Does Corporate Governance Influence Leverage Structure in Bangladesh?

Abstract

1. Introduction

2. Literature Review

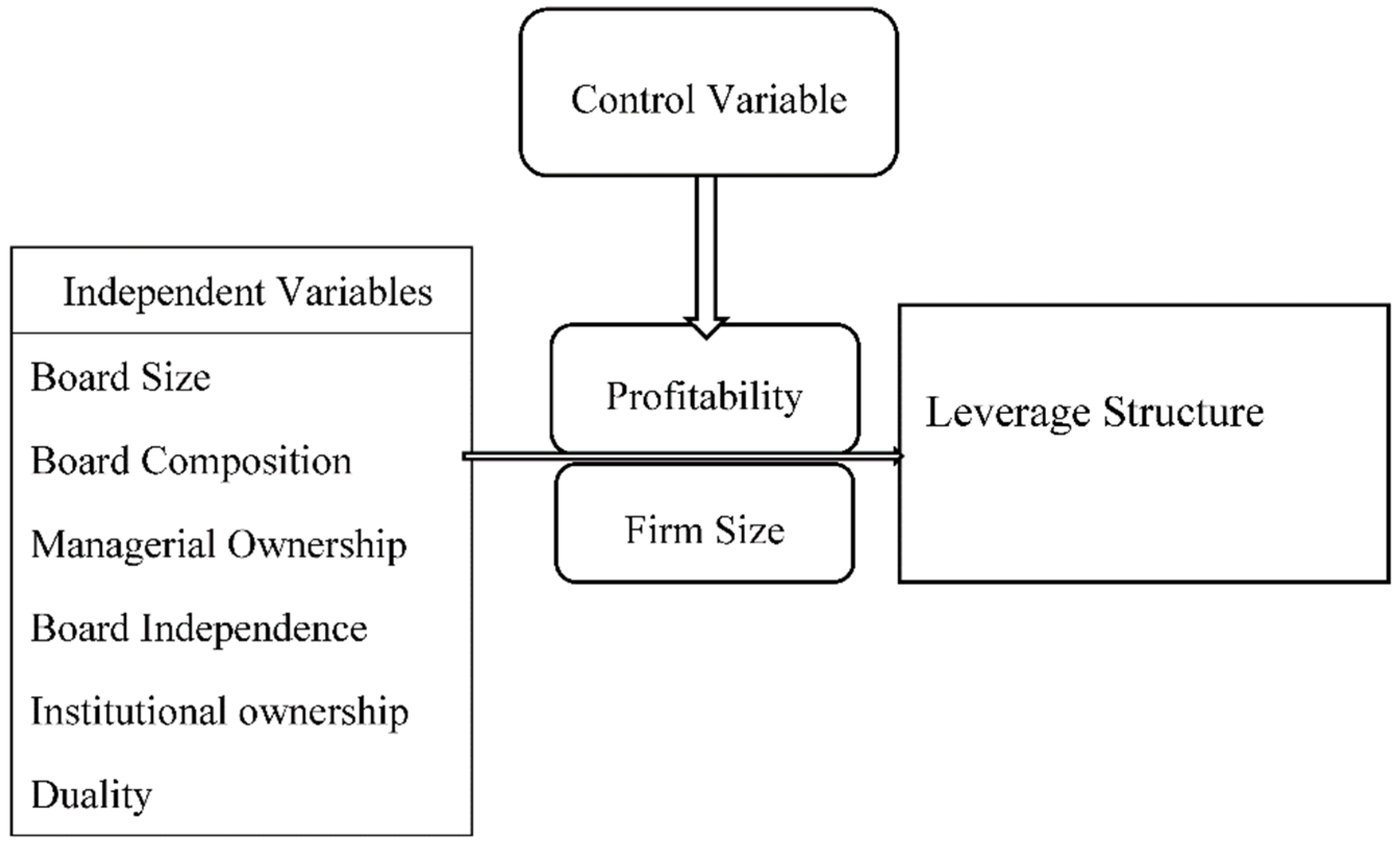

3. Variables Definitions and Hypotheses Development

3.1. Variable Definitions and Their Evidence

3.2. Formal Hypotheses Development

- . There is a positive relationship between board size and leverage structure decision-making.

- . A positive relationship exists between board composition and leverage structure decision-making.

- . Managerial ownership is positively related to leverage structure decision-making.

- . There exists a positive relationship between institutional ownership and leverage structure decision-making.

- . There is an inverse relationship between board independence and leverage structure decision-making.

- . A positive relationship exists between CEO duality and leverage structure decision-making.

3.3. Model Specification and Measurements

4. Data and Methodology

4.1. Sample Design and Data Collection

4.2. Methodology

5. Empirical Results and Discussion

5.1. Descriptive Statistics

5.2. Correlation Analysis

5.3. Test of Panel Generalized Method of Moments (GMM)

5.4. Panel Corrected Standard Error (PCSE)

6. Conclusions and Policy Implications

Author Contributions

Funding

Conflicts of Interest

References

- Abor, Joshua. 2007. Corporate Governance and Financing Decisions of Ghanaian Listed Firms Corporate Governance. The International Journal of Business in Society 7: 83–92. [Google Scholar]

- Abor, Joshua, and Nicholas Biekpe. 2007. Corporate Governance, Ownership Structure and Performance of SMEs in Ghana: Implications for financing opportunities. International Journal of Business in Society 7: 288–300. [Google Scholar] [CrossRef]

- Achchuthan, Sivapalan, Kajananthan Rajendran, and Sivathaasan Nadarajah. 2013. Corporate Governance Practices and Capital Structure: A Case in Sri Lanka. International Journal of Business and Management 21: 114–25. [Google Scholar] [CrossRef]

- Adegbile, Samuel Abraham. 2015. Corporate Governance Attributes and Capital Structure of Listed Firms in the Nigerian Food and Beverages Industry. International Journal of Public Administration and Management Research 3: 48–56. [Google Scholar]

- Aharon, David Yechiam, and Yossi Yagil. 2019. The Impact of Financial Leverage on the Variance of Stock Returns. International Journal of Financial Studies 7: 14. [Google Scholar] [CrossRef]

- Alagathurai, Ajanthan. 2013. Impact of Corporate Governance Practices on Firm Capital Structure and Profitability: A Study of selected hotels and restaurant companies in Sri Lanka. Research Journal of Finance and Accounting 10: 115–26. [Google Scholar]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of Error-component models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Barton, Sidney L., Ned C. Hill, and Srinivasan Sundaram. 1989. An Empirical Test of Stakeholder Theory Predictions of Capital. Financial Management Journal 18: 36–44. [Google Scholar] [CrossRef]

- Beck, Nathaniel, and Jonathan N. Katz. 1995. What to Do (and Not to Do) With Time-Series Cross-Section Data. American Political Science Review 89: 634–47. [Google Scholar] [CrossRef]

- Beck, T., and R. Levine. 2004. Stock markets, banks, and growth: Panel evidence. Journal of Banking and Finance 28: 423–42. [Google Scholar] [CrossRef]

- Berger, Philip G., Eli Ofek, and David L. Yermack. 1997. Managerial Entrenchment and Capital Structure Decisions. Journal of Finance 52: 411–38. [Google Scholar] [CrossRef]

- Bhagat, Sanjai, and Bernard Black. 2002. The Non-Correlation between Board Independence and Long-Term Firm performance. Journal of Corporate Law 27: 231–74. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel Data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Bokpin, Godfred A., and Anastacia C. Arko. 2009. Ownership Structure, Corporate Governance and Capital Structure Decisions of Firms: Empirical Evidence from Ghana. Studies in Economics and Finance 26: 246–56. [Google Scholar] [CrossRef]

- Castanias, Richard. 1983. Bankruptcy risk and optimal capital structure. Journal of Finance 38: 1617–35. [Google Scholar] [CrossRef]

- Chen, Sheng-Syan, and I-Ju Chen. 2012. Corporate governance and capital allocations of diversified firms. Journal of Banking & Finance 36: 395–409. [Google Scholar]

- Chowdhury, Mu. 2004. Capital Structure Determinants: Evidence from Japan & Bangladesh. Journal of Business Studies XXV: 23–45. [Google Scholar]

- Crutchley, Claire E., Marlin R. H. Jensen, John S. Jahera, Jr., and Jennie E. Raymond. 1999. Agency problem and the simultaneity of financial decision making: the role of institutional ownership. International Review of Financial Analysis 8: 177–97. [Google Scholar] [CrossRef]

- Dalton, Dan R., Catherine M. Daily, Alan E. Ellstrand, and Jonathan L. Johnson. 1998. Meta-Analytic Reviews of Board Composition, Leadership Structure, and Financial Performance. Strategic Management Journal 19: 269–90. [Google Scholar] [CrossRef]

- Diamond, Douglas W., and Raghuram G. Rajan. 2000. A theory of bank capital. Journal of Finance 55: 2431–65. [Google Scholar] [CrossRef]

- Duchin, Ran, John G. Matsusaka, and Oguzhan Ozbas. 2010. When are outside directors effective? Journal of Financial Economics 96: 195–214. [Google Scholar] [CrossRef]

- Ehikioya, Benjamin I. 2009. Corporate Governance Structure and Firm Performance in Developing Economies: Evidence from Nigeria. Corporate Governance 9: 231–43. [Google Scholar] [CrossRef]

- Eisenberg, Theodore, Stefan Sundgren, and Martin T. Wells. 1998. Larger Board Size and Decreasing Firm Value in Small Firms. Journal of Financial Economics 48: 35–55. [Google Scholar] [CrossRef]

- Erickson, Merle, and Shiing-wu Wang. 2005. Earnings Management by Acquiring Firms in Stock for Stock Mergers. Journal of Accounting and Economics 27: 149–76. [Google Scholar] [CrossRef]

- Fathi, Saeed, Farzaneh Ghandehari, and Sayyed Ya’ghoub Shirangi. 2014. Comparative Study of Capital Structure Determinants in Selected Stock Exchanges of Developing Countries and Tehran Stock Exchange. International Journal of Academic Research in Accounting, Finance and Management Sciences 4: 67–75. [Google Scholar] [CrossRef]

- Fosberg, Richard H. 2004. Agency Problems and Debt Financing: Leadership Structure Effects, Corporate Governance. International Journal of Business in Society 4: 31–38. [Google Scholar]

- Friend, Irwin, and Larry H. P. Lang. 1988. An Empirical Test of the Impact of Managerial Self-interest on Corporate Capital structure. Journal of Finance 43: 271–81. [Google Scholar] [CrossRef]

- Sanda, Ahmadu U., Aminu S. Mikailu, and Tukur Garba. 2009. Corporate Governance Mechanisms and Firm Performance: A Survey of literature. The University Journal of Corporate Governance 8: 7–21. [Google Scholar]

- Gill, Amarjit, Nahum Biger, and Neil Mathur. 2010. The Relationship between Working capital Management and Profitability: Evidence from The United States. Business and Economic Journal 10: 1–9. [Google Scholar]

- Gujarati, Damodar N. 2004. Basic Econometrics, 4th ed. Mcgraw Hill: Boston, p. 650. [Google Scholar]

- Gurarda, Sevin, Emre Ozsoz, and Abidin Ates. 2016. Corporate governance rating and ownership structure in the case of Turkey. International Journal of Financial Studies 4: 8. [Google Scholar] [CrossRef]

- Vakilifard, Hamid R., Mahdi S. Gerayli, Abolfazl M. Yanesari, and Ali Reza Ma’atoofi. 2011. Effect of Corporate Governance on Capital Structure: Case of the Iranian Listed Firms. European Journal of Economics Finance and Administrative Sciences 35: 1165–72. [Google Scholar]

- Haque, Faizul, Thankom Gopinath Arun, and Colin Kirkpatrick. 2011. Corporate Governance and Capital Structure in Developing Countries: A Case study of Bangladesh. Applied Economics 43: 673–81. [Google Scholar] [CrossRef]

- Hart, Oliver. 1995. Firms, Contracts, and Financial Structure. Oxford: Clarendon Press. [Google Scholar]

- Hausman, Jerry A. 1978. Specification Tests in Econometrics. The Journal of Econometrics 46: 1251–71. [Google Scholar] [CrossRef]

- Hsiao, Cheng. 2003. Analysis of Panel Data. New York: Cambridge University Press. [Google Scholar]

- Huynh, Phuong Dong, and Jyh-tay Su. 2010. The Relationship between Working capital Management and Profitability: A Vietnam Case. Internal Research Journal of Finance and Economics 49: 59–67. [Google Scholar]

- Jaradat, Monther S. 2015. Corporate Governance Practices and Capital Structure: A Study with Special Reference to Board Size, Board Gender, Outside Director and CEO Duality. International Journal of Economics, Commerce and Management United Kingdom 3: 264–73. [Google Scholar]

- Jensen, Michael C. 1986. Agency Cost of Free Cash Flow. Corporate Finance, and Take-Overs. American Economic Review 72: 323–29. [Google Scholar]

- Jensen, Michael C. 1993. The Modern Industrial Revolution, Exit, and the Failure of the Internal Control Systems. Journal of Finance 48: 831–80. [Google Scholar] [CrossRef]

- Joher, Huson, Mohd Ali, and M. Nazrul. 2006. The Impact of Ownership Structure on Corporate Debt Policy: Two Stage Least Square Simultaneous Model Approach for Post Crisis Period: Evidence from Kuala Lumpur Stock Exchange. International Business & Economics Research Journal 5: 51–63. [Google Scholar]

- Kallamu, Basiru Salisu. 2016. Impact of the Revised Malaysian Code on Corporate Governance on Audit Committee Attributes and Firm Performance. Global Journal of Management and Business Research: D Accounting and Auditing 16: 1–11. [Google Scholar]

- Kyereboah-Coleman, Anthony, and Nicholas Biekpe. 2006. The relationship between board size, board composition, CEO duality and firm performance: Experience from Ghana. Corporate Ownership and Control 4: 114–22. [Google Scholar]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny. 2002. Investor Protection and Corporate Valuation. The Journal of Finance 57: 1147–70. [Google Scholar] [CrossRef]

- Lefort, Fernando, and Francisco Urzúa. 2008. Board independence, firm performance and ownership concentration: Evidence from Chile. Journal of Business Research 61: 615–22. [Google Scholar] [CrossRef]

- Lev, Baruch. 1988. Toward a theory of equitable and efficient accounting policy. The Accounting Review 63: 1–21. [Google Scholar]

- Lipton, Martin, and Jay W. Lorsch. 1992. A Modest Proposal for Improved Corporate Governance. The Business Lawyer 48: 59–77. [Google Scholar]

- Marsh, Paul. 1982. The choice between equity and debt: An empirical study. The Journal of Finance 37: 121–44. [Google Scholar] [CrossRef]

- Mugenda, M. O., and A. Mugenda. 2008. Research Methods: Qualitative and Quantitative Approaches. Nairobi: African Centre for Technology Studies. [Google Scholar]

- Myers, Stewart C., and Nicholas S. Majluf. 1984. Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics 13: 187–221. [Google Scholar]

- Nyonna, Dong Y. 2012. Simultaneous Determination of Insider Ownership and Leverage: The Case of Small Businesses. Economics & Business Journal: Inquiries & Perspectives 4: 9–20. [Google Scholar]

- O’brien, Robert M. 2007. A Caution Regarding Rules of Thumb for Variance Inflation Factors. Quality and Quantity 41: 673–90. [Google Scholar] [CrossRef]

- Onaolapo, Adekunle A., and Sunday O. Kajola. 2010. Capital Structure and Firm Performance: Evidence from Nigeria. European Journal of Economics, Finance and Administrative Sciences 25: 70–82. [Google Scholar]

- Petersen, Mitchell A., and Raghuram G. Rajan. 1994. The benefits of Firm-creditor Relationships: Evidence from Small Business Research Data. Journal of Finance 49: 3–37. [Google Scholar] [CrossRef]

- Pontines, Victor, and Reza Siregar. 2008. Fundamental pitfalls of exchange market pressure-based approach to identification of currency crises. International Review of Economics & Finance 17: 345–65. [Google Scholar]

- Prasad, Sanjiva, Christopher J. Green, and Victor Murinde. 2001. Company Financing, Capital Structure, and Ownership: A Survey and Implications for Developing Economies. Ph.D. thesis, Cardiff Business School, Cardiff, UK; pp. 1–104. [Google Scholar]

- Rajan, Raghuram G., and Luigi Zingales. 1995. What do we know about Capital structure? Some Evidence from International Data. Journal of Finance 50: 1421–60. [Google Scholar] [CrossRef]

- Reed, W. Robert, and Haichun Ye. 2011. Which panel data estimator should I use? Applied Economics 43: 985–1000. [Google Scholar] [CrossRef]

- Siromi, Bulathsinhalage, and Pathirawasam Chandrapala. 2017. The Effect of Corporate Governance of Firm’s Capital Structure of Listed Companies in Sri Lanka. Journal of Competitiveness 9: 19–33. [Google Scholar]

- Somathilake, HMDN, and KGA Udaya Kumara. 2015. The Effect of Corporate Governance Attributes on Capital Structure: An Empirical Evidence from Listed Manufacturing Companies in Colombo Stock Exchange. Paper presented at the International Research Symposium, Rajarata University of Sri Lanka, Mihintale, Sri Lanka, January 26; pp. 22–29. [Google Scholar]

- Stulz, René M. 1988. Managerial Control of Voting Rights: Financing Policies and the Market for Corporate Control. Journal of Financial Economics 20: 25–54. [Google Scholar] [CrossRef]

- Taani, Khalaf. 2013. The Relationship between Capital Structure and Firm Performance: Evidence from Jordan. Global Advanced Research Journal of Management and Business Studies 2: 542–46. [Google Scholar]

- Titman, Sheridan, and Roberto Wessels. 1988. The determinants of capital structure choice. Journal of Finance 43: 1–19. [Google Scholar] [CrossRef]

- Uwuigbe, Uwalomwa. 2014. Corporate Governance and Capital Structure: Evidence from Listed Firms in Nigeria Stock Exchange. Journal of Accounting and Management 4: 5–14. [Google Scholar]

- Velnampy, T., and Aloy J. Niresh. 2012. The relationship between capital structure and profitability. Global Journal of Management and Business Research 12: 1–13. [Google Scholar]

- Wald, John K. 1999. How Firm Characteristics Affect Capital Structure: An International Comparison. Journal of Financial Research 22: 161–87. [Google Scholar] [CrossRef]

- Hewa Wellalage, Nirosha, and Stuart Locke. 2012. Corporate governance and capital structure decisions of Sri Lankan listed firms. Global review of Business and Economic Research 8: 157–69. [Google Scholar]

- Wen, Yu, Kami Rwegasira, and Jan Bilderbeek. 2002. Corporate Governance and Capital Structure Decisions of Chinese Listed Firms. Corporate Governance: An International Review 10: 75–83. [Google Scholar] [CrossRef]

- Xu, Xiaonian, and Yan Wang. 1999. Ownership Structure and Corporate Governance in Chinese Stock Companies. China Economic Review 10: 75–98. [Google Scholar] [CrossRef]

{kind=link}

| Dependent Variables | Variables | Description | Calculation Procedures | Expected Sign |

|---|---|---|---|---|

| LEV | Leverage | Computed as the Ratio of Total External Borrowings to Total Assets | - | |

| Independent Variables | BS | Board Size | Calculate the sum of directors on the board | Positive |

| BC | Board Composition | Board composition represents the proportion of total non-functional directors on board, and it is calculated as the number of total non-functional directors divided by total directors | Positive | |

| MNO | Managerial ownership | The ratio of shares held by CEOs, directors, and their immediate family members to total outstanding shares | Positive | |

| IO | Institutional owners | Institutional ownership measures as the percentage of shares held by the institution | Positive | |

| BI | Board Independence | The ratio of number of only total independent directors to the total number of directors on board | Negative | |

| FS | Firm Size (Control Variable) | Size of Firm (as the logarithm of total assets) | Negative | |

| ROA | Return on asset (Control Variable) | Return on Assets (company’s net earnings divided by its total assets) | Negative | |

| Duality | CEO/Chair | The same person holds dual responsibility as Chair and CEO (It is taken as 1 if the CEO is chairman; otherwise it is taken as 0) | Positive |

| Variable | Obs | Min. | Max. | Mean | Median | SD | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|---|

| Leverage | 945 | 0.0759 | 0.978 | 0.537 | 0.549 | 0.226 | −0.117 | 2.342 |

| BS | 945 | 3.000 | 15.00 | 7.39 | 7.00 | 2.092 | 0.364 | 2.861 |

| BC | 945 | 0.000 | 0.909 | 0.472 | 0.500 | 0.251 | −0.187 | 1.870 |

| IO | 945 | 0.000 | 0.982 | 0.243 | 0.179 | 0.219 | 1.419 | 4.180 |

| MNO | 945 | 0.000 | 0.866 | 0.331 | 0.374 | 0.224 | −0.078 | 2.141 |

| BI | 945 | 0.000 | 0.600 | 0.094 | 0.100 | 0.104 | 0.951 | 3.240 |

| FS | 945 | 9.634 | 24.284 | 20.066 | 20.41 | 2.159 | −1.451 | 6.202 |

| ROA | 945 | -0.410 | 0.479 | 0.0518 | 0.034 | 0.056 | −0.588 | 11.90 |

| Duality | 945 | 0.00 | 1.000 | 0.271 | 0.000 | 0.445 | 1.830 | 2.062 |

| LR | BS | BC | IO | MNO | BI | FS | ROA | Duality | |

|---|---|---|---|---|---|---|---|---|---|

| LR | 1.0 | ||||||||

| BS | −0.18 ** | 1.0000 | |||||||

| BC | 0.0403 | 0.231 ** | 1.000 | ||||||

| IO | 0.0108 | 0.0655 * | 0.0744 * | 1.000 | |||||

| MNO | 0.072 * | −0.0063 | 0.0138 | −0.28 ** | 1.000 | ||||

| BI | −0.0346 | −0.0047 | −0.53 ** | −0.16 ** | −0.0130 | 1.000 | |||

| FS | −0.0176 | −0.0139 | −0.0192 | −0.09 ** | 0.22 ** | 0.21 ** | 1.000 | ||

| ROA | −0.35 ** | 0.23 ** | −0.0202 | 0.0288 | −0.12 ** | 0.0018 | −0.11 ** | 1.000 | |

| Duality | 0.13 ** | −0.21 ** | 0.18 ** | 0.0469 | 0.0288 | −0.18 ** | −0.0461 | −0.18 ** | 1.000 |

| Variable | Panel Generalized Method of Moments | |||

|---|---|---|---|---|

| Co-efficient | Std. Error | t-Statistic | p-Value | |

| Constant | 0.807857 | 0.070552 | 11.45056 | 0.0000 |

| BS | −0.016472 *** | 0.003560 | −4.627448 | 0.000 |

| BC | 0.059977 * | 0.033680 | 1.780790 | 0.0753 |

| IO | 0.054142 * | 0.032631 | 1.659185 | 0.0974 |

| MNO | 0.079740 ** | 0.032532 | 2.451137 | 0.0144 |

| BI | 0.057765 | 0.081283 | 0.710663 | 0.4775 |

| FS | −0.008018 ** | 0.03327 | −2.410139 | 0.0161 |

| ROA | −1.161758 *** | 0.126061 | −9.215834 | 0.0000 |

| Duality | 0.012921 | 0.016217 | 0.796791 | 0.4258 |

| R-square. | 0.145730 | |||

| Adjusted R-squared. | 0.138429 | |||

| Prob(J-statistic) | 0.000000 | |||

| Durbin-Watson stat | 5.662 | |||

| Variable | Panel Corrected Standard Error (PCSE) | |||

|---|---|---|---|---|

| Co-Efficient | Std. Error | z-Statistic | p-Value | |

| Constant | 0.7005454 | 0.0834679 | 8.39 | 0.0000 |

| BS | 0.0012002 | 0.0050451 | 0.24 | 0.812 |

| BC | 0.0111372 | 0.0259417 | 0.43 | 0.668 |

| IO | 0.0071896 | 0.0246439 | 0.29 | 0.770 |

| MNO | 0.0746545 * | 0.041951 | 1.78 | 0.075 |

| BI | −0.0443308 | 0.0666469 | −0.67 | 0.506 |

| FS | −0.0086535 ** | 0.003804 | −2.27 | 0.023 |

| ROA | −0.6459502 *** | 0.1089191 | −5.93 | 0.000 |

| Duality | 0.0296891 ** | 0.0132562 | 2.24 | 0.025 |

| R-square. | 0.6426 | |||

| Wald statistic | 66.36 | |||

| Prob(F-statistic) | 0.000000 | |||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Uddin, M.N.; Khan, M.S.U.; Hosen, M. Does Corporate Governance Influence Leverage Structure in Bangladesh? Int. J. Financial Stud. 2019, 7, 50. https://doi.org/10.3390/ijfs7030050

Uddin MN, Khan MSU, Hosen M. Does Corporate Governance Influence Leverage Structure in Bangladesh? International Journal of Financial Studies. 2019; 7(3):50. https://doi.org/10.3390/ijfs7030050

Chicago/Turabian StyleUddin, Mohammad Nazim, Mohammed Shamim Uddin Khan, and Mosharrof Hosen. 2019. "Does Corporate Governance Influence Leverage Structure in Bangladesh?" International Journal of Financial Studies 7, no. 3: 50. https://doi.org/10.3390/ijfs7030050

APA StyleUddin, M. N., Khan, M. S. U., & Hosen, M. (2019). Does Corporate Governance Influence Leverage Structure in Bangladesh? International Journal of Financial Studies, 7(3), 50. https://doi.org/10.3390/ijfs7030050