To test the hypothesis that state-owned banks affect fiscal stability, it is advisable to start with the presence, place, and role of state-owned banks in the Ukrainian banking system.

4.1. State-Owned Banks in the Ukrainian Banking System

The Ukrainian banking system is very dynamic in terms of the number of banks, their composition and structure, and their capitalisation, according to the National Bank of Ukraine (

Table 1).

The number of commercial banks in Ukraine is sensitive to the state of Ukrainian and foreign financial markets, as well as the social and political situation in the country. A significant reduction in the number of banks occurred in 2009–2010 when insolvent banks were removed from the banking market and liquidated, which should be considered as a result of the global financial crisis of 2009–2010. The global financial crisis did not affect the number of state-owned banks in Ukraine and their position in the banking system, but state-owned banks in developed economies increased from 6.7 per cent before 2008 to 8 per cent overall (

World Bank 2012).

In 2014, the banking system entered a phase of reducing the number of banks with a simultaneous decrease in the value of assets. This followed the Revolution of Dignity, the annexation of part of Ukraine’s territory, and growing social and political instability in society. In 2014 alone, the banking system shrank by 17 commercial banks, including a 13.4% decrease in the value of assets. During 2015, the negative trend of the banking market exit accelerated, with the liquidation of 46 commercial banks. In the following years, the intensity of commercial banks’ exit from the Ukrainian banking market decreased: in 2016, 21 banks exited, while in 2017, 14 banks exited. In 2018, the number decreased further to 5 banks, and from 2019 to 2021, only 2 banks exited each year. Finally, in 2022, the exit rate remained relatively low, with only 4 banks exiting.

The presence of state-owned banks in the banking system is a characteristic feature of the Ukrainian banking system, with dynamics in terms of the number of banks (the first criterion), capitalisation (the second criterion), and share in the banking system’s capital (the third criterion). At the beginning of the period, there were six state-owned banks: Oschadbank, Ukreximbank, Kyiv Bank, Ukrgasbank, Rodovid Bank, and the Ukrainian Bank for Reconstruction and Development. The share of state-owned banks in the banking system’s capital was about 17–18%, provided that state-owned banks did not violate banking competition and did not restrict individuals and enterprises in choosing banks to receive banking services. In 2013, two state-owned banks were registered (State Land Bank and Settlement Centre), which were subsequently liquidated due to the lack of a developed and implemented business model. In 2014, Kyiv Bank was liquidated by transferring its assets and liabilities to Ukrgasbank. This process can be attributed to the takeover of one state-owned bank by another state-owned bank and the consolidation of state-owned banks’ capital. This is the only example of a takeover of a state-owned bank by another state-owned bank. In 2015, Rodovid Bank, which was previously nationalised as a “bad bank”, “bank of rehabilitation loans”, or “bank of bad loans”, was liquidated. Rodovid Bank did not attract funds from individuals and legal entities, provided a limited number of banking services, and failed to fulfil the main task set by the Government of Ukraine to effectively manage nonperforming loans and rehabilitation loans, and was therefore liquidated.

Structural changes in the banking system of Ukraine occurred in 2016–2017, which led to an increase in the capitalisation of state-owned banks. In December 2016, the Cabinet of Ministers and the National Security and Defence Council of Ukraine nationalised PrivatBank, which significantly changed the banking system of Ukraine. Over 50% of the capital of the banking system was held by four state-owned banks, accompanied by the activities of large banks such as Oschadbank, Ukreximbank, Ukrgasbank, and Privatbank. The nationalisation of Privatbank gave the state a monopoly on the number of bank branches, ATMs, self-service terminals, and electronic plastic cards. Such an advantage for state-owned banks should be seen as a manifestation of the violation of banking competition. Ukrainian scholars call this situation a violation of the requirements of free competition and a market economy (

Bazilyuk et al. 2020).

In 2018, the Ukrainian banking system overcame the banking crisis (

Drobiazko and Lyubich 2019): the capitalisation of the banking system and state-owned banks increased, financial stability and liquidity improved, and the share of nonperforming loans decreased.

The empirical analysis of the activities of state-owned banks is based on the most commonly used indicators in scientific research:

The total net financial result of Ukraine’s state-owned banks shows an overall loss in 2009–2011 due to the inefficient operation of Rodovid Bank and Ukrgasbank. The financial consequences of the global financial crisis in 2008–2009 were overcome by ensuring the profit of state banks in the amount of USD 227 million and by ensuring the profitability of state banks, except Rodovid Bank. The banking crisis caused by the Revolution of Dignity resulted in cumulative losses until 2017. The years 2014–2015 should be considered critical for the banking system as a whole and for state-owned banks. Oschadbank was unprofitable at 7–8 per cent of assets or 41–73 per cent of equity; Ukreximbank was unprofitable at 8–10 per cent of assets or 87–284 per cent of equity; and Ukrgasbank was unprofitable at 12.5 per cent of assets or 71 per cent of equity in 2014. In the following years, the state-owned banks maintained minimal performance. In 2022, the war hurt the banking system, including the activities of state-owned and commercial banks. The net profit of state-owned banks decreased by 60.14%, two state-owned banks became unprofitable (Ukreximbank and Ukrgasbank), and Oschadbank provided an ROA of 0.26% and ROE of 3%.

It is recommended to use the benchmarking technique and compare it with the profitability of the banking system (ROAbs, ROEbs) and the profitability of the Ukrainian commercial banks (ROAcb, ROEcb) when studying the ROA of state-owned banks (ROAsb) and ROE of state-owned banks (ROEsb). According to the National Bank of Ukraine, the ROAbs of Ukraine were (−4.38)% in 2009, (−1.45)% in 2010, (−0.76)% in 2011, 0.45% in 2012, 0.12% in 2013, (−4.07)% in 2014, (−5.46)% in 2015, (−12.60)% in 2016, (−1.93)% in 2017, 1.69% in 2018, 4.26% in 2019, 2.44% in 2020, 4.09% in 2021, and 1.08% in 2022. Thus, after the global financial crisis of 2008, state-owned banks operated with ROAsb lower than ROAcb, indicating that the management of state-owned banks was not efficient enough to overcome the consequences of the crisis, mainly in Ukrgasbank and Rodovid Bank. The insufficient efficiency of state-owned banks’ asset management was also repeated in the postcrisis period, in 2014, 2015, 2016, and 2017 (

Figure 2).

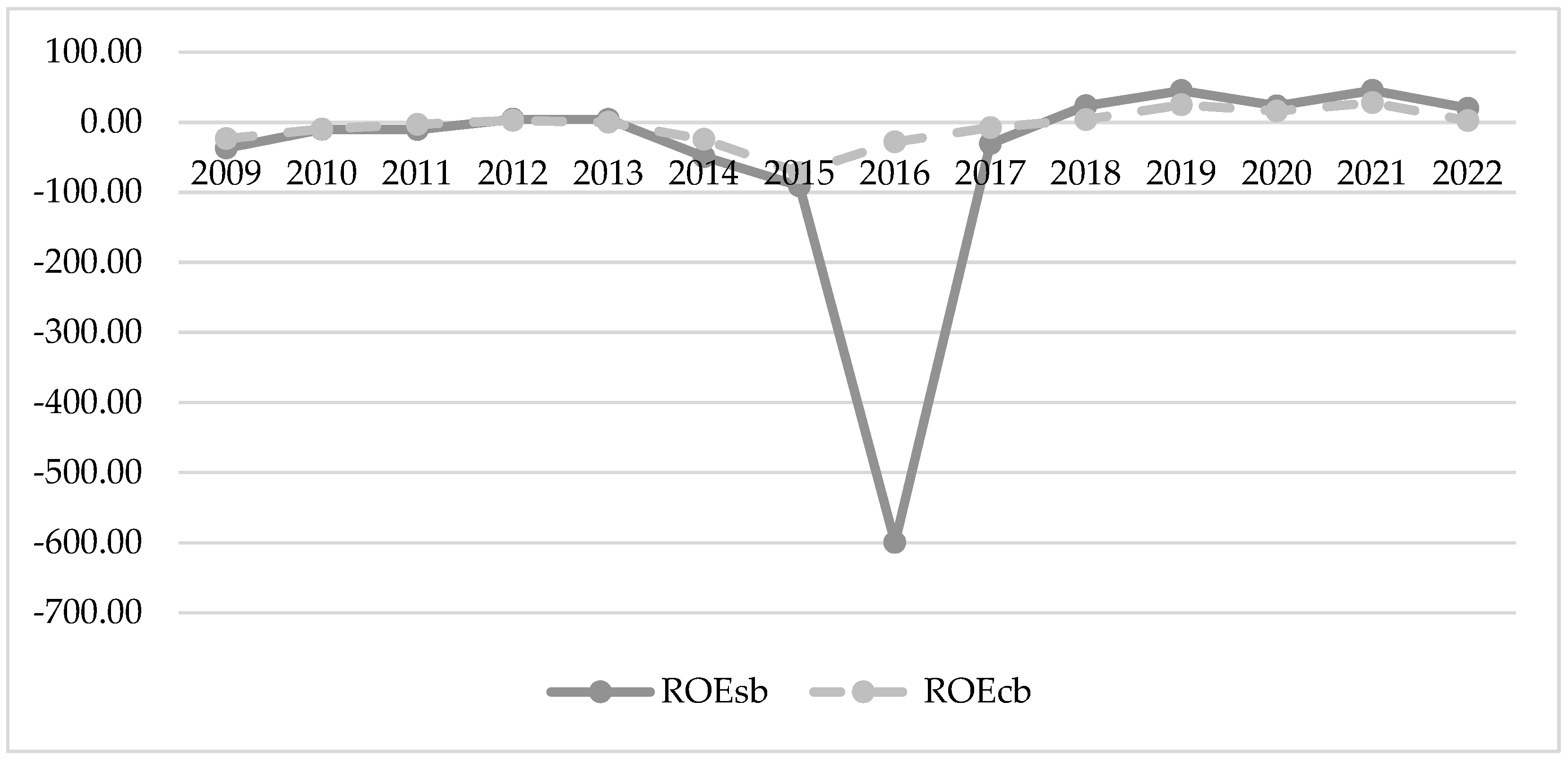

According to the National Bank of Ukraine, the ROEbs of Ukraine were (−32.52)% in 2009, (−10.19)% in 2010, (−5.27)% in 2011, 3.03% in 2012, 0.81% in 2013, (−30.46)% in 2014, (−51.91)% in 2015, (−116.74)% in 2016, (−15.84)% in 2017, 14.67% in 2018, 33.45% in 2019, 19.22% in 2020, 35.08% in 2021, and 10.06% in 2022. Thus, in the first year after the global financial crisis, the state-owned banks operated with an unprofitability (ROEsb) that was higher than the ROEcb; in 2009–2011, the lack of efficiency in the management of the state-owned banks prevailed. The lack of efficiency in the asset management of state-owned banks was also repeated in 2014, 2015, 2016, and 2017 in the postcrisis period, which completely repeats the dynamics of ROAsb (

Figure 3).

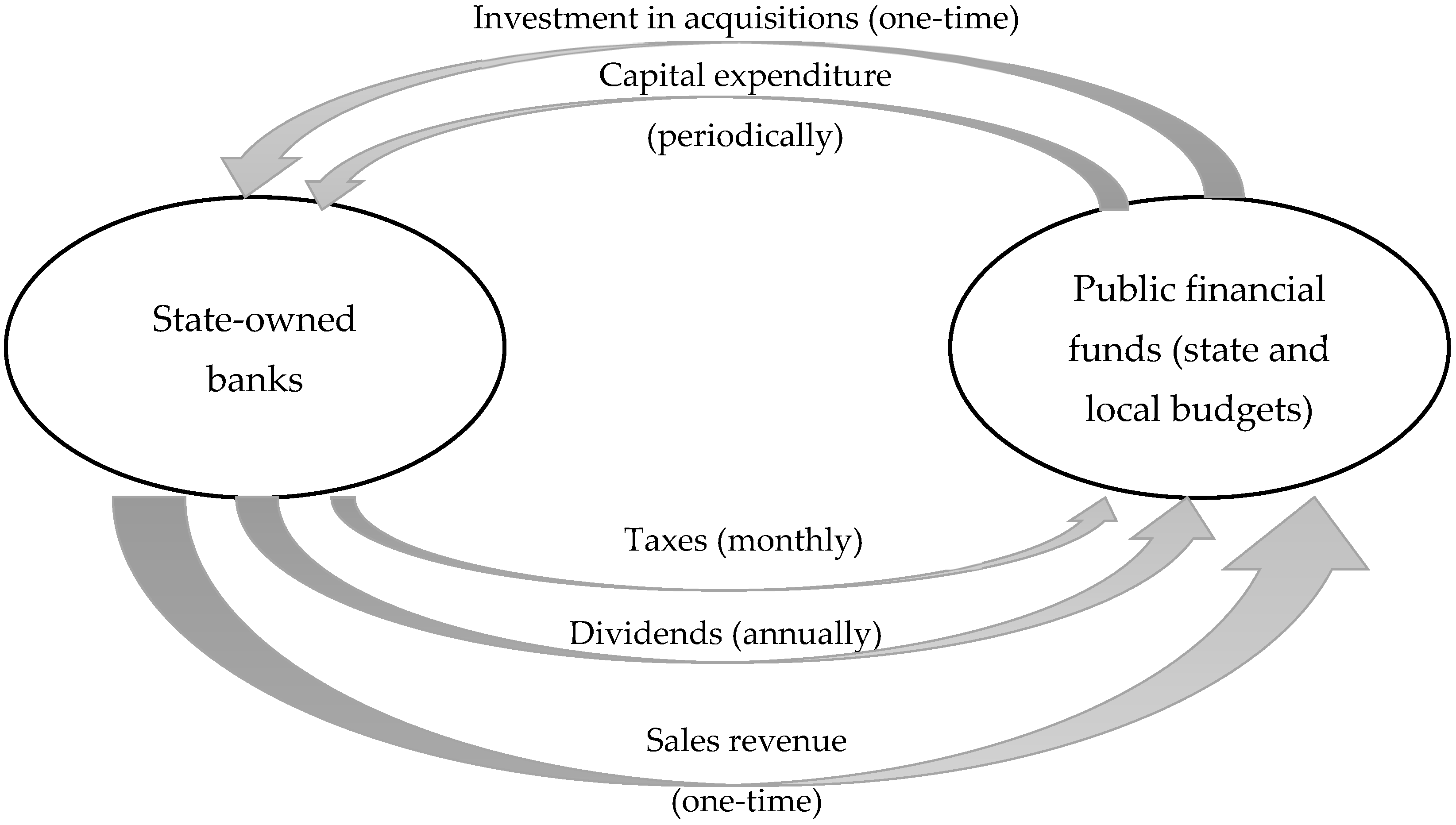

The activities of state-owned banks are coordinated and regulated by the Cabinet of Ministers of Ukraine, the Ministry of Finance of Ukraine, and the National Bank of Ukraine. State-owned banks are financed by the Cabinet of Ministers of Ukraine from public financial resources (the state budget and state loans). The financial performance of state-owned banks is not closely related to the financial performance of the Ukrainian banking system. We have observed insufficient ROEsb and ROAsb in crisis and postcrisis periods, while in periods of economic growth and macroeconomic stability state-owned banks show high ROEsb and ROAsb.

4.2. Cash Flows between State-Owned Banks and Public Funds: Analytical Aspect

We have defined the following indicators: expenditure of public funds on share capital, expenditure of public funds on other equity instruments, dividends of state-owned banks paid to the state budget, income from the sale of state-owned banks, and corporate income tax.

State budget expenditures on the capitalisation of state-owned banks are one of the items of state budget expenditures that should be classified as recurrent expenditures.

Table 5 shows that the largest amount of money was spent in 2009 to deal with the consequences of the 2008 global financial crisis and to maintain the stability of the banking system by preventing the failure of large banks, including state-owned banks. In 2009, the authorised capital of Ukreximbank, Kyiv Bank, Ukrgasbank, and Rodovid Bank was increased to prevent bankruptcy, but Kyiv Bank and Rodovid Bank were liquidated in 2014–2015, so the cost of their capitalisation should be considered an example of inefficient use of public funds. In 2011, the troubled Rodovid Bank was recapitalised for the second time, and the total capitalisation costs of these banks amounted to USD 2004 million, which had a negative impact on public finances due to the possibility of financing other expenditures that could have been social or infrastructure-related.

In the years after 2009, the capitalisation expenditures of state-owned banks were determined not by the dynamics of macroeconomic indicators and the banking system, but by the financial needs of individual state-owned banks, mainly to ensure liquidity and financial stability due to inefficient active operations of state-owned banks.

Oschadbank: The total cost of capitalisation of Oschadbank was USD 2318 million, part of which was achieved without cash flows (through capitalisation of retained net profit and an increase in the nominal value of shares). The remaining part of the capitalisation was financed by government bonds, domestic government loan bonds (“DGLBs”): 2013—UAH 1400 million with an interest rate of 9.50%; 2014—UAH 11,598 million with an interest rate of 7.05%; 2016—UAH 4956 million with an interest rate of 6%; 2017—UAH 8867 million with an interest rate of 6%. The majority of DGLBs are issued with a tenor of 10 years, so Oschadbank’s target return on equity should be at least 6%.

Comparing the return on DGLBs with ROE shows that the two rates diverge. Due to raising Oschadbank’s equity at 9.5% in 2013, the bank had an ROE of no more than 3.6% in the long term. In 2014–2015, Oschadbank’s equity was raised at 7.05%, with a loss-making rate. In 2019 and 2021–2022, the ROE level did not provide sufficient profitability to cover the interest payments on the DGLB. This is the first sign of an inefficient and risky use of public funds.

Ukreximbank: The total capitalisation costs for Ukreximbank amounted to USD 3047 million. In 2009, the Ministry of Finance of Ukraine issued a UAH 1 million DGLB with a maturity of nine years and a yield of 9.5% p.a., initiated by the Ministry of Housing and Communal Services to finance electric vehicle leasing programmes and energy saving and modernisation projects in the municipal heating sector. In this case, public funds were used to invest in a state-owned bank, but the ROE after the capital increase did not exceed one per cent until 2011, did not exceed two per cent in 2012–2013, and was negative in 2015–2016. In 2010, the share capital was increased to guarantee the fulfilment of foreign economic contracts by Ukrainian defence companies through the issue of DGLBs. In 2014, the bank capitalised by issuing UAH 5000 million of DGLBs with a 10-year maturity and an interest rate of 9.5%. In 2016, the bank’s share capital was increased by an additional UAH 9319 million through the issue of DGLBs with a maturity of 10 years and an interest rate of 6%, provided that ROEs in the previous years and the year of the loan were (−86.51)%, (−285.90)%, and (−29.36)%. In 2016–2017, the share capital was replenished at the expense of DGLBs at an interest rate of 6.00–6.86%. In 2020, equity capital was raised through the issue of UAH 6800 million of DGLBs with a maturity of 15 years and an interest rate of 9.3%.

Accordingly, due to the loss-making years 2014, 2015, 2016, 2020, and 2022, there are no financial grounds and prospects for repayment of the DGLB or payment of interest on the use of borrowed funds based on the results of Ukreximbank’s operations. The repayment of the DGLB and the interest payments is an additional burden on the state budget and public finances.

Kyiv Bank was recapitalised in 2009 with UAH 3565 million of DGLBs at an interest rate of 9.5%. This interest rate was not achieved in the form of ROE in any year before the bank’s liquidation.

Ukrgasbank: Ukrgasbank’s equity was increased by UAH 3204 million and UAH 633 million through the issuance of domestic government bonds and an interest rate of 9.5% in 2015. In 2015–2019, retained earnings as part of the bank’s net profit were a stable source of equity growth, which is unique to Ukrgasbank and demonstrates its ability to ensure efficient use of invested state capital in the face of uncertainty and financial and economic instability.

Rodovid Bank and the Ukrainian Bank for Reconstruction and Development had a slight increase in share capital at the expense of public funds. In 2016, the Ukrainian Bank for Reconstruction and Development sold the state’s share of its capital for UAH 82.2 million, which did not cover the bank’s capital requirements in 2010 and 2012. This was the second sign of inefficient and risky use of public funds, namely the discrepancy between the market value of the state bank’s stake and previous expenditures.

Privatbank: Privatbank was capitalised following Resolution of the Cabinet of Ministers of Ukraine No. 961 of 18 December 2016, and the Deposit Guarantee Fund was capitalised by Resolution of the Cabinet of Ministers of Ukraine No. 1003 of 28 December 2016. In December 2016, the Cabinet of Ministers of Ukraine decided to issue additional shares of the bank in the total amount of UAH 116,800 million, financed by domestic government bonds at an interest rate of 6.86% per annum. In June 2017, the bank again issued additional shares in the total amount of UAH 38,565 million, financed by Ukrainian government bonds at an interest rate of 9.70% per annum.

The experience of financing the capitalisation needs of state-owned banks is widespread in other countries. In Turkey, the issuance of government bonds and other reforms (reduction in the number of bank branches, labour, and operating costs) led to the profitability of state-owned banks (

Aysan and Ceyhan 2010). In Ukraine, it is not possible to determine the profitability of state-owned banks based on the results of capitalisation using the DGLB.

Dividends and taxes paid go to the state budget and are compensating cash flows that can finance the repayment and funding of the DGLB. The regulatory approach to the capitalisation of state-owned banks should be to ensure that they are self-financing and profitable, unless the state-owned bank performs social and other public functions. The dividend policy of Ukrainian state-owned banks is determined by the Cabinet of Ministers of Ukraine through the legislative definition of the dividend payment rate and is adjusted by the net financial result based on the results of their activities. The Cabinet of Ministers of Ukraine approves the net profit distribution rate on an annual basis. For instance:

2017: Oschadbank—30%, Ukrgasbank, Ukreximbank, Privatbank—75% (basic rate for state-owned companies);

2018: Oschadbank—30%, Ukrgasbank, Ukreximbank, Privatbank—90% (basic rate for state-owned companies);

2019: Oschadbank, Ukreximbank—30%, Ukrgasbank—50% (basic rate for state-owned companies), Privatbank—75%;

2020–2021: Oschadbank—30%, Ukreximbank, Ukrgasbank—50% (basic rate for state-owned companies), Privatbank—80%.

Based on the results of the regulatory requirements for profit and loss set by the Cabinet of Ministers of Ukraine, state-owned banks transferred USD 3218 million to the state budget in 2009–2022 (

Table 6), with the predominance of dividend payments in 2019–2022 (95%) and the predominance of dividend payments from Privatbank (92%).

Corporate income tax paid by state-owned banks is generally accrued and paid at a rate of 18% of pretax financial income. For 2009–2022, USD 898 million was transferred to the state budget (

Table 6), with the predominance of tax payments in 2019–2022 (73%) and the predominance of tax payments from Privatbank (59%).

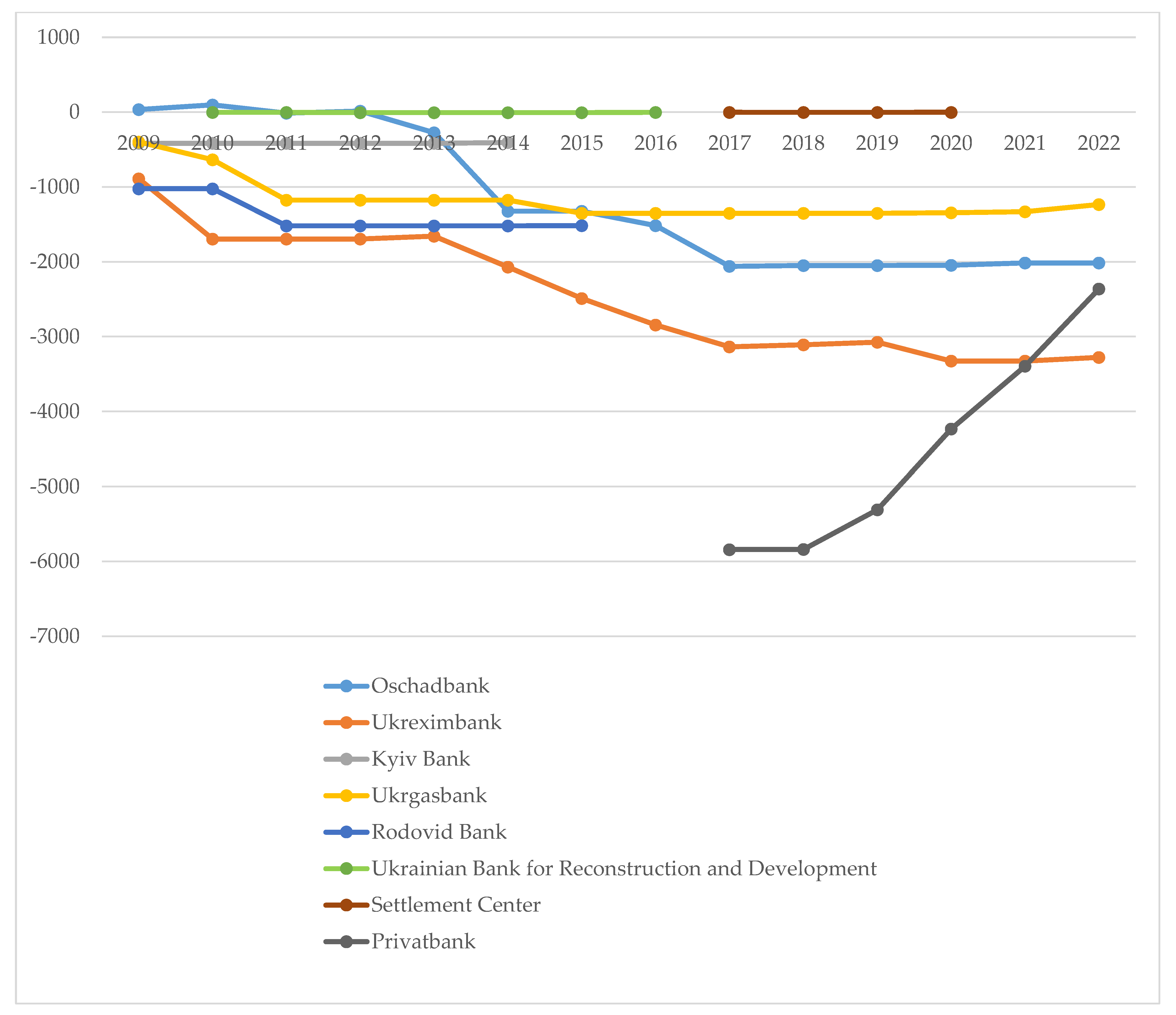

Due to the limited information available on the activities of state-owned banks in Ukraine and the limited information available on the cash flows within the public finances, we used Formula (3). We determined the cumulative cash flows for each state-owned bank as of the beginning of 2023. Oschadbank’s cumulative deficit was USD 2015 million, Ukreximbank’s cumulative deficit was USD 3277 million, Ukrgasbank’s cumulative deficit was USD 1233 million, and Privatbank’s cumulative deficit was USD 2364 million (

Figure 4). The lack of management of state-owned banks was reflected in the cumulative deficits of state-owned banks that were liquidated or privatised in 2014–2017 and have no prospects of repayment in the coming periods. The dynamics of the cumulative deficit can be used to determine the waviness of the cumulative deficit. The historical maximum of the cumulative deficit was reached in 2017, due to the issuance of DGLBs for the nationalisation of Privatbank. In 2018, the fiscal cost compensation stages of USD 38 million, USD 567 million, USD 835 million, USD 877 million, and USD 1176 million started.

Therefore, we calculated the cumulative cash flow deficit of Ukraine’s state-owned banks and public funds based on the excess of the fiscal cost of increasing the share capital of state-owned banks over dividends paid and corporate income tax paid.

4.3. Influence of State-Owned Banks on Public Finance Sustainability

The impact of state-owned banks on the sustainability of public finances is determined by the direction of alternative financing and debt financing of the capital increase of state-owned banks by the DGLB.

Expenditure on the capitalisation of state-owned banks totals USD 13,482 million over the period 2009–2022, which is ten times higher than expenditures on civil defence, military education, communications, telecommunications and information technology, and social protection of the unemployed, and several times higher than expenditures on fire and rescue, justice, national defence, agriculture, construction, environmental protection, and social protection of war and labour veterans. Expenditure on the capitalisation of state-owned banks thus exceeded other public expenditures in nominal terms, leading to structural changes in budget expenditure (

Appendix A).

In 2009–2022, DGLBs were issued for USD 13,868 million (

Figure 5), accounting for 71% of all DGLBs issued in 2009, 21% in 2010, 27% in 2011, 2% in 2013, 8% in 2014, 6% in 2015, 73% in 2016, 68% in 2017, and 3% in 2020. The accumulated public debt from DGLBs is a burden on the consolidated budget of Ukraine due to the additional debt burden, which should be considered high for the budget.

We prove the existence of a very strong inverse relationship between the amount of public debt and structural changes on the expenditure side of the budget based on an empirical analysis of the total amount of public debt, the state budget of Ukraine’s expenditures on public debt service, and the structure and structural changes on the expenditure side in the long term, using the methods of economic and statistical analysis. Thus, each additional UAH 1 billion borrowed resulted in structural changes on the expenditure side of the state budget of 0.01% in the direction of reducing expenditures on economic activity, education, healthcare, and mental and physical development (

Boiko et al. 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}