The Effects of Oil Price Volatility on South African Stock Market Returns

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Basic Concept of Copulas GARCH Approach

3.2. Volatility Models

Glosten, Jagannathan, and Runkle-Generalized Autoregressive Conditional Heteroscedastic (GJR-GARCH Model)

- E-GARCH Model

3.3. Multivariate Model

3.3.1. Sklar’s Theorem

3.3.2. Estimating Function

3.3.3. Maximum Likelihood Estimation

3.3.4. Symmetrized Joe-Clayton Copula (SJC)

4. Model Estimations and Empirical Results

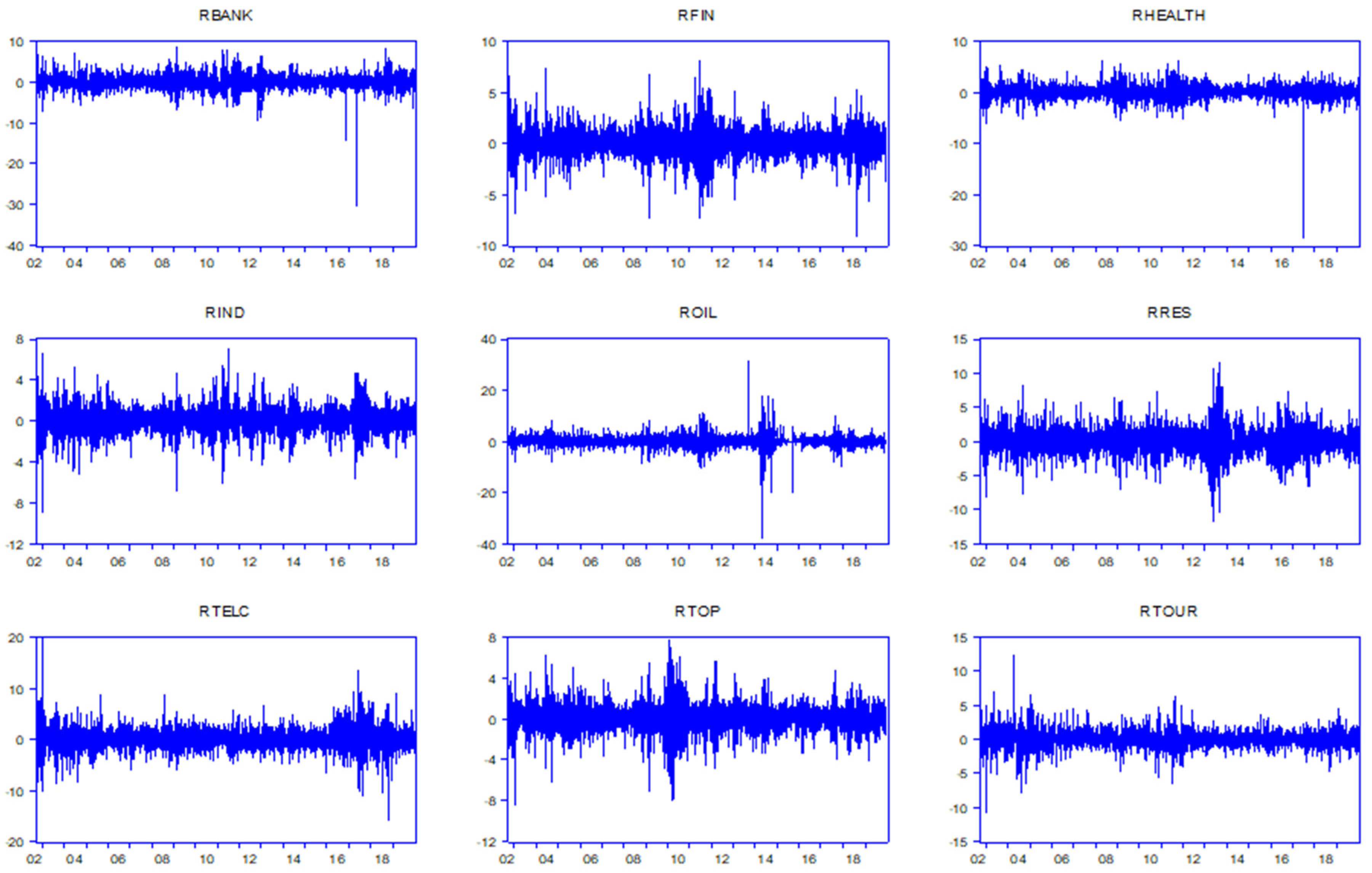

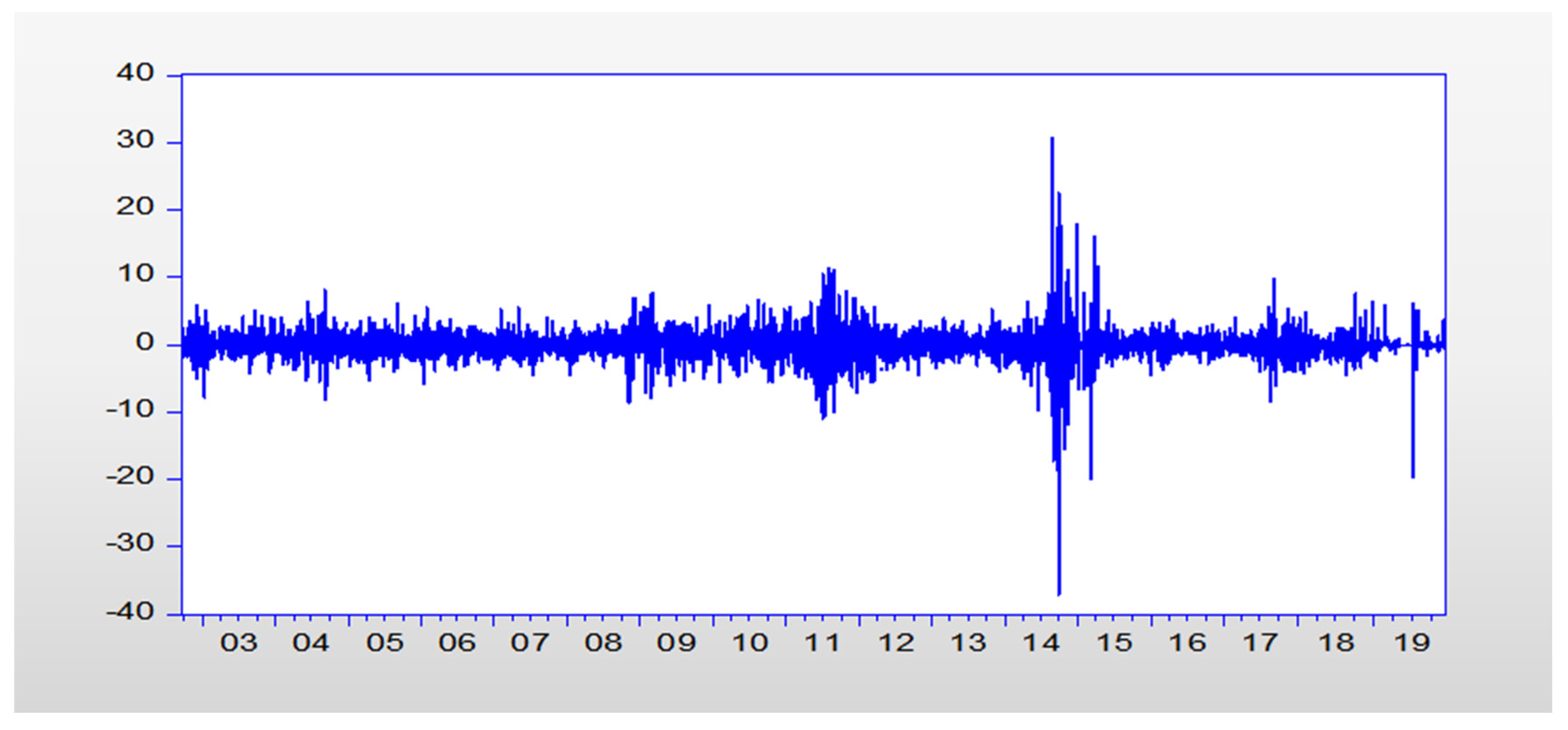

4.1. Data Description

4.2. Descriptive Statistics and Preliminary Analysis

4.3. Empirical Results

4.3.1. Volatility Models (Marginal Distributions)

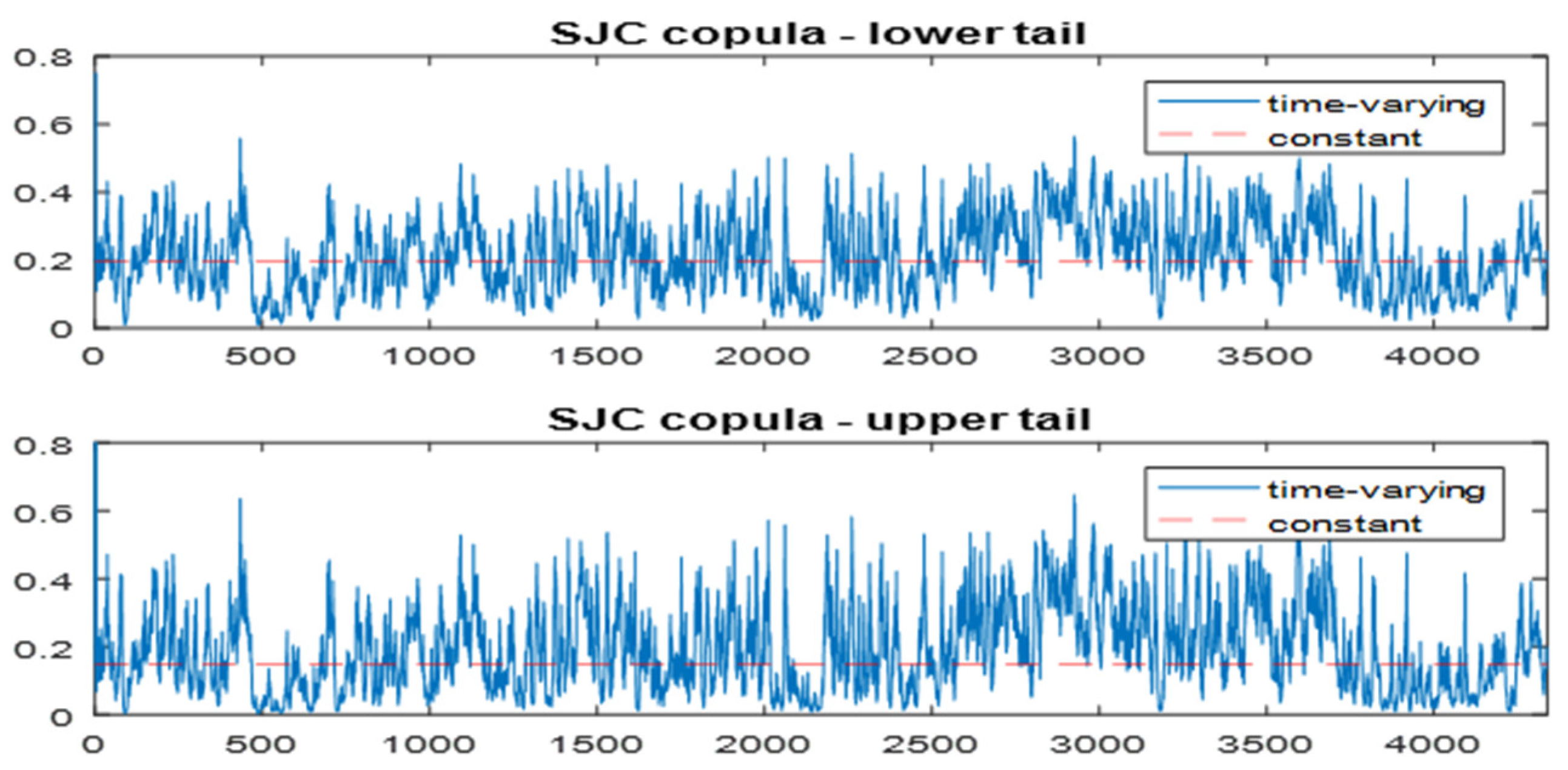

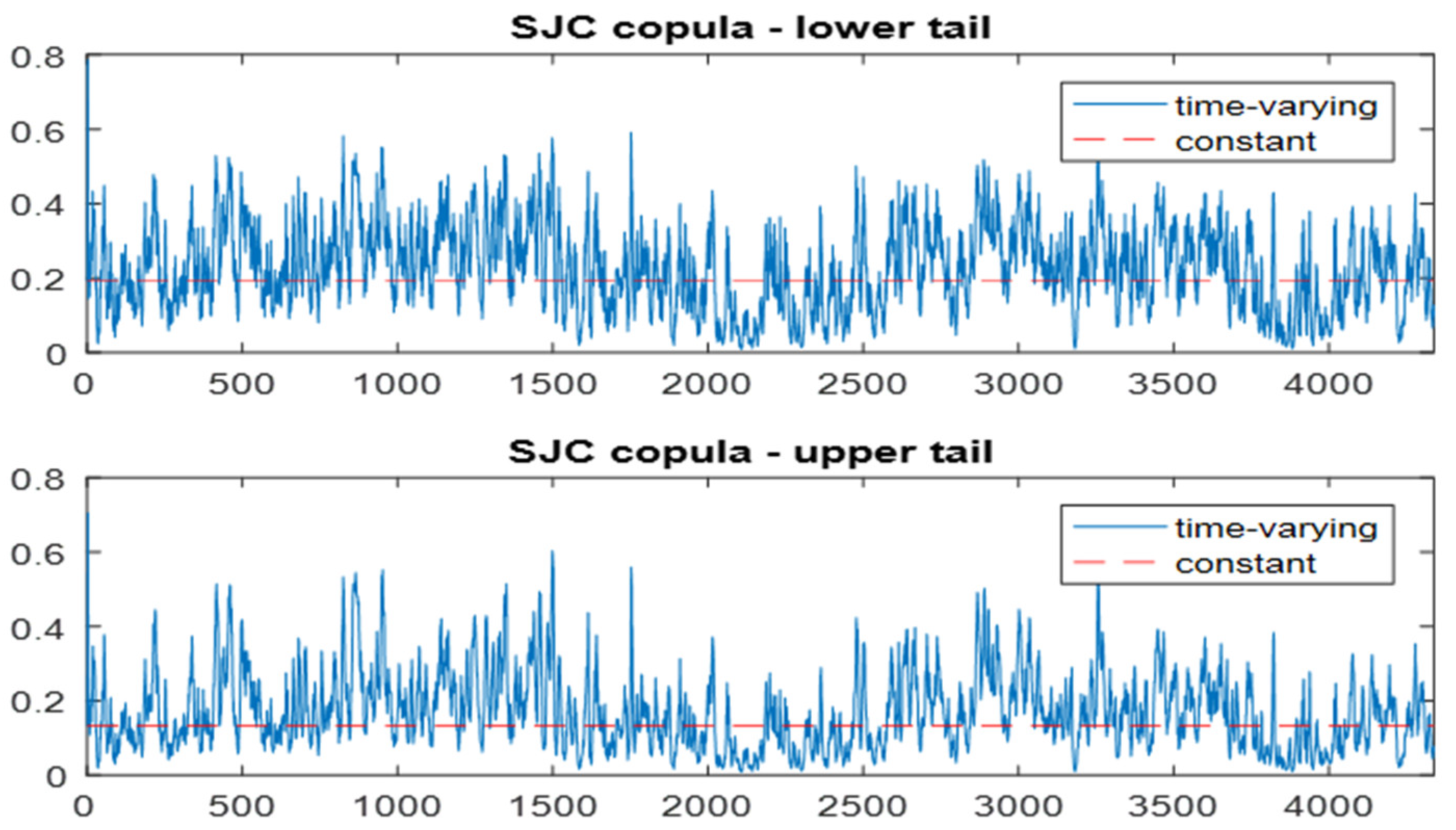

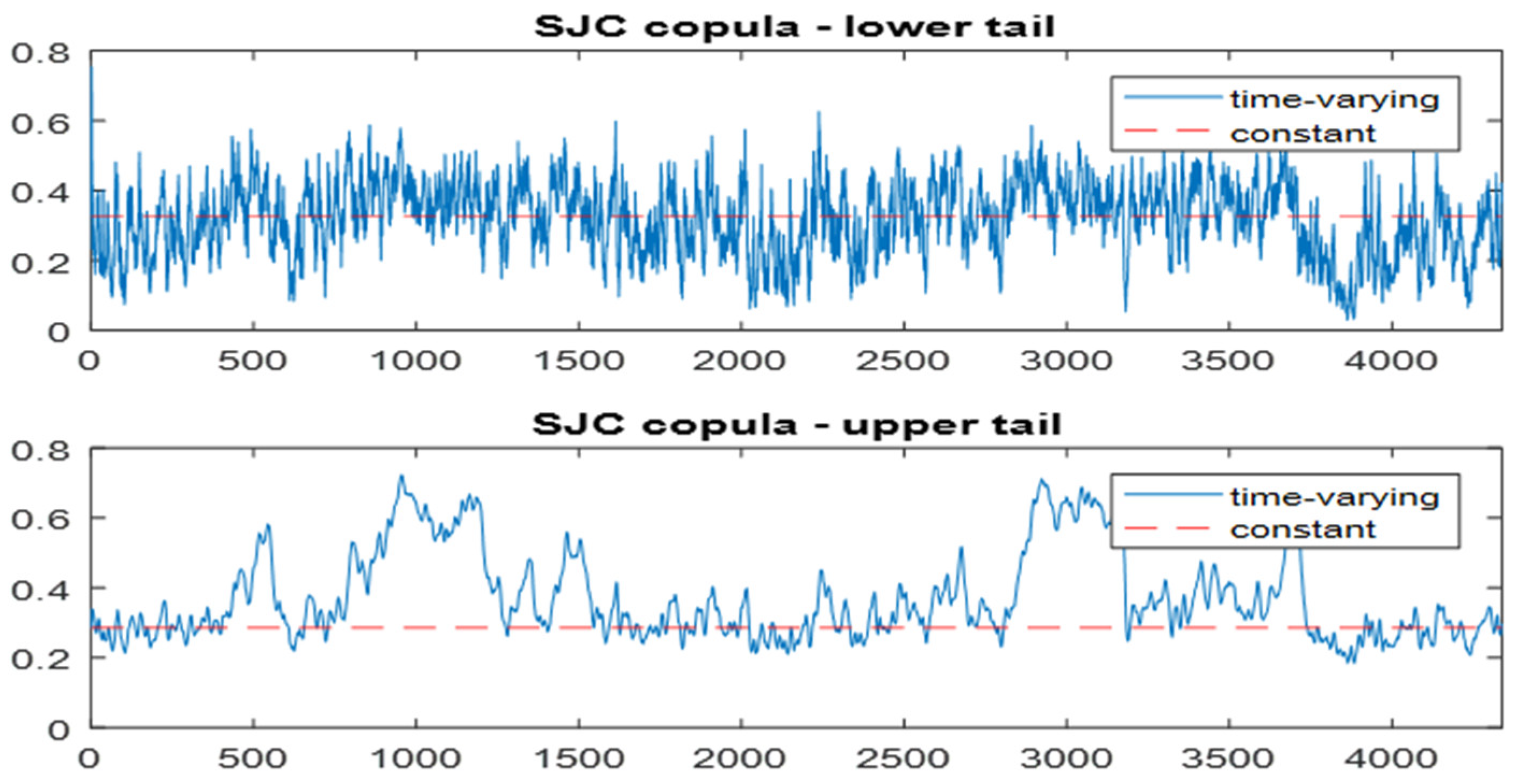

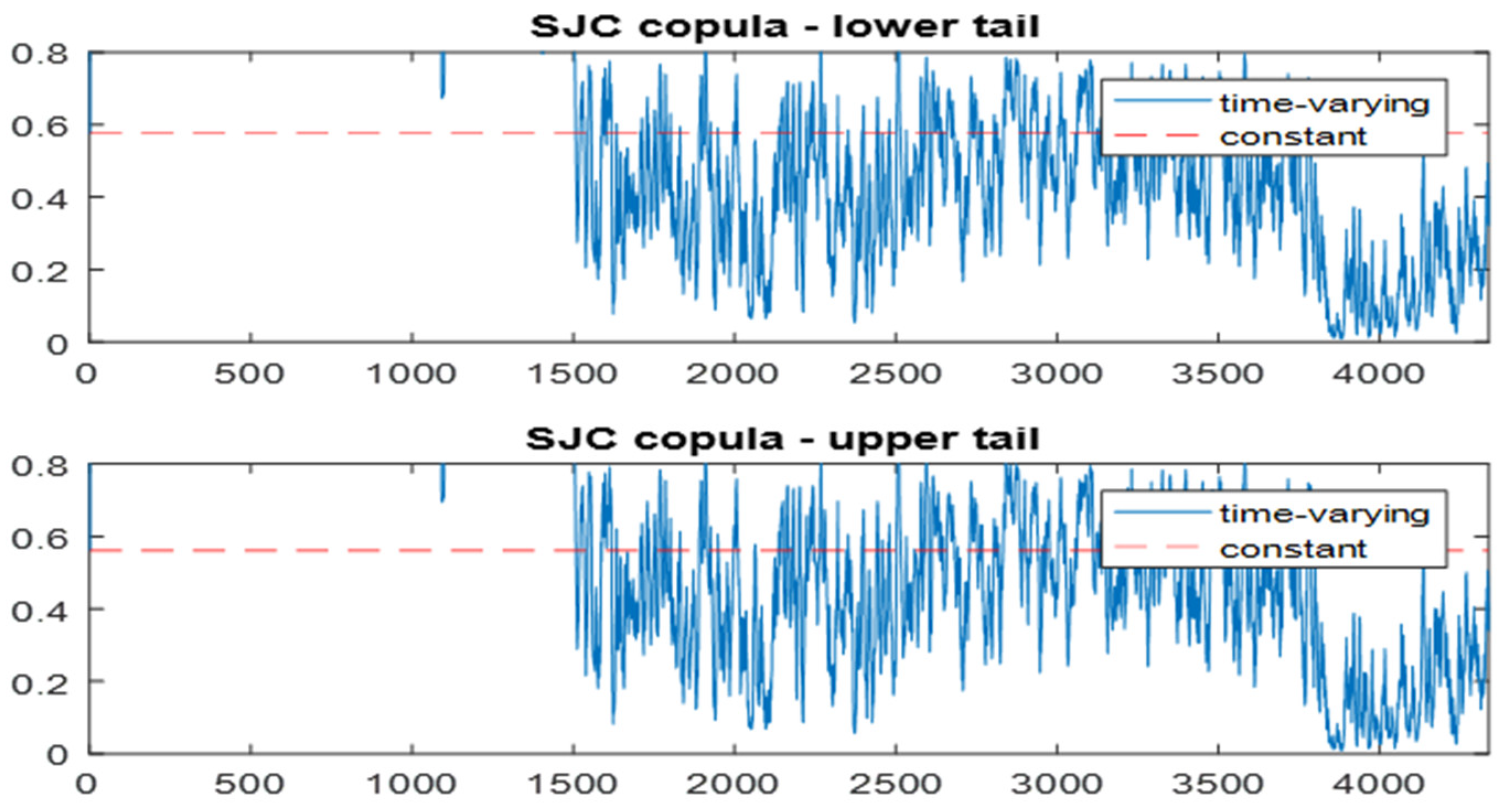

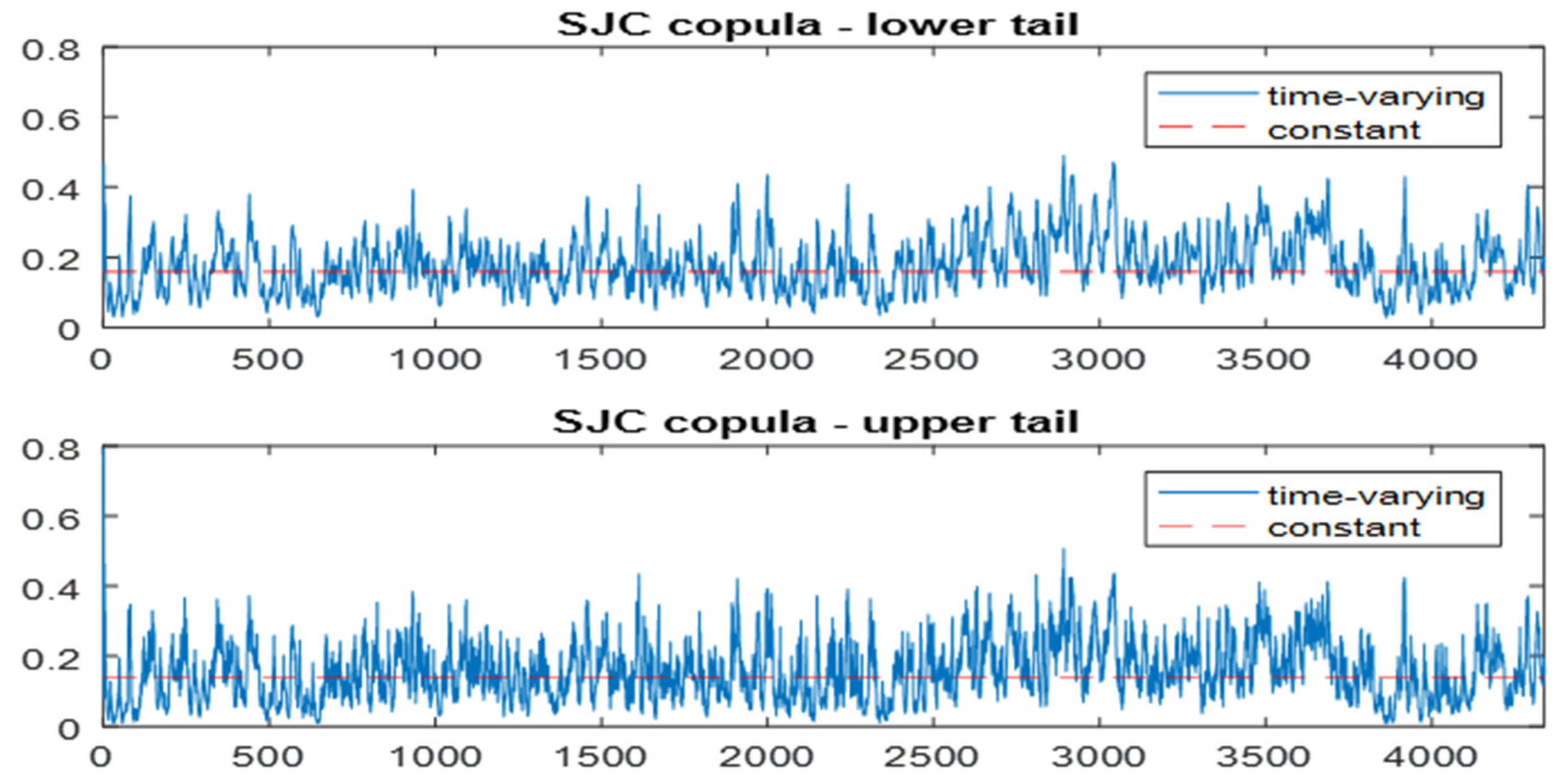

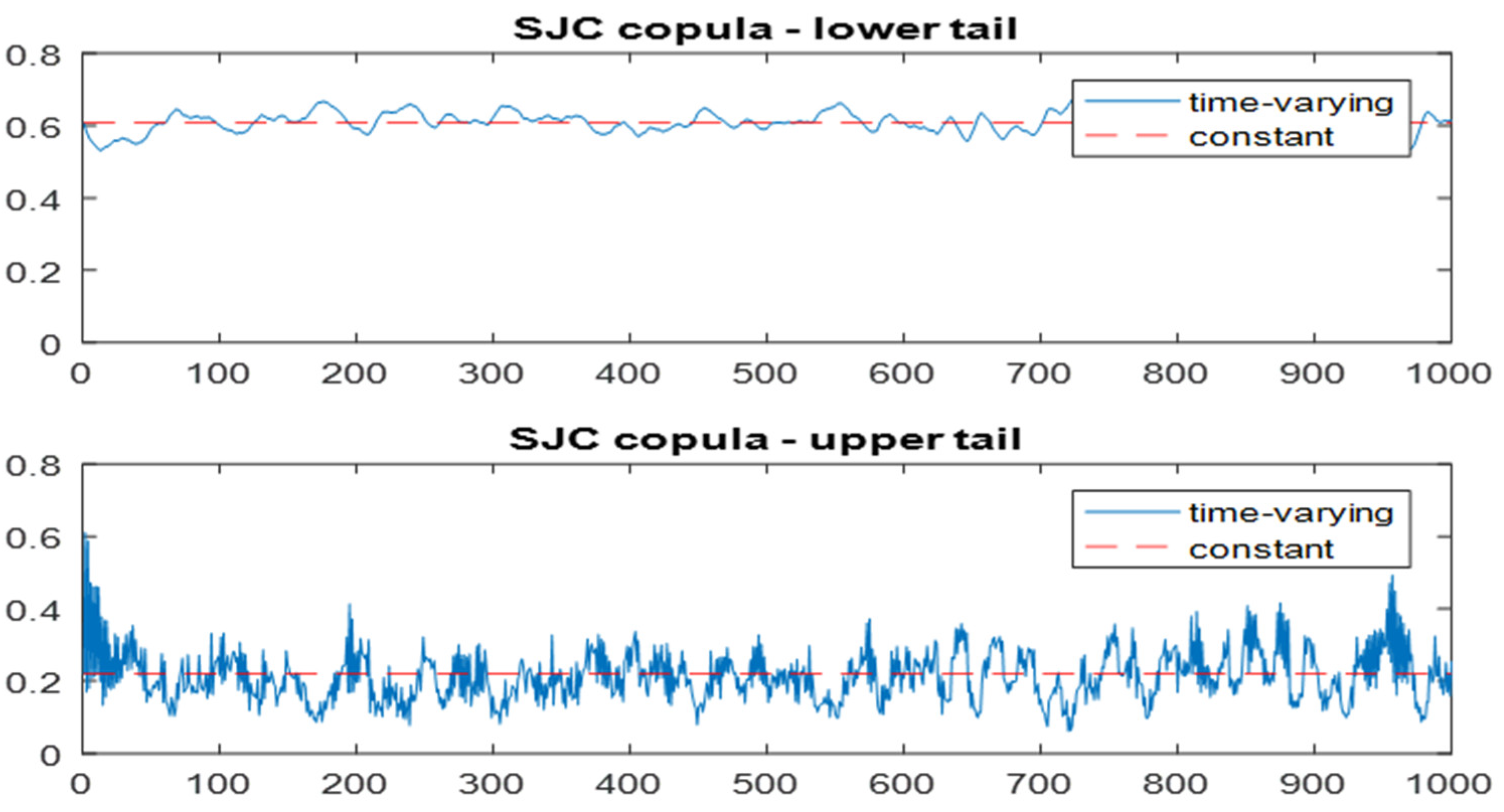

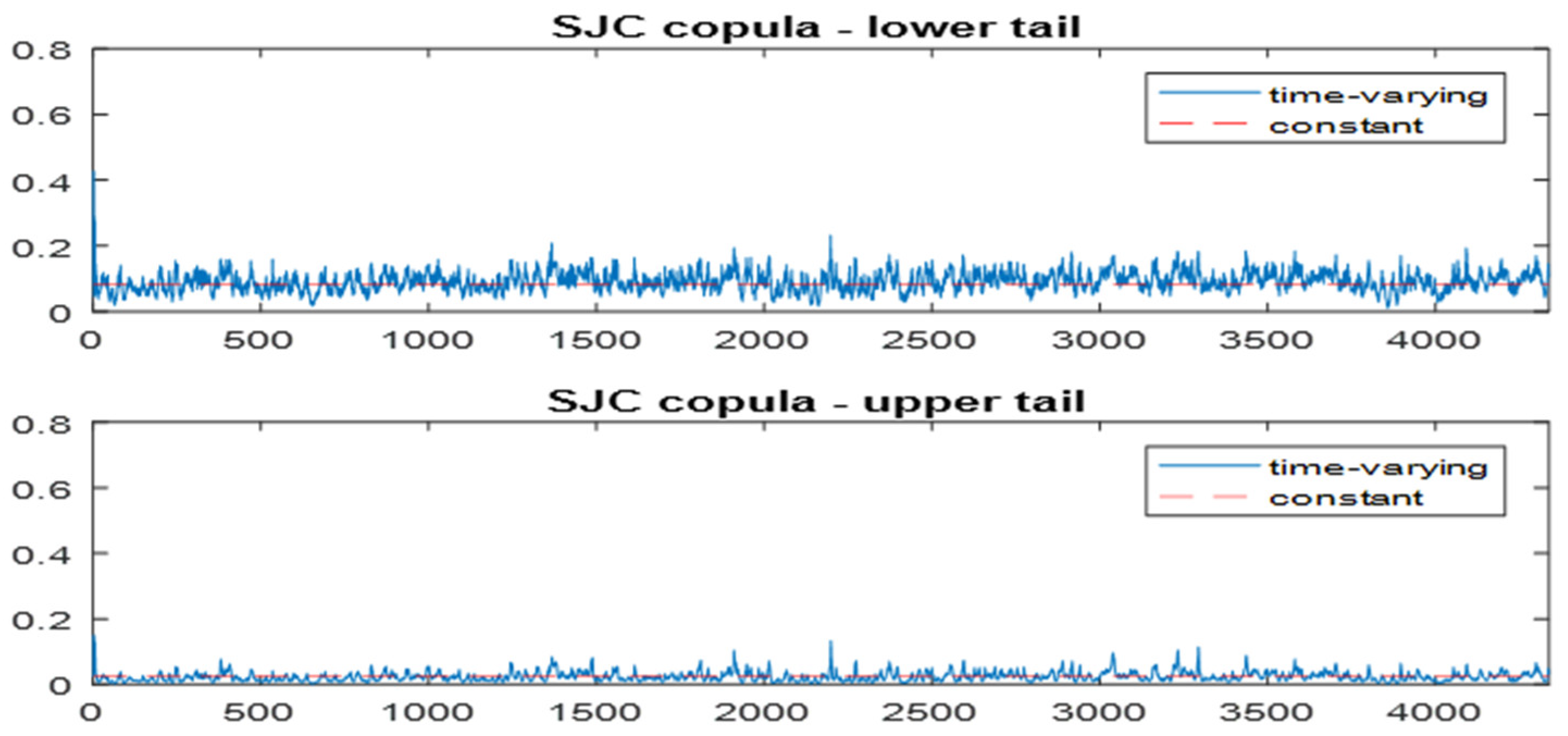

4.3.2. Bivariate Symmetrized Joe-Clayton (SJC) Copula

4.3.3. Symmetrized Joe-Clayton (SJC) Copula

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alzyoud, H., E. Z. Wang, and M. G. Basso. 2018. Dynamics of Canadian oil price and its impact on exchange rate and stock market. International Journal of Energy Economics and Policy 8: 107–14. [Google Scholar]

- Arouri, E. M., and K. D. Nguyen. 2010. Oil prices, stock markets and portfolio investment:Evidence from sector analysis in Europe over the last decade. Energy Policy 38: 4528–39. [Google Scholar] [CrossRef]

- Arouri, M. E. H. 2011. Does crude oil move stock markets in Europe? A sector investigation. Economic Modelling 28: 1716–25. [Google Scholar] [CrossRef]

- Başkaya, Y. S., T. Hülagü, and H. Küçük. 2013. Oil price uncertainty in a small open economy. IMF Economic Review 61: 168–98. [Google Scholar] [CrossRef]

- Beckmann, J., T. Berger, and R. Czudaj. 2016. Oil price and FX-rates dependency. Quantitative Finance 16: 477–88. [Google Scholar] [CrossRef]

- Bollerslev, T. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Bouri, E. 2015. Oil volatility shocks and the stock markets of oil-importing MENA economies: A tale from the financial crisis. Energy Economics 51: 590–98. [Google Scholar] [CrossRef]

- Cai, X., S. Hamori, L. Yang, and S. Tian. 2020. Multi-Horizon Dependence between Crude Oil and East Asian Stock Markets and Implications in Risk Managementk. Energies 13: 294. [Google Scholar] [CrossRef]

- Choi, K., and S. Hammoudeh. 2010. Volatility behavior of oil, industrial commodity and stock markets in a regime-switching environment. Energy Policy 38: 4388–99. [Google Scholar] [CrossRef]

- Dai, Z., and H. Zhu. 2022. Time-varying spillover effects and investment strategies between WTI crude oil, natural gas and Chinese stock markets related to belt and road initiative. Energy Economics 108: 105883. [Google Scholar] [CrossRef]

- Diebold, F. X., and K. Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Diebold, F. X., and K. Yılmaz. 2014. On the network topology of variance decompositions: Measuring the connectedness of financial firms. Journal of Econometrics 182: 119–34. [Google Scholar] [CrossRef]

- Dutta, A., J. Nikkinen, and T. Rothovius. 2017. Impact of oil price uncertainty on Middle East and African stock markets. Energy 123: 189–97. [Google Scholar] [CrossRef]

- Elyasiani, E., I. Mansur, and B. Odusami. 2013. Sectoral stock return sensitivity to oil price changes: A double-threshold FIGARCH model. Quantitative Finance 13: 593–612. [Google Scholar] [CrossRef]

- Engle, R. F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica 58: 987–1007. [Google Scholar] [CrossRef]

- Engle, R. F. 1990. Stock volatility and the crash of’87: Discussion. The Review of Financial Studies 3: 103–6. [Google Scholar] [CrossRef]

- Engle, R. F., and V. K. Ng. 1993. Measuring and testing the impact of news on volatility. The Journal of Finance 48: 1749–78. [Google Scholar] [CrossRef]

- Eyden, R. V., M. Difeto, R. Gupta, and M. E. Mark. 2019. Oil price volatility and economic growth: Evidence from advanced economies using more than a century’s data. Applied Energy 233: 612–21. [Google Scholar] [CrossRef]

- Feng, J., Y. Wang, and L. Yin. 2017. Oil volatility risk and stock market volatility predictability: Evidence from G7 countries. Energy Economics 18: 240–54. [Google Scholar] [CrossRef]

- Ferdi, K., and E. Yildirim. 2014. The causal effect of shifting oil to natural gas consumption oncurrent account balance and economic growth in 11 OECDcountries: Evidence from bootstrap-corrected panel causality test. Social and Behavioral Sciences 143: 1064–69. [Google Scholar]

- Filis, G., S. Degiannakis, and C. Floros. 2011. Dynamic correlation between stock market and oil prices: The case of oil-importing and oil-exporting countries. International Review of Financial Analysis 20: 152–64. [Google Scholar] [CrossRef]

- Glosten, L., R. Jagannathan, and D. Runkle. 1993. On the relation between expected value and the volatility of the nominal excess return on stocks. Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Gupta, R., and M. P. Modise. 2013. Does the source of oil price shocks matter for South African stock returns? A structural VAR approach. Energy Economics 40: 825–31. [Google Scholar] [CrossRef]

- Hamdi, B., M. Aloui, F. Alqahtani, and A. Tiwari. 2019. Relationship between the oil price volatility and sectoral stock markets in oil-exporting economies: Evidence from wavelet nonlinear denoised based quantile and Granger-causality analysis. Energy Economics 80: 536–52. [Google Scholar] [CrossRef]

- Hamma, W., A. Jarboui, and A. Ghorbel. 2014. Effect of oil price volatility on Tunisian stock market at sector-level and effectiveness of hedging strategy. Procedia Economics and Finance 13: 109–27. [Google Scholar] [CrossRef]

- He, Y., and S. Hamori. 2019. Conditional dependence between oil prices and exchange rates in BRICS countries: An application of the copula-GARCH model. Journal of Risk and Financial Management 12: 99. [Google Scholar] [CrossRef]

- He, Y., T. Nakajima, and S. Hamori. 2020. Can BRICS’s currency be a hedge or a safe haven for energy portfolio? An evidence from vine copula approach. The Singapore Economic Review 65: 805–36. [Google Scholar] [CrossRef]

- Jones, C. M., and G. Kaul. 1996. Oil and the stock markets. Journal of Finance 51: 463–91. [Google Scholar] [CrossRef]

- Joo, Y. C., and S. Y. Park. 2021. The impact of oil price volatility on stock markets: Evidences from oil-importing countries. Energy Economics 101: 105413. [Google Scholar] [CrossRef]

- Li, J., and P. Li. 2021. Empirical analysis of the dynamic dependence between WTI oil and Chinese energy stocks. Energy Economics 93: 104299. [Google Scholar] [CrossRef]

- Naeem, M., Z. Umar, S. Ahmed, and E. M. Ferrouhi. 2020. Dynamic dependence between ETFs and crude oil prices by using EGARCH-Copula approach. Physica A: Statistical Mechanics and Its Applications 557: 124885. [Google Scholar] [CrossRef]

- Nelson, D. B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- OPEC. 2020. Press Release for the OPEC 179th Meeting of the Conference Concludes. Available online: https://www.opec.org/opec_web/en/press_room/5963.htm#:~:text=The%20179th%20Meeting%20of,welcomed%20new%20ministers%3A%20HE%20Dr (accessed on 3 June 2023).

- Patton, A. J. 2006. A Review of Copula Models for Economic Time Series. Journal of Multivariate Analysis 110: 4–18. [Google Scholar] [CrossRef]

- Patton, A. J. 2012. Modelling asymmetric exchange rate dependence. International Economic Review 47: 527–56. [Google Scholar] [CrossRef]

- Phan, D. H. B., S. S. Sharma, and P. K. Narayan. 2015. Oil price and stock returns of consumers and producers of crude oil. Journal of International Financial Markets, Institutions and Money 34: 245–62. [Google Scholar] [CrossRef]

- Pirlogea, C., and C. Cicea. 2012. Econometric perspective of the energy consumption and economic growth relation in European Union. Renewable and Sustainable Energy Reviews 16: 5718–26. [Google Scholar] [CrossRef]

- Silvapulle, P., R. Smyth, X. Zhang, and J. Fenech. 2017. Nonparametric panel data model for crude oil and stock prices in net oil importing countries. Energy Economics 67: 255–67. [Google Scholar] [CrossRef]

- Sklar, M. 1959. Fonctions de répartition à n dimensions et leurs marges. Annales de l’ISUP 8: 229–31. [Google Scholar]

- Stocker, M., J. Baffes, and D. Vorisek. 2018. What Triggered the Oil Price Plunge of 2014–2016 and Why It Failed to Deliver an Economic Impetus in Eight Charts. Washington, DC: World Babk GroupGlobal Economic Prospects. [Google Scholar]

- Swanepoel, J. A. 2006. The impact of external shocks on South African inflation at different price stages. Journal for Studies in Economics and Econometrics 30: 1–22. [Google Scholar] [CrossRef]

- Taylor, S. 1986. Modelling Financial Time Series. Chichester: Wiley. [Google Scholar]

- Tiwari, A. K., I. D. Raheem, S. Bozoklu, and S. Hammoudeh. 2022. The oil price, macroeconomic fundamentals nexus for emerging market economies: Evidence from a wavelet analysis. International Journal of Finance and Economics 27: 1569–90. [Google Scholar] [CrossRef]

- SA. Department of Energy. 2019. The South African Energy Sector Report. Available online: https://www.energy.gov.za/files/media/explained/2019-South-African-Energy-Sector-Report.pdf (accessed on 3 June 2023).

- Valdés, A. L., L. A. Fraire, and R. D. Vázquez. 2016. A copula-TGARCH approach of conditional dependence between oil price and stock market index: The case of Mexico. Centro de Estudios Económicos 31: 47–63. [Google Scholar]

- Wang, Y., and Q. Liu. 2006. Comparison of Akaike information criterion (AIC) and Bayesian information criterion (BIC) in selection of stock–recruitment relationships. Fisheries Research 77: 220–25. [Google Scholar] [CrossRef]

- Wang, Y., C. Wu, and L. Yang. 2013. Oil price shocks and stock market activities: Evidence from oil-importing and oil-exporting countries. Journal of Comparative Economics 41: 1220–39. [Google Scholar] [CrossRef]

- Yuan, X., J. Tang, W. K. Wong, and S. Sriboonchitta. 2020. Modeling Co-Movement among Different Agricultural Commodity Markets: A Copula-GARCH Approach. Sustainability 12: 393. [Google Scholar] [CrossRef]

- Zhang, K. S., and Y. Y. Zhao. 2021. Modeling dynamic dependence between crude oil and natural gas return rates: A time-varying geometric copula approach. Journal of Computational and Applied Mathematics 386: 113243. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Rbank 1 | Rfin 2 | Rhealth 3 | Rind 4 | Roil 5 | Rres 6 | Rtelc 7 | Rtop 8 | Rtour 9 | |

|---|---|---|---|---|---|---|---|---|---|

| Mean | 0.034 | 0.031 | 0.054 | 0.050 | 0.056 | 0.025 | 0.04 | 0.042 | 0.041 |

| Std. Dev | 1.731 | 1.356 | 1.328 | 1.207 | 2.342 | 1.861 | 2.051 | 1.331 | 1.206 |

| Kurtosis | 27.156 | 6.309 | 53.051 | 6.096 | 33.303 | 6.282 | 8.358 | 6.34 | 10.09 |

| Skewness | −1.239 | −0.054 | −2.303 | −0.182 | −0.144 | −0.007 | 0.121 | −0.125 | −0.029 |

| Minimum | −30.214 | −9.112 | −28.459 | −8.96 | −37.586 | −11.815 | −15.915 | −8.393 | −10.674 |

| Maximum | 9.181 | 8.098 | 6.281 | 7.173 | 31.078 | 11.45 | 19.65 | 7.707 | 12.291 |

| Jarque-Bera | 9556.512 | 1980.179 | 456,527 | 1755.73 | 79,355.46 | 1946.217 | 5199.083 | 2098.731 | 9086.147 |

| Size | 4337 | 4337 | 4337 | 4337 | 4337 | 4337 | 4337 | 4337 | 4337 |

| Rbank | Rfin | Rhealth | Rind | Roil | Rres | Rtelc | Rtop | Rtour | |

|---|---|---|---|---|---|---|---|---|---|

| Rbank | 1 | ||||||||

| Rfin | 0.806 | 1 | |||||||

| Rhealth | 0.385 | 0.527 | 1 | ||||||

| Rind | 0.435 | 0.552 | 0.442 | 1 | |||||

| Roil | 0.179 | 0.295 | 0.227 | 0.249 | 1 | ||||

| Rres | 0.190 | 0.274 | 0.230 | 0.319 | 0.350 | 1 | |||

| Rtelc | 0.316 | 0.355 | 0.234 | 0.402 | 0.102 | 0.148 | 1 | ||

| Rtop | 0.414 | 0.549 | 0.410 | 0.565 | 0.312 | 0.433 | 0.328 | 1 | |

| Rtour | 0.243 | 0.336 | 0.256 | 0.231 | 0.140 | 0.126 | 0.145 | 0.207 | 1 |

| “Student Distribution” | “Skewed Student Distribution” | |

|---|---|---|

| Mean Equation | ||

| 0.0375 * (0.019) | 0.0422 (0.018) | |

| −0.0273 * (0.230) | −0.2751 * (0.228) | |

| Variance Equation | ||

| w | 0.0615 ** (−0.125) | 0.0617 (0.153) |

| 0.115 * (0.008) | 0.115 * (0.0031) | |

| 0.851 * (0.043) | 0.8504 * (−0.534) | |

| 0.0667 * (0.0119) | 0.0657 * (0.001) | |

| Shape | 5.0036 * (0.273) | 5.0046 * (0.237) |

| Skew | 1.0114 * (0.020) | |

| Log-likelihood | −8598.439 | −8598.275 |

| AIC | 3.9692 | 3.9688 |

| BIC | 3.9825 | 3.9806 |

| “Student Distribution” | “Skewed Student Distribution” | |

|---|---|---|

| Mean Equation | ||

| 0.0096 ** (0.004) | 0.0097 * (0.004) | |

| 0.0270 * (0.012) | 0.0272 * (0.012) | |

| Variance Equation | ||

| w | 0.0057 * (0.002) | 0.0058 * (0.002) |

| 0.0176 * (0.007) | 0.0175 * (0.008) | |

| 0.9930 * (0.000) | 0.9930 * (0.000) | |

| −0..2327 * (0.012) | −0.2326 * (0.010) | |

| Shape | 4.4058 * (0.261) | 4.4096 * (0.278) |

| Skew | 1.0024 * (0.019) | |

| Log-likelihood | −8540.415 | −8540.423 |

| AIC | 3.9507 | 3.9512 |

| BIC | 3.9610 | 3.9630 |

| Oil-Banks | Oil-Financials | Oil-Healthcare | Oil-Industrials | Oil-Resources | Oil-Telecom | Oil-Top40 | Oil-Tourism | |

|---|---|---|---|---|---|---|---|---|

| Constant symmetrized Joe Clayton (SJC) | ||||||||

| 0.157 * (0.022) | 0.223 * (0.023) | 0.132 * (0.023) | 0.327 * (0.020) | 0.575 * (0.018) | 0.159 * (0.022) | 0.234 * (0.017) | 0.023 (0.014) | |

| 0.195 * (0.021) | 0.270 * (0.021) | 0.192 * (0.021) | 0.376 * (0.022) | 0.561 * (0.019) | 0.195 * (0.021) | 0.612 * (0.017) | 0.080 * (0.018) | |

| AIC | −590.43 | −919.55 | −548.15 | −1259.54 | −3409.90 | −495.12 | −3000.43 | −182.79 |

| BIC | −577.68 | −906.80 | −535.41 | −1246.79 | −3397.15 | −482.38 | −2987.68 | −170.04 |

| Likelihood | 297.26 | 461.77 | 276.14 | 631.77 | 1706.96 | 249.56 | 1502.21 | 93.39 |

| Time-varying symmetrized Joe Clayton (SJC) | ||||||||

| 0.156 (0.075) * | 0.159 (0.054) * | 0.114 (0.028) * | 0.238 (0.046) * | 0.171 (0.014) * | 0.127 (0.041) * | 0.174 (0.034) * | 1.521 (0.508) * | |

| −1.120 (0.227) * | −0.678 (0.226) * | −0.794 (0.286) * | −0.474 (0.228) * | −0.678 (0.321) | −0.813 (0.168) * | −0.476 (0.090) * | −1.864 (0.803) * | |

| 0.963 (0.008) * | 0.971 (0.240) * | 0.965 (0.015) * | 0.976 (0.011) * | 0.980 (0.019) * | 0.969 (0.010) * | 0.975 (0.003) * | 0.876 (0.064) * | |

| 0.149 (0.049) * | 0.954 (0.487) | 0.105 (0.063) | 1.362 (0.401) * | 0.723 (0.475) | 0.095 (0.017) * | 0.140 (0.027) * | 1.527 (0.963) | |

| −9.964 (1.675) * | −0.823 (0.443) | −9.258 (3.135) * | −0.604 (0.299) | −0.848 (0.561) * | −6.958 (2.949) | −0.748 (0.363) * | −8.960 (3.522) * | |

| 0.042 (0.016) * | 0.938 (0.211) * | 0.177 (0.259) | 0.970 (0.024) * | 0.975 (0.019) * | 0.172 (0.305) | 0.986 (0.016) * | 0.732 (0.246) * | |

| AIC | −806.30 | −1179.38 | −686.56 | −1512.42 | −5316.18 | −574.85 | −4024.60 | −191.30 |

| BIC | −768.05 | −1141.13 | −648.33 | −1474.17 | −5277.93 | −536.61 | −3983.35 | −153.04 |

| Likelihood | 409.15 | 461.69 | 349.28 | 762.21 | 2664.09 | 293.42 | 2016.80 | 101.65 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Musampa, K.; Eita, J.H.; Meniago, C. The Effects of Oil Price Volatility on South African Stock Market Returns. Economies 2024, 12, 4. https://doi.org/10.3390/economies12010004

Musampa K, Eita JH, Meniago C. The Effects of Oil Price Volatility on South African Stock Market Returns. Economies. 2024; 12(1):4. https://doi.org/10.3390/economies12010004

Chicago/Turabian StyleMusampa, Kongolo, Joel Hinaunye Eita, and Christelle Meniago. 2024. "The Effects of Oil Price Volatility on South African Stock Market Returns" Economies 12, no. 1: 4. https://doi.org/10.3390/economies12010004

APA StyleMusampa, K., Eita, J. H., & Meniago, C. (2024). The Effects of Oil Price Volatility on South African Stock Market Returns. Economies, 12(1), 4. https://doi.org/10.3390/economies12010004