Determinants of Household Debt: A Systematic Review of the Literature

Abstract

1. Introduction

2. Methodology

2.1. Search Strategy

2.1.1. Identification

2.1.2. Screening

2.1.3. Eligibility

3. Results

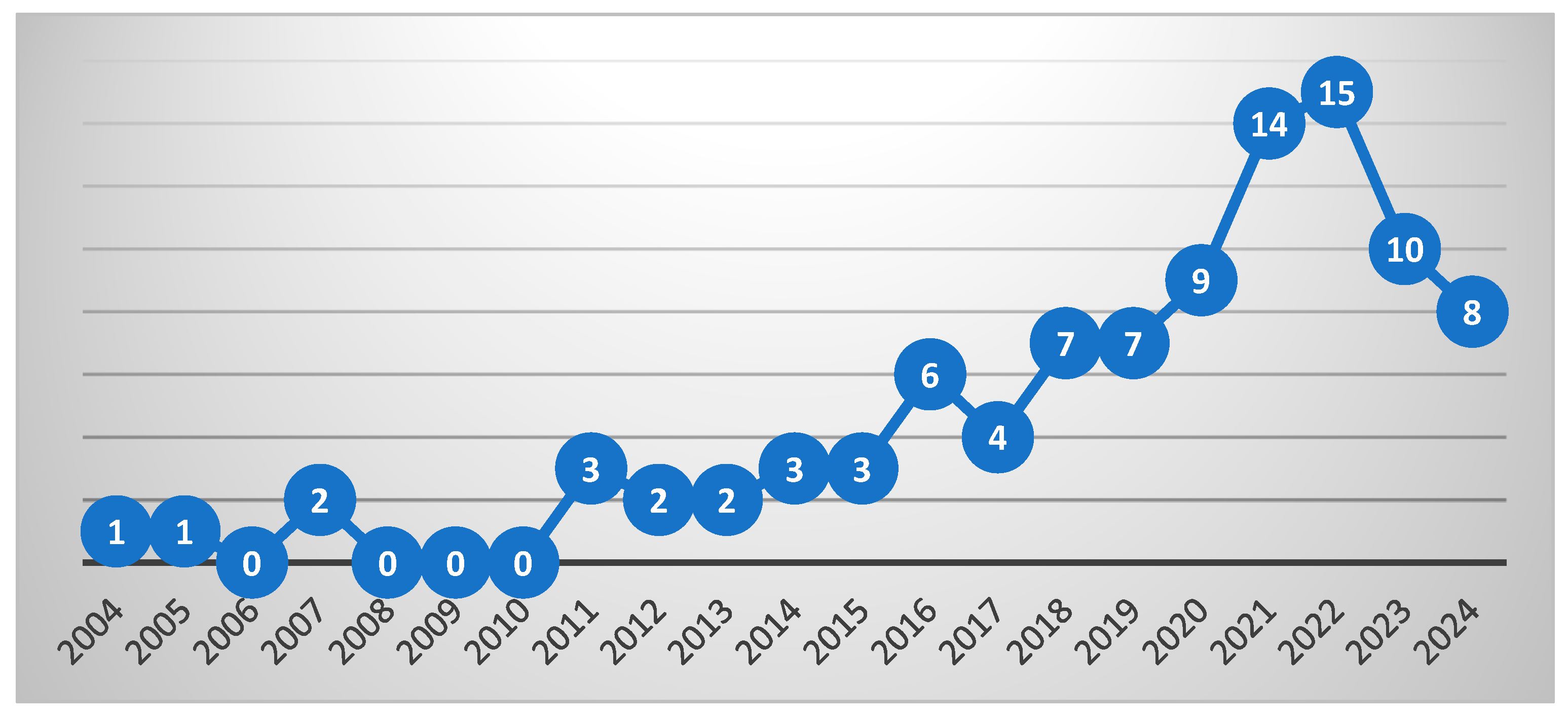

3.1. Descriptive Analysis of Publications

3.2. Country-Level Studies

3.2.1. Geographical Distribution of Country-Level Studies

3.2.2. Measures of Indebtedness

3.2.3. Time Period Covered

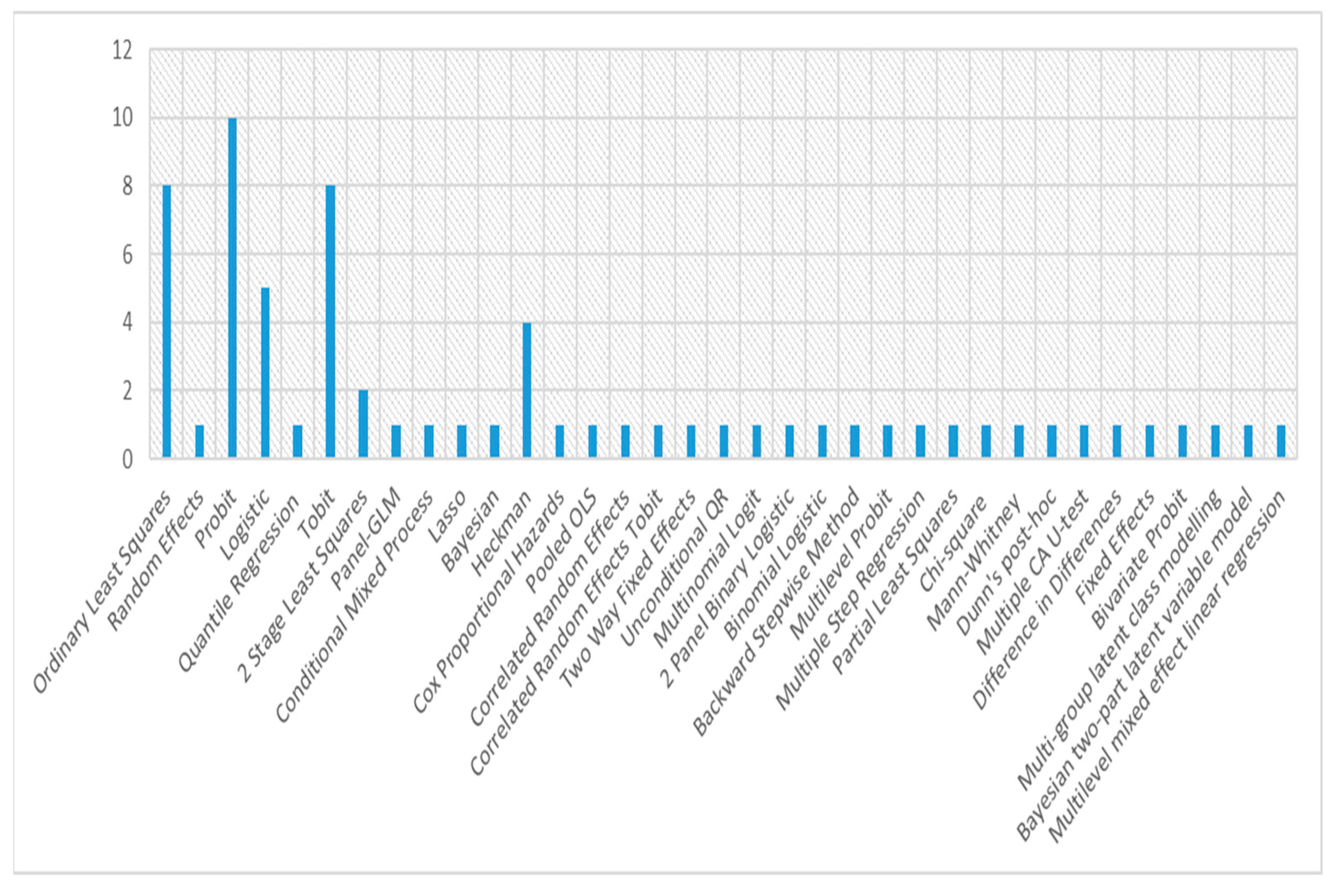

3.2.4. Econometric Approaches

3.2.5. Theories Used

3.2.6. Determinants of Household Indebtedness

3.3. Household-Level Studies

3.3.1. Geographical Distribution

3.3.2. Measures of Indebtedness

3.3.3. Time Period Covered

3.3.4. Methodological Approaches

3.3.5. Theories Used

3.3.6. Determinants of Indebtedness

4. Conclusions

5. Practical Implications

6. Limitations and Areas for Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Authors | Countries | Method | Period | UN | IN | GD | HP | IR | OG | IS | CS | SR | EA | SW | HS | HC | I | PG | II | DI | W | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Annarelli (2022) | 15 OECD | OLS | 1995–2010 | * | + | * | * | ||||||||||||||

| 2 | Pan (2023) | 30 | OLS, GMM | 1960–2018 | * | * | * | + | ||||||||||||||

| 3 | Turinetti and Zhuang (2011) | US | FDLM | 1980–2010 | - | + | - | + | - | - | + | - | ||||||||||

| 4 | Meniago et al. (2013) | South Africa | VECM | 1985–2012 | + | + | + | - | ||||||||||||||

| 5 | Bolibok (2015) | Poland | LR and PCA | 1997–2013 | - | - | - | + | ||||||||||||||

| 6 | Mamatzakis et al. (2023) | OECD | ANN VAR | 2020–2021 | ||||||||||||||||||

| 7 | Manole et al. (2016) | Romania | LSM | 2008–2015 | - | - | ||||||||||||||||

| 8 | Khan et al. (2016) | Malaysia | ARDL | 1999–2014 | + | + | - | + | + | |||||||||||||

| 9 | Vijverberg (2024) | USA | SEPM | 1999–2015 | - | |||||||||||||||||

| 10 | Nomatye and Phiri (2017) | South Africa | OLS and QR | 2002–2016 | * | + | - | - | * | + | ||||||||||||

| 11 | Moore and Stockhammer (2018) | 13 OECD | ECM | 1993–2011 | + | * | * | * | ||||||||||||||

| 12 | Bolibok (2018) | 31 OECD | FEPR | 1996–2015 | * | - | - | + | - | + | ||||||||||||

| 13 | Zain et al. (2019) | Malaysia | OLS | 2010–2017 | - | * | + | + | ||||||||||||||

| 14 | Fasianos et al. (2017) | USA | NARDL | 1913–2008 | + | |||||||||||||||||

| 15 | Berisha and Meszaros (2018) | USA | JEG | 1929–2009 | + | + | ||||||||||||||||

| 16 | Barradas and Tomas (2023) | 28 EU | FE2SLS | 1995–2016 | + | + | - | - | ||||||||||||||

| 17 | Czech and Puszer (2021) | V4 | PSP | 2019–2021 | ||||||||||||||||||

| 18 | Enache (2022) | Romania | SVAM | 2011–2021 | - | + | ||||||||||||||||

| 19 | Johnston et al. (2021) | 17 OECD | DLPA | 1995–2007 | ||||||||||||||||||

| 20 | Zimunya and Raboloko (2015) | Botswana | VECM | 1994–2012 | - | + | + | |||||||||||||||

| 21 | Park and Lee (2018) | 28 OECD | OLS, SUR | 1995–2015 | + | - | + | * | * | * | ||||||||||||

| 22 | Lim (2019) | 42 | PHP VAR | 1970–2015 | - | |||||||||||||||||

| 23 | Abd Samad et al. (2020) | 19 EM | BCLSDV, GMM | 1995–2018 | - | - | + | + | * | * | * | |||||||||||

| 24 | Maneejuk et al. (2021) | Thailand | PQRM | 2009–2017 | + | - | ||||||||||||||||

| 25 | Romao and Barradas (2022) | Portugal | NARDL | 1988–2016 | * | * | + | + | + | |||||||||||||

| 26 | Dumitrescu et al. (2022) | 26 OECD | QR, GMM | 2002–2020 | - | - | - | + | + | |||||||||||||

| 27 | Zhou and Niyitegeka (2023) | South Africa | VECM | 1980–2021 | - | + | + | - | ||||||||||||||

| 28 | Christen and Morgan (2005) | US | SUR and OLS | 1980–2003 | - | - | * | + | ||||||||||||||

| 29 | Kakuru and Kaulihowa (2022) | Namibia | ARDL | 2004–2020 | ||||||||||||||||||

| 30 | Kraft (2007) | 90 | OLS | 2003–2005 | - | + | ||||||||||||||||

| 31 | Coletta et al. (2018) | 33 OECD | FE and IV | 1995–2016 | + | + | + | - | ||||||||||||||

| 32 | Lepers (2024) | 51 | FE | 1990–2017 | * | + | * | |||||||||||||||

| 33 | T. Long et al. (2024) | 52 | FE | 1990–2019 | + | |||||||||||||||||

| 34 | Yahya et al. (2023) | Malaysia | SEM | 1991–2021 | + | * | + | * | * | |||||||||||||

| 35 | Bazillier et al. (2021) | 30 | IV | 1970–2017 | + | + | - | - | + |

| Authors | Country | Method | Period | ED | FS | HP | HO | AG | G f | E | I | W | OA | NC | M m | RT | S | FA | NM | SE | IR | HC | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Lewin-Epstein and Semyonov (2016) | 14 EU and Israel | Tobit | 2013 | * | + | * | - | + | ||||||||||||||

| 2 | Olivero and Dvalishvili (2021) | USA | OLS | 2008 | + | + | |||||||||||||||||

| 3 | Abid et al. (2012) | Tunisia | Probit | 2010 | |||||||||||||||||||

| 4 | Barrot et al. (2022) | USA | OLS | 1999–2007 | - | + | - | ||||||||||||||||

| 5 | Singh et al. (2014) | India | MSR | 2013 | + | ||||||||||||||||||

| 6 | Walks (2013) | Canada | OLS | 2001–2009 | + | - | - | + | |||||||||||||||

| 7 | Altundere (2014) | 13 EU | Probit and Tobit | 2007–2007 | - | + | + | + | - | + | |||||||||||||

| 8 | Haq et al. (2018) | Pakistan | MMELR | 2001–2014 | + | + | - | + | + | * | - | ||||||||||||

| 9 | Pandey (2016) | India | Tobit | 2011–2012 | - | + | + | ||||||||||||||||

| 10 | Handayani et al. (2016) | Indonesia | OLS | + | + | + | + | + | + | ||||||||||||||

| 11 | Rahman et al. (2020) | Malaysia | PLS | 2016, 2017 | + | * | |||||||||||||||||

| 12 | Strzelecka and Zawadzka (2020) | Poland | C, MWMCA, U, DPH | 2004–2018 | + | + | - | + | + | + | |||||||||||||

| 13 | Hake and Poyntner (2022) | 10 EU | Multilevel probit | 2008–2018 | + | + | + | - | + | ||||||||||||||

| 14 | Piovarci (2021) | Slovakia | Logistic | 2017 | - | * | + | - | + | + | |||||||||||||

| 15 | Comelli (2021) | 30 OECD | Probit | 1995–2017 | + | - | + | - | + | ||||||||||||||

| 16 | Yaparatne and Senathissa (2021) | Sri Lanka | OLS | 2018 | + | + | - | ||||||||||||||||

| 17 | G. M. Long (2018) | US | OLS | 1995–2013 | |||||||||||||||||||

| 18 | Padmaja and Ali (2019) | India | HTSSM | 2013 | + | + | - | ||||||||||||||||

| 19 | Intarapak and Supapakorn (2020) | Thailand | Logistic, BSM | 2017 | + | + | |||||||||||||||||

| 20 | Atalay et al. (2020) | Australia | HTSSM | 2002–2014 | + | ||||||||||||||||||

| 21 | Thorat et al. (2020) | IndIa | BLR | 2012–2013 | * | + | * | * | |||||||||||||||

| 22 | Cao-Alvira et al. (2020) | Colombia | Logistic | 2011–2015 | + | - | + | + | |||||||||||||||

| 23 | Tahir and Ahmed (2021) | Australia | RE, TPBLR | 2002–2018 | + | - | * | + | * | * | |||||||||||||

| 24 | Heintz-Martin et al. (2021) | Germany | Logistic | 2019 | |||||||||||||||||||

| 25 | Wang et al. (2022) | China | TWFE | 2013–2017 | * | * | * | * | - | * | * | ||||||||||||

| 26 | Lagomarsino and Spiganti (2021) | Italy | POLS, RE, CRE, CRET | 1989–2016 | - | + | + | - | |||||||||||||||

| 27 | Mishra and Bhardwaj (2021) | India | QR | 2002 | - | + | - | - | - | + | - | ||||||||||||

| 28 | Kandikuppa and Gray (2022) | India | Logistic | 2004–2012 | |||||||||||||||||||

| 29 | Tseng and Hsiao (2022) | China | QR | 2015 | -/+ | - | + | + | |||||||||||||||

| 30 | Manogna and Mishra (2022) | India | Tobit, HTSSM | 2012–2013 | + | + | + | - | + | ||||||||||||||

| 31 | Wildemauwe and Sanroman (2022) | Uruguay | Probit | 2014, 2017 | - | + | + | - | - | ||||||||||||||

| 32 | Tian (2022) | China | Tobit, 2SLS | 2019 | + | - | - | ||||||||||||||||

| 33 | Branten (2022) | Estonia | Probit, HTSSM | 2013, 2017 | - | + | + | + | |||||||||||||||

| 34 | Dharmadasa and Gunatilake (2023) | Sri Lanka | MLR | 2021 | + | + | * | * | * | * | * | * | |||||||||||

| 35 | Wong et al. (2023) | Malaysia | 2SLS | 2019 | - | + | |||||||||||||||||

| 36 | Jestl (2023) | 15 Euro | Probit | 2010 | * | - | - | + | * | - | - | - | |||||||||||

| 37 | Malan et al. (2020) | South Africa | CPHRM | 1999–2013 | + | - | * | + | + | * | |||||||||||||

| 38 | Pastrapa and Apostolopoulos (2015) | Greece | HTSSM, Probit, OLS | 2009 | + | + | + | - | + | - | - | ||||||||||||

| 39 | Camoes and Vale (2018) | Portugal | Tobit | 2010 | + | - | + | + | + | ||||||||||||||

| 40 | Ottaviani and Vandone (2011) | Italy | Probit | 2008–2009 | * | * | * | * | + | + | + | ||||||||||||

| 41 | Datta et al. (2017) | India | Bayesian, OLS, LR | 2015–2016 | - | ||||||||||||||||||

| 42 | Lee and Mori (2021) | Singapore | Panel-GLM | 2010–2012 | - | + | - | + | - | ||||||||||||||

| 43 | Fuentealba et al. (2021) | Chile | Tobit, probit, CMP | 2014 and 2017 | + | + | + | + | - | - | |||||||||||||

| 44 | Fernandez-Lopez et al. (2024) | Spain | Probit | 2016–2017 | + | + | * | - | + | - | + | * | |||||||||||

| 45 | Li et al. (2023) | China | FE | 2011–2017 | * | + | +_ | + | * | + | + | + | |||||||||||

| 46 | Fabbri and Padula (2004). | Italy | Probit | 1989–1988 | * | + | * | + | * | * | |||||||||||||

| 47 | Zanin (2017) | Italy | Bivariate Probit | 1995–2014 | |||||||||||||||||||

| 48 | Brown et al. (2019) | USA | Probit, Tobit | 1984–2005 | + | + | - | + | + | + | + | - | |||||||||||

| 49 | Bialowoski (2019) | Poland | MLCM | 2008–2018 | |||||||||||||||||||

| 50 | Feng et al. (2019) | China | BTPLVM | 2015 | + | + | + | + | - | + | + | ||||||||||||

| 51 | Abreu et al. (2024) | Portugal | DiD | 2017–2019 | |||||||||||||||||||

| 52 | Mian and Sufi (2011) | USA | IV | 2002–2006 | + | - | + | ||||||||||||||||

| 53 | Nagano and Yeom (2014) | Japan | OLS | 2001–2010 | + | - | * | - | |||||||||||||||

| 54 | Okurut and Schoombee (2007) | Uganda | HTSSM | 1999–2000 | + | * | |||||||||||||||||

| 55 | Yao et al. (2024) | China | OLS/2SLS | ||||||||||||||||||||

| 56 | Kim et al. (2016) | China | Probit | 2010, 2013 | + | - | + | - | + | - | |||||||||||||

| 57 | Li et al. (2024) | China | CMPM | 2017 | * | - | - | + | + | ||||||||||||||

| 58 | Shang and Saffar (2023) | USA | OLS | 1984–1999 | + | + | - | - | + | + | + | + | |||||||||||

| 59 | Bailey et al. (2016) | USA | FE | 2008, 2014 | |||||||||||||||||||

| 60 | Jung and Kim (2020) | Korea | 2012–2017 | ||||||||||||||||||||

| 61 | Smith et al. (2012) | USA | MLR | 1995–2007 | + | + | * | + | |||||||||||||||

| 62 | Liang and Gao (2021) | China | OLS, 2SLS | 2013 | + | - | - | + |

References

- Abd Samad, K., Idris, N. H., Abd Rahman, N. H., Sani, A., & Mohd Soffian Lee, U. H. (2023). Systematic literature review on the macroeconomic factors of household debt. In European proceedings of finance and economics. European Publisher. [Google Scholar] [CrossRef]

- Abd Samad, K., Mohd Daud, S. N., & Mohd Dali, N. R. S. (2020). Determinants of household debt in emerging economies: A macro panel analysis. Cogent Business and Management, 7(1), 1831765. [Google Scholar] [CrossRef]

- Abid, L., Zouari, D., & Zouari-Ghorbel, S. (2012). Household indebtedness in Tunisia. Journal of Business Management and Economics, 3(10), 341–350. [Google Scholar]

- Abreu, D., Felix, S., Oliveira, V., & Silva, F. (2024). The impact of a macro prudential borrower-based measure on households’ leverage and housing choices. Journal of Housing Economics, 64, 101995. [Google Scholar] [CrossRef]

- Achtziger, A., Hubert, M., Kenning, P., Raab, G., & Reisch, L. (2015). Debt out of control: The links between self-control, compulsive buying, and real debts. Journal of Economic Psychology, 49, 141–149. [Google Scholar] [CrossRef]

- Altundere, B. M. (2014). The relationship between sociability and household debt. ADAM AKADEMİ, Cilt 4(2), 27–58. [Google Scholar] [CrossRef]

- Annarelli, M. K. (2022). Welfare generosity, credit access and household debt: Clarifying relationships through a new welfare-debt typology. New Political Economy, 27(4), 680–696. [Google Scholar] [CrossRef]

- Atalay, K., Barrett, F. G., Edwards, R., & Yu, C. (2020). House price shocks, credit constraints and household indebtedness. Oxford Economic Papers, 72(3), 780–803. [Google Scholar] [CrossRef]

- Bailey, M., Davila, E., Kuchler, T., & Stroebel, J. (2016). House price beliefs and mortgage leverage choice. Review of Economic Studies 86, 2403–2452. [Google Scholar] [CrossRef]

- Baltagi, B. H. (2005). Econometric analysis of panel data (3rd ed.). Cambridge University Press. [Google Scholar]

- Barradas, R., & Tomas, I. (2023). Household indebtedness in the European Union countries: Going beyond the mainstream interpretation. PSL Quarterly Review, 76(304), 21–49. [Google Scholar] [CrossRef]

- Barrot, J., Loualiche, E., Plosser, M., & Sauvagnat, J. (2022). Import competition and household debt. The Journal of Finance, LXXVII(6), 3037–3091. [Google Scholar] [CrossRef]

- Bazillier, R., Hericourt, J., & Ligonneire, S. (2021). Structure of income inequality and household leverage: Cross country causal evidence. European Economic Review, 132, 103629. [Google Scholar] [CrossRef]

- Berisha, E., & Meszaros, J. (2018). Household debt, consumption, and income inequality. International Economic Journal, 32(2), 161–176. [Google Scholar] [CrossRef]

- Bialowoski, P. (2019). Economic sentiment as a driver for household financial behaviour. Journal of Behavioral and Experimental Economics, 80, 59–66. [Google Scholar] [CrossRef]

- Biyanwila, K. U. P. B., & Anuradha, S. N. A. P. (2023). Behavioral factors affecting household over-indebtedness: A systematic review. Vidyodaya Journal of Management, 9(I), 84–107. [Google Scholar] [CrossRef]

- Bolibok, P. (2015). An empirical evaluation of the demand-side drivers of household residential debt: The case of Poland. Finanse, Rynki Finansowe, Ubezpieczenia nr, 74, 597–608. [Google Scholar]

- Bolibok, P. (2018). The macroeconomic drivers of household debt-to-income ratio: An evidence from the OECD countries. Copernican Journal of Finance & Accounting, 7(2), 29–41. [Google Scholar] [CrossRef]

- Branten, E. (2022). The role of risk attitudes and expectations in household borrowing: Evidence from Estonia. Baltic Journal of Economics, 22(2), 126–145. [Google Scholar] [CrossRef]

- British Medical Journal [BMJ]. (2021). PRISMA 2020 explanation and elaboration: Updated guidance and exemplars for reporting systematic reviews. BMJ, 372, n160. [Google Scholar] [CrossRef]

- Brown, S., Gray, D., & Montagnoli, A. (2019). Credit supply shocks and household leverage: Evidence from the US banking deregulation. Journal of Financial Stability, 42, 97–115. [Google Scholar] [CrossRef]

- Brown, S., & Taylor, K. (2008). Household debt and financial assets: Evidence from Germany, Great Britain and the USA. Journal of the Royal Statistical Society, 171, 615–643. [Google Scholar] [CrossRef]

- Camoes, F., & Vale, S. (2018). I feel wealthy: A major determinant of Portuguese households’ indebtedness? Empirical Economics, 58, 1953–1978. [Google Scholar] [CrossRef]

- Cao-Alvira, J. J., Novoa-Hoyos, A., & Nunez-Torres, A. (2020). On the financial literacy, indebtedness, and wealth of Colombian households. Review of Development Economics, 25, 978–993. [Google Scholar] [CrossRef]

- Charpentier, A., Flachaire, E., & Antoine, L. (2018). Econometrics and machine learning. Economics and Statistics, 505, 147–169. [Google Scholar] [CrossRef]

- Charron-Chenier, R., & Seamster, L. (2021). Racialized debts: Racial exclusion from credit tools and information networks. Critical Sociology, 47(6), 977–992. [Google Scholar] [CrossRef]

- Chichaibelu, B. B., & Waibel, H. (2018). Over-indebtedness and its persistence in rural households in Thailand and Vietnam. Journal of Asian Economics, 56, 1–23. [Google Scholar] [CrossRef]

- Christen, M., & Morgan, M. R. (2005). Keeping up with the Joneses: Analyzing the effect of income inequality on consumer borrowing. Quantitative Marketing and Economics, 3, 145–173. [Google Scholar] [CrossRef]

- Chu, J. (2019). Accruals, investment, and future performance. A Journal of Accounting, Finance and Business Studies, 55(4), 783–809. [Google Scholar] [CrossRef]

- Coletta, M., De Bonis, R., & Piermattei, S. (2018). Household debt in OECD countries: The role of supply-side and demand-side factors. Social Indicators Research, 143, 1185–1217. [Google Scholar] [CrossRef]

- Comelli, M. (2021). The impact of welfare on household debt. Sociological Spectrum, 41(2), 154–176. [Google Scholar] [CrossRef]

- Cooper, C. R., Mullins, M., & Weinstock, L. R. (2021). COVID-19: Household debt during the pandemic. Congressional research service report. Available online: https://crsreports.congress.gov (accessed on 9 September 2024).

- Currit, N. (2002). Inductive regression: Overcoming OLS limitations with the general regression neural network. Computers, Environment and Urban Systems, 26(4), 335–353. [Google Scholar] [CrossRef]

- Czech, M., & Puszer, B. (2021). Impact of the COVID-19 pandemic on the consumer credit market in V4 countries. Risks, 9, 229. [Google Scholar] [CrossRef]

- D’Alessio, G., & Iezzi, S. (2013). Household over-indebtedness: Definition and measurement with Italian data. Bank of Italy Occasional Paper No. 149. Bank of Italy. [Google Scholar] [CrossRef]

- Datta, S., Tiwari, K. A., & Shylajan, C. S. (2017). An empirical analysis of nature, magnitude and determinants of farmers’ indebtedness in India. International Journal of Social Economics, 45(6), 888–908. [Google Scholar] [CrossRef]

- Dharmadasa, C., & Gunatilake, M. M. (2023). Determinants of household credit behavior of low-income households in Sri Lanka. Asian Economic and Financial Review, 13(10), 715–726. [Google Scholar] [CrossRef]

- Dumitrescu, B. A., Enciu, A., Hândoreanu, C. A., Obreja, C., & Blaga, F. (2022). Macroeconomic determinants of household debt in OECD Countries. Sustainability, 14, 3977. [Google Scholar] [CrossRef]

- Enache, C. (2022). Macroeconomic determinants of household indebtedness in Romania: An econometric approach. Journal of Social and Economic Statistics, 11(1–2), 102–117. [Google Scholar] [CrossRef]

- Estoque, R. C., Togawa, T., Ooba, M., Gomi, K., Nakamura, S., Hijioka, Y., & Kameyama, Y. (2019). A review of quality of life (QOL) assessments and indicators: Towards a “QOL-Climate” assessment framework. Ambio, 48(6), 619–638. [Google Scholar] [CrossRef]

- European Commission. (2008, February). Towards a common operational European definition of over-indebtedness. Available online: www.bristol.ac.uk/media-library/sites/geography/migrated/documents/pfrc0804.pdf (accessed on 3 July 2024).

- Fabbri, D., & Padula, M. (2004). Does poor legal enforcement make households credit-constrained? Journal of Banking & Finance, 28, 2369–2397. [Google Scholar]

- Fasianos, A., Raza, H., & Kinsella, S. (2017). Exploring the link between household debt and income inequality: An asymmetric approach. Applied Economics Letters, 24(6), 404–409. [Google Scholar] [CrossRef]

- Feng, X., Lu, B., Song, X., & Ma, S. (2019). Financial literacy and household finances: A Bayesian two-part latent variable modelling approach. Journal of Empirical Finance, 51, 119–137. [Google Scholar] [CrossRef]

- Fernandez-Lopez, S., Castro-González, S., Rey-Ares, L., & Rodeiro-Pazos, D. (2024). Self-control and debt decisions relationship: Evidence for different credit options. Current Psychology, 43, 340–357. [Google Scholar] [CrossRef]

- Friedman, M. (1957). A theory of the consumption function. Princeton University Press. [Google Scholar]

- Fuentealba, D. L. C., Mendoza, A. M. J., Yelpo, S. M. S., Ramos, V. L. C., & Fuentes-Solis, A. R. (2021). Household debt, automatic bill payments and inattention: Theory and evidence. Journal of Economic Psychology, 85, 102385. [Google Scholar] [CrossRef]

- Hake, M., & Poyntner, P. (2022). Keeping up with the Novaks? Income distribution as a determinant of household debt in CESEE. Review of Income and Wealth Series, 68(S1), S224–S260. [Google Scholar] [CrossRef]

- Handayani, D., Salamah, U., & Yusacc, N. R. (2016). Indebtedness and subjective financial wellbeing of households in Indonesia. Economics and Finance in Indonesia, 62(2), 78–87. [Google Scholar] [CrossRef]

- Haq, W., Ismail, A. N., & Satar, M. N. (2018). Household debt in different age cohorts: A multilevel study. Cogent Economics & Finance, 6(1), 1455406. [Google Scholar] [CrossRef]

- Harari, D. (2018). Household debt: Statistics and impact on economy (House of Commons Briefing Paper 7584). UK Parliament. Available online: https://commonslibrary.parliament.uk/research-briefings/cbp-7584/ (accessed on 3 September 2024).

- Heintz-Martin, V., Recksiedler, C., & Langmeyer, N. A. (2021). Household debt, maternal well-being, and child adjustment in Germany: Examining the family stress model by family structure. Journal of Family and Economic Issues, 43, 338–353. [Google Scholar] [CrossRef] [PubMed]

- Intarapak, S., & Supapakorn, T. (2020). Application of logistic regression analysis to household debt of Bangkok and metropolitan area of Thailand. WSEAS Transactions on Business and Economics, 17, 676–680. [Google Scholar] [CrossRef]

- Jestl, S. (2023). The impact of income inequality on household indebtedness in Euro area countries. European Journal of Economics and Economic Policies: Intervention, 20(2), 151–182. [Google Scholar] [CrossRef]

- Johnson, P. T. (2014). Snowball sampling: Introduction. In Wiley statsref: Statistics reference online. Wiley. [Google Scholar] [CrossRef]

- Johnston, A., Fuller, W. G., & Regan, A. (2021). It takes two to tango: Mortgage markets, labor markets and rising household debt in Europe. Review of International Political Economy, 28(4), 843–873. [Google Scholar] [CrossRef]

- Jung, D., & Kim, S. Y. (2020). Income volatility, household leverage, and consumption in Korea. Japan and World Economy, 53, 100994. [Google Scholar] [CrossRef]

- Kakuru, C., & Kaulihowa, T. (2022). Determinants of house price dynamics and household indebtedness in Namibia. Studies in Economics and Econometrics, 46(3), 185–200. [Google Scholar] [CrossRef]

- Kandikuppa, S., & Gray, C. (2022). Climate change and household debt in rural India. Climatic Change, 173(3), 20. [Google Scholar] [CrossRef]

- Karambakuwa, T. R., & Ncwadi, R. (2021). Determinants of household over-indebtedness in South Africa. International Journal of Business and Economic Development, 9(2), 11–24. [Google Scholar] [CrossRef]

- Khan, A. H. H., Abdullah, H., & Samsudin, S. (2016). Modelling the determinants of Malaysian household debt. International Journal of Economics and Financial Issues, 6(4), 1468–1473. [Google Scholar]

- Khatib, S. F. A., Abdullah, D. F., Al Amosh, H., Bazhair, A. H., & Kabara, A. S. (2022). Shariah auditing: Analyzing the past to prepare for the future. Journal of Islamic Accounting and Business Research, 13, 791–818. [Google Scholar] [CrossRef]

- Khatib, S. F. A., Al Amosh, H., & Ananzeh, H. (2023). Board compensation in financial sectors: A systematic review of twenty-four years of research. International Journal of Financial Studies, 11, 92. [Google Scholar] [CrossRef]

- Kim, K. T., Seay, M. C., & Smith, H. L. (2016). After the great recession: Financial sophistication and housing leverage. Applied Economics Letters, 23(18), 1285–1288. [Google Scholar] [CrossRef]

- Kraft, E. (2007). The boom in household lending in transition countries: A Croatian case study and a cross-country analysis of determinants. Comparative Economic Studies, 49, 345–366. [Google Scholar] [CrossRef]

- Lagomarsino, E., & Spiganti, A. (2021). Risk aversion and the size of desired debt. Italian Economic Journal, 9, 369–396. [Google Scholar] [CrossRef]

- Leandro, C. J., & Botelho, D. (2022). Consumer over-indebtedness: A review and future research agenda. Journal of Business Research, 145, 535–551. [Google Scholar] [CrossRef]

- Lee, O. K., & Mori, M. (2021). Conspicuous consumption and household indebtedness. Real Estate Economics, 49, 557–586. [Google Scholar] [CrossRef]

- Lepers, E. (2024). Fiscal policy as credit policy: Homeownership subsidization and the household debt boom. Economy and Society, 53(2), 322–349. [Google Scholar] [CrossRef]

- Lewin-Epstein, N., & Semyonov, M. (2016). Household debt in midlife and old age: A multinational study. International Journal of Comparative Sociology, 57(3), 151–172. [Google Scholar] [CrossRef]

- Li, G., Lv, X., & Han, X. (2023). Digital financial inclusion and household debt in China. Applied Economics Letters, 3019, 2862–2866. [Google Scholar] [CrossRef]

- Li, J., Vatsa, P., & Ma, W. (2024). Internet use and household debt: Insights from rural China. Applied Economics, 110, 1–21. [Google Scholar] [CrossRef]

- Liang, P., & Gao, N. (2021). Homevalue misestimation and household leverage: An empirical study of Chinese urban households. Cities, 109, 103043. [Google Scholar] [CrossRef]

- Lim, H. (2019). The response of household debt to income inequality shocks: A heterogeneous approach. Applied Economics Letters, 2698, 684–689. [Google Scholar] [CrossRef]

- Long, G. M. (2018). Pushed into the red? Female-headed households and the pre-crisis credit expansion. Forum for Social Economics, 47(2), 224–236. [Google Scholar] [CrossRef]

- Long, T., Bu, K., Du, P., & Wang, Z. (2024). Can educational investment mitigate the impact of aging on household leverage ratio? International Review of Economics and Finance, 89, 1335–1347. [Google Scholar] [CrossRef]

- Malan, S., De Clercq, B., & Meiring, J. (2020). Personal conversion factors influencing debt uptake amongst young households in South Africa. Journal of Economic and Financial Sciences, 13(1), 452. [Google Scholar] [CrossRef]

- Mamatzakis, C. M., Ongena, S., & Tsionas, G. M. (2023). The response of household debt to COVID-19 using a neural networks VAR in OECD. Empirical Economics, 65, 65–91. [Google Scholar] [CrossRef]

- Maneejuk, P., Teerachai, S., Ratchakit, A., & Yamaka, W. (2021). Analysis of difference in household debt across regions of Thailand. Sustainability, 13, 12253. [Google Scholar] [CrossRef]

- Manogna, R. L., & Mishra, K. A. (2022). Determinants of indebtedness and institutional credit to rural agricultural households: An empirical evidence from South India. International Journal of Social Economics, 49(9), 1387–1400. [Google Scholar]

- Manole, D. S., Petrescu, C., & Vlada, I. R. (2016). Determinants of household loans. Theoretical and Applied Economics, 4(609), 89–102. [Google Scholar]

- Meniago, C., Mukuddem-Petersen, J., Petersen, A. M., & Mongale, P. I. (2013). What causes household debt to increase in South Africa? Economic Modelling, 33, 482–492. [Google Scholar] [CrossRef]

- Mian, A., & Sufi, A. (2011). House prices, home equity–based borrowing, and the US household leverage crisis. American Economic Review, 101(5), 2132–2156. [Google Scholar] [CrossRef]

- Mishra, K. A., & Bhardwaj, V. (2021). The determinants of access to informal credits in India: An application of quantiles via moments method. Journal of Quantitative Economics, 20, 1–22. [Google Scholar] [CrossRef]

- Modigliani, F., & Brumberg, R. (1954). Utility analysis and the consumption function: An interpretation of cross-section data. In K. K. Kurihara (Ed.), Post-keynesian economics. Rutgers University Press. [Google Scholar]

- Mohammad, Z., Kamil, M. A. B., & Mazlan, B. R. A. (2021). Causes of household indebtedness: A systematic review. Journal of Tianjin University Science and Technology, 54(12), 53–78. [Google Scholar] [CrossRef]

- Moore, L. G., & Stockhammer, E. (2018). The drivers of household indebtedness reconsidered: An empirical evaluation of competing arguments on the macroeconomic determinants of household indebtedness in OECD countries. Journal of Post Keynesian Economics, 41(4), 547–577. [Google Scholar] [CrossRef]

- Nagano, M., & Yeom, D. (2014). Another determinant of household leverage: Evidence from Japan’s mortgage loan data. International Review of Finance, 14(1), 105–139. [Google Scholar] [CrossRef]

- Nomatye, A., & Phiri, A. (2017). Investigating the macroeconomic determinants of household debt in South Africa (Munich Personal RePEc Archive Paper No. 83303). University Library of Munich. Available online: https://ideas.repec.org/p/pra/mprapa/83303.html (accessed on 5 June 2024).

- Okurut, F. N., & Schoombee, A. (2007). Credit market access in Uganda: Evidence from household survey data 1999/2000. South African Journal of Economic and Management Sciences, 10(3), 371–383. [Google Scholar] [CrossRef]

- Olivero, M. P., & Dvalishvili, M. (2021). What do fiscal stimulus packages mean for household debt? Contemporary Economic Policy, 41(2), 282–299. [Google Scholar] [CrossRef]

- Ottaviani, C., & Vandone, D. (2011). Impulsivity and household indebtedness: Evidence from real life. Journal of Economic Psychology, 32, 754–761. [Google Scholar] [CrossRef]

- Paap, R., & Franses, H. P. (2000). A dynamic multinomial probit model for brand choice with different long-run and short-run effects of marketing-mix variables. Journal of Applied Econometrics, 15(6), 717–744. [Google Scholar] [CrossRef]

- Padmaja, S. S., & Ali, J. (2019). Correlates of agrarian indebtedness in rural India. Journal of Agribusiness in Developing and Emerging Economies, 9(2), 125–138. [Google Scholar] [CrossRef]

- Pan, W. (2023). Household debt in the times of populism. Journal of Economic Behavior and Organization, 205, 202–215. [Google Scholar] [CrossRef]

- Pandey, K. G. (2016). Extent, magnitude and determinants of indebtedness among farmers in eastern India: A survey-based study. Indian Journal of Agricultural Economics, 71(4), 450–462. [Google Scholar]

- Park, J., & Lee, Y. (2018). Corporate income taxes, corporate debt, and household debt. International Tax and Public Finance, 26, 506–535. [Google Scholar] [CrossRef]

- Pastrapa, E., & Apostolopoulos, C. (2015). Estimating determinants of borrowing: Evidence from Greece. Journal of Family Economic Issues, 36, 210–223. [Google Scholar] [CrossRef]

- Piovarci, V. (2021). The effect of socio-economic and demographic factors on household indebtedness: Evidence from Slovakia. Economic Review, 50(2), 181–201. [Google Scholar]

- Rahman, M., Azma, N., Masud, K. A. M., & Ismail, I. (2020). Determinants of indebtedness: Influence of behavioral and demographic factors. International Journal of Financial Studies, 8(8), 1–14. [Google Scholar] [CrossRef]

- Romao, A., & Barradas, R. (2022). Macroeconomic determinants of households’ indebtedness in Portugal: What really matters in the era of financialisation? International Journal of Finance & Economics, 29(1), 383–401. [Google Scholar] [CrossRef]

- Runstler, G., Balfoussia, H., Burlon, L., & Buss, G. (2018). Real and financial cycles in EU countries: Stylised facts and modelling implications (European Central Bank Occasional Paper Series No. 205). European Central Bank. Available online: https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op205.en.pdf (accessed on 22 April 2024).

- Shang, L., & Saffar, W. (2023). Employment protection and household mortgage debt. Journal of Banking & Finance, 149, 106817. [Google Scholar] [CrossRef]

- Sierminska, E. (2014). Indebtedness of households and the cost of debt by household type and income group. European Commission Research Note 10/2014. European Commission. [Google Scholar]

- Singh, S., Bhogal, S., & Singh, R. (2014). Magnitude and determinants of indebtedness among farmers in Punjab. Indian Journal of Agricultural Economics, 69(2), 243–256. [Google Scholar]

- Smith, H. L., Finke, S. M., & Huston, J. S. (2012). Financial sophistication and housing leverage among older households. Journal of Family Economic Issues, 33, 315–327. [Google Scholar] [CrossRef]

- Stockhammer, E. (2015). Rising inequality as a cause of the present crisis. Cambridge Journal of Economics, 39(3), 935–958. [Google Scholar] [CrossRef]

- Strzelecka, A., & Zawadzka, D. (2020). Why households borrow money? Socio-economic factors affecting households’ debts: A model approach. European Research Studies Journal, 23(2), 820–839. [Google Scholar] [CrossRef]

- Tahir, M. S., & Ahmed, D. A. (2021). Australians’ financial wellbeing and household debt: A panel analysis. Journal of Risk and Financial Management, 14, 513. [Google Scholar] [CrossRef]

- Thorat, S. V., Garde, Y., & Arhant, A. (2020). Incidence and determinants of indebtedness of agricultural households in Gujarat. Economic Affairs, 65(2), 249–254. [Google Scholar] [CrossRef]

- Tian, G. (2022). Influence of digital finance on household leverage ratio from the perspective of consumption effect and income effect. Sustainability, 14, 16271. [Google Scholar] [CrossRef]

- Tseng, Y., & Hsiao, I. (2022). Decomposing the factors influencing household debt: The case of China. Applied Economics, 54(23), 2627–2642. [Google Scholar] [CrossRef]

- Turinetti, E., & Zhuang, H. (2011). Exploring determinants of U. S. household debt. The Journal of Applied Business Research, 27(6), 85–92. [Google Scholar] [CrossRef]

- Vijverberg, C. C. (2024). Income inequality and household debt: A U.S. state-level spatial analysis. Economic Modelling, 138, 106772. [Google Scholar] [CrossRef]

- Walks, A. (2013). Mapping the urban debtcape: The geography of household debt in Canadian cities. Urban Geography, 34(2), 153–187. [Google Scholar] [CrossRef]

- Wang, Z., Zhang, D., & Wang, J. (2022). How does digital finance impact the leverage of Chinese households? Applied Economics Letters, 29(6), 555–558. [Google Scholar] [CrossRef]

- Wildemauwe, R. I. J., & Sanroman, G. (2022). Household debt and debt to income: The role of business ownership. Quarterly Review of Economics and Finance, 83, 52–68. [Google Scholar] [CrossRef]

- Wohlin, C. (2014). Guidelines for snowballing in systematic literature studies and a replication in software engineering. Blekinge Institute of Technology. [Google Scholar] [CrossRef]

- Wong, Z. Y., Kusairi, S., & Halim, A. Z. (2023). The nexus between households’ indebtedness and consumption: The role of gender, geographical area and income groups. International Journal of Development Issues, 22(1), 72–90. [Google Scholar] [CrossRef]

- Wooldridge, J. M. (2002). Econometric analysis of panel and cross-sectional data. MIT Press. [Google Scholar]

- Yahya, C. N., Zaki., B. M., Azid, N. N., Ali, N. F., & Hussain, N. A. (2023). The determinants of household debt in Malaysia. Information Management and Business Review, 15(3), 183–194. [Google Scholar] [CrossRef]

- Yao, L., Yi, F., & Cai, Y. (2024). The impact of e-commerce activities on rural household leverage. Applied Economics Letters, 31(5), 461–464. [Google Scholar] [CrossRef]

- Yaparatne, Y. M. N. D. K., & Senathissa, W. A. (2021). An empirical analysis to identify the major factors affecting household indebtedness in Sri Lanka. Sri Lanka Journal of Economics, Statistics, and Information Management, 1(1), 55–68. [Google Scholar]

- Zain, M. Z., Atory, A. A. N., & Hanafi, A. S. (2019). Determinants of household debt in Malaysia from the year 2010 to 2017. Advances in Business Research International Journal, 5, 91–101. [Google Scholar] [CrossRef]

- Zanin, L. (2017). Determinants of the conditional probability that a household has informal loans given liquidity constraints regarding access to credit banking channels. Journal of Behavioral and Experimental Finance, 13, 16–24. [Google Scholar] [CrossRef]

- Zhou, S., & Niyitegeka, O. (2023). On the dynamic relationship between household debt and income inequality in South Africa. Journal of Risk and Financial Management, 16, 427. [Google Scholar] [CrossRef]

- Zimunya, M. F., & Raboloko, M. (2015). Determinants of household debt in Botswana: 1994–2012. Journal of Economics and Public Finance, 1(1), 14. [Google Scholar] [CrossRef]

- Zinman, J. (2015). Household debt: Facts, puzzles, theories, and policies. Annual Review of Economics, 7(1), 251–276. [Google Scholar] [CrossRef]

- Zwane, T. T. (2018). Assessing the determinants and effects on non monetary household asset poverty in South Africa [Ph.D. Thesis, University of Johannesburg]. Available online: https://www.uj.ac.za/library/information-resources/e-theses-and-dissertations/ (accessed on 20 October 2024).

| Criteria | Eligibility | Exclusion |

|---|---|---|

| Type of literature | Peer reviewed articles from reputable journals based on empirical data analysed by quantitative methods | Book chapters, dissertations, reports, conference proceedings, and conceptual discussion papers |

| Language | English | Non-English papers |

| Time | Open | Papers published after December 2024 |

| Unit of analysis | Country-level and household data or articles on indebtedness | Individual and company indebtedness articles and those that treated over-indebtedness |

| Country | Studies | Country | Studies | Country | Studies | Country | Studies | Country | Studies | Country | Studies |

|---|---|---|---|---|---|---|---|---|---|---|---|

| USA | 16 | Czechia | 12 | Swirtzerland | 10 | Chile | 6 | Singapore | 4 | Hong Kong | 2 |

| Spain | 14 | Denmark | 12 | Korea | 9 | Luxembourg | 6 | China | 3 | Israel | 2 |

| Belgium | 14 | France | 12 | Greece | 9 | Bulgaria | 6 | Luthuania | 3 | Argentina | 2 |

| Sweden | 14 | Ireland | 12 | Norway | 8 | Slovenia | 6 | Mexico | 3 | Namibia | 1 |

| Germany | 14 | Japan | 11 | Slovakia | 8 | Latvia | 5 | Croatia | 3 | Botswana | 1 |

| Australia | 13 | Portugal | 11 | South Africa | 7 | Brazil | 5 | Thailand | 3 | Peru | 1 |

| Italy | 13 | Austria | 11 | Estonia | 7 | Russia | 5 | Malta | 3 | Taiwan | 1 |

| Finland | 13 | Hungary | 11 | Romania | 7 | Colombia | 4 | Turkey | 3 | ||

| Poland | 12 | UK | 11 | New Zealand | 7 | India | 4 | Iceland | 3 | ||

| Netherlands | 12 | Canada | 10 | Malaysia | 7 | Indonesia | 4 | Cyprus | 3 |

| Theory | Frequency |

|---|---|

| Life cycle hypothesis | 19 |

| Permanent income hypothesis | 5 |

| Rajan hypothesis | 4 |

| House price hypothesis | 3 |

| Age structure hypothesis | 3 |

| Low interest rate hypothesis | 2 |

| Financial deregulation | 2 |

| Welfare retrenchment hypothesis | 2 |

| Post Keynesian and consumption wealth effects | 2 |

| Expenditure cascade hypothesis | 1 |

| Hyperbolic effects | 1 |

| Conspicuous consumption and income inequality | 1 |

| Irrationality of household financial behaviour | 1 |

| Expectations | 1 |

| Rational bubbles | 1 |

| Confidence of storytelling | 1 |

| Absolute income hypothesis | 1 |

| Housing boom hypothesis | 1 |

| Financial asset hypothesis | 1 |

| Credit supply hypothesis | 1 |

| Falling wages hypothesis | 1 |

| Fixed income theory | 1 |

| Country | Studies | Country | Studies | Country | Studies | Country | Studies | Country | Studies | Country | Studies |

|---|---|---|---|---|---|---|---|---|---|---|---|

| China | 9 | Austria | 4 | Malaysia | 2 | Pakistan | 1 | Ireland | 1 | South Africa | 1 |

| USA | 9 | Czechia | 4 | Hungary | 2 | Indonesia | 1 | Uruguay | 1 | Singapore | 1 |

| India | 8 | Estonia | 3 | Chile | 2 | Bulgaria | 1 | Latvia | 1 | Uganda | 1 |

| Italy | 8 | Slovakia | 3 | Finland | 2 | Croatia | 1 | Lithuania | 1 | ||

| Germany | 5 | Australia | 3 | Slovenia | 2 | Romania | 1 | New Zealand | 1 | ||

| Poland | 5 | Denmark | 3 | Sri Lanka | 2 | Albania | 1 | Norway | 1 | ||

| Spain | 5 | Sweden | 3 | Japan | 2 | Bosnia | 1 | Thailand | 1 | ||

| Belgium | 4 | Canada | 2 | Korea | 2 | North Macedonia | 1 | Colombia | 1 | ||

| Netherlands | 4 | Switzerland | 2 | UK | 1 | Serbia | 1 | Cyprus | 1 | ||

| France | 4 | Luxembourg | 2 | Portugal | 1 | Tunisia | 1 | Malta | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chikeya, C.K.; Ntsalaze, L. Determinants of Household Debt: A Systematic Review of the Literature. Economies 2025, 13, 76. https://doi.org/10.3390/economies13030076

Chikeya CK, Ntsalaze L. Determinants of Household Debt: A Systematic Review of the Literature. Economies. 2025; 13(3):76. https://doi.org/10.3390/economies13030076

Chicago/Turabian StyleChikeya, Cloudio Kumbirai, and Lungile Ntsalaze. 2025. "Determinants of Household Debt: A Systematic Review of the Literature" Economies 13, no. 3: 76. https://doi.org/10.3390/economies13030076

APA StyleChikeya, C. K., & Ntsalaze, L. (2025). Determinants of Household Debt: A Systematic Review of the Literature. Economies, 13(3), 76. https://doi.org/10.3390/economies13030076