Digital Financial Inclusion, Digital Financial Services Tax and Financial Inclusion in the Fourth Industrial Revolution Era in Africa

Abstract

:1. Introduction

2. Review of Important Literature

2.1. Industry 4.0, Digitisation, Digitalisation, DFS and Financial Inclusion Defined

2.1.1. Industry 4.0

2.1.2. Digitisation

2.1.3. Financial Inclusion

2.1.4. Digital Financial Services

2.1.5. Digital Financial Inclusion

2.2. The Financial Services Sector in Africa

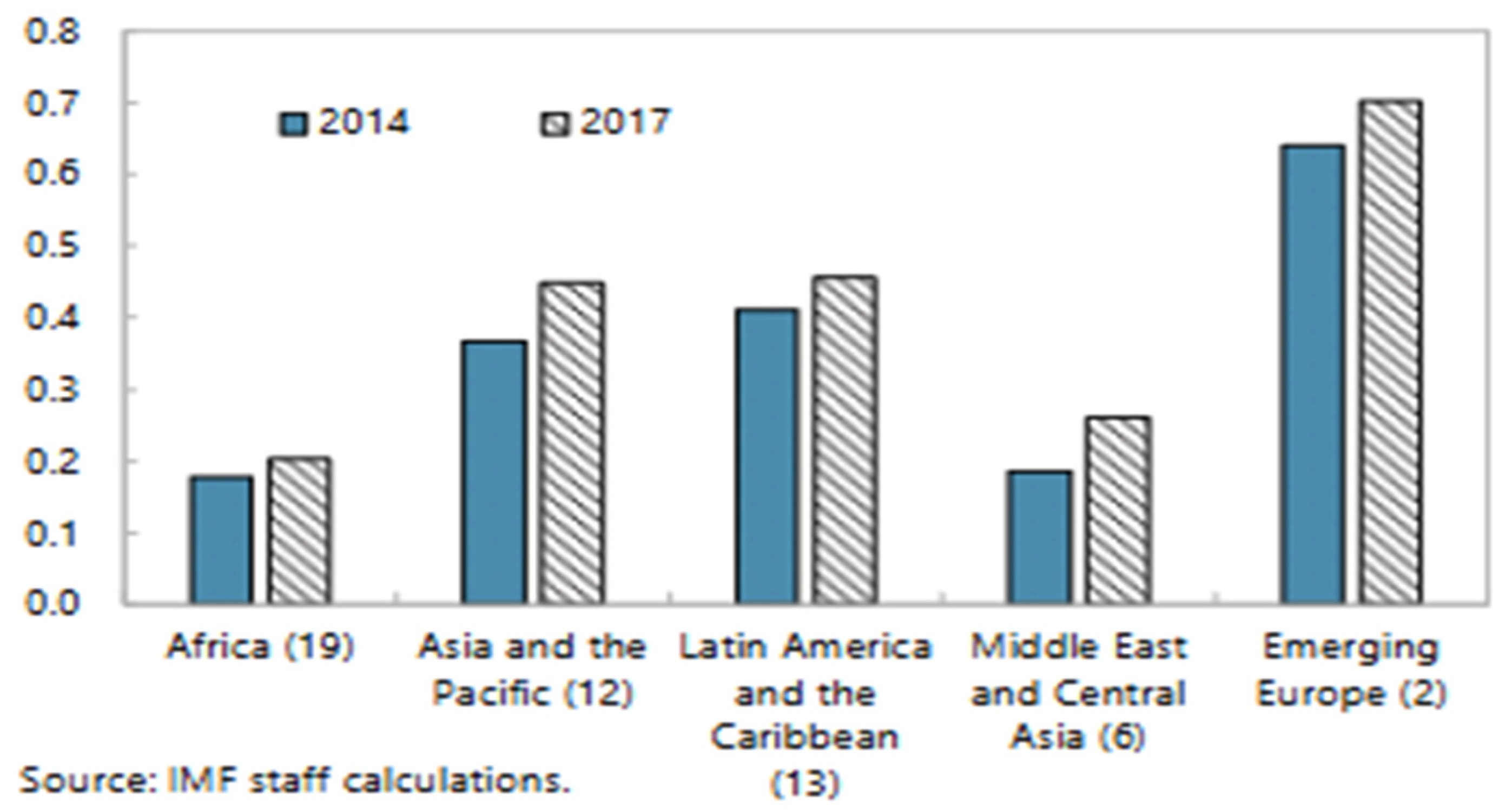

2.2.1. Usage of Digital Financial Services

2.2.2. Digital Financial Services and Financial Inclusion in Africa

2.3. The Rationale for Taxation of Digital Financial Services in Africa

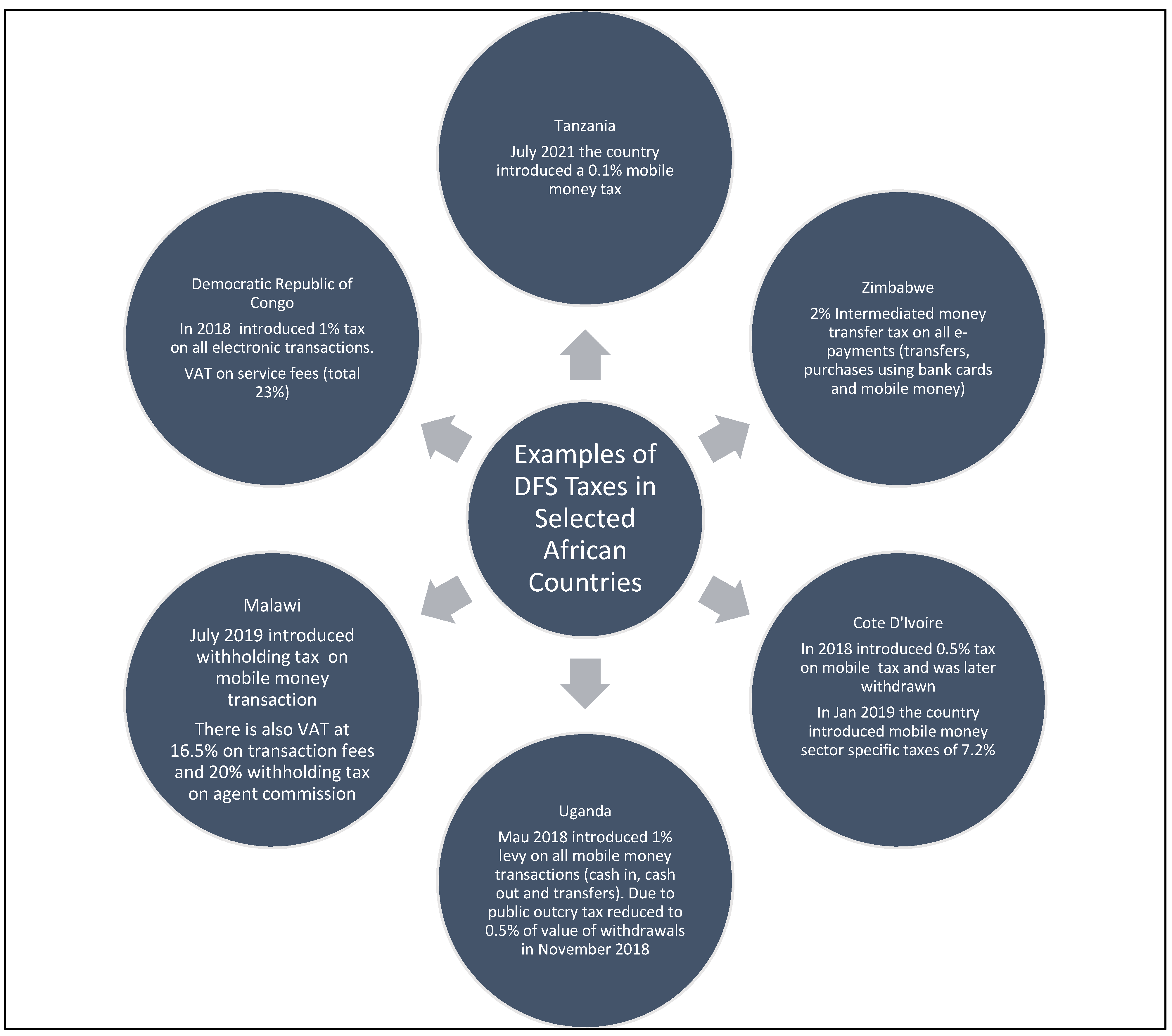

2.3.1. Digital Financial Services Taxes in Africa

2.3.2. Digital Services Taxes and Financial Inclusion in African countries

Increase in the Tax Burden and Prices of DFS

Usage Implications

The Influence on Market Development or Structure

Trust and Tax Morale

Invasion of Privacy Due to Tax Audits and Surveillance to Foster Tax Compliance

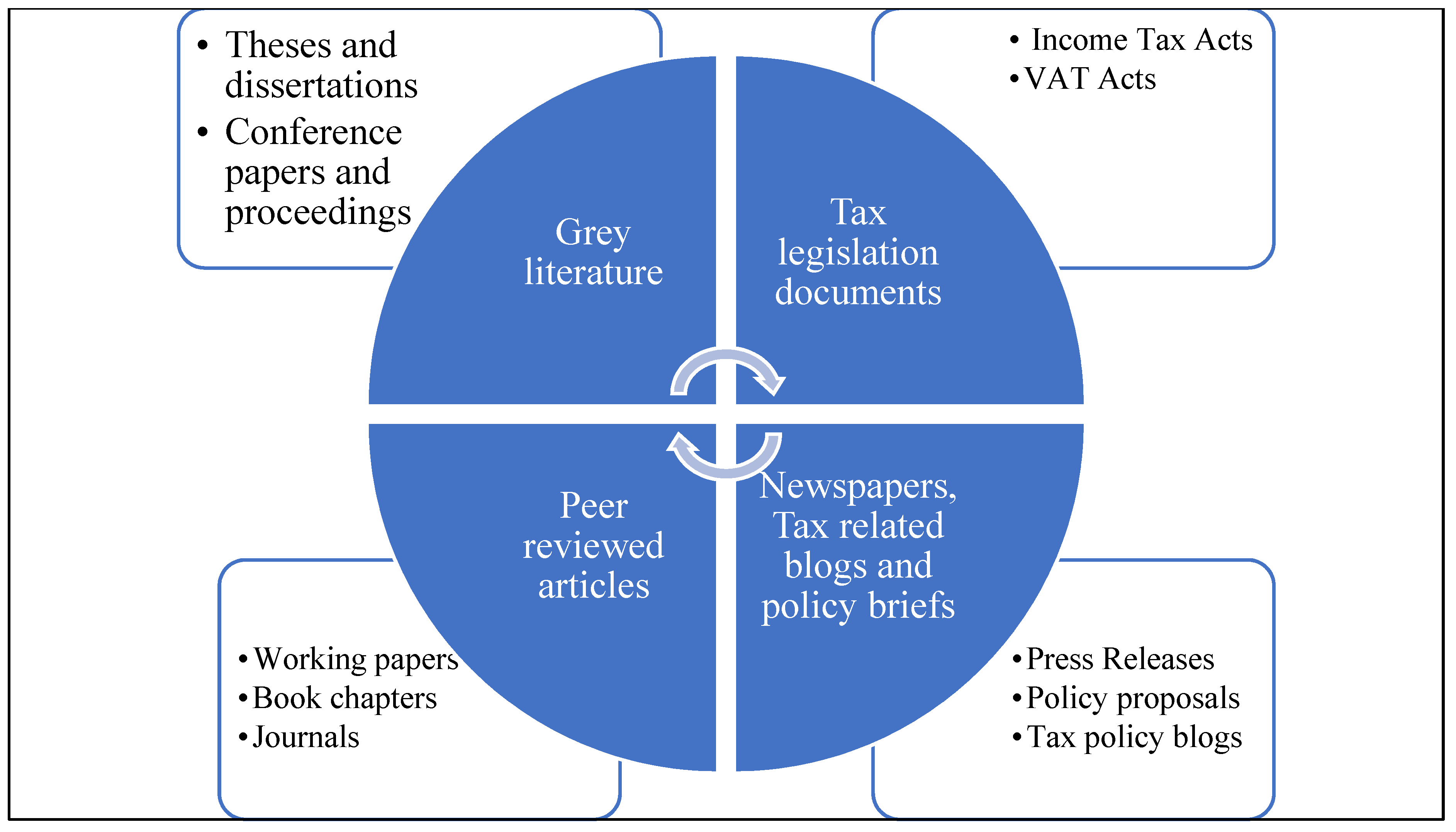

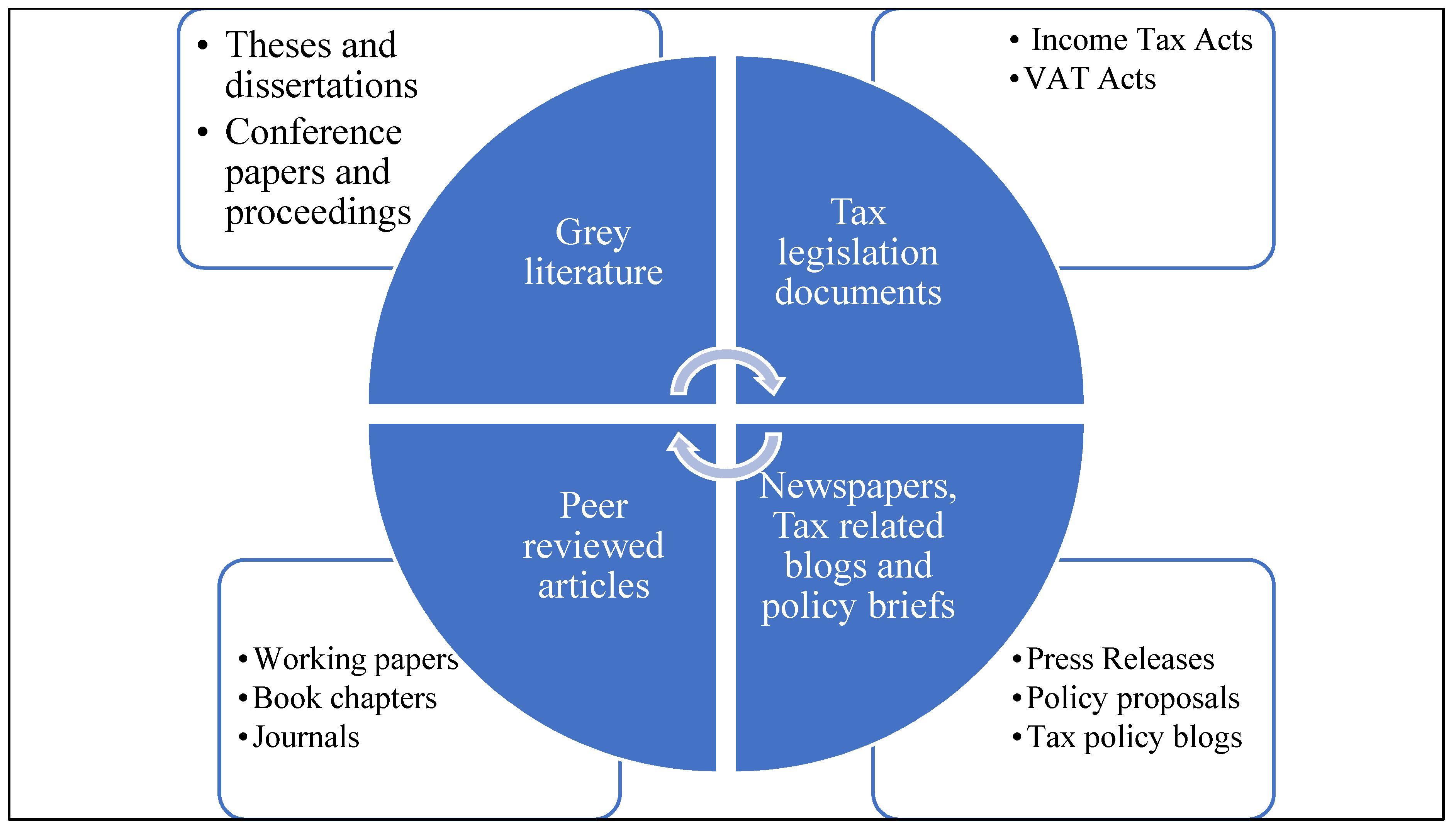

3. Review Methodology

4. Discussion of Findings

4.1. The Relationship between the Expansion of Digital Financial Services and Digital Inclusion in African Countries

4.2. Justification for DFS Taxes in Africa

4.3. Potential Consequences of DFS Taxes in African Countries

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Adaba, Godfriend B., Daniel A. Ayoung, and Pamela Abbott. 2019. Exploring the contribution of mobile money to well-being from a capability perspective. The Electronic Journal of Information Systems in Developing Countries 85: e12079. [Google Scholar] [CrossRef] [Green Version]

- Adegoke, Yinka. 2018. Ugandans are Furious with a New Tax for Using Social Media and Mobile Money. Quartz Africa 1: 1–3. [Google Scholar]

- Agur, Itai, Soledad Martinez Peria, and Celine Rochon. 2020. Digital financial services and the pandemic: Opportunities and risks for emerging and developing economies. International Monetary Fund Special Series on COVID-19 Transactions 1: 2. [Google Scholar]

- Ahmad, Ahmad Hassan, Christopher Green, and Fei Jiang. 2020. Mobile money, financial inclusion and development: A review with reference to African experience. Journal of Economic Surveys 34: 753–92. [Google Scholar] [CrossRef]

- Ahmed, Shamira, and Alison Gillwald. 2020. Multifaceted Challenges of Digital Taxation in Africa. Available online: https://www.africaportal.org/documents/20840/Final-Tax-PB_30112020.pdf (accessed on 10 March 2022).

- Ahmed, Shamira, Tapiwa Chinembiri, and Naila Govan-Vassen. 2021. COVID-19 Exposes the Contradictions of Social Media Taxes in Africa. Available online: https://www.africaportal.org/documents/21197/Covid-19-social_media_taxes_in_Africa.pdf (accessed on 10 March 2022).

- Akanle, Olayinka, Demilade Kayode, and Irenitemi Abolade. 2022. Sustainable development goals (SDGs) and remittances in Africa. Cogent Social Sciences 8: 2037811. [Google Scholar] [CrossRef]

- Asongu, Simplice, and Nicholas Odhiambo. 2022. The Role of Mobile Characteristics on Mobile Money Innovations. (No. 22/011). Brighton: African Governance and Development Institute. [Google Scholar]

- Asongu, Simplice A., and Nicholas M. Odhiambo. 2018. ICT, financial access and gender inclusion in the formal economic sector: Evidence from Africa. African Finance Journal 20: 45–65. [Google Scholar] [CrossRef] [Green Version]

- Baganzi, Amin. 2018. Internal Controls, Managerial Competence and Financial Accountability in Technical and Vocational Institutions in Uganda. Master’s thesis. Available online: https://mubsir.mubs.ac.ug/handle/20.500.12282/3119 (accessed on 10 March 2022).

- Bille, Fahima Said, Sinja Buri, Tiphaine A. Crenn, Lesley Sarah Denyes, Chabir Vali Taibo Hassam, Soren Heitmann, and Martinez Ramji. 2018. Digital Access: The Future of Financial Inclusion in Africa. (No. 128850). The World Bank: pp. 1–97. Available online: https://www.ifc.org/wps/wcm/connect/region__ext_content/ifc_external_corporate_site/sub-saharan+africa/resources/201805_report_digital-access-africa (accessed on 10 March 2022).

- Bowen, Glenn A. 2009. Document analysis as a qualitative research method. Qualitative Research Journal 9: 27–40. [Google Scholar] [CrossRef] [Green Version]

- Bunn, Daniel, Elke Asen, and Cristina Enache. 2020. Digital Taxation around the World. Washington, DC: Tax Foundation, Available online: https://files.taxfoundation.org/20200527192056/Digital-Taxation-Around-the-World.pdf (accessed on 12 March 2022).

- Carboni, Isabelle, and Hennie Bester. 2020. When the digital payment goes viral: Lessons from COVID-19’s impact on mobile money in Rwanda. Cenfri. May 19, pp. 1–8. Available online: https://cenfri.org/articles/covid-19s-impact-on-mobile-money-in-rwanda/ (accessed on 10 March 2022).

- Clifford, Killian. 2020. The Causes and Consequences of Mobile Money Taxation An Examination of Mobile Money Transaction Taxes in Sub-Saharan Africa. Available online: https://www.ictd.ac/event/mobile-money-taxation-africa-causes-consequences/ (accessed on 12 March 2022).

- De Koker, Louis, and Nicola Jentzsch. 2013. Financial inclusion and financial integrity: Aligned incentives? World Development 44: 267–80. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, and Leora F. Klapper. 2012. Financial inclusion in Africa: An overview. World Bank Policy Research Working Paper 6088. Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/9335/WPS6088.pdf?sequence=1 (accessed on 10 March 2022).

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2018a. Opportunities for Expanding Financial Inclusion Through Digital Technology. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/978–1-4648–1259-0_ch6 (accessed on 12 March 2022).

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2018b. The Unbanked. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/978–1-4648–1259-0_ch2 (accessed on 12 March 2022).

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2020. The Global Findex Database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review 34: S2–S8. [Google Scholar]

- Ebong, Jimmy, and Babu George. 2021. Financial Inclusion through Digital Financial Services (DFS): A Study in Uganda. Journal of Risk and Financial Management 14: 393. [Google Scholar] [CrossRef]

- El-Zoghbi, Mayada. 2019. Global Developments in Inclusive Financial Systems. Available online: https://www.frbsf.org/community-development/wp-content/uploads/sites/3/el-zoghbi-global-developments-in-inclusive-financial-systems.pdf (accessed on 12 March 2022).

- El-Zoghbi, Mayada, Nina Holle, and Mathew Soursourian. 2019. Emerging Evidence on Financial Inclusion. Available online: https://www.findevgateway.org/paper/2019/08/emerging-evidence-financial-inclusion-moving-black-and-white-color (accessed on 12 March 2022).

- Evans, Olaniyi. 2018. Connecting the poor: The internet, mobile phones and financial inclusion in Africa. Digital Policy, Regulation and Governance 20: 568–81. [Google Scholar] [CrossRef]

- GSMA. 2021. State of the Industry Report on Mobile Money 2021. Available online: https://www.adfi.org/publications/state-industry-report-mobile-money-2021-gsma (accessed on 12 March 2022).

- Harris, Andrew, Seymour Goodman, and Patrick Traynor. 2012. Privacy and security concerns associated with mobile money applications in Africa. The Washington Journal of Law, Technology & Arts 8: 245. [Google Scholar]

- International Monetary Fund. 2021. Measuring Digital Financial Inclusion in Emerging Market and Developing Economies: A New Index. Asian Economic Policy Review. Available online: https://www.imf.org/-/media/Files/Publications/WP/2021/English/wpiea2021090-print-pdf.ashx (accessed on 12 March 2022).

- Juju, Denabo, Gideon Baffoe, Rodolfo Dam Lam, Alice Karanja, Merle Naidoo, Abaubakari Ahmed, and Alexandros Gasparatos. 2020. Sustainability challenges in sub-Saharan Africa in the context of the sustainable development goals (SDGs). In Sustainability Challenges in Sub-Saharan Africa I. Singapore: Springer, pp. 3–50. [Google Scholar]

- Juswanto, Wawan, and Rebecca Simms. 2017. Fair Taxation in the Digital Economy. Tokyo: Asian Development Bank Institute, Available online: https://www.adb.org/publications/fair-taxation-digital-economy (accessed on 12 March 2022).

- Kakungulu-Mayambala, Ronald, and Solomon Rukundo. 2018. Implications of Uganda’s new social media tax. East African Journal of Peace & Human Rights 24: 2. [Google Scholar]

- Karppinen, Kari, and Hallvard Moe. 2019. Texts as data I: Document analysis. In The Palgrave Handbook of Methods for Media Policy Research. Cham: Palgrave Macmillan, pp. 249–62. [Google Scholar]

- Kayesa, Naomi Karen, and Maylene Shung-King. 2021. The role of document analysis in health policy analysis studies in low and middle-income countries: Lessons for HPA researchers from a qualitative systematic review. Health Policy Open 2: 100024. [Google Scholar] [CrossRef]

- Kelbesa, Mergesa. 2020. Digital Service Taxes and Their Application. Available online: https://opendocs.ids.ac.uk/opendocs/bitstream/handle/20.500.12413/16968/914_Digital_Service_Tax.pdf?sequence=1 (accessed on 17 March 2022).

- Kelikume, Ikechukwu. 2021. Digital financial inclusion, informal economy and poverty reduction in Africa. Journal of Enterprising Communities: People and Places in the Global Economy. Available online: https://www.emerald.com/insight/1750-6204.htm (accessed on 20 March 2022).

- Khera, Purva, Sumiko Ogawa, Ratna Sahay, and Mahima Vasishth. 2021. Is Digital Financial Inclusion Unlocking Growth? International Monetary Fund. Available online: https://www.imf.org/en/Publications/WP/Issues/2021/06/11/Is-Digital-Financial-Inclusion-Unlocking-Growth-460738 (accessed on 12 March 2022).

- Koomson, Isaac, Edward Martey, and Prince M. Etwire. 2022. Mobile money and entrepreneurship in East Africa: The mediating roles of digital savings and access to digital credit. Information Technology & People. ahead-of-print. [Google Scholar]

- Lees, Adrienne, and Doris Akol. 2021. There and Back Again: The Making of Uganda’s Mobile Money Tax. Available online: https://www.africaportal.org/documents/22362/ICTD_WP123.pdf (accessed on 17 February 2022).

- Llewellyn-Jones, Laura. 2016. Mobile money: Part of the African financial inclusion solution? Economic Affairs 36: 212–16. [Google Scholar] [CrossRef]

- Machasio, Immaculate Nafula. 2020. COVID-19 and Digital Financial Inclusion in Africa: How to Leverage Digital Technologies during the Pandemic. Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/34637/COVID-19-and-Digital-Financial-Inclusion-in-Africa-How-to-Leverage-Digital-Technologies-During-the-Pandemic.pdf?sequence=1 (accessed on 20 March 2022).

- Marinai, Simone. 2008. Introduction to document analysis and recognition. In Machine Learning in Document Analysis and Recognition. Berlin/Heidelberg: Springer, pp. 1–20. [Google Scholar]

- Martin, Aaron. 2019. Mobile money platform surveillance. Surveillance & Society 17: 213–22. [Google Scholar]

- Matheson, Thornton, and Patrick Petit. 2021. Taxing telecommunications in developing countries. International Tax and Public Finance 28: 248–80. [Google Scholar] [CrossRef]

- Mhlanga, David. 2020. Industry 4.0 in finance: The impact of artificial intelligence (ai) on digital financial inclusion. International Journal of Financial Studies 8: 45. [Google Scholar] [CrossRef]

- Mhlanga, David. 2021. Financial inclusion in emerging economies: The application of machine learning and artificial intelligence in credit risk assessment. International Journal of Financial Studies 9: 39. [Google Scholar] [CrossRef]

- Mhlanga, David. 2022. The Role of Artificial Intelligence and Machine Learning Amid the COVID-19 Pandemic: What Lessons Are We Learning on 4IR and the Sustainable Development Goals. International Journal of Environmental Research and Public Health 19: 1879. [Google Scholar] [CrossRef]

- Mpofu, Favourate Y. S. 2021a. Informal Sector Taxation and Enforcement in African Countries: How plausible and achievable are the motives behind? A Critical Literature Review. Open Economics 4: 72–97. [Google Scholar] [CrossRef]

- Mpofu, Favourate Y. S. 2021b. Review Articles: A Critical Review of the Pitfalls and Guidelines to effectively conducting and reporting reviews. Technium Social Sciences Journal 18: 550. [Google Scholar]

- Mpofu, Favourate Y. S. 2021c. Taxing the informal sector through presumptive taxes in Zimbabwe: An avenue for a broadened tax base, stifling of the informal sector activities or both. Journal of Accounting and Taxation 13: 153–77. [Google Scholar]

- Mullins, Peter, Sanjeev Gupta, and Jianhong Liu. 2020. Domestic Revenue Mobilization in Low-Income Countries: Where To From Here. Center for Global Development Policy Paper 195. Available online: https://www.cgdev.org/publication/domestic-revenue-mobilization-low-income-countries-where-here (accessed on 12 March 2022).

- Mungai, Kinyanjui, and Albert van der Linden. 2021. The Unpopular Choice: Taxing Digital Payments in the Era of Digitalisation. Available online: https://cenfri.org/articles/taxing-digital-payments-in-the-era-of-digitalisation/ (accessed on 12 March 2022).

- Munoz, Laura, Giulia Mascagni, Wilson Prichard, and Fabrizio Santoro. 2022. Should Governments Tax Digital Financial Services? A Research Agenda to Understand Sector-Specific Taxes on DFS. Available online: https://opendoc.ids.ac.uk/opendocs/bitstream/handle/20.500.122413/17171/ICTD_WP136 (accessed on 22 March 2022).

- Ndajiwo, Mustapha. 2020. The Taxation of the Digitalised Economy: An African Study. ICTD Working Paper 107. Brighton: Institute of Development Studies. [Google Scholar]

- Ndung’u, Njuguna S. 2019. Taxing Mobile Phone Transactions in Africa: Lessons from Kenya. Available online: https://www.africaportal.org/publications/taxing-mobile-phone-transactions-africa-lessons-kenya/ (accessed on 12 March 2022).

- Oguttu, Annet Wanyama. 2018. International tax competition, harmful tax practices and the ‘race to the bottom: A special focus on unstrategic tax incentives in Africa. Comparative and International Law Journal of Southern Africa 51: 293–319. [Google Scholar]

- Ojo, Tinuade Adekunbi. 2020. A Study of Financial Inclusion and Women’s Empowerment in South Africa: The Case of Female Entrepreneurs in Gauteng. Ph.D. dissertation, The University of Pretoria, Pretoria, South Africa. [Google Scholar]

- Ojo, Tinuade Adekunbi. 2022. Digital Financial Inclusion for Women in the Fourth Industrial Revolution: A Key towards Achieving Sustainable Development Goal 5. Africa Review 1: 1–26. [Google Scholar] [CrossRef]

- Ojo, Tinuade Adekun, and Siphamandla Zondi. 2021. Impact of Institutional Quality and Governance on Financial Inclusion for Women in South Africa: A Case of Gauteng Women Entrepreneurs. The Strategic Review for Southern Africa 43: 59–82. [Google Scholar] [CrossRef]

- Ouma, Shem Alfred, Teresa Maureen Odongo, and Maureen Were. 2017. Mobile financial services and financial inclusion: Is it a boon for savings mobilization? Review of Development Finance 7: 29–35. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2018. Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review 18: 329–40. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2020. Social inclusion and financial inclusion: International evidence. International Journal of Development Issues. Available online: https://www.emerald.com/insight/1446-8956.html (accessed on 15 March 2022).

- Ozili, Peterson K. 2021. Financial inclusion research around the world: A review. Forum for Social Economics. Available online: https://www.tandfonline.com/doi/pdf/10.1080/07360932.2020.1715238? (accessed on 20 March 2022).

- Park, Cyn-Young, and Rogelio Mercado Jr. 2018. Financial inclusion, poverty, and income inequality. The Singapore Economic Review 63: 185–206. [Google Scholar] [CrossRef]

- Pushkareva, Natalia. 2021. Taxing Times for Development: Tax and Digital Financial Services in Sub-Saharan Africa. Financing for Development 1: 33–64. [Google Scholar]

- Rogan, Michael. 2019. Tax Justice and the Informal Economy: A Review of the Debates. Available online: https://www.wiego.org/sites/default/files/publications/file/Rogan_Taxation_Debates_WIEGO_WorkingPaperNo41_2020.pdf (accessed on 20 March 2022).

- Rukundo, Solomon. 2017. Taxation of the telecommunications sector: A focus on policy issues and considerations in taxation of mobile money in Uganda. Africa Tax Research Network 2017 Congress at Antananarivo, Madagascar. Available online: https://www.researchgate.net/profile/Solomon-Rukundo/publication/323534979_Taxation_of_the_Telecommunications_Sector_A_Focus_on_Policy_Issues_and_Considerations_in_Taxation_of_Mobile_Money_in_Uganda/links/5a9a51d445851586a2aa080b/Taxation-of-the-Telecommunications-Sector-A-Focus-on-Policy-Issues-and-Considerations-in-Taxation-of-Mobile-Money-in-Uganda.pdf (accessed on 22 March 2022).

- Santoro, Fabrizio, Laura Munoz, Wilson Prichard, and Giulia Mascagni. 2022. Digital Financial Services and Digital IDs: What Potential Do They Have for Better Taxation in Africa? Available online: https://opendocs.ids.ac.uk/opendocs/bitstream/handle/20.500.12413/17113/ICTD_WP137.pdf?sequence=1 (accessed on 20 February 2022).

- Schwab, Klaus. 2015. The Fourth Industrial Revolution. What It Means and How to Respond? Snapshot. Available online: https://www.weforum.org/agenda/2016/01/the-fourth-industrial-revolution-what-it-means-and-how-to-respond/ (accessed on 17 March 2022).

- Sebele-Mpofu, Favourate Y. 2020. Governance quality and tax morale and compliance in Zimbabwe’s informal sector. Cogent Business & Management 7: 1794662. [Google Scholar]

- Sebele-Mpofu, Favourate Yelesedzani. 2021. The informal sector, the “implicit” social contract, the willingness to pay taxes and tax compliance in Zimbabwe. Accounting, Economics, and Law: A Convivium. Available online: https://doi.org/10.1515/ael-2020-0084 (accessed on 22 March 2022).

- Sekantsi, Lira Peter. 2019. Digital financial services uptake in Africa and its role in financial inclusion of women. Journal of Digital Banking 4: 161–74. [Google Scholar]

- Sekantsi, Lira Peter, and Sephooko I. Motelle. 2018. The role of mobile money in financial inclusion in Lesotho. MEFMI Research and Policy Journal 3: 77–99. [Google Scholar]

- Shapshack, Toby. 2021. Mobile Money in Africa Reaches $500 Billion during the Pandemic. Available online: https://www.forbes.com/sites/tobyshapshak/2021/05/19/mobile-money-in-africa-reaches-nearly-500bn-during-pandemic/ (accessed on 20 March 2022).

- Shipalana, Palesa. 2019. Digitising Financial Services: A Tool for Financial Inclusion in South Africa? Available online: https://www.africaportal.org/documents/19566/Occasional-Paper-301-shipalana.pdf (accessed on 24 March 2022).

- Sile, Erick. 2013. Financial inclusion in fragile states. Financial Inclusion in Africa, 94–104. [Google Scholar]

- Silue, Tarna. 2021. E-Money, Financial Inclusion and Mobile Money Tax in Sub-Saharan African Mobile Networks. Available online: https://ideas.repec.org/p/hal/wpaper/hal-03281898.html (accessed on 24 March 2022).

- Simatele, Munacinga. 2021. E-payment instruments and welfare: The case of Zimbabwe. TD: The Journal for Transdisciplinary Research in Southern Africa 17: 1–11. [Google Scholar] [CrossRef]

- Siwela, Gladys, and Tavonga Njaya. 2018. Comparative analysis of the challenges of financial inclusion of female street traders in Asia, Latin America and Sub-Saharan Africa. Scholars Journal of Economics, Business and Management 5: 218–26. [Google Scholar]

- Siwela, Gladys, and Tavonga Njaya. 2021. Opportunities and Challenges for Digital Financial Inclusion of Females in the Informal Sector through Mobile Phone Technology: Evidence from Zimbabwe. Available online: http://lis.zou.ac.zw:8080/dspace/bitstream/0/607/1/Opportunities%20and%20challlenges%20of%20digital%20fnancial%20inclusion%20of%20females%20in%20the%20informal%20sector_Siwela-2021.pdf (accessed on 17 March 2022).

- Smith, Adam. 1776. An Inquiry into the Nature and Causes of the Wealth of Nations. In RH Campbell and AS Skinner. Edited by Adam Smith. Oxford: Oxford University Press, vol. 145, p. 1976. [Google Scholar]

- Snyder, Hannah. 2019. Literature review as a research methodology: An overview and guidelines. Journal of Business Research 104: 333–39. [Google Scholar] [CrossRef]

- Tafotie, Roger. 2020. Fostering Digital Financial Services in Africa: A Case of Embracing Innovation for Business and Inclusion. University of Luxembourg Law Working Paper, 2020-005. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3557808 (accessed on 22 March 2022).

- Triki, Thouraya, and Issa Faye. 2013. Financial Inclusion in Africa. Abidjan: Ivory Coast African Development Bank, Available online: https://www.rfilc.org/wp-content/uploads/2020/08/Financial_Inclusion_in_Africa.pdf (accessed on 20 March 2022).

- World Bank. 2020. Digital Financial Inclusion. Available online: https://www.worldbank.org/en/topic/financialinclusion/publication/digital-financial-inclusion (accessed on 24 March 2022).

- World Bank. 2022a. Paying Taxes. Available online: https://subnational.doingbusiness.org/en/data/exploretopics/paying-taxes/why-matters (accessed on 20 March 2022).

- World Bank. 2022b. Taxes & Government Revenue. Available online: https://www.worldbank.org/en/topic/taxes-and-government-revenue#1 (accessed on 24 March 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Study | Focus | Methodology | Findings |

|---|---|---|---|

| Kelikume (2021) | Relationships between mobile phones, the internet, financial inclusion, the informal economy and poverty alleviation. | The generalised method of moments, and a panel of 42 countries (1995–2007) | Financial inclusion has a significant positive relationship with the increased use of mobile phones and the internet in the informal economy. Increased mobile phone usage and access to the internet have a positive relationship with poverty reduction. Increased financial inclusion reduces poverty. |

| Evans (2018) | Relationships between internet, mobile phones, and financial inclusion. | Used a three-step approach, examining the stationarity of variables, conducting tests of co-integration, and evaluating the impact of the internet and mobile phone usage on financial inclusion. The study relied on a panel FMOLS approach and Granger causality tests. | In countries where the usage of mobile financial services is significant, financial inclusion is high and there is increased economic growth. |

| (Park and Mercado 2018) | Testing the impact of financial inclusion on poverty reduction and inequality. | Used financial inclusion indicators. | Financial inclusion is vital for inclusive economic growth, as access to finance can assist economic agents to undertake long-term spending, saving, and investment decisions. |

| (Simatele 2021) | The effect of e-instruments on the welfare of citizens. | Collected data through focus groups. | Financial inclusion contributes positively to the improvement of the welfare of citizens and socio-economic development. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mpofu, F.Y.; Mhlanga, D. Digital Financial Inclusion, Digital Financial Services Tax and Financial Inclusion in the Fourth Industrial Revolution Era in Africa. Economies 2022, 10, 184. https://doi.org/10.3390/economies10080184

Mpofu FY, Mhlanga D. Digital Financial Inclusion, Digital Financial Services Tax and Financial Inclusion in the Fourth Industrial Revolution Era in Africa. Economies. 2022; 10(8):184. https://doi.org/10.3390/economies10080184

Chicago/Turabian StyleMpofu, Favourate Y., and David Mhlanga. 2022. "Digital Financial Inclusion, Digital Financial Services Tax and Financial Inclusion in the Fourth Industrial Revolution Era in Africa" Economies 10, no. 8: 184. https://doi.org/10.3390/economies10080184

APA StyleMpofu, F. Y., & Mhlanga, D. (2022). Digital Financial Inclusion, Digital Financial Services Tax and Financial Inclusion in the Fourth Industrial Revolution Era in Africa. Economies, 10(8), 184. https://doi.org/10.3390/economies10080184