77. [Google Scholar] [CrossRef]

- Huang, Roger D., and Hans R. Stoll. 1996. Dealer versus auction markets: A paired comparison of execution costs on NASDAQ and the NYSE. Journal of Financial Economics 41: 313–57. [Google Scholar] [CrossRef]

- Jain, Pankaj K. 2005. Financial market design and the equity premium: Electronic vs. floor trading. Journal of Finance 60: 2955–85. [Google Scholar] [CrossRef]

- Kang, Jun-Koo, and René Stulz. 1997. Why is there a home bias? An analysis of foreign portfolio equity ownership in Japan. Journal of Financial Economics 46: 2–28. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrej Shleifer, and Robert W. Vishny. 1998. Law and Finance. Journal of Political Economy 106: 1113–55. [Google Scholar] [CrossRef]

- Lesmond, David A. 2005. Liquidity of emerging markets. Journal of Financial Economics 77: 411–52. [Google Scholar] [CrossRef]

- Lesmond, David A., Joseph P. Ogden, and Charles A. Trzcinka. 1999. A new estimate of transaction costs. Review of Financial Studies 12: 1113–41. [Google Scholar] [CrossRef]

- Lesmond, David A., Philip F. O’Connor, and Lemma W. Senbet. 2008. Capital Structure and Equity Liquidity. Working Paper. New Orleans, LA, USA: Tulane University. [Google Scholar]

- Lipson, Marc L., and Sandra Mortal. 2007. Liquidity and capital structure. Journal of Financial Markets 12: 611–44. [Google Scholar] [CrossRef]

- McInish, Thomas H., and Robert A. Wood. 1992. An analysis of intraday patterns in bid/ask spreads for NYSE stocks. Journal of Finance 47: 753–64. [Google Scholar] [CrossRef]

- Pástor, Ľuboš, and Robert F. Stambaugh. 2003. Liquidity risk and expected stock returns. Journal of Political Economy 111: 642–85. [Google Scholar] [CrossRef]

- Roll, Richard. 1984. A simple implicit measure of the effective bid-ask spread in an efficient market. Journal of Finance 39: 1127–39. [Google Scholar] [CrossRef]

- Sadka, Ronnie. 2006. Liquidity risk and asset pricing. Journal of Financial Economics 80: 309–49. [Google Scholar] [CrossRef]

| 1 | Hasbrouck (2009) also evaluates the effectiveness of transaction costs estimated from daily data using the Bayesian Gibbs sampling approach that he developed (Hasbrouck 2004, 2009). |

| 2 | The selection of proxies is made from the set of low-frequency measures evaluated in Goyenko et al. (2009). |

| 3 | Roll (1984), and Goyenko et al. (2009) assign 0 to the value of the spread when the covariance is negative. |

| 4 | Gibbs sampler estimation programs are available at www.stern.nyu.edu/~jhasbrou. We draw 2000 times for each Gibbs sampler. Like Hasbrouck (2009), we discard the first 200 draws to “burn in the sampler” (Hasbrouck 2009, p. 1451). Hasbrouck points out that 1000 sweeps are sufficient to produce reliable estimates. |

| 5 | Lesmond et al. (1999) also develop measures (ZEROS and ZEROS2) that are similar to, but much simpler than the LOT measure, utilizing zero return days. ZEROS and ZEROS2 are based on the rationale that low liquidity and less-informed trading lead to a zero daily return. The result using ZEROS and ZEROS2 are slightly weaker than the results using the LOT measure. |

| 6 | Originally, Pástor and Stambaugh (2003) used the coefficient to measure the liquidity. They anticipated the minus (−) value of the coefficient, where the lower minus value represented the lower liquidity. We take the absolute value to measure the degree of illiquidity in this study. Moreover, we confirm that the latter performs better than the former in the analyses. |

| 7 | Turnover is calculated as the daily average number of traded shares divided by market capitalization. |

| 8 |

{kind=link}

{kind=link}

| Panel A: Spread Benchmarks and Spread Proxies | |||||||||

| Market | High-Frequency Spread Benchmark | Low-Frequency Spread Proxy | |||||||

| Region | Country | N | QS(%) | ES(%) | RS(%) | ROLL | HASB | LOT | |

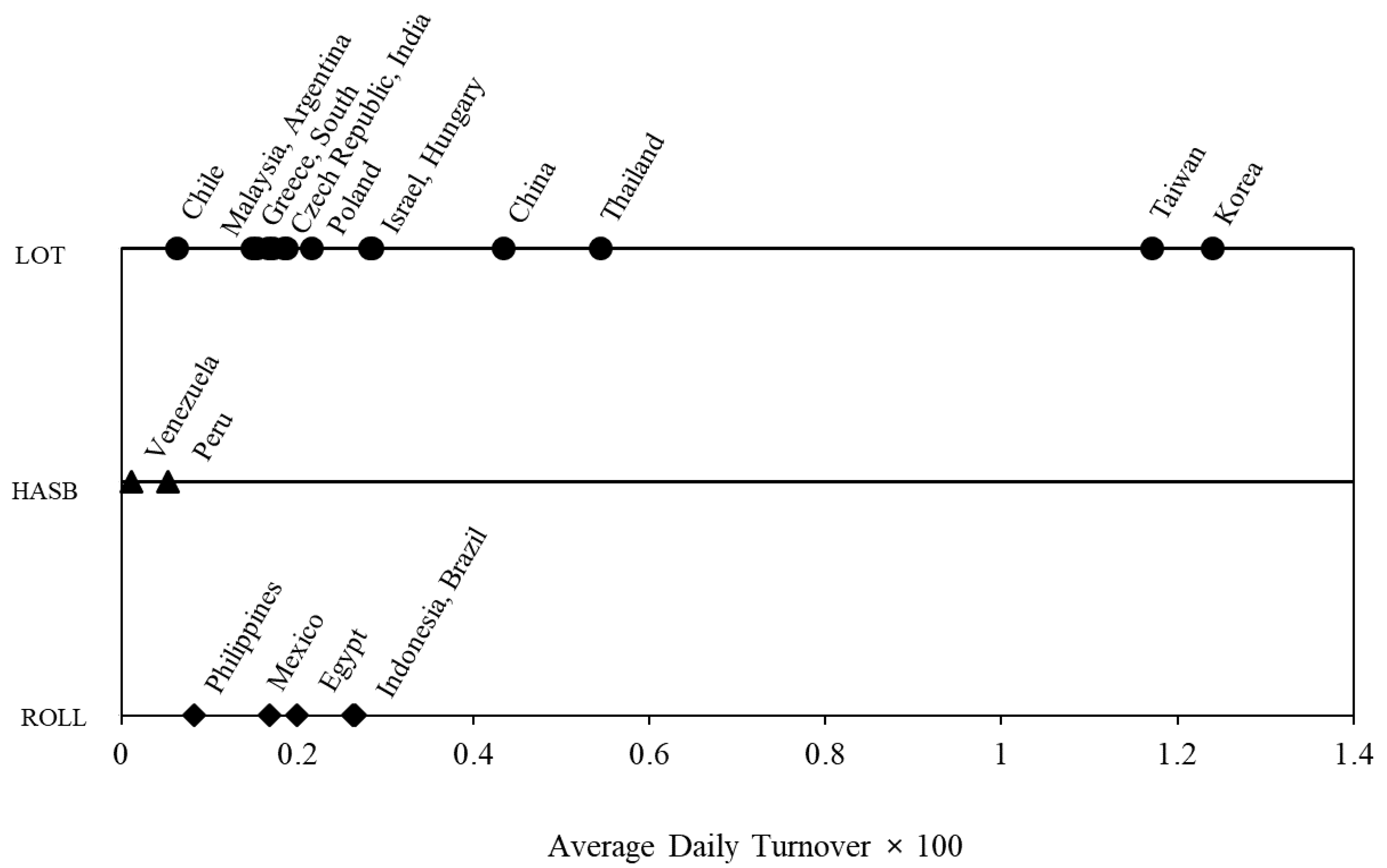

| Asia | China | 222 | 0.180 | 0.177 | 0.036 | 1.086 | 2.239 | 0.176 | |

| India | 101 | 0.318 | 0.234 | 0.103 | 2.506 | 2.942 | 0.001 | ||

| Indonesia | 43 | 2.973 | 1.996 | 1.036 | 2.246 | 3.372 | 4.075 | ||

| South Korea | 145 | 0.301 | 0.273 | 0.096 | 1.539 | 2.654 | 0.515 | ||

| Malaysia | 89 | 0.929 | 0.706 | 0.524 | 1.324 | 2.298 | 1.265 | ||

| Philippines | 39 | 2.590 | 1.760 | 0.879 | 1.797 | 2.995 | 4.514 | ||

| Taiwan | 106 | 0.464 | 0.463 | 0.211 | 1.956 | 2.841 | 0.674 | ||

| Thailand | 57 | 0.710 | 0.656 | 0.262 | 1.593 | 2.632 | 1.030 | ||

| Eastern Europe | Czech Republic | 7 | 1.672 | 0.612 | 0.241 | 1.526 | 2.092 | 0.263 | |

| Greece | 63 | 0.740 | 0.647 | 0.238 | 1.176 | 2.192 | 0.554 | ||

| Hungary | 13 | 0.916 | 0.765 | 0.378 | 1.691 | 2.550 | 0.473 | ||

| Poland | 26 | 0.534 | 0.450 | 0.229 | 1.067 | 2.041 | 0.602 | ||

| Latin America | Argentina | 12 | 0.938 | 0.643 | 0.141 | 1.694 | 1.573 | 0.527 | |

| Brazil | 23 | 2.471 | 1.486 | 0.273 | 1.830 | 2.302 | 0.132 | ||

| Chile | 35 | 1.933 | 1.568 | 0.583 | 0.732 | 1.905 | 1.333 | ||

| Mexico | 35 | 1.053 | 0.701 | 0.145 | 1.076 | 1.967 | 0.269 | ||

| Peru | 18 | 4.097 | 2.914 | 0.591 | 1.340 | 2.552 | 4.297 | ||

| Venezuela | 11 | 6.761 | 4.500 | 1.211 | 1.150 | 3.748 | 8.635 | ||

| Others | Egypt | 48 | 2.187 | 1.479 | 0.779 | 1.710 | 2.535 | 0.699 | |

| Israel | 40 | 0.429 | 0.299 | 0.121 | 1.068 | 1.726 | 0.103 | ||

| South Africa | 50 | 0.707 | 0.560 | 0.185 | 1.124 | 2.062 | 0.583 | ||

| Panel B: Price Impact Benchmarks and Price Impact Proxies | |||||||||

| Market | High-Frequency Price Impact Benchmark | Low-Frequency Price Impact Proxy | |||||||

| LAMBDA | IMP | ASC | AMIHUD | AMIVEST | PASTOR | ||||

| Asia | China | 222 | 1.216 | 0.140 | 0.136 | 0.140 | 0.017 | 0.011 | |

| India | 101 | 1.477 | 0.177 | 0.119 | 0.233 | 0.027 | 0.007 | ||

| Indonesia | 43 | 0.020 | 1.180 | 1.159 | 0.004 | 1.166 | 0.000 | ||

| South Korea | 145 | 0.073 | 0.217 | 0.185 | 0.000 | 4.415 | 0.000 | ||

| Malaysia | 89 | 1.984 | 0.241 | 0.182 | 1.639 | 0.002 | 0.070 | ||

| Philippines | 39 | 0.438 | 0.968 | 0.832 | 4.292 | 0.001 | 0.059 | ||

| Taiwan | 106 | 0.321 | 0.237 | 0.234 | 0.009 | 0.310 | 0.000 | ||

| Thailand | 57 | 0.157 | 0.420 | 0.394 | 0.040 | 0.038 | 0.004 | ||

| Eastern Europe | Czech Republic | 7 | 0.458 | 0.370 | 0.311 | 0.093 | 0.128 | 0.002 | |

| Greece | 63 | 12.519 | 0.459 | 0.358 | 10.120 | 0.000 | 0.813 | ||

| Hungary | 13 | 0.789 | 0.402 | 0.194 | 0.097 | 0.038 | 0.002 | ||

| Poland | 26 | 2.869 | 0.293 | 0.226 | 1.385 | 0.002 | 0.045 | ||

| Latin America | Argentina | 12 | 5.207 | 0.530 | 0.503 | 3.187 | 0.001 | 0.145 | |

| Brazil | 23 | 0.046 | 1.281 | 0.954 | 0.253 | 0.010 | 0.020 | ||

| Chile | 35 | 0.053 | 0.694 | 0.564 | 0.013 | 1.017 | 0.000 | ||

| Mexico | 35 | 0.807 | 0.561 | 0.468 | 0.146 | 0.031 | 0.010 | ||

| Peru | 18 | 11.545 | 1.703 | 1.712 | 31.924 | 0.000 | 0.893 | ||

| Venezuela | 11 | 1.887 | 2.493 | 2.293 | 0.267 | 0.014 | 0.007 | ||

| Others | Egypt | 48 | 4.924 | 0.534 | 0.487 | 7.518 | 0.000 | 0.512 | |

| Israel | 40 | 0.140 | 0.266 | 0.162 | 0.366 | 0.009 | 0.015 | ||

| South Africa | 50 | 0.054 | 0.382 | 0.340 | 0.231 | 0.030 | 0.008 | ||

| Panel C: Firm and Market Characteristics | |||||||||

| Market | Stock Price ($) | Firm Size ($ Million) | Turnover | Volatility | Investability | Market Volatility | Legal Origin | Trading Mechanism | |

| Asia | China | 0.89 | 571 | 0.343 | 0.018 | 0.000 | 1.147 | 0 | 1 |

| India | 5.70 | 719 | 0.123 | 0.032 | 0.490 | 2.210 | 1 | 1 | |

| Indonesia | 0.07 | 166 | 0.168 | 0.026 | 0.000 | 1.742 | 0 | 1 | |

| South Korea | 13.63 | 676 | 0.663 | 0.022 | 0.837 | 1.690 | 0 | 1 | |

| Malaysia | 1.04 | 496 | 0.101 | 0.014 | 0.503 | 0.890 | 1 | 1 | |

| Philippines | 0.28 | 228 | 0.024 | 0.018 | 0.000 | 1.155 | 0 | 1 | |

| Taiwan | 0.78 | 1521 | 0.840 | 0.025 | 0.707 | 1.951 | 0 | 1 | |

| Thailand | 0.40 | 507 | 0.296 | 0.023 | 0.435 | 1.933 | 1 | 1 | |

| Eastern Europe | Czech Republic | 15.09 | 2658 | 0.218 | 0.019 | 0.569 | 1.133 | 0 | 0 |

| Greece | 7.46 | 622 | 0.142 | 0.020 | 0.759 | 1.079 | 0 | 1 | |

| Hungary | 18.13 | 289 | 0.241 | 0.015 | 0.000 | 1.342 | 0 | 0 | |

| Poland | 13.94 | 656 | 0.147 | 0.014 | 0.684 | 1.124 | 0 | 1 | |

| Latin America | Argentina | 1.18 | 427 | 0.048 | 0.020 | 0.000 | 2.561 | 0 | 0 |

| Brazil | 0.93 | 949 | 0.126 | 0.023 | 0.923 | 2.211 | 0 | 0 | |

| Chile | 1.90 | 986 | 0.047 | 0.014 | 0.643 | 0.634 | 0 | 1 | |

| Mexico | 1.97 | 1612 | 0.110 | 0.016 | 0.718 | 1.184 | 0 | 1 | |

| Peru | 0.56 | 181 | 0.039 | 0.027 | 0.000 | 0.983 | 0 | 0 | |

| Venezuela | 0.26 | 189 | 0.005 | 0.021 | 0.000 | 0.906 | 0 | 1 | |

| Others | Egypt | 2.97 | 86 | 0.121 | 0.022 | 0.000 | 0.602 | 0 | 1 |

| Israel | 10.58 | 698 | 0.243 | 0.014 | 0.663 | 0.904 | 1 | 1 | |

| South Africa | 3.48 | 909 | 0.166 | 0.014 | 0.877 | 1.007 | 1 | 1 | |

| Panel D: Minimum Tick Size and Foreign Exchange Rates | |||||||||

| Market | Minimum Tick in Local Currency | Minimum Tick in US Currency (Cents) | Tick Size Varies by Stock Price | Local Currency | Exchange Rate (Local Currency/USD) | ||||

| Asia | China | 0.01 | 0.1208 | No | CNY | 8.28 | |||

| India | 0.01/0.05 | 0.0224/0.1120 | Yes | INR | 44.63 | ||||

| Indonesia | 1 | 0.0114 | Yes | IDR | 8768.88 | ||||

| South Korea | 1 | 0.0858 | Yes | KRW | 1165.19 | ||||

| Malaysia | 0.005 | 0.1316 | Yes | MYR | 3.80 | ||||

| Philippines | 0.0001 | 0.0002 | Yes | PHP | 56.10 | ||||

| Taiwan | 0.01 | 0.0301 | Yes | TWD | 33.21 | ||||

| Thailand | 0.01 | 0.0251 | Yes | THB | 39.79 | ||||

| Eastern Europe | Czech Republic | 0.01 | 0.0377 | Yes | CZK | 26.50 | |||

| Greece | 0.001 | 0.1220 | Yes | EUR | 0.82 | ||||

| Hungary | 1 | 0.4852 | Yes | HUF | 206.12 | ||||

| Poland | 0.01 | 0.2564 | Yes | PLN | 3.90 | ||||

| Latin America | Argentina | 0.001 | 0.0345 | Yes | ARS | 2.90 | |||

| Brazil | 0.01 | 0.3367 | No | BRL | 2.97 | ||||

| Chile | 0.001 | 0.0002 | Yes | CLP | 616.77 | ||||

| Mexico | 0.001 | 0.0089 | Yes | MXN | 11.26 | ||||

| Peru | 0.001 | 0.0288 | Yes | PEN | 3.48 | ||||

| Venezuela | 0.01 | 0.0004 | No | VEF | 3067.58 | ||||

| Others | Egypt | 0.01 | 0.1616 | No | EGP | 6.19 | |||

| Israel | 0.01 | 0.2203 | Yes | ILS | 4.54 | ||||

| South Africa | 1 | 15.1286 | No | ZAR | 6.61 | ||||

| Panel A: Spread Benchmarks and Spread Proxies | ||||

| Group | ES(%) | ROLL | HASB | LOT |

| G1 | 0.274 | 1.380 | 2.490 | 0.396 ** |

| G2 | 0.760 | 1.423 | 2.204 | 0.454 ** |

| G3 | 0.599 | 1.532 | 2.422 | 0.522 ** |

| G4 | 1.909 | 1.210 | 2.492 ** | 3.368 |

| QS (%) | ||||

| G1 | 0.297 | 1.380 | 2.490 | 0.396 ** |

| G2 | 1.074 | 0.423 ** | 2.204 | 0.454 |

| G3 | 0.792 | 1.532 | 2.422 | 0.522 ** |

| G4 | 2.620 | 1.210 | 2.492 ** | 3.368 |

| RS (%) | ||||

| G1 | 0.096 | 1.380 | 2.490 | 0.396 ** |

| G2 | 0.263 | 1.423 | 2.204 | 0.454 ** |

| G3 | 0.313 | 1.532 | 2.422 | 0.522 ** |

| G4 | 0.783 | 1.210 ** | 2.492 | 3.368 |

| Panel B: Price Impact Benchmarks and Price Impact Proxies | ||||

| Group | LAMBDA | AMIHUD | 1/AMIVEST | PASTOR |

| G1 | 0.365 | 0.029 ** | 0.010 | 0.002 |

| G2 | 0.184 | 0.213 ** | 0.046 | 0.007 |

| G3 | 2.087 | 1.135 ** | 0.336 | 0.054 |

| G4 | 0.268 | 0.404 | 0.225 ** | 0.008 |

| IMP | ||||

| G1 | 0.191 | 0.029 ** | 0.010 | 0.002 |

| G2 | 0.560 | 0.213 ** | 0.046 | 0.007 |

| G3 | 0.277 | 1.135 | 0.336 ** | 0.054 |

| G4 | 0.955 | 0.404 ** | 0.225 | 0.008 |

| ASC | ||||

| G1 | 0.179 | 0.029 ** | 0.010 | 0.002 |

| G2 | 0.390 | 0.213 ** | 0.046 | 0.007 |

| G3 | 0.224 | 1.135 | 0.336 ** | 0.054 |

| G4 | 0.832 | 0.404 ** | 0.225 | 0.008 |

| Panel A: Spread Proxies | |||

| Group | Median Measurement Error | ||

| |ROLLi − ESi| | |HASBi − ESi| | |LOTi − ESi| | |

| G1 | 1.029 *** | 2.193 *** | 0.181 |

| G2 | 0.811 *** | 1.316 *** | 0.464 |

| G3 | 0.877 *** | 1.673 *** | 0.300 |

| G4 | 1.008 ** | 1.195 *** | 1.604 |

| |ROLLi − QSi| | |HASBi − QSi| | |LOTi − QSi| | |

| G1 | 1.003 *** | 2.165 *** | 0.181 |

| G2 | 0.892 * | 1.162 *** | 0.656 |

| G3 | 0.752 *** | 1.545 *** | 0.399 |

| G4 | 1.760 | 1.199 | 1.442 |

| |ROLLi − RSi| | |HASBi − RSi| | |LOTi − RSi| | |

| G1 | 1.273 *** | 2.388 *** | 0.290 |

| G2 | 1.066 *** | 1.839 *** | 0.256 |

| G3 | 1.149 *** | 1.997 *** | 0.328 |

| G4 | 0.921 *** | 1.793 ** | 2.398 |

| Panel B: Price Impact Proxies | |||

| Group | Median Measurement Error | ||

| |AMIHUDi − LAMBDAi| | |1/AMIVESTi − LAMBDAi| | |PASTORi − LAMBDAi| | |

| G1 | 0.326 | 0.360 | 0.366 |

| G2 | 0.355 | 0.188 * | 0.145 * |

| G3 | 1.515 | 1.645 | 2.028 |

| G4 | 0.957 | 0.740 | 0.682 |

| |AMIHUDi − IMPi| | |1/AMIVESTi − IMPi| | |PASTORi − IMPi| | |

| G1 | 0.184 | 0.171 | 0.185 ** |

| G2 | 0.598 | 0.522 | 0.524 |

| G3 | 0.847 | 0.265 *** | 0.230 *** |

| G4 | 1.902 | 0.953 | 0.928 *** |

| |AMIHUDi − ASCi| | |1/AMIVESTi − ASCi| | |PASTORi − ASCi| | |

| G1 | 0.170 | 0.156 | 0.171 * |

| G2 | 0.546 | 0.423 ** | 0.372 *** |

| G3 | 0.878 | 0.265 *** | 0.183 *** |

| G4 | 1.702 | 0.874 | 0.784 *** |

| Panel A: Correlation between Spread and Spread Proxies | ||||

| Spread | Spread Proxy | |||

| Benchmark | ROLL | HASB | LOT | |

| G1 | ES | 0.274 ** | 0.255 ** | 0.582 ** |

| QS | 0.265 ** | 0.246 ** | 0.575 ** | |

| RS | 0.210 ** | 0.118 ** | 0.544 ** | |

| G2 | ES | 0.351 ** | 0.609 ** | 0.622 ** |

| QS | 0.311 ** | 0.578 ** | 0.576 ** | |

| RS | 0.260 ** | 0.503 ** | 0.691 ** | |

| G3 | ES | −0.081 | 0.062 | 0.636 ** |

| QS | −0.077 | 0.054 | 0.551 ** | |

| RS | −0.084 | 0.055 | 0.620 ** | |

| G4 | ES | 0.261 ** | 0.449 ** | 0.818 ** |

| QS | 0.258 ** | 0.438 ** | 0.802 ** | |

| RS | 0.060 | 0.211 ** | 0.457 ** | |

| Panel B: Correlation between Price Impact and Price Impact Proxies | ||||

| Price Impact | Price Impact Proxy | |||

| Benchmark | AMIHUD | 1/AMIVEST | PASTOR | |

| G1 | LAMBDA | 0.800 ** | 0.787 ** | 0.713 ** |

| IMP | −0.113 | −0.115 | −0.168 ** | |

| ASC | −0.079 | −0.080 | −0.137 ** | |

| G2 | LAMBDA | 0.606 ** | 0.633 ** | 0.550 ** |

| IMP | 0.069 | 0.006 | −0.026 | |

| ASC | −0.049 | −0.090 | −0.098 | |

| G3 | LAMBDA | 0.715 ** | 0.759 ** | 0.716 ** |

| IMP | 0.705 ** | 0.613 ** | 0.583 ** | |

| ASC | 0.636 ** | 0.563 ** | 0.534 ** | |

| G4 | LAMBDA | 0.487 ** | 0.490 ** | 0.504 ** |

| IMP | 0.510 ** | 0.475 ** | 0.467 ** | |

| ASC | 0.534 ** | 0.502 ** | 0.498 ** | |

| Panel A: The Incremental Explanatory Power of Spread Proxies | ||||||||

| Intercept | PRICE | SIZE | ROLL | HASB | LOT | Adjusted R2 | Incremental R2 | |

| ES | 5.956 *** | 0.009 | −0.306 *** | 0.325 | ||||

| (10.23) | (0.22) | (−6.48) | ||||||

| 5.345 *** | 0.022 | −0.252 *** | 0.296 *** | 0.361 | 0.036 | |||

| (8.97) | (0.57) | (−7.17) | (3.84) | |||||

| 4.879 *** | 0.023 | −0.265 *** | 0.256 *** | 0.343 | 0.018 | |||

| (8.45) | (0.53) | (−5.66) | (4.73) | |||||

| 3.699 *** | −0.001 | −0.175 *** | 0.122 *** | 0.464 | 0.139 | |||

| (5.69) | (−0.01) | (−5.61) | (3.94) | |||||

| QS | 8.852 *** | 0.026 | −0.402 *** | 0.439 | ||||

| (11.26) | (0.63) | (−8.24) | ||||||

| 8.242 *** | 0.040 | −0.348 *** | 0.295 ** | 0.463 | 0.024 | |||

| (10.15) | (1.02) | (−9.12) | (3.74) | |||||

| 7.671 *** | 0.041 | −0.357 *** | 0.280 *** | 0.453 | 0.014 | |||

| (9.88) | (0.98) | (−7.34) | (4.91) | |||||

| 6.197 *** | 0.015 | −0.248 *** | 0.144 *** | 0.573 | 0.134 | |||

| (7.79) | (0.57) | (−6.91) | (4.27) | |||||

| RS | 2.431 *** | 0.017 | −0.187 *** | 0.133 | ||||

| (4.32) | (0.49) | (−4.59) | ||||||

| 1.971 *** | 0.027 | −0.146 *** | 0.223 *** | 0.165 | 0.032 | |||

| (3.52) | (0.83) | (−4.87) | (3.19) | |||||

| 1.860 *** | 0.024 | −0.165 *** | 0.136 *** | 0.140 | 0.007 | |||

| (3.15) | (0.69) | (−4.00) | (2.75) | |||||

| 1.042 | 0.011 | −0.107 *** | 0.075 *** | 0.215 | 0.082 | |||

| (1.44) | (0.41) | (−3.95) | (2.94) | |||||

| Panel B: The Incremental Explanatory Power of Price Impact Proxies | ||||||||

| Intercept | PRICE | SIZE | AMIHUD | 1/AMIVEST | PASTOR | Adjusted R2 | Incremental R2 | |

| LAMBDA | 19.550 *** | −1.313 * | −3.495 ** | 0.087 | ||||

| (2.73) | (−1.76) | (−2.25) | ||||||

| 15.592 *** | −1.454 * | −2.724 ** | 0.047 | 0.160 | 0.073 | |||

| (2.62) | (−1.91) | (−2.15) | (1.51) | |||||

| 6.907 *** | −0.713 ** | −0.767 ** | 0.403 *** | 0.671 | 0.584 | |||

| (2.69) | (−2.18) | (−2.23) | (3.12) | |||||

| 17.158 ** | −1.274 * | −3.007 ** | 0.914 | 0.114 | 0.027 | |||

| (2.45) | (−1.72) | (−1.98) | (1.42) | |||||

| IMP | 6.561 *** | 0.024 | −0.159 *** | 0.405 | ||||

| (3.48) | (0.64) | (−5.99) | ||||||

| 6.534 *** | 0.023 | −0.153 *** | 0.001 | 0.406 | 0.001 | |||

| (3.46) | (0.62) | (−5.72) | (0.71) | |||||

| 6.486 *** | 0.028 | −0.142 *** | 0.002 * | 0.414 | 0.009 | |||

| (3.43) | (0.74) | (−5.44) | (1.93) | |||||

| 6.471 *** | 0.026 | −0.140 *** | 0.034 *** | 0.423 | 0.018 | |||

| (3.43) | (0.68) | (−5.41) | (3.92) | |||||

| ASC | 3.433 *** | −0.009 | −0.111 *** | 0.523 | ||||

| (6.12) | (−0.63) | (−7.59) | ||||||

| 3.383 *** | −0.011 | −0.101 *** | 0.001 | 0.539 | 0.016 | |||

| (6.00) | (−0.76) | (−7.51) | (1.06) | |||||

| 3.337 *** | −0.004 | −0.090 *** | 0.003 * | 0.569 | 0.046 | |||

| (5.91) | (−0.31) | (−7.34) | (1.72) | |||||

| 3.310 ** | −0.007 | −0.086 *** | 0.047 *** | 0.621 | 0.098 | |||

| (5.85) | (−0.50) | (−7.24) | (14.54) | |||||

| The Dependent Variable Is log(1/|Proxy − Benchmark|) | ||||||

|---|---|---|---|---|---|---|

| Proxy = ROLL | Proxy = HASB | Proxy = LOT | Proxy = AMIHUD | Proxy = 1/AMIVEST | Proxy = PASTOR | |

| Benchmark = ES | Benchmark = ES | Benchmark = ES | Benchmark = LAMBDA | Benchmark = LAMBDA | Benchmark = LAMBDA | |

| Intercept | −2.079 *** | −2.625 *** | −2.90 *** | −6.163 *** | −4.189 ** | −5.389 *** |

| (−2.58) | (−3.46) | (−3.56) | (−8.93) | (−5.02) | (−10.14) | |

| Stock Price | 0.052 | 0.004 | 0.120 *** | −0.046 | 0.038 | −0.016 |

| (1.15) | (0.08) | (2.64) | (−1.19) | (0.82) | (−0.53) | |

| Turnover | 5.186 | 6.535 | 22.193 *** | 34.789 *** | 4.937 | 33.427 *** |

| (0.64) | (0.85) | (2.70) | (5.00) | (0.59) | (6.23) | |

| Stock Volatility | −13.734 *** | −11.402 ** | −15.984 *** | −2.128 | −12.097 ** | −11.668 *** |

| (−2.71) | (−2.39) | (−3.12) | (−0.49) | (−2.31) | (−3.49) | |

| Firm Size | 0.091 * | 0.158 *** | 0.158 *** | 0.699 *** | 0.042 | 0.599 *** |

| (1.85) | (3.40) | (3.17) | (16.52) | (0.82) | (18.37) | |

| Investability | 0.371 ** | 0.091 | 0.371 ** | 0.803 *** | 0.313 * | 0.532 *** |

| (2.04) | (0.53) | (2.01) | (5.14) | (1.66) | (4.42) | |

| Market Volatility | 1.437 *** | 1.775 *** | 1.253 ** | −0.857 * | 1.616 *** | −0.441 |

| (2.64) | (3.46) | (2.28) | (−1.84) | (2.87) | (−1.23) | |

| Legal Origin | 0.443 * | 0.481 ** | −0.032 | 1.952 *** | 1.119 *** | 1.656 *** |

| (1.78) | (2.06) | (−0.13) | (9.16) | (4.35) | (10.09) | |

| Trading Mechanism | −0.193 | −0.696 | 0.177 | 2.678 *** | 2.155 *** | 2.379 *** |

| (−0.27) | (−1.04) | (0.25) | (4.40) | (2.93) | (5.07) | |

| Country Dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry Dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| R2 | 0.316 | 0.324 | 0.409 | 0.699 | 0.529 | 0.816 |

| Observations | 1183 | 1183 | 1183 | 1183 | 1183 | 1183 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ahn, H.-J.; Cai, J.; Yang, C.-W. Which Liquidity Proxy Measures Liquidity Best in Emerging Markets? Economies 2018, 6, 67. https://doi.org/10.3390/economies6040067

Ahn H-J, Cai J, Yang C-W. Which Liquidity Proxy Measures Liquidity Best in Emerging Markets? Economies. 2018; 6(4):67. https://doi.org/10.3390/economies6040067

Chicago/Turabian StyleAhn, Hee-Joon, Jun Cai, and Cheol-Won Yang. 2018. "Which Liquidity Proxy Measures Liquidity Best in Emerging Markets?" Economies 6, no. 4: 67. https://doi.org/10.3390/economies6040067

APA StyleAhn, H.-J., Cai, J., & Yang, C.-W. (2018). Which Liquidity Proxy Measures Liquidity Best in Emerging Markets? Economies, 6(4), 67. https://doi.org/10.3390/economies6040067