State-Dependent Stock Liquidity Premium: The Case of the Warsaw Stock Exchange

Abstract

1. Introduction

2. Literature Overview

3. Methodology and Data

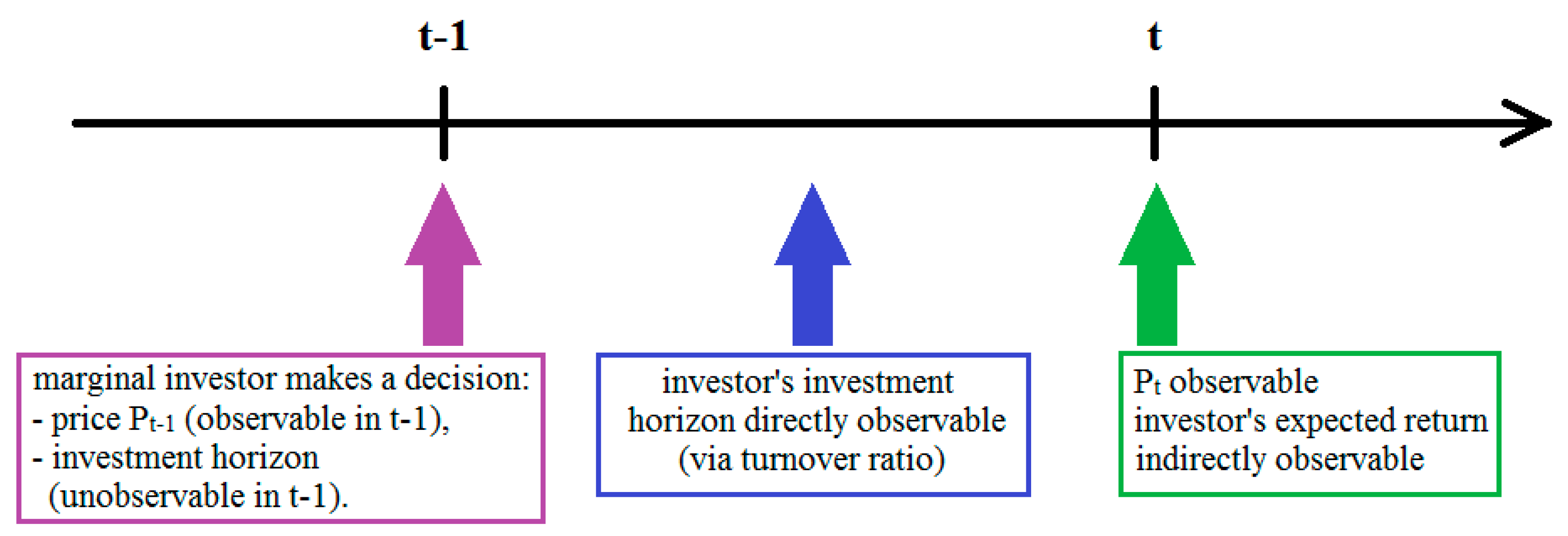

3.1. Empirical Framework and Hypotheses Development

3.2. Variables

- raw returns:

- excess returns:

- CAPM-adjusted returns:

- FF3-adjusted returns:

- Carhart-adjusted returns:

- natural logarithm of the market value of equity (ln(MV))—to take into account the size effect (Fama and French 1992, 1993),

- book-to-market value of equity (BV/MV)—to take into account the effect of company’s value (Fama and French 1992, 1993),

- dividend yield (DY)—to control for the effect of liquidity on dividend policy (Banerjee et al. 2007; Griffin 2010; Igan et al. 2011; Stereńczak 2018b),

- cumulative return from the last twelve months (rt-12-t-1)—reflecting the momentum effect (Jegadeesh and Titman 1993),

- standard deviation of monthly returns from the last 36 months (σ) or the standard error of residuals from estimated pricing model (σε)—reflecting stock risk and stock residual risk respectively.

3.3. Data

4. Empirical Results

4.1. Liquidity Premium in the Warsaw Stock Exchange

4.2. Liquidity Premium During the Bull and the Bear Market

5. Robustness Tests

5.1. Accounting for Endogeneity: DiD Approach

5.2. Application of Different Liquidity Measures

5.3. Determination of Unexpected Liquidity

5.4. Methods of Estimation

5.5. Determination of Bull and Bear Market Phases

6. Concluding Remarks

Funding

Acknowledgments

Conflicts of Interest

References

- Acharya, Viral V., and Lasse Heje Pedersen. 2005. Asset pricing with liquidity risk. Journal of Financial Economics 77: 375–410. [Google Scholar] [CrossRef]

- Aït-Sahalia, Yacine, and Jialin Yu. 2009. High frequency market microstructure noise estimates and liquidity measures. The Annals of Applied Statistics 3: 422–57. [Google Scholar] [CrossRef]

- Amihud, Yakov. 2002. Illiquidity and stock returns. Cross-section and time-series effects. Journal of Financial Markets 5: 31–56. [Google Scholar] [CrossRef]

- Amihud, Yakov. 2014. The pricing of the illiquidity factor’s systematic risk. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Amihud, Yakov, Allaudeen Hameed, Wenjin Kang, and Huiping Zhang. 2015. The illiquidity premium: International evidence. Journal of Financial Economics 117: 350–68. [Google Scholar] [CrossRef]

- Amihud, Yakov, and Haim Mendelson. 1986. Asset pricing and the bid-ask spread. Journal of Financial Economics 17: 223–49. [Google Scholar] [CrossRef]

- Amihud, Yakov, Haim Mendelson, and Lasse Heje Pedersen. 2005. Liquidity and asset prices. Foundations and Trends in Finance 1: 269–364. [Google Scholar] [CrossRef]

- Anginer, Deniz. 2010. Liquidity clienteles: Transaction Costs and Investment Decisions of Individual Investors. Policy Research Working Paper No. 5318. New York: World Bank. Available online: https://ssrn.com/abstract=1616476 (accessed on 4 May 2016).

- Asparouhova, Elena, Hendrik Bessembinder, and Ivalina Kalcheva. 2010. Liquidity biases in asset pricing tests. Journal of Financial Economics 96: 215–37. [Google Scholar] [CrossRef]

- Atkins, Allen B., and Edward A. Dyl. 1997. Transactions Costs and Holding Periods for Common Stocks. Journal of Finance 52: 309–25. [Google Scholar] [CrossRef]

- Avramov, Doron, and Tarun Chordia. 2006. Asset pricing models and financial market anomalies. Review of Financial Studies 19: 1001–40. [Google Scholar] [CrossRef]

- Banerjee, Suman, Vladimir A. Gatchev, and Paul A. Spindt. 2007. Stock market liquidity and firm dividend policy. Journal of Financial and Quantitative Analysis 42: 369–97. [Google Scholar] [CrossRef]

- Batten, Jonathan A., and Xuan Vinh Vo. 2015. Liquidity and Return Relationships in an Emerging Market. Emerging Markets Finance and Trade 50: 5–21. [Google Scholar] [CrossRef]

- Bekaert, Geert, Campbell R. Harvey, and Christian Lundblad. 2007. Liquidity and Expected Returns: Lessons from Emerging Markets. Review of Financial Studies 20: 1783–831. [Google Scholar] [CrossRef]

- Belkhir, Mohamed, Mohsen Saad, and Anis Samet. 2018. Stock extreme liquidity and the cost of capital. Journal of Banking and Finance. [Google Scholar] [CrossRef]

- Ben-Rephael, Azi, Ohad Kadan, and Avi Wohl. 2015. The diminishing liquidity premium. Journal of Financial and Quantitative Analysis 50: 197–229. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara. 2016. Liquidity Dynamics around Jumps: The Evidence from the Warsaw Stock Exchange. Emerging Markets Finance and Trade 52: 2740–55. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara. 2017. How jumps affect liquidity? Evidence from Poland. Czech Journal of Economics and Finance (Finance a úvěr) 67: 39–52. [Google Scholar]

- Będowska-Sójka, Barbara. 2018. The coherence of liquidity measures. The evidence from the emerging market. Finance Research Letters 27: 118–23. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara., and Agata Kliber. 2019. The causality between liquidity and volatility in the Polish stock market. Finance Research Letters 30: 110–15. [Google Scholar] [CrossRef]

- Brennan, Michael J., and Avanidhar. Subrahmanyam. 1996. Market microstructure and asset pricing: On the compensation for illiquidity in stock returns. Journal of Financial Economics 41: 441–64. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., and Lasse Heje Pedersen. 2009. Market Liquidity and Funding Liquidity. Review of Financial Studies 22: 2201–38. [Google Scholar] [CrossRef]

- Carhart, Mark M. 1997. On Persistence in Mutual Fund Performance. Journal of Finance 52: 57–82. [Google Scholar] [CrossRef]

- Chalmers, John M. R., and Gregory B. Kadlec. 1998. An empirical examination of the amortized spread. Journal of Financial Economics 48: 159–88. [Google Scholar] [CrossRef]

- Chen, Nai-Fu, and Raymond Kan. 1995. Expected Return and the Bid-Ask Spread. Working Paper Series No. 265. Chicago: University of Chicago. [Google Scholar]

- Chiang, Thomas C., and Dazhi Zheng. 2015. Liquidity and stock returns: Evidence from international markets. Global Finance Journal 27: 73–97. [Google Scholar] [CrossRef]

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2001. Market liquidity and trading activity. Journal of Finance 56: 501–30. [Google Scholar] [CrossRef]

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2003. Determinants of daily fluctuations of liquidity and trading activity. Latin American Journal of Economics 40: 728–51. [Google Scholar] [CrossRef]

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2011. Recent trends in trading activity and market quality. Journal of Financial Economics 101: 243–63. [Google Scholar] [CrossRef]

- Chordia, Tarun, Lakshmanan Shivakumar, and Avanidhar Subrahmanyam. 2004. Liquidity dynamics across small and large firms. Economic Notes 33: 111–43. [Google Scholar] [CrossRef]

- Chordia, Tarun, and Avanidhar Subrahmanyam. 2004. Order imbalance and individual stock returns: Theory and evidence. Journal of Financial Economics 72: 485–518. [Google Scholar] [CrossRef]

- Chulia, Helena, Christoph Koser, and Jorge M. Uribe. 2019. Analyzing the Nonlinear Pricing of Liquidity Risk according to Market States. Working Paper 2019/16. Barcelona: Research Institute of Applied Economics. Available online: https://editorialexpress.com/cgi-bin/conference/download.cgi?db_name=27finforum&paper_id=139 (accessed on 19 December 2019).

- Constantinides, George M. 1986. Capital market equilibrium with transaction costs. Journal of Political Economy 94: 842–62. [Google Scholar] [CrossRef]

- Datar, Vinay T., Narayan Y. Naik, and Robert Radcliffe. 1998. Liquidity and stock returns: An alternative test. Journal of Financial Markets 1: 203–19. [Google Scholar] [CrossRef]

- Eleswarapu, Venkat R. 1997. Cost of transacting and expected returns in the Nasdaq market. Journal of Finance 52: 2113–27. [Google Scholar] [CrossRef]

- Eleswarapu, Venkat R., and Marc R. Reinganum. 1993. The seasonal behaviour of the liquidity premium in asset pricing. Journal of Financial Economics 34: 373–86. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1992. The cross-section of expected stock returns. Journal of Finance 47: 427–65. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1993. Common risk factors in the returns on stock and bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Fang, Vivian W., Xuan Tian, and Sheri Tice. 2014. Does Stock Liquidity Enhance or Impede Firm Innovation? Journal of Finance 69: 2085–125. [Google Scholar] [CrossRef]

- Florackis, Chris, Andros Gregoriou, and Alexandros Kostakis. 2011. Trading frequency and asset pricing on the London Stock Exchange: Evidence from a new price impact ratio. Journal of Banking & Finance 35: 3335–50. [Google Scholar] [CrossRef]

- Fong, Kingsley Y. L., Craig W. Holden, and Charles A. Trzcinka. 2017. What are the best liquidity proxies for global research? Review of Finance 21: 1355–401. [Google Scholar] [CrossRef]

- Gajdka, Jerzy, Agata Gniadkowska, and Tomasz Schabek. 2010. Płynność obrotu a stopa zwrotu z akcji na Giełdzie Papierów Wartościowych w Warszawie. Zeszyty Naukowe Uniwersytetu Ekonomicznego w Poznaniu 142: 597–605. [Google Scholar]

- Garsztka, Przemysław, and Anna Rutkowska-Ziarko. 2012. Budowa portfela akcji przy wykorzystaniu wskaźnika cena/zysk oraz płynności transakcyjnej. Zeszyty Naukowe Uniwersytetu Ekonomicznego w Poznaniu 242: 69–82. [Google Scholar]

- Gniadkowska, Agata. 2012. Wpływ płynności obrotu na kształtowanie się stopy zwrotu z akcji notowanych na Giełdzie Papierów Wartościowych w Warszawie. Zarządzanie i Finanse 10: 563–70. [Google Scholar]

- Gniadkowska-Szymańska, Agata. 2018. Płynność obrotu a stopa zwrotu z akcji notowanych na Giełdzie Papierów Wartościowych w Warszawie. Łódź: Wydawnictwo Uniwersytetu Łódzkiego. [Google Scholar]

- Goyenko, Ruslan. 2006. Stock and bond pricing with liquidity risk. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Griffin, Carroll Howard. 2010. Liquidity and dividend policy: International evidence. International Business Research 3: 3–9. [Google Scholar] [CrossRef]

- Grillini, Stefano, Aydin Ozkan, Abhijit Sharma, and Mazin A. M. Al Janabi. 2019. Pricing of time-varying illiquidity within the Eurozone: Evidence using a Markov switching liquidity-adjusted capital asset pricing model. International Review of Financial Analysis 64: 145–58. [Google Scholar] [CrossRef]

- Hagströmer, Bjorn, Bjorn Hansson, and Birger Nillson. 2013. The components of the illiquidity premium: An empirical analysis of US stocks 1927–2010. Journal of Banking & Finance 37: 4476–87. [Google Scholar] [CrossRef]

- Holden, Craig W., Stacey. Jacobsen, and Avanidhar Subrahmanyam. 2014. The empirical analysis of liquidity. Foundations and Trends in Finance 8: 263–365. [Google Scholar] [CrossRef]

- Huh, Sahn-Wook. 2014. Price impact and asset pricing. Journal of Financial Markets 19: 1–38. [Google Scholar] [CrossRef]

- Igan, Deniz, Aureo de Paula, and Marcelo Pinheiro. 2011. Liquidity and Dividend Policy. MPRA Paper No. 29409. Munich: Munich Personal RePEc Archive. Available online: https://mpra.ub.uni-muenchen.de/29409/1/MPRA_paper_29409.pdf (accessed on 9 March 2016).

- Jang, Jewoon, Jangkoo Kang, and Changjun Lee. 2015. State-Dependent Illiquidity Premium in the Korean Stock Market. Emerging Markets Finance and Trade 51: 400–17. [Google Scholar] [CrossRef]

- Jang, Jewoon, Jangkoo Kang, and Changjun Lee. 2017. State-Dependent Variations in the Expected Illiquidity Premium. Review of Finance 21: 2277–314. [Google Scholar] [CrossRef]

- Jegadeesh, Narasimhan, and Sheridan Titman. 1993. Returns to buying winners and selling losers: Implications for stock market efficiency. Journal of Finance 48: 65–91. [Google Scholar] [CrossRef]

- Jensen, Gerald R., and Theodore Moorman. 2010. Inter-temporal variation in the illiquidity premium. Journal of Financial Economics 98: 338–58. [Google Scholar] [CrossRef]

- Kyle, Albert S., and Anna A. Obizhaeva. 2016. Market microstructure invariance: Empirical hypotheses. Econometrica 84: 1345–404. [Google Scholar] [CrossRef]

- Lee, Kuan-Hui. 2011. The world price of liquidity risk. Journal of Financial Economics 99: 136–61. [Google Scholar] [CrossRef]

- Lischewski, Judith, and Svitlana Voronkova. 2012. Size, value and liquidity. Do they really matter on an emerging stock market? Emerging Markets Review 13: 8–25. [Google Scholar] [CrossRef]

- Liu, Weimin. 2006. A liquidity-augmented capital asset pricing model. Journal of Financial Economics 82: 631–71. [Google Scholar] [CrossRef]

- Machado, Marcio Andre Veras, and Otavio Ribeiro Medeiros. 2013. Does the Liquidity Effect Exist in the Brazilian Stock Market? SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Maheu, John M., and Thomas H. McCurdy. 2000. Identifying bull and bear markets in stock returns. Journal of Business and Economic Statistics 18: 100–12. [Google Scholar] [CrossRef]

- Næs, Randi, and Bernt Arne Ødegaard. 2009. Liquidity and asset pricing: Evidence on the role of investor holding period. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Nowak, Sabina. 2017. Order imbalance indicators in asset pricing: Evidence from the Warsaw Stock Exchange. In Contemporary Trends and Challenges in Finance: Proceedings from the 2nd Wroclaw International Conference in Finance (s. 91-102). Edited by Krzysztof Jajuga, Lucjan T. Orłowski and Karsten Staehr. Cham: Springer International Publishing. [Google Scholar] [CrossRef]

- Olbryś, Joanna. 2014. Is illiquidity risk priced? The case of Polish medium-size emerging stock market. Bank i Kredyt 45: 513–36. [Google Scholar]

- Pástor, Lubos., and Robert. F. Stambaugh. 2003. Liquidity risk and expected stock returns. Journal of Political Economy 111: 642–85. [Google Scholar] [CrossRef]

- Piotrowski, Sebastian. 2015. Model CAPM z ryzykiem płynności na polskim rynku kapitałowym. Zeszyty Naukowe Uniwersytetu Szczecińskiego. Współczesne Problemy Ekonomiczne. Globalizacja. Liberalizacja. Etyka 11: 195–208. [Google Scholar]

- Sadka, Ronnie. 2002. The Seasonality of Momentum: Analysis of Tradability. Northwestern University Department of Finance Working Paper No. 277. Evanston: Nortwestern University. [Google Scholar] [CrossRef]

- Stereńczak, Szymon. 2017. Stock market liquidity and returns on the Warsaw Stock Exchange: An introductory survey. Finanse, Rynki Finansowe, Ubezpieczenia 86: 363–74. [Google Scholar] [CrossRef]

- Stereńczak, Szymon. 2018a. Stock liquidity on the Warsaw Stock Exchange in the 21st century: Time-series and cross-sectional dependencies. Finanse, Rynki Finansowe, Ubezpieczenia 91: 281–92. [Google Scholar] [CrossRef][Green Version]

- Stereńczak, Szymon. 2018b. Stock market liquidity and company decisions to pay dividends: Evidence from the Warsaw Stock Exchange. In Contemporary Trends in Accounting, Finance and Financial Institutions: Proceedings from the International Conference on Accounting, Finance and Financial Institutions (ICAFFI). Edited by Jacek Mizerka and Taufiq Choudhry. Cham: Springer International Publishing, pp. 27–42. [Google Scholar] [CrossRef]

- Stereńczak, Szymon. 2019a. In Search of the Best Proxy for Liquidity in Asset Pricing Studies on the Warsaw Stock Exchange. In Effective Investments on Capital Market—Capital Market Effective Invesmtments (CMEI) 2018. Edited by Waldemar Tarczyński and Kesra Nermend. Cham: Springer International Publishing, pp. 33–52. [Google Scholar]

- Stereńczak, Szymon. 2019b. Stock Liquidity Premium with Stochastic Price Impact and exogenous Trading Strategy. International Review of Financial Analysis. [Google Scholar] [CrossRef]

- Stereńczak, Szymon, Adam Zaremba, and Zaghum Umar. 2020. Is There an Illiquidity Premium in Frontier Markets? Emerging Markets Review 42C: 100673. [Google Scholar] [CrossRef]

- Włosik, Katarzyna. 2017. Płynność przy wycenie akcji na Giełdzie Papierów Wartościowych w Warszawie. Ruch Prawniczy, Ekonomiczny i Socjologiczny LXXIX: 127–41. [Google Scholar] [CrossRef][Green Version]

- Yi, Hu, Li Yong, and Zeng Jianyu. 2018. Stock Liquidity and Corporate Cash Holdings. Finance Research Letters 28: 416–22. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Dependent Variable | M1 | M2 | M3 | M4 | M5 |

|---|---|---|---|---|---|

| Intercept | 0.116 *** | 0.054 *** | 0.058 *** | 0.081 *** | 0.097 *** |

| (10.79) | (4.967) | (5.170) | (7.347) | (8.152) | |

| lnMV | −0.019 *** | −0.019 *** | −0.017 *** | −0.016 *** | −0.020 *** |

| (11.82) | (11.51) | (10.06) | (9.647) | (11.00) | |

| BV/MV | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** |

| (3.297) | (3.451) | (3.737) | (3.340) | (2.984) | |

| DY | 0.000 | 0.001 | 0.004 | 0.004 | −0.002 |

| (0.025) | (0.083) | (0.351) | (0.371) | (0.126) | |

| rt−12−t−1 | 0.008 *** | 0.009 *** | 0.005 ** | 0.003 | 0.004 * |

| (4.021) | (4.350) | (2.369) | (1.499) | (1.867) | |

| σ | −0.082 *** | −0.081 *** | |||

| (3.747) | (3.772) | ||||

| σε | −0.069 *** | −0.045 * | −0.053 * | ||

| (2.749) | (1.713) | (1.839) | |||

| amFHTt−1 | 2.636 *** | 2.667 *** | 2.571 *** | 2.460 *** | 2.394 *** |

| (4.164) | (4.208) | (4.066) | (4.151) | (4.227) | |

| FHTU | −0.010 | −0.001 | −0.028 | 0.086 | 0.076 |

| (0.102) | (0.010) | (0.271) | (0.835) | (0.744) | |

| Stocks effects | YES | YES | YES | YES | YES |

| Months effects | YES | YES | YES | YES | YES |

| N | 41,110 | 41,117 | 41,146 | 41,142 | 41,140 |

| R2 | 0.209 | 0.076 | 0.075 | 0.030 | 0.033 |

| F | 25.293 | 24.525 | 18.457 | 17.933 | 20.737 |

| D−W | 1.980 | 1.986 | 1.983 | 1.996 | 1.973 |

| AIC | −55,844.32 | −55,798.82 | −54,825.37 | −52,419.18 | −50,496.79 |

| Dependent Variable | M1a | M1b | M1c | M1d | M1e |

|---|---|---|---|---|---|

| Intercept | 0.104 *** | 0.098 *** | 0.098 *** | 0.104 *** | 0.055 *** |

| (10.27) | (9.599) | (11.41) | (4.955) | (3.096) | |

| lnMV | −0.019 *** | −0.018 *** | −0.018 *** | −0.023 *** | −0.023 *** |

| (11.82) | (11.31) | (16.45) | (6.772) | (10.25) | |

| BV/MV | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 | 0.001 *** |

| (3.297) | (3.297) | (5.291) | (0.969) | (3.577) | |

| DY | 0.000 | 0.000 | 0.003 | −0.033 | 0.004 |

| (0.025) | (0.025) | (0.274) | (1.400) | (0.379) | |

| rt−12−t−1 | 0.008 *** | 0.008 *** | 0.008 *** | −0.000 | 0.007 ** |

| (4.021) | (4.021) | (5.359) | (0.008) | (2.404) | |

| σ | −0.220 *** | −0.071 ** | |||

| (4.936) | (2.389) | ||||

| σortog_amFHT | −0.082 *** | ||||

| (3.747) | |||||

| σortog_lnMV | −0.082 *** | ||||

| (3.747) | |||||

| amFHTt−1 | 2.441 *** | 2.636 *** | 2.579 *** | 4.409 ** | 2.351 *** |

| (3.920) | (4.164) | (13.63) | (2.489) | (3.849) | |

| FHTU | −0.010 | −0.010 | 0.021 | 0.492 ** | −0.088 |

| (0.102) | (0.102) | (0.335) | (2.202) | (0.759) | |

| Stocks effects | YES | YES | YES | YES | YES |

| Months effects | YES | YES | YES | YES | YES |

| N | 41110 | 41110 | 41110 | 10455 | 30655 |

| R2 | 0.209 | 0.209 | 0.209 | 0.269 | 0.180 |

| F | 25.293 | 25.293 | 66.205 | 13.548 | 20.000 |

| D−W | 1.980 | 1.980 | 1.982 | 1.901 | 2.010 |

| AIC | −55,844.32 | −55,844.32 | −55,819.27 | −12,110.91 | −44,050.55 |

| Dependent Variable | M6 | M7 | M8 | M9 | M10 |

|---|---|---|---|---|---|

| Intercept | 0.115 *** | 0.054 *** | 0.057 *** | 0.081 *** | 0.097 *** |

| (10.78) | (4.947) | (5.158) | (7.346) | (8.154) | |

| lnMV | −0.019 *** | −0.019 *** | −0.017 *** | −0.016 *** | −0.020 *** |

| (11.82) | (11.52) | (10.07) | (9.655) | (11.01) | |

| BV/MV | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.0004 *** |

| (3.309) | (3.461) | (3.742) | (3.330) | (2.973) | |

| DY | 0.000 | 0.001 | 0.004 | 0.004 | −0.002 |

| (0.019) | (0.077) | (0.345) | (0.368) | (0.128) | |

| rt−12−t−1 | 0.008 *** | 0.009 *** | 0.005 ** | 0.003 | 0.004 * |

| (3.946) | (4.270) | (2.288) | (1.453) | (1.826) | |

| σ | −0.082 *** | −0.081 *** | |||

| (3.741) | (3.762) | ||||

| σε | −0.067 *** | −0.045 * | −0.053 * | ||

| (2.750) | (1.718) | (1.844) | |||

| amFHTt−1*H | 2.648 *** | 2.660 *** | 2.523 *** | 2.392 *** | 2.349 *** |

| (3.816) | (3.855) | (3.678) | (3.723) | (3.804) | |

| amFHTt−1*B | 2.501 ** | 2.653 ** | 2.851 ** | 2.919 ** | 2.690 ** |

| (2.569) | (2.426) | (2.463) | (2.410) | (2.469) | |

| FHTU*H | −0.093 | −0.081 | −0.110 | 0.037 | 0.032 |

| (0.860) | (0.733) | (0.990) | (0.340) | (0.291) | |

| FHTU*B | 0.575 ** | 0.082 ** | 0.542 ** | 0.414 * | 0.378 |

| (2.412) | (2.446) | (2.293) | (1.371) | (1.556) | |

| Stocks effects | YES | YES | YES | YES | YES |

| Months effects | YES | YES | YES | YES | YES |

| N | 41,110 | 41,117 | 41,146 | 41,142 | 41,140 |

| R2 | 0.209 | 0.076 | 0.075 | 0.030 | 0.033 |

| F | 21.107 | 20.177 | 15.852 | 14.590 | 16.516 |

| D−W | 1.981 | 1.986 | 1.983 | 1.996 | 1.973 |

| AIC | −55,853.02 | −55,807.00 | −54,833.85 | −52,420.07 | −50,496.28 |

| Panel A: Pre-Match and Post-Match Propensity | ||||

| Variable | Pre-Match | Post-Match | ||

| Intercept | −1.208 * | 0.215 | ||

| (1.837) | (0.800) | |||

| lnMV | 0.143 *** | −0.016 | ||

| (3.058) | (0.8045) | |||

| BV/MV | −0.007 | −0.045 | ||

| (0.669) | (0.379) | |||

| rt−12−t−1 | 0.145 | 0.067 | ||

| (0.437) | (0.800) | |||

| σ | −2.286 | 0.640 | ||

| (0.247) | (0.810) | |||

| FHT | −1.040 | −1.812 | ||

| (0.628) | (0.667) | |||

| N | 222 | 110 | ||

| p-value of χ2 | 0.000 | 0.967 | ||

| pseudo-R2 | 0.091 | 0.006 | ||

| Panel B: Post-Matching Differences | ||||

| Variable | Treatment | Control | Difference | t-Statistic |

| lnMV | 11.193 | 11.253 | −0.06 | −0.1532 |

| .BV/MV | 1.4175 | 1.7221 | −0.3046 | −0.7701 |

| rt−12−t−1 | −0.21202 | −0.25052 | 0.0385 | 0.3831 |

| σ | 0.13734 | 0.13679 | 0.00055 | 0.0578 |

| FHT | 0.022066 | 0.024574 | −0.002508 | −0.4292 |

| Variable | (1) | (2) | (3) |

|---|---|---|---|

| Intercept | −0.065 *** (3.142) | −0.096 (1.173) | −0.081 (1.030) |

| Aftert | 0.154 *** (4.577) | 0.148 *** (4.639) | 0.164 *** (5.066) |

| Treatmenti | 0.050 * (1.690) | 0.052 * (1.751) | 0.051 * (1.698) |

| Aftert*Treatmenti | −0.060 (1.176) | −0.053 (1.050) | −0.074 (1.523) |

| Control | NO | YES | YES |

| FHT | NO | NO | YES |

| N | 220 | 220 | 220 |

| R2 | 0.114 | 0.117 | 0.131 |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Stereńczak, S. State-Dependent Stock Liquidity Premium: The Case of the Warsaw Stock Exchange. Int. J. Financial Stud. 2020, 8, 13. https://doi.org/10.3390/ijfs8010013

Stereńczak S. State-Dependent Stock Liquidity Premium: The Case of the Warsaw Stock Exchange. International Journal of Financial Studies. 2020; 8(1):13. https://doi.org/10.3390/ijfs8010013

Chicago/Turabian StyleStereńczak, Szymon. 2020. "State-Dependent Stock Liquidity Premium: The Case of the Warsaw Stock Exchange" International Journal of Financial Studies 8, no. 1: 13. https://doi.org/10.3390/ijfs8010013

APA StyleStereńczak, S. (2020). State-Dependent Stock Liquidity Premium: The Case of the Warsaw Stock Exchange. International Journal of Financial Studies, 8(1), 13. https://doi.org/10.3390/ijfs8010013