Threshold of the CAPB That Can Be Attributed to Fiscal Consolidation Episodes in South Africa

Abstract

1. Introduction

- Null:

- There is a threshold of the cyclical adjusted primary balance that can be attributed to the fiscal consolidation episode.

- Alt:

- There is no threshold of the cyclical adjusted primary balance that can be attributed to the fiscal consolidation episode.

- Null:

- There is fiscal consolidation though government expenditure cuts and tax increases that impact government debt.

- Alt:

- There is no fiscal consolidation though government expenditure cuts and tax increases that impact government debt.

- Null:

- There is fiscal consolidation that reflects success in reducing government debt.

- Alt:

- There is no fiscal consolidation that reflects success in reducing government debt.

2. Literature Review

2.1. Measures of Fiscal Consolidation

2.2. Threshold of Fiscal Consolidation

3. Methodology

3.1. The Theoretical Framework of Fiscal Deficit

3.2. Model Specification

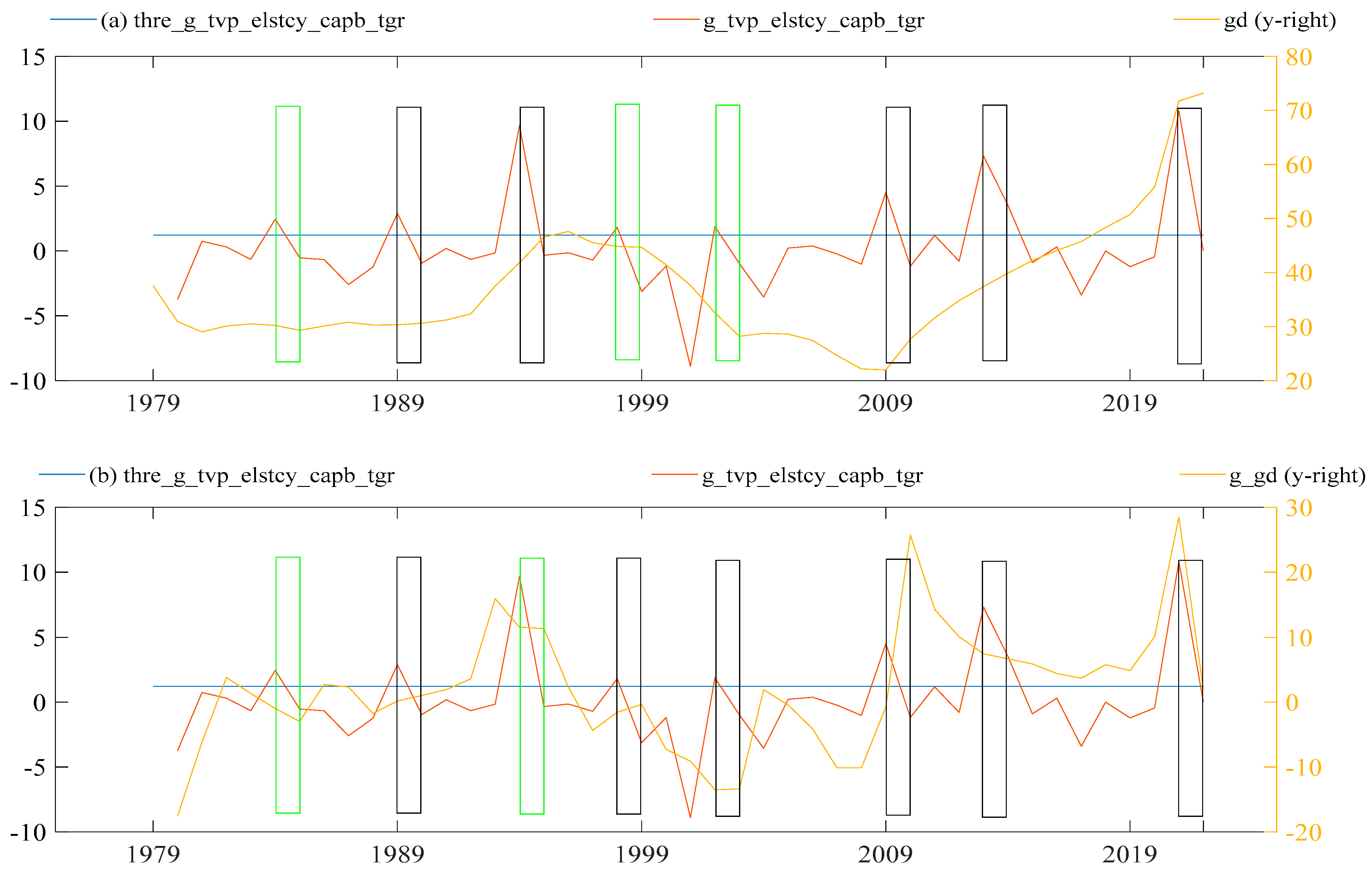

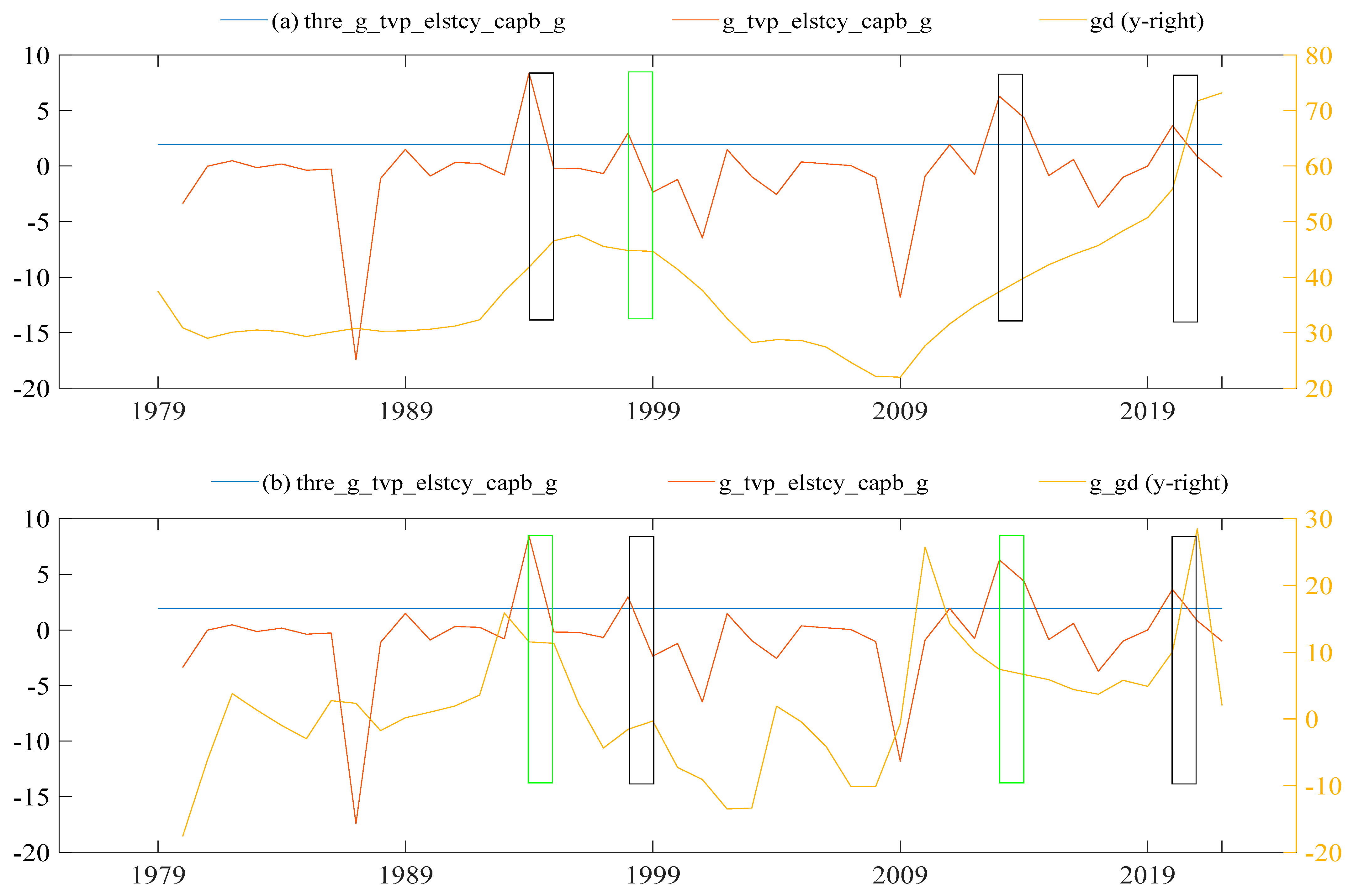

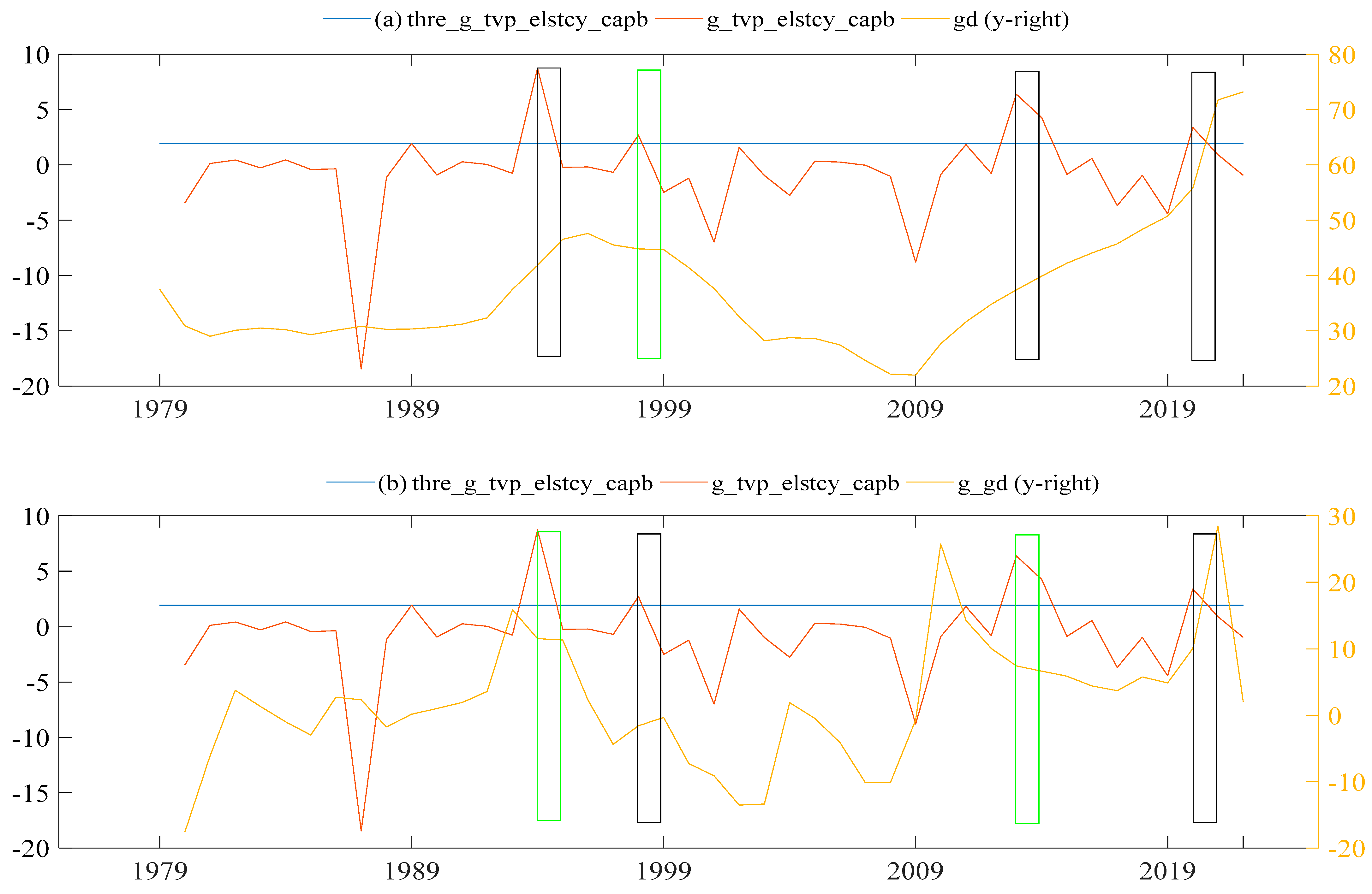

4. Results

5. Discussion and Recommendation

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | (Blanchard 1990). Defined fiscal consolidation as large observed improvements in the cyclically adjusted primary balance (CAPB). CAPB is intended to capture discretionary fiscal policy by excluding the estimated effects of business cycle fluctuations on the government budget. Therefore, taxes and transfers are cyclically adjusted with net interest payments also to be subtracted. CAPB is a discretionary measure of fiscal policy as it excludes interest payments from past government liabilities on the accumulated debt. |

| 2 | The paper uses the HM filter to find the growth of nominal potential GDP. |

References

- Afonso, António, Christiane Nickel, and Philipp C. Rother. 2006. Fiscal consolidations in the Central and Eastern European countries. Review of World Economics 142: 402–21. [Google Scholar] [CrossRef]

- Afonso, António. 2010. Expansionary fiscal consolidations in Europe: New evidence. Applied Economics Letters 17: 105–9. [Google Scholar] [CrossRef]

- Afonso, António, and João Tovar Jalles. 2013. Growth and productivity: The role of government debt. International Review of Economics & Finance 25: 384–407. [Google Scholar]

- Afonso, António, and Frederico Silva Leal. 2019. Fiscal Episodes in the EMU: Elasticities and Non-Keynesian Effects. REM Working Paper 097-2019. Lisbon: Universidade de Lisboa. [Google Scholar]

- Afonso, António, José Alves, and João Tovar Jalles. 2022a. The (non-)Keynesian effects of fiscal austerity: New evidence from a large sample. Economic Systems 46: 100981. [Google Scholar] [CrossRef]

- Afonso, António, José Alves, and João Tovar Jalles. 2022b. To consolidate or not to consolidate? A multi-step analysis to assess needed fiscal sustainability. International Economics 72: 106–23. [Google Scholar] [CrossRef]

- Afonso, António, and Frederico Silva Leal. 2022. Fiscal episodes in the Economic and Monetary Union: Elasticities and non-Keynesian effects. International Journal of Finance & Economics 27: 571–93. [Google Scholar]

- Agnello, Luca, and Ricardo M. Sousa. 2014. How does fiscal consolidation impact on income inequality? Review of Income and Wealth 60: 702–26. [Google Scholar]

- Agnello, Luca, Vítor Castro, and Ricardo M. Sousa. 2019. A competing risks tale on successful and unsuccessful fiscal consolidations. Journal of International Financial Markets, Institutions and Money 63: 101148. [Google Scholar] [CrossRef]

- Aizenman, Joshua, Sebastian Edwards, and Daniel Riera-Crichton. 2012. Adjustment patterns to commodity terms of trade shocks: The role of exchange rate and international reserves policies. Journal of International Money and Finance 31: 1990–2016. [Google Scholar] [CrossRef]

- Alesina, Alberto, and Roberto Perotti. 1995. Fiscal expansions and adjustments in OECD countries. Economic Policy 10: 205–48. [Google Scholar] [CrossRef]

- Alesina, Alberto, and Roberto Perotti. 1997. Fiscal adjustments in OECD countries: Composition and macroeconomic effects. Staff Papers 44: 210–48. [Google Scholar] [CrossRef]

- Alesina, Alberto, Roberto Perotti, José Tavares, Maurice Obstfeld, and Barry Eichengreen. 1998. The political economy of fiscal adjustments. Brookings Papers on Economic Activity 1998: 197–266. [Google Scholar] [CrossRef]

- Alesina, Alberto, and Silvia Ardagna. 2010. Large changes in fiscal policy: Taxes versus spending. Tax Policy and the Economy 24: 35–68. [Google Scholar] [CrossRef]

- Alesina, Alberto, and Silvia Ardagna. 2013. The design of fiscal adjustments. Tax Policy and the Economy 27: 19–68. [Google Scholar] [CrossRef]

- Alesina, Alberto, Carlo Favero, and Francesco Giavazzi. 2019. Effects of austerity: Expenditure-and tax-based approaches. Journal of Economic Perspectives 33: 141–62. [Google Scholar] [CrossRef]

- Amo-Yartey, Charles, Machiko Narita, Garth Peron Nicholls, Joel Chiedu Okwuokei, Alexandra Peter, and Therese Turner-Jones. 2012. The Challenges of Fiscal Consolidation and Debt Reduction in the Caribbean. WP/12/276. Washington, DC: International Monetary Fund. [Google Scholar]

- Ardagna, Silvia, Francesco Caselli, and Timothy Lane. 2007. Fiscal discipline and the cost of public debt service: Some estimates for OECD countries. The BE Journal of Macroeconomics 7: 45–67. [Google Scholar] [CrossRef]

- Ardanaz, Martín, Mark Hallerberg, and Carlos Scartascini. 2020. Fiscal Consolidations and electoral outcomes in emerging economies: Does the policy mix matter? Macro and micro level evidence from Latin America. European Journal of Political Economy 64: 101918. [Google Scholar] [CrossRef]

- Arestis, Philip, Ayşe Kaya, and Hüseyin Şen. 2018. Does fiscal consolidation promote economic growth and employment? Evidence from the PIIGGS countries. European Journal of Economics and Economic Policies: Intervention 15: 289–312. [Google Scholar]

- Aye, Goodness C. 2019. Fiscal Policy Uncertainty and Economic Activity in South Africa: An Asymmetric Analysis. Macroeconomic Discussion Paper Series 2; Pretoria: Department of Economics, University of Pretoria. [Google Scholar]

- Bamba, Moulaye, Jean-Louis Combes, and Alexandru Minea. 2020. The effects of fiscal consolidations on the composition of government spending. Applied Economics 52: 1517–32. [Google Scholar] [CrossRef]

- Barrios, Salvador, Sven Langedijk, and Lucio R. Pench. 2010. EU Fiscal Consolidation after the Financial Crisis Lessons from Past Experiences. Bank of Italy Occasional Paper. Brussels: European Commission. [Google Scholar]

- Baum, Christopher F., and Jesús Otero. 2021. Unit-root tests for explosive behavior. The Stata Journal 21: 999–1020. [Google Scholar] [CrossRef]

- Bergman, U Michael, and Michael M. Hutchison. 2010. Expansionary fiscal contractions: Re-evaluating the Danish case. International Economic Journal 24: 71–93. [Google Scholar] [CrossRef]

- Blanchard, Olivier Jean. 1990. Suggestions for a New Set of Fiscal Indicators. Organisation for Economic Co-operation and Development (OECD) (No. 79). Available online: https://www.oecd-ilibrary.org/content/paper/435618162862 (accessed on 11 March 2022).

- Braz, Cláudia, Maria Manuel Campos, and Sharmin Sazedj. 2019. The new ESCB methodology for the calculation of cyclically adjusted budget balances: An application to the Portuguese case. Banco de Portugal Economic Studies 2: 19–42. [Google Scholar]

- Buthelezi, Eugene Msizi. 2023a. Dynamics of Macroeconomic Uncertainty on Economic Growth in the Presence of Fiscal Consolidation in South Africa from 1994 to 2022. Economies 11: 119. [Google Scholar] [CrossRef]

- Buthelezi, Eugene Msizi. 2023b. Impact of government expenditure on economic growth in different states in South Africa. Cogent Economics & Finance 11: 2209959. [Google Scholar]

- Buthelezi, Eugene Msizi, and Phocenah Nyatanga. 2023. Time-Varying Elasticity of Cyclically Adjusted Primary Balance and Effect of Fiscal Consolidation on Domestic Government Debt in South Africa. Economies 11: 141. [Google Scholar] [CrossRef]

- Buthelezi, Eugene M., and Phocenah Nyatanga. 2018. Government Debt and Economic Growth: Evidence from ECOWAS and SADC. African Journal of Business & Economic Research 13: 1–25. [Google Scholar]

- Carnazza, Giovanni, Paolo Liberati, and Agnese Sacchi. 2020. The cyclically-adjusted primary balance: A novel approach for the euro area. Journal of Policy Modeling 42: 1123–45. [Google Scholar] [CrossRef]

- Chakrabarti, Shouvanik, Rajiv Krishnakumar, Guglielmo Mazzola, Nikitas Stamatopoulos, Stefan Woerner, and William J. Zeng. 2021. A threshold for quantum advantage in derivative pricing. Quantum 5: 463. [Google Scholar] [CrossRef]

- Chen, Haiqiang, Terence Tai-Leung Chong, and Jushan Bai. 2012. Theory and applications of the TAR model with two threshold variables. Econometric Reviews 31: 142–70. [Google Scholar] [CrossRef]

- David, Antonio C., Jaime Guajardo, and Juan F. Yepez. 2022. The rewards of fiscal consolidations: Sovereign spreads and confidence effects. Journal of International Money and Finance 123: 102602. [Google Scholar] [CrossRef]

- David, Antonio, and Daniel Leigh. 2018. A New Action-based Dataset of Fiscal Consolidation in Latin America and the Caribbean. Washington, DC: International Monetary Fund. [Google Scholar]

- de Rugy, Veronique, and Jack Salmon. 2020. Flattening the Debt Curve: Empirical Lessons for Fiscal Consolidation. Mercatus Special Study. [Google Scholar] [CrossRef]

- Deskar-Škrbić, Milan, and Darjan Milutinović. 2021. Design of fiscal consolidation packages and model-based fiscal multipliers in Croatia. Public Sector Economics 45: 1–61. [Google Scholar] [CrossRef]

- Devries, Pete, Jaime Guajardo, Daniel Leigh, and Andrea Pescatori. 2011. A New Action-Based Dataset of Fiscal Consolidation. IMF Working Paper 1–91. Washington, DC: International Monetary Fund. [Google Scholar]

- Duperrut, Jerome. 1998. “Successful Fiscal Adjustments”: Empirical Evidence from South Africa. Master’s thesis, University of Cape Town, Cape Town, South Africa. [Google Scholar]

- FRB. 2018. FISCAL RESPONSIBILITY BILL. Edited by The National Treasury Republic of South Africa. Pretoria: Communications Directorate, National Treasury. [Google Scholar]

- Georgantas, Georgios, Maria Kasselaki, and Athanasios Tagkalakis. 2023. The effects of fiscal consolidation in OECD countries. Economic Modelling 118: 106099. [Google Scholar] [CrossRef]

- Giavazzi, Francesco, and Marco Pagano. 1995. Non-Keynesian Effects of Fiscal Policy Changes: International Evidence and the Swedish Experience. Macroeconomics Annual NBER Working Paper w5332. Cambridge: National Bureau of Economic Research (NBER). [Google Scholar]

- Giesenow, Federico M., Juliette de Wit, and Jakob de Haan. 2020. The political and institutional determinants of fiscal adjustments and expansions: Evidence for a large set of countries. European Journal of Political Economy 64: 101911. [Google Scholar] [CrossRef]

- Giudice, Gabriele, and Alessandro Turrini. 2007. Non-Keynesian fiscal adjustments? A close look at expansionary fiscal consolidations in the EU. Open Economies Review 18: 613–30. [Google Scholar] [CrossRef]

- Glavaški, Olgica, and Emilija Beker-Pucar. 2020. Fiscal consolidation in the EU-28: Multiyear versus cold-shower episodes. Ekonomski Horizonti 22: 17–30. [Google Scholar] [CrossRef]

- Gootjes, Bram, and Jakob de Haan. 2022. Do fiscal rules need budget transparency to be effective? European Journal of Political Economy 75: 102210. [Google Scholar] [CrossRef]

- Guajardo, Jaime, Daniel Leigh, and Andrea Pescatori. 2014. Expansionary austerity? International evidence. Journal of the European Economic Association 12: 949–68. [Google Scholar] [CrossRef]

- Gupta, Sanjeev, Benedict Clements, Emanuele Baldacci, and Carlos Mulas-Granados. 2005. Fiscal policy, expenditure composition, and growth in low-income countries. Journal of International Money and Finance 24: 441–63. [Google Scholar] [CrossRef]

- Hansen, Bruce E. 2000. Sample splitting and threshold estimation. Econometrica 68: 575–603. [Google Scholar] [CrossRef]

- Hernández De Cos, Pablo, and Enrique Moral-Benito. 2013. Fiscal consolidations and economic growth. Fiscal Studies 34: 491–515. [Google Scholar] [CrossRef]

- Heylen, Freddy, and Gerdie Everaert. 2000. Success and failure of fiscal consolidation in the OECD: A multivariate analysis. Public Choice 105: 103–24. [Google Scholar] [CrossRef]

- Heylen, Freddy, Annelies Hoebeeck, and Tim Buyse. 2013. Government efficiency, institutions, and the effects of fiscal consolidation on public debt. European Journal of Political Economy 31: 40–59. [Google Scholar] [CrossRef]

- IMF. 2020. Cyclically Adjusted Balance. Available online: https://www.imf.org/external/datamapper/GGCB_G01_PGDP_PT@FM/ADVEC/FM_EMG/ (accessed on 11 August 2022).

- Iqbal, Nasir, Musleh ud Din, and Ejaz Ghani. 2017. The fiscal deficit and economic growth in Pakistan: New evidence. The Lahore Journal of Economics 22: 53–72. [Google Scholar] [CrossRef]

- Kalbhenn, Anna, and Livio Stracca. 2020. Mad about austerity? The effect of fiscal consolidation on public opinion. Journal of Money, Credit and Banking 52: 531–48. [Google Scholar] [CrossRef]

- Keynes, John Maynard. 1937. The general theory of employment. The Quarterly Journal of Economics 51: 209–23. [Google Scholar] [CrossRef]

- Kopecky, Joseph. 2022. The age for austerity? Population age structure and fiscal consolidation multipliers. Journal of Macroeconomics 73: 103444. [Google Scholar] [CrossRef]

- Lahiani, Amine, Ameni Mtibaa, and Foued Gabsi. 2022. Fiscal consolidation, social sector expenditures and twin deficit hypothesis: Evidence from emerging and middle-income countries. Comparative Economic Studies 64: 710–47. [Google Scholar] [CrossRef]

- Mankiw, N. Gregory. 2019. Brief Principles of Macroeconomics. Boston: Cengage Learning. [Google Scholar]

- Mankiw, N. Gregory. 2020. Principles of Economics. Boston: Cengage Learning. [Google Scholar]

- McDermott, C. John, and Robert F. Wescott. 1996. An empirical analysis of fiscal adjustments. Staff Papers 43: 725–53. [Google Scholar] [CrossRef]

- Morris, Richard, and Ludger Schuknecht. 2007. Structural Balances and Revenue Windfalls: The Role of Asset Prices Revisited. ECB Working Paper, No. 737. Frankfurt: European Central Bank. [Google Scholar]

- Mourre, Gilles, George-Marian Isbasoiu, Dario Paternoster, and Matteo Salto. 2013. The Cyclically-Adjusted Budget Balance Used in the EU Fiscal Framework: An Update. Citeseer: Pennsylvania State University. Available online: http://gesd.free.fr/ecp478.pdf (accessed on 5 March 2022).

- MTBPS. 2014. Medium Term Budget Policy Statement 2014. Edited by The National Treasury Republic of South Africa. Pretoria: Communications Directorate, National Treasury. [Google Scholar]

- National Treasury Republic of South Africa, ed. 2012. Budget Review. Pretoria: Communications Directorate, National Treasury. [Google Scholar]

- National Treasury Republic of South Africa, ed. 2013. Budget Review. Pretoria: Communications Directorate, National Treasury. [Google Scholar]

- National Treasury Republic of South Africa, ed. 2014. Budget Review. Pretoria: Communications Directorate, National Treasury. [Google Scholar]

- Nunes, Bruno Daniel Gonçalves. 2019. Does the Level of Public Spending Influence the Success of Fiscal Consolidations? Brussels: União Europeia, pp. 1–48. [Google Scholar]

- Perotti, Roberto. 2012. The “austerity myth”: Gain without pain? In Fiscal Policy after the Financial Crisis. Chicago: University of Chicago Press, pp. 307–54. [Google Scholar]

- Purfield, Catriona. 2003. Fiscal Adjustment in Transition: Evidence from the 1990s. Emerging Markets Finance and Trade 39: 43–62. [Google Scholar] [CrossRef]

- Quaresma, Gonçalo Dias. 2021. Monetary Policy Easing and Non-Keynesian Effects of Fiscal Policy. Lisboa: Universidade de Lisboa (Portugal). [Google Scholar]

- Ramos-Herrera, María del Carmen, and Simón Sosvilla-Rivero. 2020. Fiscal Sustainability in Aging Societies: Evidence from Euro Area Countries. Sustainability 12: 10276. [Google Scholar] [CrossRef]

- Romer, Christina D., and David H. Romer. 2010. The macroeconomic effects of tax changes: Estimates based on a new measure of fiscal shocks. American Economic Review 100: 763–801. [Google Scholar] [CrossRef]

- SADC. 2006. Protocol on Finance and Investment. Edited by Finance. Maseru: SADC. [Google Scholar]

- SARB. 2022. Online Statistical Query (Historical Macroeconomic Timeseries Information). Available online: https://www.resbank.co.za/Research/Statistics/Pages/OnlineDownloadFacility.aspx (accessed on 11 March 2022).

- Schaltegger, Christoph A., and Martin Weder. 2014. Austerity, inequality and politics. European Journal of Political Economy 35: 1–22. [Google Scholar] [CrossRef]

- Tagkalakis, Athanasios. 2011. Fiscal adjustments and asset price changes. Journal of Macroeconomics 33: 206–23. [Google Scholar] [CrossRef]

- Tavares, José. 2004. Does right or left matter? Cabinets, credibility and fiscal adjustments. Journal of Public Economics 88: 2447–68. [Google Scholar] [CrossRef]

- Wiese, Rasmus, Richard Jong-A-Pin, and Jacob de Haan. 2018. Can successful fiscal adjustments only be achieved by spending cuts? European Journal of Political Economy 54: 145–66. [Google Scholar] [CrossRef]

- Xiang, Lanxin, Yongyi Fang, Keling Zhou, and Sijia Fan. 2021. The Impact of Fiscal Consolidation Episodes on Total Factor Productivity: Evidence from LAC Countries. Paper presented at the 2021 5th International Conference on E-Business and Internet, Singapore, October 15–17. [Google Scholar]

- Yang, Weonho, Jan Fidrmuc, and Sugata Ghosh. 2015. Macroeconomic effects of fiscal adjustment: A tale of two approaches. Journal of International Money and Finance 57: 31–60. [Google Scholar] [CrossRef]

- Zaghini, Andrea. 2001. Fiscal adjustments and economic performing: A comparative study. Applied Economics 33: 613–24. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Economic Variables | Description of the Definition of Fiscal Consolidation Using Economic Variables |

|---|---|

| Government debts share to gross domestic product | A 4.5% decrease in government debt share to the gross domestic product in and (Alesina and Ardagna 2010). Mean less than 5% from the initial government debt share to GDP for 3 successive years (Alesina and Perotti 1995; Alesina and Ardagna 2010). |

| Government deficit | A fall of 2% below the initial rate for government deficit in and (Alesina and Perotti 1995; Alesina and Ardagna 2010). |

| Economic Growth | Economic growth is higher for 2 successful years for the growth rate means of cases where there was a fiscal consolidation (Alesina et al. 1998). The average economic growth rate at, is higher than, and (Giudice and Turrini 2007). |

| The cyclically adjusted primary balance | If there is a 1% change in the cyclically adjusted primary balance in 3 years (Tavares 2004). The cyclically adjusted primary balance improve by 1.5% in (Alesina and Perotti 1997; Alesina et al. 1998; Alesina and Ardagna 2010; Gupta et al. 2005; Hernández De Cos and Moral-Benito 2013; Schaltegger and Weder 2014). The cyclically adjusted primary balance improve by 1.5% in and (Alesina et al. 1998). The cyclically adjusted primary balance increased by 2% in (Alesina et al. 1998). The cyclically adjusted primary balance improves by mean plus standard deviation in (Yang et al. 2015). The cyclically adjusted primary balance increase by the mean, , plus standard deviation, , in (Yang et al. 2015). |

| Author | Definition | EB | TB | TE | TS | % S |

|---|---|---|---|---|---|---|

| Alesina and Perotti (1995) | Threshold of 1.5% CAPB | 59 | 60 | 119 | 66 | 55.46% |

| Alesina and Perotti (1997) | Changes in the CAPB that are at least 5% | 125 | 98 | 223 | 43 | 19.28% |

| McDermott and Wescott (1996) | Threshold of 1.5% CAPB | 34 | 74 | 108 | 43 | 39.81% |

| Alesina et al. (1998) | Threshold of 2% CAPB | 23 | 28 | 51 | 19 | 37.25% |

| Zaghini (2001) | Threshold of 1.6% or 1.4% of CAPB | 52 | 48 | 100 | 52 | 52.00% |

| Afonso et al. (2006) | Threshold of 2% CAPB | 72 | 20 | 27.78% | ||

| Alesina and Ardagna (2010) | Threshold of 1.5% CAPB | 107 | 91 | 85.05% | ||

| Barrios et al. (2010) | Threshold of 1.5% CAPB | 235 | 71 | 30.21% | ||

| Amo-Yartey et al. (2012) | 1% improvement in CAPB | 107 | 51 | 47.66% | ||

| Alesina and Ardagna (2013) | Debt to GDP ratio falls 2 years | 17 | 35 | 107 | 25 | 23.36% |

| Yang et al. (2015) | Narrative approach | 66 | 19 | 28.79% | ||

| de Rugy and Salmon (2020) | Debt-to GDP ratio declines by at least 5 percentage points | 45 | 67 | 112 | 66 | 58.93% |

| Ardanaz et al. (2020) | Narrative approach and threshold of 1.5% CAPB | 41% | 42% | 56.6% | ||

| Nunes (2019) | Threshold of 1.5% CAPB | 113 | 63 | 55% | ||

| Afonso and Silva Leal (2019) | Threshold of 1.5% CAPB | 51 | 18.61% | |||

| Quaresma (2021) | Threshold of 1.5% CAPB and the narrative approach | 76 | 60 | 136 | 36 | 26.47% |

| Wiese et al. (2018) | Threshold of 1.5% CAPB and the narrative approach | 42 | 58 | 110 | 50 | 45.45% |

| Nunes (2019) | Threshold of 1.5% | 61 | 52 | 113 | 25 | 22.12% |

| Agnello et al. (2019) | Threshold of 1.5% CAPB and the narrative approach | 51 | 15 | 29.41% | ||

| Afonso and Silva Leal (2022) | Threshold of 1.5% CAPB and the narrative approach | 81 | 98 | 179 | 45 | 25.13% |

| Variable | Obs | Mean | Std. Dev. | Min | Max | Skewness | Kurtosis | Shapiro–Wilk |

|---|---|---|---|---|---|---|---|---|

| 44 | 37.2268 | 11.2063 | 21.99 | 73.18 | 0.000 | 0.69 | 0.548 | |

| 43 | 0.01971 | 0.09279 | −0.176 | 0.28484 | 0.032 | 0.40 | 0.895 | |

| 44 | 27.9489 | 3.00313 | 23.3 | 37.5 | 0.000 | 0.08 | 0.901 | |

| 44 | 14.32779 | 8.754365 | −5.2537 | 36.8419 | 0.024 | 0.20 | 0.533 | |

| 44 | −3.3545 | 1.92178 | −7.2 | 0.7 | 0.001 | 0.07 | 0.951 | |

| 44 | −1.35659 | 12.22918 | −47.3 | 49.72 | 0.317 | 0.67 | 0.928 | |

| 44 | 5.259546 | 45.5113 | −247.4 | 67.85 | 0.001 | 0.32 | 0.901 | |

| 44 | 6.616136 | 56.26286 | −297.13 | 115.15 | 0.000 | 0.05 | 0.908 |

| Variables | Dickey-Fuller Test for Unit Root | ||||

|---|---|---|---|---|---|

| Test | 1% | 5% | 10% | ||

| Z(t) | −9.517 | −3.535 | −2.904 | −2.587 | |

| Z(t) | −3.902 | −3.634 | −2.952 | −2.610 | |

| Z(t) | −7.018 | −3.634 | −2.952 | −2.610 | |

| Z(t) | −9.406 | −3.736 | −2.994 | −2.628 | |

| Z(t) | −9.221 | −3.634 | −2.952 | −2.610 | |

| Z(t) | −5.857 | −3.628 | −2.950 | −2.608 | |

| Z(t) | −6.414 | −3.628 | −2.950 | −2.608 | |

| Z(t) | −6.481 | −3.634 | −2.952 | −2.610 | |

| Estimation | 1 | 2 | 3 |

|---|---|---|---|

| Variables | |||

| 36.22 ** | 34.07 ** | 34.75 ** | |

| (0.000) | (0.000) | (0.000) | |

| 45.89 ** | 45.75 ** | 45.75 *** | |

| (0.000) | (0.000) | (0.000) | |

| 2.8962 | |||

| 0.4755 | |||

| 0.4418 | |||

| 213.9803 | 213.1298 | 214.8339 | |

| 221.2665 | 220.2665 | 221.9707 | |

| 216.6269 | 215.7764 | 217.4806 | |

| 44 | 44 | 44 | |

| t statistics in parentheses, * p < 0.05, ** p < 0.01, *** p < 0.001, Akaike information criterion (AIC), Bayesian information criterion (BIC) and Hannan-Quinn information criterion (HQC) is a measure of the goodness of fit of a statistical model. | |||

| Estimation 1 is related to | |||

| Estimation 2 is related to | |||

| Estimation 3 is related to | |||

| Estimation | 1 | 2 | 3 |

|---|---|---|---|

| Variables | |||

| 2.257 *** | 1.873 *** | 1.971 *** | |

| (0.000) | (-0.001) | (0.000) | |

| −0.451 ** | −0.312 | −0.358 * | |

| (−0.008) | (−0.059) | (−0.026) | |

| −14.82 | −11.59 | −13.31 | |

| (−0.347) | (−0.443) | (−0.379) | |

| 2.024 *** | 1.475 *** | 1.018 *** | |

| (0.000) | (−0.000) | (0.000) | |

| −0.3001 ** | −0.256 | −0.253 * | |

| (−0.000) | (−0.012) | (−0.025) | |

| −19.69 | −1.211 | −3.503 | |

| (−0.221) | (−0.94) | (−0.827) | |

| −1.2168 | |||

| 1.9182 | |||

| 1.927 | |||

| 213.9803 | 213.1298 | 214.8339 | |

| 221.2665 | 220.2665 | 221.9707 | |

| 216.6269 | 215.7764 | 217.4806 | |

| 44 | 44 | 44 | |

| t statistics in parentheses, * p < 0.05, ** p < 0.01, *** p < 0.001, Akaike information criterion (AIC), Bayesian information criterion (BIC) and Hannan-Quinn information criterion (HQC) is a measure of the goodness of fit of a statistical model. | |||

| Estimation 1 is related to | |||

| Estimation 2 is related to | |||

| Estimation 3 is related to | |||

| Author | Definition | EB | TB | TE | TS | % S |

|---|---|---|---|---|---|---|

| Alesina and Perotti (1995) | Threshold of 1.5% CAPB | 59 | 60 | 119 | 66 | 55.46% |

| (McDermott and Wescott 1996) | Threshold of 1.5% CAPB | 34 | 74 | 108 | 43 | 39.81% |

| Alesina et al. (1998) | Threshold of 2% CAPB | 23 | 28 | 51 | 19 | 37.25% |

| Zaghini (2001) | Threshold of 1.6% or 1.4% of CAPB | 52 | 48 | 100 | 52 | 52.00% |

| Duperrut (1998) | Threshold of 1.6% or 1.4% of CAPB | 9 | 2 | 22.22% | ||

| Afonso and Silva Leal (2019) | Threshold of 1.5% CAPB | 51 | 18.61% | |||

| Quaresma (2021) | Threshold of 1.5% CAPB and the narrative approach | 76 | 60 | 136 | 36 | 26.47% |

| Wiese et al. (2018) | Threshold of 1.5% CAPB and the narrative approach | 42 | 58 | 110 | 50 | 45.45% |

| Nunes (2019) | 61 | 52 | 113 | 25 | 22.12% | |

| Agnello et al. (2019) | Threshold of 1.5% CAPB and the narrative approach | 51 | 15 | 29.41% | ||

| Afonso and Silva Leal (2022) | Threshold of 1.5% CAPB and the narrative approach | 81 | 98 | 179 | 45 | 25.13% |

| This paper | 1.2168% | 8 | 8 | 3 | 37.50% | |

| 1.9182% | 4 | 4 | 1 | 25.00% | ||

| 1.9270% | 4 | 1 | 25.00% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Buthelezi, E.M.; Nyatanga, P. Threshold of the CAPB That Can Be Attributed to Fiscal Consolidation Episodes in South Africa. Economies 2023, 11, 152. https://doi.org/10.3390/economies11060152

Buthelezi EM, Nyatanga P. Threshold of the CAPB That Can Be Attributed to Fiscal Consolidation Episodes in South Africa. Economies. 2023; 11(6):152. https://doi.org/10.3390/economies11060152

Chicago/Turabian StyleButhelezi, Eugene Msizi, and Phocenah Nyatanga. 2023. "Threshold of the CAPB That Can Be Attributed to Fiscal Consolidation Episodes in South Africa" Economies 11, no. 6: 152. https://doi.org/10.3390/economies11060152

APA StyleButhelezi, E. M., & Nyatanga, P. (2023). Threshold of the CAPB That Can Be Attributed to Fiscal Consolidation Episodes in South Africa. Economies, 11(6), 152. https://doi.org/10.3390/economies11060152