Examining the "Natural Resource Curse" and the Impact of Various Forms of Capital in Small Tourism and Natural Resource-Dependent Economies

Abstract

:1. Introduction

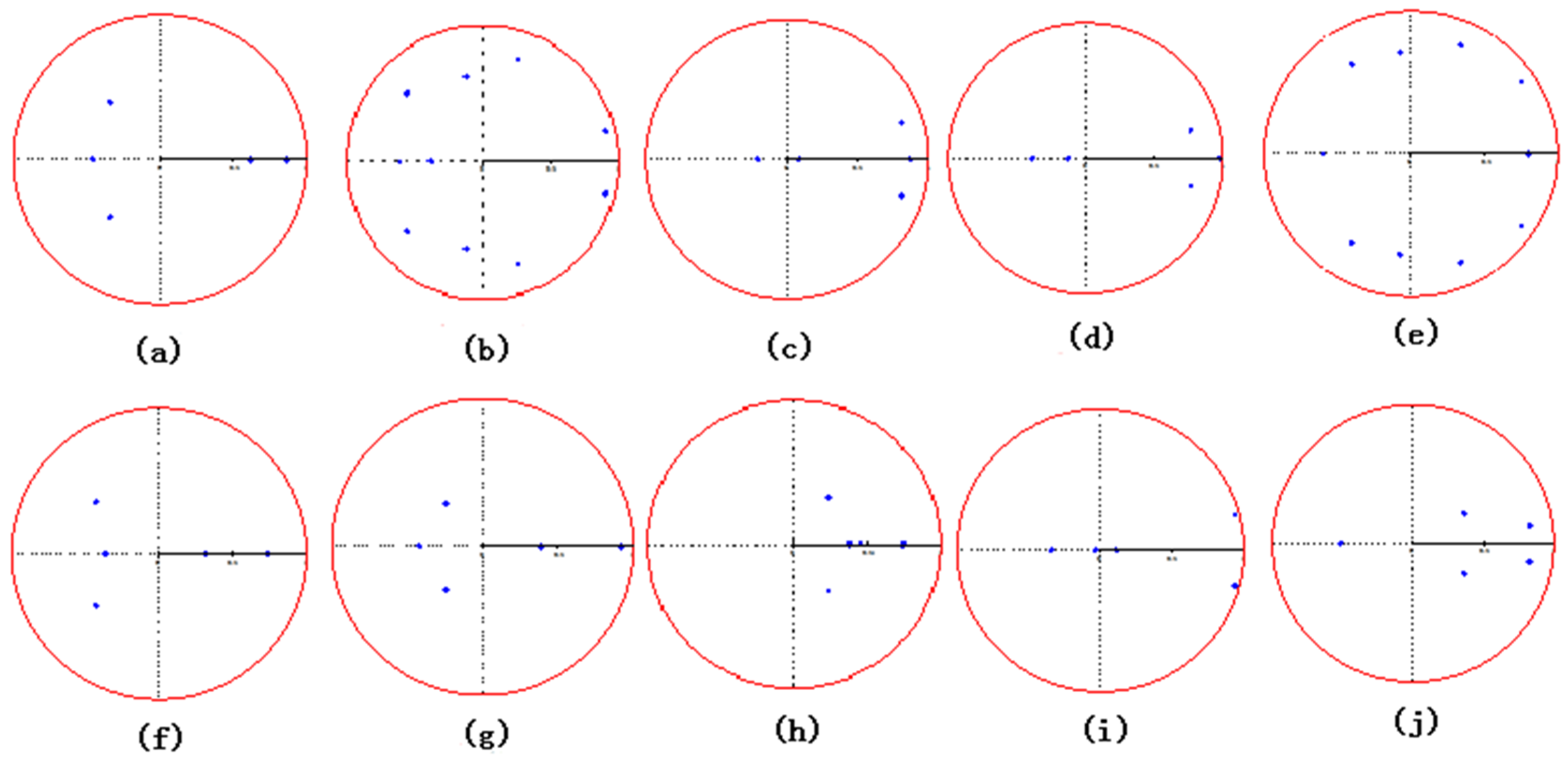

2. Methodology

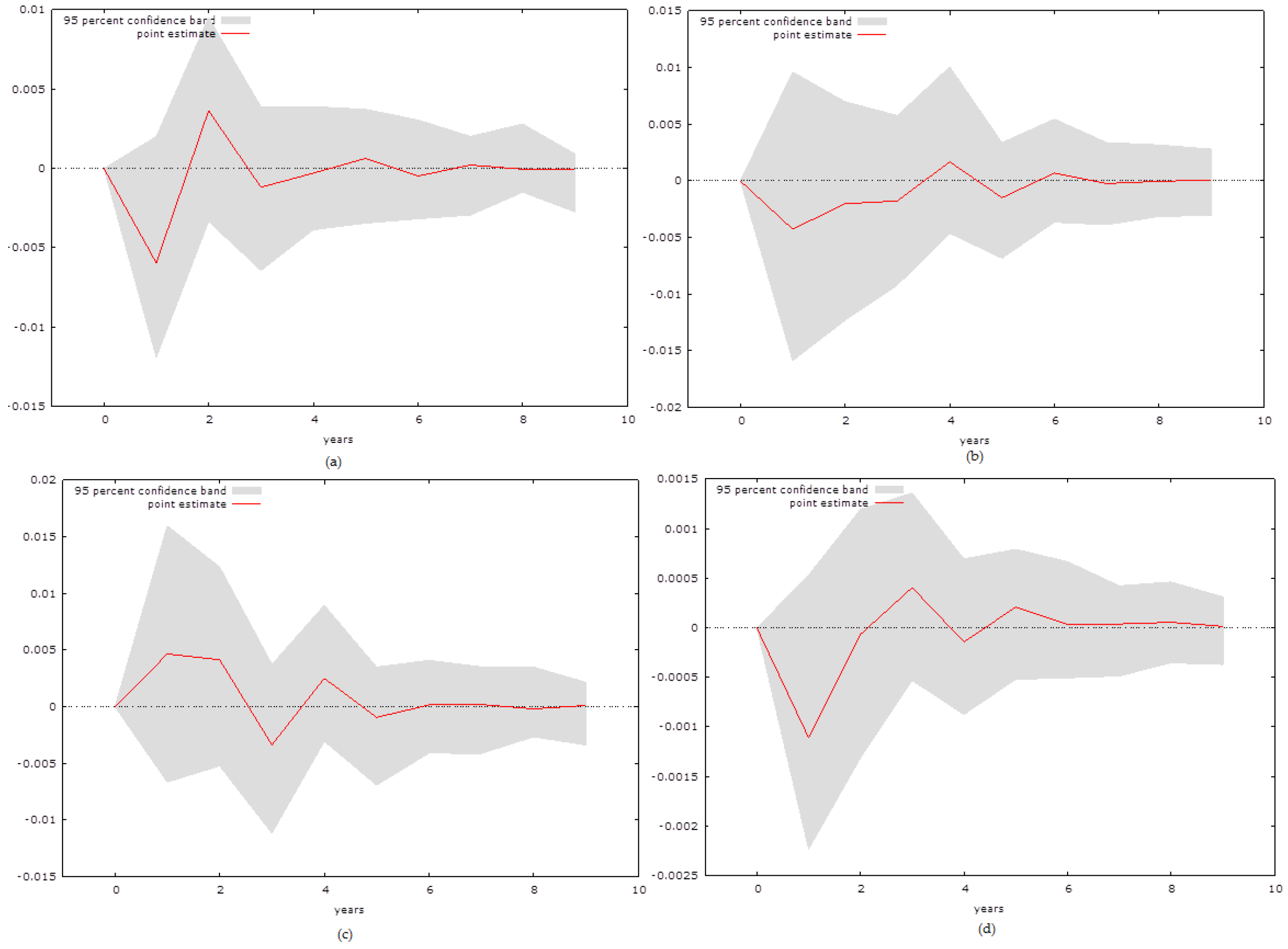

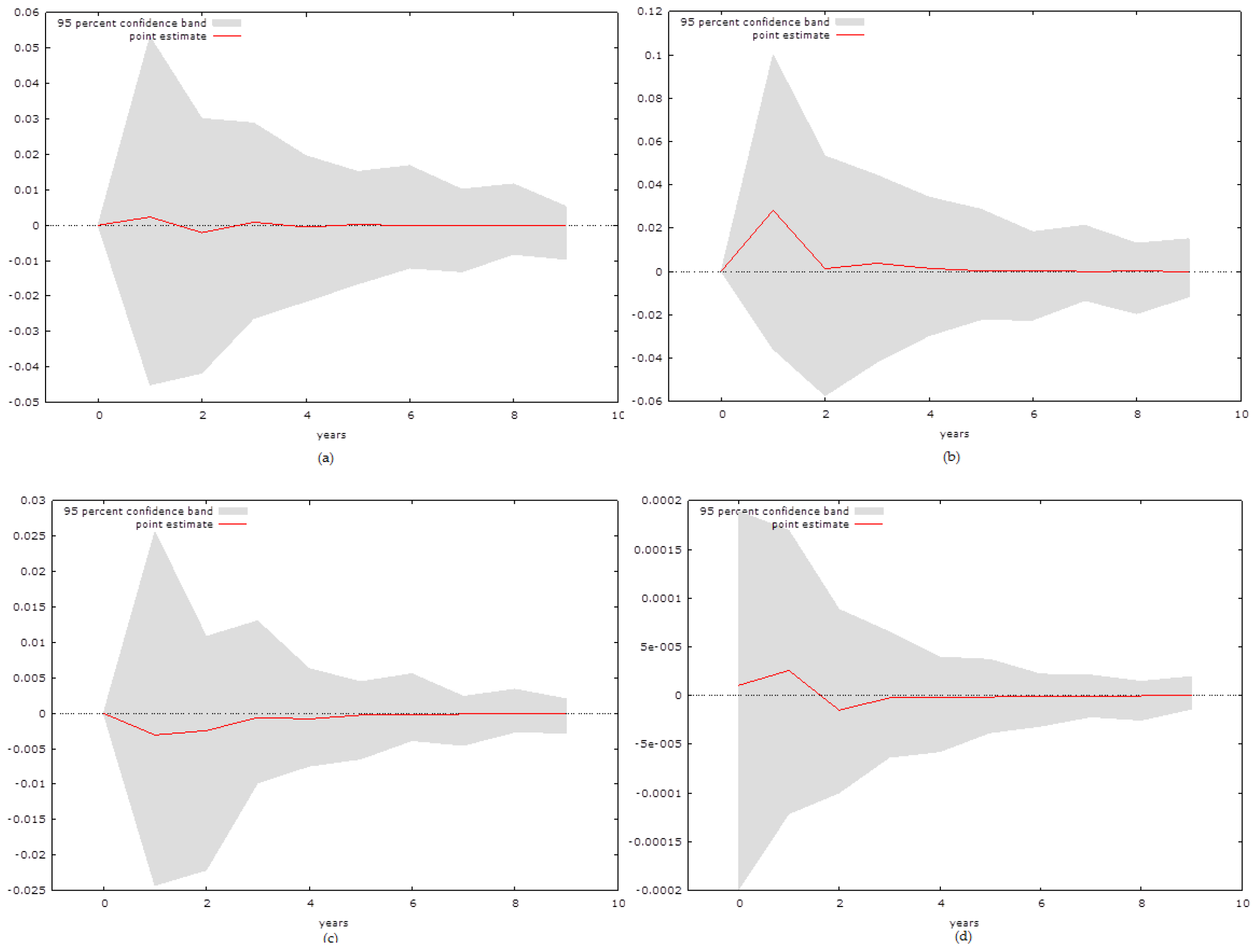

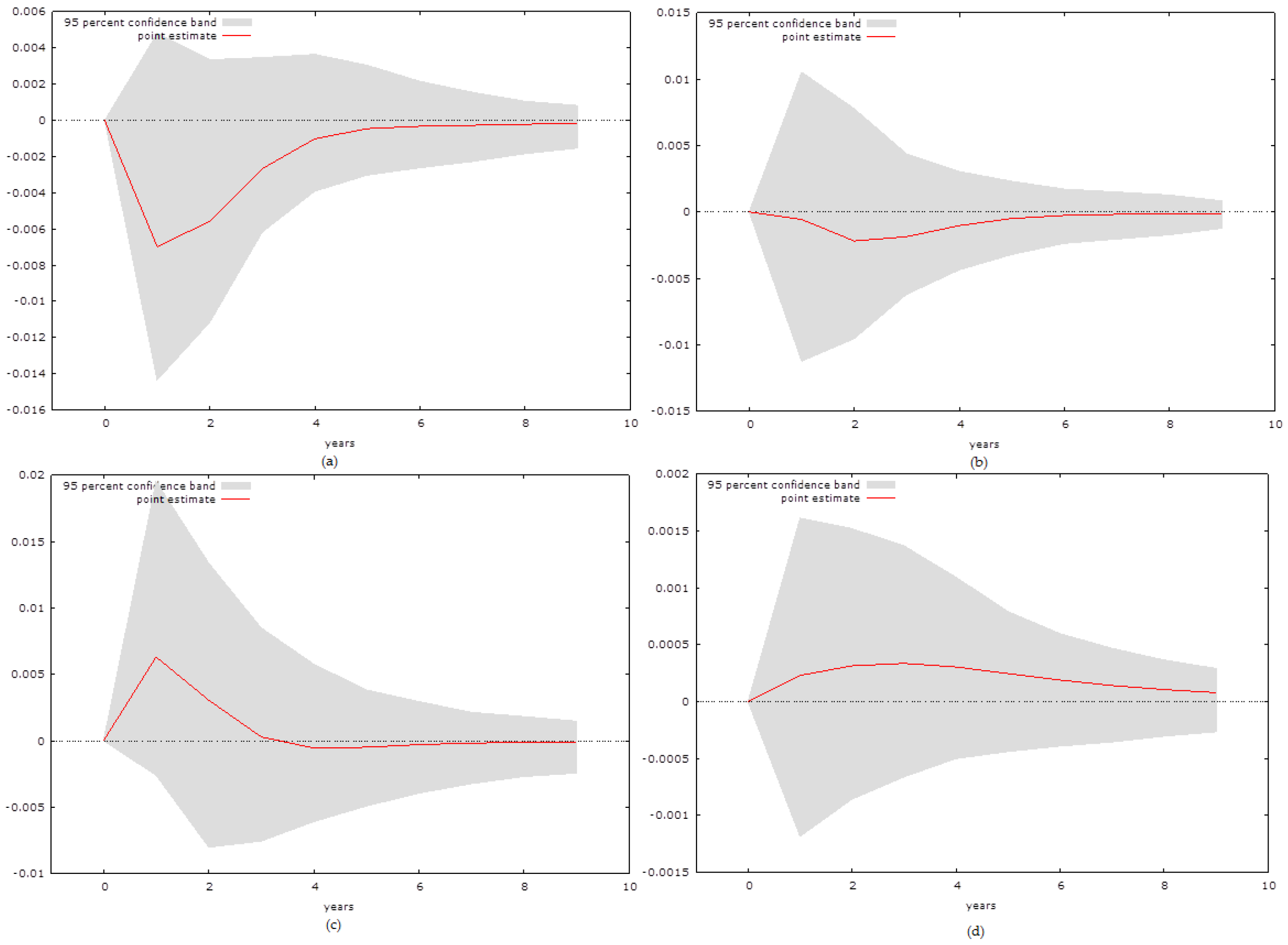

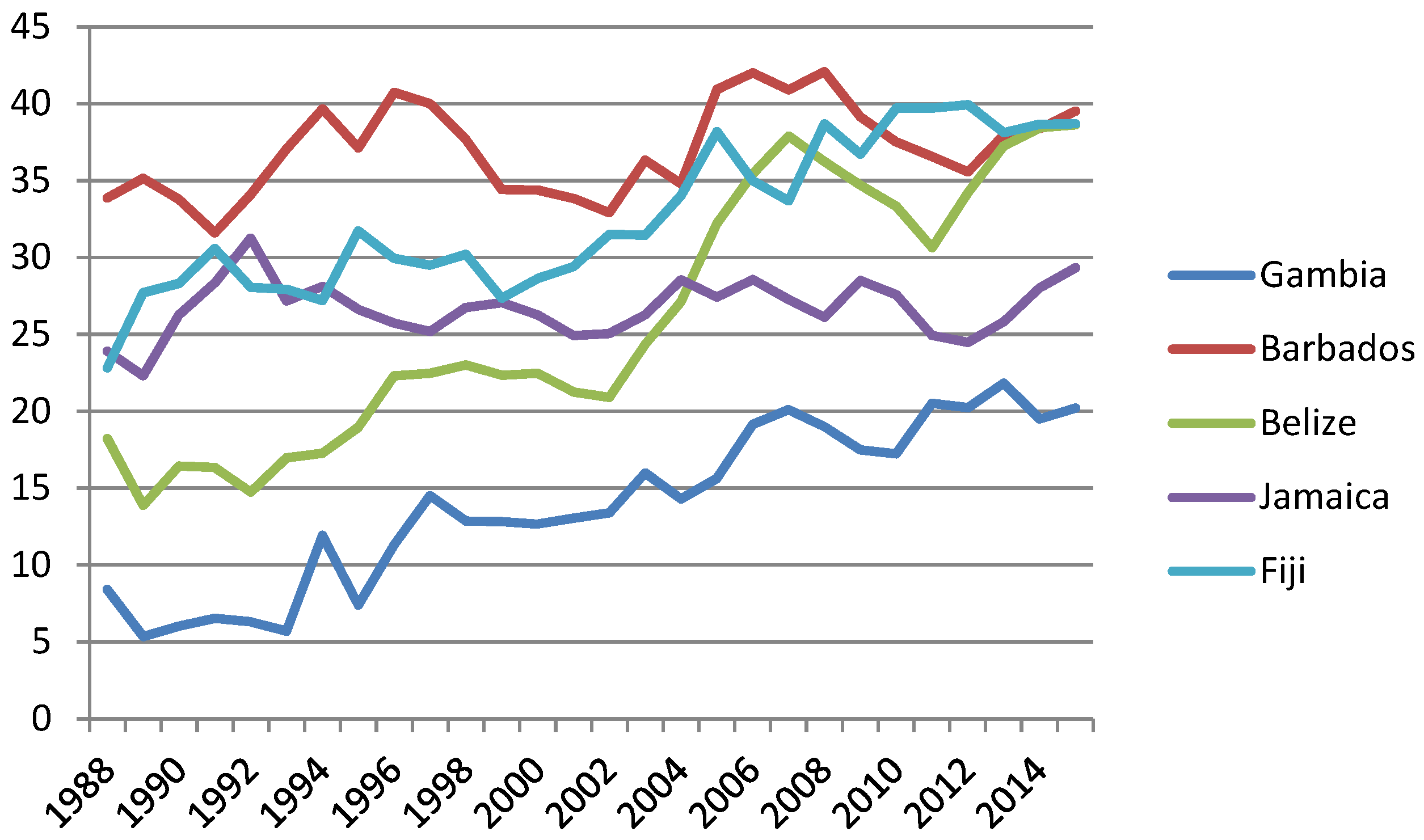

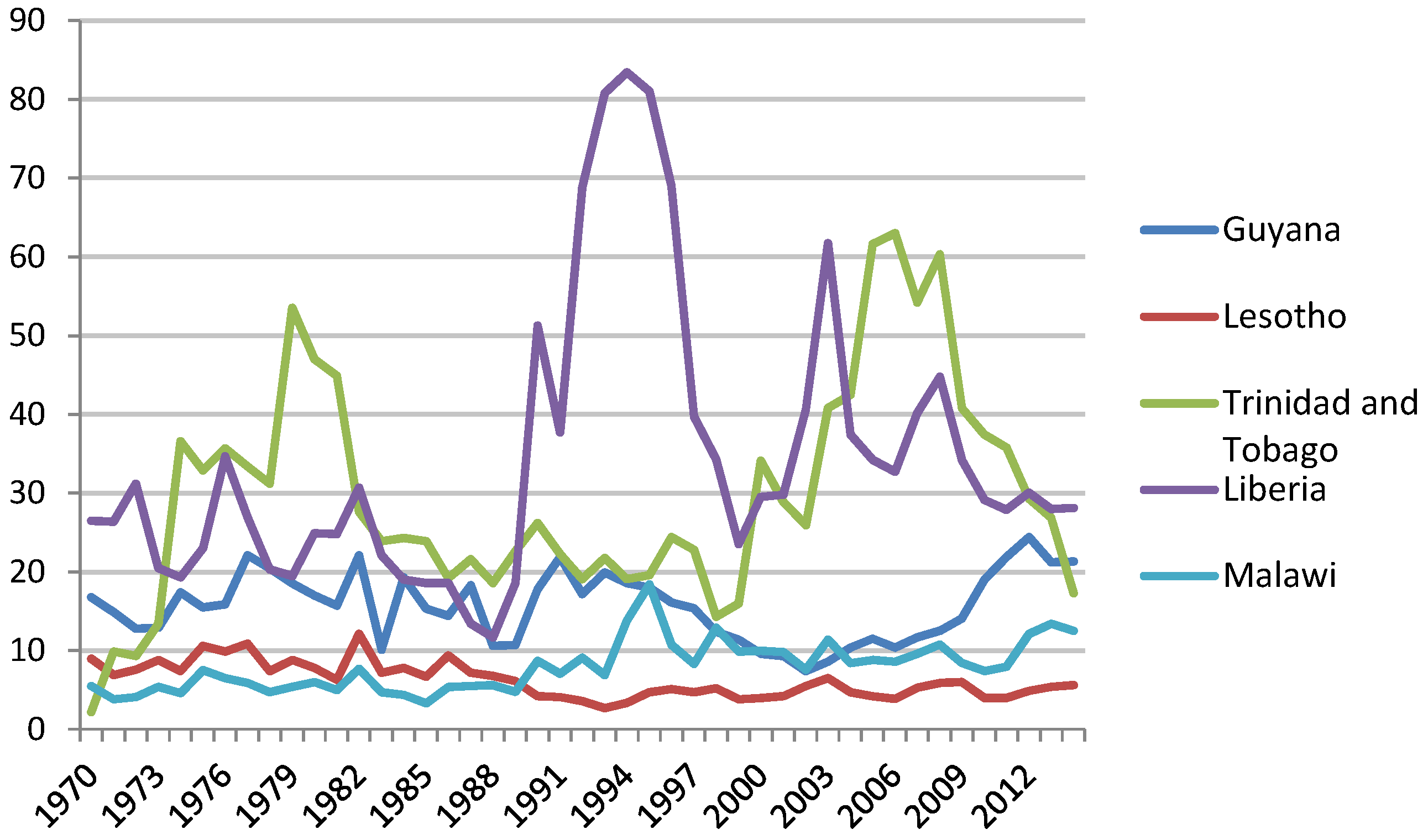

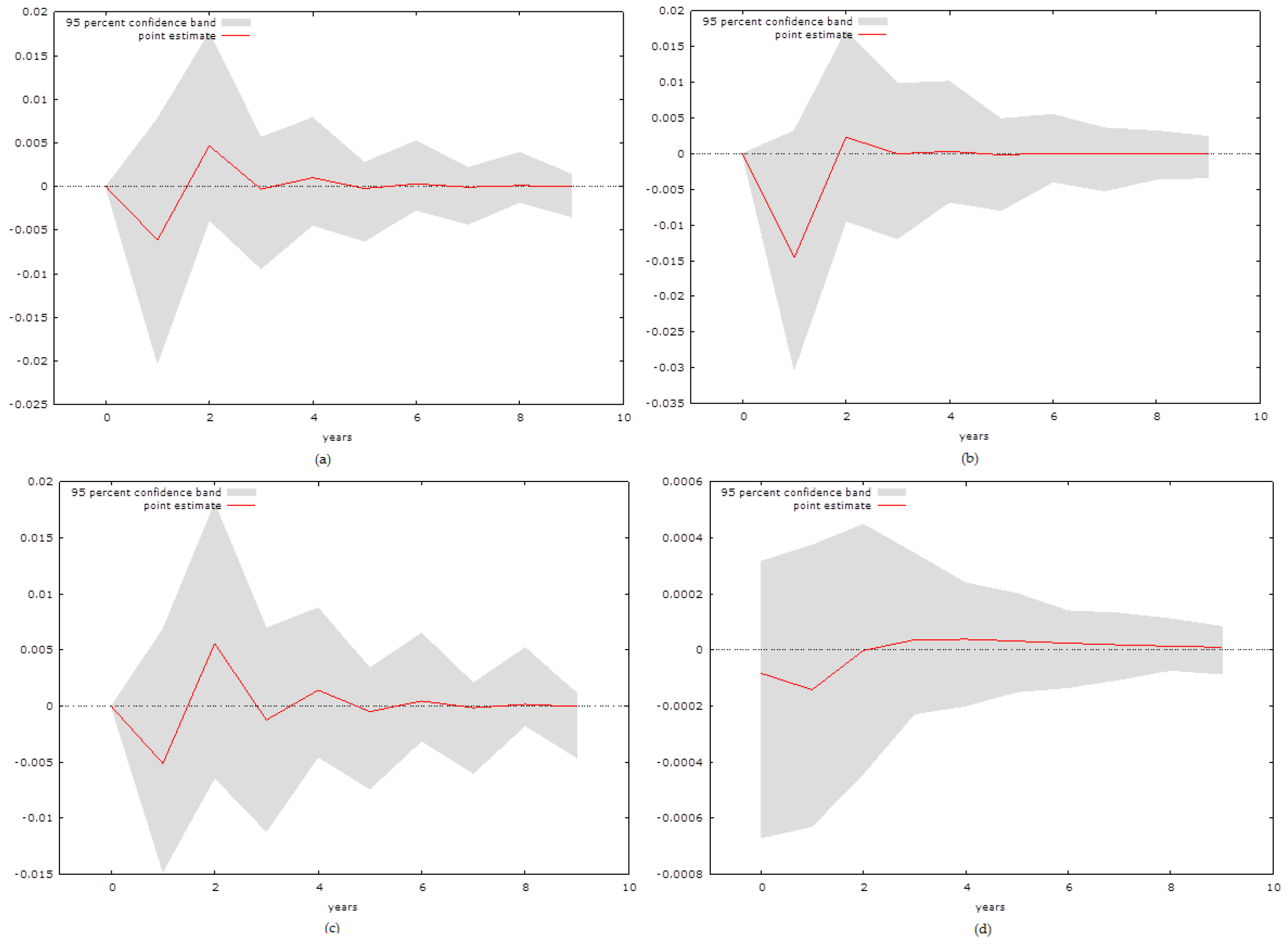

3. Results

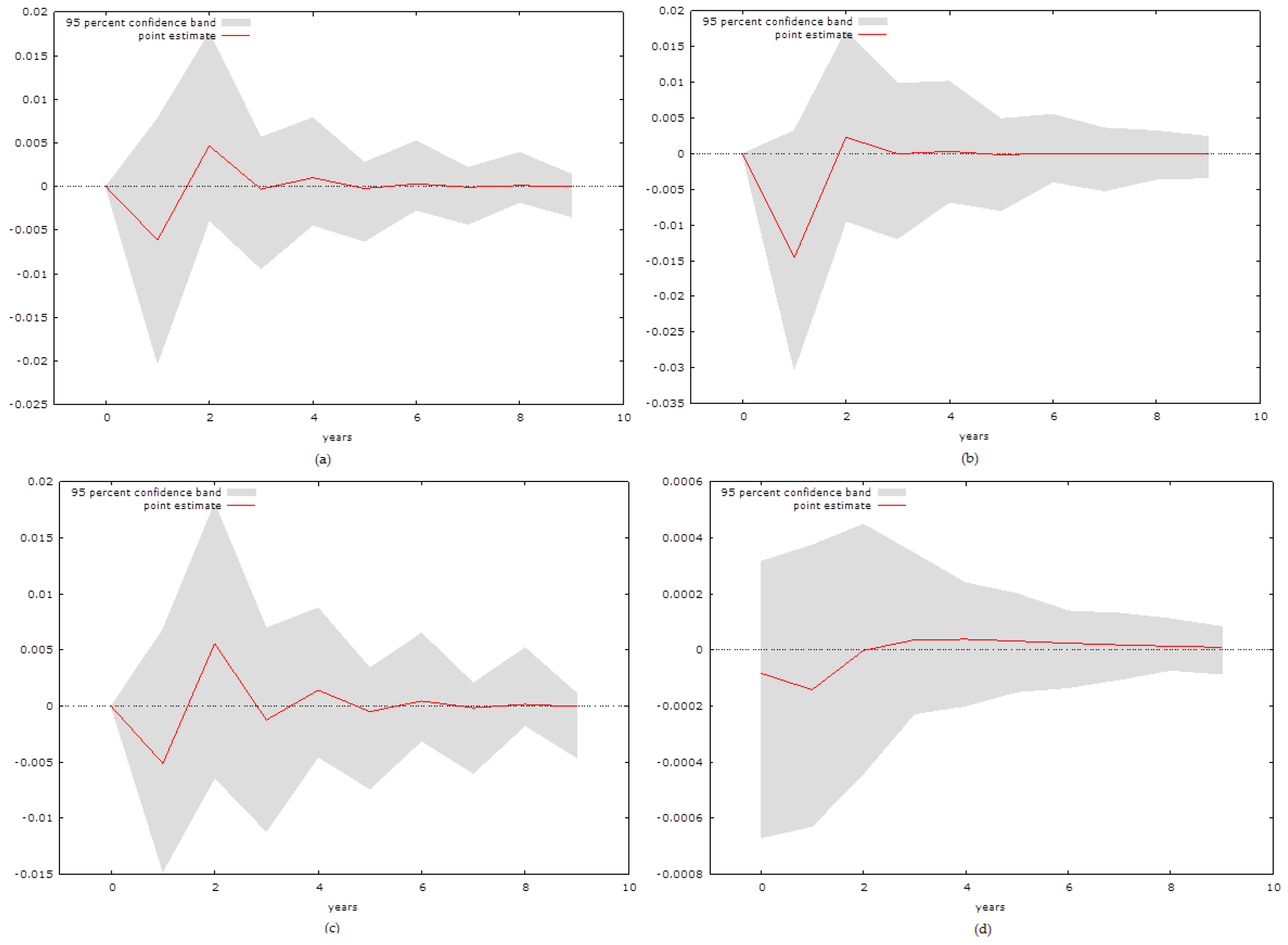

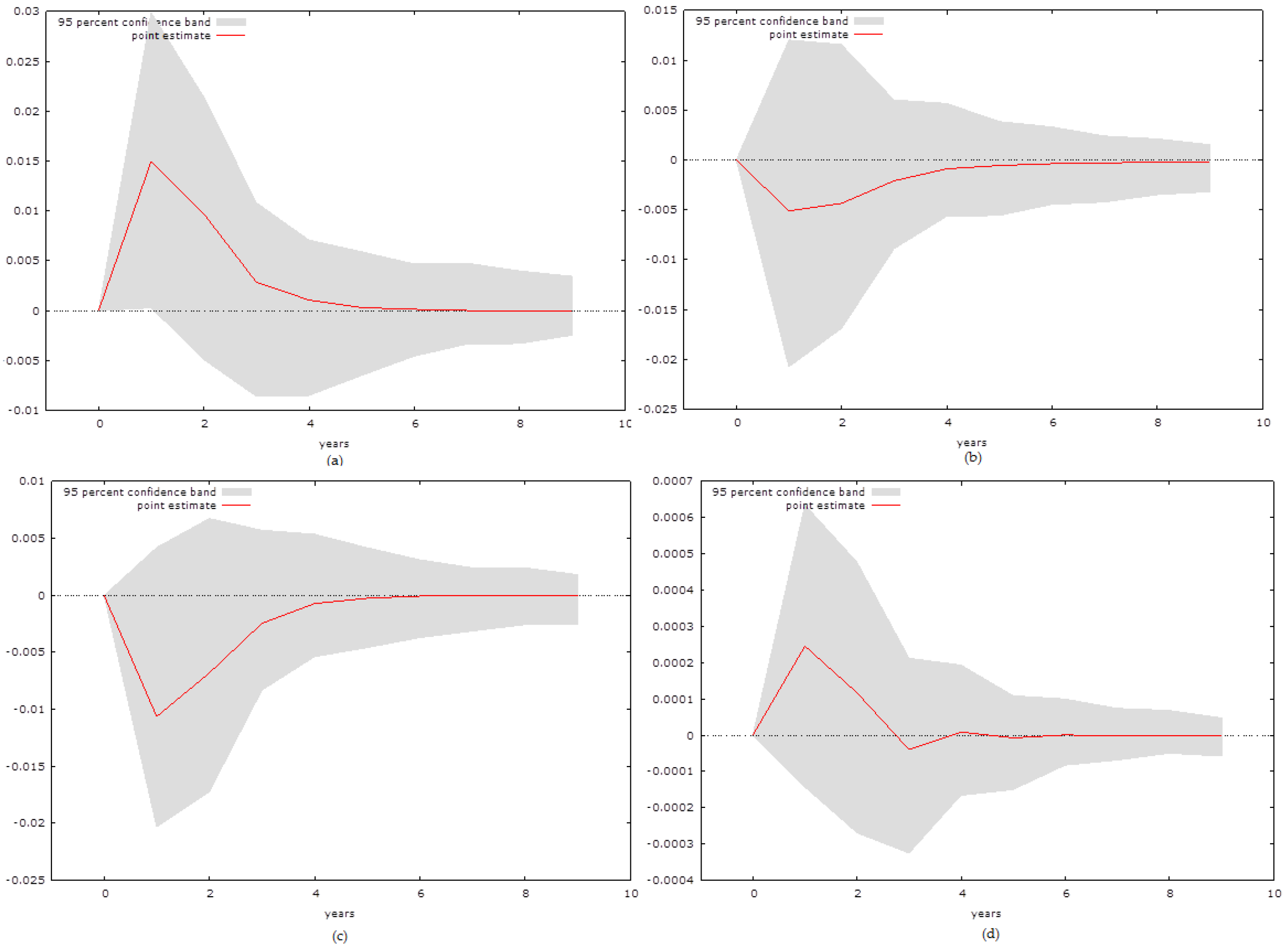

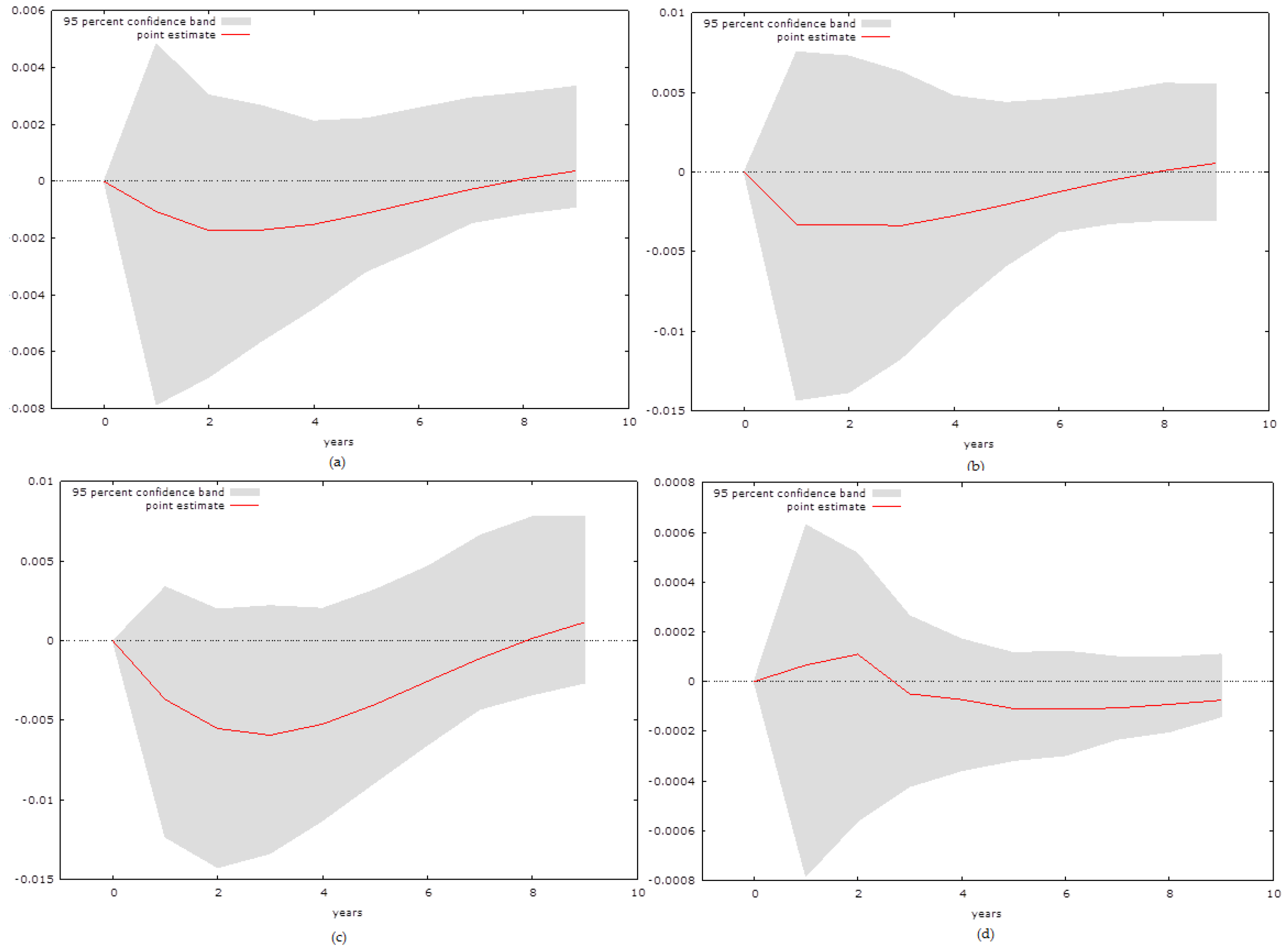

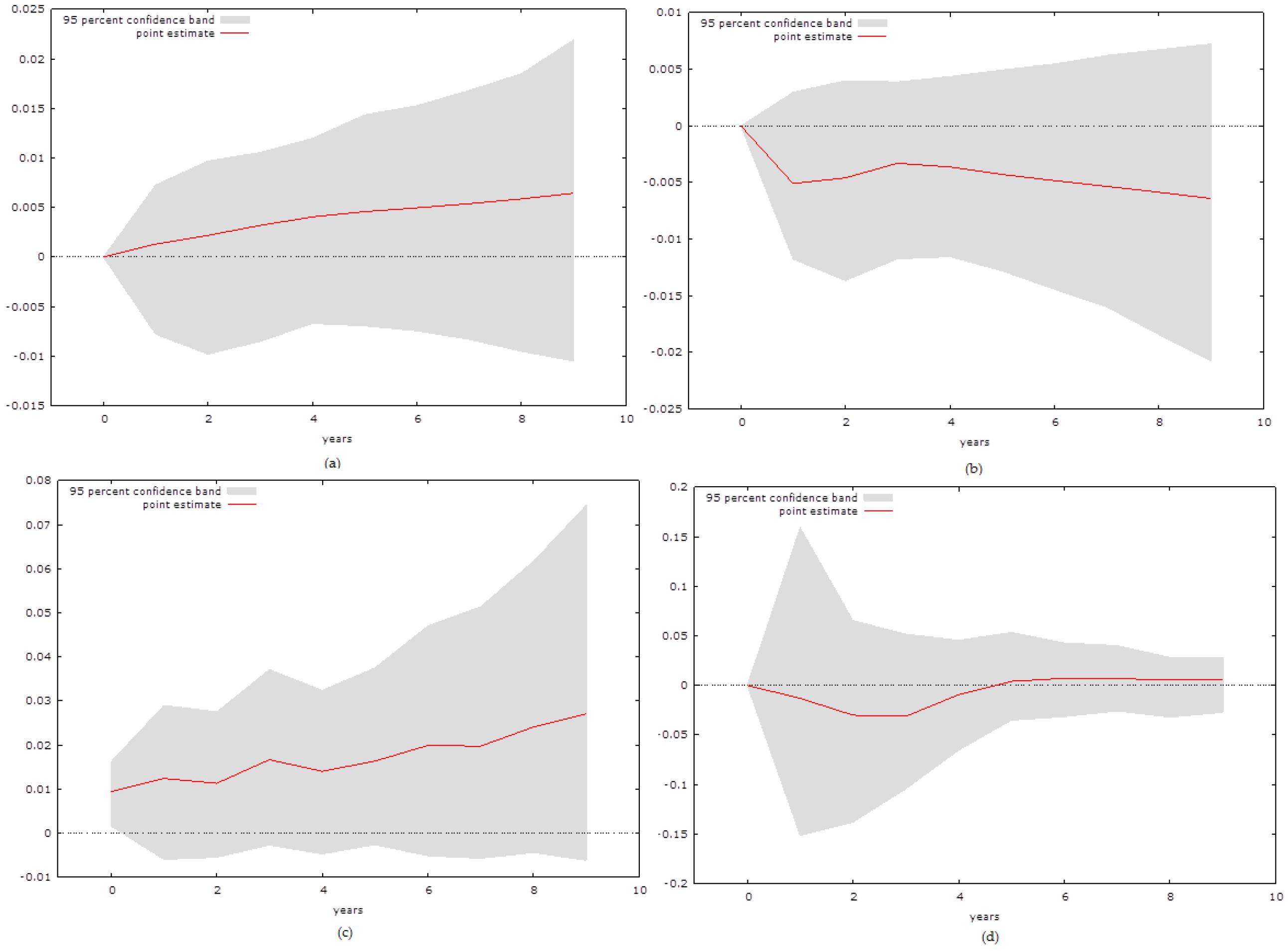

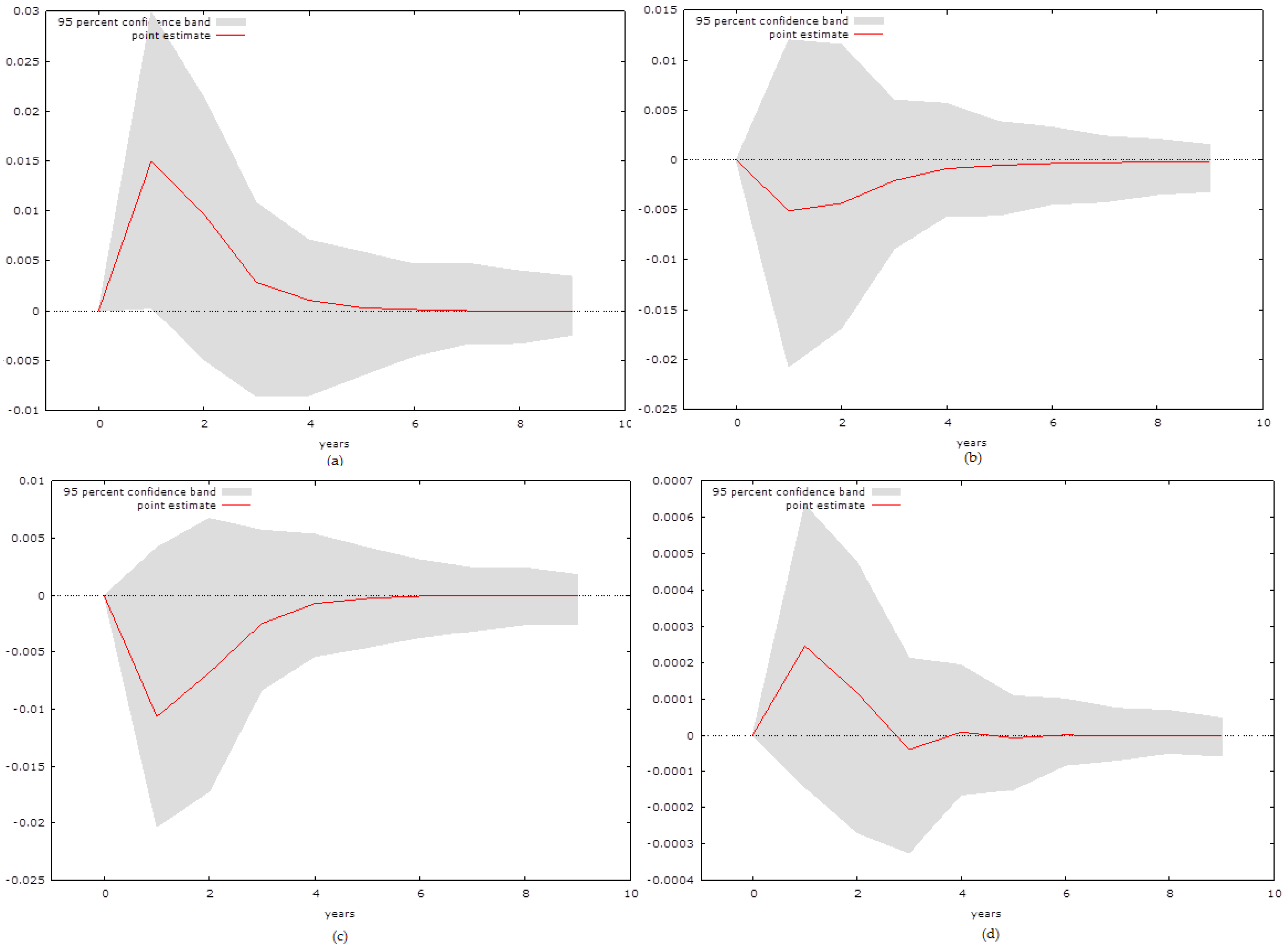

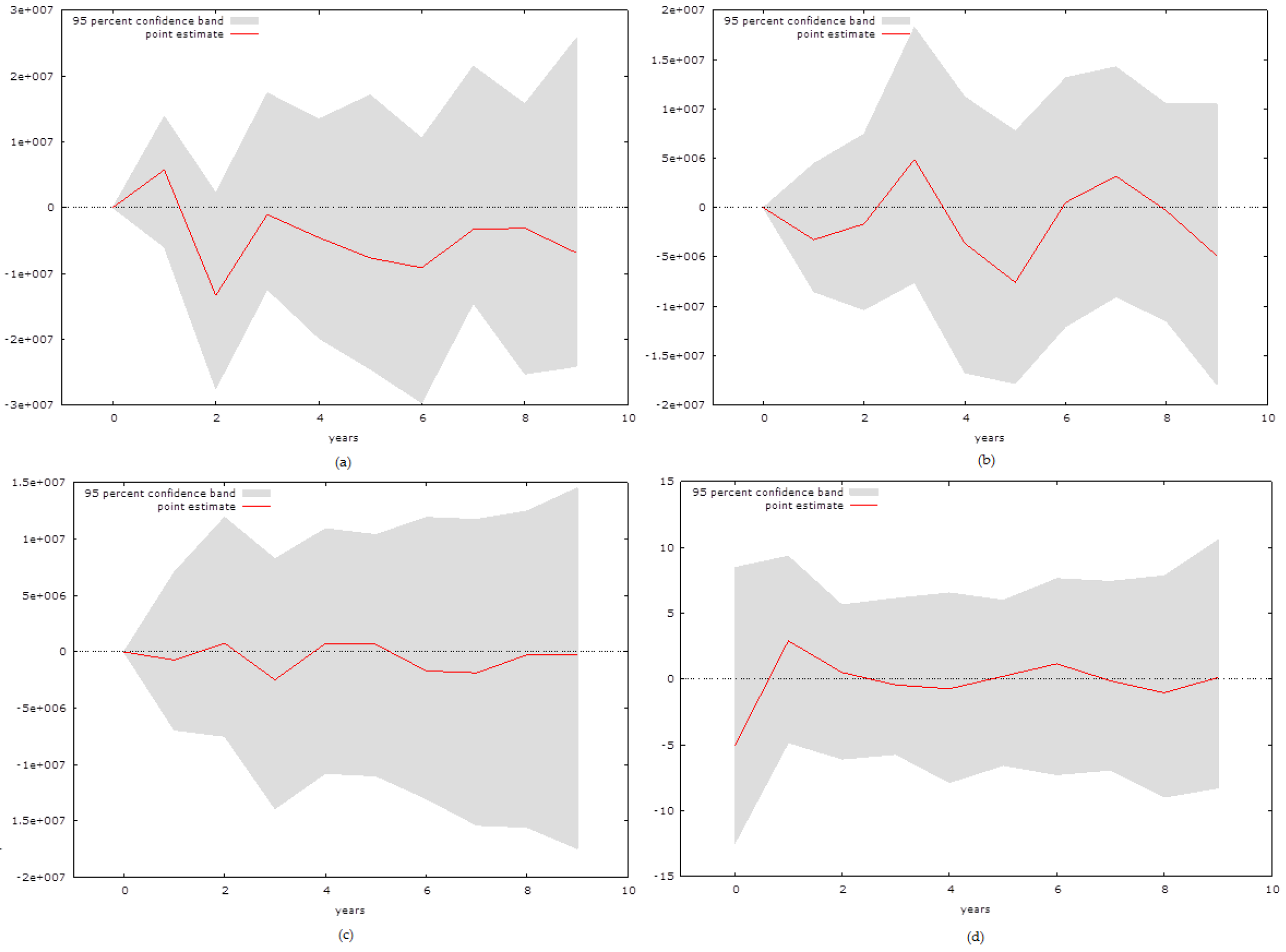

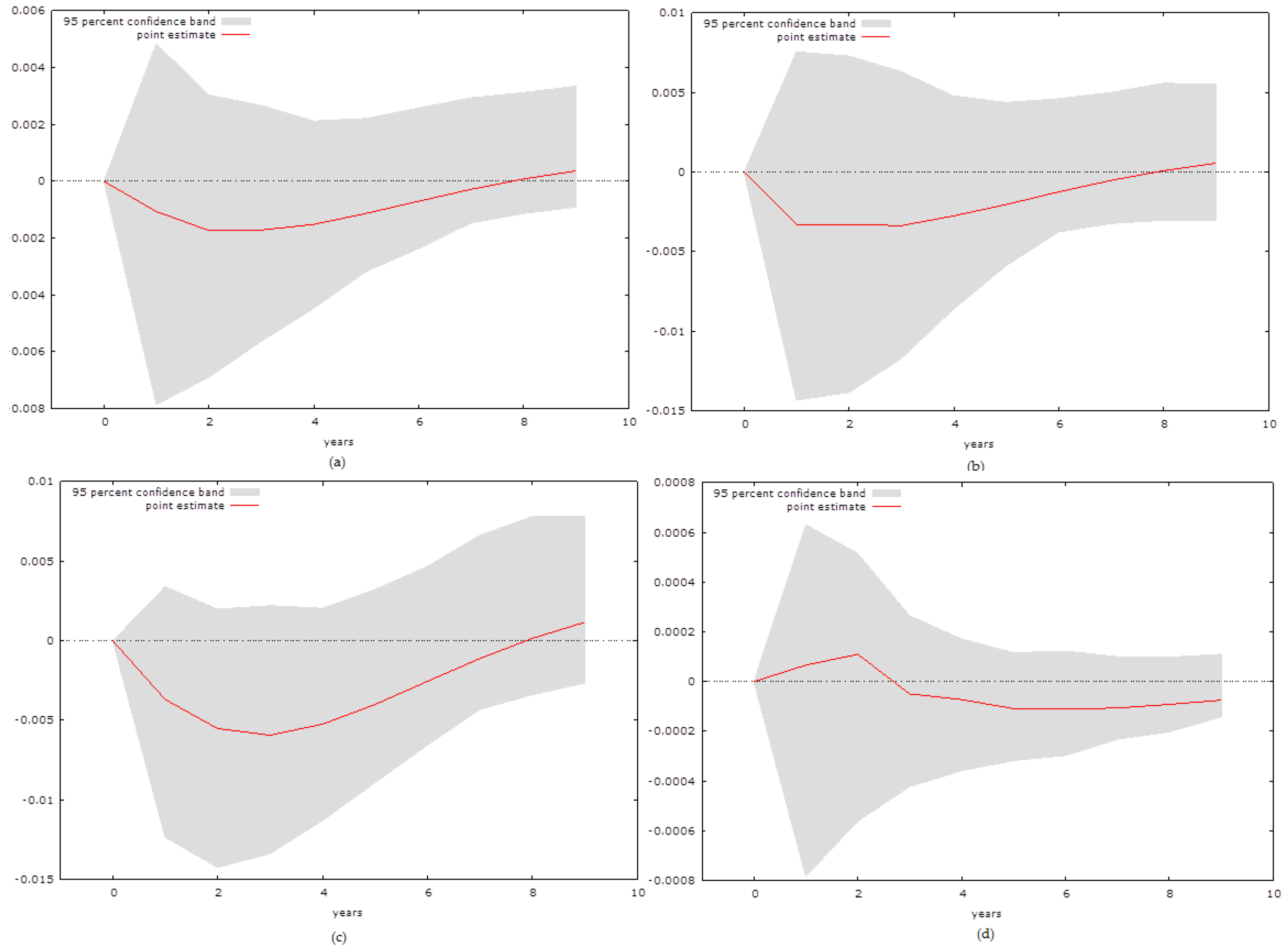

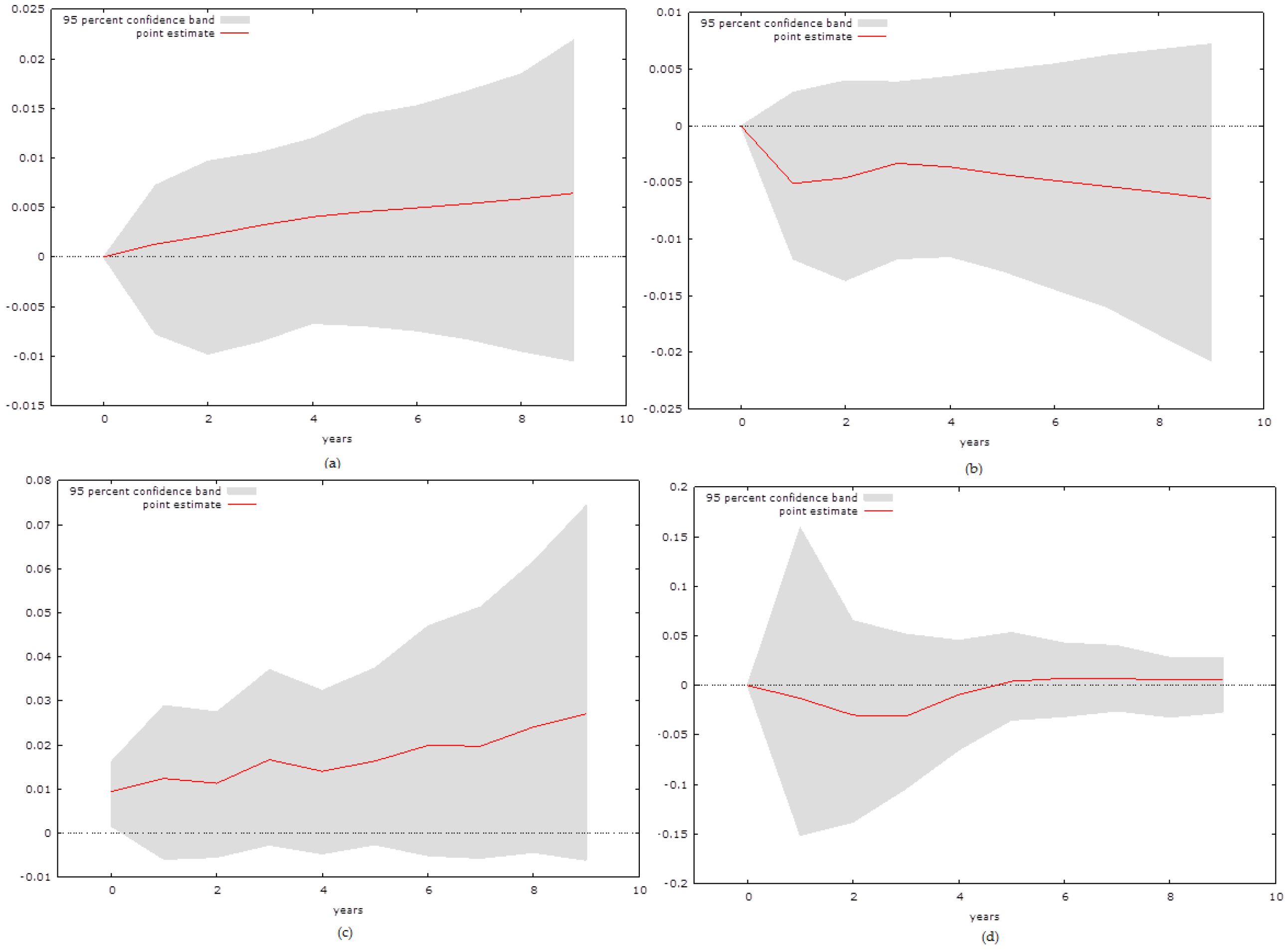

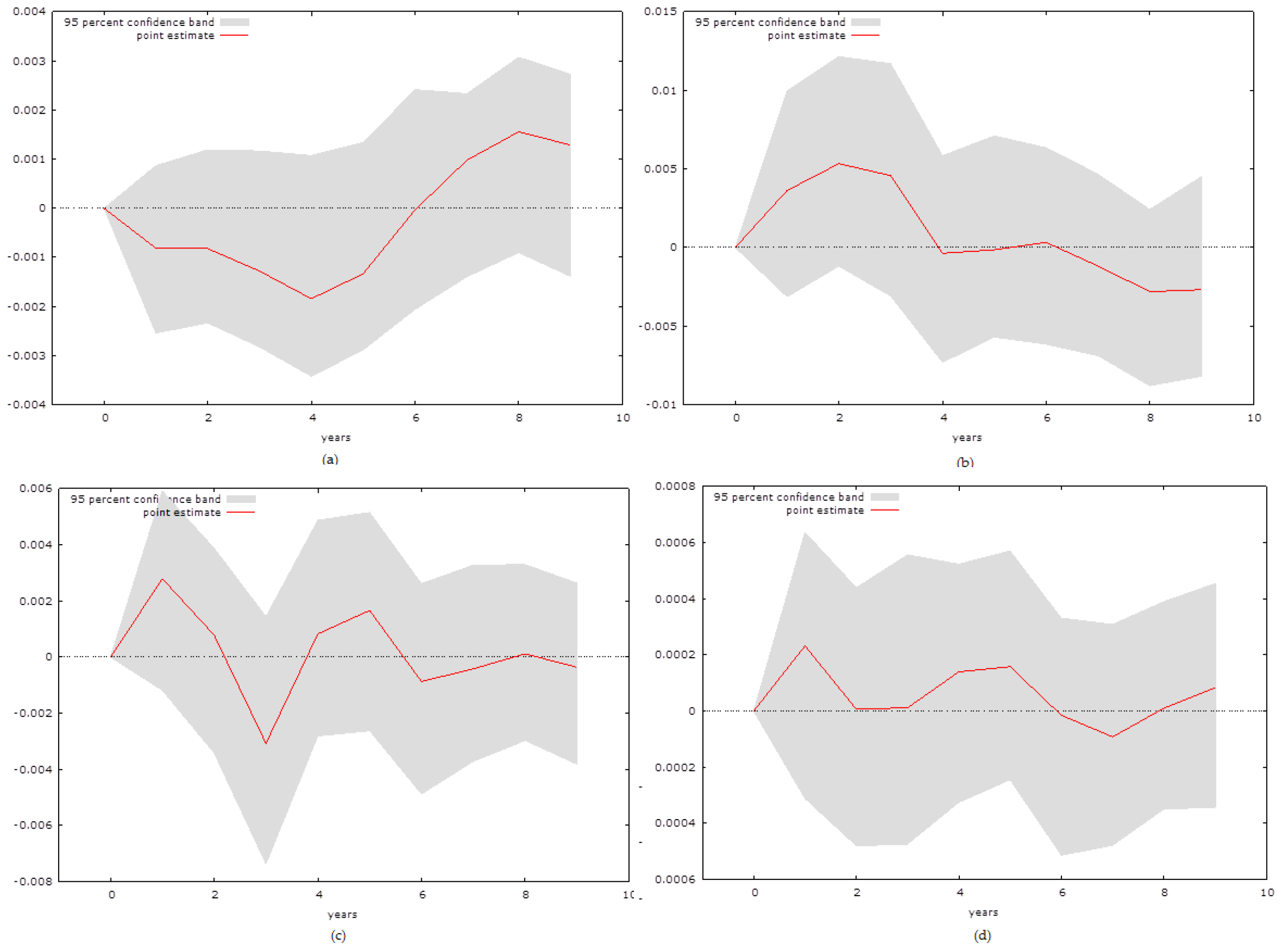

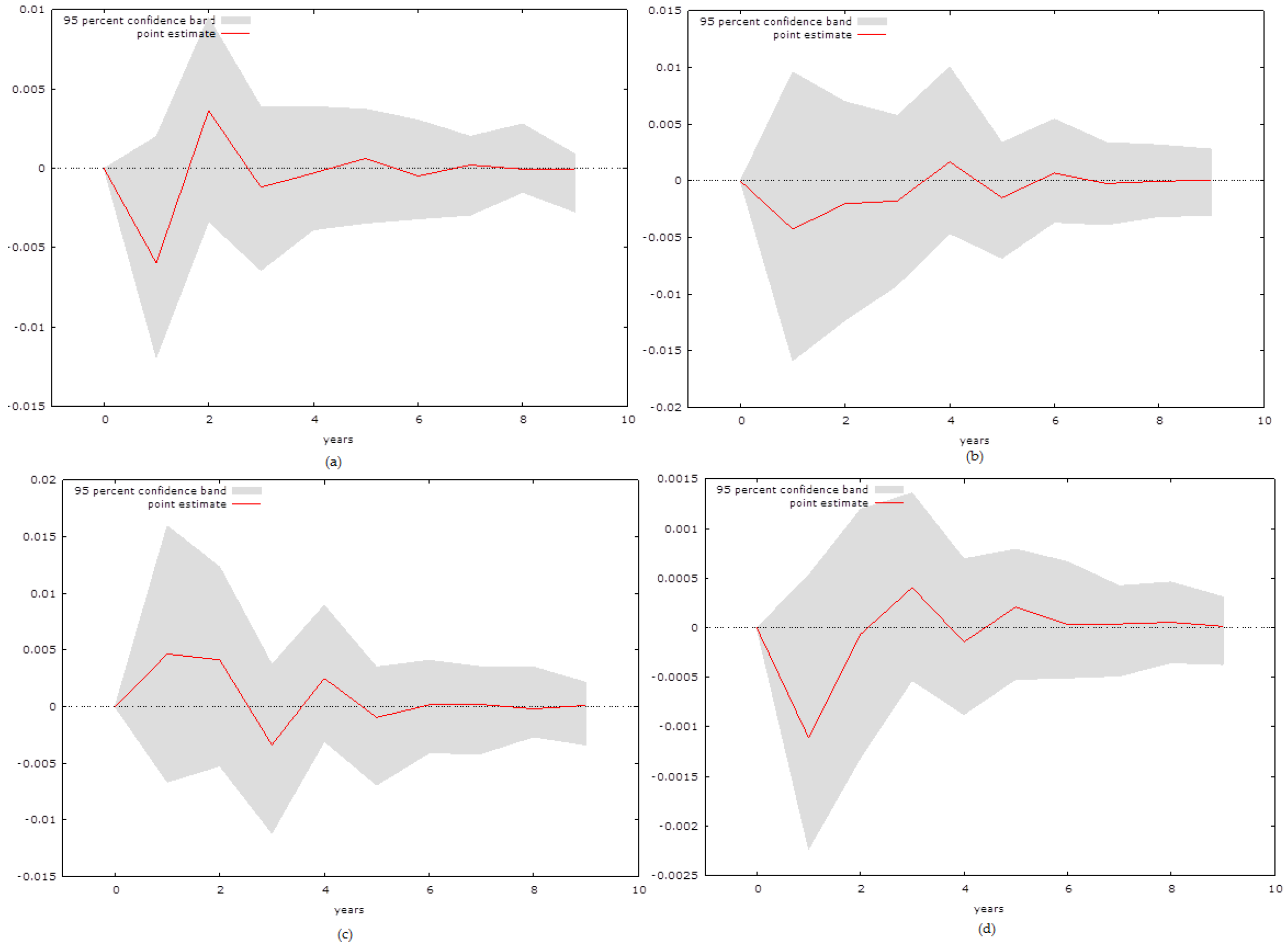

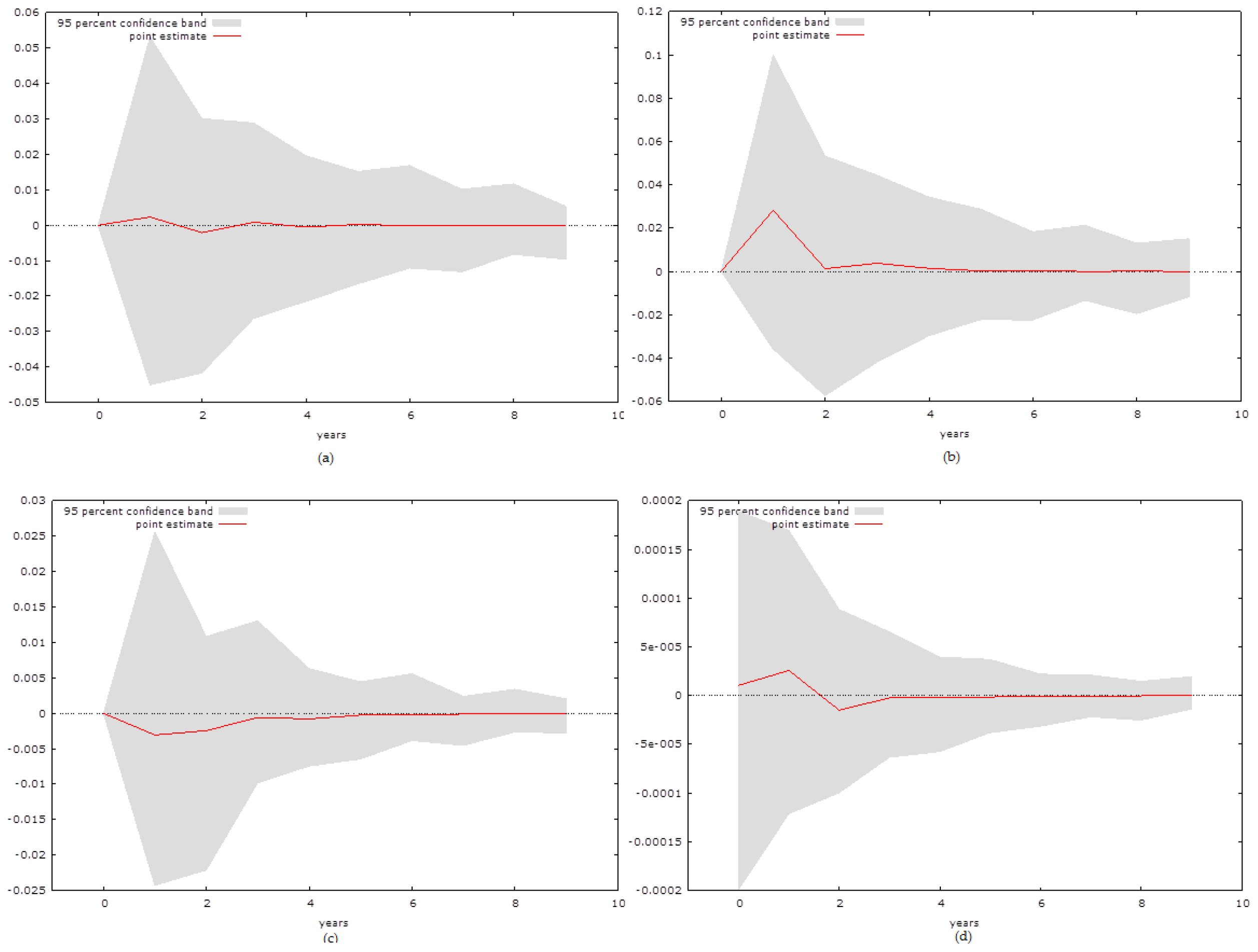

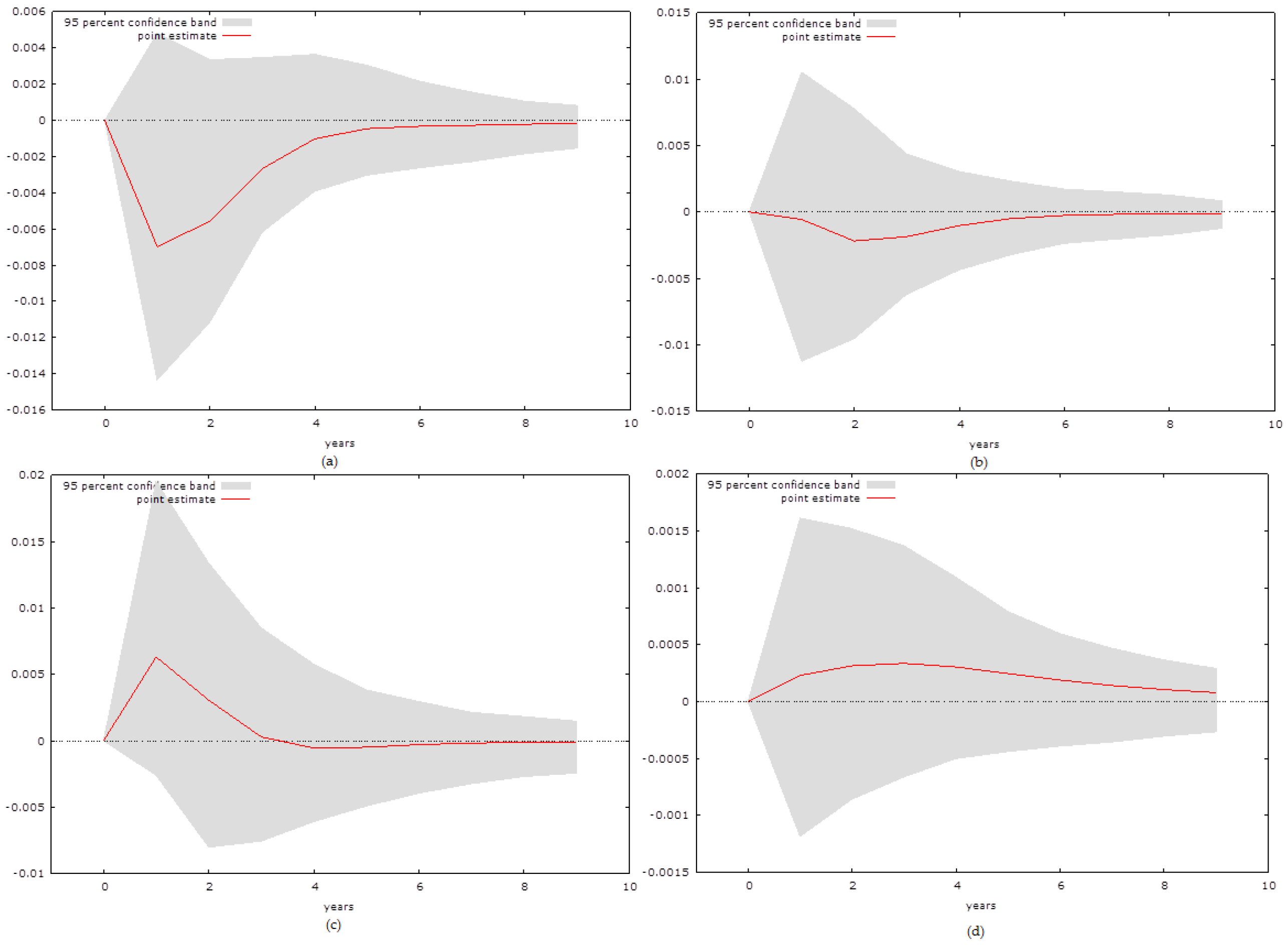

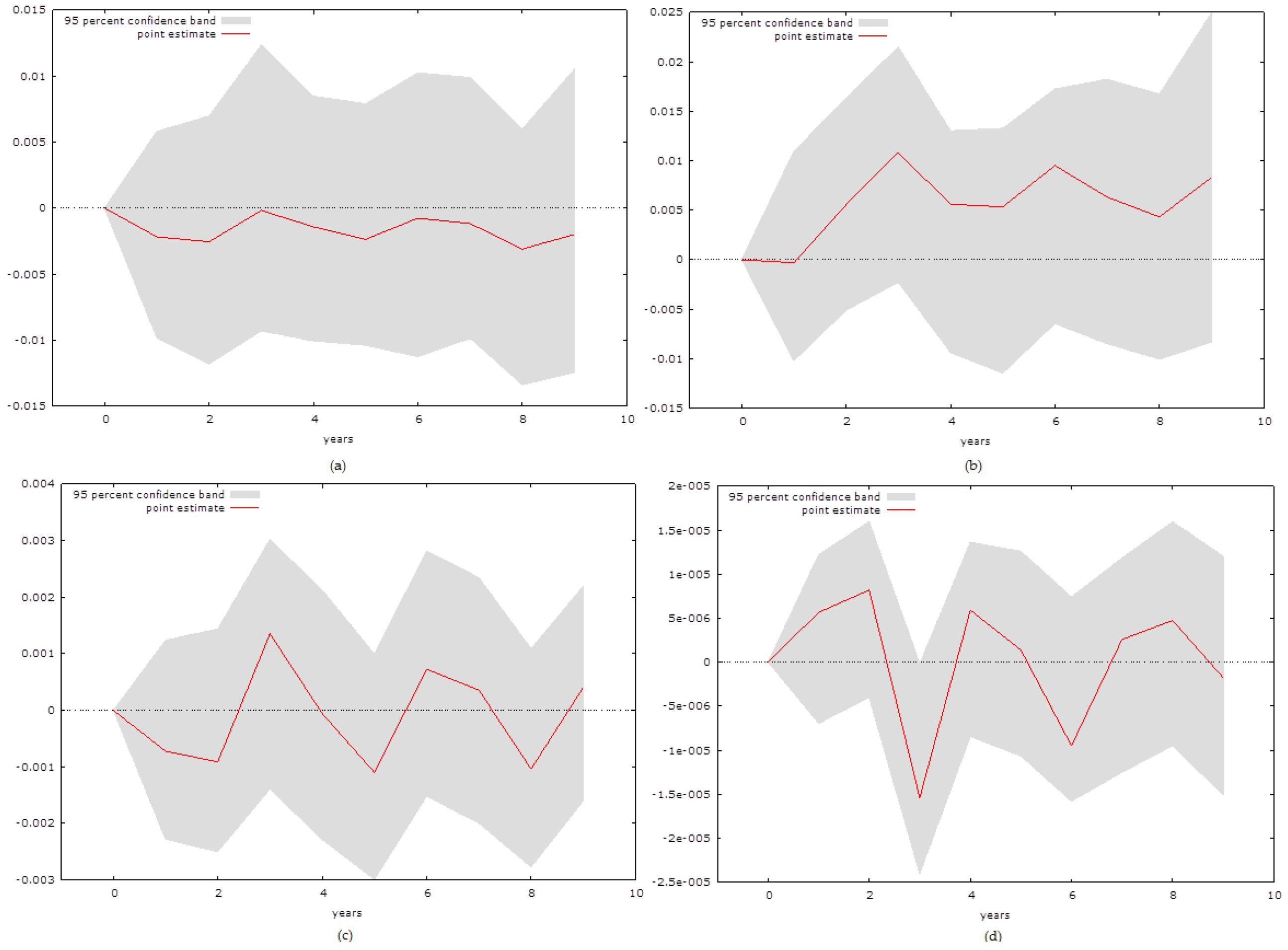

3.1. VAR IRF Results

4. Discussion

4.1. Discussion of Analysed Natural Resource-Dependent Economies

- (1)

- The negative impact of NC on economic growth is more evident in countries that are dependent upon the export of commodities whose prices are significantly influenced by shocks in the international market;

- (2)

- Generally, more diverse economies tend to have a smaller negative impact of NC on economic growth, as well as economies that export resources whose prices are less prone to shocks in the international market;

- (3)

- There is enough empirical evidence of the oil curse in the case of Trinidad and Tobago;

- (4)

- The negative effect is more pronounced in countries with a larger average TNRR, unless the commodity they are dependent on has a highly stable price and is difficult to substitute.

4.2. Discussion of Analysed Tourism-Dependent Economies

4.3. Theoretical Discussion Regarding the Natural Resource Curse and Human Capital

5. Conclusions

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | GDP | Tourism | HC | NC | GDPpc |

|---|---|---|---|---|---|

| The Gambia | –1.073 (0.782) | –3.548** (0.0068) | –0.134 (0.9943) | –1.895 (0.6566) | –2.803 (0.0507) |

| In first difference | –4.647** (0.0001) | / | –0.308 (0.9214) | –10.79** (0.0000) | –4.436** (0.00025) |

| In second difference | / | / | –7.628** (0.0000) | / | / |

| Trinidad and Tobago | –2.086 (0.2502) | –2.119 (0.237) | 1.153 (0.9979) | –4.678** (0.0075) | –2.138 (0.8004) |

| In first difference | –3.693** (0.0035) | –3.04* (0.031) | –1.356 (0.5795) | / | –3.097* (0.0361) |

| In second difference | / | / | –4.309** (0.0043) | / | / |

| Lesotho | 1.316 (0.9967) | –1.962 (0.2992) | –1.436 (0.5661) | –3.683** (0.0048) | 1.214 (0.9969) |

| In first difference | –3.509* (0.03829) | –4.903** (0.0011) | –0.767 (0.8043) | / | –4.115** (0.0059) |

| In second difference | / | / | –4.032** (0.0072) | / | / |

| Belize | –6.128** (0.0000) | –3.325** (0.0092) | 0.977 (0.9891) | –4.239** (0.0023) | –6.267** (0.0000) |

| In first difference | / | / | –1.232 (0.6364) | / | / |

| In second difference | / | / | –4.2549** (0.005) | / | / |

| Guyana | –2.694 (0.076) | –3.467** (0.0089) | –2.765 (0.2251) | –4.785** (0.0062) | 0.744 (0.9871) |

| In first difference | –4.507** (0.0011) | / | –1.205 (0.6481) | / | –4.012** (0.0073) |

| In second difference | / | / | –7.354** (0.0000) | / | / |

| Jamaica | –1.451 (0.8685) | –3.383* (0.0093) | –2.392 (0.1566) | –2.223 (0.2049) | –2.261 (0.1848) |

| In first difference | –5.176** (0.0000) | / | –8.781** (0.0000) | –5.283** (0.0000) | –4.986** (0.0001) |

| Fiji | –1.985 (0.2936) | –2.049 (0.2655) | –1.442 (0.563) | –1.623 (0.4604) | –1.262 (0.6496) |

| In first difference | –7.948** (0.0000) | –6.087** (0.0000) | –1.712 (0.4182) | –5.83** (0.0000) | –7.896** (0.0000) |

| In second difference | / | / | –6.325** (0.0000) | / | / |

| Liberia | –0.9836 (0.7144) | –1.15 (0.649) | –1.541 (0.5421) | –2.234 (0.194) | –0.7063 (0.708) |

| In first difference | –9.479** (0.0000) | –4.205** (0.0013) | –4.253** (0.00007) | –10.744** (0.0000) | –4.759** (0.0002) |

| Malawi | 1.039 (0.9971) | –2.583 (0.093) | –1.847 (0.3578) | –3.067* (0.0456) | 0.056 (0.9624) |

| In first difference | –3.741* (0.0125) | 4.9047** (0.0000) | –1.032 (0.5521) | / | –4.137 (0.0053) |

| In second difference | / | / | –4.237** (0.0046) | / | / |

| Barbados | –2.767 (0.0817) | –2.695 (0.0747) | –1.218 (0.6687) | 1.696 (0.997) | –2.83 (0.0728) |

| In first difference | –3.146* (0.041) | –4.025** (0.0071) | –5.523** (0.0000) | –5.9101** (0.0000) | –3.142* (0.041) |

| Country | Autocorrelation GDP equation | Autocorrelation HC equation | ARCH GDP equation | ARCH HC equation |

|---|---|---|---|---|

| The Gambia | 0.34 (0.56) | 0.155 (0.866) | 0.008 (0.929) | 0.162 (0.779) |

| Trinidad and Tobago | 0.454 (0.5) | 1.502 (0.22) | 0.319 (0.572) | 1.766 (0.183) |

| Lesotho | 0.8505 (0.356) | 0.124 (0.899) | 0.549 (0.4587) | 0.266 (0.623) |

| Belize | 0.925 (0.336) | 0.943 (0.331) | 0.742 (0.3889) | 0.701 (0.403) |

| Guyana | 1.641 (0.201) | 0.021 (0.804) | 0.181 (0.671) | 0.966 (0.325) |

| Jamaica | 1.005 (0.316) | 0.988 (0.321) | 2.307 (0.1287) | 0.8591 (0.354) |

| Fiji | 0.2456 (0621) | 0.227 (0.633) | 0.144 (0.704) | 0.093 (0.7599) |

| Liberia | 0.2516 (0.616) | 1.099 (0.294) | 0.148 (0.7003) | 1.0054 (0.3159) |

| Malawi | 0.421 (0.431) | 0.187 (0.821) | 0.625 (0.428) | 0.055 (0.814) |

| Barbados | 0.583 (0.445) | 0.196 (0.658) | 0.079 (0.7788) | 0.324 (0.569) |

| Dependent variable | Cholesky ordering |

|---|---|

| GDP | GDP, GDPpc, Tourism, NC, HC. |

| HC | HC, GDPpc, GDP, Tourism, NC. |

Appendix B

References

- T. Gylfason. “Natural Resources and Economic Growth: From Dependence to Diversification.” In Economic Liberalization and Integration Policy: Options for Eastern Europe and Russia. Edited by H.G. Broadman, T. Paas and P.J.J. Welfens. Berlin, Germany: Springer, 2006, pp. 201–231. [Google Scholar]

- N.R. Goodwin. Five Kinds of Capital: Useful Concepts for Sustainable Development. Global Development and Environment Institute Working Paper; Medford, MA, USA: Tufts University, 2003, Available online: http://www.ase.tufts.edu/gdae/publications/working_papers/03–07sustainabledevelopment.PDF (accessed on 28 June 2016).

- R.W. England. “Should we pursue measurement of the natural capital stock? ” Ecol. Econ. 27 (1998): 257–266. [Google Scholar] [CrossRef]

- D.W. Pearce, and R.K. Turner. Economics of Natural Resources and the Environment. Baltimore, MD, USA: Johns Hopkins University Press, 1990, pp. 51–53. [Google Scholar]

- H. Daly. “Operationalizing sustainable development by investing in natural capital.” In Investing in Natural Capital. Edited by A.M. Jansson, M. Hammer, C. Folke and R. Costanza. Washington, DC, USA: Island Press, 1994. [Google Scholar]

- F. Berkes, and C. Folke. “Investing in cultural capital for sustainable use of natural capital.” In Investing in Natural Capital. Edited by A.M. Jansson, M. Hammer, C. Folke and R. Costanza. Washington, DC, USA: Island Press, 1994. [Google Scholar]

- F. Van der Ploeg. “Natural Resources: Curse or Blessing? ” J. Econ. Lit. 49 (2011): 366–420. [Google Scholar] [CrossRef]

- R. Torvik. “Why do some resource-abundant countries succeed while others do not? ” Oxf. Rev. Econ. Policy 25 (2009): 241–256. [Google Scholar] [CrossRef]

- F. Hinterberger, F. Luks, and F. Schmidt-Bleek. “Material flows vs. ‘natural capital’: What makes an economy sustainable? ” Ecol. Econ. 23 (1997): 1–14. [Google Scholar] [CrossRef]

- G. Atkinson, and K. Hamilton. “Savings, growth and the resource curse hypothesis.” World Dev. 31 (2003): 1793–1807. [Google Scholar] [CrossRef]

- K. Hamilton, and G. Atkinson. Wealth, Welfare and Sustainability: Advances in Measuring Sustainable Development. Northampton, MA, USA: Edward Elgar Publishing, 2006. [Google Scholar]

- D.A. Fleming, T.G. Measham, and D. Paredes. “Understanding the resource curse (or blessing) across national and regional scales: Theory, empirical challenges and an application.” Aust. J. Agric. Res. Econ. 59 (2015): 624–639. [Google Scholar] [CrossRef]

- D.A. Fleming, and T.G. Measham. “Income Inequality across Australian Regions during the Mining Boom: 2001–11.” Aust. Geogr. 46 (2015): 203–216. [Google Scholar] [CrossRef]

- R.J. Barro. “Economic Growth in a Cross Section of Countries.” Q. J. Econ. 106 (1991): 407–443. Available online: http://www.nber.org/papers/w3120 (accessed on 29 June 2016). [Google Scholar] [CrossRef]

- R. Judson. “Measuring Human Capital Like Physical Capital: What Does It Tell us? ” Bull. Econ. Res. 54 (2002): 209–231. [Google Scholar] [CrossRef]

- R. Costanza, M. Hart, S. Posner, and J. Talberth. Beyond GDP: The Need for New Measures of Progress. The Pardee Papers; Boston, MA, USA: Boston University, 2009, Available online: https://www.bu.edu/pardee/files/documents/PP-004-GDP.pdf (accessed on 29 June 2016).

- L.-E. Borge, P. Parmer, and R. Torvik. “Local natural resource curse? ” J. Public Econ. 131 (2015): 101–114. [Google Scholar] [CrossRef]

- M. Humphreys, J. Sachs, and J. Stiglitz. Escaping the Resource Curse. New York, NY, USA: Columbia University Press, 2007. [Google Scholar]

- C.W. Cobb, and P.H. Douglas. “A Theory of Production.” Am. Econ. Rev. 18 (1928): 139–165. Available online: http://www2.econ.iastate.edu/classes/econ521/orazem/Papers/cobb-douglas.pdf (accessed on 1 July 2016). [Google Scholar]

- R.M. Solow. “Technical Change and the Aggregate Production Function.” Rev. Econ. Stat. 39 (1939): 312–320. Available online: http://faculty.georgetown.edu/mh5/class/econ489/Solow-Growth-Accounting.pdf (accessed on 1 July 2016). [Google Scholar] [CrossRef]

- R.W. Diamond, and B.J. Spencer. Trevor Swan and the Neoclassical Growth Model. NBER Working Paper series; Cambridge, MA, USA: National Bureau of Economic Research, 2008, Available online: http://www.nber.org/papers/w13950.pdf (accessed on 1 July 2016).

- N.G. Mankiw, D. Romer, and D.N. Weil. “A Contribution to the Empirics of Economic Growth.” Q. J. Econ. 107 (1992): 407–437. [Google Scholar] [CrossRef]

- R.J. Barro, and J.W. Lee. “A New Data Set of Educational Attainment in the World.” J. Dev. Econ. 104 (2013): 184–198. Available online: http://www.barrolee.com/ (accessed on 3 July 2016). [Google Scholar] [CrossRef]

- “The World Bank Database.” Available online: http://data.worldbank.org/ (accessed on 3 July 2016).

- D.A. Dickey, and W.A. Fuller. “Distribution of the Estimators for Autoregressive Time Series with a Unit Root.” J. Am. Stat. Assoc. 74 (1979): 427–431. [Google Scholar] [CrossRef]

- H. Akaike. “A new look at the statistical model identification.” IEEE Trans. Autom. Control 19 (1974): 716–723. [Google Scholar] [CrossRef]

- H.M. Peseran, and Y. Shin. “An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis.” In Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium. Edited by S. Strom. Cambridge, MA, USA: Cambridge University Press, 1999. [Google Scholar]

- C.A. Sims. “Macroeconomics and Reality.” Econometrica 48 (1980): 1–48. [Google Scholar] [CrossRef]

- T.S. Breusch. “Testing for Autocorrelation in Dynamic Linear Models.” Aust. Econ. Pap. 17 (1978): 334–355. [Google Scholar] [CrossRef]

- L.G. Godfrey. “Testing Against General Autoregressive and Moving Average Error Models when the Regressors Include Lagged Dependent Variables.” Econometrica 46 (1978): 1293–1301. [Google Scholar] [CrossRef]

- R.F. Engle. “Exact Maximum Likelihood Methods for Dynamic Regressions and Band Spectrum Regressions.” Int. Econ. Rev. 21 (1980): 391–407. [Google Scholar] [CrossRef]

- H. Lütkepohl. Introduction to Multiple Time Series Analysis. Berlin, Germany: Springer, 1991. [Google Scholar]

- “The World Travel & Tourism Council.” Available online: http://www.wttc.org/ (accessed on 3 July 2016).

- D. Artana, S. Auguste, R. Moya, S. Sookram, and P. Watson. Trinidad and Tobago: Economic Growth in a Dual Economy. Washington, DC, USA: Inter-American Development Bank, 2007, Available online: http://www.iadb.org/res/publications/pubfiles/pubCSI-116.pdf (accessed on 24 July 2016).

- Website of the Lesotho Government. “Lesotho Economy. Economic Overview. ” Available online: http://www.gov.ls/gov_webportal/economy/economy_menu.html (accessed on 24 July 2016).

- Liberia Ministry of Commerce and Industry. “Major Export Trading Partners. ” Available online: http://www.moci.gov.lr/2content.php?sub=74&related=18&third=74&pg=sp (accessed on 24 July 2016).

- M. Beevers. “Forest resources and peacebuilding: Preliminary lessons from Liberia and Sierra Leone.” In High-Value Natural Resources and Peacebuilding. Edited by P. Lujala and S.A. Rustad. London, UK: Earthscan, 2012. [Google Scholar]

- Index Mundi. “Iron Ore vs Crude Oil (Petroleum)―Price Rate of Change Comparison.” Available online: http://www.indexmundi.com/commodities/?commodity=iron-ore&months=360&commodity=crude-oil (accessed on 27 July 2016).

- J. Braveboy-Wagner. “Opportunities and Limitations of the Exercise of Foreign Policy Power by a Very Small State: The Case of Trinidad and Tobago.” Camb. Rev. Int. Aff. 23 (2010): 407–425. [Google Scholar] [CrossRef]

- “Guyana Bureau of Statistics. ” Available online: http://www.statisticsguyana.gov.gy/trade.html (accessed on 27 July 2016).

- D.G. Baur, and T.K. McDermott. “Is Gold a Safe Haven? International evidence.” J. Bank. Finan. 34 (2010): 1886–1898. [Google Scholar] [CrossRef]

- “Jamaica State of the Environment Government Report, 1996–1996. ” Available online: http://www.nepa.gov.jm/publications/SoE/SOE/soe.htm (accessed on 27 July 2016).

- African Development Bank Group. “Gambia Economic Outlook.” Available online: http://www.afdb.org/en/countries/west-africa/gambia/gambia-economic-outlook/ (accessed on 27 July 2016).

- J. Mitchell, and J. Faal. “Holiday Package Tourism and the Poor in the Gambia.” Dev. South. Afr. 24 (2007): 445–464. [Google Scholar] [CrossRef]

- F. Carneiro. “Belize: Right Choices, Bright Future.” World Bank group, 2016. Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/24046/Belize00right00c0country0diagnostic.pdf?sequence=1&isAllowed=y (accessed on 27 July 2016).

- W. More, M. Korkeakoski, J. Luukkanen, L. Alleyne, A. Abdulkadri, N. Brown, T. Chambers, O. Costa, A. Evans, S. McKenzie, and et al. “Identifying Inconsistencies in Long-Run Development Plans: The Case of Barbados' Vision for Energy Development.” Central Bank of Barbados WP/15/13. 2015. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2772617 (accessed on 28 July 2016).

- P.K. Narayan. “Economic Impact of Tourism on Fiji's Economy: Empirical Evidence from the Computable General Equilibrium Model.” Tour. Econ. 10 (2004): 419–433. [Google Scholar] [CrossRef]

- O. Neagu. “The Market Value of Human Capital: An Empirical Analysis.” Ann. Univ. Oradea Econ. Sci. Ser. 21 (2012): 256–264. [Google Scholar]

- A.G. Akpolat. “The Long-Term Impact of Human Capital Investment on GDP: A Panel Cointegrated Regression Analysis.” Econ. Res. Int., 2014. Available online: http://www.hindawi.com/journals/ecri/2014/646518/cta/ (accessed on 29 July 2016). [Google Scholar] [CrossRef]

- S.A. Castello, and T. Ozawa. Globalization of Small Economies as a Strategic Behavior in International Business, 1st ed. Abingdon, UK: Routledge, 1999. [Google Scholar]

- S.J. Camilleri, and J. Falzon. “The Challenges of Productivity Growth in the Small Island States of Europe: A Critical Look at Malta and Cyprus.” Isl. Stud. J. 8 (2013): 131–164. Available online: https://mpra.ub.uni-muenchen.de/62489/ (accessed on 30 July 2016). [Google Scholar]

- World Bank. “Expanding the Measure of Wealth: Indicators of Environmentally Sustainable Development.” 1994. Available online: http://documents.worldbank.org/curated/en/555261468765258502/Expanding-the-measure-of-wealth-indicators-of-environmentally-sustainable-development (accessed on 28 July 2016).

- H. Mehlum, K. Moene, and R. Torvik. “Institutions and the Resource Curse.” Econ. J. 116 (2006): 1–20. [Google Scholar] [CrossRef]

- D.W. Pearce, and G. Atkinson. “Capital theory and the measure of sustainable development: An indicator of weak sustainability.” Ecol. Econ. 3 (1993): 103–108. [Google Scholar] [CrossRef]

- K. Hamilton. “Green adjustments to GDP.” Res. Policy 20 (1994): 155–168. [Google Scholar] [CrossRef]

- K. Hamilton. “Pollution and pollution abatement in the national accounts.” Rev. Income Wealth 42 (1996): 13–33. [Google Scholar] [CrossRef]

- J. Farley. “Natural Capital.” In Berkshire Encyclopedia of Sustainability: Ecosystem Management and Sustainability. Edited by R.C. Craig, J.C. Nagle, B. Pardy, O. Schmitz and W. Smith. Gt Barrington, MA, USA: Berkshire Publishing, 2012, pp. 264–267. [Google Scholar]

- R. Naidoo. “Economic Growth and Liquidation of Natural Capital: The Case of Forest Clearance.” Land Econ. 80 (2004): 194–208. [Google Scholar] [CrossRef]

- V.A. Voora, and H.D. Venema. The Natural Capital Approach: A Concept Paper. Winnipeg, Canada: International Institute for Sustainable Development, 2008, Available online: https://www.iisd.org/pdf/2008/natural_capital_approach.pdf (accessed on 29 July 2016).

- S.J.C. Moreira, P.C. Vieira, and A.A.C. Teixeira. Estimating the Human Capital Stock for Cape Verde, 1950–2012. FEP Working Papers 547; Porto, Portugal: Faculty of Economics and Management, 2014. [Google Scholar]

- V.H. Nam, T. Sonobe, and K. Otsuka. “An Inquiry into the Development Process of Village Industries: The Case of a Knitwear Cluster in Northern Vietnam.” J. Dev. Stud. 46 (2010): 312–330. [Google Scholar] [CrossRef]

- A. Quisumbing, and S. McNiven. “Moving Forward, Looking Back: the Impact of Migration and Remittances on Assets, Consumption, and Credit Constraints in the Rural Philippines.” J. Dev. Stud. 46 (2010): 91–113. [Google Scholar] [CrossRef]

- M.D. Moore, and J. Daday. “Barriers to human capital development: Case studies in Swaziland, Cameroon and Kenya.” Afr. Educ. Rev. 7 (2010): 283–304. [Google Scholar] [CrossRef]

| Variable | Abbreviation used | Source | Function |

|---|---|---|---|

| Gross Domestic Product | GDP | World Bank (2016) | Dependent variable |

| Tourism as percentage of GDP | Tourism | World Bank (2016), World Tourism Council (2016) | Independent variable |

| Total Natural Resource Rent | NC | World Bank (2016) | |

| Human capital stock | HC | Barro-Lee database (2013) | |

| Gross Domestic Product per capita | GDPpc | World Bank (2016) |

| Country | GDP (in constant $2010) | Tourism (as percentage of GDP) | GVA (as percentage of GNI) | HC (stock of human capital) | GDPpc (in constant $2010) |

|---|---|---|---|---|---|

| The Gambia | 536,971,279.76 | 6.56 | −0.26 | 1,249.89 | 518.45 |

| Trinidad and Tobago | 12,012,729,470.09 | 3.34 | −6.29 | 2,463.22 | 9,847.27 |

| Lesotho | 1,206,862,818.90 | 4.86 | 18.26 | 1,719.04 | 701.54 |

| Belize | 711,605,918.56 | 11.03 | 9.98 | 2,150.78 | 3,027.54 |

| Guyana | 1,647,108,974.58 | 3.63 | 5.1 | 2,150.98 | 2,209.12 |

| Jamaica | 10,996,282,998.37 | 8.35 | 10.43 | 2,262.16 | 4,582.56 |

| Fiji | 2,293,187,461.92 | 12.59 | 1.57 | 2,430.64 | 3,075.16 |

| Liberia | 1,640,762,520.67 | 1.382 | −26.79 | 1,362.07 | 780.92 |

| Malawi | 3,781,976,645.782 | 2.825 | 7.96 | 1,410.4 | 384.81 |

| Barbados | 3,809,503,148.58 | 11.64 | 11.21 | 2,415.8 | 14,216.92 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kurecic, P.; Kokotovic, F. Examining the "Natural Resource Curse" and the Impact of Various Forms of Capital in Small Tourism and Natural Resource-Dependent Economies. Economies 2017, 5, 6. https://doi.org/10.3390/economies5010006

Kurecic P, Kokotovic F. Examining the "Natural Resource Curse" and the Impact of Various Forms of Capital in Small Tourism and Natural Resource-Dependent Economies. Economies. 2017; 5(1):6. https://doi.org/10.3390/economies5010006

Chicago/Turabian StyleKurecic, Petar, and Filip Kokotovic. 2017. "Examining the "Natural Resource Curse" and the Impact of Various Forms of Capital in Small Tourism and Natural Resource-Dependent Economies" Economies 5, no. 1: 6. https://doi.org/10.3390/economies5010006

APA StyleKurecic, P., & Kokotovic, F. (2017). Examining the "Natural Resource Curse" and the Impact of Various Forms of Capital in Small Tourism and Natural Resource-Dependent Economies. Economies, 5(1), 6. https://doi.org/10.3390/economies5010006