Ownership of Assets in Chinese Shipping Funds

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. The Issue of Ownership in a Chinese Shipping Fund

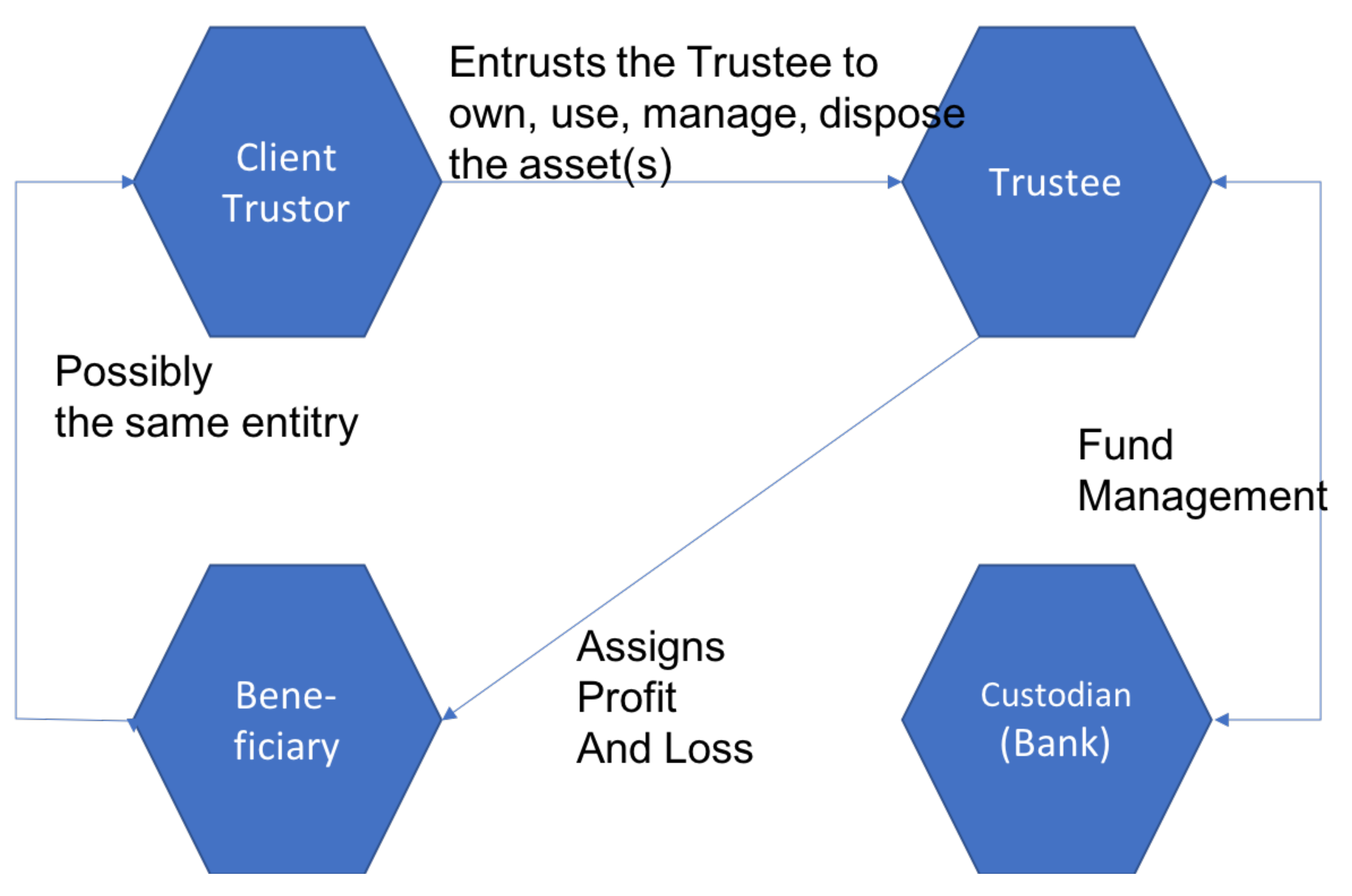

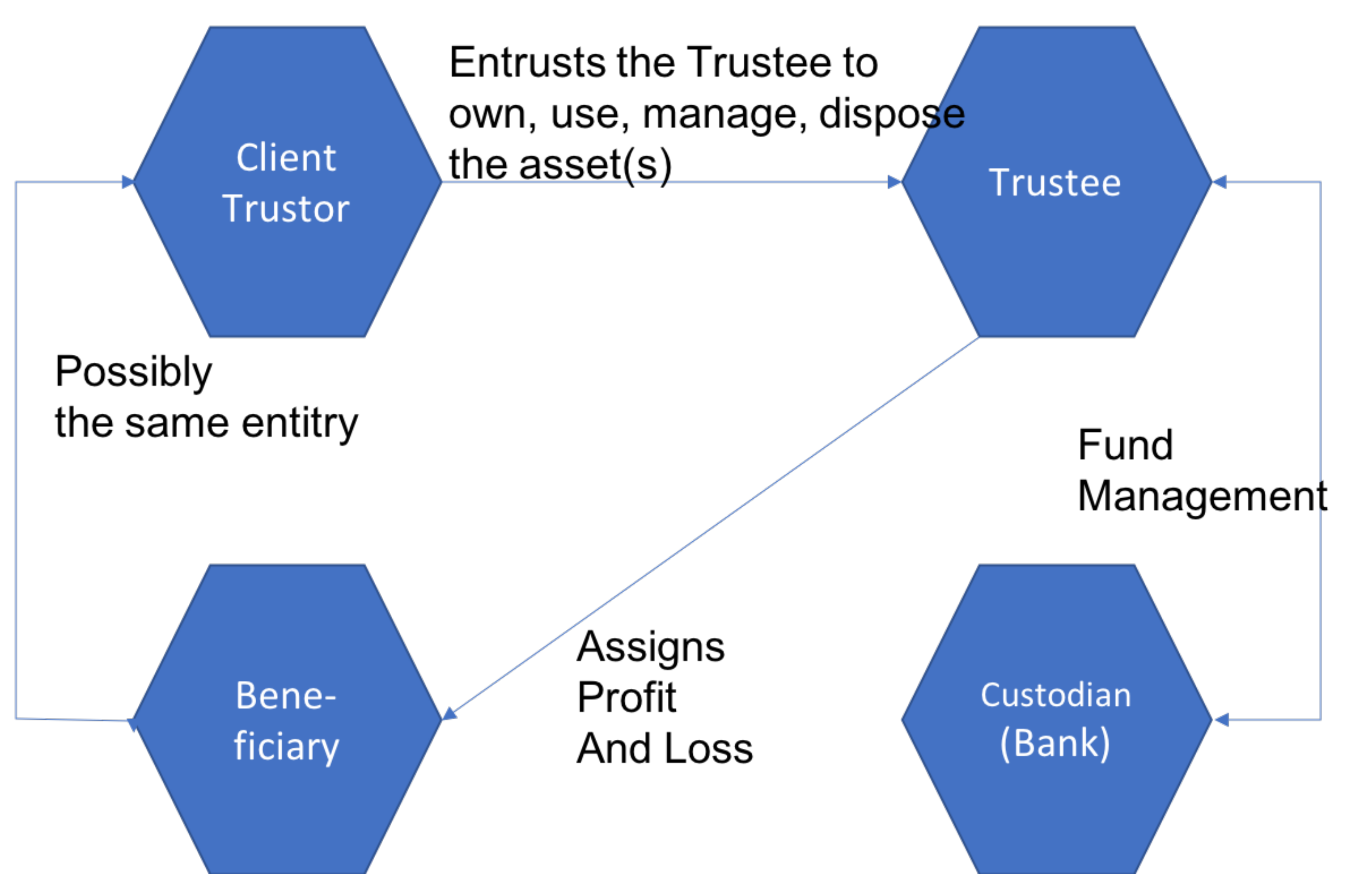

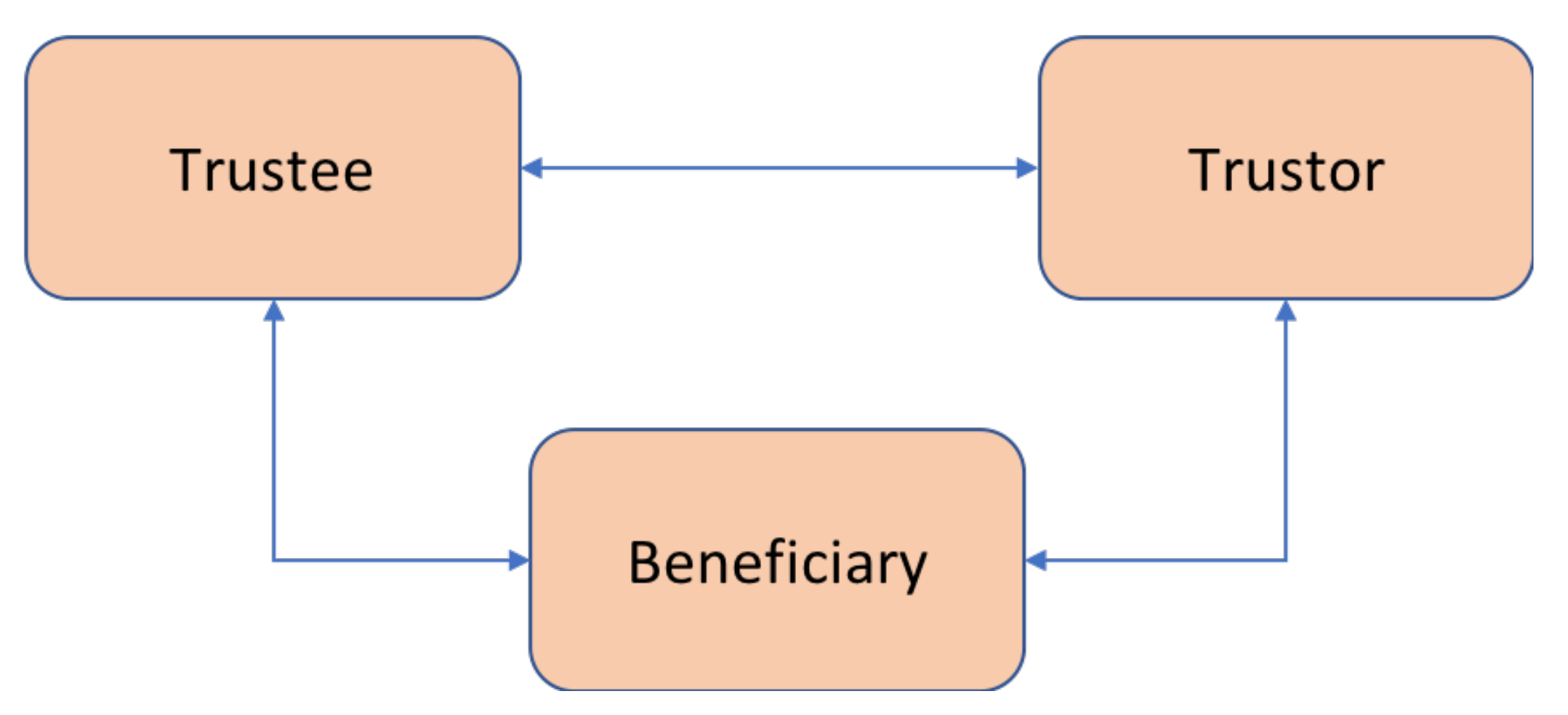

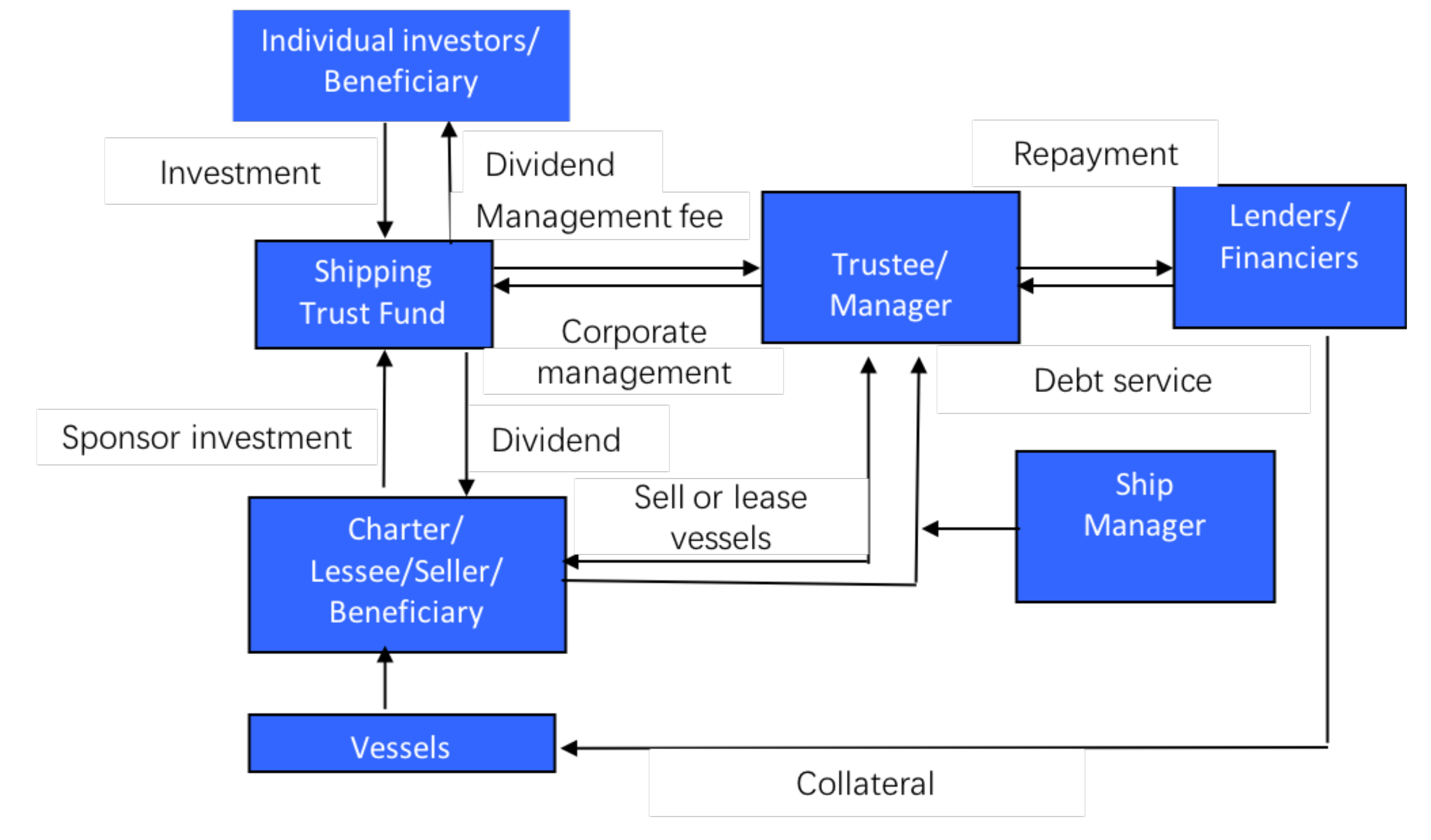

2.1. Introduction to Shipping Trusts in China

- The trust company and the fund management team are responsible for the work in which they are individually specialized—i.e., the trust company is only responsible for raising the trust fund capital from investors and plays a role of the trustee, while the fund management team as the manager of the trust fund is responsible for the specific operation and investment decision-making of the fund.

- The fund is dominated by the trust company—i.e., the trust company is responsible for the raising and management of the whole trust fund but usually recruits a fund management team as the external investment counselor to provide it with legal consultation services. However, Article 26 of China’s Regulations on Administration of Trust Companies stipulates: “The trust company should manage the trust affairs personally.” Therefore, under the Chinese law, the shipping trust fund should be operated in the mode of proprietary trading. However, trust companies are at the stage of conversion from the financing function to the management function; thus, they can recruit professional investment advisors to provide advices or guides for their investment decision-making in terms of assets, business, and technology to manage and operate the trust fund property. This not only guarantees that the trust company independently manages the trust property under the shipping trust fund, but also helps in the professional management of the trust property and gives full play to the financing and investment functions of the shipping trust fund in the shipping and finance fields.

2.2. Explaining the Current Framework

- According to the regulation of Article 97 of China’s current Property Law and Article 16 of Maritime Commerce Law, the disposal of property in common should be approved by more than 2/3rd of the co-owners; thus, the disposal of the ship by the trustee of the shipping trust fund should be approved by co-owners of the ship, which conflicts with the professional management and independent operation of the trustee and does not help to reduce investment costs of the trust property.

- If the client under the shipping trust fund places the cash under the trust fund of the trustee, the ownership of the cash should be transferred to the trustee when it is delivered to the trustee, because cash belongs to the generic good. But a practical problem is: If the trustee purchases ships with the capital, is the owner of the ship the client or the trustee? If the trustee is registered as the owner, does it conflict with the regulation of the current trust law, which specifies that that the client still enjoys the ownership?

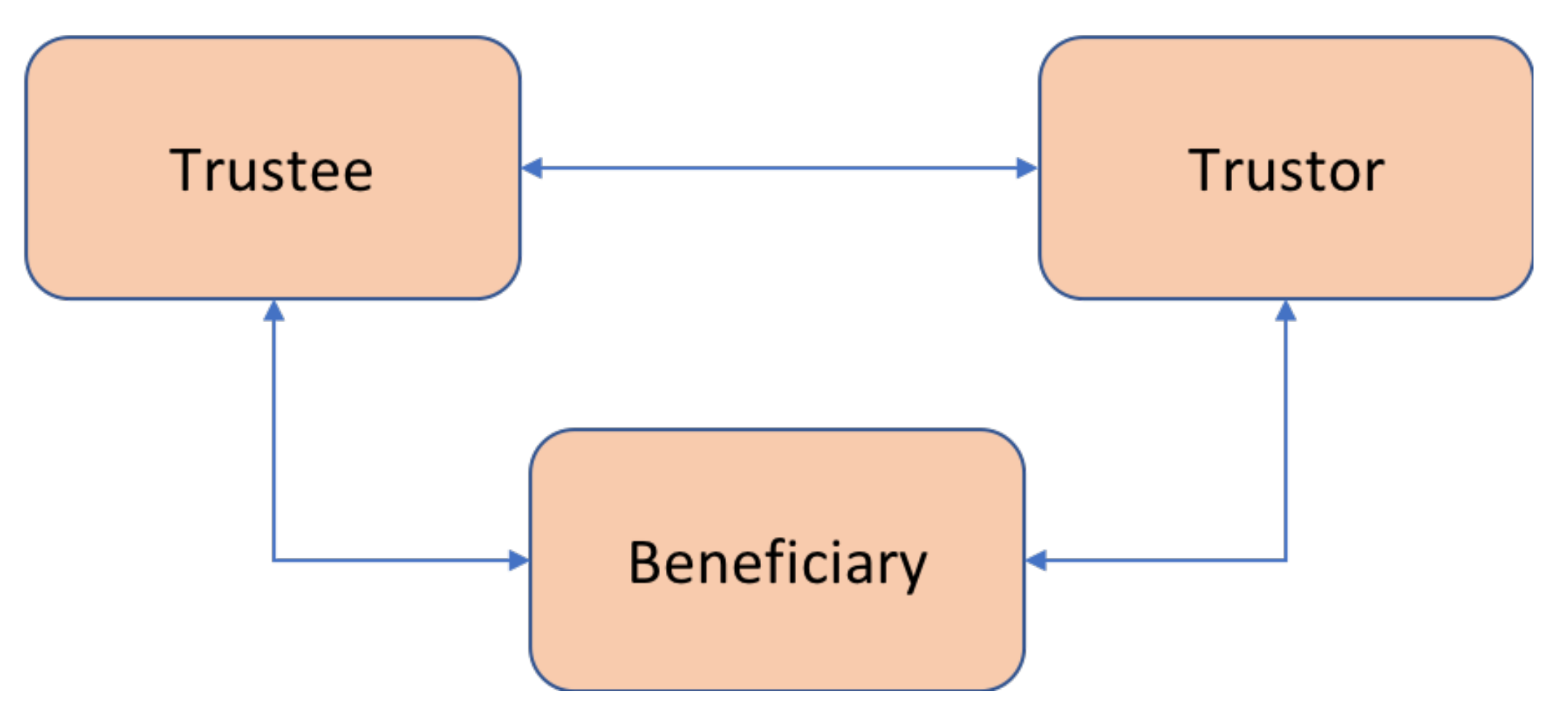

- If the ownership of the trust property is not transferred, it will not help in the establishment of the independent legal status of the trustee or guarantee the rights and interests of the beneficiary (Chen 2011). If the ownership of the trust property is not transferred, it will not be confirmed effectively whether the client has mortgaged the trust property to others or will not free assets from the effect of ownership claim effect. As a result, the non-client beneficiary trust under the current trust law exists in name only and significantly affects the execution scope of the right of revocation of the beneficiary, since the usufruct (the exclusive rights of the non-owner for including possessing, employing, and benefiting from others’ objects) of the beneficiary is not specified and both the client and the beneficiary have the right to revoke the trust (Article 22 and Article 49 of the Trust Law). This is likely to give rise to conflicts between their respective rights of revocation in the non-beneficiary trust (Edwards and Stockwell 2005).

- The trustee’s disposal of the trust property lacks basis. In the period during which the trust is in force, the trustee needs to dispose the trust property in his/her own name in order to realize the objectives of the trust, which requires the trustee to either possess the ownership of the trust property or obtain the authorization of the client. However, there is a large degree of contact with other units in the trust affairs and the counterparty changes frequently, making it impractical for the trustee to ask for the authorization of the client with respect to any a matter.

- In the case of the testamentary trust, the ownership of the trust property cannot be specified. According to the regulation of Paragraph 2, Article 8 of the Trust Law, the testamentary trust comes into effect after the client is dead, and a dead client will certainly not possess the ownership of the trust property, as stipulated in the General Principles of Civil Law. Hence, it conflicts with the regulation that the ownership of the trust property belongs to the client.

- There will be difficulties in the actual execution if the trust property belongs to the client. The trustee possesses only the rights of management and disposal and not the ownership; thus, the trustee cannot independently dispose the real estate in his/her own name, because the disposal of the real estate must happen on the basis of publicity of the property right registered.

3. Transferring the Asset; a Justification

3.1. A Chinese Contract Law Perspective

3.2. Effects of the Registration System and Solutions

3.3. The Justification of the Transfer

4. Conclusions

- Financial structures and compatibility of Chinese trusts for intra-jurisdictional projects;

- Use of securities, capital as well as consideration of risk and yield issues;

- Promotion of national shipping and relevant objectives through capital availability provided by shipping trusts;

- Evolution of the Chinese financial and shipping legal framework; and last but not least

- Understanding better China’s maritime strategy that impacts all relevant international markets.

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| KG | Kommanditgesellschaft (in German)—a limited partnership business entity in Germany |

| KS | Kommandittselskap (in Norwegian)—a limited partnership business entity in Germany |

References

- Chen, Xueping. 2011. Nature of rights of the beneficiary of trusts: Human rights or object-based rights. Studies in Law and Business 1: 78. [Google Scholar]

- Clarksons Research. 2019. Shipping Intelligence Network. Available online: https://sin.clarksons.net (accessed on 15 July 2019).

- Clausius, Philip. 2015. Ship Leasing Philip Clausius. Berlin and Heidelberg: Springer, pp. 245–67. [Google Scholar] [CrossRef]

- Edwards, Richard, and Nigel Stockwell. 2005. Trust and Equity. Harlow: Pearson Education, vol. 1, p. 10. [Google Scholar]

- Ferdinand, Peter. 2016. Westward ho—The china dream and ‘one belt, one road’: Chinese foreign policy under xi jinping. International Affairs 92: 941–57. [Google Scholar] [CrossRef]

- Haralambides, Hercules. 2017. One-belt-one-road (obor), china-eu trade relations, and (geo)political positioning statements. Paper presented at the Intermodal Asia 2017, Shanghai, China, March 21–23. [Google Scholar]

- Huang, Yongshen. 2007. Change of Property Right and Registration of Ship Ownership. Available online: http://www.simic.net.cn/news_show.php?id=5370 (accessed on 25 March 2015).

- Jia, Linqing. 2005. Personal opinions on the legal nature and structure of trust property rights. Jurist 1: 81–90. [Google Scholar]

- Johns, Max, and Christoph Sturm. 2015. The German KG System. Berlin and Heidelberg: Springer, pp. 71–85. [Google Scholar] [CrossRef]

- Li, Peifeng. 2009. The primary causes of difficult integration of anglo-american trust property ownership with the continental law property ownership system. Global Law Review 1: 9–18. [Google Scholar]

- Li, Yu. 2012. The legal status of the client in commerce trusts. Legal Forum 1: 121–27. [Google Scholar]

- Liu, Wei, Jingtao Bai, and Hongbin Chen. 2008. Investment and Financing of Water Transportation. Beijing: China Communications Press, vol. 1, pp. 8–13. [Google Scholar]

- Liu, Yingshuang. 2011. Discussion about the nature of trusts—Theory of alienation of trusts. Law Review 1: 75–82. [Google Scholar]

- Mayr, Daniel. 2015. Valuing Vessels. Berlin and Heidelberg: Springer, pp. 141–63. [Google Scholar] [CrossRef]

- Penner, James E. 2014. The law of trusts. Botterworths 1: 42. [Google Scholar]

- Schinas, Orestis. 2018. Chapter 8—Financing ships of innovative technology. In Finance and Risk Management for International Logistics and the Supply Chain. Edited by Stephen Gong and Kevin Cullinane. Amsterdam: Elsevier, pp. 167–92. [Google Scholar] [CrossRef]

- Schinas, Orestis, Harm Hauke Ross, and Tobias Daniel Rossol. 2018. Financing green ships through export credit schemes. Transportation Research Part D: Transport and Environment 65: 300–11. [Google Scholar] [CrossRef]

- Schinas, Orestis, and Arnd Graf von Westarp. 2017. Assessing the impact of the maritime silk road. Journal of Ocean Engineering and Science 2: 186–95. [Google Scholar] [CrossRef]

- Scott, Austin W., and William Franklin Fratcher. 2006. Scott on trusts. Aspen Law and Business 1: 135. [Google Scholar]

- Sheng, Xuejun. 2003. Defects of china’s trust legislation and its removal effect on functions of trusts. Modern Law Science 1: 139–43. [Google Scholar]

- Sheu, Jiuh Biing, and Tanmoy Kundu. 2017. Forecasting time-varying logistics distribution flows in the one belt-one road strategic context. Transportation Research Part E: Logistics and Transportation Review 117: 5–22. [Google Scholar] [CrossRef]

- Sun, Yigang, and Yu Zheng. 2009. On the Dissimilation of China’s Trust Institution: Some Comments on Legal Structure of China’s Present Trust Products. Journal of Northwest University of Politics Science and Law 4: 146–53. [Google Scholar]

- UNCTAD. 2019. Review of Maritime Transport 2018. Technical Report UNCTAD/RMT/2018. New York: UNCTAD. [Google Scholar]

- von Oldershausen, Christian. 2015. Other Equity Markets for Shipping. Berlin and Heidelberg: Springer, pp. 99–108. [Google Scholar] [CrossRef]

- Yan, Yang. 2004. The trust law of the people’s republic of china and china’s shipping law system. Technology and Economy Information of Shipbuilding Industry 1: 52–54. [Google Scholar]

- Yang, Liangyi. 2003. Ship Financing and Mortgage. Dalian: Dalian Maritime University Press, pp. 66–68. [Google Scholar]

- Zeng, Jinghan. 2017. Does europe matter? the role of europe in chinese narratives of ‘one belt one road’ and ‘new type of great power relations’. JCMS: Journal of Common Market Studies 55: 1162–76. [Google Scholar] [CrossRef]

- Zhai, Lihong, and Linfeng Yang. 2008. Development Innovation of Trust Products. Beijing: China Financial and Economic Publishing House, vol. 1, p. 27. [Google Scholar]

- Zhang, Tianmin. 2002. Trusts without the Support of the Law of Equity. Ph.D. thesis, China University of Political Science and Law China CNKI, Beijing, China; p. 94. [Google Scholar]

- Zhang, Tianmin. 2004. Trusts without the Support of the Law of Equity. Beijing: China CITIC Press, vol. 1, p. 132. [Google Scholar]

- Zhang, Xiang. 2014. China Is a Major Country of the Shipping Industry while not a Powerful Shipping Country. Available online: http://finance.ifeng.com/news/special/1stjjnh/20100117/1718843.shtml (accessed on 20 May 2019).

- Zhou, Xiaoming. 1996. Comparative Laws of the Trust System. Beijing: Law Press China, vol. 1, pp. 12–18. [Google Scholar]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jin, H.; Schinas, O. Ownership of Assets in Chinese Shipping Funds. Int. J. Financial Stud. 2019, 7, 69. https://doi.org/10.3390/ijfs7040069

Jin H, Schinas O. Ownership of Assets in Chinese Shipping Funds. International Journal of Financial Studies. 2019; 7(4):69. https://doi.org/10.3390/ijfs7040069

Chicago/Turabian StyleJin, Hai, and Orestis Schinas. 2019. "Ownership of Assets in Chinese Shipping Funds" International Journal of Financial Studies 7, no. 4: 69. https://doi.org/10.3390/ijfs7040069

APA StyleJin, H., & Schinas, O. (2019). Ownership of Assets in Chinese Shipping Funds. International Journal of Financial Studies, 7(4), 69. https://doi.org/10.3390/ijfs7040069