Abstract

This comprehensive study explored the efficiency landscape of the Jordanian banking industry from 2006 to 2021, utilizing a dual-pronged approach. First, we assessed the efficiency scores of 15 commercial banks, comprising 13 conventional and 2 Islamic institutions, through data envelopment analysis (DEA). Secondly, we investigated the determinants influencing relative efficiency using the Tobit regression model. Our dataset, spanning 240 observations over 16 years, provides a nuanced examination of industry dynamics. DEA, specifically focusing on variable return to scale (VRS), unveils efficiency scores by accounting for scale inefficiencies. The research contributes insights into the operational efficacy of Jordanian banks and provides a robust methodology for understanding efficiency dynamics in the broader financial landscape. The results reveal significant relationships between return on assets, return on equity, GDP growth, and efficiency. Furthermore, it is noteworthy that Islamic banks demonstrate higher efficiency compared to conventional banks. Additionally, non-significant associations were observed with credit risk, bank size, and the ratio of loan loss provision over net income. The findings hold implications for policymakers, industry stakeholders, and researchers aiming to bolster the resilience and competitiveness of Jordan’s banking sector.

1. Introduction

In the ever-evolving realm of financial systems, the banking industry stands as a cornerstone, playing a pivotal role in economic stability and growth. The economic performance of any nation is intricately linked to the strength of its financial and banking infrastructure. Consequently, a robust banking system contributes to economic stability, thereby positively affecting the well-being of the populace.

This study delves into the dynamic landscape of the Jordanian banking sector, a critical component of the nation’s economic infrastructure. Over the period from 2006 to 2021, the industry has witnessed transformative changes, both in its structural composition and operational strategies. The primary aim of this study was to conduct a multifaceted analysis of the efficiency landscape within the Jordanian banking industry, employing sophisticated methodologies such as data envelopment analysis (DEA) and the Tobit regression model. Through this exploration, we sought to evaluate the efficiency scores of 15 commercial banks and understand the underlying determinants influencing their relative efficiency. Additionally, our research aimed to contribute valuable insights that transcend the temporal boundaries of the study, fostering a foundation for informed decision-making and strategic planning in the ever-evolving financial landscape.

The banking sector in Jordan stands as a crucial economic pillar, actively contributing to the GDP and fostering economic growth, stability enhancement, and increased employment opportunities (Jawarneh 2021). Furthermore, the financial landscape in Jordan is notably dominated by banks, encompassing 96% of the total assets within the financial sector, equivalent to 186% of the GDP as of the conclusion of 2021.

The largest segment within banks’ total assets is represented by credit facilities, constituting approximately 49% and notably contributing to 94% of the GDP by the end of 2021. Deposits play a pivotal role as the primary source of funding, comprising 69% of the total sources and significantly accounting for 124% of the GDP by the close of 2021. The Jordanian banking system comprises a total of 23 licensed banks, including 16 Jordanian banks (3 of which are Islamic banks) and 7 branches of foreign banks, 1 of which operates as a foreign Islamic bank branch. The distinctive features of Jordanian banks elucidate a substantial portion of the variance observed in bank profitability.

Efficiency, a linchpin for sustained success, is at the heart of this exploration. In this comprehensive study, we embark on a multifaceted analysis, aiming to unravel the intricacies of efficiency within the Jordanian banking industry. The efficiency of the bank is a comprehensive metric encompassing various performance aspects and employing multiple financial variables (Wu et al. 2006). By employing sophisticated methodologies, including data envelopment analysis (DEA) and the Tobit regression model, we seek to not only evaluate the efficiency scores of 15 commercial banks but also understand the underlying determinants influencing their relative efficiency. The data envelopment analysis (DEA) approach was actually introduced by Abraham Charnes, William W. Cooper, and Edward Rhodes in the late 1970s, with their seminal work published in 1978. Data envelopment analysis (DEA) swiftly emerged as the predominant non-parametric methodology for evaluating the efficiency of decision-making units employing multiple inputs to generate multiple outputs (Pereira et al. 2021). According to Kumar and Singh (2014), one of the advantages of DEA is the capability of being used with any input–output measurement. Simultaneously, our research endeavors to unpack the intricacies of the factors influencing efficiency variations. The Tobit regression model becomes a powerful lens through which we scrutinize these determinants, offering a quantitative dimension to our exploration.

Amid ongoing transformations in the economic and financial landscape, the significance of evaluating the efficiency of commercial banks becomes paramount as a vital element that significantly influences enhancing institutional performance and achieving financial sustainability. The enhancement of institutional performance serves as a comprehensive measure encompassing effectiveness and efficiency in resource utilization and the improvement of banking services. On the other hand, achieving financial sustainability represents a crucial challenge amidst continuous economic fluctuations and market variables.

While numerous studies have examined the efficiency of Jordan’s banking sector, some research has concentrated on related topics. Al-Shammari and Salimi (1998) and Ajlouni et al. (2011) conducted studies on the performance of Jordanian banks in specific periods. Existing research has primarily focused on specific aspects within shorter timeframes. Furthermore, these studies often excluded the growing sector of Islamic banks. Our study aims to contribute to this body of research by providing a comprehensive efficiency analysis over an extended period, encompassing both conventional and Islamic banking institutions. The results and discussions shed light on the intricate dynamics of the Jordanian banking industry, offering a nuanced perspective on efficiency trends and their determinants. Notably, the analysis reveals distinct phases in the industry’s efficiency trajectory, spanning periods of stability, decline, and subsequent improvement. The influence of dynamic factors on operational efficacy becomes evident, prompting further exploration into the specifics of each phase. Islamic banks emerge as consistent outperformers, raising questions about the transferability of their operational models to conventional counterparts. Tobit regression analysis unravels significant relationships between efficiency scores and key determinants, providing valuable insights into the delicate balance between profitability and operational effectiveness.

This study’s relevance extends beyond the realms of academia, resonating with policymakers, industry stakeholders, and researchers alike. Insights gleaned from our findings can inform strategic decisions, enabling policymakers to formulate measures that enhance the resilience and competitiveness of Jordan’s banking sector. Bank executives and regulators can leverage these insights to identify areas for improvement and best practices, fostering a more efficient and robust financial landscape.

In essence, this study forms a crucial bridge between theory and practice, offering a comprehensive analysis of the efficiency landscape within the Jordanian banking industry. As we navigate through the intricate tapestry of financial operations, our aim was to contribute valuable insights that transcend the temporal boundaries of the study, fostering a foundation for informed decision-making and strategic planning in the ever-evolving financial landscape.

This article is structured as follows. Section 1 sets the stage by providing an overview of the evolving Jordanian banking sector and the context of our study. Section 2 presents a thorough literature review, providing a contextual foundation for our study. In Section 3, we articulate the objective of the study, outlining our specific research goals. Moving on to Section 4, we introduce the sample banks. Section 5 encompasses the analysis results, followed by a combined results and discussion in Section 6. We draw overarching insights and conclude our study in Section 7. Lastly, the references cited throughout the article are presented for further exploration. This systematic arrangement aims to present a coherent and detailed account of our study’s methodology, findings, and implications.

2. Literature Review

Efficiency analysis has been a focal point in studies examining the global banking sector. Scholars such as Berger and Humphrey (1997) and Sherman and Gold (1985) have extensively used data envelopment analysis (DEA) to evaluate the operational efficiency of banks across various countries. Their findings underscore the importance of efficiency as a determinant of financial stability and sustainable growth, emphasizing the need for robust methodologies to assess and enhance operational performance. Operational efficiency has been identified as a factor influencing the financial performance of commercial banks, as highlighted by Nataraja et al. (2018). Furthermore, Buchory (2015) analyzed the effect of operational efficiency on banking profitability. Operational efficiency was measured by the ratio of operating expenses to operating income (OEOI), and banking profitability was measured by return on assets (ROA). According to the results, OEOI had a negative and significant impact on ROA. Shah et al. (2019a) introduced a comprehensive three-phase framework incorporating DEA for assessing bank efficiency, a Tobit regression model, and a neural network. The application of this model was demonstrated on an empirical dataset encompassing commercial banks from nations participating in the Belt and Road Initiative. The outcomes of their study furnish valuable insights into the optimization of bank efficiency as a strategic approach to leverage the opportunities presented by the Belt and Road Initiative. DEA has been widely employed in most studies to assess the efficiency of the banking sector in India. It demonstrates versatility by effectively handling multiple inputs and outputs, revealing relationships that might remain obscured when employing alternative methodologies (Kumar and Singh 2014). Jackson and Fethi (2000) used DEA to evaluate the technical efficiency of individual Turkish banks and the Tobit model to investigate the determinants of efficiency. They discovered that larger and more profitable banks are more likely to have higher levels of technical efficiency. Moreover, Aysan and Ceyhan (2008) endeavored to illuminate the trajectory of the Turkish banking sector’s performance through panel data fixed effects regression analysis. Their findings indicated a negative association between efficiency change and branch count. They observed a positive correlation between the loan ratio and the performance indices efficiency and efficiency change. However, return on equity did not exhibit statistical significance in explaining any of the efficiency measures. Casu and Molyneux (2003) explored the impact of the single internal market on productive efficiency in European banking. Utilizing DEA estimation for efficiency measures, they assessed determinants of bank efficiency through the Tobit regression model. The findings indicate a modest enhancement in bank efficiency levels post the EU’s Single Market Programme. Milenković et al. (2022) also employed data envelopment analysis (DEA) to evaluate the intermediate function efficiency of banks across Western Balkan countries from 2015 to 2019. Their findings revealed variations in efficiency levels both among and within countries during the specified timeframe.

As we turn our focus to the Middle East, the studies by Eisazadeh and Shaeri (2012) and Lemonakis et al. (2015) provide valuable insights into the efficiency landscape of the region’s banking industry. These studies, although not exclusively focused on Jordan, shed light on the contextual factors shaping banking efficiency in the Middle East, offering a foundation for our exploration. Apergis and Polemis (2016) examined the correlation between competition and efficiency within the banking sector of Middle East and North African (MENA) countries over the period from 1997 to 2011. The degree of bank efficiency was evaluated using the nonparametric data envelopment analysis (DEA) methodology and bootstrap data envelopment analysis (BDEA). The results revealed a unidirectional (negative) Granger causality, running from efficiency to competition, and attempted to measure the relative efficiency of the top 100 Arab banks.

Mostafa (2007) utilized DEA. The outcomes highlighted suboptimal performance in several banks, pointing to opportunities for substantial improvements. These findings underscore the imperative of addressing inefficiencies to enhance the overall performance of Arab banks. Within the realm of efficiency, Mostafa (2009) delved into an examination of the efficiency levels of prominent Arab banks employing two quantitative methodologies: data envelopment analysis and neural networks. Additionally, he underscored the economic significance of fostering heightened efficiency across the banking sector in the Arab world. Achi (2023) also utilized DEA to evaluate the efficiency of Algerian banks and examined the effects of explanatory factors on their performance.

The efficiency of Islamic banking institutions has received considerable attention as Islamic finance has grown. Muslim jurists have recognized the importance of engaging in banking activities that adhere to legitimate methods in accordance with Islamic principles (Qasim et al. 2017). Hasan and Dridi (2011) investigated the performance of Islamic banks, and Rosman et al. (2014) contributed to this debate by using DEA to assess the efficiency of Islamic banks. Their research sheds light on the unique characteristics and challenges that Islamic banking institutions face, emphasizing the importance of factoring these nuances into efficiency assessments. Johnes et al. (2014) conducted a comparative analysis of Islamic and conventional banks from 2004 to 2009, employing data envelopment analysis (DEA) and meta-frontier analysis (MFA). Their findings indicate that, while Islamic banks exhibit comparable gross efficiency to conventional counterparts, they demonstrate significantly higher net efficiency and lower type efficiency. The diminished type of efficiency in Islamic banks is ascribed to a lack of product standardization, whereas the heightened net efficiency is indicative of strong managerial capabilities within Islamic banking institutions. Additionally, Alexakis et al. (2019) assessed the performance and productivity of Islamic and conventional banks. Their investigation centered on the relatively homogeneous Gulf Cooperation Council (GCC) region spanning the period from 2006 to 2012, a period inclusive of the global financial crisis. The study unveiled that Islamic banks exhibited lower cost and profit performance in comparison to their conventional counterparts, while maintaining comparable revenue performance. The research conducted by Saleh and Zeitun (2007) investigated Islamic banking in Jordan, with a focus on the two largest banks: Jordan Islamic Bank for Finance and Investment and Islamic International Arab Bank. Both banks demonstrated increased efficiency, expanded investments, and played a vital role in financing projects in Jordan. The analysis also highlighted significant growth in credit facilities and profitability within Islamic banks, underscoring their noteworthy contribution to Jordan’s economic development. Qasim et al. (2017) examined the performance of Islamic banks in Jordan from 2010 to 2013, employing three measurement methods, including the DEA approach. Their findings indicated that Jordan Dubai Islamic Bank achieved the highest performance ranking across the three measurement tools, followed by Islamic International Arab Bank. In contrast, Jordan Islamic Bank Finance and Investment recorded the lowest rank.

The reviewed literature emphasizes the global importance of banking efficiency, provides insights into efficiency dynamics in Islamic banking, provides context for the Middle East, including Jordan, and lays the groundwork for further research into the determinants shaping banking efficiency. Our research adds to this body of knowledge by providing a comprehensive assessment of the efficiency landscape in the Jordanian banking industry, combining insights from various strands of the literature.

3. Objective of the Study

The objective of this study was twofold. First, using data of 15 Jordan commercial banks, this study employed a non-parametric frontier method, data envelopment analysis (DEA), to measure the efficiency scores of the Jordan banking industry. Secondly, the study attempted to investigate the determinants of the relative efficiency of the Jordan banking industry using the Tobit regression model.

4. Methods

4.1. The Sample Banks

The total sample comprised 15 banks for a period of 16 years ranging from 2006 to 2021 (Table 1). The data therefore comprised 240 observations (16 observations per bank). Among the 15 banks, 13 were conventional banks and 2 were Islamic banks.

Table 1.

Sample composition.

4.2. Analysis Methods

All analyses were performed using R Statistical Software (v4.2.2; R Core Team 2022). DEA was performed using the rDEA R package (v1.2-7; Simm and Besstremyannaya 2023). Tobit regression was performed using the AER R package (v1.2-10; Kleiber and Zeileis 2008). For any test, a p-value less than 0.05 indicated significance.

4.2.1. DEA (1st Stage Analysis)

Data envelopment analysis (DEA) (Charnes et al. 1978) was used to determine the efficiency for the sample of banks in Jordan. For a comprehensive understanding of DEA techniques and models, refer to the detailed descriptions available in the references (Färe et al. 1994; Ray 2004; Coelli et al. 2005; Cooper et al. 2007; Bogetoft and Otto 2011; Cooper et al. 2011). In brief, DEA is a non-parametric analytical method based on linear programming that can be used to estimate the production frontier of peer decision-making units (DMUs) with multiple inputs and multiple outputs (Cook and Seiford 2009). DEA offers the advantage of being a flexible and nonparametric technique that does not require any assumptions about the production function’s form (Siriopoulos and Tziogkidis 2010). It calculates an empirically best-practice production frontier based on the observed inputs and outputs of individual DMUs, replicating their individual behavior rather than relying on average sample estimates from conventional production functions or assigning prior weight to the input and output (Cook et al. 2014). DEA has been empirically applied in the banking sectors for appraisal of performance (Haslem et al. 1999; Thanassoulis 1999; Siriopoulos and Tziogkidis 2010; Defung 2018; Shah et al. 2019a; Razipour-GhalehJough et al. 2021).

Within the DEA framework, models for calculating efficiencies can be either constant return to scale (CRS), developed by Charnes et al. (1978), or variable return to scale (VRS), developed by Banker et al. (1984). The first method (CRS) assumes that all DMUs operate at an optimal level of efficiency, and this requires the DMUs to operate at the flat portion of the long run average cost curve (Banker et al. 1984; Coelli 1996). In practical applications, certain factors, such as financial and legal constraints, imperfect information, and more, can hinder a DMU from operating at its optimal scale (Coelli et al. 2005). Coelli (1996) emphasized that using the CRS specification when some DMUs are not operating at their optimal scale may lead to measures of technical efficiency mixed up with scale efficiency. The second method (VRS) assumes that there are scale inefficiencies and that not all DMUs operate at an optimal level, and hence imperfect competition is accounted for in the analysis of VRS (Coelli 1996; Banker et al. 1984). As a result, in this study, the VRS approach was employed.

DEA analyses largely fall into the categories of being either input-oriented or output-oriented models (Cook and Seiford 2009). The input-oriented model minimizes the using of inputs for a given level of outputs (i.e., inputs are proportionally reduced while outputs remain fixed). The output-oriented model maximizes the producing of outputs for a given level of the inputs (i.e., outputs are proportionally increased while inputs are held constant) (Cook and Seiford 2009). The choice of input- or output-oriented models depends on the properties of DMUs in the production process or the degree of control that managers have over their inputs and outputs. Given that managers or DMUs, specifically banks, have greater control over their inputs, and banks often prioritize cost control over demand increase (Taylor et al. 2022), the input-oriented model was selected for this study.

Following the notation of Cook and Seiford (2009), consider a set of n DMUs: with each DMU j (j = 1, …, n) using m inputs xij (i = 1, …, m) and generating s outputs yrj (r = 1, …, s), the efficiency score of a DMU () can be computed as

where

- ur is a vector of output weights,

- vi is a vector of input weights,

- yrj and xij are the rth output and ith input for DMU j,

- xio and yro are the ith input and rth output for the considered DMU, and

- is a non-archimedian value designed to enforce strict positivity on the variables.

The primary criticism of the initial DEA findings centers around the lack of statistical inference, which suggests that the estimated efficiency scores may be unreliable. This research tackles this limitation by utilizing the DEA bootstrapping technique introduced by Simar and Wilson (1998). By employing the bootstrap procedure, it becomes possible to obtain statistical inference for the efficiency results. This approach offers bias-corrected estimations and confidence intervals for the original DEA efficiency score.

Input/Output Variables

Selecting appropriate input–output variables is a crucial aspect of DEA models, because the measurement of efficiency and productivity could be meaningless if the chosen measures for inputs and outputs are not carefully specified (Das and Ghosh 2009). According to the literature, intermediation and production methodologies are the most employed approaches for specifying inputs and outputs in studies regarding efficiency (Berger and Humphrey 1997). In the production approach, banks are viewed as production centers, with deposits considered as outputs. On the other hand, in the intermediation approach, banks are seen as intermediaries that facilitate the flow of funds from depositors to borrowers. In this approach, deposits are considered as inputs, along with other relevant input variables (Sealey and Lindley 1977; Hancock 1986). There is not any consensus on which approach works best (Giannakis et al. 2005). Therefore, this research uses an intermediation approach, focusing on the banks’ role in intermediating funds from surplus to deficit units.

The definition of outputs and inputs for financial firms lacks a unanimous consensus, as pointed out by Benston (1972) and Clark (1984). After reviewing the literature on banking industry related DEA studies (e.g., Haslem et al. 1999; Thanassoulis 1999; Siriopoulos and Tziogkidis 2010; Defung 2018; Shah et al. 2019b; Razipour-GhalehJough et al. 2021) and considering the data availability, the researcher has chosen (1) total cost, total liability, and total deposit as input variables, and (2) total assets and total equity as output variables. These data were retrieved from the association of banks in Jordan.

Table 2 summarizes the variables considered in the first stage of analysis for this study. All variables were converted to real value using the GDP deflator, i.e., real value = nominal value/(GDP deflator/100). All variables were measured in millions of USD.

Table 2.

Study variables for DEA.

4.2.2. Tobit Regression (Second Stage Analysis)

Following the suggestion of Coelli et al. (2005), in the second stage of the analysis, this study attempted to investigate the determinants of efficiency scores for the banking industry in Jordan.

To investigate the impact of other factors that possibly affect the efficiency measure, some explanatory variables, representing economic conditions (gross domestic product (GDP) growth), bank characteristics (credit risk, return on assets, return on equity, bank size, and ratio of loan loss provision over net income), and bank type, were chosen to provide explanations as to Jordan banking efficiency differences (See Table 3). A brief of data summary of these variables is presented in Table 3, which presents descriptive statistic for the potential determinants of bank efficiency over the study period.

Table 3.

Study variables for Tobit regression.

To accommodate the limited range of efficiency scores, which range from 0 to 1, this study employed the Tobit regression method (Long 1997). Specifically, the two-limit Tobit model developed by Rosett and Nelson (1975) was applied to allow both upper and lower censoring. Following the notations of Long (1997), with upper and lower censoring, the observed censored variable for subject i can be defined by the following measurement equation:

where

- is the observed censored outcome variable for subject i.

- and are the lower and upper censoring values ( = 0 and = 1 for this study).

- y* is a latent variable that cannot be observed over its entire range. However, y* is observed for outcome values between and , and is censored for outcome values less than or equal to or outcome values greater than or equal to .

- is the structural equation for the Tobit model.

- The x’s are factors observed for all cases and β’s are regression coefficients.

- .

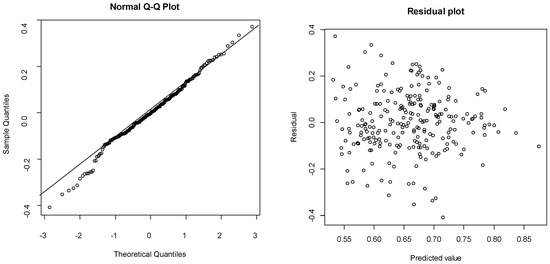

The maximum likelihood estimation (MLE) method can be used to estimate the regression parameters (i.e., the β’s) of the Tobit model (Long 1997). The utilization of the Tobit regression and maximum likelihood estimation (MLE) aligns seamlessly with prior research in the realm of efficiency analysis within the banking sector. This methodological alignment enhances the comparability of our study with the existing literature, thereby augmenting our contribution to the overarching academic discourse on this subject. For instance, Souza et al. (2006) employed data envelopment analysis (DEA) metrics to evaluate the technical efficiency of Brazilian banks, assessing the significance of technical effects. In their investigation, they adeptly applied the maximum likelihood estimation within the framework of general Tobit models. Our adherence to a similar methodological framework not only establishes coherence with established research practices but also fosters a more meaningful dialogue within the academic community. The maximum likelihood estimator for the Tobit model assumes that the errors are normal and homoscedastic (i.e., equal variance). The normality assumption was checked using the quantile–quantile (QQ) plot, and the homoscedasticity assumption was checked using the residual plot in this study.

In Table 4, the definitions of the variables used in our analysis are provided to clarify their roles and meanings in assessing Jordan banking efficiency.

Table 4.

Defining variables.

5. Analysis Results

Table 5 present the efficiency scores determined using DEA for the 15 Jordan banks between 2006 and 2021. It appears that between 2006 and 2011, the efficiency of individual Jordan banks stayed fairly stable, with efficiency scores ranging from 0.519 and 1.000. A decreasing trend in bank efficiency was observed starting at 2011 and continuing toward 2014. In 2014, 6 out of 15 banks (ABC, SGDB, CBJ, IB, BAE, and JCB) had efficiency scores below 0.4. Between 2014 and 2017, bank efficiency showed an upward trend; however, a negative slope was observed right after the year 2017.

Table 5.

Efficiency score for each bank from 2006–2021.

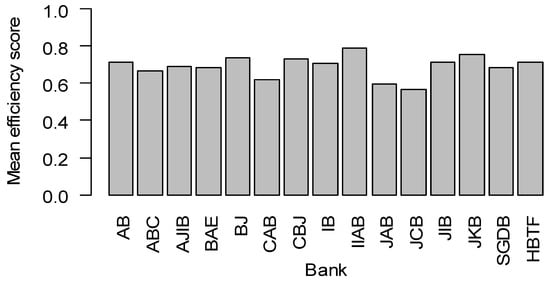

The mean efficiency scores for the 15 banks ranged from 0.595 to 0.792 (Table 2 and Figure 1). Banks had mean efficiency scores above 0.70 (JKB, HBTF, AB, BJ, CBJ, IB, IIAB, and JIB), five banks had mean efficiency scores above 0.60 (ABC, SGDB, CAB, BAE, and AJIB), and two banks had mean efficiency scores above 0.50 (JAB and JCB).

Figure 1.

Mean efficiency scores by bank in Jordan.

Table 6 shows the mean efficiency scores estimation using DEA and the bootstrap results for each year. The original DEA result is column 2, followed by bias-corrected estimates and bias (i.e., the bootstrapping results) in columns 3 and 4, respectively. The other two columns give the lower and upper bounds of the estimated efficiency for the 95% confidence interval (CI). The efficiency estimate reveals that the initial DEA efficiency scores fell within the 95% CI. However, these scores were positively skewed (i.e., upwardly biased) when compared to the bias-corrected efficiency scores. This discrepancy can be attributed to sampling fluctuations, which influenced the sensitivity of the efficiency estimate. The biases vary across the period. The bias was less than 0.04 in 2008–2016 and 2019–2021, but in the remaining years (2006, 2007, 2017, and 2018), the bias was above 0.04, with 2017 showing the largest bias. In sum, the Jordan banking industry was not very efficient in the analysis period. The yearly mean efficiency estimates ranged between 0.463 and 0.882, with the highest level occurred in 2011.

Table 6.

Mean efficiency scores estimation using DEA and the bootstrap results.

Table 7 shows the mean efficiency scores estimation using DEA by bank type. During the period of 2006 and 2021, the mean efficiency scores ranged from 0.451 to 0.872 for conventional banks, and from 0.541 to 0.944 for Islamic banks.

Table 7.

Mean efficiency scores estimation using DEA by bank type.

Table 8 shows the results for Tobit regression. Note that the Tobit regression coefficients can be interpreted in the similar manner to the ordinary least square regression coefficients. However, for the Tobit regression, the linear effect is on the uncensored latent variable, not the observed outcome.

Table 8.

Tobit regression.

According to the results of the Tobit regression, there was a statistically significant relationship between bank efficiency scores and the following determinants: return on assets (z = 4.644, p < 0.001), return on equity (z = −3.074, p = 0.002), bank type (z = 5.115, p < 0.001), and GDP growth (z = 2.880, p = 0.004). In particular,

- A one-unit increase in return on assets was associated with a 16.243 point increase in the predicted value of efficiency score.

- A one-unit increase in return on equity was associated with a 1.484 point decrease in the predicted value of efficiency score.

- The predicted value of efficiency score for Islamic banks was expected to be 0.170 point higher than the predicted value of efficiency score for conventional banks.

- A one-unit increase in GDP growth was associated with a 0.012 point increase in the predicted value of efficiency score.

There was no statistically significant relationship between the bank efficiency scores and the following determinants: the credit risk (z = 1.090, p = 0.276), bank size (z = −0.350, p = 0.727), and the ratio of loan loss provision over net income (z = 1.710, p = 0.087). Figure 2 suggested that the errors of the Tobit model were normal and homoscedastic, and hence the fit of the Tobit model was adequate for the data.

Figure 2.

Assumption assessment for Tobit model.

6. Results and Discussion

The data envelopment analysis (DEA) conducted on the Jordanian banking industry from 2006 to 2021 reveals intriguing dynamics. The examination of efficiency scores unveils that, between 2006 and 2011, individual banks maintained relatively stable efficiency levels, suggesting a period of consistent operational performance. However, a discernible decline in efficiency transpired from 2011 to 2014, with six banks exhibiting scores below 0.4 in 2014. The discernible decrease in efficiency prompts investigations into potential external influences or internal managerial changes that may have contributed to the downturn. As a result, the timeframe from 2014 to 2017 shows a discernible upward trend, implying that banks are implementing adaptive measures or strategic shifts to improve efficiency. However, a negative slope after 2017 invites further investigation into the potential challenges or disruptions affecting the industry during this period. Mean efficiency scores displayed a range from 0.595 to 0.792, showcasing diverse levels of efficiency among the banks and suggesting varying degrees of effectiveness in their operations. It is critical to delve deeper into the contextual factors causing this fluctuation and evaluate the impact of managerial decisions made during this time. This observation underscores the importance of conducting a thorough analysis to elucidate the nuanced dynamics at play and to draw meaningful conclusions regarding the factors influencing efficiency trends in the banking sector.

The observed trends in efficiency, as gleaned from our analysis, delineate distinct phases within the temporal trajectory of Jordanian banks. The first phase, spanning from 2006 to 2011, reveals a period of stability. Subsequently, a downturn in efficiency is discernible from 2011 to 2014, and although there appears to be an attempt at amelioration from 2014 to 2021, the negative slope after 2017 invites further investigation into potential challenges or disruptions affecting the industry during this period. These fluctuations underscore the impact of dynamic factors on the operational efficacy of Jordanian banks. To gain a comprehensive understanding, it is imperative to delve deeper into the specifics of each aforementioned phase and discern the driving forces behind these discernible trends. A meticulous examination of the strategies employed by banks during both the periods of decline and improvement can furnish valuable insights into the adaptability and resilience of the Jordanian banking sector. The academic formulation aims to present the information in a structured and formal manner. Additionally, it encourages a thorough exploration of each phase while highlighting the importance of scrutinizing strategies for a nuanced comprehension of the sector’s adaptability and resilience.

Islamic banks consistently outperformed their conventional counterparts throughout the study period, prompting inquiries into the operational strategies and practices that contribute to the heightened efficiency of Islamic banks. This outcome aligns with findings from a study conducted by Bilal et al. (2011), which employed data envelopment analysis (DEA) to compare the efficiency of Islamic and commercial banks in Pakistan. The study similarly concluded that Islamic banks exhibit higher efficiency levels. The noteworthy and sustained outperformance of Islamic banks raises intriguing questions about the potential transferability of their operational models to conventional banks. Exploring the specific practices and risk management strategies employed by Islamic banks could offer valuable lessons for enhancing the overall efficiency of the Jordanian banking sector.

The Tobit regression analysis brought to light significant relationships between efficiency scores and several determinants. Particularly noteworthy were the statistically significant impacts of return on assets, return on equity, bank type, and GDP growth on efficiency scores. A one-unit increase in return on assets correlated with a noteworthy increase in the predicted efficiency score. This positive relationship emphasizes the importance of asset management in driving overall efficiency. Conversely, a one-unit increase in return on equity corresponded to a decrease in the predicted efficiency score, suggesting a potential trade-off between profitability and efficiency. Further exploration into the nature of this relationship could uncover nuanced dynamics in the banking industry. There is an apparent contradiction between this finding and the general expectation that profitability should be positively related to efficiency, at least in financial terms. The observed relationship indeed appears counterintuitive at first glance. However, this finding can be explained through several theoretical and empirical perspectives:

1. Financial performance vs. operational efficiency: It is important to differentiate between financial performance (e.g., ROE) and operational efficiency. While profitability is a crucial aspect of a bank’s overall performance, it may not necessarily reflect the efficiency of its operational processes. A bank can have high profitability due to various factors, such as leverage and investments, without necessarily optimizing its resource allocation or operational processes.

2. Potential trade-off: The statement in our article about a potential trade-off between profitability and efficiency was intended to highlight the complex nature of the relationship. In some cases, banks might prioritize short-term profits at the expense of long-term operational efficiency, leading to a negative correlation between ROE and efficiency scores.

3. Context-specific factors: The relationship between ROE and efficiency can vary depending on the specific circumstances of the banks in our study. Factors such as market conditions, regulatory requirements, and management decisions can influence this relationship. It is possible that certain banks in Jordan’s context prioritize other objectives over operational efficiency, leading to this observed result.

4. Data envelopment analysis (DEA) limitations: DEA, while a powerful tool for efficiency assessment, has its limitations. It assumes that all banks operate under the same technological and environmental conditions, which may not always be the case. Deviations from these assumptions can result in unexpected findings. DEA exhibits fewer limitations compared to alternative performance measurement methods in selecting input and output variables; however, the efficiency measure derived from DEA is influenced by the combination of inputs and outputs (Debasish 2006).

To address the constrained range of efficiency scores, the study employed the Tobit regression model, which accounts for both upper and lower censoring. The model’s robustness was substantiated through rigorous checks for normality and homoscedasticity. These methodological considerations contribute to the academic rigor of the study, providing a solid foundation for the interpretation and generalizability of the findings. The comprehensive analysis of efficiency trends and determinants, coupled with methodological robustness, positions this study as a valuable contribution to the understanding of the Jordanian banking industry and its operational dynamics.

GDP growth exhibited a positive association with efficiency scores, indicating a potential symbiotic relationship between economic growth and the efficiency of the banking sector. In a study undertaken by Banna and Alam (2020), an anticipation was posited for a positive correlation between GDP growth and the efficiency of Islamic banks. However, credit risk, bank size, and the ratio of loan loss provision over net income did not manifest statistically significant relationships with efficiency scores. While these factors may not have directly influenced efficiency scores in the studied context, their non-significant relationships highlight the need for continued exploration of additional variables that may impact banking efficiency.

In alignment with the extensive body of research presented in the literature review, our study resonates with prior investigations on banking efficiency, particularly within the Middle East. Building upon the insights offered by Eisazadeh and Shaeri (2012), Lemonakis et al. (2015), and Apergis and Polemis (2016), our analysis of the Jordanian banking sector contributes a nuanced understanding of the contextual factors influencing efficiency trends. Additionally, in addressing the efficiency of Islamic banks, our study aligns with the work of Hasan and Dridi (2011), Rosman et al. (2014), and Saleh and Zeitun (2007), extending their perspectives to the Jordanian financial landscape. Furthermore, our investigation into the dynamics of efficiency over time bears some resemblance to the comprehensive framework proposed by Shah et al. (2019a) for assessing bank efficiency. Our findings diverged from the observations offered by Jackson and Fethi (2000) concerning the association between bank size and efficiency scores. Contrary to their study, our analysis did not reveal a statistically significant relationship between bank efficiency scores and bank size. In line with the research conducted by Yuhasril (2019), a discernible relationship has been identified between return on assets and operational efficiency. It is noteworthy that this correlation arises from the understanding that operational efficiency constitutes an integral component of overall efficiency. By acknowledging the existing body of knowledge and integrating it into our analysis, we strive to enhance the coherence and cumulative understanding of banking efficiency.

While our results offer insights into the operational dynamics of the sector, we recognize the importance of translating these findings into actionable recommendations for stakeholders. Considering our robust methodological approach and the Tobit regression model’s ability to address censored efficiency scores, we propose the following considerations for policymakers, regulators, and bank executives. Policymakers may explore targeted measures to enhance the resilience of the banking sector, informed by our efficiency trends. Regulators could consider leveraging the identified best practices to formulate policies that foster a more efficient financial landscape. Bank executives might find value in using our insights to identify specific areas for improvement within their institutions. By explicitly connecting our results to these recommendations, we aim to bridge the gap between academic analysis and practical implications, thereby contributing to informed decision-making within the Jordanian banking industry.

Future research endeavors could undertake a more granular exploration of the identified best practices; this may involve a detailed examination of the implementation nuances and their effectiveness across diverse banking environments. Additionally, an in-depth longitudinal analysis could be pursued to assess the sustained impact of the proposed targeted measures on the resilience and efficiency of the banking sector. Such an investigation would not only contribute further insights to academic discourse but also furnish policymakers and industry stakeholders with a more comprehensive understanding, facilitating more informed and strategic decision-making in the realm of ongoing policy development within the Jordanian banking industry.

7. Conclusions

In conclusion, this comprehensive study provides a nuanced examination of the efficiency landscape within the Jordanian banking industry. Employing data envelopment analysis (DEA) and Tobit regression, our analysis offers valuable insights into the operational efficacy of banks in Jordan. The study reveals dynamic variations in efficiency levels over time and discerns differences between conventional and Islamic banks.

The findings underscore the significance of key determinants, including return on assets, return on equity, bank type, and GDP growth. These identified factors not only contribute to our understanding of efficiency dynamics but also serve as essential guides for policymakers and industry stakeholders. The implications extend beyond the individual banks to the broader resilience and competitiveness of Jordan’s banking sector.

However, it is imperative to acknowledge the limitations of our analysis. The Tobit regression model is predicated on the assumption that errors are normally distributed and homoscedastic. While we checked these assumptions using quantile–quantile (QQ) plots and residual plots, it is important to note that such assumptions, while common in statistical modeling, introduce a level of abstraction that may not fully capture the complexities of real-world scenarios.

Inherent challenges include data constraints, assumptions made during the modeling process, and potential biases. The limitations identified in this study improve the transparency of our research and, more importantly, point to future research avenues to address these limitations.

In essence, the robust methodology and detailed analysis of this study significantly contribute to a broader understanding of the efficiency dynamics in Jordan’s banking sector. As the financial landscape evolves, the insights presented here will be useful in developing policies and strategies to foster a more resilient and competitive banking industry.

Author Contributions

Conceptualization, R.I. and M.M.M.; methodology, R.I.; software, R.I.; validation, R.I. and A.E. formal analysis, R.I.; investigation, R.I.; resources, M.M.M.; data curation, R.I. and A.E. writing—original draft preparation, R.I.; writing—review and editing, R.I. and A.E.; supervision, R.I.; project administration, R.I. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Achi, Adel. 2023. Efficiency and its determinants in the Algerian banks: Network data envelopment analysis and partial least squares regression. International Journal of Productivity and Performance Management 72: 1479–508. [Google Scholar] [CrossRef]

- Ajlouni, Mohd Mahmoud, Mohammad Waleed Hmedat, and Waleed Hmedat. 2011. The relative efficiency of Jordanian banks and its determinants using data envelopment analysis. Journal of Applied Finance and Banking 1: 33. [Google Scholar]

- Alexakis, Christos, Marwan Izzeldin, Jill Johnes, and Vasileios Pappas. 2019. Performance and productivity in Islamic and conventional banks: Evidence from the global financial crisis. Economic Modelling 79: 1–14. [Google Scholar] [CrossRef]

- Al-Shammari, Minwir, and Anwar Salimi. 1998. Modeling the operating efficiency of banks: A nonparametric methodology. Logistics Information Management 11: 5–17. [Google Scholar] [CrossRef]

- Apergis, Nicholas, and Michael Polemis. 2016. Competition and efficiency in the MENA banking region: A non-structural DEA approach. Applied Economics 48: 5276–91. [Google Scholar] [CrossRef]

- Aysan, Ahmet Faruk, and Şanli Pinar Ceyhan. 2008. What determines the banking sector performance in globalized financial markets? The case of Turkey. Physica A: Statistical Mechanics and Its Applications 387: 1593–602. [Google Scholar] [CrossRef]

- Banker, Rajiv, Abraham Charnes, and William Cooper. 1984. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science 30: 1078–92. [Google Scholar] [CrossRef]

- Banna, Hasanul, and Md Rabiul Alam. 2020. Islamic banking efficiency and inclusive sustainable growth: The role of financial inclusion. Journal of Islamic Monetary Economics and Finance 6: 213–42. [Google Scholar] [CrossRef]

- Benston, George J. 1972. Economies of scale of financial institutions. Journal of Money, Credit and Banking 4: 312–41. [Google Scholar] [CrossRef]

- Berger, Allen, and David Humphrey. 1997. Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research 98: 175–212. [Google Scholar] [CrossRef]

- Bilal, Hazrat, Khursheed Ahmad, Habib Ahmad, and Sajid Akbar. 2011. Returns to scale of Islamic banks versus small commercial banks in Pakistan. European Journal of Economics. Finance and Administrative Sciences 30: 136–51. [Google Scholar]

- Bogetoft, Peter, and Lars Otto. 2011. Benchmarking with DEA, SEA, and R. Cham: Springer. [Google Scholar]

- Buchory, Herry Achmad. 2015. Banking profitability: How does the credit risk and operational efficiency effect. Journal of Business and Management Sciences 3: 118–23. [Google Scholar]

- Casu, Barbara, and Philip Molyneux. 2003. A comparative study of efficiency in European banking. Applied Economics 35: 1865–76. [Google Scholar] [CrossRef]

- Charnes, Abraham, William W. Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Clark, Jeffrey A. 1984. Estimation of economies of scale in banking using a generalized functional form. Journal of Money, Credit and Banking 16: 53–68. [Google Scholar] [CrossRef]

- Coelli, Tim. 1996. A guide to DEAP version 2.1: A data envelopment analysis (computer) program. Centre for Efficiency and Productivity Analysis, University of New England, Australia 96: 1–49. [Google Scholar]

- Coelli, Timothy, Dodla Sai Prasada Rao, Christopher O’Donnell, and George Battese. 2005. An Introduction to Efficiency and Productivity Analysis. New York: Springer. [Google Scholar]

- Cook, Wade D., and Larry M. Seiford. 2009. Data envelopment analysis (DEA)-Thirty years on. European Journal of Operational Research 192: 1–17. [Google Scholar] [CrossRef]

- Cook, Wade D., Kaoru Tone, and Joe Zhu. 2014. Data envelopment analysis: Prior to choosing a model. Omega 44: 1–4. [Google Scholar] [CrossRef]

- Cooper, William, Lawrence Seiford, and Joe Zhu. 2011. Handbook on Data Envelopment Analysis. International Series in Operations Research & Management Science. New York: Springer. [Google Scholar]

- Cooper, William, Lawrence Seiford, and Kaoru Tone. 2007. Data Envelopment Analysis, a Comprehensive Text with Models, Applications, References and DEA-Solver Software. New York: Springer. [Google Scholar]

- Das, Abhiman, and Saibal Ghosh. 2009. Financial deregulation and profit efficiency: A nonparametric analysis of Indian banks. Journal of Economics and Business 61: 509–28. [Google Scholar] [CrossRef]

- Debasish, Sathya Swaroop. 2006. Efficiency performance in Indian banking—Use of data envelopment analysis. Global Business Review 7: 325–33. [Google Scholar] [CrossRef]

- Defung, Felisitas. 2018. Determinants of bank efficiency during financial restructuring period: Indonesian case. Jurnal Keuangan dan Perbankan 22: 518–31. [Google Scholar] [CrossRef]

- Eisazadeh, Saeid, and Zeinab Shaeri. 2012. An analysis of bank efficiency in the Middle East and North Africa. International Journal of Banking and Finance 9: 28–47. [Google Scholar] [CrossRef]

- Färe, Rolf, Shawna Grosskopf, and C. Knox Lovell. 1994. Production Frontiers. New York: Cambridge University Press. [Google Scholar]

- Giannakis, Dimitrios, Tooraj Jamasb, and Michael Pollitt. 2005. Benchmarking and incentive regulation of quality of service: An application to the UK electricity distribution networks. Energy Policy 33: 2256–71. [Google Scholar] [CrossRef]

- Hancock, Diana. 1986. A model of the financial firm with imperfect asset and deposit elasticities. Journal of Banking & Finance 10: 37–54. [Google Scholar] [CrossRef]

- Hasan, Maher, and Jemma Dridi. 2011. The effects of the global crisis on Islamic and conventional banks: A comparative study. Journal of International Commerce, Economics and Policy 2: 163–200. [Google Scholar] [CrossRef]

- Haslem, John A., Carl A. Scheraga, and James P. Bedingfield. 1999. DEA efficiency profiles of US banks operating internationally. International Review of Economics & Finance 8: 165–82. [Google Scholar] [CrossRef]

- Jackson, Peter M., and Meryem Duygun Fethi. 2000. Evaluating the Efficiency of Turkish Commercial Banks: An Application of DEA and Tobit Analysis. Leicester: University of Leicester. Available online: https://hdl.handle.net/2381/369 (accessed on 4 December 2023).

- Jawarneh, Saleh. 2021. Financial Performance of Commercial Banks inJordan: Application of the CAMELS Model. Prosperitas 8: 4. [Google Scholar] [CrossRef]

- Johnes, Jill, Marwan Izzeldin, and Vasileios Pappas. 2014. A comparison of performance of Islamic and conventional banks 2004–2009. Journal of Economic Behavior & Organization 103: S93–S107. [Google Scholar] [CrossRef]

- Kleiber, Christian, and Achim Zeileis. 2008. Applied Econometrics with R. New York: Springer. Available online: https://cran.r-project.org/package=AER (accessed on 26 November 2023).

- Kumar, Nand, and Archana Singh. 2014. Efficiency analysis of banks using DEA: A review. International Journal of Advance Research and Innovation 1: 120–26. [Google Scholar] [CrossRef]

- Lemonakis, Christos, Fotini Voulgaris, Konstantinos Vassakis, and Stylianos Christakis. 2015. Efficiency, capital and risk in banking industry: The case of Middle East and North Africa (MENA) countries. International Journal of Financial Engineering and Risk Management 2: 109–23. [Google Scholar] [CrossRef]

- Long, John. 1997. Regression Models for Categorical and Limited Dependent Variables. Thousand Oaks: Sage. [Google Scholar]

- Milenković, Nada, Boris Radovanov, Branimir Kalaš, and Aleksandra Marcikić Horvat. 2022. DEA’s two-stage external analysis of bank efficiency in the Western Balkan countries. Sustainability 14: 978. [Google Scholar] [CrossRef]

- Mostafa, Mohamed. 2007. Benchmarking top Arab banks’ efficiency through efficient frontier analysis. Industrial Management & Data Systems 107: 802–23. [Google Scholar] [CrossRef]

- Mostafa, Mohamed M. 2009. Modeling the efficiency of top Arab banks: A DEA–neural network approach. Expert Systems with Applications 36: 309–20. [Google Scholar] [CrossRef]

- Nataraja, N. S., Nagaraja Rao Chilale, and L. Ganesh. 2018. Financial performance of private commercial banks in India: Multiple regression analysis. Academy of Accounting and Financial Studies Journal 22: 1–12. [Google Scholar]

- Pereira, Miguel Alves, Diogo Cunha Ferreira, José Rui Figueira, and Rui Cunha Marques. 2021. Measuring the efficiency of the Portuguese public hospitals: A value modelled network data envelopment analysis with simulation. Expert Systems with Applications 181: 115169. [Google Scholar] [CrossRef]

- Qasim, Yazan Radwan, Yazis Mohamad, and Norhazlina Ibrahim. 2017. Measuring the performance of Jordanian Islamic banks. Journal of Public Administration and Governance 7: 25–47. [Google Scholar] [CrossRef][Green Version]

- Ray, Subhash. 2004. Data Envelopment Analysis: Theory and Techniques for Economics and Operations Research. New York: Cambridge University Press. [Google Scholar]

- Razipour-GhalehJough, Somayeh, Farhad Hosseinzadeh Lotfi, Mohsen Rostamy-Malkhalifeh, and Hamid Sharafi. 2021. Benchmarking bank branches: A dynamic DEA approach. Journal of Information and Optimization Sciences 42: 1203–36. [Google Scholar] [CrossRef]

- R Core Team. 2022. R: A Language and Environment for Statistical Computing. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Rosett, Richard N., and Forrest D. Nelson. 1975. Estimation of the two-limit probit regression model. Econometrica: Journal of the Econometric Society 43: 141–46. [Google Scholar] [CrossRef]

- Rosman, Romzie, Norazlina Abd Wahab, and Zairy Zainol. 2014. Efficiency of Islamic banks during the financial crisis: An analysis of Middle Eastern and Asian countries. Pacific-Basin Finance Journal 28: 76–90. [Google Scholar] [CrossRef]

- Saleh, Ali Salman, and Rami Zeitun. 2007. Islamic banks in Jordan: Performance and efficiency analysis. Review of Islamic Economics 11: 41–62. [Google Scholar]

- Sealey, C. W., Jr., and James T. Lindley. 1977. Inputs, outputs, and a theory of production and cost at depository financial institutions. The Journal of Finance 32: 1251–1266. [Google Scholar] [CrossRef]

- Shah, Akber Aman, Desheng Dash Wu, Vladimir Korotkov, and Gul Jabeen. 2019a. Do commercial banks benefited from the belt and road initiative? A three-stage DEA-tobit-NN analysis. IEEE Access 7: 37936–37949. [Google Scholar] [CrossRef]

- Shah, Vladimir, Desheng Wu, and Vladimir Korotkov. 2019b. Are sustainable banks efficient and productive? A data envelopment analysis and the Malmquist productivity index analysis. Sustainability 11: 2398. [Google Scholar] [CrossRef]

- Sherman, H. David, and Franklin Gold. 1985. Bank branch operating efficiency: Evaluation with data envelopment analysis. Journal of Banking & Finance 9: 297–315. [Google Scholar] [CrossRef]

- Simar, Leopold, and Paul W. Wilson. 1998. Sensitivity analysis of efficiency scores: How to bootstrap in nonparametric frontier models. Management Science 44: 49–61. [Google Scholar] [CrossRef]

- Simm, Jaak, and Galina Besstremyannaya. 2023. rDEA: Robust Data Envelopment Analysis (DEA) for R. R Package Version 1.2-7. Available online: https://cran.r-project.org/package=rDEA (accessed on 24 November 2023).

- Siriopoulos, Costas, and Panagiotis Tziogkidis. 2010. How do Greek banking institutions react after significant events?—A DEA approach. Omega 38: 294–308. [Google Scholar] [CrossRef]

- Souza, Geraldo S., Roberta Blass Staub, and Benjamin Miranda Tabak. 2006. Assessing the significance of factors effects in output oriented dea measures of efficiency: An application to Brazilian banks. Revista Brasileira de Economia de Empresas 6: 7. [Google Scholar]

- Taylor, Daniel, Bernard Sarpong, and Eunice Yaa Cudjoe. 2022. Cost-efficiency and bank profitability during health crisis. Applied Economics Letters, 1–6. [Google Scholar] [CrossRef]

- Thanassoulis, Emmanuel. 1999. Data envelopment analysis and its use in banking. Interfaces 29: 1–13. [Google Scholar] [CrossRef]

- Wu, Desheng Dash, Zijiang Yang, and Liang Liang. 2006. Using DEA-neural network approach to evaluate branch efficiency of a large Canadian bank. Expert Systems with Applications 31: 108–15. [Google Scholar] [CrossRef]

- Yuhasril, Yuhasril. 2019. The effect of capital adequacy ratio (CAR), non performing loan (NPL), operational efficiency (BOPO), net interest margin (NIM), and loan to deposit ratio (LDR), on return on assets (ROA). Research Journal of Finance and Accounting 10: 166–76. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).