Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment

Abstract

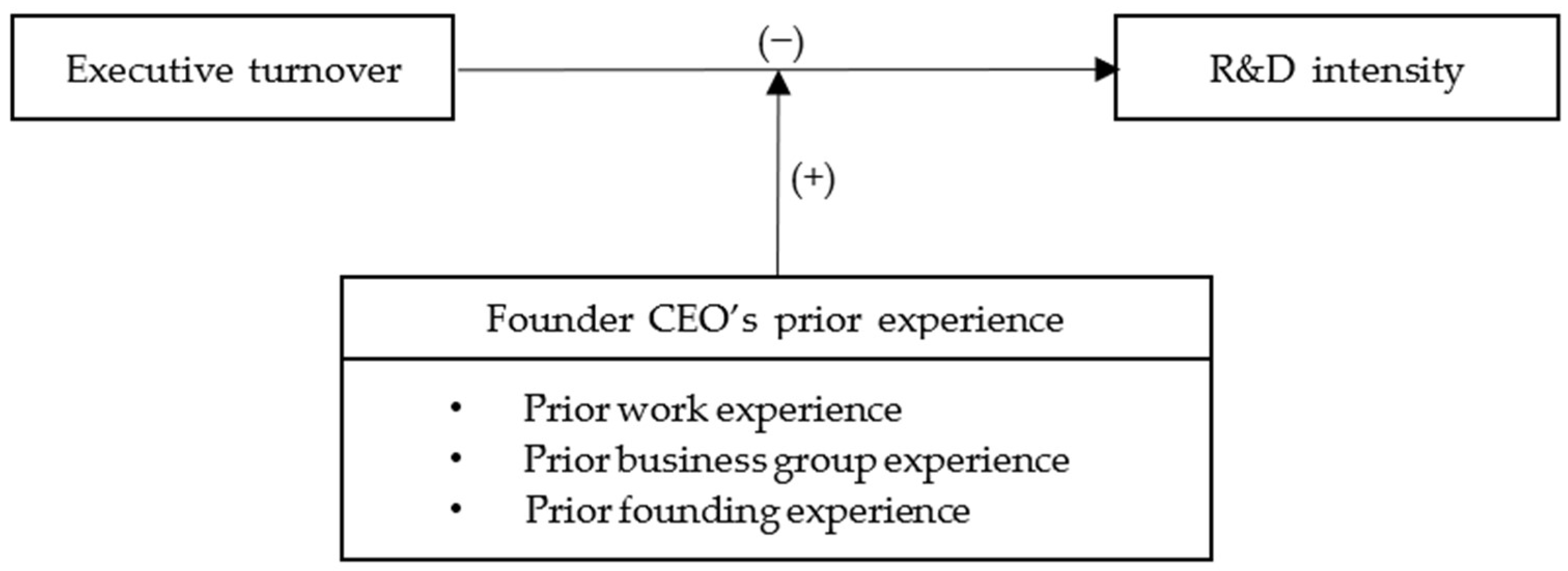

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Executive Turnover and R&D Investment

2.2. Moderating Effect of Founder’s Prior Work Experience

2.3. Moderating Effect of Founder’s Prior Business Group Experience

2.4. Moderating Effect of Founder’s Prior Founding Experience

3. Method

3.1. Sample

3.2. Measures

4. Empirical Results

5. Conclusions and Discussion

5.1. Theoretical Contribution and Implications

5.2. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Definition |

|---|---|

| R&D intensity | the ratio of R&D investment to total sales |

| Executive turnover | the ratio of executive leave to total employment size |

| Work experience | the number of working years before founding the new venture |

| Business group experience | a dichotomous variable coded as “1” if a founder has worked for a business group affiliated firm before and “0” otherwise |

| Founding experience | the number of firms founded before founding the new venture |

| Firm size | a logarithmic value of total assets |

| ROA | a net income divided by total assets |

| Debt ratio | a total debt divided by total assets |

| Age | the number of years since the firm’s foundation |

| Capital financing | the size of capital raising divided by total assets |

References

- Acharya, Viral, and Zhaoxia Xu. 2017. Financial dependence and innovation: The case of public versus private firms. Journal of Financial Economics 124: 223–43. [Google Scholar] [CrossRef] [Green Version]

- Acquaah, Moses. 2012. Social networking relationships, firm-specific managerial experience and firm performance in a transition economy: A comparative analysis of family owned and nonfamily firms. Strategic Management Journal 33: 1215–28. [Google Scholar] [CrossRef]

- Athanassiou, Nicholas, and Douglas Nigh. 2000. Internationalization, tacit knowledge and the top management teams of MNCs. Journal of International Business Studies 31: 471–87. [Google Scholar] [CrossRef]

- Bamford, Charles E., Thomas J. Dean, and Patricia P. McDougall. 2000. An examination of the impact of initial founding conditions and decisions upon the performance of new bank start-ups. Journal of Business Venturing 15: 253–77. [Google Scholar] [CrossRef]

- Bradley, Steven W., Dean A. Shepherd, and Johan Wiklund. 2011. The importance of slack for new organizations facing ‘tough’environments. Journal of Management Studies 48: 1071–97. [Google Scholar] [CrossRef]

- Chandler, Gaylen N., Benson Honig, and Johan Wiklund. 2005. Antecedents, moderators, and performance consequences of membership change in new venture teams. Journal of Business Venturing 20: 705–25. [Google Scholar] [CrossRef]

- Chang, Sea-Jin, Chi-Nien Chung, and Ishtiaq P. Mahmood. 2006. When and how does business group affiliation promote firm innovation? A tale of two emerging economies. Organization Science 17: 637–56. [Google Scholar] [CrossRef] [Green Version]

- Choi, Young Rok, and Dean A. Shepherd. 2004. Entrepreneurs’ decisions to exploit opportunities. Journal of Management 30: 377–95. [Google Scholar] [CrossRef]

- Choi, Young Rok, Shaker A. Zahra, Toru Yoshikawa, and Bong H. Han. 2015. Family ownership and R&D investment: The role of growth opportunities and business group membership. Journal of Business Research 68: 1053–61. [Google Scholar] [CrossRef]

- Chrisman, James J., and Pankaj C. Patel. 2012. Variations in R&D investments of family and nonfamily firms: Behavioral agency and myopic loss aversion perspectives. Academy of Management Journal 55: 976–97. [Google Scholar] [CrossRef]

- Coff, Russell W. 1999. When competitive advantage doesn’t lead to performance: The resource-based view and stakeholder bargaining power. Organization Science 10: 119–33. [Google Scholar] [CrossRef]

- Cooper, Arnold C., and Albert V. Bruno. 2000. Success among high technology firms. In Small Business: Critical Perspectives on Business Management. London and New York: Routledge, pp. 1183–91. [Google Scholar]

- Cooper, Arnold C., F. Javier Gimeno-Gascon, and Carolyn Y. Woo. 1994. Initial human and financial capital as predictors of new venture performance. Journal of Business Venturing 9: 371–95. [Google Scholar] [CrossRef]

- Cope, Jason. 2005. Toward a dynamic learning perspective of entrepreneurship. Entrepreneurship Theory Practice 29: 373–97. [Google Scholar] [CrossRef]

- Costa, Joana, Aurora A. C. Teixeira, and Anabela Botelho. 2020. Persistence in innovation and innovative behavior in unstable environments. International Journal of Systematic Innovation 6: 1–19. [Google Scholar] [CrossRef]

- Cummings, Trey, and Anne Marie Knott. 2018. Outside CEOs and innovation. Strategic Management Journal 39: 2095–119. [Google Scholar] [CrossRef]

- Dai, Guangrong, Kenneth P. De Meuse, and Dee Gaeddert. 2011. Onboarding externally hired executives: Avoiding derailment–accelerating contribution. Journal of Management & Organization 17: 165–78. [Google Scholar] [CrossRef]

- Dai, Shengli, Yingchun Li, and Wei Zhang. 2019. Personality traits of entrepreneurial top management team members and new venture performance. Social Behavior and Personality: An International Journal 47: 1–15. [Google Scholar] [CrossRef]

- De Cock, Robin, Petra Andries, and Bart Clarysse. 2021. How founder characteristics imprint ventures’ internationalization processes: The role of international experience and cognitive beliefs. Journal of World Business 56: 101163. [Google Scholar] [CrossRef]

- Deb, Palash, and Johan Wiklund. 2017. The effects of CEO founder status and stock ownership on entrepreneurial orientation in small firms. Journal of Small Business Management 55: 32–55. [Google Scholar] [CrossRef]

- Delmar, Frédéric, and Scott Shane. 2006. Does experience matter? The effect of founding team experience on the survival and sales of newly founded ventures. Strategic Organization 4: 215–47. [Google Scholar] [CrossRef]

- Dencker, John C., and Marc Gruber. 2015. The effects of opportunities and founder experience on new firm performance. Strategic Management Journal 36: 1035–52. [Google Scholar] [CrossRef]

- Dess, Gregory G., and Jason D. Shaw. 2001. Voluntary turnover, social capital, and organizational performance. Academy of Management Review 26: 446–56. [Google Scholar] [CrossRef]

- Eisenhardt, Kathleen M., and Claudia Bird Schoonhoven. 1990. Organizational growth: Linking founding team, strategy, environment, and growth among US semiconductor ventures, 1978–1988. Administrative Science Quarterly 35: 504–29. [Google Scholar] [CrossRef]

- Ensley, Michael D., Allison W. Pearson, and Allen C. Amason. 2002. Understanding the dynamics of new venture top management teams: Cohesion, conflict, and new venture performance. Journal of Business Venturing 17: 365–86. [Google Scholar] [CrossRef]

- Eva, Nathan, Alexander Newman, Qing Miao, Brian Cooper, and Kendall Herbert. 2019. Chief executive officer participative leadership and the performance of new venture teams. International Small Business Journal 37: 69–88. [Google Scholar] [CrossRef]

- Forés, Beatriz, and César Camisón. 2016. Does incremental and radical innovation performance depend on different types of knowledge accumulation capabilities and organizational size? Journal of Business Research 69: 831–48. [Google Scholar] [CrossRef] [Green Version]

- García-García, Raquel, Esteban García-Canal, and Mauro F. Guillén. 2017. Rapid internationalization and long-term performance: The knowledge link. Journal of World Business 52: 97–110. [Google Scholar] [CrossRef]

- Garms, Florian Peter, and Andreas Engelen. 2019. Innovation and R&D in the upper echelons: The association between the CTO’s power depth and breadth and the TMT’s commitment to innovation. Journal of Product Innovation Management 36: 87–106. [Google Scholar] [CrossRef] [Green Version]

- Gartner, William B., Barbara J. Bird, and Jennifer A. Starr. 1992. Acting as if: Differentiating entrepreneurial from organizational behavior. Entrepreneurship Theory and Practice 16: 13–32. [Google Scholar] [CrossRef]

- Geletkanycz, Marta A., and Donald C. Hambrick. 1997. The external ties of top executives: Implications for strategic choice and performance. Administrative Science Quarterly, 654–81. [Google Scholar] [CrossRef]

- Hashai, Niron, and Shaker Zahra. 2021. Founder team prior work experience: An asset or a liability for startup growth? Strategic Entrepreneurship Journal 16: 155–84. [Google Scholar] [CrossRef]

- Hemmert, Martin, Adam R. Cross, Ying Cheng, Jae-Jin Kim, Masahiro Kotosaka, Franz Waldenberger, and Leven J. Zheng. 2021. New venture entrepreneurship and context in East Asia: A systematic literature review. Asian Business Management, 1–35. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Michael A. Hitt, Richard A. Johnson, and Wayne Grossman. 2002. Conflicting voices: The effects of institutional ownership heterogeneity and internal governance on corporate innovation strategies. Academy of Management Journal 45: 697–716. [Google Scholar] [CrossRef]

- Johnson, Victoria. 2007. What is organizational imprinting? Cultural entrepreneurship in the founding of the Paris Opera. American Journal of Sociology 113: 97–127. [Google Scholar] [CrossRef]

- Klein, Howard J., and Paul W. Mulvey. 1995. Two investigations of the relationships among group goals, goal commitment, cohesion, and performance. Organizational Behavior Human Decision Processes 61: 44–53. [Google Scholar] [CrossRef]

- Kor, Yasemin Y. 2006. Direct and interaction effects of top management team and board compositions on R&D investment strategy. Strategic Management Journal 27: 1081–99. [Google Scholar] [CrossRef]

- Kor, Yasemin Y., and Andrea Mesko. 2013. Dynamic managerial capabilities: Configuration and orchestration of top executives’ capabilities and the firm’s dominant logic. Strategic Management Journal 34: 233–44. [Google Scholar] [CrossRef]

- Landstrom, Hans, and Donald L. Sexton. 2000. The Blackwell Handbook of Entrepreneurship. Oxford: Blackwell Business. [Google Scholar]

- Lester, Richard H., S. Trevis Certo, Catherine M. Dalton, Dan R. Dalton, and Albert A. Cannella Jr. 2006. Initial public offering investor valuations: An examination of top management team prestige and environmental uncertainty. Journal of Small Business Management 44: 1–26. [Google Scholar] [CrossRef]

- Mathias, Blake D., David W. Williams, and Adam R. Smith. 2015. Entrepreneurial inception: The role of imprinting in entrepreneurial action. Journal of Business Venturing 30: 11–28. [Google Scholar] [CrossRef]

- McDougall, Patricia Phillips, Jeffrey G. Covin, Richard B. Robinson Jr., and Lanny Herron. 1994. The effects of industry growth and strategic breadth on new venture performance and strategy content. Strategic Management Journal 15: 537–54. [Google Scholar] [CrossRef]

- Menz, Markus. 2012. Functional top management team members: A review, synthesis, and research agenda. Journal of Management 38: 45–80. [Google Scholar] [CrossRef]

- Nielsen, Sabina. 2010. Top management team internationalization and firm performance. Management International Review 50: 185–206. [Google Scholar] [CrossRef]

- O’brien, Robert M. 2007. A caution regarding rules of thumb for variance inflation factors. Quality & Quantity 41: 673–90. [Google Scholar] [CrossRef]

- Qian, Cuili, Qing Cao, and Riki Takeuchi. 2013. Top management team functional diversity and organizational innovation in China: The moderating effects of environment. Strategic Management Journal 34: 110–20. [Google Scholar] [CrossRef]

- Roberts, Edward B. 1991. The technological base of the new enterprise. Research Policy 20: 283–98. [Google Scholar] [CrossRef] [Green Version]

- Shane, Scott. 2000. Prior knowledge and the discovery of entrepreneurial opportunities. Organization Science 11: 448–69. [Google Scholar] [CrossRef]

- Shane, Scott, and Sankaran Venkataraman. 2000. The promise of entrepreneurship as a field of research. Academy of Management Review 25: 217–26. [Google Scholar] [CrossRef] [Green Version]

- Shepherd, Dean A., Andrew Zacharakis, and Robert A. Baron. 2003. VCs’ decision processes: Evidence suggesting more experience may not always be better. Journal of Business Venturing 18: 381–401. [Google Scholar] [CrossRef]

- Simon, Herbert A. 1978. Administrative Behavior. New York: The Free Press. [Google Scholar]

- Smith, Ken G., Ken A. Smith, Judy D. Olian, Henry P. Sims Jr., Douglas P. OBannon ’, and Judith A. Scully. 1994. Top management team demography and process: The role of social integration and communication. Administrative Science Quarterly 17: 412–38. [Google Scholar] [CrossRef]

- Suarez, Diana. 2014. Persistence of innovation in unstable environments: Continuity and change in the firm’s innovative behavior. Research Policy 43: 726–36. [Google Scholar] [CrossRef]

- Tribo, Josep A., Pascual Berrone, and Jordi Surroca. 2007. Do the type and number of blockholders influence R&D investments? New evidence from Spain. Corporate Governance: An International Review 15: 828–42. [Google Scholar] [CrossRef] [Green Version]

- Tzabbar, Daniel, and Jaclyn Margolis. 2017. Beyond the startup stage: The founding team’s human capital, new venture’s stage of life, founder–CEO duality, and breakthrough innovation. Organization Science 28: 857–72. [Google Scholar] [CrossRef]

- Welter, Friederike, Ted Baker, David B. Audretsch, and William B. Gartner. 2017. Everyday Entrepreneurship—A Call for Entrepreneurship Research to Embrace Entrepreneurial Diversity. Entrepreneurship Theory and Practice 41: 311–21. [Google Scholar] [CrossRef]

- Westhead, Paul, Deniz Ucbasaran, and Mike Wright. 2005. Decisions, actions, and performance: Do novice, serial, and portfolio entrepreneurs differ? Journal of Small Business Management 43: 393–417. [Google Scholar] [CrossRef]

- Xiong, Ran, Ping Wei, Jingyi Yang, and Luis Antonio Cristofini. 2021. Impact of top executive turnover on firms’ R&D investment: Evidence from China. Innovation 23: 400–24. [Google Scholar] [CrossRef]

| Variable | Mean | St. Dev. | Min | Max |

|---|---|---|---|---|

| R&D intensity | 0.15 | 0.26 | 0 | 1.04 |

| Executive turnover | 0.02 | 0.13 | 0 | 2 |

| Work experience | 11.50 | 7.85 | 0 | 40 |

| Business group experience | 0.16 | 0.37 | 0 | 1 |

| Founding experience | 0.26 | 0.63 | 0 | 6 |

| Firm size | 7.58 | 1.44 | 2.04 | 12.95 |

| ROA | 0.01 | 0.12 | −0.30 | 0.14 |

| Debt ratio | 0.72 | 0.85 | −23.88 | 0.99 |

| Age | 5.51 | 1.33 | 2 | 7 |

| Capital financing | 0.27 | 0.93 | 0 | 13.32 |

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. R&D intensity | |||||||||

| 2. Executive turnover | −0.01 | ||||||||

| 3. Work experience | −0.03 | 0.09 * | |||||||

| 4. Business group experience | −0.02 | 0.04 | 0.08 * | ||||||

| 5. Founding experience | 0.04 * | 0.03 | 0.11 * | −0.06 * | |||||

| 6. Firm size | −0.33 * | −0.06 * | 0.03 | 0.06 * | −0.00 | ||||

| 7. ROA | −0.42 * | −0.04 | 0.07 * | −0.01 | −0.05 * | 0.12 * | |||

| 8. Debt ratio | −0.17 * | −0.03 | 0.06 * | 0.01 | −0.04 * | 0.24 * | 0.25 * | ||

| 9. Age | −0.14 * | −0.04 | −0.03 | 0.03 | −0.04 | 0.21 * | 0.02 | 0.03 | |

| 10. Capital financing | 0.26 * | 0.02 | −0.08 * | −0.02 | 0.06 * | −0.27 * | −0.11 * | −0.42 * | −0.17 * |

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| Executive turnover | −0.062 ** | −0.105 ** | −0.083 ** | −0.067 ** |

| (0.010) | (0.006) | (0.001) | (0.008) | |

| Executive turnover × Work experience | 0.005 ** | |||

| (0.009) | ||||

| Executive turnover × Business group experience | 0.084 † | |||

| (0.094) | ||||

| Executive turnover × Founding experience | 0.019 * | |||

| (0.047) | ||||

| Work experience | 0.001 † | |||

| (0.097) | ||||

| Business group experience | 0.001 | |||

| (0.105) | ||||

| Founding experience | 0.001 | |||

| (0.143) | ||||

| Firm size | −0.033 *** | −0.026 *** | −0.033 *** | −0.033 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ROA | −0.646 *** | −0.341 *** | −0.646 *** | −0.647 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Debt ratio | −0.033 | −0.023 * | −0.033 | −0.034 |

| (0.187) | (0.032) | (0.188) | (0.186) | |

| Age | −0.004 | −0.001 | −0.004 | −0.004 |

| (0.428) | (0.707) | (0.416) | (0.434) | |

| Capital financing | 0.197 *** | 0.112 *** | 0.197 *** | 0.197 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Constant | 0.399 *** | 0.301 *** | 0.399 *** | 0.399 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ∆R2 | 0.255 | 0.273 | 0.254 | 0.254 |

| F value | 23.92 | 30.13 | 18.56 | 18.09 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cho, H.; Lee, P.; Shin, C.H. Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment. Economies 2022, 10, 97. https://doi.org/10.3390/economies10050097

Cho H, Lee P, Shin CH. Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment. Economies. 2022; 10(5):97. https://doi.org/10.3390/economies10050097

Chicago/Turabian StyleCho, Hyejin, Pyoungsoo Lee, and Choong Ho Shin. 2022. "Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment" Economies 10, no. 5: 97. https://doi.org/10.3390/economies10050097

APA StyleCho, H., Lee, P., & Shin, C. H. (2022). Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment. Economies, 10(5), 97. https://doi.org/10.3390/economies10050097